Quick Answer

Yes: Form 3520-A is the annual return for a foreign trust with at least one U.S. owner, and you must ensure it is handled even when the trustee is the named filer. If the trust does not file, complete a substitute Form 3520-A, include the required annual statements, and submit it through Form 3520 instead of filing it alone. Timing depends on the trust year-end and your own filing calendar, so verify current instructions before submitting.

Your Form 3520-A Playbook: A CEO's Guide to Foreign Trust Compliance#

The form 3520-a foreign trust return is the annual information return for a foreign trust with at least one U.S. owner. It reports the trust, its U.S. beneficiaries, and its U.S. owner to the IRS. The core point is simple: the foreign trust files the return, but you are still responsible for making sure the filing and required annual statements happen.

That accountability split comes from section 6048(b). The foreign trust files Form 3520-A, and the U.S. owner must make sure it is complete and filed. If the trust does not file, you must complete and attach a substitute Form 3520-A to Form 3520. For 6048(b) failures, section 6677 places penalty liability on the U.S. person.

| Role | Core responsibility | Filing action | Exposure if missed |

|---|---|---|---|

| Foreign trustee / foreign trust | File the annual return and furnish required annual statements | File Form 3520-A | Filing failure does not remove U.S. owner responsibility |

| U.S. owner | Ensure Form 3520-A and required statements are filed or provided under section 6048(b) | Confirm trust filing; if not filed, attach substitute Form 3520-A to Form 3520 | Section 6677 framework applies to the U.S. person for 6048(b) failures |

Start with one timing check. Confirm the trust tax year-end. Form 3520-A is due by the 15th day of the 3rd month after that year-end. If you file a substitute Form 3520-A with Form 3520, it is due the same day as Form 3520, generally the 15th day of the 4th month after your tax year-end.

| Form | Purpose | Who files | When used |

|---|---|---|---|

| Form 3520-A | Annual information return for a foreign trust with at least one U.S. owner | Foreign trust; if it fails, the U.S. owner must complete a substitute attached to Form 3520 | Annual foreign trust reporting |

| Form 3520 | Report certain foreign trust transactions, foreign trust ownership, and certain large foreign gifts or bequests | U.S. person | When ownership, transactions, or gift reporting triggers apply |

That is the working model for the rest of the article. Understand penalty risk, manage the trustee early, execute substitute filing if needed, and keep records that support your position if the IRS asks questions.

We covered a related ownership framework in What is a 'Controlled Foreign Corporation' (CFC) for a US Shareholder?.

Why a Foreign Trust? The Strategic Context for Global Professionals#

A foreign trust is a planning tool, not a secrecy tool. The real question is whether it solves a specific cross-border problem well enough to justify the reporting burden and classification risk that come with it.

The IRS recognizes legitimate trust uses, including estate planning, and also treats trusts used to hide true ownership or income as fraudulent. So the right posture is straightforward: use the structure for real planning goals, and expect a U.S. reporting analysis to follow from that choice.

| Strategic benefit | What it helps you do | Reporting burden you accept |

|---|---|---|

| Asset protection planning | Place assets in a trustee-managed structure that may separate them from your personal balance sheet | Confirm whether the arrangement is a foreign trust for U.S. tax purposes and whether you are treated as a U.S. owner |

| Cross-border estate planning | Coordinate assets and beneficiaries across countries under one legal arrangement | Planning is detail-heavy, and weak structuring can lead to severe tax consequences |

| Centralized international holdings | Manage a major asset or pooled assets for multiple beneficiaries while keeping the asset intact | Ownership, transfer, and beneficiary facts can trigger U.S. owner treatment and annual information reporting |

| Pre-immigration planning | Set up ownership before U.S. tax residency begins | Transfers within 5 years can be treated as occurring on your U.S. residency start date for U.S. owner-treatment analysis |

Four valid use cases, with the tradeoff stated plainly#

If liability exposure is the concern, asset protection is often why this comes up first. The practical effect is that assets may sit in a trustee structure instead of your personal name. The tradeoff is real. Legal effect is jurisdiction-specific, and reporting failures can still create U.S. penalty exposure.

If your family and assets span countries, estate planning is often the stronger reason. A trust can coordinate beneficiaries, administration, and succession across legal systems. The tradeoff is complexity. A structure that works locally can still create poor U.S. tax outcomes if it is not designed correctly.

If you are managing a business interest, real estate, or another concentrated asset for multiple beneficiaries, centralized holdings can simplify administration and keep the asset intact. The tradeoff is the U.S. tax ownership analysis. Labels do not control, and section 679 can treat a U.S. transferor as owner of the relevant trust portion when a U.S. beneficiary is involved.

If you are planning around a future U.S. move, pre-immigration trust work is highly timing-sensitive. A pre-residency structure may fit into a broader plan, but the 5-year lookback can deem certain transfers to occur on your U.S. residency start date.

The guardrails that stop bad decisions#

Start with classification, not marketing labels. A trust is foreign for U.S. tax purposes if it is not domestic, and domestic status depends on the court test and control test. In practice, verify whether a U.S. court can exercise primary supervision and whether U.S. persons control all substantial decisions.

| Trigger | What to verify |

|---|---|

| Court test and control test are not clearly mapped from the governing documents | Settle the classification analysis |

| You transferred property to the trust, or a U.S. beneficiary is involved | Verify section 679 owner treatment and the current filing consequences |

| You are moving to the United States, recently became a U.S. tax resident, or funded the trust within the last 5 years | Verify the current pre-immigration timing analysis |

| Local advisers promise outcomes based on local law alone | Check the U.S. consequences against the actual jurisdiction and structure |

| The arrangement may be a retirement, education, medical, disability, or other tax-favored trust | Verify whether a current reporting exemption actually applies |

Before you get to filing, review the governing facts: trust deed and amendments, trustee appointment and removal rights, protector powers, and who controls investment, distribution, and administration. Do not assume a structure is exempt just because it is described as a trust, foundation, pension, or similar vehicle. Some tax-favored foreign trusts may qualify for reporting exemptions, but eligibility needs to be verified under current rules.

Use one final filter. This is planning-specific, not universal. If the structure does not solve a real legal, family, or ownership problem, the ongoing compliance burden may outweigh the benefit. Escalate early if any of these are true:

- You cannot clearly map the court test and control test from the governing documents, and the classification analysis is not settled.

- You transferred property to the trust, or a U.S. beneficiary is involved. Verify section 679 owner treatment and the current filing consequences.

- You are moving to the United States, recently became a U.S. tax resident, or funded the trust within the last 5 years. Verify the current pre-immigration timing analysis.

- Local advisers are promising asset protection, succession, or tax outcomes based on local law alone. The U.S. consequences need to be checked against the actual jurisdiction and structure.

- The arrangement may be a retirement, education, medical, disability, or other tax-favored trust. Verify whether a current reporting exemption actually applies.

The benefits can be real, but so is the exposure. Before you rely on the structure, get clear on what a filing failure can cost you. If you want a deeper dive, read The Ultimate Digital Nomad Tax Survival Guide for 2025.

The High Stakes: Understanding Non-Compliance Penalties#

Your main risk here is an information return failure, not an income tax calculation error. Treat Form 3520-A as a filing control process that you actively manage.

For a foreign trust with a U.S. owner, Form 3520-A is due by the 15th day of the 3rd month after the end of the trust's tax year. The key question is whether a complete return was filed on time, because late, incomplete, or incorrect filings can all trigger penalties. Use this penalty framework before you file:

- Baseline trigger: the return is late, incomplete, or incorrect.

- Asset-linked component: for Form 3520-A owner exposure under section 6048(b), the initial penalty is the greater of a fixed amount or a percentage of the gross value treated as owned by the U.S. person at year-end (under current instructions revised 12/2025: $10,000 or 5%).

- Post-notice escalation: if the issue is still unresolved more than 90 days after IRS notice, continuation penalties can apply (currently $10,000 per 30-day period or fraction, subject to the gross-value cap).

- Current-year check: confirm the latest instruction amounts before relying on any dollar figure.

| Filing status | Exposure path | What you should confirm |

|---|---|---|

| On time and complete | No failure-to-file penalty on this issue | Filed date, complete return package, submission proof |

| Late but complete | Initial penalty framework can apply | Actual filing date and cure timing |

| Missing, incomplete, or incorrect | Initial penalty framework can apply | What required information was missing or inaccurate |

| Still unresolved after IRS notice | Continuation-penalty pathway can apply after 90 days | Notice date, response timeline, cure evidence |

Do not assume trustee responsibility removes your exposure. Even when the foreign trustee is the named filer, you remain responsible for ensuring Form 3520-A is filed. If it is not, the owner-side substitute Form 3520-A attached to Form 3520 is the stated path to avoid the trust-failure penalty.

Reasonable cause is facts-and-circumstances based, not automatic. Your defense is documented good-faith effort and ordinary care: outreach records, follow-ups, draft and filing checks, and proof of timely submission. This defense is strongest when you manage the trustee early enough to act before the deadline. For related timing issues, see 183-Day Rule Explained: Stop the Tax Myths Before They Cost You.

Step 1: The Proactive Mandate - Manage Your Foreign Trustee Like a CEO#

Do not run this as a passive "wait for the trustee" exercise. Run it as your annual compliance process, with written checkpoints, required inputs, and an internal cutoff that triggers action.

The form mechanics support that approach. The return can be marked as Substitute Form 3520-A, and the signature line allows a trustee's or a U.S. owner's signature. So the point of Step 1 is to control readiness early, not chase updates late.

Use a phased checklist, not open-ended reminders#

| Phase | Main task | Key detail |

|---|---|---|

| Kickoff request | Confirm the expected signer and whether a U.S. agent is appointed | Ask whether an Authorization of Agent was last attached and for which year; a "Yes" entry changes how lines 2a through 2e are handled |

| Document request package | Send one consolidated request covering all required inputs | Form 3520-A reporting must be in English and amounts must be in U.S. dollars |

| Internal review buffer | Review for completeness, not just activity | Confirm owner statements, beneficiary statements, U.S. agent status, and trust-document attachment requirements are resolved in a reviewable package |

| Escalation trigger | Move to substitute filing preparation if required deliverables are still incomplete at your cutoff | Do not extend based on informal promises |

- Kickoff request (set kickoff date after verification)

Confirm the expected signer and whether a U.S. agent is appointed. Ask whether an Authorization of Agent was last attached and for which year, since a "Yes" entry changes how lines 2a through 2e are handled.

- Document request package (send one complete request)

Send one consolidated request that covers all required inputs. State up front that Form 3520-A reporting must be in English and amounts in U.S. dollars, so translation and conversion work is part of readiness.

- Internal review buffer (set internal cutoff before filing)

Review for completeness, not just activity. Confirm that owner statements, beneficiary statements, U.S. agent status, and trust-document attachment requirements are all resolved in a package you can actually review.

- Escalation trigger (execute at internal cutoff)

If required deliverables are still incomplete at your cutoff, move to substitute filing preparation. Do not extend based on informal promises.

Must-have inputs for Form 3520-A preparation#

- Owner statement readiness: Form 3520-A asks for the number of Foreign Grantor Trust Owner Statements (pages 3 and 4).

- Beneficiary statement readiness: Form 3520-A asks for the number of Foreign Grantor Trust Beneficiary Statements (page 5).

- U.S. agent status and authorization year: If a U.S. agent is appointed, the form requests the authorization year and directs you to skip lines 2a through 2e.

- Trust-document set when no U.S. agent is appointed: Required attachments include the trust instrument, a summary of written and oral agreements or understandings, and an organizational chart and other trust documents.

- Prior-file reference: If those trust documents were attached within the previous 3 years, attach relevant updates only.

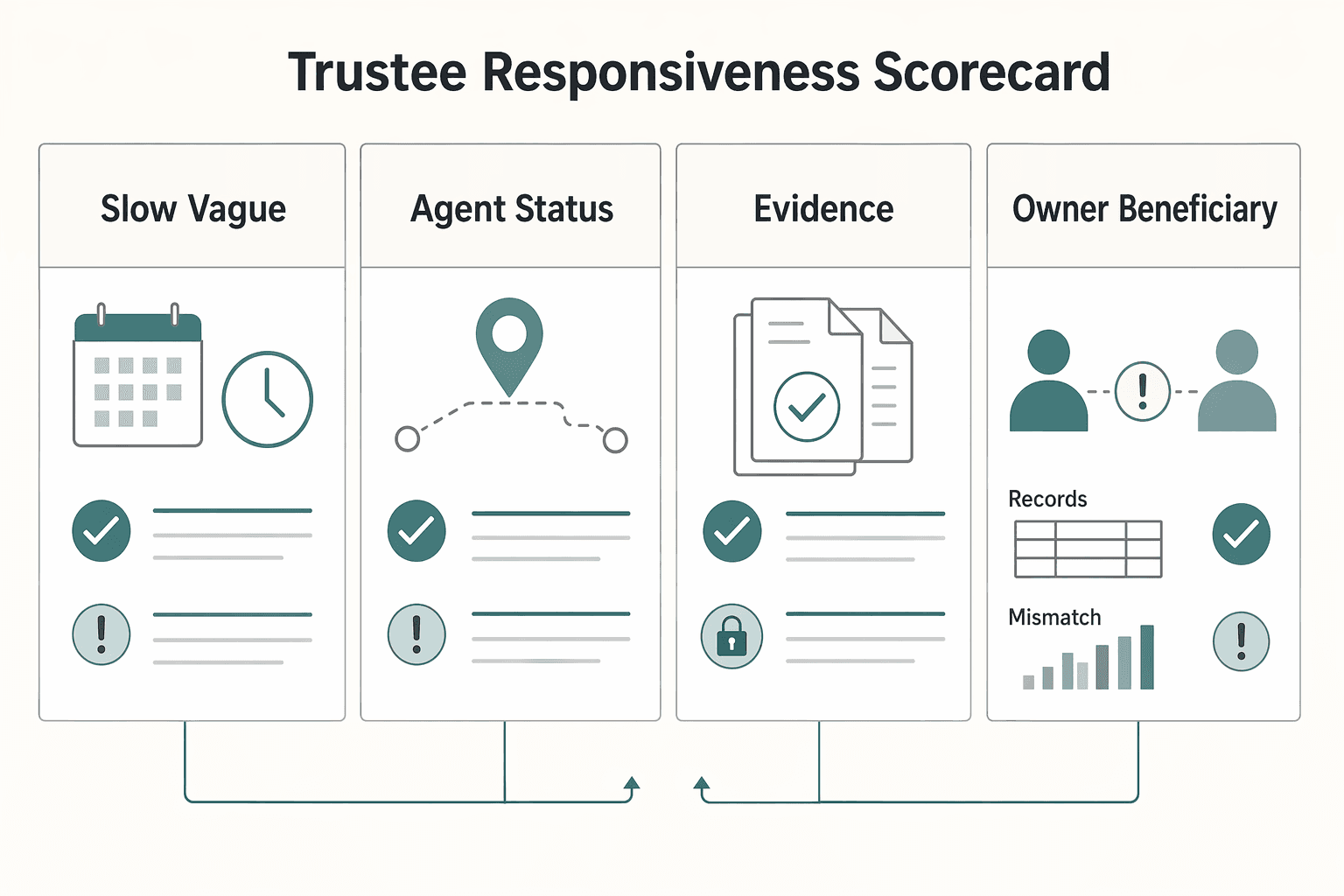

Trustee responsiveness scorecard#

| Signal | Why it matters | Your next action |

|---|---|---|

| Slow or vague responses | You cannot confirm filing readiness from acknowledgments alone | Convert to a dated deliverables list; start substitute prep in parallel |

| U.S. agent status or authorization year is unclear | Affects form handling and attachment path | Request prior authorization and prior filing support immediately |

| Records arrive only in non-English or non-USD form | Package is not review-ready for Form 3520-A requirements | Request translated and converted support before review |

| Owner or beneficiary statement counts are missing or inconsistent | The form explicitly asks for statement counts | Treat as incomplete; escalate at the internal cutoff |

| Trust-document package is withheld when no U.S. agent is appointed | Attachment requirements may not be met | Document the gap and move to the contingency process |

If owner statements, beneficiary statements, U.S. agent confirmation, or required trust documents are still incomplete by your internal cutoff, move to Step 2 and begin the substitute filing process. Do not wait longer.

For another step-by-step walkthrough, see A Deep Dive into the Foreign Tax Credit (Form 1116).

Step 2: The Contingency Plan - Master the "Substitute" Form 3520-A#

If the trust has not filed Form 3520-A, or you cannot verify a correct, on-time filing, move to the substitute path. You are still responsible for making sure Form 3520-A and the required annual statements are handled, even when the trustee is unresponsive.

If the trust does not file, your fallback is to complete and attach a substitute Form 3520-A. The goal is a complete package built from the records you can support now.

If trustee stalls, do this next#

- Confirm the trigger

Treat the substitute path as triggered when the trust has not filed Form 3520-A. If filing status is unclear and you cannot verify a correct, on-time filing with reviewable documentation, treat it as unresolved and prepare the substitute package.

- Gather controlled records

Pull the records you can support now, including prior filings, trust financial records, owner and beneficiary data, distribution support, trust documents, and trustee correspondence.

- Prepare the substitute package

Complete Form 3520-A using the best available support and check the "Substitute Form 3520-A" box.

- Include required statements

Prepare and include the Foreign Grantor Trust Owner Statement and Foreign Grantor Trust Beneficiary Statement as part of the substitute package.

- Sign as U.S. owner

In substitute mode, you sign the form.

- File through the correct path

A substitute Form 3520-A is not filed standalone. It must be attached to Form 3520. For a refresher on that companion return, see A Deep Dive into Form 3520 (Annual Return To Report Transactions With Foreign Trusts).

Deciding between the standard and substitute filing path#

| Decision point | Standard trustee path | Substitute path (you) |

|---|---|---|

| Who files | Foreign trust | You, as U.S. owner |

| Where submitted | Separate Form 3520-A filing path (verify current IRS where-to-file details before sending) | Submitted with Form 3520, not standalone |

| What it must be attached to | Filed separately from your U.S. income tax return | Must include substitute Form 3520-A plus owner and beneficiary statements attached to Form 3520 |

| Timing path | Due by the 15th day of the 3rd month after the trust tax year ends (verify current instructions for your year) | Same due date path as Form 3520 (verify current instructions for your year) |

Use this table as a decision check. Choose the right path first, then verify current-year timing and filing-location instructions before you file.

Common mistakes to avoid#

- Filing substitute Form 3520-A by itself instead of attaching it to Form 3520

- Forgetting to check the "Substitute Form 3520-A" box

- Leaving out the required owner or beneficiary statements

- Assuming trustee silence removes your reporting duty

- Using unverified prior-year timing or mailing details for the current filing year

You might also find this useful: A Deep Dive into Form 5472 for Foreign-Owned US LLCs.

Step 3: The Documentation Vault - Build Your "Reasonable Cause" Defense#

Filing is only half the job. A clean evidence trail can help you explain what you requested, what you received, what stayed missing, and what you did next as the U.S. owner.

Use the same structure every year, one vault per tax year and per trust. That matches the rule to file a separate Form 3520 for each foreign trust. It also keeps the file ready if you need to escalate, respond to a notice, or support a reasonable-cause position.

Build one vault per year, per trust#

Use one consistent folder map every year so nothing gets scattered:

| Folder | Contents |

|---|---|

| 01_Governing_Documents | Trust instrument, subsequent variances, and summaries of written or oral agreements and understandings |

| 02_Trustee_Records | Trustee-provided records and U.S. agent details, if appointed |

| 03_Draft_Filings | Working drafts of Form 3520-A, owner statements, beneficiary statements, and Form 3520 |

| 04_Final_Filed_Package | Signed final forms, attachments, and the exact packet submitted |

| 05_Delivery_Proof | Mailing or courier proof and submission cover materials |

| 06_Correspondence_Log | One row per contact with counterparty, channel, date, summary, requested action, and follow-up status |

| 07_Memo_to_File | Trust name and tax year, filing path used, who you contacted, what was missing, whether a U.S. agent existed, which trust documents were attached, and why the package was complete or completed in good faith with available records |

01_Governing_Documents

Trust instrument, subsequent variances, and summaries of written or oral agreements and understandings.

02_Trustee_Records

Trustee-provided records and U.S. agent details, if appointed.

03_Draft_Filings

Working drafts of Form 3520-A, owner statements, beneficiary statements, and Form 3520.

04_Final_Filed_Package

Signed final forms, attachments, and the exact packet submitted.

05_Delivery_Proof

Mailing or courier proof and submission cover materials.

06_Correspondence_Log07_Memo_to_File

Use sortable filenames, for example: 2026-02-12_Trustee_Email_Request-owner-statement.pdf and 2026_Form3520A_Substitute_FINAL_signed.pdf. Keep version tags like v1, v2, and FINAL, and never overwrite prior files.

Keep a correspondence log in real time#

Log each interaction when it happens so you do not have to rebuild the timeline later. For internal tracking, use one row per contact with fields like:

- Counterparty

- Channel

- Date

- Summary

- Requested action

- Follow-up status

The log should make the sequence obvious when data is incomplete: request, reminder, response or non-response, gap identified, escalation, and filing decision.

Required records checklist#

| Record | Keep this in the vault | Why it matters | Retention note |

|---|---|---|---|

| Governing trust docs | Trust instrument, variances, summary of written or oral agreements | Form 3520-A calls for these attachments in the relevant cases | Confirm your current retention standard |

| Trustee or U.S. agent support | Trustee statements and U.S. agent details, if any | Supports whether additional trust documents must be attached when no U.S. agent is appointed | Confirm your current retention standard |

| Filed forms package | Final Form 3520-A (or substitute), Form 3520, owner statements (pages 3-4), beneficiary statements (page 5) | Shows exactly what you filed and included | Confirm your current retention standard |

| Delivery proof | Mailing or courier receipts and submission packet proof | Supports your internal submission trail | Confirm your current retention standard |

| Memo to file | Contemporaneous note on missing data, trustee non-response, and judgment calls | Organizes facts and decisions for advisor follow-up | Confirm your current retention standard |

Before filing, run one final check: the signed final packet is present, and Form 3520 information is prepared in English with amounts in U.S. dollars.

Use a memo-to-file template every year#

Write the memo while facts are fresh, not after a notice arrives. Use the same template each year so your explanation stays consistent:

- Trust name and tax year

- Filing path used (standard or substitute)

- Who you contacted and what you requested

- What was missing at decision time

- Whether a U.S. agent existed

- Which trust documents were attached

- Why the package was complete, or completed in good faith with available records

Include two explicit notes when relevant:

- If no U.S. agent was appointed, record that and preserve the attached trust document set.

- If those trust documents were attached to a Form 3520-A filed within the previous 3 years, record that and include only relevant updates for the current year.

This pairs well with our guide on A guide to 'Form 8233' for foreign individuals receiving US scholarship or fellowship grants. Before you submit anything, sanity-check your process with practical templates and calculators: Explore Gruv tools.

Conclusion: You Are in Command of Your Compliance#

You remain accountable for Form 3520-A compliance, even when the trustee is the named filer. Treat this as a repeatable process you control and verify each year. For a foreign trust with at least one U.S. owner, filing is annual, and failure can trigger an initial penalty measured as the greater of $10,000 or 5% of the relevant gross value.

Your default framework has three moves. First, manage the trustee early so you can confirm whether the trust will file Form 3520-A by the 15th day of the 3rd month after the trust year-end and furnish the required annual statements. Second, keep a substitute path open. If the trust does not file, you must attach a substitute Form 3520-A to Form 3520, and that substitute follows the Form 3520 due date. Third, keep records that support a reasonable-cause position under IRC 6677 if a failure occurs despite real diligence.

Your records should include trust documents, owner and beneficiary statements, deadline tracking, filing confirmations, and notes explaining any missing data. Do not assume filing is complete until you have the full package or clear proof of filing.

For your next filing cycle, confirm trustee status early, verify whether the regular or substitute path applies, maintain records as the process moves, and review the full package before submission. If records are incomplete, trustee responses conflict, or Form 3520 coordination is unclear, consider engaging a qualified cross-border tax professional before you file.

Need the full breakdown? Read A Guide to Form 1042-S for Foreign Persons' U.S. Source Income. If your trustee is unresponsive or your records conflict, get help mapping a safer filing workflow: Contact Gruv.

Frequently Asked Questions

What is the difference between Form 3520 and Form 3520-A?

Form 3520-A covers the foreign trust's annual information, and Form 3520 is your separate U.S. person reporting form. Use the table below to sort out who files, what it reports, and where it goes. | Form | Who files | What it reports | Where it is filed | |---|---|---|---| | Form 3520-A | Foreign trust (you, as U.S. owner, must ensure filing and required statements) | Annual trust information, including owner and beneficiary statement information | Per current Form 3520-A instructions | | Form 3520 | You, if filing rules apply | Foreign trust transactions and ownership reporting, and certain foreign gifts | Separately from your income tax return, per current Form 3520 instructions | | Substitute Form 3520-A | You, if the trustee does not file | Trust-level annual information as a substitute filing | Attached to Form 3520 and filed using current Form 3520 instructions | For deeper owner-side detail, see A Deep Dive into Form 3520 (Annual Return To Report Transactions With Foreign Trusts).

Who is officially responsible for filing Form 3520-A?

The foreign trust (through its trustee) is the filer, but you remain responsible for ensuring Form 3520-A is filed and that the required annual statements are furnished. Do not rely on verbal updates alone. If you do not have the completed filing package or clear filing confirmation, treat substitute filing as the active backup path.

When are Form 3520 and 3520-A due, and how do extensions work?

Form 3520-A generally follows the 15th day of the 3rd month after the trust year-end, and Form 3520 generally follows the 15th day of the 4th month after your tax year-end. A substitute Form 3520-A attached to Form 3520 is due the same day as Form 3520. If you live and work outside the United States, Form 3520 may follow the 15th day of the 6th month rule, so confirm the current deadline for your year. For regular Form 3520-A filing, an automatic 6-month extension may be requested with Form 7004. Do not assume your individual return extension automatically extends the regular Form 3520-A deadline.

What do you do if the trustee does not file?

Prepare a substitute Form 3520-A, attach it to Part II of Form 3520, and file it using the Form 3520 filing instructions. You also need to furnish the required annual statements by your Form 3520 due date. If records are incomplete near the deadline, file the best supportable substitute package and document the gaps in your records.

How serious are the penalties?

They are serious: IRS guidance says failures to satisfy foreign-trust information-reporting requirements can result in significant penalties. If the trust does not file Form 3520-A, filing the required substitute Form 3520-A with Form 3520 is one of the key steps IRS instructions tie to avoiding penalties for the trust's non-filing.

When should you escalate to a qualified cross-border tax professional?

Escalate quickly if trustee records are incomplete, trust documents conflict with annual statements, or you are unsure how Form 3520 and substitute Form 3520-A should be coordinated. Bring a complete evidence pack so a professional can act fast: trust documents, correspondence log, draft and final statements, and filing-extension proof if relevant. This matters most when timing is tight and data quality is uncertain.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- cops.usdoj.gov/pdf/2020AwardDocs/cpd/AOM.pdftrusted

- dot.nj.gov/transportation/capital/pd/documents/PEPhaseG...trusted

- ecfr.gov/current/title-26/chapter-I/subchapter-A/part...trusted

- irs.gov/pub/fatca/failure-to-file-form-3520-3520a-pe...trusted

- irs.gov/forms-pubs/about-form-3520trusted

- uscode.house.gov/view.xhtmltrusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Digital Nomad Taxes in 2026 With a Defensible Filing Plan

With digital nomad taxes, the first move is not optimization. It is figuring out where you may be taxable, where filings may be required, and what proof supports that position.

183-Day Rule Tax Myths That Trigger Residency Filing Mistakes

If you are a mobile freelancer or consultant, start here: the "183 day rule tax" idea is not a single universal test. It is a shortcut phrase people use for different residency rules that do not ask the same question. If you mix federal and non-federal residency logic, you can create filing risk even when your travel calendar looks clean.

Form 3520 Playbook: A 3-Step Framework for Foreign Trust Transactions and Foreign Gift Reporting

You can help lower Form 3520 filing risk with a simple three-step process: classify early, document as you go, and prepare for exceptions. This is an operations playbook, not a tax theory lesson. It is designed to help you make cleaner decisions before transactions, keep better filing records, and respond from evidence if questions come later.