Quick Answer

Marketplace platforms should start FATCA compliance with valid W-9 or W-8BEN collection, clear account-holder classification, and payout holds when documentation is missing or unreliable. GIIN checks matter when a counterparty may be an FFI, and FATCA Registration System or IDES controls matter only if the facts create a real reporting path. This sequence reduces reporting errors and potential 30% withholding exposure.

How Marketplace Platforms Handle FATCA Review and Reporting#

For marketplace teams handling cross-border payouts, FATCA work is mostly a control-design problem. You need to decide what to implement first, what evidence to keep, and what to escalate before a payout creates avoidable reporting or withholding risk. The practical question is not whether FATCA exists, but which controls actually reduce reporting errors and potential 30% withholding outcomes.

FATCA, enacted in 2010, functions as both a reporting and withholding regime. Certain foreign entities report foreign assets held by U.S. account holders or face withholding on withholdable payments. Chapter 4 withholding-agent scope is broad and can include a U.S. or foreign person with control, receipt, custody, disposal, or payment of a withholdable payment. But not every cross-border payout is automatically a withholdable payment, so payment type and source still need case-level review.

This article ranks practical control options, not abstract theory. The goal is to help compliance, legal, finance, and risk owners reduce surprises on withholdable payments without building heavy process where reporting outcomes do not change.

- Documentation first

Start with records that establish the payee's tax posture. Form W-9 provides a correct TIN to a requester that must file an IRS information return, while Form W-8BEN is provided by a foreign beneficial owner to a withholding agent or payer. If you cannot show current form status and change dates, your control quality is already weak.

- Classification before payout

Separate FATCA-relevant classification from generic KYC so the team can explain why a seller, contractor, or institutional counterparty followed a specific path. FATCA decisions depend on U.S. account-holder reporting and foreign-entity status, not identity checks alone. Clear classification logic reduces ad hoc decisions that are hard to defend later.

- Reporting and withholding readiness where it applies

Form collection alone is not enough if reporting or transmission duties are triggered. FATCA operations can involve the FATCA Registration System and IDES for electronic transmission, and Form 8966 is used to report certain U.S. accounts and certain substantial U.S. owners of passive NFFEs. Build this capability when the facts support it, not as a default everywhere.

A quick operator check is to sample one passed payout case and one failed case. Confirm the file shows current W-9 or W-8BEN status, the classification decision, and an escalation owner. A failure mode to watch for is storing the form but not the decision trail. That leaves finance with payout risk and legal reconstructing facts later.

Choose the right FATCA control depth before you build#

Choose the lightest control set your facts support, but do not confuse low payout volume with low FATCA risk. If you cannot show account-holder classification evidence, current Form W-9 or Form W-8BEN status, and a named escalation owner, you are likely not operationally FATCA-ready for IRS-facing review.

Use this list if you own payout onboarding, tax documentation, or reporting operations where a U.S. account-holder question can change payout treatment. Do not use it as a substitute for legal advice on treaty position, FFI/NFFE classification, or host-country interpretation issues.

- Documentation gate only

Require a valid Form W-9 or Form W-8BEN before payout activation. This is the fastest control depth when the immediate gap is missing forms, but forms alone do not establish full FATCA readiness. Risk to watch: weak traceability. The form is stored, but the file cannot show status-change timing, reviewer ownership, or why payout proceeded.

- Documentation plus classification evidence

Add a distinct FATCA classification step so the file shows why a person or entity followed a specific path. Under 26 CFR 1.1471-5, account-holder treatment is tied to the listed or identified holder or owner, not an internal shortcut label. Treat this as a practical minimum when you need reporting readiness and audit traceability without a full reporting buildout.

- Institution-risk verification

Use this when a counterparty may be an FFI rather than a typical seller or contractor. Add a real verification checkpoint: capture and validate the 19-character GIIN, then recheck against the IRS FFI list, which is updated on the first day of each month. A one-time GIIN check is a weak control because registration status can change.

- Reporting execution readiness

Build this only when the facts indicate actual FATCA reporting operations. The differentiator is execution capability: FATCA Registration System status, IDES enrollment, digital certificate readiness, and IGA-dependent transmission steps. If the issue is treaty interpretation or Form 8966 preparation, escalate to tax or legal early because IDES support does not answer tax-law questions.

Before adding depth, run one approved case and one blocked case and confirm each file shows document status, classification basis, GIIN evidence if relevant, and escalation ownership.

If you want a deeper dive, read FATCA Reporting for Platform Operators: When Foreign Accounts Trigger US Obligations.

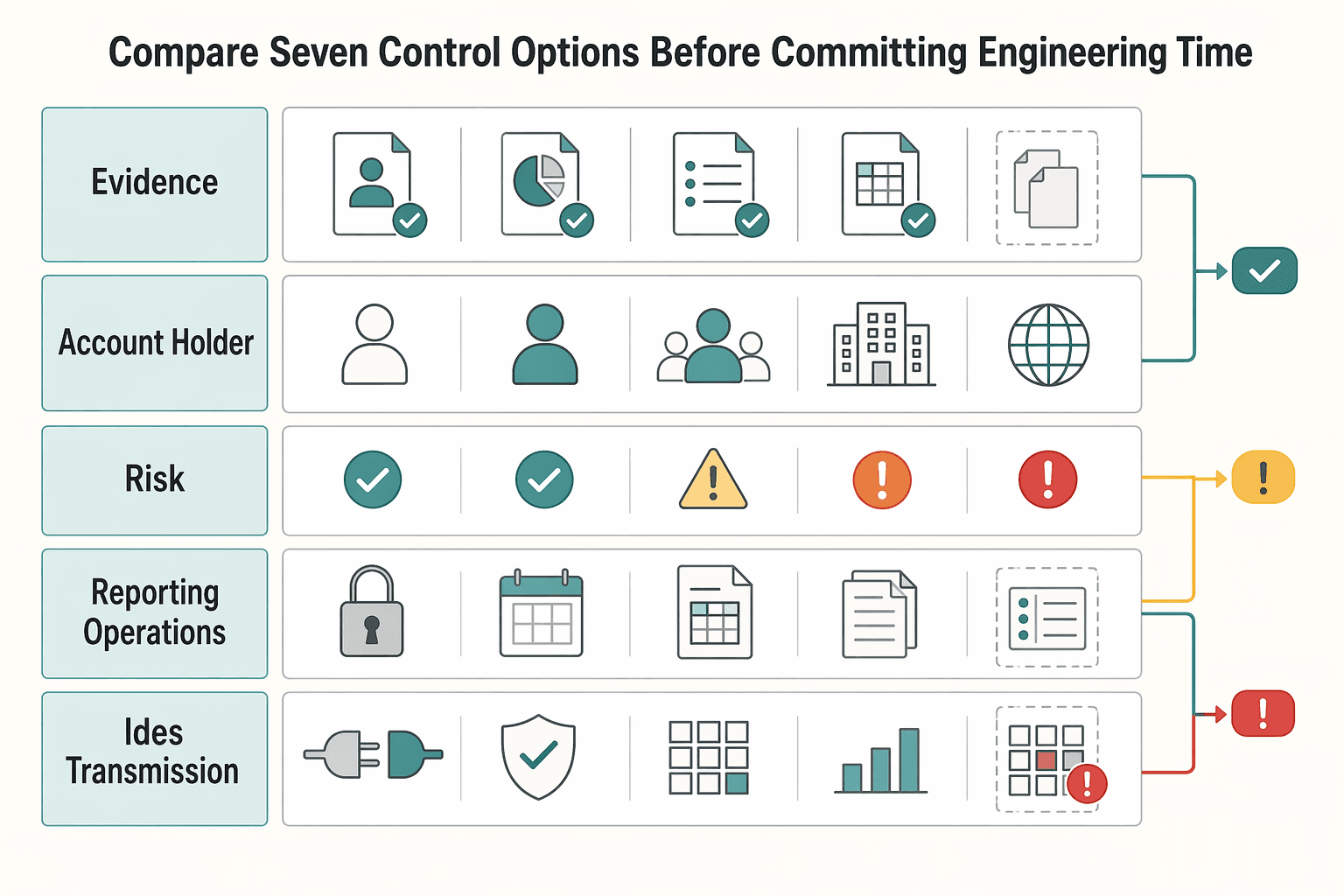

Compare the seven control options before committing engineering time#

Start with the controls that reduce withholding exposure fastest: documentation, classification, and payout holds for unresolved status. Add FATCA Registration System and IDES controls when your facts show a real reporting execution need.

| Option name | Best for | Required hard artifacts | Key pros | Key cons | Trigger to escalate to tax/legal |

|---|---|---|---|---|---|

| Onboarding documentation gate | Mixed U.S. and non-U.S. individual sellers with missing tax forms | Valid Form W-9 for U.S. persons, valid Form W-8BEN for foreign individuals, form status record, payout activation block | Fastest way to close basic documentation gaps | Can slow onboarding and create exception queues | You cannot map the person cleanly to a W-9 or W-8BEN path, or facts point to an entity case |

| Account-holder classification before payout eligibility | Teams that cannot explain why a holder followed a U.S., foreign individual, FFI, or NFFE path | Classification decision record, reviewer or rule source, linked form state, escalation owner | Makes FATCA treatment auditable instead of implicit | Ambiguous cases still require policy ownership and human review | Possible FFI or NFFE status, or unresolved substantial U.S. owner questions |

| GIIN verification for institution risk | Counterparties that may be financial institutions | 19-character GIIN, IRS FFI list result, verification date, recheck cadence | Concrete verification point for FFI-related withholding decisions | Weak if done once and never refreshed | GIIN missing, not on the IRS FFI list, or inconsistent with counterparty facts |

| Reporting operations readiness | Teams with documentation in place but no proven reporting path | FATCA Registration System status, ownership, certification lifecycle record, transmission readiness checklist | Establishes accountability before filing pressure | Easy to overbuild when reporting scope is unclear | Unclear whether your platform is acting in a reporting role or withholding-agent role for the flow |

| IDES transmission readiness | Teams near live FATCA transmission | IDES readiness evidence, access or certificate readiness, failed-handoff exception log | Turns reporting into an operational process | Heavier operating burden than documentation controls | Filing responsibility, transmission format, or transmission routing is unclear |

| Withholding-risk controls for stale or missing documentation | Finance and risk teams managing payout-release decisions | Missing or invalid W-9 or W-8BEN status, payout hold rule, remediation timer, owner assignment | Directly reduces release risk when status drives treatment | Overly strict holds can disrupt valid payouts | Possible Chapter 4 withholding-agent posture without confirmed status or documentation treatment |

| Escalation matrix for edge cases | Ops teams that need explicit stop points | Trigger list, required evidence pack, named tax or legal owner, decision SLA | Prevents silent acceptance of unresolved risk | Too many triggers slow throughput, too few leave risk unowned | Unresolved U.S. account-holder signal, FFI vs NFFE ambiguity, or conflict between documentation and business facts |

A few checks do most of the work. Form W-9 is used to provide a correct TIN for information return reporting, so your file should show which version was active when payout was approved. Form W-8BEN is for foreign individuals establishing foreign status in a U.S. withholding context, so do not use it as a catch-all for entity cases.

For institution-risk paths, GIIN evidence should be durable. Store the 19-character GIIN, the IRS FFI list result, and the lookup date, then revalidate on the IRS monthly list cycle, updated on the first day of each month. A one-time onboarding check is weak if registration status later changes.

For reporting rails, apply the same standard. The FATCA Registration System supports registration and ongoing certification lifecycle actions, and IDES is the transmission channel for FATCA data to the IRS. If ownership, access, or failed-handoff handling is unclear, reporting readiness is not established.

Recommended sequence: implement the first three rows first unless you already know live FATCA transmission is required. That order closes the fastest gaps tied to Chapter 4 outcomes, including potential 30% withholding exposure when status or documentation conditions are not met, before heavier reporting and governance buildout.

Before you lock scope, map each control to concrete payout policy gates, status visibility, and audit-traceable events in Gruv Docs.

Best option 1 onboarding documentation gate with W-9 and W-8BEN#

For mixed U.S. taxpayer and non-U.S. individual onboarding, ship this control first. Consider blocking payout activation until the right baseline form is complete. A hard gate around Form W-9 and Form W-8BEN can close documentation gaps early and leave a cleaner record for later FATCA decisions.

Form W-9 is used to provide the correct TIN to the person required to file an IRS information return. Form W-8BEN is used by a foreign individual to establish foreign status in a U.S. withholding or reporting context and is provided to the withholding agent or payer when requested. That makes this gate a practical first control for marketplaces onboarding freelancers, creators, and sellers.

Why this option works early#

This gate standardizes the first decision branch before money moves: U.S. person path or foreign individual path. When form status is explicit before payout eligibility, finance and compliance teams do not have to reconstruct documentation logic after payouts begin.

It also improves auditability. Your record should show which form state was active when payout was enabled, who or what changed status, and when that change happened.

The setup that actually holds up#

The minimum viable gate is more than "upload a form." Tie payout activation to a clear documentation state.

| Path | Minimum document state before payout | Red flag that should stop the flow |

|---|---|---|

| U.S. taxpayer | Valid Form W-9 on file | Missing TIN, unreadable form, or form not linked to the approved payee record |

| Foreign individual | Valid Form W-8BEN on file | User is clearly acting as an entity, or form details conflict with account facts |

| Foreign entity signal | Do not accept W-8BEN as the answer | Route for review because entity cases may require Form W-8BEN-E |

Store masked form data in operational views, and log status events such as requested, received, validated, rejected, expired if applicable, and payout enabled. If that event chain is missing, the gate is weaker than it looks.

Where teams get into trouble#

The biggest error is treating Form W-8BEN as a catch-all for every non-U.S. payee. It is for foreign individuals, so entity signals should trigger review instead of being forced through the individual path.

The second error is adding friction without clear exceptions. If rejection reasons are vague, support queues can grow and manual side-channel exceptions can undo the control. Use a short fixed reject-reason set, and require replacement documentation on the record before lifting holds.

This gate improves documentation hygiene, but it does not by itself determine whether your platform is a Chapter 4 withholding agent. That depends on payment-control facts. Wrong or missing documentation can still raise exposure quickly. In certain undocumented foreign-entity U.S.-source payment scenarios, that can include 30% withholding, which is separate from 24 percent backup withholding rules.

If you implement one rule, make it this: no payout activation until the minimum documentation state is complete, with automatic escalation when the facts indicate "foreign entity" rather than "foreign individual."

Best option 2 account holder classification before payout eligibility#

If you run a separate FATCA-related review before payout eligibility, treat it as an internal control choice, not an IRS-defined workflow. If your team cannot explain why a case stayed in ordinary onboarding versus enhanced review, record that gap and escalate.

This option is mainly about process clarity. The IRS excerpts in scope address taxpayer filing obligations, not marketplace KYC or payout-classification design.

Why this is worth doing#

A dedicated internal review can separate onboarding operations from personal tax filing obligations. The IRS says certain U.S. taxpayers with foreign financial assets generally report using Form 8938, and that form is attached to the taxpayer's annual return.

The practical benefit is clearer boundaries: identify facts, document decisions, and escalate unclear cases without drifting into filing advice.

What the rule should actually do#

Keep the internal rule narrow and auditable. The IRS excerpts here confirm filing checkpoints, including Form 8938 obligations and Form 8938/FBAR separation, but they do not provide platform-specific payout decision criteria. When facts are ambiguous, escalate to tax or legal specialists.

Evidence to keep#

Keep a consistent minimum record for each internally reviewed case:

- trigger reason for moving out of standard onboarding

- facts reviewed, including user statements that raised possible FATCA relevance

- reviewer, decision date, and disposition

- reason payout was allowed, held, or escalated

- confirmation the team did not treat Form 8938 or FBAR as onboarding artifacts

That boundary matters because Form 8938 and FinCEN Form 114 (FBAR) are separate requirements, and some individuals may need both.

Where teams get this wrong#

The first mistake is turning IRS filing checkpoints into platform payout rules. The IRS says $50,000 is the general aggregate-value threshold for Form 8938 reportability, with higher thresholds in some cases, but that is a taxpayer filing threshold.

The second mistake is asking for the wrong document. Form 8938 belongs with the annual tax return, and if no income tax return is required for the year, Form 8938 is not required.

The stakes for individuals can be significant. The IRS cites a $10,000 penalty for failure to report on Form 8938, potential continued-failure penalties up to $50,000 after notification, and a 40 percent substantial understatement penalty in some cases. That is why ambiguous cases should be escalated rather than treated as routine onboarding.

If you adopt this option, keep one non-negotiable internal boundary: separate FATCA-related internal review from generic onboarding, and avoid treating IRS filing forms as payout-gating documents.

Best option 3 counterparty verification with GIIN checks when institution risk appears#

Use GIIN verification for flagged institutional counterparties, not for every business account. That keeps the control targeted and avoids treating FFI and NFFE paths as interchangeable.

Under FATCA, FFIs and certain NFFEs are within Chapter 4 withholding and reporting rules, so institutional status can change your risk decision in ways standard onboarding does not.

What to verify#

The core artifact is the Global Intermediary Identification Number, or GIIN. It is a 19-character identifier in the format XXXXXX.XXXXX.XX.XXX that entities use to identify themselves to withholding agents and tax administrators for FATCA reporting purposes.

For each flagged case, keep the step simple and auditable:

- collect legal name, claimed FATCA status, country, and GIIN if provided

- check the GIIN or legal name in the IRS FATCA FFI List Search and Download Tool

- record the exact search input, match result, search date, and reviewer

- if no match appears, classify the outcome as timing, scope/classification, or hold-and-escalate

The lookup method matters because the IRS tool supports search by legal name, GIIN, or country.

What counts as a strong control#

A strong control is not just "GIIN received." It confirms whether the entity appears on the IRS monthly FFI list when list inclusion is expected. The list is updated on the first day of each month, and inclusion generally reflects approved status at least 5 business days before month start.

That timing changes how you handle no-match results. If a counterparty says it just completed FATCA registration, a near-month-end no-match result is not enough on its own to treat the entity as noncompliant. Document the explanation, hold risk-sensitive actions if needed, and queue a recheck after the next monthly update.

Where teams get false comfort#

The first failure mode is a one-time GIIN check treated as permanent. The FFI list tool is useful, but ongoing relationships often warrant risk-based rechecks.

The second failure mode is forcing GIIN logic onto every foreign entity. IRS pages do not describe list scope in identical terms across all pages, and some entities may not map cleanly to a list expectation. If your team cannot determine whether the entity should appear on the list, escalate to tax or legal review instead of treating it as a simple failed check.

Recommendation#

Require GIIN evidence only when FFI status plausibly matters, log verification outcomes, and use a risk-based recheck cadence. If FFI versus NFFE status is unclear, pause the decision and escalate before treating GIIN verification as sufficient.

Related reading: How to Build a Currency Reserve Strategy for Marketplace Platforms Operating in Volatile Markets.

Best option 4 reporting operations readiness with registration and transmission controls#

Build this control when your team can collect documents but cannot reliably execute a FATCA filing end to end. The goal is operational readiness: a reporting obligation can move through the FATCA Registration System and IDES, then be remediated if transmission fails.

This option is strongest when a reporting path may exist but filing operations were deferred. If legal classification is still unresolved or filing events are rare, keep the process narrow and manual, but still assign owners and retain evidence.

What makes this option different#

The difference here is explicit ownership across two IRS dependencies. The FATCA Registration System is the IRS online account workflow for financial institutions to register, renew agreements, and complete and submit FATCA certifications. IDES is the secure web application used by FIs and host country tax authorities to transmit FATCA data to the IRS.

The practical readiness test is simple: can the correct entity move from registration-ready status to valid transmission, and handle a rejection without improvising?

Use this order of operations#

| Step | What to confirm | Evidence to retain | Common failure mode |

|---|---|---|---|

| Registration state check | Registration is current and, where applicable, tied to an IRS-issued GIIN or FATCA Entity ID before transmission work starts | Current registration record, named account owner, GIIN evidence, and date checked against the monthly IRS FFI list | Teams rely on an old GIIN value and do not recheck current status |

| Data readiness validation | Reporting data can populate required output, including Form 8966 fields where applicable, and file prep is FATCA XML v2.0 | Extract version, schema-validation result, sample output, field-mapping notes, and reviewer signoff | Unsupported format or incomplete data elements |

| Transmission rehearsal | Team can produce the encrypted package, use required credentials, and complete an IDES handoff in a controlled test | Rehearsal date, operator, certificate details, archive naming check, and outcome notes | Credential, certificate, or packaging issues appear late |

| Exception logging | Alert codes, failed handoffs, deleted transmissions, and retransmissions are logged with owner, cause, and resolution date | Alert-code log, corrected archive reference, retransmission record, and escalation notes | Ad hoc fixes with no audit trail or repeat-issue tracking |

The registration checkpoint should be current, not one-time. IRS guidance states a registered and compliant FI with a GIIN appears on the monthly IRS FFI list, and the list is updated on the first day of each month.

Operational details that break filings#

IDES transmission guidance assumes the filer already has an IRS-issued GIIN or FATCA Entity ID, so identity readiness sits upstream of transmission. If that is unresolved, transmission readiness is already incomplete.

Format controls matter too. IDES requires FATCA XML v2.0, and file naming is case sensitive. Variation in file name, extension, or format can cause transmission failure.

Before first live filing, and after material changes to schema generation, certificates, or ownership, run a controlled rehearsal of packaging and transmission. IRS does not prescribe a universal rehearsal cadence, so keep this proportional to your volume and risk.

Keep the evidence pack small but real#

Keep the evidence pack compact:

- registration owner, backup owner, and current access status for the FATCA Registration System and IDES

- current GIIN or FATCA Entity ID evidence where applicable, plus monthly FFI list check date

- schema-validation result confirming FATCA XML v2.0 output

- final archive naming check before submission

- certificate or key-pair expiry date, which are generally valid for one year

- alert-code log with correction and retransmission notes

Do not overbuild early if volume is low. Use disciplined access control, a compact evidence pack, and a manual exception log with clear ownership. If IDES marks a transmission deleted, treat it as not transmitted to IRS processing: review the alert code, correct the archive, and retransmit.

Keep escalation paths split. IDES customer support handles technical issues, but not tax-law interpretation or instructions to prepare Form 8966, so filing-position questions should go to tax or legal review.

Best option 5 withholding risk controls tied to unresolved documentation#

Use this control to stop payout release when tax documentation is missing, expired, or no longer reliable for withholding treatment. Build it if your team can detect bad document states but cannot yet stop or reroute a payment before a withholding error reaches the platform.

The decision should stay narrow: gate payouts only on document states that can change withholding outcomes, and keep reason codes separate. Withholding treatment can depend on whether a payment can be reliably associated with documentation you can rely on. If that association is unresolved, do not release the payment as if the file were clean.

Where the control actually matters#

| Trigger state | Why it matters | Recommended control response | Evidence to retain |

|---|---|---|---|

| No valid Form W-8BEN for a foreign individual beneficial owner on an amount subject to withholding | IRS instructions state the withholding agent may need to withhold 30% under chapters 3 and 4 if the form is not provided | Stop auto-release, assign an owner, and route for form remediation before release under prior status | Form request date, last valid form date, payee communication, reviewer decision |

| Form W-8BEN has a change in circumstances or is past its general validity horizon | A W-8BEN is generally valid through the last day of the third succeeding calendar year unless facts change sooner; the holder must notify the payer, withholding agent, or FFI within 30 days of a change | Open a timed remediation case and block release under the outdated form state until redocumentation is reviewed | Change trigger, notice date, timer start, replacement form, approval record |

| No usable Form W-9 or uncertified TIN in a Form 1099 reporting context | A properly completed and signed Form W-9 can be relied on to avoid backup withholding; certain reportable payments to U.S. persons can trigger 24% backup withholding | Do not route this as FATCA 30% exposure. Use a separate backup-withholding lane with its own hold reason and resolution steps | W-9 status, TIN issue flag, payment type, withholding decision, outreach log |

Build separate lanes, not one generic tax hold#

Treat missing Form W-9 and missing Form W-8BEN as different control paths. A W-9 issue points to backup withholding in applicable Form 1099 cases. A W-8BEN issue can point to chapter 3 or chapter 4 treatment, including the 30% rate if the form is not provided.

That separation matters because not every marketplace payout is automatically a FATCA withholdable payment. For chapter 4, withholdable payments are generally U.S.-source FDAP income. Before applying a rate, confirm the payment sits in a lane where withholding analysis is required.

What to verify before a payout is released#

At payout approval, confirm the active document type, review status, and whether the payment is still linked to documentation you can rely on. For Form W-8BEN, check both validity horizon and changed circumstances. For Form W-9, confirm a properly completed and signed form and the TIN path needed to avoid backup withholding where that regime applies.

Keep the evidence pack compact:

- current form type and status for the payee

- review date and reviewer name

- reason code for hold, release, or withholding treatment

- communication sent to the payee

- remediation due date and owner

- final disposition tied to the payment record

The failure mode to avoid#

The common failure is a blanket hold with unclear messaging, which drives support escalations and manual overrides. If you apply this control, make the reason explicit: expired Form W-8BEN, change in circumstances under review, or missing valid Form W-9 for reportable payment processing.

If your team cannot yet separate those states confidently, start with manual approval for exception cases instead of a full product block. That still reduces late surprises while avoiding silent release under unresolved documentation.

Best option 6 boundary controls between platform duties and individual tax filing#

Use this control when teams start treating platform FATCA operations as personal tax advice. Your platform should handle onboarding, classification, document collection, and any institution-side FATCA reporting steps it is responsible for where applicable, while user-level filing obligations stay with the user and their advisor.

Keep the boundary explicit because these are separate regimes. FATCA generally involves reporting by certain foreign institutions and certain other non-financial foreign entities on foreign assets held by U.S. account holders, while U.S. persons can also have separate reporting duties depending on value. Form 8938 is an IRS form for specified foreign financial assets, with a commonly referenced baseline threshold of $50,000 for certain U.S. taxpayers, and FBAR is FinCEN Form 114, which can apply when aggregate foreign financial accounts exceed $10,000 at any time during the calendar year.

What the control should say#

Publish one internal decision note used by support, compliance, and product:

- Platform scope: collect and review platform tax documents, and retain platform reporting evidence.

- User scope: personal filing questions about Form 8938 and FBAR remain user-side, with advisor escalation as needed.

- Escalation line: explain the difference at a high level, but do not decide whether a specific user must file.

Keep two statements fixed in help content: Form 8938 does not replace FBAR, and FBAR is filed with FinCEN, not with the IRS. If asked who must file, state that some people may need Form 8938, FBAR, or both, depending on their situation.

Verification and failure mode#

Review help-center content, macros, and sampled tickets for language that implies a personal filing conclusion. Examples include "you do not need FBAR" or "our FATCA form covers your Form 8938 requirement." Retain an evidence pack with the approved decision note, current support language, owner signoff, and ticket examples showing advisor escalation.

The common failure is answering a personal filing question as if platform documentation settles it. If that appears, tighten scripts and route users to general education such as A guide to the Foreign Account Tax Compliance Act (FATCA) for individuals, not platform-specific determinations. For additional background, see FBAR and FATCA Reporting for US Expats.

Best option 7 escalation matrix for legal and tax edge cases#

Use an escalation matrix to define clear stop points for FATCA edge cases so operations does not make legal or tax determinations by default. In practice, a short matrix can reduce silent risk acceptance and give legal or tax owners a consistent evidence pack for decisions.

This control works when ops can gather documents and flag inconsistencies, but cannot resolve entity-classification disputes, jurisdiction conflicts, or ambiguous U.S. account-holder signals. The tradeoff is throughput versus exposure: too many triggers slow reviews, too few leave risk unowned.

Where ops should stop#

Escalate only where a wrong answer is costlier than a pause. Missing or unresolved entity documentation is one of those cases because U.S. withholding agents may need to withhold 30% on certain U.S. source payments to foreign entities they cannot document.

Escalate NFFE classification ambiguity, especially when facts suggest a passive NFFE and possible substantial U.S. owners. Form 8966 scope includes substantial U.S. owners of passive NFFEs, so this should not be resolved by ops guesswork.

Escalate unresolved U.S. indicia when account facts change and valid self-certification of U.S. status is not obtained. In qualifying Model 2 IGA situations, unresolved indicia can move to the pooled reporting category for recalcitrant account holders with U.S. indicia.

A matrix that is worth maintaining#

Keep the matrix short enough to be used. Four rows can cover core FATCA edge cases.

| Trigger | Primary owner | Required evidence | Decision timing rule |

|---|---|---|---|

| Missing or contradictory entity documentation with payout pending | Tax or legal, with finance copied if payment release is affected | Collected tax form status, onboarding notes, payment type, outreach log, and reason documentation remains unresolved | Before payout release where withholding exposure could attach |

| Passive NFFE ambiguity or possible substantial U.S. owner not resolved by onboarding review | Tax counsel or internal tax lead | Entity self-certification, ownership information provided, beneficial owner details on file, reviewer notes on why passive or active status is unclear | Before classification is finalized and before any related Form 8966 reporting path is set |

| U.S. indicia present but no valid self-certification obtained after facts changed | Tax lead first, legal if local-law issues block collection | Indicia found, self-certification requests, account history, prior status, and current reviewer summary | Before reporting treatment is chosen for the account |

| Jurisdiction conflict involving Model 1 IGA, Model 2 IGA, or local-law restrictions | Legal with tax input | Jurisdiction, applicable IGA route, local-law concern, reporting channel assumption, and why ops cannot complete the step without interpretation | Before deciding whether reporting goes through local authority, direct IRS route, or a hold or remediation path |

The jurisdiction row is critical. A Model 1 IGA route generally means a reporting Model 1 FFI reports certain U.S. reportable account information through its local tax authority, while a Model 2 route requires IRS registration and compliance with an FFI agreement. If definitions differ under an applicable IGA or domestic-law context, treat it as a legal or tax interpretation issue.

Operator details that prevent weak escalations#

Require one reviewer sentence that states the unresolved question, then attach the raw facts that support it. Escalations with screenshots but no clear unresolved question can slow legal and tax review.

Add one recurring GIIN check for institution cases. When an entity is treated as an FFI and provides a GIIN, recheck status in the FATCA FFI List Search and Download Tool on the first day of each month. Use that as a control point, not proof of full FATCA compliance across due diligence, reporting, and withholding.

Verification and the common failure mode#

Review closed escalations monthly for three checks: trigger accuracy, evidence-pack completeness, and named decision owner. If routing rationale is not reconstructable, the matrix is not operational.

A common failure is routing tax-law interpretation to the wrong channel. IDES is for secure FATCA data transmission, but IDES support does not answer tax-law questions or provide Form 8966 preparation advice. Another failure is treating temporary relief as permanent. Notice 2024-78 provides conditional, time-bounded Model 1 TIN-missing relief for 2025, 2026, and 2027. It is tied to significant non-compliance concepts under Article 5(2) or 5(3) of the relevant IGA. If a case depends on that relief, escalate and document the basis.

For related context, see Form 3520 Playbook: A 3-Step Framework for Foreign Trust Transactions and Foreign Gift Reporting.

Sequence implementation so controls survive real payout volume#

Build controls in risk order: first prevent payouts with unresolved documentation, then verify institution status, then harden reporting transmission only where your reporting route requires it.

Phase 1#

Start by enforcing intake checks for the applicable form, with payout gated when the artifact is missing or unusable. For U.S. persons, Form W-9 is used to provide the correct TIN. For foreign persons, Form W-8BEN is provided to the withholding agent or payer when requested.

Make form handling stateful and auditable, not just a file upload. Track statuses such as requested, received, failed review, and approved, and log each status change with reviewer and rationale.

Phase 2#

Next, add GIIN verification and an FFI/NFFE escalation path for institution exposure. If an entity is treated as an FFI and provides a GIIN, verify it in the IRS FFI List Search and Download Tool instead of relying on the submitted value.

Use the GIIN format and list cadence as control inputs: the GIIN is a 19-character identifier, and the IRS posts an updated FFI list on the first day of each month. Keep recurring checks for relevant institution cases, and route unresolved FFI/NFFE classification questions to escalation before payout or reporting treatment is finalized.

Phase 3#

Harden reporting operations only after intake and institution controls are stable. Confirm whether IRS registration and IDES apply to your entity type and reporting route, then test transmission readiness before live filing periods.

IDES is the IRS secure transmission channel for FATCA data, using FATCA XML schema-formatted reports. As an internal quality checkpoint, sample both passed and failed cases and verify evidence completeness, decision consistency, and audit traceability from intake through hold, approval, or escalation.

Conclusion#

A strong FATCA posture is usually the one you can defend clearly, not the one with the most moving parts. In practice, that means building only the controls you can explain, operate, and evidence later.

- Prioritize evidence over process volume.

Focus first on whether your team can reconstruct each decision: who reviewed the case, what documentation state was active, what decision was made, and when escalation happened. If that record is unclear later, more intake steps will not fix the core risk.

- Keep platform operations separate from individual filing obligations.

IRS guidance says certain U.S. taxpayers with financial assets outside the United States must generally report them on Form 8938, and that form is attached to the taxpayer's annual tax return. The IRS also states that Form 8938 and FinCEN Form 114 (FBAR) are separate requirements, and some individuals may need to file both. If a U.S. taxpayer does not have to file an income tax return for the year, they do not file Form 8938 for that year. In the same guidance, $50,000 is presented as a general reportability level, not a universal threshold for every filer scenario.

- Tighten controls where downside is documented.

IRS guidance says failure to report foreign financial assets on Form 8938 may trigger a $10,000 penalty, with additional exposure up to $50,000 after IRS notification, plus a 40 percent understatement penalty for certain underpayments tied to non-disclosed foreign financial assets. Criminal penalties may also apply. Use that documented risk to prioritize your sequence: resolve unclear facts, separate individual filing questions from platform operations, and escalate non-routine cases with a complete evidence pack.

Start with clear classification records, clean documentation history, and explicit escalation triggers. Tighten only where real cases and review findings show exposure.

If you want to pressure-test your FATCA control sequence against your current payout flow, talk with Gruv to confirm what is supported for your market and program.

Frequently Asked Questions

What does FATCA require from an online marketplace platform handling foreign account holders?

It depends on the platform's entity role and payment flow, so not every marketplace has the same direct reporting duty. A practical baseline is to collect and retain the right payee documentation, classify the account holder, and pause payouts when required tax documentation is missing or unusable. U.S. withholding agents may need to withhold 30% on certain U.S.-source payments to foreign entities they cannot document.

How is Form 8938 different from a platform’s FATCA reporting responsibilities?

Form 8938 is a taxpayer filing for specified foreign financial assets when reporting thresholds are met. The article notes a general threshold of $50,000, with higher thresholds in some cases. That is separate from a platform's onboarding, documentation, withholding, and institution-side FATCA reporting processes. Form 8938 also does not replace FBAR, and FinCEN Form 114 is not filed with the IRS.

When should a platform request Form W-9 versus Form W-8BEN?

Request Form W-9 when the payee is a U.S. person and you need the TIN and certifications. Request Form W-8BEN when the payee is a foreign beneficial owner and you are the withholding agent or payer requesting it. If status signals conflict, pause payout and escalate classification instead of switching forms ad hoc.

What is a GIIN, and when should teams use the FATCA FFI List Search and Download Tool?

A GIIN is a Global Intermediary Identification Number issued through FATCA registration. Use the FATCA FFI List Search and Download Tool when a counterparty may be an FFI and provides a GIIN. The tool supports lookup by legal name, GIIN, or country, and the IRS list is updated on the first day of each month.

When do FATCA Registration System and IDES become operational requirements rather than “nice to have” controls?

They become operational requirements when your entity type and reporting route place you on FATCA registration or transmission rails. The FATCA Registration System is the IRS web system financial institutions use to register under FATCA, and IDES is the electronic delivery point for FATCA data exchange with the United States. If your facts do not put you on that path, prioritize documentation intake and verification controls first.

What minimum controls reduce withholding surprises without overbuilding the process?

Start with core intake controls: collect the correct form at onboarding, pause payout activation when documentation is missing or fails review, and keep an auditable status trail with reviewer and rationale. Add GIIN verification when institution exposure appears instead of treating every foreign payee as an FFI case. This sequence closes the fastest gaps before heavier reporting operations are built.

Which situations should always be escalated to tax or legal counsel?

Escalate conflicting U.S. versus foreign status signals, unresolved FFI versus NFFE classification, unverifiable GIINs, and unclear FATCA Registration System or IDES applicability. These are judgment-heavy decisions that frontline operations should not improvise. Send counsel a compact evidence pack with the submitted Form W-9 or Form W-8BEN, relevant account facts, GIIN search results if any, reviewer notes, and payout history.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.

How to Respond to a Subpoena for Business Records

Move fast, but do not produce records on instinct. If you need to **respond to a subpoena for business records**, your immediate job is to control deadlines, preserve records, and make any later production defensible.

A US Expat's Guide to Investing in UCITS ETFs to Avoid PFIC Issues

The real problem is a two-system conflict. U.S. tax treatment can punish the wrong fund choice, while local product-access constraints can block the funds you want to buy in the first place. For **us expat ucits etfs**, the practical question is not "Which product is best?" It is "What can I access, report, and keep doing every year without guessing?" Use this four-part filter before any trade: