Quick Answer

Start by treating reserve policy as an operating control across Finance, Payments Ops, and Engineering, not a rate prediction exercise. Build corridor-level exposure maps, set a strict decision order, and tie each reserve move to approver, obligation, conversion terms, and payout release. Use firm quotes, stale-quote rejection, and fallback routes to manage execution risk. Then enforce ledger-first reconciliation with webhook inputs before releasing payout batches, and gate releases on required compliance and tax-document status.

Why Marketplace Platforms Need a Currency Reserve Strategy#

A useful reserve policy starts as an operating decision, not a market call. In marketplace payments, foreign exchange (FX) choices can affect how reliably teams convert funds, reconcile balances, and release payouts.

Step 1. Treat the problem as cross-functional from day one#

Do not leave this with finance alone or payments ops alone. The real work often cuts across finance, operations, and adjacent teams, and someone needs clear authority to make the final call when timing gets tight.

That matters because the currency market is broad, spanning spot activity and instruments like forwards, futures, and swaps. In practice, teams still need to translate those choices into funded payouts, ledger entries, and customer-facing timing.

If you are building a reserve approach for a marketplace in volatile markets, start with one practical question: what must stay reliable even when rates move fast or approvals slow down? Many teams prioritize payout continuity first, then align the rest of the operating choices around that.

Step 2. Decide the order of decisions before you debate tactics#

You will often get more value from a clear decision sequence than from an elaborate view on where rates are heading. Keep the sequence explicit so you do not optimize one step while critical dependencies are still unclear.

A useful checkpoint is whether any reserve move can be explained in one record without extra detective work. You should be able to show who approved it, what obligation it was meant to cover, what conversion terms were accepted, and which payout release depended on it. If that chain is missing, the issue is not market complexity. It is decision hygiene.

Step 3. Build for adaptation, not a single policy#

Controls, product coverage, and available routes can vary by market and by program, so treat this guide as a decision structure you adapt. The reserve approach for a platform paying out in a few stable corridors may not match the approach for one handling many currencies with uneven settlement timing. That is why this article stays operational: what to decide, in what order, and what evidence to keep.

One failure mode to keep in mind from the start is timing mismatch. Finance may think funds are ready to convert while ops is still waiting on reconciliation, or engineering may retry an event that ops assumed was final. When that happens, cross-functional reliability can degrade for operational reasons, not just market mechanics. The sections that follow focus on building a shared path to reduce that risk and tighten coordination.

What to prepare before you set reserve policy#

Set reserve policy only after you lock three basics: clear owners, a minimum evidence pack, and explicit stop authority. If one team can move reserves but no one can reliably pause payout batches when data conflicts, the policy will break under volatility.

Step 1: Name one working group and make authority explicit. Use one decision group across Treasury/Finance, Payments Ops, and Engineering. Document who approves reserve moves, who can halt payout batches, and the escalation backup when the primary owner is unavailable.

Step 2: Assemble a minimum evidence pack before you debate tactics. Start with corridor-level payout obligations, current Virtual Accounts balances, recent webhooks status/error logs, and your latest reconciliation view. Keep this pack current enough to support same-day decisions, or you will end up debating conversion timing on conflicting data.

Step 3: Define operating constraints up front. Write down which currencies must be supported, where liquidity must be available to fund payouts, and which compliance gates can block fund movement. Prioritize foreign-currency liquidity and shock absorption before optimization, and flag any corridor where delays are unacceptable.

Step 4: Turn recent pain points into test cases. List recent failures such as delayed payouts, stale quote rejects, reconciliation breaks, and manual override frequency. Use these as policy tests: if a proposed approach would not have prevented at least one recent incident, it is still too theoretical.

For a step-by-step walkthrough, see How to Build a Predictable Content Strategy for Your Agency.

Map exposure and obligations corridor by corridor#

Do not run reserve policy off a blended FX number. Map each corridor to the exact obligation, currency pair, and payout timing so decisions follow real payables.

Step 1 Build the map at obligation level, not monthly average level. For each corridor, track inflow currency, outflow currency, and payout timing together. A USD-in, GBP-out corridor with same-day payouts is a different reserve problem than USD-in, MXN-out with a two-day release window. If you average them, you can hide a near-term funding gap in one corridor while another looks overfunded.

Anchor each row to the payout file and ledger view. A practical checkpoint: every corridor should tie to a known payable amount, current available balance, and next release date. If those three items do not reconcile for upcoming cycles, do not optimize conversion timing yet.

Step 2 Separate liquidity risk from market risk. Classify each corridor into two decisions: what must be paid regardless of rates, and what can be timed. The first is liquidity risk; the second is market risk.

Also account for the quote-to-settlement gap, where exposure opens between rate commitment and settlement. One cited example shows Day 1 to Day 7 exposure: a 1.5-3% GBP/USD move on $8 million monthly volume can put $120,000 to $240,000 of margin at risk. You do not need the same profile to use the principle: if a corridor cannot tolerate timing drift, fund certainty first and optimize second.

Step 3 Add execution venue detail to the same map. Track where each corridor executes: bilateral trading with a provider or multilateral trading platforms. Then log your own execution evidence: quote timestamp, firm vs indicative quote, expiry, executed rate, and any re-quote or reject reason.

This keeps reserve decisions tied to observable execution behavior, not assumptions about venue quality.

Step 4 Use BIS market-structure context as a monitor, not a rulebook. Use the Bank for International Settlements (BIS) and the Triennial Central Bank Survey as market context, not as standalone policy inputs. Let your corridor obligations, timing windows, and execution results determine how much reserve to hold and where to place it.

Related reading: How to Create a Secure Backup Strategy for Your Freelance Business.

Set reserve objectives and governance rules your team can enforce#

Set objective order first, then enforce it with written triggers and approvals. Keep the sequence explicit: payout continuity first, margin protection second, optimization third. If payout reliability is already unstable, tighten execution windows and increase near-term liquidity coverage before adding hedge complexity.

Step 1 Write the objective order into policy. Define each objective in operational terms your Finance, Ops, and Engineering teams can apply the same way. If different teams classify the same corridor differently, the policy is still too vague to enforce.

Step 2 Define trigger rules using external context plus internal evidence. Treat Federal Reserve communications and CPI/PCE periods as context, not automatic commands. Change reserve behavior only when your internal signals also deteriorate (for example, more rejects, delays, settlement breaks, or manual overrides), and pair each trigger with a preset action and owner.

Step 3 Stabilize core execution before expanding complexity. If payout windows are being missed, do not rely on added hedge layers to fix operating gaps. Narrow quote-to-release timing, pause optional optimization, and require confirmed funding checks before non-routine reserve actions.

Step 4 Require a complete approval trail for exceptions. Every non-routine reserve action should have an audit-ready record: corridor, rationale, balances before/after, approvers, expiry, and post-event review. When legal or policy interpretation relies on Federal Register material, verify against official editions rather than treating prototype pages as final authority.

If you want a deeper dive, read A Guide to Pricing and Packaging for International Markets.

Choose reserve currencies hedging mix and execution channels#

Choose your reserve mix to match your objective order, then keep execution rules tight enough to enforce under stress. There is no universally superior model, so decide corridor by corridor where you want timing risk, operating effort, and conversion exposure to sit.

Step 1. Choose the reserve mix by corridor behavior, not preference#

| Policy choice | Payout predictability | Operational load | Conversion cost risk |

|---|---|---|---|

| Mostly USD reserve | Strong for USD obligations; non-USD payouts depend on conversion timing | Lower local-balance management | More exposure near release windows when conversion happens late |

| Corridor-local reserve | Strong where local payouts are frequent and timing-sensitive | Higher balance monitoring and rebalancing effort | More exposure in pre-funding and rebalancing decisions |

| Hybrid reserve | Balanced when you clearly define which corridors get local buffers | Medium to high, based on number of local pools | Exposure is split across pre-funding and top-ups |

Use a simple rule: keep local reserve where non-USD payouts are recurring and timing-sensitive; keep more USD where flows are less predictable and can run under tighter cutoffs.

Step 2. Keep hedging narrower than your team's monitoring capacity#

Use cash-flow hedging only where payout needs are forecastable enough to track. Use balance-sheet hedging only where foreign-currency assets or liabilities are material to your books. Use FX derivatives only when you can reliably monitor exposures, trade terms, settlement dates, roll/close decisions, and accounting treatment without fragile manual handoffs.

| Approach | Use when |

|---|---|

| Cash-flow hedging | Payout needs are forecastable enough to track |

| Balance-sheet hedging | Foreign-currency assets or liabilities are material to your books |

| FX derivatives | You can reliably monitor exposures, trade terms, settlement dates, roll/close decisions, and accounting treatment without fragile manual handoffs |

Step 3. Shift execution toward higher-confidence channels when visibility drops#

If quote quality degrades or venue reliability becomes less predictable, reduce discretionary routing and move flow to channels your team can monitor and escalate cleanly. When conditions are stable, keep routing diversified across available venues so one path does not become a single point of failure.

Treat market moves as context, not auto-trade instructions. In the cited market update, implied volatility was higher, 10-year U.S. Treasury yields were down 15 basis points, and two-year yields had fallen by nearly 40 basis points. Use that kind of repricing as a trigger to tighten controls and review execution logs, not to improvise reserve policy mid-cycle.

Step 4. Set non-negotiable execution rules#

- Require a firm quote for conversions tied to payout batches.

- Auto-reject stale quotes.

- Maintain a documented fallback route for each primary venue, with clear switch authority and evidence requirements.

If you want one operator rule to remember: when transparency drops, simplify.

Need the full breakdown? Read How to Choose a Presentation Currency for Financial Reports.

Implement conversions and payouts in the right order#

Use a strict operating sequence to reduce payout risk: confirm obligations, lock conversion terms, execute FX, post ledger events, then release payout batches. Treat this as an internal control pattern, not a sourced regulatory requirement.

| Order | Step | Control |

|---|---|---|

| 1 | Confirm obligations before FX | Freeze the batch inputs so payer, payee, currency, and amount are stable before you convert |

| 2 | Lock conversion terms to the batch | Tie each conversion to a specific batch or funding reference so allocation stays clear during reconciliation |

| 3 | Post ledger events before release | Treat the ledger as the source of truth, and reconcile asynchronous Virtual Accounts webhook events before funds move to available |

| 4 | Make retries safe and auditable | Use stable idempotency keys for conversion and payout calls so retries replay safely instead of creating duplicates |

Your verification checkpoint is end-to-end traceability: each payout file should map cleanly from internal request to provider reference to ledger posting to reconciliation export.

Related: Local Currency Payouts vs USD Payouts: What Contractors Prefer and What Platforms Should Offer.

Build compliance and tax gates into reserve movements#

Treat reserve availability as necessary but not sufficient: release cross-border payouts only when compliance and tax states are complete in your own policy model.

Step 1 Gate release on explicit compliance status. For higher-risk corridors, require a machine-readable status before a reserve-funded payout moves to releasable. Whether you track this through KYC/KYB/AML or equivalent controls, avoid "missing status" paths and fail closed when required checks are unresolved.

Step 2 Make incomplete tax profiles a visible hold state. Do not let tax-data gaps pass silently. If a payee profile is incomplete for the route you are using, place the payout in a controlled hold with a clear reason code so ops and finance can resolve it before funds are released.

Step 3 Separate payout gating from payee tax outcomes. Define required tax-document states during onboarding and carry them into payout decisioning and reporting workflows (including cases where Form 1099 may be relevant). Keep FEIE and FBAR in the right lane: FEIE eligibility includes conditions such as foreign earned income, a foreign tax home, and a physical presence route of 330 full days during any period of 12 consecutive months, and claiming FEIE still means filing a U.S. return reporting the income; FBAR is a FinCEN reporting framework for foreign bank and financial accounts.

Step 4 Protect sensitive fields while preserving auditability. Mask sensitive tax and identity values in ops views, encrypt records at rest, and log approvals and exceptions with user and timestamp metadata. A practical control is simple: no reserve-funded cross-border payout should be releasable unless both compliance status and tax-document status are present and readable by your workflow engine.

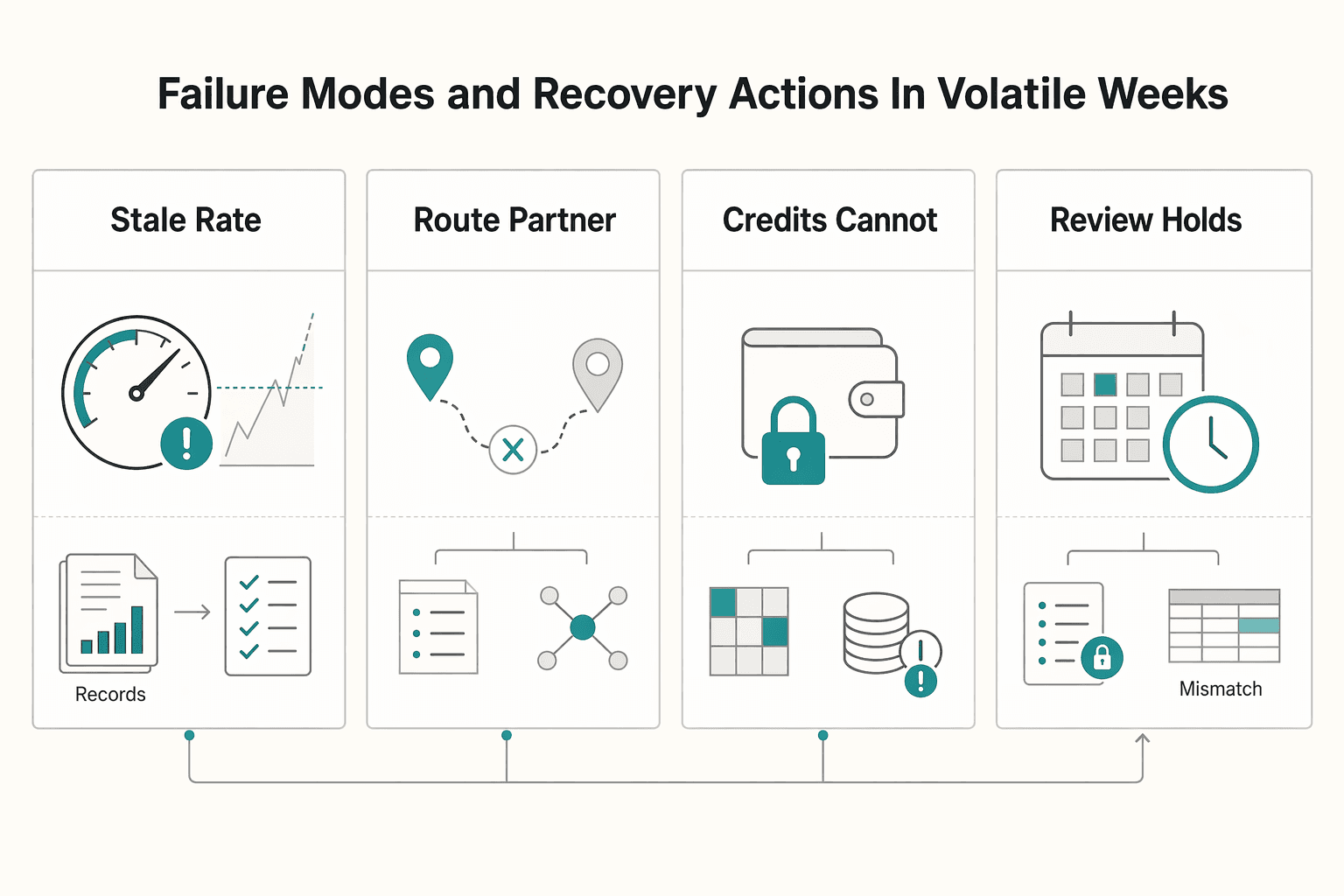

Failure modes and recovery actions in volatile weeks#

Volatile weeks usually break on timing gaps first. Protect payout continuity by tightening how you handle unsettled cash and delayed decisions, then calibrate controls to your own operating conditions.

| Failure mode | Recovery action | Keep visible or logged |

|---|---|---|

| Stale-rate rejects increase | Shorten decision time with your existing escalation path | Quote time and expiry |

| A route or partner becomes less reliable | Rebalance flow under your risk policy | Tighter temporary controls on larger conversions |

| Credits cannot be matched cleanly | Hold release | Clear exceptions before marking funds available |

| Review holds surge | Route cases through named escalation lanes | Reason, reviewer, timestamp, and supporting context in one log |

Step 1 Address quote-expiry spikes as a speed issue. If stale-rate rejects increase, treat it as approval-latency stress and shorten decision time with your existing escalation path. Keep quote time and expiry visible so approvals happen inside the usable window.

Step 2 Reduce route concentration when confidence drops. If a route or partner becomes less reliable, avoid pushing normal volume through it by default. Rebalance flow under your risk policy and apply tighter temporary controls on larger conversions until stability returns.

Step 3 Pause release when status signals and settlement timing diverge. If credits cannot be matched cleanly, hold release and clear exceptions before marking funds available. This is the same core risk seen in broader markets: a T+2 cycle is a two-day lag between execution and settlement, and that lag was cited as amplifying volatility in January 2021.

Step 4 Use documented compliance escalation, not ad hoc overrides. When review holds surge, route cases through named escalation lanes and keep a complete decision trail. Keep reason, reviewer, timestamp, and supporting context in one log so finance, compliance, and audit can reconstruct outcomes later.

No single checklist is definitive for every platform, so keep these controls explicit and adjust them to your institution's actual risk profile and operating constraints.

Put this into motion this quarter#

Use this as a six-action operating checklist for the quarter, with an owner, approval path, and verification point on every item.

-

Define objectives and owners first. Set priority order (payout continuity, then margin protection, then optimization) and assign accountable owners across Finance, Ops, and Engineering. Separate reserve-move approval from payout-release authority.

-

Build a corridor exposure map before tuning execution. For each corridor, capture inflow currency, outflow currency, payout timing, balance location, and whether the main risk is liquidity or market movement. Verify you can show the next payout obligation, required currency, and funding status.

-

Publish conversion rules in writing. Require firm quotes, define quote-validity windows, auto-reject stale quotes, and document fallback routing. If approval takes too long and a quote expires, reprice instead of overriding.

-

Gate payout release with reconciliation checkpoints. Treat the ledger as source of truth, and treat

webhooksas inputs rather than standalone release signals. Keep the chain auditable from request to provider reference to ledger posting to release decision, with idempotent conversion and payout retries. -

Enforce compliance and tax gates before scale-up. Define corridor/program release requirements and block release when required records are incomplete, including

KYC/KYB/AMLandW-8/W-9/VAT data where required. For exceptions, log approver, reason code, timestamp, and document status. -

Run one volatility drill and keep a recovery note. Simulate quote expiry, counterparty stress, and settlement delay. Document halt authority, reroute ownership, customer-status messaging, and reconciliation checks required before restart.

If you are also tightening funding buffers, pair this with How to Build a Float Management Strategy for Marketplace Platforms.

Frequently Asked Questions

What is a currency reserve strategy for marketplace platforms?

A marketplace-specific definition is not established by the available evidence here. What is supported is that market conditions can change, so reserve policy should be reviewed as conditions shift rather than treated as fixed.

How is a reserve strategy different from hedging in FX operations?

The available evidence here does not provide a documented boundary between reserve strategy and hedging. Any strict distinction should be treated as an internal policy choice unless supported by additional sourced material.

When should we hold local currency instead of USD for payouts?

Keep this as an internal risk and operations decision unless you have separate, validated support.

How do we set reserve levels without relying on arbitrary percentages?

Confirm reserve-sizing thresholds and timing rules with a qualified adviser before presenting them as authoritative.

What controls are non-negotiable before scaling cross-border payout volume?

A control baseline is not defined by the available evidence here. Treat any checklist as your internal operating standard unless it is supported by separate authoritative sources.

How do bilateral versus multilateral execution venues change FX outcomes?

The provided evidence does not quantify bilateral versus multilateral venue outcomes, so avoid claiming guaranteed pricing or risk results. A limited supported point is that ESMA's MiFID II review material discusses algorithmic trading and OTC trading as distinct topics, which supports evaluating venue structure directly rather than relying on a single quoted rate.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- congress.gov/crs-product/R48451trusted

- congress.gov/event/118th-congress/house-event/115803/texttrusted

- dni.gov/files/documents/Global%20Trends_2025%20Repor...trusted

- ecfr.gov/current/title-12/chapter-II/subchapter-A/par...trusted

- fdic.gov/news/board/2019/2019-08-20-notice-dis-a-fr.pdftrusted

- federalregister.gov/documents/2019/11/14/2019-22695/prohibitions...trusted

- federalreserve.gov/publications/files/trading.pdftrusted

- federalreserve.gov/publications/files/cbem-4000-202602.pdftrusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

SaaS International Pricing That Protects Cashflow First

If you are a freelancer or a small team selling software across borders, protect cashflow first. The first job is not maximizing conversion in every market. It is building an international pricing approach that works from quote to invoice to collection.

How to Build a Float Management Strategy for Marketplace Platforms

If you searched for **float management strategy marketplace platforms**, start by defining float correctly. Here, float means money-timing decisions in a marketplace context. It is not the schedule buffer used in critical path analysis, where teams talk about total float and similar timing slack. It is also not Float, the resource management software built around planning, scheduling, resources, and team capacity.

Local Currency Payouts vs USD Payouts for Contractor Platforms

USD versus local currency is not just a finance setting. For a platform, it changes compliance scope, recipient certainty, reconciliation effort, and how much engineering depth your payout layer needs. In practice, many teams avoid picking one currency forever. A common approach is to set corridor-level rules: use local currency where it is legally and operationally supported, and keep USD as a fallback where legal, coverage, or operational constraints are still real.