Quick Answer

Platforms should treat Form W-8ECI as a narrow exception path, not a routine foreign-payee form, and accept it only when the record supports U.S.-source income that is effectively connected with a U.S. trade or business. Verify foreign-person status, the payment's U.S. income link, and the payee's U.S. TIN if withholding relief is claimed, then keep withholding and Form 1042-S reporting as separate decisions.

When a Platform Should Collect Form W-8ECI#

-

Form W-8ECI is a narrow claim, not a generic foreign-payee form. Risk starts when a foreign contractor presents Form W-8ECI instead of the more familiar Form W-8BEN. The Internal Revenue Service describes W-8ECI as the certificate a foreign person uses when they are the beneficial owner of U.S.-source income that is effectively connected with the conduct of a trade or business within the United States. That is a very different tax posture from simply being a non-U.S. contractor. If your intake treats W-8ECI like a routine substitute form, you can assign the wrong withholding treatment before anyone checks the underlying facts.

-

This matters most when your team is making repeatable payout decisions at scale. It is not just a one-off tax memo issue. It affects compliance, legal, finance, tax ops, and risk owners who need a consistent answer each time a nonresident alien, foreign corporation, or other non-U.S. payee claims ECI. One practical detail is often missed: Form W-8ECI is given to the withholding agent or payer, not sent to the IRS. That means the withholding agent or payer needs an internal process to decide whether the form supports the requested treatment and to document how the claim was handled. A weak intake record is not just messy documentation. It is a control gap tied directly to withholding and reporting outcomes.

-

The goal is controlled decisioning, not maximum paperwork. If you receive a valid W-8ECI with the required payee representations, the IRS says you generally do not need to withhold tax on ECI income, including where the income is represented as includible in the payee's gross income. If the beneficial owner fails to provide a requested W-8ECI, the instructions warn that withholding at the 30% rate may apply. Those are the accept-or-reject stakes, but they do not solve the hard middle. You still need an escalation point for claims that mention ECI but do not clearly support a U.S. trade or business (USTB) position.

Start with a simple checkpoint. Verify that the payee is actually claiming foreign status and using the right form for that claim. Then confirm that the record ties the form to U.S.-source income and an ECI position. A common failure mode is accepting the document because it is signed and looks current, while never capturing the business facts that explain why W-8ECI was used instead of W-8BEN. Where source detail is limited, such as exact refresh cadence, this article flags legal-tax escalation points instead of pretending the IRS gives platforms one clean decision matrix. Related reading: How Platforms Are Reshaping Foreign Exchange in 2026.

How to choose the right W-8ECI control depth#

Choose control depth based on operational risk, not maximum process. If you pay both nonresident alien individuals and foreign corporations across multiple payout rails, and you see recurring U.S.-source income claims, simple form collection is usually not enough.

| Control depth | Use when | Core controls | Tradeoff |

|---|---|---|---|

| Light control depth | Foreign-payee volume is low, U.S.-linked payments are infrequent, and you can handle occasional manual review | Collect Form W-8ECI, confirm foreign-person status, verify the form was received before income is paid, credited, or allocated, and require a short note explaining the ECI basis | Fast when exceptions are rare, but weaker support later for withholding and Form 1042-S decisions if the file has only a signed form and no reasoning |

| Moderate control depth | You handle mixed foreign payees, recurring U.S.-source payments, and multiple payment methods | Add defined checkpoints for form receipt, payee type, income linkage, and escalation when the ECI narrative is incomplete or inconsistent | Prevents avoidable payout errors, but does not settle every tax question in-product |

| Tight control depth | U.S.-source cases are frequent, reporting accuracy risk is high, or audit expectations require full decision reconstruction | Keep decision notes, reviewer identity, timestamps, and a clear explanation of why W-8ECI treatment was accepted | More review overhead and slower contractor onboarding, but cleaner support for Form 1042-S preparation and fewer surprises in withholding treatment |

- Light control depth

Use this when foreign-payee volume is low, U.S.-linked payments are infrequent, and you can handle occasional manual review. Collect Form W-8ECI, confirm foreign-person status, and verify the form was received before income is paid, credited, or allocated.

This is fast when exceptions are rare. The tradeoff is weaker support later for withholding and Form 1042-S decisions if the file has only a signed form and no reasoning. At minimum, require a short note explaining the ECI basis.

- Moderate control depth

Use this when you handle mixed foreign payees, recurring U.S.-source payments, and multiple payment methods. Add defined checkpoints for form receipt, payee type, income linkage, and escalation when the ECI narrative is incomplete or inconsistent.

The goal is to prevent avoidable payout errors, not to settle every tax question in-product. This matters because withholding agents have Form 1042-S filing obligations for covered foreign-person payments, and reporting can still apply when no amount is withheld.

- Tight control depth

Use this when U.S.-source cases are frequent, reporting accuracy risk is high, or audit expectations require full decision reconstruction. Keep decision notes, reviewer identity, timestamps, and a clear explanation of why W-8ECI treatment was accepted.

The benefit is fewer surprises in withholding treatment and cleaner support for Form 1042-S preparation. The cost is more review overhead and slower contractor onboarding, especially for borderline facts that still need legal or tax escalation. That tradeoff is often justified where invalid or missing documentation can create exposure to 30% assessed tax under chapter 3 or 4.

If you only pay domestic contractors and have no W-8 intake path, this control layer is usually unnecessary. If you do accept foreign-payee tax forms, start with the lightest version that still forces one hard checkpoint before payment: is there a complete W-8ECI, and does the record explain why this is an ECI claim?

If you need a quick next step, try the W-8 form generator.

Best for low-complexity payout programs#

A light W-8ECI lane is usually the right fit when your cross-border payouts are limited and service types are narrow. The goal is a defensible intake gate, not a heavy review workflow.

- Where this fits

Use this model when foreign-payee volume is low and most payouts follow a small number of repeatable fact patterns, such as an early-stage creator marketplace onboarding its first foreign contractors.

- Minimum viable controls

Collect Form W-8ECI, confirm the payee is a foreign person, and require a short written rationale tying the claim to income effectively connected with a U.S. trade or business. If you are relying on the ECI withholding exemption, the form must include the payee's U.S. TIN. Keep a record of when the form was received and who accepted it.

- Main tradeoff

This is fast to implement with basic platform compliance controls, but it is easier to break when facts change. If circumstances change, the payee must notify the payer within 30 days and provide a new Form W-8ECI or other appropriate form. If your process cannot reliably surface those changes, escalate sooner instead of assuming this light model will remain sufficient. Related: Crypto Payouts for Contractors: USDC vs. USDT - What Platforms Must Know.

Best for mixed contractor and seller models#

If you run mixed contractor and seller models, use one onboarding flow that routes to Form W-8ECI, Form W-8BEN, or Form 8233 based on income facts, not payee preference or product segment.

This model fits platforms handling services on one side and inventory-linked or marketplace earnings on the other. The benefit is fewer misclassified forms across segments. The tradeoff is higher policy complexity and more reviewer training on Internal Revenue Code concepts like Effectively Connected Income (ECI), USTB, FDAP income, and withholding exemptions.

| Lane | Trigger conditions | Required evidence | Likely withholding treatment | Form 1042-S step |

|---|---|---|---|---|

| Form W-8ECI | Facts indicate the foreign beneficial owner is claiming ECI tied to U.S. business activity | Valid Form W-8ECI plus a short written rationale tying the payment to ECI and U.S. business activity | ECI is generally not handled under NRA withholding in the same way as FDAP when valid ECI documentation supports the claim | Do not treat reduced withholding as no reporting; ECI is often still reportable, so check the Form 1042-S path |

| Form W-8BEN | Foreign beneficial owner is providing standard withholding documentation for amounts subject to withholding, and ECI facts do not control | Valid Form W-8BEN plus decision notes showing why the ECI lane was not used | Test whether the payment is U.S.-source income subject to withholding, including possible FDAP treatment | If reporting applies, map the payment for Form 1042-S handling |

| Form 8233 | Payee is claiming a withholding exemption on eligible personal services compensation, often where treaty logic is central | Form 8233 plus support that the payment is personal services compensation and the exemption claim matches the facts | Test the exemption claim first. If it does not apply, section 1441 generally requires 30% withholding on independent personal services compensation | Compensation and any withholding result may still feed Form 1042-S reporting |

The key routing rule is simple: if the facts support ECI plus a USTB position, route to the W-8ECI lane first. For withholding exemption on ECI, IRS materials point to Form W-8ECI or Form 8233 depending on the facts, so treaty logic is not a shortcut around the ECI analysis.

Use intake notes to separate three points: what the payment is for, what tax basis is claimed, and what facts support U.S. business activity. That means distinguishing personal services compensation, seller proceeds, or another income type; separating ECI, standard foreign-status documentation, or treaty exemption; and capturing the facts offered to support U.S. business activity. USTB analysis requires judgment because the activity must be "considerable, continuous and regular."

A common failure mode is classifying by segment instead of tax character, such as treating all contractor payments as treaty-exemption cases and all seller payments as automatic W-8BEN files. That can miss cases where services or business activity support ECI, or where inventory-linked earnings still lack enough facts to resolve FDAP versus ECI.

If a submission includes both a treaty exemption claim and a USTB story, do not auto-approve either lane. Hold the treatment decision, document the conflict, and escalate for specialist review. The strongest control is a clear reviewer note showing why one form was accepted and why the other two were not, linked to a Form 1042-S reporting flag so withholding and reporting stay separate decisions.

For a step-by-step walkthrough, see India Equalisation Levy: What Foreign Platforms Must Pay on Digital Advertising Services.

Best for high-risk edge cases and legal escalation#

Use this lane when the intake record does not support a reliable classification and a reasonably prudent reviewer would question the claim. In these files, stop automation and require manual legal or tax review.

| Escalation case | What to check | Handling |

|---|---|---|

| Borderline USTB facts | Whether the record supports activity that is "considerable, continuous and regular," whether Form W-8ECI includes the payee's U.S. TIN, and how the payment ties to U.S.-linked business activity | Stop automation and require manual legal or tax review |

| Conflicting tax positions | Whether treaty logic and an ECI position overlap, or statements conflict across contracts, invoices, and onboarding responses | Treat it as a reason-to-know issue and pause approval rather than guessing between W-8ECI and treaty treatment |

| Reliability and source-income gaps | Whether the certificate appears unreliable or the relationship to U.S.-source income is unclear | Do not rely on the form as submitted for chapter 3 treatment; presumption-rule withholding may apply, including the default 30 percent rate |

- Borderline USTB facts

Escalate when a payee claims Effectively Connected Income but the record does not clearly support activity that is "considerable, continuous and regular." There is no mechanical checkbox cutoff for this test. Start with baseline validity: a Form W-8ECI must include the payee's U.S. TIN, then document how the payment ties to U.S.-linked business activity.

- Conflicting tax positions

Escalate when treaty logic and an ECI position overlap, or when the payee's statements conflict across contracts, invoices, and onboarding responses. If a reasonably prudent reviewer would question the claim, treat it as a reason-to-know issue and pause approval rather than guessing between W-8ECI and treaty treatment. For overlap cases, W-8ECI vs W-8BEN is a useful comparison, but the decision still belongs in manual review.

- Reliability and source-income gaps

If the certificate appears unreliable or the relationship to U.S.-source income is unclear, do not rely on the form as submitted for chapter 3 treatment. In that situation, presumption-rule withholding may apply, including the default 30 percent rate. Using an outside reviewer does not shift the withholding-agent knowledge standard away from your platform.

Best for audit-heavy compliance teams#

Use this lane when you need to reconstruct a W-8ECI decision months later under internal or regulator review. The core test is whether you could reasonably rely on the form without actual knowledge, or reason to know, that its certifications were unreliable or incorrect.

- Decision-grade evidence pack

Keep each file complete enough for a new reviewer to re-run the judgment without the original analyst. Include the submitted Form W-8ECI, the payee entity type (nonresident alien or foreign corporation), decision notes tying the claim to U.S.-source income and an Effectively Connected Income posture, reviewer identity, and timestamped approval records. The key control is the written rationale for using the ECI path for a foreign beneficial owner, not just a completed intake form.

- Policy versioning tied to approval date

Save the exact rule set or decision standard in force when the case was approved. That lets you defend not only what was decided, but why it was correct at that time. In practice, store a policy version ID with the case, plus masked record snapshots and audit-trail links that cannot be quietly overwritten. Federal sources here do not require a specific immutable-trail technology, but this control improves defensibility when policies or teams change.

- Reporting and retention linkage

Link the W-8ECI decision to downstream reporting evidence, especially Form 1042-S treatment. IRS materials position Form 1042-S as the core information return for amounts paid, withheld, and deposited, and withholding agents must retain each Form 1042-S copy for the statute-of-limitations period on assessment and collection. If intake decisions, payment outcomes, and 1042-S records do not reconcile, the file is weak even when the original form is present.

This model fits enterprise marketplaces with centralized compliance sign-off and recurring control testing. If reviewer notes do not explain why the team had no reason to doubt form reliability, the file is not audit-ready. If reliability later fails, chapter 3 exposure can revert to the 30 percent baseline.

The tradeoff is straightforward: stronger Internal Revenue Service defensibility in exchange for higher storage and governance overhead across policy changes.

Need the full breakdown? Read How Gig Platforms Report 1099s for Thousands of Contractors at Year-End.

Best for reporting and withholding readiness#

If year-end breaks are your main risk, design the W-8ECI lane for clean reconciliation before payment release. Finance should be able to show the withholding result, the Form 1042-S path, and the supporting record at the same time.

- Checkpoint chain from intake to reporting output

Treat an accepted Form W-8ECI as the start of the finance decision, not the end of intake. Record four states in order: form accepted, tax treatment assigned, withholding flag validated, and Form 1042-S path confirmed. Keep each state visible in the payment record so reviewers can trace whether a foreign payee's U.S.-source income was handled as Effectively Connected Income and carried through to reporting.

Include one hard control in that chain: if withholding is below 30%, capture the chapter 3 exemption code in output. Also separate these statuses in your logic: no chapter 3 withholding does not automatically mean no 1042-S filing.

- Pause treatment when documentation is incomplete or conflicting

If records are incomplete or contradictory, hold payout treatment and route to exception handling before payment release. Apply that rule when ECI is claimed but support is unclear, when the payee record conflicts with the submitted form, or when required reporting fields are missing.

This is mostly a timing control. Waiting until payment ops or year-end prep increases the chance of default 30% withholding exposure when required documentation is not on file. Your exception packet should include the submitted W-8ECI, treatment rationale, withholding flag state, and the reason the record is not yet reliable.

- Document unresolved policy points and assign ownership

Do not invent rules that are not clearly established in the materials you rely on. If refresh cadence is not clearly established, mark it as a legal-tax interpretation item, assign an owner, and define interim operating steps for finance.

This prevents deadline surprises. For e-file operations, IRIS is available beginning January 1, 2026 for 2026 Forms 1042-S due March 15, 2027, so unresolved classification issues should be escalated well before file generation. If finance cannot explain why a payment was below standard withholding and still reportable on 1042-S, the process is not ready.

We covered this in detail in Form 1042-S for Foreign Persons With U.S.-Source Income.

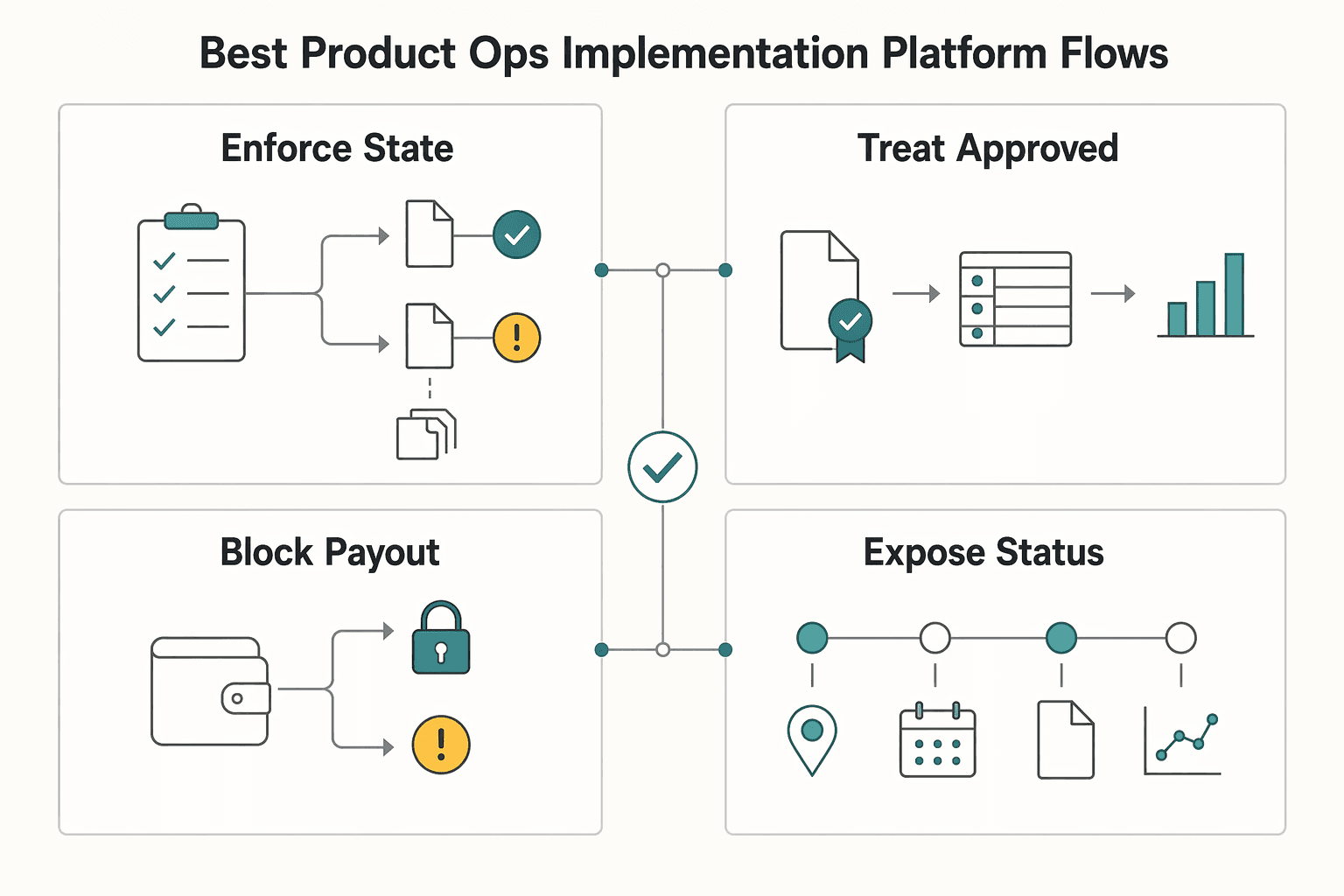

Best for product and ops implementation in platform flows#

Once finance sets the withholding and 1042-S outcome, product and ops should enforce it in flow logic. Do not let form uploaded unlock payout; in a W-8ECI lane, payout eligibility should turn true only after tax form validation and compliance approval are complete.

| Flow control | Operational rule | Key detail |

|---|---|---|

| Enforce state order before payout | Use a fixed sequence: intake -> tax form validation -> compliance approval -> payout eligibility -> monitored status events | Form W-8ECI is documentation given to the withholding agent or payer, not an IRS filing step, and onboarding can still complete before payout is enabled |

| Treat approved status as conditional | Move status back to review-required or restricted when a change in circumstances makes the form incorrect | IRS instructions require updates within 30 days after a change in circumstances that makes the form incorrect |

| Block payout and make retries safe | Use a payout-eligibility flag with machine-readable hold reasons and make approval or release actions idempotent | This prevents payout attempts from racing ahead of tax resolution and reduces duplicate side effects in compliance and payout retries |

| Expose status through events | Surface states like review-required, approved, payout-disabled, and re-verification-needed through a webhook endpoint or equivalent event channel | Monitoring should continue after initial approval because requirements can change over time |

- Enforce state order before payout

Build onboarding as a fixed sequence: intake -> tax form validation -> compliance approval -> payout eligibility -> monitored status events. Form W-8ECI is documentation given to the withholding agent or payer, not an IRS filing step, so the first checkpoint is whether your platform has a usable form on file for its own records. Onboarding can still complete before payout is enabled.

After approval, assign treatment explicitly. If the case is accepted as Effectively Connected Income, that may support no withholding in non-partnership contexts when a valid W-8ECI is on file, but only as a review outcome, not because a file was uploaded.

- Treat approved status as conditional, not permanent

A valid form today is not a permanent green light. IRS instructions require updates within 30 days after a change in circumstances that makes the form incorrect, so you need a stale-state trigger tied to changed facts, not just one-time intake checks. When facts change, move status back to review-required or restricted.

Quiet drift is the main failure mode: case details can stop matching what was approved. Without a reopen-review path, ops often finds this only after payout or during year-end work.

- Block payout explicitly and make retries safe

Prevent payout attempts from racing ahead of tax resolution. Use a payout-eligibility flag with machine-readable hold reasons, and make approval or release actions idempotent so retries do not create duplicate reviews or accidental releases. Idempotency keys directly reduce duplicate side effects in compliance and payout retries.

If your provider supports tax-based payout gating, connect that behavior to your own hold logic. One published example disables payouts when required tax information is not collected and verified once connected accounts reach $600 in charges, but treat that threshold as provider-specific, not universal.

- Expose status through events, not only admin UI

Tax status changes should be visible where ops already monitors payout and verification risk. A webhook endpoint or equivalent event channel should surface states like review-required, approved, payout-disabled, and re-verification-needed, and compliance exports should carry the operational record needed for review. Monitoring should continue after initial approval because requirements can change over time.

Use qualifiers like "where supported" and "when enabled" in UX and policy text so global programs do not overstate coverage across regions, entities, or payout setups.

If you want a deeper dive, read IRS Form 8233: When Foreign Contractors Claim Treaty Exemptions and What Platforms Must Verify.

Conclusion#

The practical takeaway is not to collect more forms. It is to make the right call at the right checkpoint, then be able to explain that call later.

- Use Form W-8ECI as an exception path

Treat Form W-8ECI as a specific claim posture, not your generic foreign-payee intake option. The form is for a foreign person claiming that the income is effectively connected with a U.S. trade or business and will be included in U.S. gross income, so your acceptance decision should start with those facts, not with the payee's preference. The hard checkpoint is not just foreign status. It is whether the file supports U.S. trade-or-business engagement for the tax year, plus the required form representations. If the payee wants withholding relief on that basis, the W-8ECI must include a U.S. TIN. A missing TIN or other material fact conflicts are strong signals to pause and escalate.

- Separate intake approval from withholding and reporting approval

A valid ECI claim can change withholding treatment, but it does not end your tax operations work. The IRS instructions for Form 1042-S make the key point plainly: you may still need to file Form 1042-S even when you did not withhold tax under chapter 3. The common failure mode is assuming "no withholding" means "no reporting." Build one checkpoint after form review and another before year-end reporting so finance can confirm that the treatment still maps to Form 1042-S output and the March 15 filing deadline. Also remember that W-8ECI is not blanket no-withholding logic in every case; the IRS specifically notes situations where withholding is still normally required, including some payments for independent personal services performed by a foreign individual.

- Keep an evidence pack that explains the judgment, not just the form

If a decision is worth making, it is worth being able to defend months later. The record should include the submitted form and the facts you relied on, such as the payee's beneficial-owner representation, the ECI claim, the gross-income inclusion representation, and the basis for believing the income is tied to U.S. business activity. Do not confuse storage with defensibility. A PDF alone is often not enough when the facts were borderline. You want enough context to show why the claim was accepted, rejected, or routed to specialist review, especially if the same payee later presents different facts or a reporting question tied to Form 1042-S.

If you keep W-8ECI narrow, fact-based, and reviewable, you can reduce both over-withholding and under-documented exceptions. That is the outcome most likely to hold up under Internal Revenue Service scrutiny.

Frequently Asked Questions

What is Form W-8ECI, and how is it different from Form W-8BEN?

Form W-8ECI is used when a foreign person claims that U.S.-source income is effectively connected with a U.S. trade or business. Form W-8BEN is used to establish foreign status and, where applicable, claim treaty relief. The practical difference is ECI on W-8ECI versus foreign status and possible treaty relief on W-8BEN.

When can a foreign contractor’s income be treated as Effectively Connected Income?

Income can be treated as Effectively Connected Income when the foreign person is generally engaged in a U.S. trade or business during the tax year. For platform review, the file should show a real business-activity story, not just a preference for different withholding treatment. The W-8ECI posture also represents that the income will be included in the payee's gross income.

Does performing services in the U.S. automatically create a U.S. trade or business?

No. The IRS materials here say foreign persons generally are engaged in a U.S. trade or business when personal services are performed in the U.S., but the activities must also be considerable, continuous and regular. Thin or one-off U.S. connections should trigger review instead of auto-approval.

What should a platform verify before accepting a W-8ECI claim?

Verify that the payee claims to be the beneficial owner, that the income is includible in gross income, and that the form includes a U.S. TIN. Also confirm that the facts support the claimed U.S. business activity and that the form is complete and usable for your records. A missing U.S. TIN is a hard red flag when withholding relief is requested.

How does a W-8ECI decision affect withholding and Form 1042-S preparation?

If you are not a partnership, a qualifying W-8ECI generally means you do not need to withhold tax on ECI. Reporting is separate, because Form 1042-S can still be required even when no tax was withheld. Keep both the accepted form and the treatment decision in the file.

When should a platform escalate to specialist review instead of auto-approving intake?

Escalate when the ECI claim and the facts do not line up cleanly. Common triggers include a missing U.S. TIN, weak support for a U.S. trade or business, contradictory statements about where services were performed, or overlapping treaty and ECI positions. In those cases, pause approval and require specialist review.

Where do Form 8233 and tax treaty claims fit when facts overlap with ECI?

Form 8233 applies to nonresident alien individuals claiming exemption from withholding on compensation for personal services because of an income tax treaty. If the case is treaty-first rather than ECI-first, route eligible personal-services cases to a Form 8233 or treaty review lane. Do not force those cases into a W-8ECI path.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

IRS Form 1042-S for Platforms: How to Report US-Source Income Paid to Foreign Contractors

The core question is simple: is your entity acting as a withholding agent for payments to a foreign person, and if so, does that create a **Form 1042-S** duty? This guide helps you answer that question, document the support behind it, and escalate early before a weak assumption becomes a filing problem.

W-8ECI vs W-8BEN for Foreign Contractors With US Business Income

Treat **w-8eci vs w-8ben** as a classification decision first and a form-collection task second. For compliance, legal, finance, and risk owners, the real exposure is not just a missing document. It is putting a contractor, seller, or creator payout on the wrong document path and only discovering the withholding impact after money is already scheduled.

IRS Form 8233: When Foreign Contractors Claim Treaty Exemptions and What Platforms Must Verify

Form 8233 is used by nonresident alien individuals to claim exemption from withholding on compensation for personal services, but for platform operators the key exposure is often operational: scope decisions, review quality, recordkeeping, and escalation. When you pay nonresident individuals for U.S.-source personal services income, the real risk is often not whether a form exists, but whether your team can show why a claim was accepted.