Quick Answer

To pay contractors in Mexico reliably, choose your market entry model first, then build a SAT and CFDI document process, and only then approve payout rails such as SPEI or CoDi. Use one default rail for recurring payouts, require finance, legal, and payments ops sign-off by method, and keep traceable records for onboarding, approval, execution, reconciliation, and exceptions.

Why Mexico contractor payouts break after launch#

Mexico contractor payouts usually break for a simple reason: teams launch from a generic Latin America plan, then discover that payout rail choices, tax steps, and operating structure cannot be separated in practice. If you are evaluating multiple rails and operating models at the same time, you need Mexico-specific decisions before you send the first live payout.

Step 1. Start with Mexico-specific assumptions#

A regional guide can tell you that cross-border contractor payouts involve banking, tax, and compliance. What it often misses is who actually carries those obligations in Mexico and how a provider program changes what you can do day to day. That is where launches slip.

The product team may think it is choosing a payout rail, legal may think it is choosing a market-entry structure, and ops may think it is only onboarding contractors.

That mismatch matters early. The Mexico fintech guide in Chambers was marked last updated on March 31, 2026, and its contributor profile frames work in regulated sectors around regulatory compliance and decision-making. That is the right lens here.

Before you compare providers, verify three basics in writing: which Mexico payout routes the program supports, which entity is contracting with the contractor, and whether the money movement pattern matches that legal setup.

Step 2. Define the decisions before you scale#

This guide is meant to help founders and ops leads define an entry approach, assemble a minimum payout control path, and pressure-test rollout risk before volume makes every exception more expensive.

The sequence matters. First, choose how you are entering Mexico. Then define the minimum document and control pack. Then match rails to the use case. Then test how your team handles failures, holds, and reconciliation.

A useful pre-pilot checkpoint is simple: can you name the owner for contractor onboarding, tax document capture, payout approval, and payout exceptions? If not, you do not have a launchable process yet.

Step 3. Treat this as an execution map#

Use this guide as an execution map, not a universal rulebook. Coverage varies by provider program, banking partner, and legal structure. Different provider setups may all support contractor payouts differently, even if the outward product looks similar.

The surprises usually show up in the documents. For example, Intercam Banco's Service and Multiple Banking Products Agreement includes a customer statement that funds are of legal origin, and warns that false information or undeclared third-party account use may become a crime commission. That does not mean every bank uses the same wording. It does mean banking and payout arrangements are likely to be tested against actual account documentation, not just a sales-call summary.

The red flag is assuming your provider absorbs all Mexico-specific complexity. The better move is to confirm requirements before go-live, keep the written evidence, and expand only after your pilot proves the structure works under real exceptions.

If you want a deeper dive, read How to Pay Contractors in Kenya: M-Pesa Pesalink and KRA Compliance for Platforms.

Choose your market-entry model before choosing rails#

Pick the market-entry model first, then choose rails. Partner-led entry, local licensing, and intermediary setups can all be viable, but only if responsibility is clear in signed documents and your team has done its own due diligence.

Step 1. Compare models as operating choices, not rail choices#

| Model | Why teams evaluate it | What to verify before pilot |

|---|---|---|

| Partner with a local licensed entity | Often used when teams want to enter with local operating support | Which entity contracts with the contractor, what the partner is contractually responsible for, and what remains with your team |

| Obtain a Mexican license | Often evaluated when teams want more direct long-term operating control | Scope, timeline, internal ownership, and readiness for ongoing regulatory monitoring after launch |

| Use an invoicing and payment intermediary | Often considered to reduce internal operational buildout | Whether the intermediary's role is clearly defined in contract terms, and what records and controls your team still must maintain |

Use the table as a decision frame, not a legal conclusion. The Mexico 2020 U.S. Country Commercial Guide presents market-entry guidance as input for business judgment and explicitly says businesses should conduct their own due diligence before relying on that information.

Step 2. Assign responsibility in writing before you scale#

Do not rely on model labels alone. Responsibility should be explicit across your agreement set, including who contracts, who operates, who supports compliance work, and who manages exceptions.

Before pilot, confirm in writing:

- The contracting structure for contractor onboarding and payouts

- The compliance responsibilities each party accepts

- The reporting, records, and escalation process your team will rely on

If those points are ambiguous, rail selection is premature.

Step 3. Use a due-diligence checkpoint before rail selection#

Treat this as a documented checkpoint, not a feature comparison. Keep the signed commercial terms, role definitions, and compliance/process exhibits together so responsibilities are auditable.

That posture matches regulated-market practice: continuous regulatory monitoring supports better decisions over time. Even with partner support, your business still owns its decisions and remains responsible for complying with applicable laws and regulations.

You might also find this useful: Pay Contractors in Mexico With SPEI for Platform Operators.

Prepare the minimum document and control pack#

Treat the pre-payout pack as a hard release gate: if finance, legal, and payments ops cannot point to the same documents and owners, keep production payouts closed.

| Pack element | Included items | Release check |

|---|---|---|

| Prerequisites | Contractor classification policy; tax-document handling path; payout-method matrix for MXN and USD | Matrix shows allowed, disallowed, or approval-required by contractor segment and currency |

| Per-contractor evidence | Signed contract; tax-profile artifacts; proof of the selected payout method; audit trail | Traceability from onboarding and approval to payout submission and payout outcome |

| Method sign-off | Finance, legal, and payments ops sign-off by method | Finance confirms settlement and reconciliation impact; legal confirms contract and retention assumptions; payments ops confirms exception handling visibility |

| Exceptions gate | Owners for failed payouts, missing CFDI cases, and compliance-triggered holds | Escalation path and required record updates are in place before production payout |

- Write prerequisites before first payout.

Document your contractor classification policy, your tax-document handling path (including SAT/CFDI steps where your model requires them), and an approved payout-method matrix for MXN and USD. The matrix should show allowed, disallowed, or approval-required by contractor segment and currency so reviewers can confirm approval without relying on sales material.

- Build a defensible per-contractor evidence pack.

Keep the signed contract, tax-profile artifacts (including W-8 where relevant), proof of the selected payout method, and an audit trail linking onboarding, approval, payout submission, and payout outcome. The goal is traceability: not just that a payout happened, but why that payee, route, and currency were approved.

- Require finance, legal, and payments ops sign-off by method.

Finance should confirm settlement and reconciliation impact, legal should confirm contract and retention assumptions, and payments ops should confirm exception handling visibility. If PayPal is approved, record whether each flow is treated as domestic (same market) or international (different markets), and capture that its published pages include Currency Conversions and Withdrawals Out of PayPal, with exchange rates or card-issuer/bank fees that may still apply.

- Set an exceptions gate before go-live.

No production payout should go out until owners are named for failed payouts, missing CFDI cases, and compliance-triggered holds, with an escalation path and required record updates. For methods tied to policy-driven pricing or terms, log the reviewed page/version and approver; PayPal explicitly points users to its Policy Updates Page for rate/fee changes and timing.

This pairs well with our guide on Gig Worker Tax Compliance at Scale: How Platforms Handle 1099s W-8s and DAC7 for 50000+ Contractors.

Match payout rails to use cases in Mexico#

Set one default rail for recurring payouts, and treat other rails as exception paths until they pass the same operational checks. The goal is not the lowest headline fee. It is predictable status visibility, clean reconciliation, and clear ownership when payouts fail or are challenged.

Step 1. Build a rail table around evidence and exception handling#

Use a rail-selection table to force the same approval standard across methods:

| Rail | When to use it | What to verify before approval | Reconciliation burden |

|---|---|---|---|

| SPEI | Candidate for recurring flows if your provider supports it | Status lifecycle, return/hold handling, reference IDs, and audit-trail completeness | Depends on provider data quality |

| CoDi | Candidate only after product and ops validate the recipient flow | Completion states, proof-of-payment artifact, and failure-state ownership | Depends on completion and status visibility |

| Bank transfer | Common fallback path for approved banked contractors | Account validation, return-reason visibility, and change-control on recipient details | Depends on reference and return-code quality |

| Digital wallet | Exception or targeted segment path | Ownership checks, withdrawal path visibility, and support playbook for failed withdrawals | Often split across payout and withdrawal events |

| Card payouts (Visa/Mastercard) | Program-specific path where contract and provider support it | Recipient verification, decline/reversal handling, and end-to-end payout-state reporting | High if recipient receipt is hard to prove |

| PayPal | Exception path when recipient preference and support coverage are clear | Whether flow is treated as domestic or international (same market vs different markets), plus the exact approved product/fee pages | Medium to high when conversion, disputes, or withdrawals are in scope |

| SWIFT | Cross-border exception path | Intermediary handling, delay/return evidence, and full message/reference visibility | High unless full message trail is exposed |

For PayPal specifically, keep approval tied to the exact product context because published pages separate fee and exception buckets such as PayPal Payouts, Hyperwallet, Chargeback Fees, Dispute Fees, and Currency Conversions.

Step 2. Make exceptions earn approval#

Use the rail with the clearest status visibility and lowest exception load as your recurring default. Require explicit approval for all other rails, backed by a pilot trail from internal payout ID to provider submission ID to final paid/held/returned state.

Step 3. Decide MXN vs USD by conversion ownership and support boundaries#

Choose currency based on who absorbs conversion and where support issues will surface. In PayPal-related flows, document domestic vs international treatment under PayPal's market definition and record who owns conversion or withdrawal complaints, since exchange rates or card-issuer/bank fees may still apply.

Airtm and similar alternatives can help in some corridors, but keep them out of the recurring default until coverage, compliance scope, and support ownership are confirmed in writing. Related: How to Pay Contractors in Argentina: FX Restrictions and Compliance for Platforms.

Build a SAT and CFDI compliance sequence your team can run#

After you choose payout rails, set one written compliance sequence before any payout is released. The goal is operational traceability: who was onboarded, how the contractor was classified, which document was expected, what was received, and who approved release if anything was pending.

Step 1. Set the sequence before first payout. Use a fixed order your team can execute every time: onboarding checks, contract review, tax-profile capture, payout-method confirmation, payout approval, document retention, and post-payout reconciliation. For Mexico-facing records, define when a contractor-issued CFDI is expected under your model and where that status is recorded. Block approval when required fields are missing.

Step 2. Assign one owner per compliance question. If your model expects a contractor-issued CFDI or another SAT-facing artifact, keep issuance with the contractor and collection/storage with the platform. Internally, keep ownership explicit: legal for contract language, ops for document-status tracking, and finance for payout release plus post-payout matching. This avoids the common handoff failure where everyone assumes someone else has the record.

Step 3. Add a repeatable misclassification checkpoint. Before first payout, review contract language against actual scope of work together. If the engagement no longer matches the approved contractor model, escalate before release. Re-run the same check when scope changes on later payouts.

Step 4. Keep U.S. reporting touchpoints separate from Mexico payout approval. W-8 and FATCA workflows can sit in your broader tax profile, but they are separate from the Mexico payout-document sequence. Separately, Form 8938 can apply to certain U.S. taxpayers with specified foreign financial assets above $50,000, with higher thresholds for joint filers and taxpayers residing abroad; specified domestic entities can also have filing obligations above stated thresholds. Form 8938 reporting applies to taxable years starting after March 18, 2010, and if no income tax return is required for the year, Form 8938 is not required.

This does not mean every payout flow triggers Form 8938 or FBAR work. Route those questions to tax/treasury owners, keep contractor support focused on payout operations, and retain records that let your team answer year-end reporting reviews. FinCEN's FBAR page should sit on your compliance calendar because it publishes filing and extension notices.

For a step-by-step walkthrough, see IRS Form 1042-S for Platforms: How to Report US-Source Income Paid to Foreign Contractors.

Implement payout execution with traceable system states#

Use a single internal payout-state workflow so finance, ops, and support read the same record and act from the same source of truth.

Step 1. Define one internal state model and keep it authoritative. Set one lifecycle from request through close, and require every payout to sit in one current state at a time. For each transition, log who or what moved it, when it moved, and why.

Step 2. Treat retries as controlled reprocessing, not new payouts by default. When a request is retried, keep it tied to the original payout record unless a new payout is intentionally approved. This helps keep delayed responses from turning into accidental duplicate processing.

Step 3. Reconcile from your ledger outward. Keep one record per payout that links your internal payout ID to provider-side references and batch context. If those links are fragmented across tools, reconciliation and exception handling get slower and less reliable.

Step 4. Escalate by defined time windows and owners. Set explicit escalation paths for unresolved statuses, unmatched returns, and contractor-reported non-receipt. Require each dispute to be tied to the payout record before support responds so investigations stay traceable.

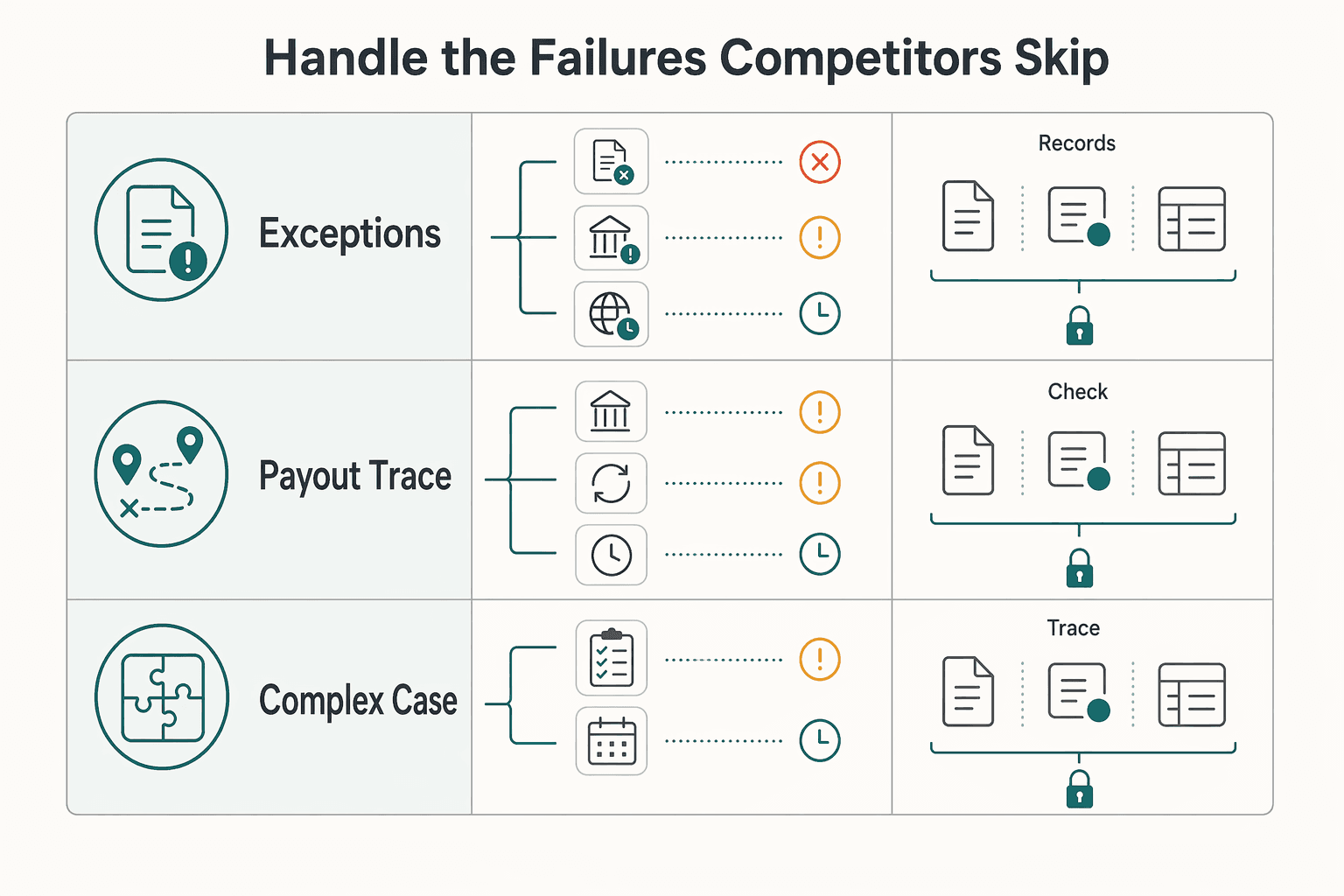

Handle the failures competitors skip#

Payout failures are part of operating this workflow; the objective is a repeatable response that prevents duplicate payments, contains risk, and improves the next decision.

| Failure case | Action | Record or control |

|---|---|---|

| SAT/CFDI document mismatch | Route back to compliance-gated and hold resubmission until contractor record, contract, and CFDI evidence align | Keep one record with the current state, latest provider or bank message, and the document set used at approval |

| Rejected transfer details or stale instructions | Keep in a payment-exception path and ask the contractor to reconfirm destination account or method | Attach the contractor confirmation to the case |

| Delayed SWIFT settlement | Keep in a payment-exception path and pause retries while one recovery path runs at a time | If rails are switched, use only a fallback already approved by finance and legal for that contractor segment |

| Repeated returns, identity-data conflicts, or unresolved classification concerns | Send to manual review immediately and do not auto-retry repeated returns for the same contractor | Close the incident with an update to routing rules, approval gates, or required evidence |

1. Classify the failure before any retry. Route SAT/CFDI document mismatches back to compliance-gated. Keep rejected transfer details, stale instructions, and delayed SWIFT settlement in a payment-exception path. In every case, keep one record with the current state, latest provider or bank message, and the document set used at approval.

2. Pause retries and run one recovery path at a time. For document mismatches, trigger compliance review and hold resubmission until contractor record, contract, and CFDI evidence align. For stale payout details, ask the contractor to reconfirm destination account or method and attach that confirmation to the case. If you switch rails, use only a fallback already approved by finance and legal for that contractor segment, and tell the contractor what is being checked plus the next update window.

3. Send high-risk cases to manual review immediately. Do not auto-retry repeated returns for the same contractor. Require manual review when identity data conflicts across contract, tax profile, and payout instructions, or when classification concerns remain unresolved. The risk is not only delay; it is paying the wrong person or paying before compliance concerns are cleared.

4. Close incidents with a control change, not a one-off fix. When a failure has a clear lesson, update routing rules, approval gates, or required evidence so the same SAT, CFDI, or SWIFT issue does not reappear under a new ticket.

Need the full breakdown? Read When Platforms File 1099 for Foreign Contractors and When W-8 Applies.

Use this launch checklist before scaling beyond pilot#

Use this as an internal readiness checklist and validate each item with your legal, tax, and payments owners before you expand volume.

| Readiness area | What to verify | Text signal |

|---|---|---|

| Ownership and documentation | Chosen operating path, who owns it, what is signed, and when renewals are reviewed | If finance, legal, and ops cannot give the same answer, stay in pilot |

| Routing and fallback rules | Allowed payout paths by contractor segment, currency handling, and fallback decisions | If exceptions still force ad hoc routing decisions, the setup is not scale-ready |

| Compliance and records | A full sample flow from onboarding through payout and one exception case | Required records can be retrieved quickly without manual reconstruction |

| Production controls | Retry behavior is duplicate-safe, status updates are captured in case history, and reconciliation ties each payout to provider or bank references | Payments ops and finance share explicit escalation ownership |

| Written scale gate | Pilot thresholds for error rate, manual-review load, and payout-timing reliability | If performance depends on heavy manual intervention, treat that as a no-scale signal |

- Lock ownership and documentation.

Document your chosen operating path, who owns it, what is signed, and when renewals are reviewed. If finance, legal, and ops cannot give the same answer, stay in pilot.

- Approve routing and fallback rules.

Define allowed payout paths by contractor segment, plus currency handling and fallback decisions. If exceptions still force ad hoc routing decisions, the setup is not scale-ready.

- Test compliance and records end to end.

Run a full sample flow from onboarding through payout and one exception case. Confirm required records can be retrieved quickly without manual reconstruction.

- Verify production controls are live.

Confirm retry behavior is duplicate-safe, status updates are captured in case history, and reconciliation ties each payout to provider/bank references. Confirm payments ops and finance share explicit escalation ownership.

- Pass a written scale gate.

Set and enforce pilot thresholds for error rate, manual-review load, and payout-timing reliability before expansion. If performance depends on heavy manual intervention, treat that as a no-scale signal.

We covered related tax-operations context in FATCA Compliance for Marketplace Platforms: Identifying and Reporting Foreign Account Holders.

Make the expansion decision with operations, not marketing#

Make the call in this order: entry model first, rail strategy second, compliance sequence third. The right setup is the one your team can run with clear controls, fast exception handling, and records you can retrieve without friction.

- Choose the entry model before debating rails.

Mexico sits in a regulated fintech environment, and the Chambers Mexico fintech guide describes work in highly regulated sectors with compliance as a core concern (last updated March 31, 2026). Before rail selection, align one accountable owner for the contractor relationship, payout responsibility, and record retention path.

- Set rail strategy only after ownership is clear.

CoDi is a named electronic payment platform (Digital Collection, Cobro Digital), but naming a rail is not the same as proving operations. Use pilot samples to confirm each payout can be traced end to end in one record set, including approval, execution status, and supporting compliance documentation.

- Prove the compliance sequence in a pilot before broad rollout.

Run a pilot cohort, log real failure modes, and confirm your team can resolve them without manual heroics. This is especially important when macro conditions are softer: the IMF notes Mexico's activity has been soft since mid-2024 and that rising trade uncertainty contributed to the slowdown.

Related reading: W-8ECI for Platforms Handling Foreign Contractors With Effectively Connected US Income.

Frequently Asked Questions

Can a foreign platform pay contractors in Mexico without setting up a local entity?

Sometimes. Before payouts, align the contract terms, payout flow, and documented responsible party, and validate the setup with local counsel.

What is the practical difference between partnering with a local licensed entity and getting a Mexican license?

It depends on the structure and agreement terms. In either model, confirm in signed documents who contracts with the contractor, who handles contractor checks and payout exceptions, and who owns record retention and compliance responsibilities.

When should we use SPEI versus CoDi for contractor payouts?

There is no universal default. Use the rail your team can reconcile and support reliably at expected volume, and approve it only after testing status visibility, audit-trail retrieval, and failure handling.

What is the minimum SAT and CFDI process we should enforce before releasing payouts?

There is no one-size-fits-all legal minimum in this section. Define SAT and CFDI requirements with local tax and legal advisors. Hold payouts when required identity, tax, or invoice records are missing or inconsistent.

Do we need an EOR, or can we use an invoicing and payment intermediary model?

It depends on worker classification and your risk posture. An invoicing and payment intermediary can support operations, but it does not automatically remove classification or compliance obligations. Use an EOR model when your legal analysis requires employer-of-record coverage.

How should we handle MXN versus USD payouts to reduce operational and reconciliation risk?

Set a documented currency policy by contractor segment that defines who absorbs FX, when rates are fixed, and how ledger amounts are reconciled. If both currencies are offered, define the fallback path before launch and assign ownership for conversion or withdrawal issues.

Where do FATCA, W-8, FBAR, and FinCEN considerations enter a Mexico contractor payout program?

These items sit in the broader U.S. tax reporting process, not the Mexico payout approval sequence. Form 8938 is attached to the taxpayer's tax return and can apply to certain U.S. taxpayers with specified foreign financial assets above stated thresholds, while FBAR is a separate FinCEN filing for U.S. persons with a financial interest in, or signature authority over, foreign financial accounts. W-8 handling should follow your tax documentation process, and FBAR and Form 8938 should not be treated as interchangeable.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- bis.org/publ/bppdf/bispap143.pdftrusted

- documents1.worldbank.org/curated/en/232351656600389457/txt/Mexico-COV...trusted

- documents1.worldbank.org/curated/en/099122125121523841/pdf/P505272-3c...trusted

- downloads.regulations.gov/USTR-2025-0016-0053/attachment_1.pdftrusted

- downloads.regulations.gov/FAA-2025-1571-0437/attachment_1.pdftrusted

- elibrary.imf.org/view/journals/002/2025/286/article-A001-en.xmltrusted

- executive.berkeley.edu/thought-leadership/blog/7-essential-steps-pu...trusted

- files.eric.ed.gov/fulltext/ED326366.pdftrusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

FATCA and W-8 Tax Compliance for Platforms: When to Release, Hold, or Withhold Foreign Payouts

---

How to Pay Contractors in Kenya with M-Pesa, PesaLink, and KRA Controls

Kenya is worth serious consideration for contractor payouts, but you should not greenlight a launch just because M-Pesa is familiar and PesaLink is on the shortlist. The real decision is practical. Confirm which rail fits your contractor base, put local compliance and tax controls in place before money moves, and keep enough evidence to explain each payout later.

Pay Contractors in Argentina Under FX Restrictions as a Platform Operator

**Step 1. Start with the decision, not the market story.** This guide is for founders and ops leads deciding whether Argentina should ship now. If you have not already committed product, treasury, and support capacity, the real question is not market size or broad LATAM demand. It is whether you can pay contractors in Argentine peso (ARS) while handling FX-related constraints with a level of compliance work and exception handling your team can actually sustain.