Quick Answer

Set corridor-level defaults, not one global rule: use local currency where wage-currency legality, rail coverage, and quote controls are verified, and keep USD fallback where they are not. The decision should pass three checks before rollout: expected amount shown before confirmation, status visibility after initiation, and ledger journals that let Finance Ops explain sent versus received amounts without manual reconstruction.

How to evaluate local currency vs USD payouts#

USD versus local currency is not just a finance setting. For a platform, it changes compliance scope, recipient certainty, reconciliation effort, and how much engineering depth your payout layer needs. In practice, many teams avoid picking one currency forever. A common approach is to set corridor-level rules: use local currency where it is legally and operationally supported, and keep USD as a fallback where legal, coverage, or operational constraints are still real.

The first decision point is not preference. It is jurisdiction. Local labor laws govern wage currency requirements, so before you debate FX or contractor experience, you need to confirm whether paying in USD is appropriate for the worker and country involved. After that, the comparison becomes operational. Deel's November 04, 2025 guidance points to four factors that matter here: currency stability, legal requirements, operational efficiency, and your team's geographic distribution.

That is why this choice belongs to product, Finance Ops, compliance, and engineering together. Currency choice can affect payroll costs, compliance requirements, recipient satisfaction, and vendor relationships. On the platform side, those same pressures show up as payout support volume, exception handling, and finance rework. If your provider can handle multi-currency payments, local rails, and international compliance requirements, local-currency defaults become a realistic product option. If not, USD may stay necessary longer than the team wants.

The infrastructure question is easy to underestimate. A marketplace payout API becomes critical as you scale. It is the automated connection that lets your marketplace communicate with bank systems for payouts. That matters because the common failure mode is not theoretical FX strategy. It is trying to support cross-border variation with manual payout uploads, then discovering those uploads become time-consuming and error-prone as volume rises. If you are still relying on manual files for key corridors, treat broad local-currency coverage as conditional, not launch-ready.

There is a cost argument for local currency, but use it carefully. Vendor guidance says local-currency payments can reduce conversion fees by 1-5%. That is a useful signal, not an outcome you should promise internally. The more durable reason to care is operational ownership: who absorbs FX friction, who explains net receipt differences, and who cleans up exceptions when bank, compliance, or routing details do not line up.

The goal of this guide is practical. You need policy rules by corridor, a rollout order, clear control points, and a short list of measurable outcomes. If you can verify legal fit, payout-rail support, and reconciliation readiness, local-first may be the stronger direction in those corridors. If you cannot, keep USD as an explicit fallback and expand corridor by corridor instead of overcommitting early.

At a glance comparison of USD and local currency payouts#

If you can operationally support local currency, it can improve recipient certainty. Keep USD as an explicit fallback where your controls or corridor support are not yet strong enough.

| Evaluation point | USD payouts | Local currency payouts | What your team should verify |

|---|---|---|---|

| Recipient certainty | Lower when conversion happens after receipt; final local amount may differ from expectations. | Higher when payout is confirmed in the recipient currency before release. | In your payout platform, show payout currency and expected received amount before confirmation. |

| Conversion burden | Usually pushed to the contractor, receiving bank, or both. | Usually pushed to the platform and payout provider. | Define who owns FX execution and who answers net-receipt disputes. |

| Reconciliation complexity | Often heavier on rails that involve manual reconciliation. | Can be simpler if FX and fee data are returned in structured form. | Keep ledger journals separated by principal, provider fees, FX impact, and reversals. |

| Common failure modes | Wire-fee deductions, intermediary deductions, banking-hours delays, and legacy settlement windows that can run 3-5 days. | Wrong displayed local amount, silent fallback behavior, or unclear FX treatment. | Give support one view with payout ID, rate used, timestamp, bank response, and fee lines. |

| Support-ticket risk | Higher when expected-vs-received disputes repeat. | Lower only when quoted amount and payout status are visible. | Tag disputes by corridor: amount mismatch, missing funds, delayed settlement. |

| FX quote handling | Less controlled when conversion is done downstream. | More controlled only when a usable pre-confirmation quote is available. | Verify whether pre-confirmation rates are shown and retained for audit. |

| Stale-quote rejection | Less central if you are not promising a local amount. | Important if you are promising one. | If you cannot expire and requote cleanly, avoid promising precise local outcomes. |

| Expected-vs-received visibility | Needs clear notice that receiving banks may convert at receipt. | Needs clear local amount plus status trail. | Check both recipient UI and support tooling, not only API docs. |

| Provider fee exposure | Wire transfers are described at $15-45 per payment with 2-4% FX markups; some digital platforms are described at 3-5% per transaction. | Can reduce recipient-side conversion friction, but provider and FX costs still apply. | Compare corridor-level all-in cost, not only headline payout fees. |

| Downstream finance rework | More cleanup when bank or intermediary deductions alter net receipt. | Lower only when conversion and fee details post cleanly into finance records. | Test exports for paid, failed, and reversed payouts before rollout. |

| API-first infrastructure | File-based workflows may work early, then become error-prone at volume. | API support becomes more important as currency logic grows. | Confirm payout API coverage and workflow automation support. |

| Webhooks and payout batches | Core for both models; without events and batch support, teams chase status manually. | Same, with higher expectation pressure when local amounts are shown upfront. | Score status events, retry behavior, and batch-level reconciliation output. |

Where the real difference shows up#

The core difference is who owns FX uncertainty. In USD flows, uncertainty often lands on the contractor and receiving bank. In local-currency flows, it shifts to your platform and provider. That can improve trust, but only when amount, currency, and settlement status are transparent.

Your finance team should also evaluate the full cost stack, not just payout-line pricing. Treat the ranges here as warning signals, not universal outcomes: wire transfers are described as $15-45 per payment, 3-5 day settlement, and 2-4% FX markups, while some digital payment platforms are described as 3-5% per transaction with multi-day settlement windows.

How to score feasibility before changing the default#

Before changing defaults, test top corridors with real payout samples and compare three values: promised amount, sent amount, and received amount. If finance cannot explain the differences line by line, or support cannot quickly retrieve rate, fee, and payout status, your controls are not ready for stronger local-currency promises.

The main risk is false certainty. If you display a local amount without dependable quote handling, status visibility, and clean batch reconciliation, keep USD fallback explicit and message bank-side conversion clearly. Promote local-currency defaults only on corridors that pass those checks in production.

Related: Crypto Payouts for Contractors: USDC vs. USDT: What Platforms Must Know.

What contractors actually prefer and what is still unknown#

Set preference policy as a product measurement problem by corridor, not as an industry fact.

Be strict about the evidence. Aite Group may appear in vendor marketing, but verify its methodology independently before citing it as proof of cross-platform contractor preference. Confirm with neutral industry benchmarks that payout-currency behavior data is actually covered before relying on any single source. Neutral benchmark data on contractor preference is still missing.

Given that gap, capture the inputs that actually drive preference in onboarding and payout settings:

| Input to capture | Why it matters | What to verify |

|---|---|---|

| Preferred payout currency | Determines whether the recipient expects a local amount up front or accepts USD | Confirm the UI selection matches the payout instruction sent to the provider |

| Bank country and account constraints | Accounts in the same country can have different currency/rail constraints | Verify whether the receiving account accepts USD without forced conversion or rejection |

| Sensitivity to payout timing | Some recipients prioritize speed; others prioritize amount certainty | Capture whether they prioritize speed, exact amount received, or lower fees |

Operationally, store a timestamped record of selected currency, bank-country details, and fallback consent. Country is not preference, and if you do not capture these fields, you should not claim either payout model matches what contractors actually want.

Where USD payouts break down as you scale#

USD payouts usually break down at scale when conversion and settlement are pushed downstream, because that makes net receipt less predictable for contractors and exceptions harder for your team to close. The issue is not USD alone; it is uncertainty around conversion path, timing, and final credited amount.

The friction appears after payout initiation#

In non-USD markets, sending USD can shift complexity to the recipient side. The receiving bank may accept USD, force conversion, or route through a foreign currency wire transfer path with additional checks before funds are credited. When that happens, contractors may not know what amount will actually land, even if your product showed a clear USD gross amount.

This is where hidden costs, slow transactions, and avoidable inefficiencies start to show up. Some vendor sources describe local-currency payments as potentially reducing conversion fees by 1-5% and improving processing speed, but that should be treated as directional, not universal.

| Scaling issue | USD-heavy default | Local-currency enabled corridor |

|---|---|---|

| Who handles conversion | Often recipient bank or downstream intermediary | Usually handled before funds reach the recipient |

| Net receipt predictability | Lower when recipient-side FX applies | Higher when amount is sent in local currency |

| Settlement visibility | Can blur across intermediary checkpoints | Often clearer on local-friendly rails |

| Reconciliation effort | Higher when sent and received amounts diverge | Lower when payout and receipt currency align |

Where operations and finance feel the impact#

The operational pattern is familiar: payout shows as sent, the recipient still sees no funds, and support volume rises because status clarity is weak. Finance then sees reconciliation drift in ledger journals when USD disbursements and reported local receipts do not match, which creates manual exception work.

| Field to verify | What to check |

|---|---|

| Selected payout currency | Verify the selected payout currency on each exception before treating the issue as a provider failure |

| Receiving bank country/account capability | Confirm whether the receiving bank and account can accept USD without forced conversion or rejection |

| Provider confirmation of instructed currency and amount | Verify the provider confirmation of the instructed currency and amount on each exception |

Before you treat these as provider failures, verify those three fields on each exception: selected payout currency, receiving bank country/account capability, and provider confirmation of instructed currency and amount. Assuming a bank can cleanly receive USD without forced conversion is a repeat-ticket trap.

Treasury's September 2022 recommendation to prioritize cross-border payment improvements is useful context here: this friction scales with volume. If your top corridors show rising exception rates, keep USD as fallback only and prioritize local-currency enablement in those corridors first.

For a step-by-step walkthrough, see Cash Pickup Payouts for Unbanked Contractors in Cash-Preferred Markets.

Where local currency payouts can backfire if controls are weak#

Local-currency payouts improve outcomes only when your controls are stronger than your certainty claims. If FX quote handling, fallback rules, and payout status signaling drift out of sync, you replace USD uncertainty with a different kind of ambiguity for the contractor.

Weak implementations usually fail in the same places:

| Control area | Weak implementation | What the contractor experiences |

|---|---|---|

| FX quote handling | A quote is shown early and reused after conditions or provider availability change | Expected amount and received amount diverge |

| Fallback logic | The preferred local route is unavailable and the system switches path or currency without clear notice | Surprise conversion, fees, or delay |

| Status signaling | Payout state changes are not reflected clearly in product status updates | "Where is my money?" tickets and trust loss |

| Rail coverage | Local rail support is uneven by market or program | Local payout is promised, but completion is inconsistent |

Rail coverage is not uniform, even if your UI is#

Payment rails are the infrastructure that moves money, and access to those rails is uneven across countries, bank relationships, and compliance programs. Banking access and compliance hurdles can make rail access difficult, so "local currency everywhere" is often a roadmap claim before it is an operational reality.

This matters most where outbound currency controls or formal-channel restrictions cause delays. The risk is not that every market behaves this way; it is that strict outbound controls can disrupt legitimate outbound payments and can push users toward informal alternatives when formal routes are too slow. In those corridors, broader promises without tighter controls increase risk.

Before rollout, verify supported rails by receiving country, recipient account type, and payout program, and define the exact fallback behavior when a route is unavailable.

Certainty claims fail fastest when visibility is thin#

Trust drops when you promise certainty but cannot clearly show what was quoted before confirmation and what happened after initiation. For payout exceptions, keep a complete record of the quoted rate shown, instructed currency and amount, provider acknowledgment, and payout status changes so support can explain whether the issue came from quote timing, routing, or downstream handling.

If you cannot reliably keep quote checks, fallback behavior, and status signaling aligned, do not roll out local currency broadly. Ship corridor by corridor, keep strict guardrails, and only promise certainty where controls are already proven.

We covered this in detail in Choosing SWIFT or Local Bank Transfers for Cross-Border Platform Payouts.

Decision rules by corridor and payout rail#

Set payout defaults at the corridor-and-rail level, not across your whole program. Default to local currency only where rail coverage is reliable and FX quotes are rechecked at confirmation. If either control is weak, default to USD and state clearly that conversion may happen at receipt. Keep payment stablecoins in an exception lane unless legal and operational readiness is already in place.

Use a simple matrix: rail availability, quote reliability, support-ticket volume, and recent failure frequency. Define policy by receiving country, recipient account type, payout program, and rail, because that is where payout promises usually fail.

| Corridor and rail option | Default when | Verify first | Main tradeoff or failure mode |

|---|---|---|---|

| Local bank rail with local currency | Rail coverage is stable and quote checks happen at confirmation | Receiving-country support, recipient account type, payout-program eligibility, fallback behavior | Stale quotes, silent reroutes, or rail gaps can create expected-vs-received disputes |

| USD payout path | Local coverage is inconsistent or quote reliability is not strong enough to promise certainty | Conversion expectations are disclosed, status visibility is clear, ledger-journal reconciliation is defined | Recipient conversion uncertainty can increase support load |

| Payment stablecoin rail | Traditional rails are weak in that corridor and compliance owners approve | Licensing, custody, consumer protection, risk management, and on/off-ramp readiness | Regulation is fragmented across jurisdictions, and ramp friction can offset speed/cost benefits |

The default rule is straightforward: when local rails are consistent and quote freshness is enforced, local currency reduces recipient ambiguity. When those controls are not dependable, USD is the more defensible promise.

Split policy by payout shape, not just by country#

Country defaults are too coarse on their own. Keep separate defaults for payout batches versus one-off contractor payouts, and for urgency tiers (same-day expectation versus standard settlement). Only label a route "same-day" where your own operating data supports that outcome; otherwise keep standard expectations explicit.

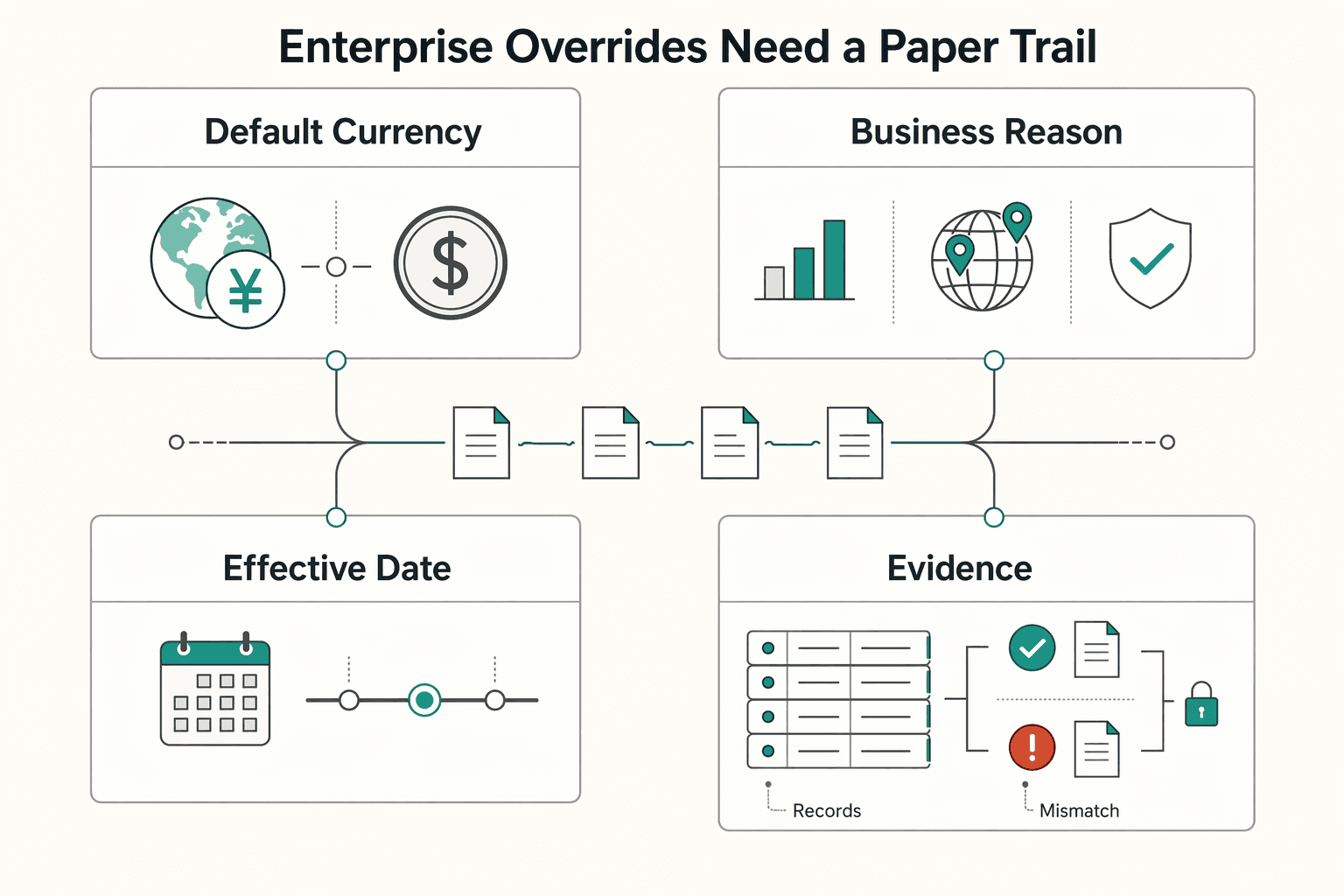

Enterprise overrides need a paper trail#

Allow enterprise overrides only when account, finance, and compliance owners approve the risk and support model. Record each exception in ledger journals with:

| Override record | What to include |

|---|---|

| Default currency and rail | Approved default currency and rail for that account or corridor |

| Business reason | Business reason for the override |

| Effective date and approver | Effective date and approver |

| Dispute evidence requirements | Quoted amount, instructed currency, and provider acknowledgment |

For U.S.-connected stablecoin programs, keep the timeline explicit: the Federal Reserve notes that the Genius Act established a U.S. framework for payment stablecoins in July 2025. That improves U.S. policy clarity, but cross-border rollout still requires jurisdiction-by-jurisdiction readiness because regulation remains fragmented and on/off-ramps add friction.

If stablecoins are on your roadmap, use this as the next step: stablecoin payouts for platforms.

Need a broader rail decision framework? Read When Platforms Should Use Wires vs Local Rails for Cross-Border Payouts.

Want a quick operational next step for your payout strategy? Try the free invoice generator.

Implementation sequence for product, ops, and engineering#

Roll out in sequence, not all at once: baseline metrics first, currency preference capture second, corridor pilots third, and broader expansion only after pilot performance is reliable.

Rollout order that reduces avoidable rework#

Start by measuring the current state before changing payout defaults. Keep the baseline focused on the core cross-border pain points of cost, speed, access, and transparency, then track operational signals like time from payout request to provider confirmation, exception and retry counts, expected-versus-received complaints, and finance reconciliation effort from ledger journals.

Next, add currency preference capture in onboarding and payout settings. Capture preferred payout currency, receiving country, account type, and whether USD fallback is accepted when the local route is unavailable. At payout creation, stamp the chosen currency, instructed amount, and any FX quote reference in the journal trail, and avoid post-funding currency changes that can create dispute risk on retries.

Then run corridor pilots instead of a global launch. Use routes where local rail coverage and quote handling already look strong, keep a USD or foreign currency wire transfer control group, and only promote corridors that pass user acceptance testing and live performance review.

Technical gates before you widen coverage#

Keep engineering gates strict before expansion:

| Technical gate | What to verify |

|---|---|

| Idempotent payout requests | Retries do not create duplicate payouts |

| Webhooks for status transitions | Clear internal-to-provider state mapping |

| Reconciliation exports from ledger journals | Finance can match them to provider acknowledgments without manual stitching |

In user acceptance testing, replay the same payout request and delayed events, then verify ledger consistency under retries and out-of-order updates. If state can regress incorrectly or confirmation cannot be tied to the original journal entry, hold expansion for that corridor.

Module choices by architecture role#

| Module | Best role in rollout | What to verify first | Main tradeoff |

|---|---|---|---|

| Core payout platform | Control layer for requests, status, and payout evidence | State model, webhook handling, journal export completeness, retry behavior | Weak controls turn each corridor launch into a support issue |

| Virtual Accounts | Useful where supported for clearer balance attribution before disbursement | How funds map to contractors, wallets, or sub-balances, and how journals reconcile | Adds another balance layer to explain and reconcile |

| Merchant of Record (MoR) | Use only if your model already needs merchant and tax ownership changes | What MoR owns versus what the payout stack still owns for contractor disbursement | Can solve commercial scope issues without solving payout transparency |

UI should follow the same logic: show expected amount, payout currency, and status from request through provider confirmation, not just a generic processing label.

The practical sequence is straightforward: ship core payout controls first, add preference capture second, pilot by corridor third, and add Virtual Accounts or MoR only where each closes a defined architecture gap. For notification design on payout state changes, see Push Notification Strategy for Payment Platforms: How to Alert Contractors About Payouts.

Compliance and tax gates you cannot bolt on later#

Do not widen corridors after a technical pilot until policy and tax owners clear explicit launch gates. Treat each gate as a blocker with named evidence, not as cleanup for later.

| Gate area | What must be clear before launch | What to verify in the evidence pack | Common miss |

|---|---|---|---|

| KYC and AML policy gating | Which internal policy owner approves the corridor, recipient type, and payout method | Written approval, escalation path, and documented market or program limits | A route is enabled before policy review is complete |

| W-8, W-9, 1099 readiness | How your program handles tax-document collection and operational handoffs | Onboarding fields, document status visibility, and ownership across ops, tax, and support | Payouts launch without a workable path for missing or invalid forms |

| U.S. foreign-asset reporting review | Whether the program needs formal review for cross-border reporting intersections | A documented review covering FATCA, FinCEN, FBAR, and Form 8938 steps | Teams treat cross-border payouts as only a payments workflow |

The U.S. reporting checkpoint is where surprises usually happen. The IRS says Form 8938 (Statement of Specified Foreign Financial Assets) is used to report specified foreign financial assets when total value exceeds the applicable threshold; IRS guidance also cites a $50,000 aggregate value trigger for certain U.S. taxpayers. For certain specified domestic entities, the instructions cite $50,000 on the last day of the tax year or $75,000 at any time during the tax year. The IRS also says if no income tax return is required for the year, Form 8938 is not required.

Operationally, avoid hard-coded assumptions: keep FinCEN FBAR due-date references and extension notices out of product logic, and require documented tax and compliance review before expanding corridor coverage.

Conclusion#

The practical answer is not to force one payout currency everywhere. Use local-currency defaults only in corridors where operational coverage and reconciliation are dependable, and keep USD as a fallback where real constraints remain, including expensive wire fees, payment delays, or tax and onboarding friction.

That recommendation matters because cross-border payout problems are rarely just about denomination. Teams still end up wrestling with international wire transfers, payment-delay explanations, multiple currencies, and tax-form handling, even when a payout appears initiated. If a provider confirms initiation but your ops team cannot verify what was quoted, what was sent, what settled, and what landed in the contractor account, that default is not production-ready at scale.

The operator move is to treat payout currency as a policy decision, not a preference toggle. Your policy should be backed by corridor-level evidence, compliance checks, and traceable records. At minimum, each corridor you promote to a local-currency default should pass three checks:

- Pre-payout certainty: you can show the expected payout currency and FX details before confirmation, and handle stale quotes explicitly.

- Post-initiation visibility: you can track state changes after initiation instead of stopping at API success, especially where payment delays trigger support tickets.

- Settlement proof: finance can reconcile provider outputs to internal records without manual guesswork or exception hunting.

The common failure mode is easy to miss: product flips the default, but ops still cannot explain delays, and tax-document or onboarding gaps surface only after launch. Cross-border programs often struggle with vendor onboarding delays and tax forms such as W-8BEN/1042-S, so do not widen rollout until those documents and checks are tied to payout eligibility. If a corridor still relies on costly wire routes and your team cannot reliably explain receipt timing or received amount, keep that corridor in fallback status for now.

Your next step should be concrete. Publish a corridor decision matrix, run a controlled pilot, and promote only the defaults that clear reliability, reconciliation, and contractor-trust checkpoints. This removes ambiguity before rollout: which rail is used, what the contractor should expect, what evidence support can pull, and how finance will close the books when payouts span multiple currencies.

Related reading: Xero Multi-Currency for Payment Platforms: How to Reconcile Foreign Currency Payouts.

Frequently Asked Questions

Do contractors prefer USD or local currency for payouts?

There is no grounded basis here to claim a universal winner. The practical answer is that preference depends on currency stability, legal requirements, operational efficiency, and where your contractors are based. If you do not capture payout-currency preference during onboarding and payout setup, you are largely guessing.

When should a platform default to USD instead of local currency?

Use USD as a fallback when local wage-currency rules are unclear or restrictive, or when you cannot clearly set expectations on timing and received amount. Batch-processed rails such as ACH and SWIFT can add timing uncertainty, so avoid promising payout certainty you cannot actually deliver.

What minimum capabilities should a contractor payout platform support before rollout?

At minimum, it should support the full path from onboarding to disbursement to settlement reconciliation, not just payment initiation. You also want a consistent, local-friendly recipient experience, plus tax-document handling strong enough to avoid delayed payments or misfiled forms. If your provider can return an API success but cannot show whether funds actually reached the contractor bank account, that is not rollout-ready for broad defaulting.

How do FX quote transparency and payout timing affect contractor satisfaction?

They matter because contractors judge the payout by what lands and when, not by whether your API accepted the request. The grounded caution is explicit: many providers advertise speed based on API success, even though the contractor bank account may update later. For cross-border payouts, common settlement windows are still cited at 2-5 business days, and even ACH is usually 1-3 business days, so set expected timing and received-amount expectations before confirmation.

What are the most common failure modes when enabling local-currency payouts?

The big ones are unclear amount expectations, weak status visibility after initiation, delayed settlement on batch rails, and tax-document readiness gaps that surface only after launch. Another common miss is treating local currency as universally better without checking local labor-law constraints on wage currency. If your support team cannot verify payout state and final settlement outcome clearly, you will create avoidable escalations.

How should teams measure success after switching default payout currency?

Measure contractor-facing outcomes first: fewer tickets about expected versus received amount, fewer timing complaints, and fewer payout exceptions that need manual follow-up. Then check operational proof: lower reconciliation effort, fewer delayed-payment cases in key markets, and cleaner tax-document completion before funds are sent. If those do not improve after the switch, your default changed faster than your controls.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- acquisition.gov/far/part-52trusted

- bis.org/cpmi/publ/d207.pdftrusted

- calhoun.nps.edu/server/api/core/bitstreams/af6b9dc8-106d-4ce...trusted

- comptroller.war.gov/Portals/45/Documents/defbudget/FY2026/budget...trusted

- congress.gov/crs-product/R47751trusted

- federalreserve.gov/econres/notes/feds-notes/the-state-of-ai-com...trusted

- federalreserve.gov/econres/notes/feds-notes/payment-stablecoins...trusted

- fincen.gov/report-foreign-bank-and-financial-accountstrusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Stablecoin Payouts for Platforms Disbursing USDC to Global Contractors

**Step 1. Set the operating model before you talk about speed.** This guide is for platform operators shipping stablecoin contractor payouts in production, not for freelancers choosing a wallet. The core stance is simple: approve compensation in USD, use a stablecoin as the settlement rail, and treat controls as product requirements from day one. Stablecoins are built to behave like money, and businesses already use them for supplier payments, cross-border invoicing, and treasury movement. That makes stablecoin payouts worth a look, but only if your payout process is as disciplined as your fiat process.

Push Notification Strategy for Payment Platform Payouts

**Payout alerts fail when your message language gets ahead of a verified payout state.** If you want notifications your contractors can trust, optimize for what you can prove in your payout lifecycle. Do not optimize only for send speed or open rate.

Crypto Payouts for Contractors: USDC vs. USDT - What Platforms Must Know

Treat this as an operating decision first. If you are a platform team building contractor payroll, the early mistake is to frame USDC versus USDT as a recipient wallet preference. The real choice sits with Finance, Ops, Product, and Engineering.