Quick Answer

Form 8233 lets a nonresident alien individual claim a treaty exemption from withholding on U.S.-source compensation for personal services, and platforms should accept it only after verifying the payee, income type, and treaty basis. It applies per withholding agent and per income type, is not interchangeable with Form W-8BEN for personal-services income, and for independent personal services the default baseline is 30% withholding until a valid exemption is established.

Why this article matters for platform operators#

Form 8233 is used by nonresident alien individuals to claim exemption from withholding on compensation for personal services, but for platform operators the key exposure is often operational: scope decisions, review quality, recordkeeping, and escalation. When you pay nonresident individuals for U.S.-source personal services income, the real risk is often not whether a form exists, but whether your team can show why a claim was accepted.

If you work in compliance, legal, finance, or risk, this issue sits at the seam between tax rules and payout operations. Weak handling can lead to underwithholding, inconsistent treatment, and evidence gaps when decisions are challenged.

-

Start with scope, not paperwork. Form 8233 is for nonresident alien individuals claiming exemption from withholding on compensation for personal services. IRS materials tie it to specific categories, including independent personal services, dependent personal services, and certain personal services income paired with scholarship or fellowship income from the same withholding agent. For independent personal services, the Form 8233 instructions point to a general section 1441 baseline of 30% withholding before a valid exemption applies. If coverage is unclear, route the case to manual review.

-

Map ownership before controls. In the Form 8233 process, the withholding agent has explicit duties: review the form, sign acceptance, and forward it to the IRS within 5 days of acceptance. The instructions also say to keep a copy for records, and claimants must submit Form 8233 to each withholding agent paying covered amounts. Collecting forms is not the same as owning the acceptance duties, so define who the withholding agent is in each payout model and who performs each step.

-

Use current treaty references, not memory. IRS instructions state the claimant must know the treaty terms to complete Form 8233 properly. Publication 901 explains whether a treaty offers a reduced rate or a full exemption, and IRS sourcing rules state a nonresident alien generally is subject to U.S. income tax only on U.S.-sourced income. A defensible review record should capture the form copy, the U.S.-source rationale, the treaty basis consulted, the acceptance date, and the approver.

That is why we use this guide. The eight checkpoints that follow are not IRS-mandated. They give you a practical way to keep verification consistent at scale without turning every case into a legal memo.

If you want more detail, read IRS Form 1042-S for Platform Operators: How to Report and Withhold on Foreign Contractor Payments.

How to select the right verification depth for your platform#

In practice, we recommend a two-layer approach: give every claim the same minimum review floor, then route higher-risk cases to a stricter lane. IRS rules set the baseline. Your policy should decide when review happens before payout, when sampling is acceptable, and when escalation is required.

- Mandatory floor for every claim

Confirm the payee is a nonresident alien individual, the payment is compensation for personal services, and the treaty claim is submitted on Form 8233 rather than Form W-8BEN for personal-services income. Review at the required granularity: for each withholding agent and for each type of income. Do not apply a treaty rate if required documentation is missing or if you have reason to know the claim is ineligible. For independent personal services, default exposure remains the section 1441 30% withholding baseline until a valid exemption is established.

- Light-touch lane for clean, low-impact cases

Use this lane only when your documentation is complete and the treaty position is straightforward. A practical internal standard is that your reviewer can match country and income type using Publication 901 without unresolved questions and document the acceptance date, reviewer, and basis used. Keep this lane auditable. Post-review sampling is reasonable only when the file already supports a clear reconstruction of why your team accepted the claim. IRS describes Publication 901 as quick reference, not complete treaty guidance.

- Strict lane for ambiguity, scale, or reporting impact

We recommend pre-payout review when treaty eligibility is unclear, TIN-related eligibility is incomplete, or the reviewer cannot support the position beyond a quick Publication 901 check. You can also route recurring edge cases or higher-volume cohorts here as a policy control. This lane adds friction, but it lowers the risk of granting exemptions you cannot defend later. Preserve a full decision trail for withholding and Form 1042-S reporting, including cases where compensation is treaty-exempt.

Related: How to Get a Refund of Over-Withheld US Taxes as a Foreigner.

Quick comparison table of the eight Form 8233 verification checkpoints#

Use IRS requirements as the control floor, then layer your platform routing policy on top. This table separates IRS-driven obligations from internal operating choices so teams do not confuse withholding review with payout operations. The checkpoint count, table columns, and decision labels are operating choices, not IRS-prescribed requirements.

A practical guardrail: "hold pending evidence" should usually mean hold the treaty exemption decision, not automatically hold payout. Whether payout is paused is an internal policy choice.

| Checkpoint | Primary owner | Required evidence | Common failure mode | Escalation trigger | Decision for nonresident alien individual claim | IRS reference or policy basis |

|---|---|---|---|---|---|---|

| 1. Payment fits Form 8233 scope | Tax/compliance, tax-only | Form 8233 and payment classification showing compensation for personal services (independent services, dependent services, or covered personal-services plus scholarship/fellowship income from the same withholding agent). | Form 8233 used for income that should be handled on Form W-8BEN because it is not compensation for personal services. | Income type is unclear, mixed, or inconsistent with contract and payout coding. | Reject if clearly out of scope; escalate if classification is unclear. | IRS-driven. Form 8233 is not interchangeable with W-8BEN for all treaty scenarios. |

| 2. Claim is filed at the right granularity | Tax/compliance, tax-only | Separate Form 8233 for each tax year, withholding agent, and type of income. | One accepted form reused across entities, years, or income types. | New tax year, new payor entity, or new income type appears without a new form. | Hold pending evidence until a separate form is received; reject if the payee will not resubmit correctly. | IRS-driven from Instructions for Form 8233. |

| 3. Treaty basis is supportable with current IRS materials | Tax/compliance, tax-only | Completed Form 8233, treaty-article rationale, current Instructions for Form 8233, and Publication 901 only as quick reference. | Reviewer relies on Publication 901 alone or stale internal notes without confirming treaty terms. | Publication 901 does not resolve the issue, or reviewer cannot explain article basis. | Accept only when supportable; otherwise escalate. | IRS-driven floor with specialist judgment. |

| 4. Identity and form integrity are complete | Shared: tax/compliance plus onboarding or payments ops | Signed, complete Form 8233 and required claimant details; required treaty statements for students, trainees, teachers, or researchers when applicable. | Missing signatures, incomplete fields, or missing required statements. | Form details do not match platform records, or required attachments are missing. | Hold pending evidence for curable gaps; reject if materially incomplete. | Mixed: IRS form-completion requirements plus internal identity-control policy. |

| 5. Acceptance and IRS forwarding are controlled | Tax/compliance, tax-only | Acceptance date, withholding-agent acceptance/signature record, and proof accepted form was forwarded to IRS within 5 days. | Intake recorded but no acceptance record or forwarding proof or timing. | Accepted form cannot be tied to reviewer, date, and forwarding evidence. | Escalate if acceptance occurred without evidence; hold pending evidence before acceptance if trail is incomplete. | IRS-driven on review, acceptance, and forwarding timeline. |

| 6. Tax decision is kept separate from payout release | Shared: tax/compliance plus payments operations | Documented rule for payout handling while unresolved treaty claims are treated as non-exempt for withholding purposes, with owner and override path. | Ops treats unresolved Form 8233 review as automatic payout block, or tax approves exemption without ops alignment. | Ownership conflict between tax and payments, or high-value payout needs manual exception. | Accept or hold tax treatment separately from payout status. | Internal policy choice, not an IRS mandate. |

| 7. Evidence pack and revalidation controls exist | Tax/compliance, tax-only | Form 8233 copy, reviewer notes, references used, decision log, and version tracking against current IRS materials, including your current Instructions baseline such as 12/2025. | Team cannot reconstruct why claim was accepted, or relies on outdated materials after IRS updates. | IRS materials change, contractor facts change, or repeated exceptions in one treaty cohort. | Accept only when reconstructible; otherwise escalate or hold pending evidence. | Mostly internal policy layered on IRS requirements. |

| 8. Outcome is tied to Form 1042-S reporting | Shared: tax/compliance plus finance/reporting | Withholding decision mapped to Form 1042-S logic, including that reporting may still be required even with treaty-exempt withholding and that a chapter 3 exemption code is required when withholding is below 30%. | No withholding taken, so finance assumes no Form 1042-S filing is required. | Decision log and reporting extract do not reconcile before filing. | Escalate if reporting treatment is unclear; accept only when reporting path is mapped. | IRS-driven: treaty-exempt compensation can still be reportable on Form 1042 and Form 1042-S. |

The rows most dependent on current IRS references are 1, 2, 3, 5, and 8. Rows 4, 6, and 7 are where platform policy turns those rules into operating controls through ownership, evidence discipline, and revalidation. With that division clear, start where most mistakes start: scope.

For a step-by-step walkthrough, see Form 3520 Playbook: A 3-Step Framework for Foreign Trust Transactions and Foreign Gift Reporting.

Checkpoint 1 confirm the payment can use Form 8233#

This is a triage gate, not a paperwork check. Before you do any treaty analysis, decide whether Form 8233 is even the right intake path. If the payment is not compensation for personal services by a nonresident alien individual, stop and reroute before making a withholding decision.

The IRS frames Form 8233 as the exemption form for compensation for independent personal services and certain dependent personal services. That makes this a useful first pass when your queue includes mixed payment types.

What to verify first#

Use the current Instructions for Form 8233 as your baseline, for example 12/2025, and confirm:

- the claimant is an individual claiming as a nonresident alien, not an entity

- the payment is compensation for personal services, not another income type

- the claim is being given to the withholding agent for exemption from withholding on that compensation

Cross-check the form against the payout description and contract coding. If records indicate non-service income and the claimant is only claiming foreign status or treaty benefits, use Form W-8BEN instead of Form 8233.

Why this gate matters and where it fails#

This checkpoint helps avoid treating every treaty claim as a Form 8233 case. For independent personal services, the instructions cite a default 30% withholding rule under section 1441 unless a treaty exemption applies. For dependent personal services, withholding can apply at 30% or graduated rates, so correct classification comes first.

Passing this gate does not establish treaty entitlement. The IRS also states that the claimant must know the treaty terms to complete Form 8233 properly. If compensation type is unclear, mixed, or inconsistent across the form, contract, and payout coding, pause and resolve the mismatch before deciding withholding.

You might also find this useful: Form 8233 for Foreign Individuals With U.S. Scholarship or Fellowship Income.

Checkpoint 2 validate treaty basis with current IRS materials#

A favorable Publication 901 entry is not enough on its own. Use current IRS materials in sequence, then document whether the claim is supportable on the actual facts.

Run the same four-part check every time so decisions stay consistent and escalation is defensible:

- Publication 519: confirm status first

Verify the individual is still treated as a nonresident alien. If status is wrong, the treaty analysis may be wrong even when the article citation looks correct.

- Publication 901: use as a quick map only

Use Publication 901 to locate a likely treaty article, rate, or exemption category. Treat it as quick reference, not final authority.

- Treaty text and technical explanation: do the real interpretation

The Instructions for Form 8233 require knowing the treaty terms. This is where limiting conditions appear, including office or fixed-base issues that can block exemption unless the treaty provides otherwise.

- Instructions for Form 8233: verify operational controls

Use the current instructions (Rev. December 2025) and related IRS process guidance to confirm requirements: a separate form is required for each withholding agent and each income type; if accepted, the withholding agent must review the form, sign acceptance, and forward it to the IRS within 5 days; after proper mailing, wait at least 10 days before applying the exemption.

The common failure mode is stopping at the summary source. A reviewer sees a favorable Publication 901 entry, skips treaty text review, and misses a condition that changes the result.

Keep the evidence pack simple and controlled: treaty country, claimed article, IRS materials checked, version date used, and reason for accept, reject, or escalate. As of this writing, IRS review dates shown are 23-Jan-2026 for Form 8233, 30-Mar-2026 for Publication 901, and 27-Mar-2026 for Publication 519.

This work also feeds reporting. Treaty-exempt compensation still appears on Form 1042-S even when it is fully exempt under a treaty.

Checkpoint 3 verify identity and foreign tax documentation integrity#

Do not approve a treaty claim on legal theory alone. Accept the form only when identity fields, residence details, and supporting tax documentation line up with the specific payer and income type.

Run this checkpoint in order and stop at the first hard mismatch:

- Match the person to the Form 8233 record

Confirm the core identity fields on the form: U.S. taxpayer identification number, foreign tax identification number if any, and permanent residence address. The withholding agent must review, sign acceptance, and forward an accepted form to the IRS within 5 days, so this is an acceptance decision tied to a specific individual, not just form intake.

- Treat permanent residence as a validation field, not a mailing field

The Form 8233 instructions do not allow a financial institution address, a post office box, or an address used only for mailing as permanent residence. If that appears, hold and correct it before acceptance.

- Use the correct form for the income type

Do not substitute Form W-8BEN for personal-services treaty claims. W-8BEN is for income not earned from personal services, while personal-services claims belong on Form 8233. For compensatory scholarship or fellowship tied to personal services, Form 8233 is also required instead of W-8BEN. If an ITIN is needed, Form W-7 may be relevant, but not every accepted 8233 case requires it.

- Validate filing granularity and apply reason-to-know escalation

Form 8233 applies for each withholding agent and for each type of income. If the setup involves different legal payors or multiple income streams, verify that the form matches that exact structure. If eligibility cannot be readily determined, or you otherwise have reason to know the reduced-withholding claim may be wrong, escalate before signature.

The red flags are usually predictable: W-8BEN used for contractor services, a mailing-only address entered as permanent residence, one form reused across multiple withholding agents, or identity fields that do not match the payee record. When one appears, hold the exemption and resolve it before you start treaty-rate withholding, with at least 10 days between submission and treaty-rate withholding.

We covered this in detail in our guide to the Foreign Tax Credit (Form 1116).

Checkpoint 4 separate tax withholding decisions from payout release#

If you collapse tax review and payout release into one decision, you create avoidable control problems. A pending Form 8233 review should generally stay on standard withholding treatment, not automatically freeze the payment.

Start by separating the statuses your teams control, then tie them back together only where policy requires it.

- Use two statuses for each payment record

Track a payout status and a withholding status separately. Let payout release follow your operational checks, while treaty-rate withholding changes only after the withholding agent accepts the Form 8233 claim. Until acceptance, do not treat treaty relief as effective.

- Apply withholding decisions at the right scope

Change withholding only when the form matches the specific withholding agent and the specific income type. Form 8233 is not a blanket approval across payors or income streams, and the general baseline for independent personal services is 30% withholding unless an exemption applies. If the claim is incorrect, or you have reason to know it is ineligible, do not apply the treaty rate and begin withholding immediately.

- Keep reporting ownership independent from payout release

Your reporting lane still needs the final tax outcome even when payouts were released. Form 1042-S is still required even when chapter 3 withholding is zero due to an exemption. Maintain an evidence set with the accepted or rejected form copy, reviewer notes, acceptance date, payout date, withholding rate applied, and confirmation that the accepted form was forwarded to the IRS within 5 days.

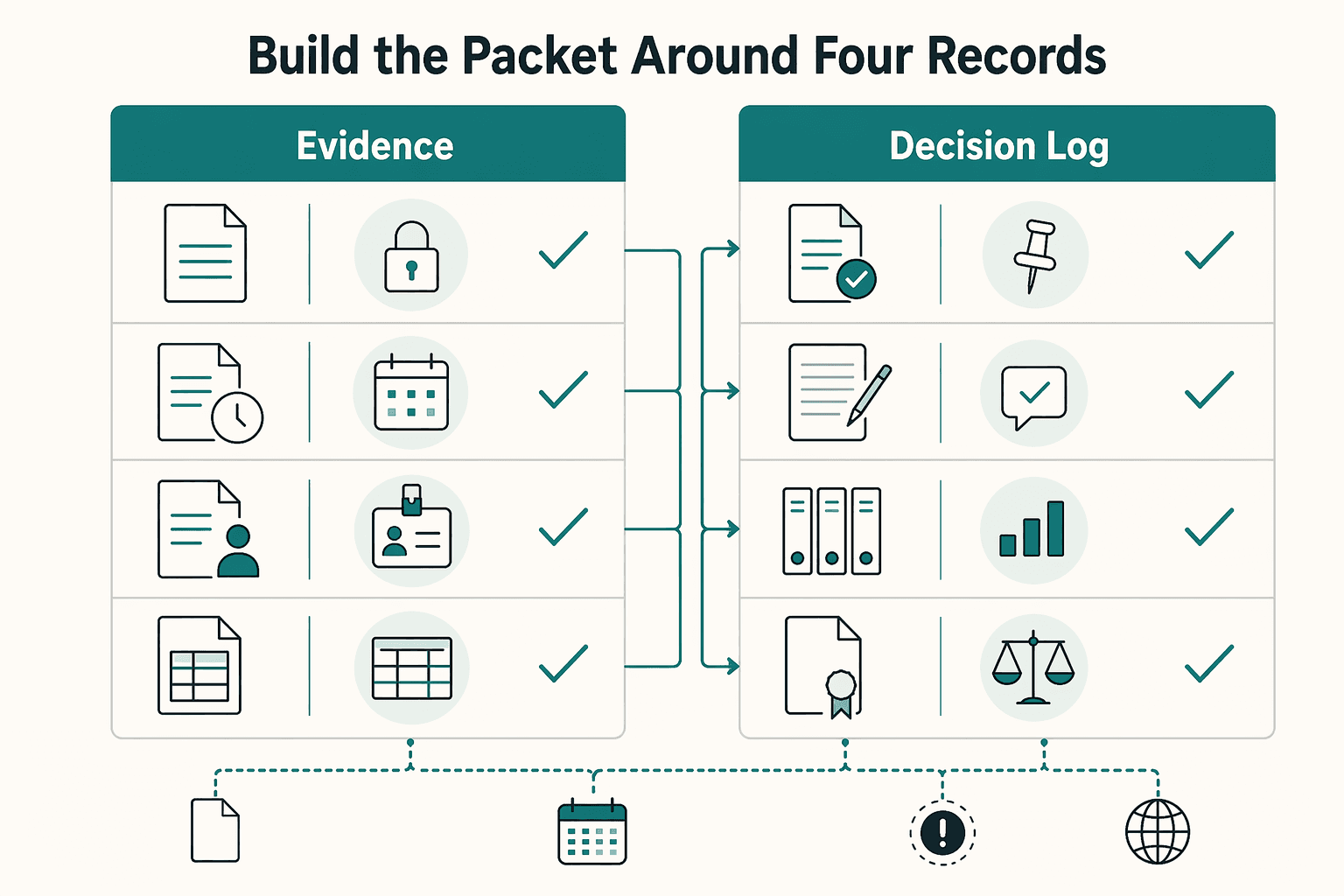

Checkpoint 5 create an audit evidence pack that survives scrutiny#

If you cannot show exactly why a Form 8233 claim was accepted or rejected, or how that result flowed into Form 1042-S, the case is not audit-ready.

Build the packet around four records#

- Claim record

Store the exact Form 8233 reviewed, intake timestamp, contractor identifier, payment identifier, and the income type in scope. Make clear that this is a decision for a specific withholding-agent and payment context, not a blanket contractor setting.

- Authority record

Keep reviewer notes plus the IRS materials used at decision time. Date the source set so the file shows which rules were in effect at the time, including the Belarus treaty-change context (effective December 17, 2024 through December 31, 2026, unless ended earlier) where certain qualifying-interest treaty claims may not be accepted, and the Russia suspension context requiring statutory 30% withholding on or after August 16, 2024.

- Decision log

Preserve a timestamped sequence of review steps, reviewer identity, accept or reject outcome, withholding rate applied, and any later override or correction. The timeline should reconcile cleanly to payment and tax records.

- Reporting handoff record

Capture the fields needed for Forms 1042 and 1042-S reporting obligations. For 2025 Forms 1042-S, due March 15, 2026, e-file through IRIS or FIRE. For 2026 Forms 1042-S, due March 15, 2027, e-file through IRIS, available January 1, 2026. Prior-year Forms 1042-S and submissions by foreign filers continue through FIRE during transition.

Set internal redaction and retrieval rules#

The IRS materials here do not set a complete redaction standard or a required retrieval timeline, so define both in platform policy. Specify what stays restricted in full-copy records, what appears in audit copies, and a measurable retrieval SLA so compliance can produce a complete packet quickly.

What usually breaks first#

The first break point is consistency at scale: retention, naming, and retrieval across many contractors and review teams. If a reviewer cannot pull a complete packet and explain the decision path quickly, your evidence standard is still too loose.

Related reading: What UK Companies Should Enter in Foreign TIN on Form W-8BEN-E.

Checkpoint 6 set explicit accept reject escalate rules#

You need three hard lanes: accept only when the withholding-agent standard is met, reject when the file is wrong or incomplete, and escalate when treaty or status analysis is unclear. Anything softer usually turns into reviewer habit.

| Decision | Use when | Required checks | Key differentiator |

|---|---|---|---|

| Accept | The claim fits Form 8233 and treaty support is clear | Confirm the claimant is a nonresident alien individual, is the beneficial owner of the income, the income is compensation for personal services, treaty support is clear in current IRS materials, including Publication 901 and the Instructions for Form 8233, the withholding agent is prepared to accept the statement, and there is no actual knowledge or reason to know otherwise | This is the only lane that supports withholding-agent certification that an exemption is warranted |

| Reject | The claim is wrong-form, incomplete, or unsupported | Reject for non-personal-services income, the wrong-form scenario, missing required support, or facts inconsistent with the claim | Return a fixed required-doc or correction checklist, not free-text reviewer opinion |

| Escalate | The reviewer must interpret unclear treaty or status issues | Escalate when treaty article mapping is unclear, when Publication 519 is needed to determine resident versus nonresident status, or when available facts do not clearly support a treaty position | Escalation pauses first-line tax judgment until specialist review is complete |

1. Accept only when the withholding-agent standard is met#

Accept only when the reviewer can affirm that the exemption is warranted and has no actual knowledge or reason to know otherwise. In practice, that means confirming nonresident alien individual status, beneficial ownership, personal-services income, and supportable treaty treatment under current IRS materials.

Treat each approval as granular, not portable. The form is tied to tax year and withholding-agent context, so do not reuse last year's approval or another payer's approval as blanket evidence.

2. Reject quickly when the file is wrong or incomplete#

Reject immediately when the claim does not belong on Form 8233. If the claim is for foreign status or treaty benefits on income that is not compensation for personal services, route it to the Form W-8BEN path.

Also reject when required support is missing or is inconsistent with the claim. Use a standardized correction checklist and store it in the case file so the rejection basis is auditable.

3. Escalate when treaty text or status analysis is doing the work#

Escalate when the case depends on interpretation rather than straightforward rule application. If treaty mapping is unclear, or if resident versus nonresident status is uncertain under Publication 519, send it to tax or legal specialists for written disposition.

If your process includes mailing Form 8233 to the IRS, build in the instructions' 10-day waiting period after proper mailing before checking for IRS objections.

4. Recalibrate rules on a schedule#

Hard gates only stay useful if you recalibrate them. Sample reject and escalate outcomes against current references, including the 12/2025 Instructions revision marker and the 23-Jan-2026 Form 8233 page review date.

If teams are handling similar fact patterns differently, tighten the trigger language and update the checklists so decisions stay grounded in current IRS materials rather than reviewer habit.

When your accept/reject/escalate thresholds are set, document owner handoffs and evidence requirements in one operating playbook using Gruv docs.

Checkpoint 7 control version drift and revalidation timing#

Version drift is a real control problem. If you do not record the exact IRS materials behind each approval and revalidate when scope changes, teams will drift into old PDFs, stale treaty notes, or last year's logic.

1. Stamp the exact reference set used for each decision#

For each accepted Form 8233, store the exact references used at review time, not a generic note that guidance was checked. At minimum, capture the Instructions for Form 8233 revision (12/2025), the form revision those instructions pair with (September 2018), and any treaty or status references used in the decision, typically Publication 901 and Publication 519.

This gives you historical defensibility when decisions are reviewed later. Keep prior reference sets intact, and use the IRS prior-year archive for lookbacks instead of overwriting older decision records.

2. Revalidate on hard IRS scope changes#

Do not treat an approval as evergreen. Form 8233 is separate for each tax year, each withholding agent, and each type of income, so those are your minimum re-check triggers.

Use this as an operating rule:

| Revalidation trigger | Why it reopens review |

|---|---|

| New tax year | Form 8233 is required separately by tax year |

| Different withholding agent | Form 8233 is required separately by withholding agent |

| Different income type | Form 8233 is required separately by type of income |

If facts change in ways that could affect treaty eligibility or status, reassess against current Publication 901 and Publication 519. If concerns arise, do not apply the treaty rate. When a refreshed form is accepted, the withholding agent forwards one copy to the IRS within 5 days of acceptance.

3. Monitor live IRS change signals, not just stored PDFs#

Check IRS source pages on a recurring cadence so your controls follow current materials. As of this snapshot, the About Form 8233 page includes current-revision and all-revisions entry points and shows 23-Jan-2026 as last reviewed or updated; Publication 901 and Publication 519 pages show 30-Mar-2026 and 27-Mar-2026.

Also check the instructions' Future Developments notice. As of this snapshot, About Form 8233 and About Publication 901 list recent developments as none at this time; log that the check occurred either way.

4. Add policy triggers for repeat exception patterns#

Use internal policy triggers when repeat exception patterns appear, and sample prior approvals from that cohort for retesting against current instructions and publications.

This is not an IRS-mandated trigger. It is a platform control to catch drift early when guidance is stale, vague, or being applied inconsistently.

Checkpoint 8 tie Form 8233 outcomes to reporting and downstream tax ops#

Treat approvals and reporting as one control chain. A treaty-exempt withholding result can change tax withheld, but it does not remove the payment from reporting.

1. Reconcile approved withholding treatment to every reportable payment#

Do not let accepted claims live only in reviewer notes. Link each accepted outcome to the payout rows that feed annual reporting, because IRS rules separate withholding requirements from reporting requirements under nonresident alien withholding.

Keep a three-way reconciliation before filing:

- withholding decision log

- payment ledger

- Form 1042-S export

If a payment is in the ledger but missing from the 1042-S export because no tax was withheld, that is a reporting failure. If Form 1042-S is required, Form 1042 is also required.

2. Lock the exact fields finance must carry through#

Do not hand finance a note that just says "treaty approved." Pass structured fields from the accepted tax record: tax year, withholding agent, income type, recipient identifiers on file, applied withholding rate, and the basis for a rate below 30%.

Validate these before filing:

- if tax withheld is below 30%, chapter 3 exemption code must be present on Form 1042-S

- when recipient identifiers are available to the withholding agent, those identifiers must be entered on Form 1042-S

3. Treat missing TIN or incomplete documentation as a reporting-risk trigger#

Do not grant treaty treatment without proper documentation. IRS guidance states that a treaty benefit cannot be granted until a proper Form 8233, W-8BEN, or W-8BEN-E is received; if a required TIN is missing (and no exception applies), withholding defaults to 30%.

Use a hard exception queue for incomplete files. IRS recurring quality failures include unknown recipient status, invalid income codes, invalid tax rates, and required boxes left blank, so block reduced-rate records from final export until documentation is complete and consistent.

4. Align filing-year operations before reporting freeze#

Check filing-year instructions before finalization. Current instructions state:

- 2025 Forms 1042-S, due March 15, 2026: either IRIS or FIRE may be used

- 2026 Forms 1042-S, due March 15, 2027: IRIS must be used, available beginning January 1, 2026

Make this a release control: finance confirms the reporting population is tied to accepted Form 8233 records, and tax ops confirms the filing channel and due-date workflow match the applicable filing year.

Need the full breakdown? Read Form 3520-A for Foreign Trusts With a U.S. Owner.

What a defensible Form 8233 program looks like by year end#

By year end, defensibility comes down to consistency: for the same facts, your team reaches the same outcome, keeps the same audit trail, and applies the right Form 1042-S filing path for that reporting year.

1. Use one dated IRS baseline#

Use one current IRS baseline for reviewers, and record the date and version used for each decision. For this control, Publication 515 is a practical anchor because it directs teams to check IRS.gov/Pub515 for developments after publication.

If your platform applies stricter internal rules, label them as internal policy. Do not present house rules as IRS requirements.

2. Keep Form 8233 as one lane, not the catchall lane#

Treat Form 8233 as a specific control lane within intake, not the destination for every foreign-payee tax issue. A useful year-end check is whether the queue contains only the cases your team meant to review there.

Publication 515 gives a useful failure test for affected treaty-suspension cases: withholding agents may not accept treaty claims for withholding on interest payments on credits, loans, and other forms of indebtedness. If those appear in the Form 8233 queue, tighten triage.

3. Revalidate when treaty status changes#

Do not rely on old approvals when treaty status changes. Publication 515 flags a partial suspension of the income tax convention with Russia. It also describes a Belarus suspension, effective December 17, 2024, continuing until December 31, 2026, or earlier if mutually ended.

For affected cases, reopen and revalidate the file with a dated check. Publication 515 also states that beginning on or after August 16, 2024, affected cases require statutory 30% withholding.

4. Tie case decisions to filing channel and year#

Connect Form 8233 outcomes to the Form 1042-S filing channel for the applicable year. A simple year-and-filer-type matrix prevents channel errors.

For 2025 Forms 1042-S, due March 15, 2026, either IRIS or FIRE may be used. For 2026 Forms 1042-S, due March 15, 2027, IRIS must be used. Publication 515 also states that prior-year Forms 1042-S and submissions by foreign filers continue through FIRE, and FIRE is set to retire for tax year 2026.

This pairs well with our guide on Foreign Exchange Risk for Platform Operators and the Decisions That Cut FX Exposure.

If you want to stress-test this Form 8233 control framework against your payout and reporting workflow, contact Gruv.

Frequently Asked Questions

What is Form 8233 and when does it apply to foreign contractors?

Form 8233 is used by a nonresident alien individual to claim exemption from withholding on compensation for personal services. In contractor settings, that generally means independent personal services. If no exemption or reduction applies, the general baseline for independent personal services is 30% withholding.

Who can claim a tax treaty withholding exemption under Form 8233?

Only a nonresident alien individual can claim under Form 8233. The claim must cover personal-services income under an applicable treaty. Verify both before moving to deeper treaty analysis.

Is Form 8233 interchangeable with Form W-8BEN for platform operations?

No. Form 8233 is for income earned from personal services, while Form W-8BEN is for income not earned from personal services. Using the wrong form can lead to incorrect withholding treatment.

What should a platform verify before accepting a treaty-based withholding claim?

Verify that the payee is a nonresident alien individual, the payment is compensation for personal services, and the treaty position is supportable under current IRS materials. Handle the form separately for each withholding agent and each type of income. After acceptance, the withholding agent must review and sign the form and forward it to the IRS within 5 days.

When should a platform escalate a Form 8233 case to tax or legal specialists?

Escalate when the treaty basis, income classification, or nonresident status is unclear. Also escalate if there is reason to know the claim may be ineligible. Do not apply the treaty rate unless eligibility is clearly supportable.

How does Form 8233 review affect Form 1042-S reporting obligations?

A treaty exemption under Form 8233 does not by itself remove Form 1042-S reporting. Form 1042-S may still be required even when the compensation is fully treaty-exempt. Keep the withholding decision tied to reporting controls.

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.

How to Respond to a Subpoena for Business Records

Move fast, but do not produce records on instinct. If you need to **respond to a subpoena for business records**, your immediate job is to control deadlines, preserve records, and make any later production defensible.

A US Expat's Guide to Investing in UCITS ETFs to Avoid PFIC Issues

The real problem is a two-system conflict. U.S. tax treatment can punish the wrong fund choice, while local product-access constraints can block the funds you want to buy in the first place. For **us expat ucits etfs**, the practical question is not "Which product is best?" It is "What can I access, report, and keep doing every year without guessing?" Use this four-part filter before any trade: