Quick Answer

Use SPEI for domestic MXN contractor payouts in Mexico when recipients can provide a valid CLABE and your provider confirms your sending setup. Keep non-MXN or cross-border flows on another rail, and do not treat submission as final until downstream status updates and ledger posting agree. Clear ownership for compliance review, retries, and exception handling is what prevents avoidable delays.

How to pay Mexico contractors via SPEI with CLABE validation, ownership gates, and ledger traceability#

Treat SPEI as a fast domestic rail in Mexico, not as a shortcut around payout design. SPEI, or Sistema de Pagos Electronicos Interbancarios, is Mexico's interbank electronic payments system, created and operated by Banco de Mexico. A World Bank case study places its launch in 2004 and notes 24/7 functionality since 2015. That makes it a credible core path for platform payouts, but it does not solve finance, compliance, or support on its own.

Start with the rail. SPEI is not just a consumer payment brand or a wallet feature. It is central bank operated infrastructure, and published case material places it in the fast payments category, with real-time or near-real-time transfers and 24/7 functionality since 2015. The same material lists bulk or batch payments as a use case, which matters if you are designing scheduled contractor disbursements rather than one-off transfers.

From there, frame the decision as an operating question, not a marketing claim. For a platform team, the real work is turning that rail into a payout process that survives real volume and real exceptions. Product needs a recipient experience that does not confuse payout readiness with payout success. Engineering needs request tracking, idempotency, and status visibility. Finance needs reconciliation that ties each payout request to a provider reference and then to your ledger. Payments ops needs clear ownership when something lands in review, fails, or sits in an in-between state longer than expected. Bank transfers in Mexico were reported as growing 60% from 2020 to 2022, so the rail itself is familiar in the market. The harder part is making your implementation boring and auditable.

Before launch, separate confirmed system behavior from provider-specific unknowns. Do not assume your bank or payout provider exposes SPEI in a way that matches the rail's headline characteristics. Get written answers on who can originate payouts, how batch submissions work, what identifiers you receive back for traceability, how rejects and delayed statuses are surfaced, and who owns first-line exception handling. Ask for sample acknowledgements or API responses for at least an accepted payment, a rejected payment, and a delayed payment. A common failure mode is building around the idea of "instant" payouts, then discovering that status updates arrive asynchronously or that exception reporting is too thin for support and finance to use.

The rest of this guide stays focused on that operating layer. You will work through eligibility, onboarding, execution, monitoring, and failure recovery with a bias toward the questions that create compliance and ops debt when they stay vague.

Related: Invisible Payouts: How to Remove Payment Friction for Contractors Without Sacrificing Compliance.

For a step-by-step walkthrough, see How Platform Operators Pay Contractors in Indonesia With GoPay, OVO, DANA, or BI Fast.

Decide when SPEI is the right rail for contractor payouts#

SPEI is usually a strong first option when your payout lane is domestic MXN settlement to contractors who can provide local bank details, including an 18-digit CLABE for routing. If your core need is cross-border delivery or non-MXN settlement, evaluate another rail first, including SWIFT where relevant.

The useful decision here is not whether SPEI is fast. It is whether the rail matches your actual payout job. Build the decision matrix before provider demos so the team aligns on requirements, not brand familiarity.

| Decision factor | SPEI is usually the better fit when | Another rail is usually a better fit when | Verification point |

|---|---|---|---|

| Payout currency fit | You are paying in MXN domestically | You need non-MXN or cross-border settlement | Confirm your provider can originate domestic MXN payouts to local bank accounts |

| Recipient reach in Mexico | Most contractors can receive into local bank accounts and provide required details | A meaningful share cannot receive locally | Check what share of recipients can submit required bank details at onboarding |

| Operational speed | You want a real-time domestic MXN rail with 24/7 availability | You can accept batch timing and banking-hour cutoffs | Compare API success timestamps with when funds are visible in contractor accounts |

| Exception complexity | You want a clear exception path after recipient bank details validate | You can tolerate more delayed-status follow-up | Map ownership for data fixes, holds, and delayed statuses |

| Dependency on a Mexican bank account | Local bank account requirement is acceptable | You need a method that works without one | Decide whether bank-account readiness is a launch gate |

For a Mexico-specific breakdown, read How to Pay Contractors in Mexico: SPEI CoDi and SAT Compliance for Foreign Platforms.

For a parallel operating model, read How Platform Teams Pay Brazil Contractors with Pix.

Prepare the prerequisites before sending your first payout#

Get the prerequisites in place before money moves. If approvals, data checks, and submission rules are not clear before launch, you end up inventing them during live exceptions.

For in-country contractor payouts, local bank transfers are often an efficient default, so confirm early that SPEI fits your payout lane. Then lock down who can send, what data is required, and who can review or release a payout.

| Step | Focus | Key evidence |

|---|---|---|

| 1 | Bank account and sender ownership | Written confirmation on whether your setup needs a Mexican bank account, which entity is the sender, and who owns compliance approval internally |

| 2 | Single payout schema | Required identity and bank fields in one source record, including a valid 18-digit CLABE and any fields your provider and internal policy require |

| 3 | Policy gates before submission | Explicit outcomes of pass, fail, or manual review, with an owner and turnaround expectation for manual review |

| 4 | Launch evidence pack | Approved policy docs, test payout logs, one reconciliation sample, and escalation contacts |

Step 1#

Treat the Mexican bank account requirement as something to verify, not something to assume.

Get written confirmation on three points before production: whether your setup needs a Mexican bank account, which entity is the sender, and who owns compliance approval internally. Put one named compliance owner in the launch checklist so approvals do not stall under shared ownership.

Step 2#

Use one payout schema for every contractor and avoid off-system exceptions. Keep required identity and bank fields in a single source record, including a valid 18-digit CLABE and any fields your provider and internal policy require.

In practice, each test contractor record should be complete enough to pass review without follow-up in chat or email.

Step 3#

Because bank-transfer flows in Mexico are governed by formal rules and guidelines, put policy gates before submission with explicit outcomes: pass, fail, or manual review. If you use compliance controls, define an owner and turnaround expectation for manual review so payout requests do not sit in an unowned queue.

Require a recorded decision before release. That record is what finance, support, and audit teams rely on later when they need to confirm why a payout was held or sent.

Step 4#

Create a launch evidence pack before the first live transfer: approved policy docs, test payout logs, one reconciliation sample, and escalation contacts for both your provider and internal ops. Include an escalation path for held payouts, since account holds can disrupt contractor cash flow. Make the logs usable by including timestamps, approver, provider reference when available, and final status for each test payout.

For a step-by-step walkthrough, see The Best Way to Pay a Team of Contractors in Latin America.

We covered this in detail in How to Pay Contractors in Nigeria Using Local Rails for Compliance-Safe Operations.

Set up contractor onboarding and tax controls without slowing activation#

Keep activation fast, but separate it from payout access. Contractors should be able to create profiles quickly, while SPEI payouts stay disabled until the required data and control checks in your policy are complete and recorded, including the contractor CLABE.

That separation helps prevent avoidable support and finance noise. It keeps onboarding operational instead of ad hoc: collect only required fields, route unresolved items to review, and keep tax-control decisions inside approved workflows rather than chat threads.

| Step | Control area | Rule |

|---|---|---|

| 1 | Activation vs payout eligibility | Use statuses such as profile created, payout details submitted, review complete, and payout enabled; do not show payout-ready while any required field or required review is unresolved, and require CLABE before payout enablement |

| 2 | Tax-control ownership | Assign internal ownership for tax-related decisions and recordkeeping before you automate payout behavior; when using Banxico materials for interpretation, check high-impact points against the Spanish original and account for preliminary data |

| 3 | Routing labels | Use a small set of labels to distinguish standard cases from records that need extra review; route missing or unclear tax-profile data to review by default |

| 4 | Data minimization | Limit tax and bank data to what payout and compliance workflows require, mask sensitive values in logs and tickets, and store sensitive fields with encryption |

Step 1#

Separate profile activation from payout eligibility. Define clear statuses such as profile created, payout details submitted, review complete, and payout enabled. A contractor should never show as payout-ready while any required field or required review is unresolved, and CLABE should be on file before payout initiation.

Step 2#

Set tax-control ownership before scale. Assign internal ownership for tax-related decisions and recordkeeping before you automate payout behavior. If you rely on Banxico materials for policy interpretation, treat the Spanish original as the official reference, note that published data may be preliminary, and verify English-language interpretations before high-impact decisions.

Step 3#

Use simple segmentation to avoid blanket handling. Add a small set of routing labels so finance and ops can distinguish standard cases from records that need extra review. If tax-profile data is missing or unclear, route to review by default instead of automatic payout release.

Step 4#

Apply data minimization in the implementation. Keep CLABE and other sensitive payout and tax data limited to what payout and compliance workflows require, mask sensitive values in logs and tickets, and store sensitive fields with encryption. Review failed-payout tickets and operational logs regularly so sensitive values are not exposed beyond teams that need access.

For broader context, see Applying the US-Mexico Tax Treaty as a Remote Worker.

Related: Pay Contractors in India With UPI Without Losing Control.

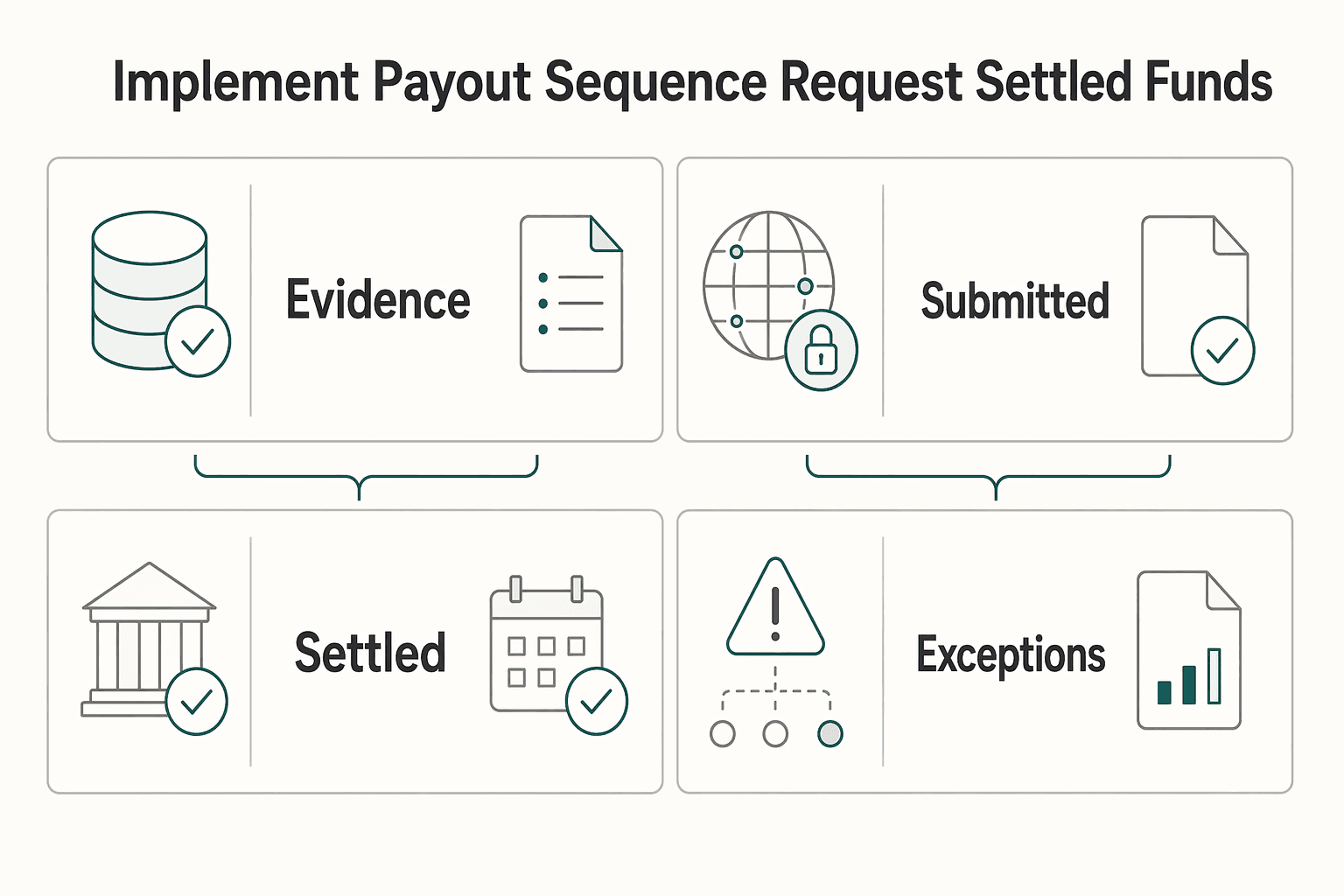

Implement the payout sequence from request to settled funds#

Treat execution as a controlled sequence, not a single API call. Record once, submit once, track every transition, and rerun only failed items.

Step 1 Create one canonical payout record before any external submission. At intake, store one payout instruction with the contractor, amount, recipient identifier such as an 18-digit CLABE, destination account snapshot, funding source, and eligibility decision. Assign the idempotency key here and keep it stable for retries of that same business instruction.

If you cannot trace retries and state changes back to one payout record, duplicates and reconciliation ambiguity get much more likely.

Step 2 Run a final gate, then submit once. Before submission, recheck eligibility, confirm the payout is not already terminal, and verify required payout details still match the approved record. If a check fails, route to exception instead of patching it in flight.

SPEI is an electronic funds transfer system operated by Banco de México. Your status model is the control layer on top of it, so keep one internal taxonomy across product, finance exports, and support.

| Internal checkpoint | Internal meaning | Minimum evidence | Primary owner |

|---|---|---|---|

| recorded | Request recorded and passed internal validation | payout ID, idempotency key, timestamp, actor/service | engineering |

| submitted | Submitted and awaiting processing outcome | provider reference, submission timestamp, latest event/response ID | engineering, then payments ops |

| settled | Final success recorded in internal ledger | settled timestamp, ledger entry ID, provider reference | finance or payments ops |

| exception | Requires review before release/retry | reason, last known status, assigned owner, next action timestamp | payments ops |

Step 3 Make retries idempotent by design. A replay in your system should resolve to the existing payout by idempotency key and return current state, not create a new outbound transfer unless you intentionally moved it to a retryable exception state.

SPEI supports near real-time transfers and continuous availability for participants, but that does not mean every initiated payout settles instantly. For transfer orders settled through SPEI clearing, treat that legal-finality checkpoint as when you can mark funds as finally settled internally.

Step 4 Handle scale with item-level batch control. Bulk or batch payments are a listed SPEI use case, so model batches as containers of individual payouts, each with its own status and traceability. A batch can be mostly successful while a subset moves to exception.

Rerun by item, not by whole batch. Keep successful items locked from reprocessing, and require rerun evidence: original batch ID, failed item IDs, operator reason, and new submission timestamps.

Build ownership handoff into the flow. Engineering owns integrity through submission and state capture. Payments ops owns exception resolution and release decisions after provider interaction.

Related reading: How to Pay Contractors in Czech Republic with CZK Routing and CNB Controls.

If you want a reference implementation for idempotent retries, payout status tracking, and audit-ready records, review Gruv Payouts.

Operate day to day with monitoring, reconciliation, and controls#

Day-to-day reliability comes from control discipline, not from the rail alone. SPEI supports real-time MXN transfers, but contractor payout operations can still face delays and reconciliation complexity.

| Step | Control | Minimum record |

|---|---|---|

| 1 | KPI monitoring | Timestamps for payout requested, sent to provider, provider update, and ledger posted, plus views such as time to funds, cost per transaction, and delay-driven support tickets |

| 2 | Reconciliation before close | Payout ID, recipient CLABE, idempotency key, provider reference, journal entry ID, posted timestamp, and latest exception note on the same record |

| 3 | Ledger-first discrepancy review | Pull the payout record, provider reference, and status timeline before changing anything manually |

| 4 | Risk and velocity overrides | Log approver, reason, timestamp, and supporting notes on the payout record itself |

Step 1 Track a short KPI set your team can act on quickly. Monitor time to funds, total cost per transaction, and support tickets caused by delays. Slice those views by provider and contractor cohort in Mexico so you can spot where delays are accumulating.

Use timestamps as the minimum proof on every payout record: payout requested, sent to provider, provider update, and ledger posted. If an early provider acknowledgement is treated as success, stalled downstream updates can hide in plain sight.

Step 2 Reconcile from the ledger outward before finance close. Match the payout request, recipient CLABE, provider reference, and posted journal event on the same record before confirming close. If one is missing, treat the item as unresolved even when a wallet or provider view looks paid.

Keep the reconciliation evidence together: payout ID, recipient CLABE, idempotency key, provider reference, journal entry ID, posted timestamp, and latest exception note. This is an operating control choice, not a SPEI mandate, but it keeps partial status noise out of close decisions.

Step 3 Treat wallet and balance views as projections, then resolve against ledger entries. When updates arrive late, retries occur, or manual adjustments happen, projections can drift. When balances disagree, use ledger entries as the reference point and trace the event chain before changing anything manually.

For account-level discrepancies, pull the payout record, provider reference, and status timeline first. That preserves one auditable story for support and finance.

Step 4 Run periodic risk and velocity reviews with explicit overrides. Review payout patterns on a fixed cadence, and log override decisions with approver, reason, timestamp, and supporting notes. Keep those logs on the payout record itself, not in chat or email.

When contractor payout operations cross teams, aligned audit trails matter even more.

Recover from failures without breaking contractor trust#

Contractor trust usually breaks in the exception path, not on the happy path. The practical fix is to classify failures early, assign one owner per case, and give contractors a clear next step that matches the actual workflow.

Step 1 Classify the exception before you retry or contact the contractor. Treat failed and pending payouts as different states, and store the failure tag with the latest provider reference and status timestamp.

| Failure bucket | Owner | Verify first |

|---|---|---|

| Payout data mismatch | Payments ops plus contractor | Submitted payout or identity fields vs contractor profile and latest correction request |

| Compliance hold | Compliance | Review trigger, case owner, and required evidence |

| Provider rejection | Payments ops | Provider message, reference, and whether correction or resubmission is possible |

| Delayed status | Payments ops or engineering | Current provider status and last external update timestamp |

| Unmatched return | Finance plus payments ops | Ledger posting, provider reference, and link to original payout |

If you misclassify the bucket, support asks for the wrong action and trust erodes quickly.

Step 2 Route by root cause, not queue age. Data-quality issues, such as payout-detail or identity mismatch, should go to a contractor correction flow with only the fields needed to fix the record. Policy-gate issues should go to compliance review with an internal SLA and an evidence pack: payout ID, contractor profile ID, trigger or reason code, owner, due time, and collected documents.

Step 3 Handle returns and possible reversals as a separate branch. Re-attempt a SPEI payout once your internal records show the original payout is closed as failed or returned and the underlying issue is resolved. For batch operations, retry only the affected record. If repeated failures show the current route is not workable for that account, pause further payouts on that account until corrected and reviewed, then decide whether another payout rail is required.

Because SPEI is described as having 24/7 functionality since 2015, and fast payment outcomes can be real time or near real time, delay alone does not confirm a failure, so check the timestamp trail first.

Step 4 Give support teams contractor-safe language. Use plain status updates without exposing sensitive compliance details or internal risk logic.

- "Your payout is awaiting confirmation. No action is needed right now, and we will update you by [time]."

- "We need you to review and correct your payout details before we can resend funds. Please use the secure form in your account."

- "Your payout is under review. We will contact you if we need anything else."

Tell contractors what happens next, who will contact them, and whether they need to do anything now.

Need the full breakdown? Read Crypto Payouts for Contractors: USDC vs. USDT - What Platforms Must Know.

Should you run SPEI alone or combine it with other payout rails#

Run SPEI as the primary rail when the job is domestic MXN payout to contractors with a Mexican bank account. Add another rail only when you can show a real coverage, currency, or reliability gap.

Step 1 Keep SPEI primary when your payouts are domestic MXN and contractors can receive funds in a Mexican bank account. SPEI is a domestic fiat rail, and CLABE quality is central to successful routing. Check accepted-to-posted outcomes, CLABE correction rates, and whether exceptions are data-fix issues or true rail-coverage issues.

| Rail choice | Best fit | Verify before launch | Main burden |

|---|---|---|---|

| SPEI | Domestic MXN payouts to contractors with valid CLABE and a Mexican bank account | Acceptance rate, status visibility, transaction-reference-to-ledger match | Lowest added complexity when coverage fits |

| Cross-border rail | Non-MXN payouts or contractors who cannot receive through a Mexican bank account | Beneficiary data requirements, currency support, status mapping, reconciliation fields | More corridor variation and more support follow-up |

| Hybrid stablecoin + local-rail bridge | Cases where stablecoins are part of the funding flow but final delivery still needs MXN bank payout | Conversion policy, reconciliation references (hash/ID), limits, and risk alerts | Added operational controls and monitoring |

Step 2 Add a second rail only for a measurable reason. Valid triggers include a contractor cohort that cannot be served through Mexican bank delivery, a non-MXN requirement, or repeated failures that persist after onboarding-data fixes. In some stacks, routing without local instant rails can add slower settlement, intermediary fees, or unpredictable holds, so confirm those risks with your own payout data before expanding rails. If the root issue is weak CLABE collection, fix that first before adding a new rail.

You might also find this useful: How Platform Operators Pay Contractors in Colombia with PSE Nequi and DIAN Controls.

Final checklist before you launch at scale#

If you plan to use SPEI for Mexico contractor payouts, do not scale until every gate below is a pass with a named owner and proof artifact.

| Gate | Owner | Pass when | Verification |

|---|---|---|---|

| Rail decision approved | Payments Ops | The rail matrix and exclusions are written and approved | Written rail matrix; provider confirmation of supported payout types; decision record with excluded cases |

| Fallback routing approved | Finance | Fallback logic is documented by payment type, not decided ad hoc in live ops | Fallback decision table; approver list; one reconciliation trace showing rerouted payout-to-ledger mapping |

| Compliance ownership locked | Risk/Compliance | Review ownership, escalation responsibility, and data-handling path are documented | Ownership matrix; onboarding checklist; escalation contacts; documented tax identity handling path |

| Exception handling tested | Payments Ops | A delay case and a rejection or mismatch case are tested and routed through the real escalation flow | Status mapping; incident notes; escalation steps; decision record for retry, hold, or switch outcomes |

| Dry run evidence signed off | Finance + Engineering | Request, provider reference, timestamps, status progression, and ledger outcome are linked in one chain | Dry-run packet; audit trail; payout-to-ledger trace; exception playbook |

- Rail decision approved by Payments Ops

Action (owner: Payments Ops): approve SPEI only for the payout types you intentionally scoped for Mexico, and document excluded cases. The Visa LATAM report separates domestic and cross-border disbursements, so rail choice should be explicit. Pass/Fail rule: Pass only when the rail matrix and exclusions are written and approved. Verification: written rail matrix, provider confirmation of supported payout types, and decision record with excluded cases.

- Fallback routing approved by Finance

Action (owner: Finance): define when a payout stays on the primary rail, when it moves to an alternate method, and who can approve the switch. Pass/Fail rule: Pass only when fallback logic is documented by payment type, not decided ad hoc in live ops. Verification: fallback decision table, approver list, and one reconciliation trace showing rerouted payout-to-ledger mapping.

- Compliance ownership locked by Risk or Compliance

Action (owner: Risk/Compliance): assign named owners for KYC, KYB, AML review, tax identity handling where applicable, and escalation when a payout cannot be released. Pass/Fail rule: Pass only when review ownership, escalation responsibility, and data-handling path are documented. Verification: ownership matrix, onboarding checklist, escalation contacts, and documented tax identity handling path. For related onboarding context, see Hiring Contractors in Mexico: RFC ISR Withholding and SPEI Payouts.

- Exception handling tested by Payments Ops

Action (owner: Payments Ops): run a delay case and a rejection or mismatch case before go-live. Visa's research tracks cash-flow issues tied to disbursement delays, so happy-path testing is not enough. Pass/Fail rule: Pass only when both exception types are tested and routed through your real escalation flow. Verification: status mapping, incident notes, escalation steps, and decision record for retry, hold, or switch outcomes.

- Dry run evidence signed off by Finance and Engineering

Action (owners: Finance + Engineering): run one production-like batch with one successful payout and one controlled exception, then confirm evidence can be retrieved quickly end to end. Pass/Fail rule: Pass only when request, provider reference, timestamps, status progression, and ledger outcome are linked in one chain. Verification: dry-run packet, audit trail, payout-to-ledger trace, and exception playbook.

For next steps after this gate review, try the free invoice generator, or talk to Gruv for a pre-scale setup check.

This pairs well with our guide on Cash Pickup Payouts for Unbanked Contractors in Cash-Preferred Markets.

Before you finalize your launch checklist, confirm Mexico coverage and compliance gating for your specific program: Talk to Gruv.

Frequently Asked Questions

Can a foreign platform pay contractors in Mexico via SPEI without opening a Mexican bank account?

Do not assume a universal yes. The grounded sources support that setup depends on provider rules and Mexico's regulatory context, so confirm your exact eligibility before launch. Verify with your provider whether your entity and account setup can send SPEI payouts and whether a local account requirement applies in your case. For broader foreign-platform compliance context, see How to Pay Contractors in Mexico: SPEI CoDi and SAT Compliance for Foreign Platforms.

Is SPEI available for contractor payouts outside business hours?

Treat 24/7 availability as provider-dependent until you have written confirmation. One source claims verified accounts can send instant peso transfers on weekends and holidays, but that should not be generalized across every bank, provider, or account type. Verify weekend and holiday processing and any provider-specific availability limits.

What payout data do you need to send a contractor payment successfully?

A valid CLABE is the clearly supported must-have. Do not assume a universal field list beyond CLABE, because required beneficiary data can vary by provider flow. Verify the exact required fields and whether CLABE validation happens before release. For tax and onboarding detail, see Hiring Contractors in Mexico: RFC ISR Withholding and SPEI Payouts.

What should finance and ops monitor right after a payout is initiated?

Use the references and status fields your provider exposes, and reconcile them to your ledger before treating a payout as complete. Because status models are provider-specific, verify which state is final and how exceptions are handled in your provider flow.

How should you retry a failed payout without creating duplicates?

Retry behavior is provider-specific, so do not apply a generic rule. Confirm with your provider how to handle failed or uncertain transfers, including duplicate-prevention behavior and whether an instruction can still settle after an error state.

When should you switch a contractor payout from SPEI to another rail?

Switch rails when SPEI is not a fit for the specific payout setup your provider supports. Local rails are often used to reduce international-wire delays and fee drag, so compare fallback options on eligibility, required beneficiary fields, and fee or FX impact. Also confirm whether verification level affects access to alternatives such as SWIFT.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 1 external source outside the trusted-domain allowlist.

- documents1.worldbank.org/curated/en/784831625137368238/pdf/Building-F...trusted

- downloads.regulations.gov/USTR-2025-0016-0053/attachment_1.pdftrusted

- fastpayments.worldbank.org/sites/default/files/2021-09/World_Bank_FPS_M...trusted

- fastpayments.worldbank.org/sites/default/files/2021-11/Fast%20Payment%2...trusted

- imf.org/-/media/files/publications/cr/2023/english/1...trusted

- stripe.com/ae/resources/more/mexico-bank-transfers-an-i...trusted

- stripe.com/resources/more/mexico-bank-transfers-an-in-d...trusted

- banxico.org.mx/payment-systems/d/%7B611C4F2A-0CE2-03E3-081D...external

Educational content only. Not legal, tax, or financial advice.

Related Posts

Hiring Contractors in Mexico With RFC, ISR, and SPEI Controls

For operators, when you are hiring contractors in Mexico, the problem is mainly sequence, not sourcing. Classification comes first, then RFC and invoice readiness, then ISR ownership, then payout execution. When you let that order slip, a file can look clean on paper and still fail under review.

Pay Contractors in Mexico: SPEI, CoDi, SAT, and CFDI Decisions for Platforms

Mexico contractor payouts usually break for a simple reason: teams launch from a generic Latin America plan, then discover that payout rail choices, tax steps, and operating structure cannot be separated in practice. If you are evaluating multiple rails and operating models at the same time, you need Mexico-specific decisions before you send the first live payout.

Invisible Payouts: How to Remove Payment Friction for Contractors Without Sacrificing Compliance

Invisible payouts should make life easier for contractors without hiding the controls your team needs. Contractors should get a predictable, low-friction flow, while internal teams can still enforce and document payout decisions when needed. If you run contractor payouts at scale, you need both outcomes at once. We recommend treating every easy payout as a controlled release path your team can replay later.