Quick Answer

Start with ownership and evidence, then decide whether to launch. For pay contractors colombia pse nequi dian compliance platform decisions, the article’s standard is clear: no production rollout until contractor classification, DIAN-linked document handling, and reconciliation controls are written, assigned, and testable. PSE and Nequi are treated as non-production rails until provider artifacts prove your exact payout direction, status behavior, and exception handling.

Why Colombia contractor payouts need a stricter go or no-go decision#

Treat Colombia contractor payouts as a launch decision with a real stop condition, not something you clean up after the first transfers go out. This guide is for platform operators deciding whether to launch Colombia now, with current team and vendor capacity, not for generic advice on hiring freelancers.

Use market context, but do not confuse it with rollout readiness#

Colombia is covered in digital economy research, but country-level research is not the same as an operator spec. The World Bank's Country Diagnostic: Colombia, published in June, 2023 as Report No: AUS0003147, includes a dedicated Digital Financial Services section, marked at 86 in the table of contents. That is useful context for why the market merits attention.

It is not enough to approve a launch. The same report states that the World Bank does not guarantee the accuracy of the data included, and that the findings do not necessarily reflect the views of its Executive Directors. In practice, that is a reminder to use public material as directional input, then verify payout and compliance mechanics yourself before committing product, legal, and ops resources.

Verify the gaps that public market content leaves open#

The scope of this article is narrow and practical. It does not invent certainty where the evidence is thin. In the source set reviewed for this guide, specific DIAN contractor payout obligations are not provided, and PSE and Nequi implementation details are not evidenced. That gap matters because operator teams often mistake a rail mention for production readiness.

Your first verification checkpoint should be simple. Before you say Colombia is live, you should have written answers to three questions. Who owns the tax and document interpretation if DIAN-related requirements apply to your model? Which provider can prove your intended payout direction works, with settlement and reconciliation evidence? What record will you rely on when a payout is marked successful by a provider but cannot be matched cleanly in your finance books?

If those answers are still verbal, scattered across vendors, or deferred with "we'll handle it later," that is a no-go. The common failure mode is not that money cannot move; it is that money moves before responsibilities, document rules, and traceability are pinned down.

Judge this rollout by three outcomes#

A Colombia launch is only worth shipping if you can show all three outcomes up front:

| Outcome | What to show |

|---|---|

| Contractor setup discipline | Onboarding data and documents defined before activation based on your legal/compliance interpretation |

| Traceable payout operations | Auditable records from approval through settlement and reconciliation |

| Clear ownership | Tax handling, document issuance, and exception resolution across your team and any vendors |

Those are the standards the rest of this guide uses. If you can meet them, Colombia is a serious rollout candidate. If you cannot, pause and close the evidence gaps before you add PSE, Nequi, or any other local rail to production. Related reading: How Platform Operators Pay Creators Globally Across YouTube, Twitch, and Substack.

What to prepare before you start implementation#

If these prep items are still informal, pause implementation. The risk is building payout flows before legal, tax, and finance ownership is clear.

Gather the minimum evidence pack first#

Start by locking down the records you will rely on when a contractor is activated, paid, or disputed. Keep your contractor-classification policy, your current service-agreement template, and a named owner for DIAN documentation in one controlled place with current versions. DIAN is the National Tax and Customs Directorate, so this ownership should be explicit, not a placeholder.

Do not treat employee-payroll guidance as contractor proof. One available operational source is explicitly about paying employees in Colombia, so use it as directional context only.

Write down compliance boundaries before vendor talks#

Define scope ownership in writing before anyone commits to PSE, Nequi, or API timelines. For retención en la fuente, electronic invoicing, and Certificado de Retención en la Fuente, document who interprets the requirement, who executes it, and what evidence is retained.

When a provider says they "support compliance," require the specific artifact they deliver, your internal approver, and the fallback path for missing payout data. If those answers are still verbal, scope is not ready.

Define ops artifacts before coding starts#

Set your payout status taxonomy, exception queue, and reconciliation export structure before engineering starts. Keep COP mandatory in the design, because one cited operational source states domestic payments must be made in Colombian pesos. If you also report internally in USD, treat that as an internal reconciliation field, not as proof that a rail or provider output will be audit-ready.

Your validation test is simple: finance can match approval, payout result, provider reference, and ledger entry from a single export. If matching depends on screenshots or ad hoc CSV edits, you are too early to ship. Related reading: Pay Contractors in Mexico With SPEI for Platform Operators.

Step 1 set the legal and classification baseline before paying anyone#

Set this gate before any payout build work: document why each worker is on a contractor path in your operating model, and who approved that decision.

The only Colombia-specific operational source in this set is about paying employees, not classifying contractors. Use it as a boundary signal, not a contractor rulebook: it ties employee payroll to DIAN-validated electronic payroll and invoicing, PILA flows, and a 37.5% employer statutory-benefit contribution model.

Write the classification check before activation#

Use one documented pre-activation check that your legal team accepts and apply it consistently. If your team uses a four-factor screen internally, keep it explicit in policy and treat it as a risk screen, not a legal shortcut.

Before activation, your file should show:

- CPS draft or signed agreement

- Classification review notes (including the risk markers your team tracks, such as subordinacion and dependencia economica)

- Named approver and decision date

If the decision is only verbal or buried in chat, stop and formalize it.

Stop when role design looks employment-like#

Make escalation binary. If role design shows ongoing control or practical dependency, pause contractor onboarding and route the case to legal review before payout setup continues.

Rail choice will not fix a misclassification pattern later, so keep this as a go/no-go gate.

Lock product language around AFP, EPS, and ARL#

Define ownership for AFP, EPS, and ARL questions, then review onboarding copy, help text, payout FAQs, and support macros so they do not imply employer obligations your model is not taking on.

Keep the standard simple: platform language must match your approved classification position before launch.

Related: How to Pay Contractors in Mexico: SPEI CoDi and SAT Compliance for Foreign Platforms.

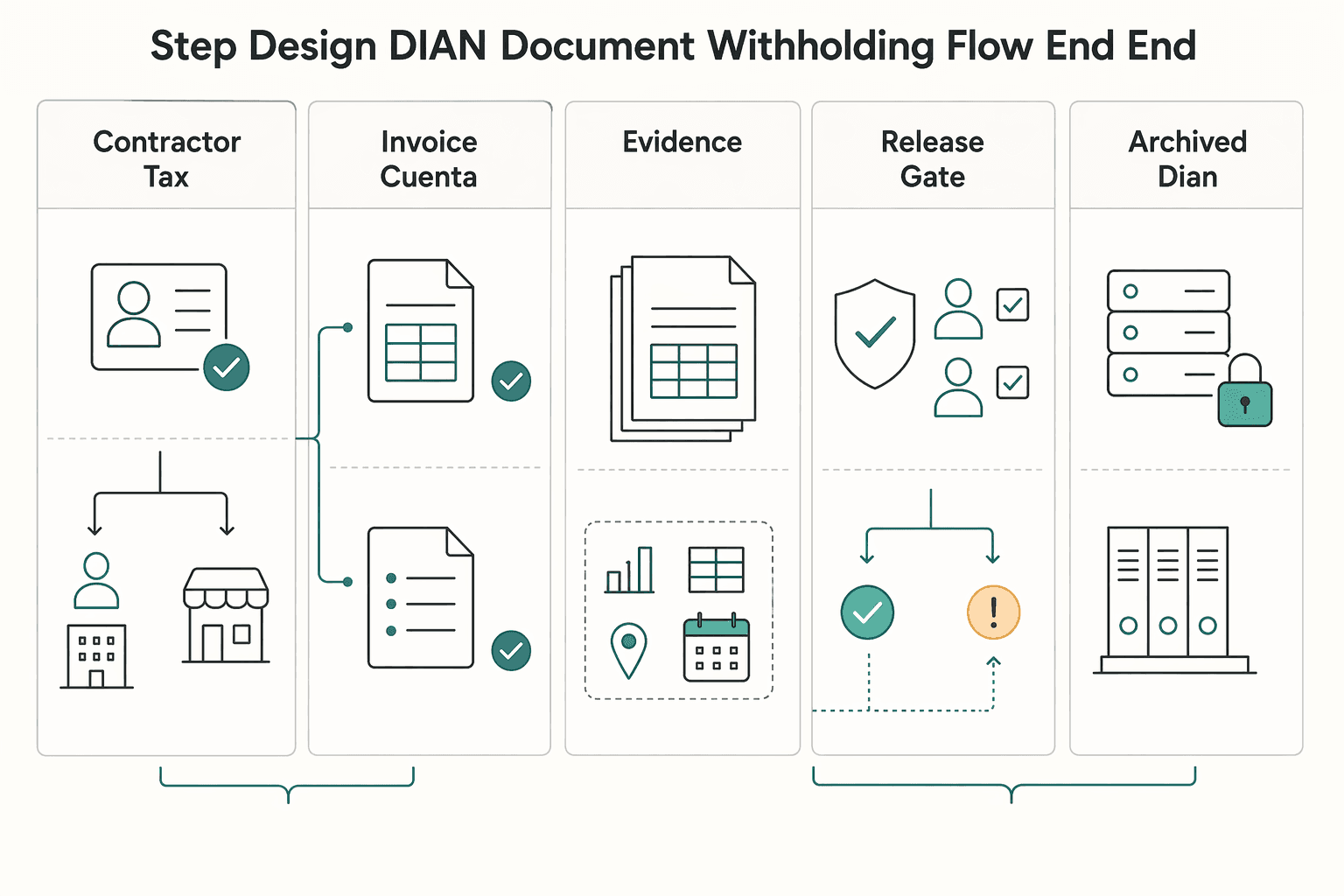

Step 2 design the DIAN document and withholding flow end to end#

After classification, treat this as an evidence-design step: define one auditable path from contractor billing input to payout approval and archived records for DIAN (National Tax and Customs Directorate).

Write the flow before you automate it. If your operation uses an invoice in some cases and a cuenta de cobro in others, document that intake rule clearly. If you apply retención en la fuente, record who reviews it, who approves payout, and where the final record is stored so the same case can be reconstructed later.

Keep ownership explicit for each item you include in scope, such as electronic invoicing, VAT review, and Certificado de Retención en la Fuente handling. Do not assume "the vendor handles it" is enough; define who is accountable for issuance, review, retention, and retrieval in your operating model.

Use one reference ID across intake, review, approval, payout, and archive. Without that, you may settle funds successfully but still fail an internal or external documentation check.

| Required artifact | System of record | Responsible owner | Failure impact |

|---|---|---|---|

| Contractor tax profile | Contractor compliance file | Onboarding or tax ops | Review decisions cannot be traced to a complete profile |

Invoice or cuenta de cobro | Billing repository linked to contractor ID | AP or contractor ops | Payment basis is unclear during reconciliation |

| Withholding review record (if applicable) | Finance workpaper or ledger attachment | Finance or tax team | Paid amount cannot be reproduced cleanly |

| Payout approval log | Payments or treasury approval system | Payments ops or treasury | Approval trail is incomplete |

| Archived DIAN-supporting case file | Central compliance archive | Finance with legal oversight | Document response becomes slow and error-prone |

Need the full breakdown? Read How to Write a Payments and Compliance Policy for Your Gig Platform.

Step 3 decide how PSE and Nequi fit your payout architecture#

Treat PSE and Nequi as production rails only after direct provider validation. Public SERP material is too thin for implementation decisions, so your go/no-go call should come from provider evidence tied to your operating flow.

You can see that evidence gap in the source set behind this guide. The World Bank diagnostic includes a digital financial services section, but the retrieved MDPI page was machine-readable access content and the retrieved Issuu result was mostly advertisement shell content. Use that as a filter: market visibility is not operational proof.

Qualify each rail with provider evidence#

Use a written checklist for PSE and Nequi that maps to contractor payouts and your DIAN document flow. Ask providers to confirm your exact payout direction and beneficiary model in writing, then validate that against your approval and archive controls.

At minimum, require artifacts for:

- payout-direction support for your outbound contractor use case

- settlement behavior, including final vs pending/reversible statuses

- failure states and machine-readable failure codes

- reversal/return handling and how it appears in reporting

- reconciliation outputs with provider reference IDs joinable to contractor ID, invoice or

cuenta de cobro, andretención en la fuenterecords

Prefer real sample exports or API payloads over slides. If the provider cannot show reconciliation files, example status sets, and exception-support paths, the rail is still in discovery.

Apply a strict production rule#

Use a hard decision rule: if a provider cannot show auditable DIAN-linked reporting and operational support for your target rail, treat that rail as non-production.

| Rail option | Availability | Ops burden | Compliance evidence required |

|---|---|---|---|

| PSE | Provider-verified for your exact payout direction and beneficiary model only | Unknown until statuses, reversals, and reconciliation outputs are tested | Written confirmation, sample status set, sample reconciliation export, support escalation path, and joinable reference IDs for your DIAN archive |

| Nequi | Provider-verified for your exact wallet payout use case and beneficiary-matching rules only | Unknown until rejects, returns, and beneficiary mismatches are tested | Same evidence pack, plus proof beneficiary data maps to the contractor file without guesswork |

| Fallback rail | Rail your finance team already reconciles and can evidence today | Usually lower operational surprise because exception paths are already known internally | Same DIAN-linked audit trail: payout reference, contractor ID, billing document, and withholding record |

Keep your fallback rail live until PSE or Nequi pass this evidence test.

If you want a deeper dive, read How to Pay Contractors in Peru: Yape Plin and SBS Compliance for Platform Operators.

Step 4 lock the settlement and FX model before scale#

Once you know which rail might work, lock the money model before volume hides mistakes. Track each contractor obligation in either COP or USD, and require one auditable TRM reference path whenever a conversion is involved.

Define the obligation and reporting currency first#

Set one source currency per contractor obligation and keep it consistent across payout, approval, and ledger records. If you contract in USD, keep USD as the obligation currency and define how the local COP reporting value is captured for DIAN support records. If you contract in COP, keep COP as the source amount and treat any USD view as secondary unless finance approves otherwise.

| Record element | Include |

|---|---|

| Obligation | Obligation currency and amount |

| Payout | Payout currency and amount |

| Conversion reference | TRM reference used for conversion, plus capture date or timestamp |

| Provider reference | Provider payout reference |

| Ledger link | Internal ledger entry ID |

| Supporting link | Linked contractor billing and tax-support record |

Use that record shape for every payout event. Before release, finance should be able to trace one contractor case from obligation amount to payout to ledger posting without manual recomputation.

Reject stale or unprovable FX handling#

Your FX control should be simple: if the rate used cannot be shown, timed, and approved, do not release the payout. Mixed timing across approval, settlement, and posting creates avoidable breaks in audit traceability.

Because public material here is thin, and one candidate payment-method source was blocked at access time, treat this as an internal policy decision and make it testable in operations.

Gate USDC the same way you gate fiat payouts#

If USDC rails are enabled, do not run them as an exception path. Require the same approval flow, local-value capture, contractor-level linkage, and archived reporting record you require for fiat payouts.

The production checkpoint is one joined record per payout event: provider reference, conversion evidence, and ledger posting must all point to the same contractor case.

Step 5 pick the right platform model for compliance ownership#

After settlement is defined, the key decision is ownership: who performs compliance operations, and who only provides tooling. Treat every model comparison as a contract-scope review, not a feature review.

Force each model through the same ownership test#

Use the same checklist for a software layer, a payment intermediary, and an EOR: named actions, named records, and named escalation duties. Do not infer legal responsibility from product labels alone; require written scope for who does what and who keeps which records.

For each model, ask practical questions for one contractor case: who reviews onboarding data, who handles document operations, who stores the payout-linked file set, and who answers escalation requests later. If a provider can show only transfer status and payout references, you are evaluating payout tooling, not proven ownership.

| Model | Compliance ownership question to settle in contract | Audit trail proof to request | Integration effort checkpoint | Ministerio del Trabajo escalation question |

|---|---|---|---|---|

| Software layer | Which tasks remain with your team, and which outputs are product-generated only? | One redacted contractor case showing onboarding, payout record, and archive export | Can your systems link ledger, tax-profile inputs, and payout events without manual stitching? | If classification risk is raised, who assembles the file and drafts first response? |

| Payment intermediary | Is scope limited to funds movement, or are document operations explicitly included? | Signed scope language plus sample exception handling output | Which extra fields must you pass for complete contractor records? | If labor-risk questions arise, do they provide only transfer logs or a fuller case file? |

EOR | Which actions are managed end to end, and which still require your approval/data? | Named deliverables, retention terms, and one sample case pack | How much of your onboarding/contract/finance flow must be replaced or duplicated? | Who is contractually responsible for escalation handling and document package delivery? |

Separate product language from legal responsibility#

Prioritize signed responsibility language over marketing claims. A provider can automate payments and still leave compliance operations with your team unless ownership is explicitly assigned.

Use a simple matrix with three labels only: vendor owns, you own, shared with approval split. Keep ambiguous phrases out of scope documents, because ambiguity usually becomes an operational gap during exceptions.

Choose managed scope when your team cannot run the document operation#

If your team cannot reliably run document operations internally, choose a model with explicit managed compliance scope rather than payout rails alone. The model label matters less than whether the agreement clearly transfers defined duties.

Before you sign, request one redacted end-to-end contractor evidence pack and test one escalation scenario: who pulls the file, who explains the decision trail, and what response time is committed. If the answer is only "the platform helps you manage it," treat ownership as yours until contract language proves otherwise.

For a step-by-step walkthrough, see Gig Worker Tax Compliance at Scale: How Platforms Handle 1099s W-8s and DAC7 for 50000+ Contractors.

Common rollout mistakes and how to recover fast#

Once ownership is written down, weak evidence hygiene is the fastest way to derail rollout. In the source set behind this section, the World Bank excerpt is front matter and disclaimer content, one payment-method page was blocked, and one Issuu excerpt is platform advertising copy rather than regulatory guidance.

| Issue | Recovery |

|---|---|

| Non-regulatory excerpts used as policy | Remove policy assumptions tied to that excerpt and mark those requirements as unverified until supported by authoritative, accessible sources |

| Blocked pages used as proof | Pause any requirement derived from that page, log the gap, and revalidate with accessible documentation before release |

| Marketing copy used as compliance scope | Separate commercial claims from compliance ownership and keep unresolved obligations explicitly marked as unknown until verified |

| Incomplete evidence filled with assumptions | Remove unsupported claims, document uncertainty, and reopen decisions only after the missing evidence is grounded |

The recovery pattern is simple: strip unsupported claims out of policy, mark unresolved requirements as unverified, and revalidate with accessible documentation before release. If the only support you have is marketing copy, blocked pages, or country-context material, slow rollout rather than filling the gap with assumptions.

You might also find this useful: How to Pay Contractors in Kenya: M-Pesa Pesalink and KRA Compliance for Platforms.

Final decision checklist before committing Colombia rollout#

Approve a Colombia rollout only when each item below has a named owner and a retrievable record. The evidence reviewed here supports country-level digital-finance context and terminology (including DIAN and COP), not platform-specific readiness.

- Validate the legal baseline.

Confirm your contractor path is documented in a signed contrato de prestación de servicios (CPS) flow and that your chosen classification controls (including four-factor risk) are applied in operations. Before go-live, you should be able to retrieve the contract template, role-approval record, and escalation path for borderline cases.

- Prove DIAN ownership end to end.

For DIAN (Colombia's National Tax and Customs Directorate), make ownership explicit for retención en la fuente, electronic invoicing, and the Certificado de Retención en la Fuente. Run a dry test and verify one system can produce the tax profile, payment support, withholding treatment used, and payout reference as a single audit packet.

- Qualify PSE and Nequi with provider evidence, not assumptions.

Treat both rails as non-production until your provider confirms your exact payout direction, reconciliation output, failure handling, and reversal behavior in writing. Country diagnostics can support market context, but they do not validate your specific rail setup.

- Test operating controls before launch.

Verify idempotent behavior, exception routing, and audit export completeness with test cases. You should be able to show that duplicate submissions do not create duplicate disbursements, failed transfers route to a named owner, and exports link identity, amount, currency, provider reference, and document status.

- Match the commercial model to your compliance capacity.

Choose the model your team can run consistently, not just the one with the lowest fees. If ownership for classification, DIAN records, or payout exceptions is still ambiguous, delay launch or move to a model with explicit compliance ownership.

This pairs well with our guide on How to Launch a Legal Compliance Platform for Freelancers and Handle Their Payments.

Frequently Asked Questions

Can a foreign platform pay contractors in Colombia compliantly without becoming the employer?

Potentially, but this grounding pack does not provide legal thresholds for contractor-vs-employee classification. It also does not establish that payout tooling by itself changes employer status, so classification has to be treated as a separate legal and tax determination.

What DIAN requirements are non-negotiable for contractor payout operations?

DIAN is Colombia's National Tax and Customs Directorate. For a definitive checklist of documentation requirements for contractor payouts, confirm the specific record requirements directly with DIAN or a qualified Colombian tax adviser.

Do PSE and Nequi support the same contractor payout use cases for platforms?

Do not assume they do. The grounded evidence here supports only a general point that bank accounts or digital wallets can be essential for secure, efficient money movement, and that each transfer method should be evaluated for advantages, restrictions, costs, and requirements. It does not confirm rail-specific behavior for PSE versus Nequi.

Who should own retención en la fuente and Certificado de Retención en la Fuente in a multi-vendor stack?

This grounding pack does not establish a universal owner for retención en la fuente or Certificado de Retención en la Fuente in all stacks. Ownership should be explicitly defined in your own contracts and operating procedures.

How should operators handle COP/USD contracts and TRM-based reporting in audits?

COP is the Colombian peso. No single TRM method or COP/USD audit treatment is mandated; whichever method you use should be internally documented and applied consistently.

When should a platform use an EOR model instead of a software-led payout model?

Digital financial services are a named topic area in the World Bank Colombia diagnostic, but that broader context is not a legal model-selection rule. Confirm decision criteria for choosing an EOR versus a software-led payout model with a qualified adviser.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 1 external source outside the trusted-domain allowlist.

- bancadelasoportunidades.gov.co/sites/default/files/2023-12/10302023_APR%20Y...trusted

- graduateschool.edu/learn/federal-human-resources/initial-pay-se...trusted

- gsa.gov/sell-to-government/step-1-learn-about-govern...trusted

- openknowledge.worldbank.org/bitstreams/8d6e85a7-fc28-4536-8bc0-3110aebc2...trusted

- thedocs.worldbank.org/en/doc/f6b57240332d70f3dbdfad5661c8c88d-0400...trusted

- thedocs.worldbank.org/en/doc/61714f214ed04bcd6e9623ad0e215897-0400...trusted

- ww2.ufps.edu.co/public/archivos/oferta_academica/47286337071...trusted

- archive.org/download/selectedepigrams00martuoft/selected...external

Educational content only. Not legal, tax, or financial advice.

Related Posts

Pay Contractors in Peru with Yape, PLIN, and SBS Checks

Treat Peru as a posture decision, not just a rail decision. If you choose a local wallet-style method first, then sort out contractor status, tax data, and evidence later, you may get a smoother payout experience. You also raise launch risk in areas that are much harder to fix once money starts moving.

Pay Contractors in Mexico: SPEI, CoDi, SAT, and CFDI Decisions for Platforms

Mexico contractor payouts usually break for a simple reason: teams launch from a generic Latin America plan, then discover that payout rail choices, tax steps, and operating structure cannot be separated in practice. If you are evaluating multiple rails and operating models at the same time, you need Mexico-specific decisions before you send the first live payout.

How to Pay Contractors in Kenya with M-Pesa, PesaLink, and KRA Controls

Kenya is worth serious consideration for contractor payouts, but you should not greenlight a launch just because M-Pesa is familiar and PesaLink is on the shortlist. The real decision is practical. Confirm which rail fits your contractor base, put local compliance and tax controls in place before money moves, and keep enough evidence to explain each payout later.