Quick Answer

Map FX exposure by workflow first, then measure materiality by currency pair and timing, and only then choose mitigation. For platform operators, the practical sequence is to classify transaction versus translation versus economic risk, tie committed items to payout and conversion records, and review open positions on a standing cadence. Use the simplest instrument your team can operate and reconcile, and reject stale quote paths so retries do not create duplicate financial events.

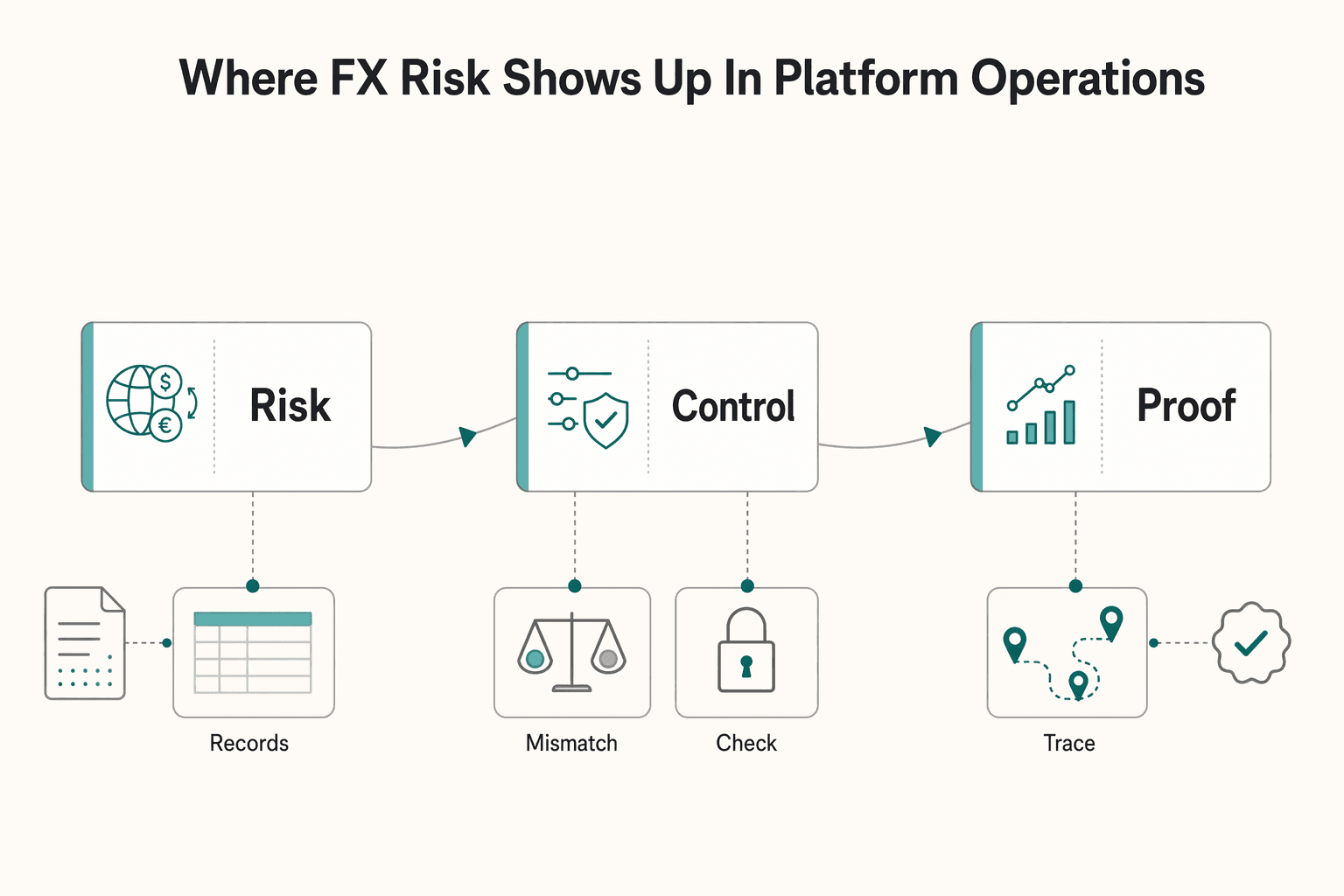

Where FX Risk Shows Up in Platform Operations#

Foreign exchange risk is not just a problem for large multinationals. If your marketplace, embedded payments product, or contractor payout stack touches more than one currency, exchange-rate moves can affect margins and financial stability in very practical ways.

FX risk is the risk that exchange-rate moves change business outcomes. For platform operators, that exposure can show up quickly. You do not need a treasury desk to feel it.

A payout approved today may be funded later. A balance may sit in a non-functional currency. A pricing decision may be made in one currency and settled in another. Any of those can create losses or volatility.

The most useful starting point is to stop treating FX as one bucket. Most teams need to separate three exposure types early:

- Identify transaction risk in committed inflows and outflows where a rate move changes what you actually pay or receive.

- Separate translation risk from cash risk so reporting volatility does not distract you from live payout exposure.

- Flag economic risk where longer-term pricing, supplier, or market decisions are sensitive to currency moves.

That split is more than accounting hygiene. It changes what you do next. If the issue is transaction risk in cross-border payouts, you may need tighter timing, funding, or conversion controls. If the issue is broader profit volatility, hedging may help. Forward contracts, broader hedging approaches, and multi-currency accounts are all common options, but none is right for every flow.

This guide takes an execution-first approach. You will map where exposure is created in real workflows, measure which currency pairs and timing gaps are actually material, and then choose mitigation tactics with explicit tradeoffs. The goal is not theoretical completeness. It is to give finance, product, ops, and engineering the same exposure picture so you can act without creating fresh reconciliation problems.

One checkpoint matters from the start: if an exposure number cannot be traced to a real transaction, payout event, balance, or conversion record, it is not ready to drive decisions. One failure mode is chasing spreadsheet totals while the actual payout or settlement path remains unclear. Another is overreacting to translation noise while committed transaction risk stays open.

As you work through the next sections, keep evidence showing how each exposure was classified, what data fed the measurement, and who approved the mitigation choice. That record is what makes the process credible when rates move against you.

Related: IRS Form 1042-S for Platform Operators: How to Report and Withhold on Foreign Contractor Payments.

What to prepare before you start#

Start by locking ownership, data, and compliance records in one place. Otherwise your FX analysis can look right on paper and still fail in execution.

-

Assign named owners. Finance owns policy and hedge approval, payments ops owns execution, engineering owns automation and data movement, and compliance owns KYC, KYB, and AML gates. Put one person's name next to each role so escalation is clear when payouts fail, webhooks lag, or document gaps appear.

-

Build one source file for all foreign-currency flows. Include receivables, payables, Virtual Accounts inflows, payouts, and treasury conversions tied to your Ledger. Each line should map to entity, product, currency, and transaction state so you can tell whether exposure is still open or already closed.

-

Collect the documents you will need later. Keep a hedge policy draft, payout operations SOP, and tax/compliance artifacts together with the flow inventory, including W-8, W-9, IRS Form 1042-S support, and FATCA-related records where applicable. This keeps policy, operations, and reporting aligned.

-

Set phase-one boundaries early. Define which entities, currencies, and products are in scope now, and what stays out until controls are stable. If Form 8938 may apply, treat thresholds as filer-specific, not universal; for specified domestic entities, the instructions excerpt cites $50,000 at year-end or $75,000 at any time during the year, and Form 8938 is attached to the annual return. Also, do not assume Form 8938 replaces FBAR.

If you want a deeper dive, read How Platforms Are Reshaping the Market of Foreign Exchange: A 2026 Deep Dive.

Step 1 identify your real FX exposure by workflow#

Start by separating cash-impact FX risk from reporting effects. Classify every foreign-currency flow as transaction exposure, translation exposure, or economic risk before you discuss mitigation.

Classify each flow before you map it#

Use the table below as your working definition for each flow.

| Exposure type | Where it shows up | Article signal |

|---|---|---|

| Transaction exposure | Revenue or expenses in multiple currencies | A rate move can change what you actually collect or pay on an open item |

| Translation exposure | Foreign-currency-denominated assets, liabilities, equity, or income affecting reporting | The effect is mainly in reported balances or results |

| Economic risk | Longer-term competitiveness and company value | Exchange-rate moves affect competitiveness and company value |

A practical check: if a rate move can change what you actually collect or pay on an open item, treat it as transaction exposure. A €1 million invoice due in 60 days is a clear example. If the effect is mainly in reported balances or results, that is translation exposure. If the effect is on long-term competitiveness, that is economic risk.

Map the workflow where exposure is created#

After classification, trace the operating flow end to end for each in-scope entity and currency:

- invoice or receivable creation

- customer collection

- conversion event

- wallet credit or balance hold

- payout batch creation

- final settlement timing for cross-border payments

Your map should show where exposure is created, transferred, and closed. Use that map to decide whether operational changes or hedge design should come first.

Treat traceability as the control: each exposure point should tie to a Ledger event, payment record, conversion record, or payout batch record. If a step exists only in a spreadsheet, treat it as higher risk for manual error and weak inputs.

For a step-by-step walkthrough, see Foreign Exchange Risk for Freelancers Getting Paid Internationally.

Step 2 measure materiality before picking instruments#

Before you choose any hedge or treasury instrument, decide what is material. Measure exposure by currency pair, and keep committed obligations separate from forecast volume so your totals stay decision-useful.

Start with two exposure lanes:

- Committed obligations: amounts tied to an existing operational record (for example, an issued invoice, payout file, funding event, or settlement instruction).

- Forecast risk: expected volume that is relevant for planning but not yet locked by a concrete record.

Then add timing buckets to each line so you can see when rate risk is still open and what event closes it.

| Timing bucket | What it should answer |

|---|---|

| Same day | What is still open today, and what closes today |

| Short lag | What stays open into the next operating cycle |

| Longer lag | What remains open beyond the next cycle |

Publish one consistent weekly pack across finance, payments ops, and engineering:

- Open FX exposure (by pair, flow type, owner, timing bucket)

- Realized conversion variance

- Unreconciled exceptions

- Coverage status by flow type (committed vs forecast)

Treat this as a documented, repeatable risk assessment process and refresh it on a standing cadence. If you use bank-style governance references, apply them to your own context rather than copying another institution's setup.

Keep one strict verification rule: each exposure line should trace to system records, not spreadsheet-only assumptions. If a line is estimate-only, label it clearly and keep it separate from committed totals until records catch up.

Step 3 choose mitigation tactics with explicit tradeoffs#

Choose the tactic your team can execute and reconcile reliably under real liquidity constraints; precision is secondary if execution breaks. After Step 2, the decision is less about finding the right instrument in theory and more about avoiding a setup that cannot be funded, operated, or explained when timing shifts.

Use the same screening standard for every tactic: clear underlying exposure, clear owner, clear close event, and a clear reconciliation path. If those are missing, defer complexity until the operating controls are in place.

| Tactic | What to confirm before approval | Operational tradeoff to document |

|---|---|---|

| Forward contract | The underlying exposure is documented and traceable to an operational record | Execution and reconciliation load |

| Currency option | The exposure and ownership are documented, with explicit rationale for flexibility | Upfront cash impact and ongoing monitoring load |

| Futures contract | The exposure match and ownership model are documented | Standardized execution and monitoring burden |

| Currency swap | The recurring exposure and ownership model are documented | Multi-period coordination and control burden |

| Natural hedge | The offset is measured, durable, and reviewable over time | Cross-team discipline and ongoing verification burden |

Put liquidity and payout timing ahead of hedge precision. BIS defines liquidity as the ability to meet obligations when due without unacceptable losses, and that is the practical test: if a tactic strains funding or payout operations, it is not a good fit yet.

Treat complexity as a governance risk, not just a market choice. A May 2024 study on foreign currency risk management strategies reports that policies can be suboptimal and may fail to create value in family-firm settings, especially where family control and family management are combined. The takeaway for a platform is straightforward: if ownership and execution discipline are weak, adding instrument complexity is unlikely to fix outcomes.

Build controls into product and ops#

Treat these controls as launch criteria, not post-launch cleanup. In embedded payments and high-frequency payout programs, small execution failures can turn ordinary FX risk into duplicate conversions, blocked payouts, and unreconciled cash movement.

| Control step | Main action | Key evidence |

|---|---|---|

| Reject stale execution paths and make retries non-destructive | Reject and requote stale quotes; retry with the same idempotency key | One business event, one provider reference, and one intended Ledger outcome |

| Put compliance gates exactly where money can still move | Run KYC and KYB before funds leave; route suspicious Virtual Accounts activity to AML review; send failed payouts into an owned exception queue | Review before continuing payouts if party details, account details, or transaction behavior changes |

| Make every state transition auditable end to end | Trace the path from internal request to provider reference to Ledger posting; record each status change with timestamp, trigger, and owner | Request ID, idempotency key, provider reference, webhook event IDs, final settlement status, and Ledger entry IDs |

Step 1 Reject stale execution paths and make retries non-destructive#

Prevent one failed attempt from becoming two financial events. If a quote is stale when a conversion or payout reaches the provider, reject and requote instead of forcing execution. If a call times out, retry with the same idempotency key so one payable maps to one provider instruction.

This aligns with the operational baseline: control operational risk and keep controls in place until settlement is confirmed and reconciled. Your checkpoint is simple: for any retried request, show one business event, one provider reference, and one intended Ledger outcome. The common failure mode is split ownership, where engineering sees a timeout, ops sees no confirmation, and both sides re-initiate.

Step 2 Put compliance gates exactly where money can still move#

Place compliance gates before payout release, where they can still stop a loss. Run KYC and KYB checks before funds leave, route suspicious Virtual Accounts activity to AML review before conversion or payout, and send failed payouts into an owned exception queue.

Keep this practical, not static. If party details, account details, or transaction behavior changes, require review before continuing payouts under prior approval.

Step 3 Make every state transition auditable end to end#

Make the request-to-settlement path fully traceable from internal request to provider reference to Ledger posting. Record each status change with timestamp, trigger, and owner, and handle late or out-of-order webhooks by matching provider reference and current state before posting or reversing Ledger entries.

Your evidence pack should include request ID, idempotency key, provider reference, webhook event IDs, final settlement status, and Ledger entry IDs. If these are incomplete, reconciliation slows down and exposure can stay open longer than expected. If spreadsheet matching is your fallback, controls are not ready to scale.

Common mistakes that create avoidable FX losses#

Most avoidable FX loss comes from misclassified exposure and split ownership, not market drama. Start by protecting committed payout risk, then handle forecast and reporting noise.

- Hedge committed payables before forecast volume.

The first hedge should map to approved payout batches with known currency, amount, and timing, not broad quarterly expectations. If you cannot tie a hedge to a specific batch ID, currency pair, value date, and owner, you are likely hedging the wrong thing while ops still converts urgent payouts at spot.

- Treat translation volatility and cash exposure as different problems.

Reporting volatility can matter, but open payout obligations create immediate cash risk. Prioritize exposures that can force a currency buy or sell to complete payouts, and keep accounting translation effects from crowding out transaction-risk controls.

- Link FX execution records with tax/compliance records before release.

Running FX, tax, and compliance in separate lanes creates avoidable delays and rework. Keep FATCA/Form 8938/FBAR checks distinct: Form 8938 is attached to an annual tax return, and some taxpayers may also need FinCEN Form 114 (FBAR), so one does not automatically replace the other. Threshold and penalty details also matter: IRS guidance notes a general $50,000 reportable threshold for Form 8938 (with higher thresholds in some cases), and instructions for specified domestic entities reference over $50,000 on the last day of the tax year or over $75,000 at any time during the year. Failure to report can trigger a $10,000 penalty, which can rise up to $50,000 after IRS notice, and criminal penalties may also apply. The practical rule is simple: if these records are relevant to your structure, route them into the same exception queue as payout and FX holds.

- When losses spike, reduce complexity before changing strategy.

Do not add instruments, currencies, or looser hedge rules during a control failure. Freeze new hedge complexity, reconcile Ledger-to-bank mismatches, confirm provider references and settlement states, then restart with narrower scope and clear ownership across finance and ops.

Related reading: How to use 'Deel Shield' to mitigate contractor misclassification risk.

Your first 30 days and a copy-paste operating checklist#

Treat the first 30 days as a control build, not an optimization sprint. If ownership, traceable inputs, and one tested control path are not in place by day 30, do not add more currencies or instruments.

| Week | Focus | What to put in place |

|---|---|---|

| Week 1 | Inventory exposures and assign owners | Build one exposure map from Ledger records, payout batches, wallet balances, and conversion activity; classify each line; assign owners |

| Week 2 | Stand up a measurement cadence | Run a weekly pack; feed it from Ledger data, payout systems, and conversion logs; set escalation thresholds by owner |

| Week 3 | Pilot one mitigation tactic on one corridor | Keep scope to one tactic and one currency corridor, with documented entry and exit rules and dated evidence |

| Week 4 | Run one end-to-end control test | Test KYC/KYB/AML gates, payout batches, provider responses, Ledger posting, reconciliation artifacts, and incident response steps |

Week 1: inventory exposures and assign owners. Build one exposure map from Ledger records, payout batches, wallet balances, and conversion activity. Classify each line as transaction, translation, or economic risk, and note whether it is committed or forecast. Assign owners for policy, execution, engineering changes, and compliance review. Every line should tie to a currency pair, timing bucket or value date, source record, and named owner. If teams use different definitions, publish a shared glossary before moving on.

Week 2: stand up a measurement cadence. Run a weekly pack built around a clear lifecycle: identify, measure, monitor, and control. Feed it from Ledger data, payout systems, and conversion logs, and set escalation thresholds by owner for unreconciled items, missed funding windows, and out-of-policy conversions. If a dashboard line cannot be traced to a batch ID or provider reference, treat that as a control gap.

Week 3: pilot one mitigation tactic on one corridor. Keep scope tight: one tactic, one currency corridor, and documented entry and exit rules. Define who approves exceptions and what happens when payout timing slips. Keep dated evidence for the rule, approvals, execution, and reconciliation.

Week 4: run one end-to-end control test. Test one full path across KYC/KYB/AML gates, payout batches, provider responses, Ledger posting, reconciliation artifacts, and incident response steps. Archive dated policy and record-control artifacts so the process is repeatable and auditable.

Exposure map completeMeasurement pack liveHedge rule documentedControls testedException process assignedAudit evidence archived

Need the full breakdown? Read How to Handle Realized and Unrealized Gains/Losses on Foreign Currency.

Need a quick operational next step while you work through "foreign exchange risk platform operators identify measure mitigate"? Try the free invoice generator.

Conclusion#

If the main decision still feels fuzzy, keep the order simple: map the exposure first, measure it with traceable records, then choose the lightest mitigation you can operate reliably. That sequence helps you avoid a common trap: buying hedge complexity before you can prove what is actually exposed.

- Map the workflows that create currency risk.

Do this at the level where money actually moves: collections, conversions, payout batches, and settlement timing. Verification point: every exposure line should trace to a real operational event such as a ledger posting, payout instruction, bank movement, or provider reference, not just a spreadsheet estimate.

- Measure the positions that matter before you pick an instrument.

Review exposure by currency pair and by timing, especially where payout windows and funding windows do not line up. A regular review pack can keep the team aligned: open FX exposure, realized conversion variance, unreconciled exceptions, and hedge coverage by flow type. Failure mode to watch: if finance and ops use different definitions for the same balance, you can end up hedging forecast risk while committed payables stay exposed.

- Mitigate with tools your team can execute and reconcile.

The grounded options here are clear: forward contracts, currency swaps, multi-currency bank accounts, and hedging strategies such as matching currency flows. A natural hedge can be a simple answer when inflows and outflows line up in the same currency. If timing is uncertain, forcing a rigid hedge onto unstable volume can create more cleanup work later. Document pack to keep: instrument choice, covered exposure line, timing assumption, approvals, execution records, and the reconciliation trail back to the ledger.

One detail matters: define explicit FX-risk targets in writing. In the IMF working-paper context, adopting a strategy with well-defined FX-risk targets is described as a critical element. That point is not specific to platform payouts, but it still carries: clear targets help teams judge whether a forward contract, multi-currency account, or flow matching is reducing the right exposure.

Disciplined handling of currency risk can improve visibility and control when execution is consistent. When FX is unmanaged, the downside is straightforward: unpredictable costs, slower settlements, and harder reconciliation. So if you need one next move, make it operational: publish the exposure map, stand up the review pack, and refuse new hedge complexity until both are stable.

Frequently Asked Questions

What are the three types of FX risk platform operators must track first?

Start with transaction risk, translation risk, and economic risk. The source material describes these as the three main FX risk types: transaction risk affects individual payments, translation risk can affect financial reporting, and economic risk affects long-term value and competitiveness. One source also mentions a less-common fourth type, jurisdiction risk.

How is transaction risk different from translation risk in a payout-heavy marketplace platform?

Transaction risk sits on actual payment activity and affects individual payments. Translation risk is different because it can show up when foreign-currency balances or results are converted for reporting, even if no cash moved that day.

When should we use a forward contract instead of a currency option?

The evidence here supports forward contracts and broader hedging strategies as mitigation tools, but it does not provide a fixed rule for choosing a forward over an option. Treat that decision as context-specific, and document the exposure and timing assumptions behind the instrument choice.

What is a natural hedge for cross-border payments, and when is it enough?

For a platform operator, that generally means aligning inflows and outflows in the same currency to reduce conversion exposure.

How often should a platform review FX exposure and hedge performance?

There is no universal review cadence in the evidence, so avoid treating weekly or monthly reviews as a fixed rule. Set a written cadence that fits your payout profile and exposure, then revisit it when volumes, corridors, or hedge behavior change.

Which controls are mandatory before scaling payout batches across new currency corridors?

The source set does not provide a universal mandatory checklist, so do not treat any generic list as complete. It does include AML guidance for remittance service providers as a risk-management tool, and the rest of the control design should be tailored to your operating model.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- acquisition.gov/afars/chapter-5-definitionstrusted

- bis.org/publ/bcbs229.pdftrusted

- bis.org/publ/bcbs144.pdftrusted

- cbp.gov/sites/default/files/documents/C-TPAT%27s%20F...trusted

- dodcio.defense.gov/Portals/0/Documents/CMMC/AssessmentGuideL2.pdftrusted

- eba.europa.eu/sites/default/files/document_library/Publica...trusted

- ecfr.gov/current/title-12/chapter-II/subchapter-A/par...trusted

- fda.gov/media/166672/downloadtrusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

How Platforms Are Reshaping Foreign Exchange in 2026

Treat Foreign Exchange (FX) as an early product and operations decision, not a setting you clean up after launch. Global standard-setters still describe [cross-border payments](https://www.fsb.org/work-of-the-fsb/financial-innovation-and-structural-change/cross-border-payments) through the same four frictions: high costs, low speed, limited access, and insufficient transparency. If your platform pays people or businesses across borders, those frictions show up in user pricing, payout timing, and operational handling.

IRS Form 1042-S for Platform Operators: How to Report and Withhold on Foreign Contractor Payments

If you own compliance, legal, finance, or risk for a platform paying foreign contractors, sellers, or creators, you may need to make **Form 1042-S** operational. That means clear decisions, reliable checks, and escalation points your team can apply and defend.

FATCA Compliance for Marketplace Platforms: Identifying and Reporting Foreign Account Holders

For marketplace teams handling cross-border payouts, FATCA work is mostly a control-design problem. You need to decide what to implement first, what evidence to keep, and what to escalate before a payout creates avoidable reporting or withholding risk. The practical question is not whether FATCA exists, but which controls actually reduce reporting errors and potential 30% withholding outcomes.