Quick Answer

Build corridor evidence first, then choose rails. Confirm country eligibility for YouTube and Substack, model Twitch payout thresholds ($50 for ACH/direct deposit, eCheck/local bank, PayPal, and check; $100 for wire), and run live tests before expanding. Use bank accounts as baseline reach, add wallets or local rails such as PIX and UPI only where verified, and keep stablecoin-backed options as opt-in pilots. Release payouts only after beneficiary validation, quote-expiry checks, and idempotent retry controls are in place.

Payout Reality Over Coverage Claims#

Global creator payouts can break when you treat them like a single integration. For YouTube, Twitch, and Substack-style products, payout behavior changes by country, destination type, threshold, and provider program. The launch decision is really a series of smaller operating decisions. If you want creator trust, optimize for predictable delivery and clear exception handling first, not for the broadest coverage claim.

Start with country rules, not provider marketing#

Your first filter is country-specific payout reality. YouTube states that available forms of payment depend on the creator's payment address, which is a direct reminder that payout method availability is not universal. Substack makes the same point differently: paid subscriptions depend on Stripe-supported countries, and it publicly notes exceptions for India, Brazil, Indonesia, Mexico, and Malaysia for additional technical reasons.

Before you scope product work, build a simple country-by-country matrix. For each launch market, record the creator country, the payout destination you expect to support, and the public rule that confirms or limits that path. Coverage changes over time, so a support page is a starting point, not a permanent fact. Use one simple rule: if you cannot show the current country condition and the expected endpoint for a corridor, mark that corridor unverified.

Separate payout eligibility from payout delivery#

A creator can be onboarded and still not be ready for an actual payout. Twitch is a useful reference because it makes thresholds explicit: the minimum payout is $50 for ACH or direct deposit, eCheck or local bank, PayPal, and check, while wire transfers require $100. Twitch also notes that final payout is only guaranteed once the minimum threshold is reached.

| Payout method | Minimum payout | Threshold note |

|---|---|---|

| ACH or direct deposit | $50 | Final payout only guaranteed once the minimum threshold is reached |

| eCheck or local bank | $50 | Final payout only guaranteed once the minimum threshold is reached |

| PayPal | $50 | Final payout only guaranteed once the minimum threshold is reached |

| Check | $50 | Final payout only guaranteed once the minimum threshold is reached |

| Wire transfer | $100 | Final payout only guaranteed once the minimum threshold is reached |

That matters if your platform has a long tail of creators with small balances. A rail may exist, but if many creators do not regularly clear the threshold, the payout experience can still feel slow or uncertain. A good early check is to model how many creators in each target country are likely to cross the threshold each cycle. If you skip that step, your support team may end up explaining why an "available" payout method is not practically usable for lower-earning accounts.

Treat every untested corridor as unknown#

Public coverage pages do not prove real settlement behavior for your specific corridors. They may not tell you enough about return handling, local currency disbursement, or whether a listed country works the way your payout model needs it to work. This is where teams get burned: they launch broadly, then discover that a corridor is technically listed but operationally unsuitable.

So treat incomplete or unverified provider data as unknown until you run your own corridor tests. Keep one evidence pack per target corridor with the support page, the eligibility rule, the threshold rule if one applies, and the result of a live or pilot payout. That is what lets you decide where to launch first, which methods to enable, and which controls you need before volume starts to compound. Related: EdTech Platform Payouts: Paying Tutors Course Creators and Content Authors.

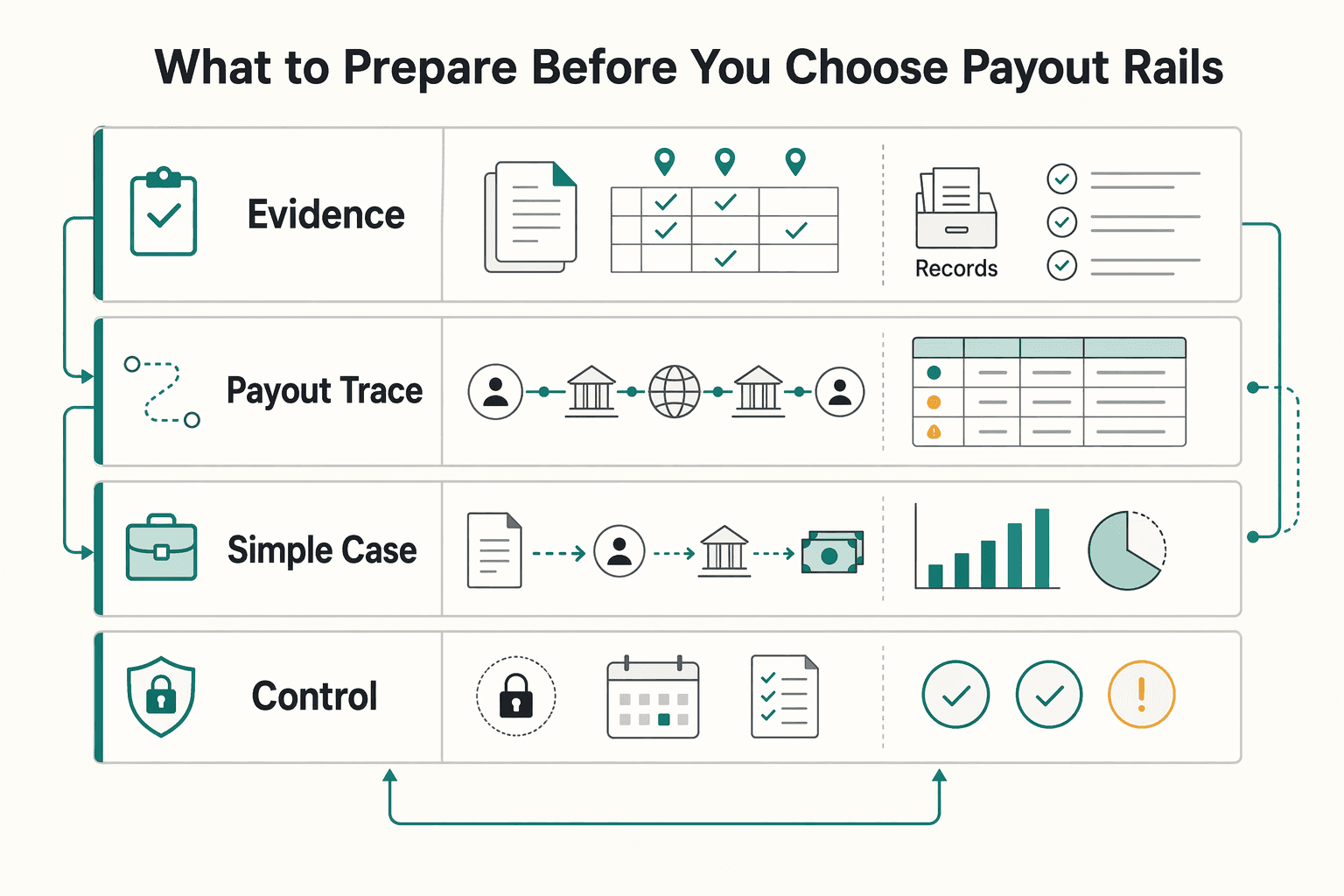

What to prepare before you choose payout rails#

Prepare your operating evidence before you compare providers. Once you have a country matrix, turn it into a selection file so each rail decision is tied to corridor reality, not coverage marketing.

-

Build a corridor evidence pack. For each launch corridor, record top creator countries, expected payout frequency, average payout size, and the endpoint type you expect to support first:

bank accounts,digital wallets, oralternative payment methods (APMs). Add a hard checkpoint: "preferred endpoint confirmed by creator mix: yes/no." -

Define operating limits before product conversations. Set your acceptable payout failure rate, target payout-time SLA, where compliance gates must sit, and what reconciliation evidence you need for

cross-border payments. Keep these as explicit internal thresholds and ledger outcomes, not labels like "fast" or "low failure." -

Collect provider proof, not claims. Require corridor behavior docs, webhook semantics, and beneficiary field requirements. Nium's country and regional guides cover payout behavior, beneficiary requirements, processing timelines, and return scenarios. Airwallex webhook docs cover subscriptions, delivery, retries, and signature verification, and its beneficiary flow uses a dynamic schema API for scenario-specific fields. Ask a simple question: can your team point to the exact doc or schema for retries, returns, and required beneficiary data?

-

Create a baseline shortlist and label unknowns.

Nium,Airwallex, andThunesare valid starting candidates because each publishes broad network coverage, but published footprint is only a filter. Nium publishes payouts to over 190 countries and real-time payments in more than 100 countries; Airwallex publishes bank payouts to over 200 countries/regions and local clearing in over 120 countries/regions; Thunes cites more than 720 members across 140 countries. For beneficiary verification, note whether a control such as Nium Verify (over 50 markets) matters in your first corridors.

If you want a deeper dive, read AI Influencer Payouts: How Platforms Pay Virtual Creators and Synthetic Brand Ambassadors.

Choose your first corridors with a market reality filter#

Choose first-wave corridors only where creator concentration, payout-method fit, and verified payout behavior align. If a country looks good on provider coverage but weak on creator demand, leave it for later.

| Launch filter | What to verify | Wave-one rule |

|---|---|---|

| Country presence is not enough | Supported payout methods, available currencies, delivery time and cut-off, and min/max limits | If you cannot verify method, currency, timing, and limits, keep that corridor out of wave one |

| Frequent, low-value payouts | Global average cost of 6.49 percent; PIX near-immediate transfers; UPI 24/7 operation | Do not assume PIX or UPI are available in every payout program or provider setup |

| Platform archetypes | YouTube monetization is country/region-dependent; TikTok Creator Rewards is country-dependent; Twitch Affiliate is globally available; Substack paid subscriptions are country-limited | Confirm each target corridor reflects your real creator mix, not a generic creator-economy assumption |

| Settlement and returns | Settlement behavior, return handling, and whether disbursement lands in local currency | If any of those outcomes are unverified, delay launch |

- Rank by creator concentration, then confirm corridor capability.

Start with countries that already drive your creator pipeline, then confirm the endpoint those creators need. In your corridor capability matrix, require more than country presence: supported payout methods, available currencies, delivery time and cut-off, and min/max limits. Filter: if you cannot verify method, currency, timing, and limits, keep that corridor out of wave one.

- For frequent, low-value payouts, prioritize strong local rails where available.

Cost pressure shows up quickly at micro-payout size. The World Bank's remittance data cites a global average cost of 6.49 percent, which is a practical warning for bank-only cross-border routes on small payouts. Where your program and provider support it, rails like PIX (near-immediate transfers) and UPI (24/7 operation) can be a better first fit. Do not assume PIX or UPI are available in every payout program or provider setup.

- Use platform archetypes to test corridor assumptions before launch.

Country access differs by creator model: YouTube monetization is country/region-dependent, TikTok Creator Rewards is country-dependent, Twitch Affiliate is globally available, and Substack paid subscriptions are country-limited. That changes who you can recruit and what payout pattern you will actually run. Checkpoint: confirm each target corridor reflects your real creator mix, not a generic creator-economy assumption.

- Set a no-go rule for settlement, returns, and local-currency clarity.

Do not launch a corridor until you can verify settlement behavior, return handling, and whether disbursement lands in local currency. A payout marked posted does not guarantee recipient receipt, and returned is a separate failure state that must be handled per corridor. If any of those outcomes are unverified, delay launch.

Match payout methods to creator behavior and unit economics#

Use a tiered default: bank accounts for broad reach, wallets/APMs for corridor-specific fit, and stablecoin options only as explicit pilots. Once corridors are validated, choose the endpoint that matches creator behavior and payout size, not the one marketed most aggressively.

Step 1. Set the default by creator segment. Bank accounts are usually the baseline for reach. Global Findex 2021 reports 76 percent global adult account ownership, which makes bank-linked payouts the least exclusionary starting point for many launches.

Wallets and other APMs are often a better fit in specific markets, but only when corridor support is confirmed. Worldpay reports digital payments at 66 percent of online payment value in 2024, while Stripe notes wallet coverage varies by country and device. So treat wallet fit as local, not universal.

| Endpoint | Best fit | Payout arrival predictability | Fee visibility | Changing payout destination | Verify before launch |

|---|---|---|---|---|---|

| Bank accounts | Broad creator base; larger or less frequent payouts | Varies by corridor and receiving bank | Usually clearer when FX and payout fees are separated | Can be high-friction if support review is required | Beneficiary field requirements, local-currency support, return handling |

| Digital wallets | Markets where creators already use wallets and expect faster access | Must be tested by country, wallet, and device | Can be opaque if wallet/conversion fees sit outside your UI | Works best when creators can switch destinations self-serve | Country coverage, device limits, wallet eligibility |

| APMs | Wallet-dominant markets with strong local method adoption | Depends on local partner coverage and program setup | Harder to predict unless fee labels are explicit | Varies by method/provider | Method availability by corridor, settlement behavior, support burden |

| Stablecoin-backed card issuance or USDC rails | Narrow segments that explicitly want crypto-linked access | Program-specific and still maturing | Can be unclear if spread/conversion/off-ramp costs are not shown | Needs a clear path back to fiat destinations | Program enablement, recipient eligibility, fallback payout options |

Step 2. Apply a unit-economics rule before UX debates. If payouts are small and frequent, prioritize local rails and wallet-like options you have tested live. If payouts are larger and less frequent, bank rails can still be acceptable when acceptance and reconciliation matter more than speed.

Step 3. Score creator experience, not just provider coverage. Evaluate each method on arrival predictability, fee visibility, and how easily creators can change their payout destination without opening a ticket. A method that is technically available but repeatedly creates payout-status support volume is a weak launch choice.

Step 4. Keep emerging options contained to explicit programs. Stablecoin-backed card issuance and USDC can be useful where program support is real, but they are not baseline defaults. Visa's 9/05/2023 USDC settlement expansion was framed as pilot and partner rollout activity, and Mastercard has said more work is needed for scale.

If you offer these options, keep them opt-in and reversible, with clear eligibility, fee display, and fallback to bank payouts.

Design funding and FX so margin does not erode at scale#

Protect margin by separating funding timing from payout execution, then enforce quote discipline at release time. Most FX leakage comes from timing drift, stale quotes, and weak guardrails, not one obviously bad rate.

| Rate or reference | Grounded facts | Operator use |

|---|---|---|

| ECB reference rates | Informational benchmarks published around 16:00 CET on working days for 30 currencies; averages rather than transaction prices | Use for context and benchmarking, not for promising settlement amounts |

| Indicative rates | Can differ at execution | Log when rates are indicative, what benchmark was used, and any spread or amount change between quote time and payout time |

| Executable rates | Quote-linked flows should track quote IDs and expiry timestamps | Validate quote ID, quote expiry, and payout initiation time before release, and block execution when the quote is expired |

| WMR references | Reuters-linked references built from transaction data | Use as a market reference, but not as your executable payout rate |

Step 1. Separate funding from payout timing. Decide whether you will hold value in the source currency, pre-convert into the destination currency, or convert with quote-linked execution close to payout release. In higher-volatility corridors, converting closer to the payout window can reduce open rate risk. In lower-volatility corridors with reliable forecasting, pre-conversion can reduce operational pressure if reconciliation stays clean.

Step 2. Label every FX rate as benchmark, indicative, or executable. ECB reference rates are informational benchmarks, published around 16:00 CET on working days for 30 currencies, and they are averages rather than transaction prices. Use them for context and benchmarking, not for promising settlement amounts. Treat indicative rates the same way: they can differ at execution, and quote-linked flows should track quote IDs and expiry timestamps.

Step 3. Reject stale quotes before payout initiation. Do not assume providers enforce expiry the same way. Your payout service should validate quote ID, quote expiry, and payout initiation time before release, and block execution when the quote is expired. That prevents old-rate batches from becoming reconciliation issues or creator support tickets later.

Step 4. Use pricing transparency as an operator control. Compare displayed rates to a public benchmark such as Reuters-linked WMR references, or to an available FX comparison tool from your provider. WMR can be a stronger market reference because it is built from transaction data, but it is still not your executable payout rate. Log when rates are indicative, what benchmark was used, and any spread or amount change between quote time and payout time.

Add compliance and beneficiary controls before volume ramps#

Before volume ramps, control failure risk by gating payout release behind verification and destination checks, not after money movement starts.

Step 1. Gate in order: setup -> identity -> destination validation -> release. For cross-border payments, this order keeps setup errors from becoming payout incidents. Required verification information, supported settlement currencies, and bank account formats vary by country and route, so release should stay blocked until required identity and destination fields are complete.

For each launch corridor, keep proof of every blocked release event: creator account ID, missing-field list, provider response (if any), timestamp, and the internal state change that prevented release.

Step 2. Validate the beneficiary before the first live payout per destination type. Run beneficiary validation before creating or activating a destination. Worldpay, Nium, and Airwallex all position this as a pre-payout control, and Airwallex can return a 400 with validation errors, which lets teams fix issues early.

Treat this as risk reduction, not a guarantee. It helps cut avoidable failures and duplicate support tickets tied to bad account details and format mismatches.

Step 3. Define explicit internal policy outcomes and evidence. Use internal states such as approved, held, returned, and escalated, and log why each transition happened. Provider statuses are not a substitute for your internal state model.

When a payout is held, capture hold reason and missing evidence. When it is returned, capture provider reference, return reason, and whether beneficiary validation had already passed.

Step 4. Keep availability language strict in product and ops docs. Do not claim broad coverage without verified corridor, onboarding, and program conditions. Stripe limits self-serve cross-border payouts to listed regions and requires the Full service agreement for that flow. Adyen notes that when local payout is unavailable or no local bank account exists, settlement uses cross-border transfer behavior.

Document those conditions in launch checklists. If the enabling condition is unclear, treat the route as unconfirmed, not launch-ready.

You might also find this useful: Affiliate Marketing for Creators Who Need Predictable Payouts.

Build failure handling that protects creators and ops teams#

Failure handling should be designed before payout volume ramps, because unclear failure states and unsafe retries are what turn routine issues into duplicate disbursements, unreconciled returns, and creator support spikes.

Step 1. Define failure classes before money leaves your ledger. Keep the list short and enforced so product, ops, and support use the same logic, messages, and evidence requirements.

| Failure class | What it means | Operator action |

|---|---|---|

| Invalid destination | Destination details are wrong or incomplete | Pause reissue, review return reason, collect corrected details |

| Compliance hold | Payout cannot proceed until review or hold clears | Keep funds held, collect missing evidence, do not auto-retry |

| Provider timeout | Request/webhook timed out before a usable result | Check provider state before any retry |

| FX expiry | FX quote is no longer valid | Requote, then create a new payout attempt tied to the new quote |

| Unmatched return | Funds returned but cannot be mapped to a payout record | Freeze reissue until IDs and ledger events reconcile |

Keep invalid destination distinct from returned payout: incorrect destination information is a primary driver of returned payouts, and returns can appear 2-3 business days later. Also model hold states explicitly; in some creator stacks, payout-method changes can trigger a 5-day hold.

Step 2. Enforce idempotent retries across global payout rails. Retries must be safe by default: replaying the same request should not create a second disbursement. Attach the idempotency key to a single internal payout intent, not to UI clicks, queue retries, or webhook deliveries. If amount, currency, beneficiary, or quote changes, create a new intent.

Timeouts are where teams most often create duplicates. A provider timeout or webhook timeout does not confirm failure, so verify current provider state before issuing another payout attempt.

Step 3. Require traceability from initiation to final state. Store one complete chain: internal payout intent ID, provider payout/transfer ID, beneficiary ID, timestamps, state transitions, and structured failure reason (code plus description). For reconciliation, keep the provider payout identifier (for example, a Stripe-style po_xxx) so transaction-level records can be retrieved and matched to ledger impact.

Step 4. Use a fixed incident sequence for operators. Run every incident through the same flow: detect, classify, decide retry or reroute, communicate ETA to the creator, and close with root-cause tags. Include severity (P0/P1/P2) in that workflow so triage is explicit, not improvised.

Apply strict decision rules by class: no auto-retry for invalid destination or compliance hold; verify provider state first for timeouts; requote and issue a new intent for FX expiry. Close with tags for corridor, endpoint type, provider, failure class, and root cause so recurring failure patterns stay visible and usable.

For a step-by-step walkthrough, see Best Merch Platforms for Creators Who Want Control and Compliance.

Score providers with a weighted matrix and rollout sequence#

Use a weighted matrix to pick test order, then let pilot evidence decide rollout. Documented coverage is useful, but broad launch should wait until each provider proves corridor fit, exception handling, and reconciliation in your stack.

Weight the matrix around payout reality#

Start with practical weights: corridor depth 30, payout methods 20, FX controls 15, validation tools 15, webhook quality 10, failure-state support 10. If your creator base is concentrated in a few high-volume corridors, shift weight toward local payout methods over headline country count.

| Provider | Documented inputs you can score now | Confidence flag now |

|---|---|---|

| Nium | 190+ payout countries, 100+ real-time locations, local rails including PIX and UPI, FX lock up to 24-hours, payout webhooks from initiation to settlement, sandbox access | Unknown until sandbox and pilot proof |

| Airwallex | Local and SWIFT payouts across 200+ countries/regions and 90+ currencies, beneficiary validation with explicit 200/400 outcomes, webhook event and payload structure, sandbox-to-production test path | Unknown until sandbox and pilot proof |

| Thunes | Production and pre-production environments, payout endpoints for mobile wallet, bank account, cards, and cash pickup, published rejected/compliance statuses (including 30392 REJECTED-COMPLIANCE-REASON) | Unknown where endpoint specifics are not public pre-onboarding |

Do not force a winner from public docs alone. In creator-economy payouts, marketing claims are hypotheses until your own payouts confirm them.

Promote confidence only after proof#

Move a row to verified in sandbox only after you can create a beneficiary, initiate a payout, capture the expected status/webhook event, and reconcile it to your internal payout intent. Move a row to verified in live pilot only after 1-2 pilot corridors show both successful payouts and observed failure paths with clean end-to-end records.

Roll out in phases, not by coverage headline#

Pilot 1-2 corridors first, then expand only when pilot thresholds are met. Track: payout completion stability, validation-failure rate, timeout/retry handling quality, manual exception volume, and reconciliation match rate.

Apply a hard rule: no broad launch until pilot corridors show stable payout completion, clear exception handling, and reconciled records from initiation through final ledger impact.

Need the full breakdown? Read Best Way for a German Agency to Pay a US-Based Freelancer.

Conclusion and launch checklist#

Teams that execute well usually do not start by switching on the most countries. They sequence the launch: choose corridors with real creator demand, match the endpoint to how those creators want to get paid, and prove controls before widening coverage.

Build a corridor pack you can defend#

Start with a corridor evidence pack, not a provider map. For each proposed launch country, document creator density, expected payout size and frequency, and the preferred endpoint type across bank accounts, digital wallets, and alternative payment methods (APMs). A useful external sanity check is the World Bank corridor baseline, which tracks 367 corridors from 48 sending countries to 105 receiving countries. It is not your business case, but it helps you compare corridor reality against assumptions.

The verification point is simple: can your team explain why each first corridor made the cut, what method you expect to use there, and what success looks like in delivery time, failures, and support load? If you cannot answer that in one page per corridor, you are still too early. One failure mode is launching where a provider has nominal reach but your creator concentration is weak or payout behavior does not fit the available rail.

Define FX and compliance before first live money movement#

The money flow should follow the payout sequence: capture accurate recipient details first, choose the payout currency, then apply compliance checks before funds move. Your FX policy should state whether you are using an indicative rate or a time-bounded quote, how long that quote is valid, and what happens at expiry. It should also say when conversion occurs and how quote validity is checked at execution time. Published quote windows such as 5 minute, 1 hour, and 24 hour are useful because they force an explicit expiry rule.

Add beneficiary validation before payment initiation, not after the first return. BIS frames pre-validation as checking the accuracy, validity, and completeness of payment information before sending, and links it to fewer rejections, returns, and manual interventions. Test two things on purpose: a stale FX quote path and an invalid beneficiary path. If your product cannot hold, reject, or escalate those cleanly, scale will expose it.

Label provider confidence before expansion#

Score providers, but label confidence honestly. "Verified in sandbox," "verified in live pilot," and "unknown" are more useful labels than polished coverage claims. Sandbox verification is useful, but it is not proof of identical live-market behavior. Require a reconciliation trace from your internal payout intent ID through the provider reference or quote ID to the final ledger state, including failures and returns.

Keep the go-live rule strict: no broad expansion until you have verified settlement behavior, return handling, and local-currency disbursement in the actual corridors you plan to use. That discipline matters because BIS has already warned that end-2027 cross-border targets may not be achieved on time.

Use this checklist in your launch doc:

- Corridor evidence pack complete (creator density, payout size/frequency, preferred endpoint type)

- Payout method matrix complete (

bank accountsvsdigital walletsvsalternative payment methods (APMs)) - FX policy defined (quote type, expiry handling, conversion timing, verification reference)

- Compliance and

beneficiary validationgates implemented and tested - Failure-state runbook tested with reconciliation trace

- Provider matrix scored with unknowns explicitly marked before go-live decisions

Frequently Asked Questions

What are the main ways to pay creators globally today?

The common payout endpoints are bank accounts, cards, and digital wallets. In practice, the bigger split is often between local payout rails in supported markets and traditional cross-border routes such as SWIFT when local options are not available. If you are deciding where to start, map endpoint type by corridor first, then test actual delivery and reconciliation behavior.

How do local rails like PIX and UPI change creator payout outcomes?

They can improve speed and cost where the provider actually supports those routes. PIX and UPI are large domestic payment infrastructures with published monthly transaction reporting, not niche options. The operator caution is simple: do not assume better outcomes until you verify settlement timing, return handling, and beneficiary data requirements in your own Brazil and India tests.

When should a platform use digital wallets instead of bank accounts?

Use wallets when your target market and provider support direct wallet payouts and creators actively use wallets. Bank accounts remain a core destination type across many cross-border payout networks. A practical rule is to pilot wallets in markets where your provider can show direct wallet connectivity and your support team can still trace status from payout initiation to final receipt.

What should we compare first when evaluating Nium, Airwallex, and Thunes?

Compare corridor and endpoint fit before anything else. Can the provider reach your target country through bank, wallet, or card, and is that route local or cross-border? Nium publicly states 190+ payout markets, and Airwallex explicitly documents local payouts as faster and more cost-effective than SWIFT. Then move straight to proof: create a beneficiary, send a test payout, capture the provider reference ID and webhook payload, and confirm your ledger matches the final state.

What usually breaks first in cross-border payments for creator platforms?

Wrong or missing beneficiary information is a documented early failure point, and it drives errors, exceptions, and manual support work. Another recurring problem is duplicate payment risk caused by system design rather than one-off operator mistakes. If you want one preventive control to implement early, do beneficiary pre-validation before first live payout and make retries idempotent with an internal payout intent ID tied to the provider transfer ID.

Are USDC and stablecoin-linked options practical for mainstream creator payouts yet?

They are practical in some programs, but they are not a universal default for mainstream creator disbursements. Visa has announced stablecoin payout pilots, and Thunes states that stablecoin payouts are available through a licensed partner, which tells you the market is still program-dependent. Use them only when recipients can actually receive value in a stablecoin wallet and your compliance, support, and treasury teams can handle the extra operational edge cases. For a deeper operator view, see Stablecoin Payouts for Platforms: How to Disburse USDC to Contractors Globally.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 1 external source outside the trusted-domain allowlist.

- bis.org/cpmi/publ/brief9.htmtrusted

- bis.org/publ/bisbull119.htmtrusted

- data.ecb.europa.eu/key-figures/ecb-interest-rates-and-exchange-...trusted

- docs.stripe.com/global-payouts/manage-payoutstrusted

- docs.stripe.com/payments/currencies/localize-prices/fx-quote...trusted

- remittanceprices.worldbank.orgtrusted

- worldbank.org/en/publication/globalfindex/brief/the-global...trusted

- airwallex.com/docs/payouts/beneficiaries/validate-a-benefi...external

Educational content only. Not legal, tax, or financial advice.

Related Posts

Stablecoin Payouts for Platforms Disbursing USDC to Global Contractors

**Step 1. Set the operating model before you talk about speed.** This guide is for platform operators shipping stablecoin contractor payouts in production, not for freelancers choosing a wallet. The core stance is simple: approve compensation in USD, use a stablecoin as the settlement rail, and treat controls as product requirements from day one. Stablecoins are built to behave like money, and businesses already use them for supplier payments, cross-border invoicing, and treasury movement. That makes stablecoin payouts worth a look, but only if your payout process is as disciplined as your fiat process.

AI Influencer Payouts for Virtual Creators

Treat this category as a money movement decision before you treat it as a growth story. A lot of the public discussion around **ai influencer payouts virtual creators** mixes product marketing with monetization advice. That tells you the market is paying attention. It does not tell you whether a payout program will launch cleanly or scale without constant exceptions.

How to Launch EdTech Platform Payouts for Tutors and Course Creators

**EdTech platform payouts are an operating decision before they are a product feature.** Once you start paying tutors, education agents, or other partners, you are not just sending money out. You are taking on partner disbursements, status tracking, and reconciliation across the money coming in and the money going back out.