Quick Answer

Assign FX ownership first, then harden execution controls before scaling any corridor. Pick a bank-led, PSP-led, or embedded model based on who can absorb stale-quote and return risk, and document that in your operating map. Require firm-quote expiry checks, store quote IDs and acceptance timestamps, and block payouts when required artifacts are missing. For higher-volatility routes, run separate rules for USD, CHF, and JPY instead of one global setting, and expand only after pilot gates for retries and reconciliation are passing.

Why FX Operations Are Moving Onto Platforms#

Before you start#

Treat Foreign Exchange (FX) as an early product and operations decision, not a setting you clean up after launch. Global standard-setters still describe cross-border payments through the same four frictions: high costs, low speed, limited access, and insufficient transparency. If your platform pays people or businesses across borders, those frictions show up in user pricing, payout timing, and operational handling.

- Reframe FX as architecture.

In practice, the shift toward platform-led FX means someone on your side has to make the hard calls earlier. The FX market is enormous, with BIS reporting $7.5 trillion in daily turnover in April 2022, and its structure has become more complex over the past three decades. That matters because quote logic, settlement paths, and reconciliation design now sit much closer to the product than many teams expect.

Check: if nobody on your side can clearly answer which team owns rate selection, quote acceptance rules, and payout exception handling, you are still treating FX like back-office cleanup. That is often where launch delays and opaque user outcomes begin.

- Identify whether this guide fits your operating model.

This guide is for founders, product leaders, finance owners, ops teams, and engineering leads running contractor payouts, creator payouts, marketplace disbursements, or embedded cross-border payments. Those teams are already pushing providers for local-currency payment and settlement support. Once you support that model, FX ownership is no longer abstract.

The tradeoff is simple. More control can improve transparency and user experience, but it also raises implementation and control demands. An IMF note published in October 2024 explicitly recognized that platforms can improve efficiency in payments and foreign exchange, including lower transaction costs and better liquidity. That still leaves you responsible for clean operating controls.

- Set decision goals before you compare providers.

Your goal here is practical: decide who should own FX, how quote risk should be controlled, and what you need to implement first so launch is audit-ready and able to scale. If you skip that order and start with vendor demos, you can end up comparing the wrong things. Teams often focus on headline rates while missing who owns stale quotes, how failures are handed off, and what evidence finance will need later.

Check: before you move on, write down three items in plain language: your proposed FX owner, the moment a rate becomes binding for the user or payee, and the minimum evidence you need to prove what happened when a payout is delayed, repriced, or returned. If those three are fuzzy, provider selection will be fuzzy too.

The rest of this guide moves from that first ownership decision into the controls you actually need to operate.

What changed in 2026 and why platform teams cannot treat FX as a back-office setting#

In 2026, FX moved quickly enough that product teams had to treat it as an operating input, not a treasury cleanup task.

Step 1. Use volatility signals as operating inputs, not market trivia. The broad signal is the US Dollar Index (DXY), which tracks USD against a currency basket. BIS analysis says FX volatility broadly tracked moves in DXY, and late March 2026 showed the pace: DXY touched 100.64 and was up 2.8% through March. If your team prices cross-border payments as if rates stay stable until someone checks later, you are already behind.

Step 2. Set corridor-specific rules instead of one hedge rule for all payouts. Safe-haven rotation does not move USD, CHF, and JPY the same way at the same time. Recent reporting showed USD outperforming other perceived safe assets, while JPY also reacted to Bank of Japan signaling, including intervention threats and the chance of a near-term rate hike if weakness continued. USD/JPY moving past the 160-per-dollar level is exactly the kind of move that breaks one-size-fits-all corridor logic. If you pay out in JPY, CHF, and USD, use separate quote, funding, and escalation rules for each corridor.

Step 3. Turn macro moves into hard product controls. The product impact is concrete: payout timing windows, quote-expiry risk, and margin leakage. ECB material is direct that funding tied to FX settlement may not occur in time, and IMF analysis notes that payment outages and settlement failures can raise FX transaction costs. Your checkpoint is simple: log the quote ID, acceptance timestamp, execution timestamp, applied rate, and any reprice event for every payout. The common failure mode is a firm quote accepted by the user but executed after the market moved or a funding window slipped, leaving you with a delayed payout or hidden loss.

Those risks lead straight to the next decision: who actually owns them in your operating model.

Choose your FX ownership model before you choose providers#

Choose the FX ownership model first. It determines liability, retry safety, reconciliation ownership, and margin exposure before provider feature comparisons matter.

Step 1#

Start with one question: who owns the outcome when an FX-backed payout fails?

In a bank-led model, control is typically split across treasury, bank processes, and correspondent banking rails, so product teams often have less direct control over rate logic and payout behavior. In a PSP-led model, launch is usually faster and payout tooling is packaged, but customer promises can still sit with your team while quote mechanics and execution sequencing sit with the provider. In an embedded platform-led model, you gain the most control and usually the most exposure.

If you operate as Merchant of Record (MoR), treat it as a liability decision, not a checkout setting. The MoR carries legal transaction responsibility, and in many marketplace setups the platform is the MoR.

| Model | Who owns rate logic | Who owns failures | Who owns reconciliation | Directional fit |

|---|---|---|---|---|

| Bank-led | Bank + internal treasury | Shared across bank execution and your customer commitments | Your finance team across bank records and internal ledger | Often workable for digital banks with established treasury operations |

| PSP-led | PSP-driven quote/conversion behavior | Shared: provider execution + your user-facing commitments and retry policy | Shared provider references + your internal transaction IDs | Often workable for fintech platforms prioritizing speed with thinner treasury capacity |

| Embedded platform-led | Platform-led, often aligned to MoR and internal orchestration | Platform owns stale-quote, routing, and connected-account loss exposure | Internal ledger first, enriched by provider references and payout-batch reporting | Often workable for multi-entity marketplaces needing unified controls |

Treat this mapping as directional, not universal.

Step 2#

Match the model to the risk you cannot absorb.

If you need strict payout orchestration, unified controls, and one investigation surface, a tighter embedded model (MoR + payout batches) is usually the stronger fit. If treasury capacity is thin, starting PSP-heavy is often the faster path. Either way, require transaction-level reconciliation fields that tie provider references and your internal references in the same payout flow.

Step 3#

Do not move forward if diligence leaves any of these unclear:

- Liability for stale quotes, repricing, or post-acceptance rate movement.

- Explicit API idempotency behavior for repeated POST requests (including idempotency-key handling and retry outcomes).

- An auditable handoff between card-network and closed-loop legs, including whether references persist across each leg.

The highest-risk incident is split ownership: the provider shows executed, your ledger shows pending, and no one can prove whether a retry duplicated execution or a stale quote was honored. In embedded setups, that can become direct platform loss exposure when connected account balances go negative, including documented reserve-transfer handling if a balance remains negative for 180 days.

Set quote and conversion rules that protect margin#

Protect margin by separating firm-quote promise flows from indicative-rate estimate flows, then enforcing expiry and reprice controls in execution.

Step 1#

Use firm quotes only when you are making a payout promise (locked currency or amount). Use indicative rates only in flexible-timing flows, and label them clearly in product and internal states.

If payout currency is locked at checkout, acceptance, or contract confirmation, require a firm quote with a visible expiry and a defined retry path. Stripe supports attaching an FX quote directly to a PaymentIntent, and extended quote windows can be set to 5 minutes, 1 hour, or 24 hours (maximum lock duration: 1 day).

If payout timing is flexible, do not treat indicative rates as executable. Airwallex distinguishes indicative rate information from a guaranteed rate period; use that same operating model and document when delayed conversion is allowed versus when you must stop and reprice.

- If payout currency is locked at checkout: require firm quote + expiry timestamp + stored quote ID + retry behavior.

- If payout timing is flexible: allow delayed conversion with indicative pricing only until execution is triggered.

- If user reapproval is required after a rate move: define that state in advance.

For each conversion-capable transaction, store quote_type, quote_id, expires_at, and whether the rate was firm or indicative.

Step 2#

Block stale quotes before execution. An expired quote ID should fail hard, trigger recalculation, and follow a clean re-quote decision path.

Stripe states that attaching an expired FX Quote to PaymentIntent or Transfer returns HTTP 400, and it can send fx_quote.expired when a quote becomes invalid due to expiration or significant rate drift.

Keep controls explicit: reject expired quote IDs, request a fresh quote before execution, and log each repricing event for finance review (old quote ID, new quote ID, reason, and operator/service action).

Step 3#

Define corridor-level controls for USD, CHF, and JPY before volatility spikes. They are commonly treated as safe-haven currencies, but you should not run them through identical execution rules.

| Corridor focus | What to monitor | What to do |

|---|---|---|

| USD payouts | Safe-haven demand and DXY strength. Reporting as of March 31, 2026 referenced DXY at 100.61 and +2.9% through March. | Shorten quote-lock use for auto-convert flows, review repricing volume daily, and escalate when delayed conversions breach approved tolerance bands. |

| CHF payouts | Safe-haven demand during risk-off periods. | Keep auto-convert only while spread behavior stays within finance-approved bounds; otherwise pause auto-convert and require manual approval for larger or time-sensitive batches. |

| JPY payouts | Intervention-sensitive conditions around 160 JPY/USD, plus BOJ policy context including the move to around 0.75% in December 2025. | Pause auto-convert in stress windows, require manual approval for high-value JPY batches, and recheck quotes immediately before execution. |

Codify these corridor rules before repricing volume rises. When timing pressure and volatility pressure happen together, prefer shorter quote validity and faster escalation.

Build compliance gates into the payout path from day one#

Build compliance into the payout path, not after approval. A practical default is to gate onboarding first, then VAT status where relevant, then tax-document readiness, and only then payout eligibility and release, with finance/legal adjusting for jurisdiction-specific requirements.

| Gate | When | Evidence |

|---|---|---|

| Onboarding checks | Before payout details can be created or activated | Entity type, beneficial-owner status where relevant, AML result, and decision time for each check |

| VAT validation | Before VAT-sensitive invoicing or intra-EU activation | VAT number checked, country, result, and check time |

| Tax-document checkpoints | Before the first payable event; block release when required documentation is missing | Tax classification at onboarding and document completeness before the first payable event |

| Reporting dependencies | With finance and legal before release | One traceable evidence record with decision timestamp, policy result, reviewer or escalation path, and masked artifact references |

Step 1 Gate onboarding before payout setup. Run KYB/KYC intake and AML controls before payout details can be created or activated. For legal entities in covered contexts, beneficial-owner checks belong at new-account opening under 31 CFR 1010.230.

Keep payout records blocked until identity checks are complete. Before a bank account or wallet is payout-ready, the record should show entity type, beneficial-owner status where relevant, AML result, and decision time for each check.

Step 2 Run VAT validation before VAT-sensitive invoicing or intra-EU activation. If you support intra-EU trade, validate VAT registration through VIES. Because VIES is a search engine, store the VAT number checked, country, result, and check time, then recheck on your internal cadence.

Do not let cross-border invoice treatment depend on an off-platform email trail.

Step 3 Attach tax-document checkpoints to payout lifecycle events. Use Form W-9 when a payee must provide a correct TIN for IRS information-return workflows. Use Form W-8BEN for foreign beneficial owners when requested by the withholding agent or payer. Use Form 8233 when an eligible nonresident alien individual claims treaty-based withholding exemption on personal-services compensation.

Collect tax classification at onboarding, verify document completeness before the first payable event, and block release when required documentation is missing.

Step 4 Track reporting dependencies with finance and legal before release. FATCA can create reporting duties for certain foreign financial institutions and certain non-financial foreign entities regarding U.S. account holders' assets. FBAR (FinCEN Form 114) and Form 8938 are separate obligations; one does not replace the other.

For covered U.S. persons, FBAR uses an aggregate foreign account value trigger above $10,000 during the calendar year. IRS comparison guidance shows Form 8938 thresholds such as more than $50,000 on the last day of the tax year or more than $75,000 at any time during the year for unmarried individuals living in the U.S. Form 1099-NEC is used to report nonemployee compensation.

For each gate, keep one traceable evidence record with decision timestamp, policy result, reviewer/escalation path when manual handling occurs, and masked artifact references.

Related: IRS Form 8233: When Foreign Contractors Claim Treaty Exemptions and What Platforms Must Verify.

Design your ledger and reconciliation evidence pack for audits and incident response#

Treat your ledger as the primary source of truth, with a traceable chain from quote acceptance to final settlement or return.

Step 1 Post each payout lifecycle change as a separate journal event. Record quote acceptance, conversion, payout creation, payout attempt, webhook update, reversal, and manual adjustment as distinct events tied to one internal transaction ID. Store provider reference IDs alongside internal IDs, since reconciliation and settlement reports commonly use provider-side identifiers.

From a single payout record, you should be able to see a full status timeline (for example: pending, paid out, held, returned, reversed). Do not collapse asynchronous updates into one mutable status field, or you lose the timeline needed when webhook events arrive late or are delivered more than once.

Step 2 Keep a minimum reconciliation pack that finance and ops can both use. Include internal transaction IDs, provider reference IDs, payout status history, fee detail, applicable exchange-rate fields, internal FX spread attribution, and exception logs. Where available, store ledger-like provider records (such as balance transaction IDs with fee, net, and exchange-rate fields), not just gross payout amounts.

Use both transaction-level and batch-level evidence: transaction-level views support per-transaction cost and reconciliation, while batch-level views validate credits, debits, and counts at the settlement batch level. This prevents "batch looks right" false confidence when an underlying payment attempt is still pending or later returned.

Step 3 Unify Virtual Accounts and Payout Batches into one investigation view. Ops should be able to see the inbound credit, batch assignment, payment attempts in that batch, and latest provider event in one place to resolve credited, held, or returned funds quickly.

Account for provider timing in that same view. Some reconciliation reports are generated after confirmation windows, often around 2 business days after capture, and some methods can take longer.

Step 4 Show that breaks, unmatched items, and retries are controlled. Run a daily break report against provider settlement/reconciliation outputs and route unmatched items to a visible queue. Treat reconciliation exceptions as explicit mismatches where auto-reconciliation cannot match an internal transaction to a provider or statement line.

Keep replay-safe retry evidence for asynchronous flows: processed webhook event IDs, deduplication outcomes, idempotency keys, request fingerprints, first responses, and retry timestamps. If you cannot prove retries are idempotent within the provider reuse window, you have an incident risk.

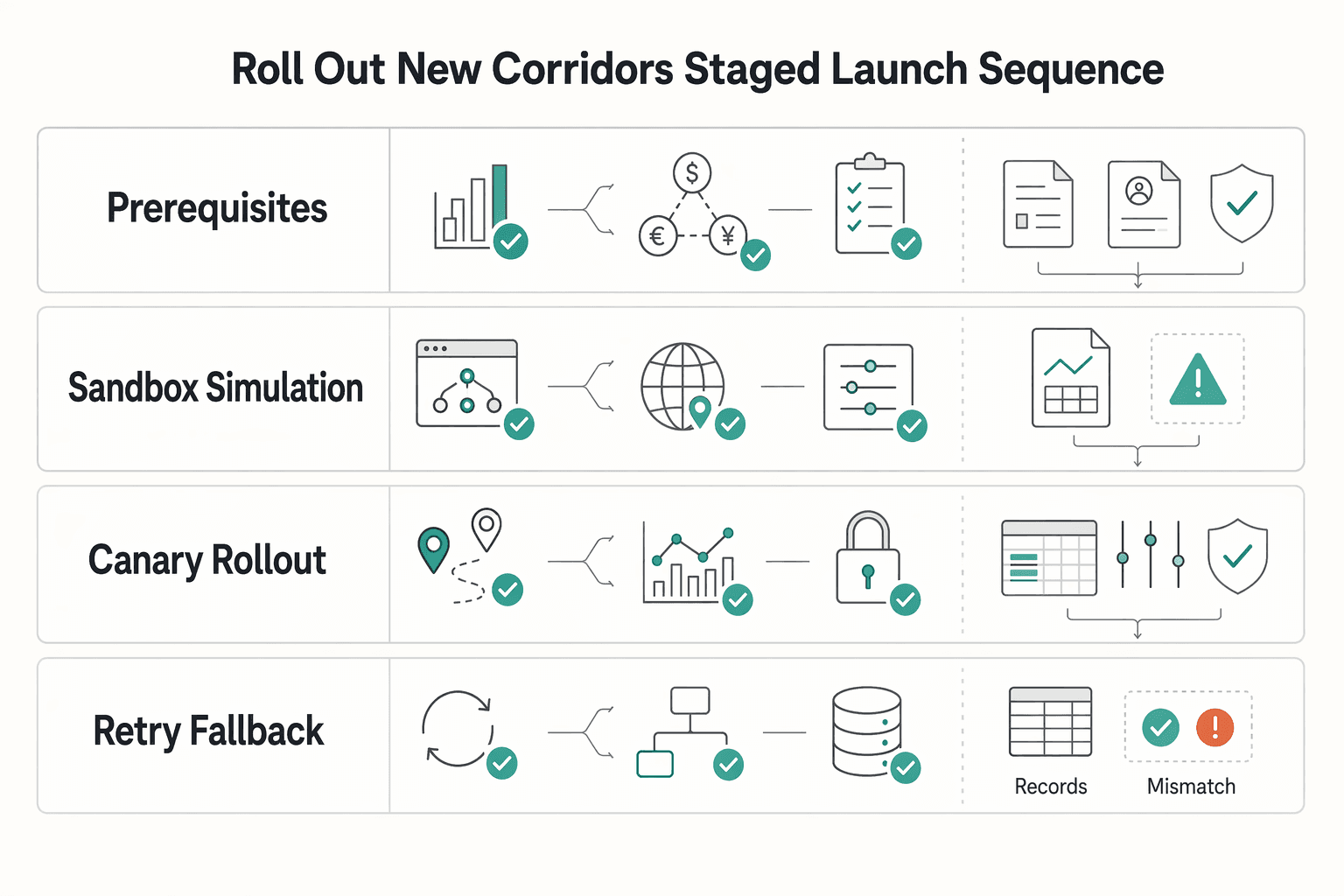

Roll out new corridors with a staged launch sequence#

Launch new corridors in stages, and require each stage to pass clear gates before you widen exposure.

| Stage | When | Checks |

|---|---|---|

| Prerequisites | Before the corridor is marked build-ready | Validate demand, confirm the payment method support matrix, and confirm compliance and tax readiness |

| Sandbox simulation | Before any live traffic | Test quote and payout creation, webhook delivery and retries, reconciliation events, and exception handling; verify event types, payload shape, signature checks, duplicate delivery handling, and ordering assumptions |

| Canary rollout | Internal pilot, then a limited live cohort, then broader release by risk tier | Set go/no-go gates for quote rejection rate, payout success rate, reconciliation lag, and unresolved compliance exceptions |

| Retry and fallback | For multi-PSP or multi-route setups and for each failed payout | Define in-transaction reroute versus later retry, test both behaviors, and record the original route, response code, retry decision, idempotency key, and whether fallback was permitted for that method |

Step 1 Confirm prerequisites before you mark the corridor build-ready. Validate demand, then verify the payment method support matrix so country, currency, and payout method are supported together. Also confirm compliance and tax readiness: KYC/KYB requirements, AML procedures that include beneficial-owner verification for legal entities where applicable, and required tax forms (such as W-8BEN when relevant) before payment.

Step 2 Run end-to-end simulation in sandbox before any live traffic. Use sandbox to test quote and payout creation, webhook delivery and retries, reconciliation events, and exception handling, not just API connectivity. Treat webhook contract testing as a launch gate by verifying event types, payload shape, signature checks, duplicate delivery handling, and ordering assumptions. Include delayed and repeated webhooks in tests, because redelivery can continue for up to three days in live mode.

Step 3 Use a canary-style production rollout: internal pilot, then a limited live cohort, then broader release by risk tier. Keep the first live cohort small enough for manual ops review, but real enough to surface corridor-specific failure patterns. Define go/no-go gates in advance for quote rejection rate, payout success rate, reconciliation lag, and unresolved compliance exceptions, and hold expansion if those gates are not met.

Step 4 Make retry and fallback routing explicit and testable. If you run multi-PSP or multi-route setups, define what supports in-transaction reroute versus later retry, and test both behaviors. For each failed payout, record the original route, response code, retry decision, idempotency key, and whether fallback was permitted for that method. If reroute is not explicitly supported and testable for a corridor or method, treat it as single-path and launch with tighter exposure.

Common failure modes in cross-border FX and how to recover fast#

When cross-border FX breaks, the fastest recovery pattern is consistent: block expired quotes, isolate async mismatches in investigation, and hold payouts until compliance artifacts are complete.

| Failure mode | Action | Evidence |

|---|---|---|

| Expired firm quotes | Block conversion and require explicit re-quote acceptance before proceeding | Quote ID, valid_to_at, server submit time, and re-quote acceptance |

| Async status mismatches | Treat as an investigation state, reconcile by provider reference first, and replay undelivered events chronologically with idempotent handling | Provider payload ID, internal transaction ID, and matched reference |

| Late compliance holds | Freeze payout release until the missing artifact is collected and checks pass again | The exact missing document attached to the case and rerun policy checks before release |

1) Expired firm quotes A locked quote is valid only for its stated window, and valid_to_at is the control point. If that window has passed (for example 1 minute, 15 minutes, 30 minutes, 1 hour, 4 hours, 8 hours, or 24 hours), block conversion and require explicit re-quote acceptance before proceeding. Log quote ID, valid_to_at, server submit time, and re-quote acceptance so finance can separate market movement from stale-quote execution issues.

2) Async status mismatches Treat payout status mismatches as an investigation state, not a blind retry signal. Reconcile by provider reference first, then replay undelivered events chronologically with idempotent handling, and return success for already-processed events to stop duplicate retries. Keep the provider payload ID, internal transaction ID, and matched reference in the case file, and plan for automatic retries that can continue for up to three days.

3) Late compliance holds If verification or documentation checks fail late in the flow, freeze payout release until the missing artifact is collected and checks pass again. Request the exact missing document (such as W-8BEN or W-9), attach it to the case, and rerun policy checks before release. Missing W-8BEN when requested can lead to 30% withholding, and W-9 collection requires written TIN certification; treaty-exemption cases should follow a dedicated Form 8233 path.

Related reading: Merchant of Record for Platforms and the Ownership Decisions That Matter.

Conclusion and copy/paste launch checklist#

Treat this as your go or no-go gate. If any item below is fuzzy, especially ownership, quote expiry, or document blocking, you are not ready to launch cross-border payouts at scale.

- Lock the FX ownership and liability map.

Write down who is principal, who is agent, who sets the rate logic, and who absorbs financial risk when a conversion, payout, or settlement step goes wrong. This must cover each PSP, bank, and your own platform services, because role boundaries are contract-specific and a provider can state plainly that it acts as principal and not as your agent or fiduciary. If you run a Merchant of Record structure, confirm which entity actually absorbs transaction risk before you expose a user-facing converted amount. Verification: one signed ownership matrix tied to the live provider contracts, settlement terms, and internal service owners. Red flag: if finance, legal, and engineering give different answers about who owns stale-quote losses or returned funds, stop.

- Enforce quote controls before money moves.

Your production path should reject expired firm quotes, require a fresh quote on retry, and log every repricing event with quote ID, acceptance timestamp, and execution reference. Indicative rates can support previews, but final conversion should point to a firm quote and an auditable acceptance event. Silent repricing is the failure mode to avoid, because it turns margin loss into an argument instead of a traceable incident. Verification: finance can trace any executed conversion from internal transaction ID to quote ID, expiry check, provider reference, and any re-quote that happened before payout.

- Make compliance and tax gates explicit and blocking.

Your exact sequence can vary by jurisdiction and provider, but applicable KYC/KYB/AML checks, VAT validation, and tax-document checks should each have a recorded pass, fail, or escalation result before funds move. For EU cross-border trade, VAT validation can be done through the VIES check. For tax documents, collect Form W-9 when you need a correct TIN for IRS information returns, request Form W-8BEN when foreign-status documentation is required by the withholding agent or payer, and use IRS Form 8233 only for eligible nonresident personal-services treaty claims. Keep FATCA and Form 8938 dependencies on your finance and legal review list where applicable, rather than assuming they follow the same trigger as W-8 or W-9. Verification: each gate stores a decision timestamp, masked artifact reference, and reviewer or escalation path.

- Prove operational readiness with audit trails and retry safety.

The ledger should be immutable and complete enough to reconstruct quote acceptance, conversion, payout attempt, webhook update, and reversal without stitching together guesses from multiple tools. Your reconciliation pack should include provider reference IDs, internal transaction IDs, payout status history, fee attribution, FX spread attribution, and exception logs. Confirm idempotent retries for API calls and async event handling, because some providers can resend undelivered events for up to three days. Verification: run one failed payout and one webhook redelivery test in staging, then confirm no duplicate side effects, no missing journal events, and a named escalation path for unresolved breaks.

Frequently Asked Questions

What does “platforms reshaping Foreign Exchange” actually mean for marketplaces and embedded payments?

It means FX is no longer only a treasury workflow in many platform setups. Teams now decide when rates are shown, when money is converted, how quote risk is handled, and how fees and spread are exposed to users. That matters because newer cross-border platforms compete on speed, fewer fees, and transparency, so FX choices can affect both margin and trust.

When should we use indicative rates versus firm FX quotes?

Use indicative rates for estimation, routing, and user previews only. They are non-tradable reference prices, so they should never drive final conversion logic or a guaranteed payout amount. Use a tradable or detailed quote when you are actually converting funds or locking a user-visible amount.

How do we reduce FX slippage in cross-border payments without slowing payouts too much?

Convert as close as possible to the real execution point, not long before it. If payout timing is flexible, show an estimate first and request a firm quote only when the transfer is ready. If the amount is locked at checkout, get the executable quote then and treat expiry as a hard stop. Finance should be able to trace every executed conversion back to a quote ID, acceptance time, and repricing event if one occurred.

What controls prevent stale-quote losses in production systems?

Start with a hard reject on expired quote IDs and check the expiry field before every conversion attempt. Some providers can invalidate unused quotes within 30 minutes, so your service should force a fresh quote and explicit re-acceptance instead of auto-converting at a new rate. The failure mode to avoid is silent repricing, where ops sees a completed payout but cannot prove whether spread loss came from market movement or a stale-quote path.

When should we pass FX risk to users versus absorbing it in platform pricing?

There is no single universal rule. The choice depends on the promise you make and your product or contract terms. If you advertise or contract around an exact converted amount, many teams treat that as a platform commitment and manage that risk. If users approve a payout at the prevailing rate later in the flow, more risk can be passed through, but only if the rate basis and timing are clearly disclosed.

What should finance teams audit before enabling a new payout corridor?

Audit one full evidence pack before launch, not after the first incident. That pack should include the quote type used, expiry handling, provider reference IDs, internal transaction IDs, fee and FX spread attribution, payout status history, and any exception logs. If a corridor cannot produce that trail on demand, it is not operationally ready.

How should geopolitical volatility change payout policy for USD, CHF, and JPY corridors?

Treat uncertainty as a reason to shorten the gap between quote and execution and to review auto-convert behavior more aggressively. CHF often attracts demand in high uncertainty, JPY can appreciate in risk-off periods, and USD strength can create cross-border spillovers that change corridor economics quickly. In practice, that means more frequent re-quoting, tighter manual review for delayed payouts, and a willingness to pause automatic conversion when repricing starts to repeat.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 1 external source outside the trusted-domain allowlist.

- bis.org/publ/work1094.htmtrusted

- bis.org/publ/qtrpdf/r_qt2212f.htmtrusted

- ecfr.gov/current/title-31/subtitle-B/chapter-X/part-1...trusted

- imf.org/-/media/Files/Research/imf-and-g20/2024/g20-...trusted

- imf.org/-/media/files/publications/gfsr/2025/october...trusted

- irs.gov/forms-pubs/about-form-w-9trusted

- irs.gov/forms-pubs/about-form-w-8-bentrusted

- fsb.org/work-of-the-fsb/financial-innovation-and-str...external

Educational content only. Not legal, tax, or financial advice.

Related Posts

FATCA Compliance for Marketplace Platforms: Identifying and Reporting Foreign Account Holders

For marketplace teams handling cross-border payouts, FATCA work is mostly a control-design problem. You need to decide what to implement first, what evidence to keep, and what to escalate before a payout creates avoidable reporting or withholding risk. The practical question is not whether FATCA exists, but which controls actually reduce reporting errors and potential 30% withholding outcomes.

IRS Form 8233: When Foreign Contractors Claim Treaty Exemptions and What Platforms Must Verify

Form 8233 is used by nonresident alien individuals to claim exemption from withholding on compensation for personal services, but for platform operators the key exposure is often operational: scope decisions, review quality, recordkeeping, and escalation. When you pay nonresident individuals for U.S.-source personal services income, the real risk is often not whether a form exists, but whether your team can show why a claim was accepted.

EDI for Platforms Automating Invoice Exchange With Large Buyers

If your platform needs to invoice enterprise buyers through EDI, the real decision is operational: which delivery model will let you exchange the required document set with the fewest surprises in production. Electronic Data Interchange (EDI) is a standards-based way to transmit business documents such as invoices and purchase orders between organizations, and it is primarily used in B2B exchange.