Quick Answer

Start with filing scope and evidence controls before adding automation. For FATCA reporting platforms, require GIIN status, certificate validity, Form 8966/FATCA XML quality checks, the IDES transmission package, and retrievable ICMM notification archives. If your team cannot explain a DocRefId change or classify accounts with confidence, pause filing and escalate to tax/legal. Keep Form 8938 and FinCEN Form 114 determinations distinct so one workflow is not treated as full coverage.

FATCA reporting platforms for operators who need control without overbuilding#

Start with accountability, not a vendor demo. The first question is whether your team can produce and defend the artifacts that make a FATCA filing traceable, reviewable, and correctable when something goes wrong.

| Artifact | Where it fits | Article detail |

|---|---|---|

| Approved GIIN | Before filing | Part of the minimum, testable control set for an IRS IDES path |

| Digital certificate from an IRS-approved certificate authority | Before filing | Part of the minimum, testable control set for an IRS IDES path |

| FATCA XML file | File preparation | Part of the minimum, testable control set for an IRS IDES path |

| Proof the file was compressed and encrypted before upload | Before upload | Retain as submission evidence |

| IRS confirmation message after transmission | After transmission | Retain as submission evidence |

| Correction records | Correction handling | Part of the clear evidence chain from account data to submission |

-

Scope ownership before tooling. In cross-market payouts, responsibilities are often split across teams. Name one owner for submission readiness and one escalation owner for interpretation before GIIN validation, certificate management, and correction handling become urgent.

-

Install a minimum, testable control set first. If a late or incorrect filing would create risk for your team, start with controls that produce evidence. For an IRS IDES path, that means an approved GIIN, a digital certificate from an IRS-approved certificate authority, a FATCA XML file, proof the file was compressed and encrypted before upload, and the IRS confirmation message after transmission.

-

Tie escalation to known failure points. Escalate before filing if your team cannot explain a DocRefId change, cannot show how correct, amend, or void handling works, or has unresolved data-prep errors feeding Form 8966 output. IRS guidance and sample files point to these as operational issues, so treat unresolved GIIN status, certificate validity, or source-data quality as a hard stop.

-

Keep adjacent reporting regimes separate. Form 8938 has its own thresholds, including $50,000 aggregate value for certain U.S. taxpayers and $50,000 year-end or $75,000 anytime for certain specified domestic entities, but those figures are not a shortcut for FATCA platform filing triggers. Filing Form 8938 also does not remove separate FBAR (FinCEN Form 114) obligations.

-

Evaluate platforms on traceability, not feature count. This is an operator decision, not a coverage claim. Require a clear evidence chain from account data to submission: FATCA XML output, compression and encryption package, GIIN-linked submission evidence, IRS confirmation, and correction records.

If you want a deeper dive, read FATCA Compliance for Marketplace Platforms: Identifying and Reporting Foreign Account Holders.

How to choose a FATCA reporting platform for your operating model#

Choose the platform based on your filing route and evidence trail, not feature breadth. The strongest setup is the one your team can explain and retrieve under review.

- Pick the filing lane first

Decide which lane your model will use, for example IRS IDES, HCTA, or both where applicable. For the IRS lane, confirm the tool supports the route you will actually use. The IRS describes IDES as the system used to exchange taxpayer information with foreign tax authorities, and its FAQ states FATCA reports can be submitted on the Intergovernmental FATCA XML schema or by paper Form 8966. If HCTA or dual-route scope applies, require that scope in writing.

- Buy for evidence you can defend under review

Ask for a proof pack instead of a demo. At minimum, verify the platform can show submission records and post-submission notices in a form your team can retrieve later. This matters because IDES processing alerts are sent by unsecured plain-text email, while ICMM notifications are encrypted transmission archives, so inbox alerts alone are not a durable evidence trail.

- Stabilize classification before heavy automation

If your data is fragmented, fix classification and reconciliation first, then automate more filing steps. If classification is already stable, prioritize packaging and submission workflow automation. That keeps speed from amplifying data inconsistencies.

- Keep adjacent obligations separate in your operating model

Do not let a platform blur individual Form 8938 obligations with institutional FATCA reporting workflows. Form 8938 is attached to the annual return and filed by that return's due date, including extensions. Filing Form 8938 does not remove separate FBAR obligations where they apply.

Related: DAC7 for Non-EU Platforms: Does Your Marketplace Owe Tax Data to European Authorities?.

Compare the four practical platform paths before you commit#

Pick the path that preserves a defensible evidence trail first, then add automation. If you cannot retrieve the submitted FATCA file, the related IDES transmission record, and the ICMM response archive later, the setup is weak no matter how polished the demo looks.

| Path | Best for | Primary stack | Required in-house skill | Strongest control benefit | Biggest failure mode | Escalation trigger |

|---|---|---|---|---|---|---|

| IRS-native process in IDES | Internal preference for direct handling (IRS excerpts do not rank platform models) | Internal data extract, Intergovernmental FATCA XML schema file, direct IDES transmission, ICMM retrieval | Not specified in the IRS excerpts | Direct access to submission and response artifacts | Team relies on unsecured plain-text IDES email alerts instead of retaining transmission artifacts | Submitted files or ICMM archives are not retrievable |

| FATCA XML software | Internal preference for tooling support (IRS excerpts do not rank platform models) | Source mapping to an Intergovernmental FATCA XML schema file, then IDES transmission and ICMM retrieval | Not specified in the IRS excerpts | Standardized preparation workflow before transmission, if implemented | Output is produced, but filed artifacts and ICMM history are not retained | Vendor cannot provide filed output and matching ICMM response history |

| Managed FATCA service | Internal preference for outsourced operations (IRS excerpts do not rank platform models) | Managed intake, file prep, submission handling, and return of filed artifacts to the client | Not specified in the IRS excerpts | Operational execution can be delegated while retaining evidence access, if contractually defined | Evidence access drifts to provider summaries instead of primary artifacts | Contract does not require delivery of filed output and retrievable ICMM history |

| Hybrid model | Internal preference for split ownership (IRS excerpts do not rank platform models) | Internal policy/approval steps, external transformation/transmission support, internal artifact retention | Not specified in the IRS excerpts | Keeps oversight internal while delegating selected execution steps | Split ownership leaves gaps in final artifact retention or follow-up | No named internal owner for final transmitted file and ICMM follow-up |

| Decision checkpoint | Scope decision before tool decision | Confirm FATCA filing scope first, then map evidence retention and filing obligations; Form 8938 filing and separate FBAR obligations depend on taxpayer/entity status and thresholds | Medium to high policy discipline | Reduces mismatch between obligations and operating model | Assuming one filing obligation replaces another | Filing scope or ownership is still disputed between tax, legal, and ops |

What to verify in a live sample#

Ask for a real evidence pack, not a demo flow: the submitted Intergovernmental FATCA XML schema file, the transmission package used for IDES, and the related ICMM response archive. Treat IDES unsecured plain-text email alerts as notifications only, not your record of control.

Related reading: What Is RegTech? How Compliance Technology Helps Payment Platforms Automate Regulatory Reporting.

Option 1 IRS native IDES process with internal ownership#

Keep this route in-house only if your team can prepare the filing data, transmit through International Data Exchange Services (IDES), and later retrieve the same submission evidence without relying on a vendor. That is the core control test for this option.

If direct evidence ownership is the priority, this is the clearest path. It also means your team owns the weak points if source mapping, packaging, or archive retention is inconsistent.

Best fit#

This option fits teams that can repeatedly produce a valid transmission file, for example Intergovernmental FATCA XML schema submissions where applicable, and explain how records moved from source data to the final file. The test is repeatability across tax, ops, and engineering, not a one-time successful send.

Use it when you already run formal approvals, versioned data changes, and retrievable filing records, with a named owner for the final transmitted file and response follow-up.

What you gain#

You keep direct control of the filing evidence trail. IDES is the IRS system used to exchange taxpayer information with foreign tax authorities, and ICMM is the IRS system that receives, processes, stores, and manages FATCA data. In practice, that means you can retain the submitted file and related ICMM notification archive yourself.

Set one hard verification checkpoint: after submission, can someone outside the filing team retrieve the exact filing package and the related ICMM notification archive containing encrypted documents? Treat IDES alerts as prompts only, not proof of filing, because they are unsecured plain-text emails.

Where it breaks#

This model breaks when execution discipline is weak, especially when transmission artifacts, ICMM archives, or pre-submission validation records are not consistently retained.

Keep the scope boundary clear. Internal FATCA filing ownership does not replace separate Form 8938 or FBAR analysis. Form 8938 must be attached to the annual return and filed by the due date, including extensions. Filing Form 8938 does not remove FinCEN Form 114 obligations. Thresholds also vary by filer type, including higher thresholds for some taxpayers and, for specified domestic entities, $50,000 on the last day of the tax year or $75,000 at any time during the tax year.

This pairs well with our guide on 1099-K Reporting Threshold After the IRS Delay: Control Updates for Platform Operators.

Option 2 FATCA XML software layer for submission readiness#

Use this option when your team already knows what should be reported and needs more consistent Intergovernmental FATCA XML schema output, plus tighter handling of submission evidence. This will not improve legal judgment; it gives you cleaner file preparation and a more disciplined handoff into IDES processing.

This fits operators that can prepare filing data but want a dedicated layer to standardize schema-formatted output and support transmission follow-up. The upside is more consistent preparation for the IRS XML submission path and clearer operational ownership for ICMM notification follow-up, since ICMM notifications are transmission archives that contain encrypted documents. The tradeoff is straightforward: weak source mapping will still produce weak reporting, even if the XML is well formed.

A good use case is a payments, tax, and engineering team with defined ownership for transmission follow-up and exception handling. Before you buy, run a real test cycle where the team can produce the submission file, monitor IDES transmission processing, and review the related ICMM notification archive. Treat IDES alert emails as prompts, not filing proof, because they are unsecured plain-text processing alerts. Keep filing boundaries clear: filing Form 8938 does not remove a separate FBAR filing requirement when FBAR is otherwise required. Need the full breakdown? Read FBAR and FATCA Reporting for US Expats.

Option 3 Managed FATCA and CRS reporting service#

Choose a managed service when your team lacks the bandwidth to run annual FATCA operations, but keep internal ownership of filing scope, triggers, and evidence quality. Outsourcing the mechanics can help; outsourcing the filing conclusion is where teams get into trouble.

This path can fit lean compliance teams expanding into additional markets without mature in-house reporting operations. It may reduce internal operational load if the provider is contractually responsible for producing filing-ready outputs. The tradeoff is lower direct control, especially if the contract leaves you with activity summaries instead of audit-ready records.

One use case is a fast-growing platform that needs execution support but still wants controlled sign-off on reportability decisions. Keep that sign-off in-house. Form 8938 must be attached to the annual return and filed by that return's due date, including extensions, so require outputs that tie back to that deadline.

Set two early control checks. First, confirm the provider can distinguish cases where no income tax return is required, because Form 8938 is not required in that case. Second, require clear threshold logic for specified domestic entities. Filing applies when specified foreign financial assets exceed $50,000 at year-end or $75,000 at any time during the tax year.

Also watch for false completeness. Filing Form 8938 does not satisfy the separate FBAR requirement (FinCEN Form 114), so track evidence separately for each regime. Ask directly how the provider handles Model 1 IGA disregarded-entity cases, where a disregarded entity may need separate FATCA registration from its owner.

If a provider cannot deliver a packet tied to the applicable calendar year or tax year, threshold determination, and Form 8938 support, do not treat the service as full outsourcing.

For a step-by-step walkthrough, see FATCA and W-8 Tax Compliance for Platforms: When to Release, Hold, or Withhold Foreign Payouts.

Option 4 Hybrid model with internal controls and external filing support#

In a hybrid model, document ownership for reporting judgment, evidence, and filing mechanics before work starts. Decide scope first, then package and submit, because Form 8938 still must be attached to the annual return and filed by that return's due date, including extensions.

Best fit#

Use the hybrid path only if your decision record is defensible before filing-preparation starts. The point of this model is to keep control of that record.

Form 8938 applies only when specified foreign financial assets exceed the applicable reporting threshold. For certain specified domestic entities, that is $50,000 on the last day of the tax year or $75,000 at any time during the tax year. If you cannot support that threshold call, filing support will not fix the core risk.

Internal control checkpoints#

Before anything is handed off, your file should stand on its own. At minimum, keep clear records of the following, and fix any reconciliation break before submission. If the deposit-account count on the form does not reconcile to your underlying account inventory, correct it first.

- whether an income tax return is required for the year (if no return is required, Form 8938 is not required)

- which threshold test was applied, including whether the filer is a specified domestic entity

- the structured account summary supporting the form, such as the number of deposit accounts reported in Part V

External support scope#

If you use external support, require a complete, year-specific filing package that ties back to your approved account list and threshold determination. If the output cannot be tied back to that record, treat it as a control gap.

Red flags#

Do not treat filing mechanics as compliance by themselves. Filing Form 8938 does not remove separate FBAR (FinCEN Form 114) obligations when FBAR is otherwise required.

Also flag conflicting account-status documentation early. IRS guidance states a Form W-8 is treated as unreliable if account information includes a U.S. address. If that conflict is missed upstream, the filing record is harder to defend.

You might also find this useful: ICFR (Internal Control Over Financial Reporting) for Platforms: SOX Compliance Without a Big Finance Team.

Map the trigger points when foreign accounts become a US reporting risk#

Map the legal trigger before you map the filing route. Classify each case as Form 8938, FBAR, both, or neither, and if classification confidence is weak, pause automation and escalate to tax or legal review.

Teams often invert this sequence by starting with routing or vendor workflow first. The stronger control is to start with filer type, account facts, and threshold, then record the filing consequence.

| Decision point | Core trigger | Filing path | What to verify first |

|---|---|---|---|

| Form 8938 | Specified individuals and certain specified domestic entities with an interest in specified foreign financial assets that exceed the applicable reporting threshold | Attach to the annual return by that return's due date, including extensions | Whether an income tax return is required, and which threshold pair applies |

| FBAR (FinCEN Form 114) | Aggregate value of foreign financial accounts exceeds $10,000 at any time during the calendar year | Filed directly with FinCEN, not with the IRS | Whether the foreign-account population is complete and aggregation is done across relevant accounts |

| Both may apply | The facts meet the Form 8938 test and the FBAR test separately | Separate filings through separate paths | Whether both determinations are documented independently |

If your program also tracks other cross-border routing fields, keep that as a separate matrix. The IRS materials here support scope and trigger decisions, not broader transmission-path design.

- Start with the legal trigger, not the account label.

Internal labels are not enough. For U.S. reporting, confirm what the account or asset is, who has the interest, and whether the filer is a specified individual or a specified domestic entity for Form 8938 analysis.

- Test Form 8938 on filer category, return requirement, and threshold.

Form 8938 applies only when the filer and threshold tests are met. For specified domestic entities, the threshold is more than $50,000 on the last day of the tax year or more than $75,000 at any time during the tax year. For individuals living in the U.S., the IRS comparison page lists $50,000 last day / $75,000 anytime (unmarried or married filing separately) and $100,000 last day / $150,000 anytime (married filing jointly). Form 8938 is attached to the annual return and filed by that return's due date, including extensions. If no income tax return is required, Form 8938 is not required. Also, some accounts are excluded from Form 8938 reporting, including financial accounts maintained by a U.S. payer.

- Test FBAR separately and aggregate early.

FBAR is a separate obligation. The trigger is whether the aggregate value of foreign financial accounts exceeds $10,000 at any time during the calendar year, and the filing goes to FinCEN, not the IRS. Filing Form 8938 does not remove a separate FBAR obligation, so your file should show a distinct FBAR determination.

- Treat incomplete source data as a stop sign.

Boundary cases can leave key facts unclear, especially around account ownership, foreign status, or whether the filer has a reportable interest. When source records do not support a defensible classification, stop and escalate before filing. The rule is simple: if you cannot clearly justify Form 8938, FBAR, both, or neither, you are not ready to automate.

For related UK platform rules, see HMRC Reporting Rules for Platforms for UK Marketplace Operators.

Define the minimum evidence pack before any filing cycle#

Before you start a Form 8938 cycle, make sure the file can prove four things: why filing is required, which tax period it covers, what was intentionally excluded, and whether a separate FBAR check was completed.

| Evidence item | Keep | Shows |

|---|---|---|

| Filing-basis record | Filer category, whether an income tax return is required, and the threshold test used | Why Form 8938 applies; for specified domestic entities, this can include the more than $50,000 year-end or more than $75,000 any time during year test; if no income tax return is required, Form 8938 is not required |

| Return-linkage and period proof | Evidence that Form 8938 is tied to the correct annual return and filing window | That Form 8938 is attached to the annual return, filed by that return's due date, including extensions, and tied to the applicable calendar year or tax year |

| Identity, asset, and exclusion support | Name and TIN, asset support, and the exclusion basis for anything left out | What was reported and what was intentionally excluded, including when an account is maintained by a U.S. payer |

| Open-issue log and separate FBAR check | Unresolved classification or data-quality gaps and a separate FBAR determination | Whether support is complete before filing and that Form 8938 does not by itself remove a separate FinCEN Form 114 obligation |

- Filing-basis record

Document why Form 8938 applies: filer category, whether an income tax return is required, and the threshold test used. Keep the tax-period logic explicit. For specified domestic entities, that can include the more than $50,000 (year-end) or more than $75,000 (any time during year) test. Also record the negative test: if no income tax return is required for the year, Form 8938 is not required.

- Return-linkage and period proof

Keep evidence that Form 8938 is tied to the correct annual return and filing window. The instructions require Form 8938 to be attached to the annual return, filed by that return's due date, including extensions, and tied to the applicable calendar year or tax year. A complete form without clear return linkage is weak evidence.

- Identity and asset support

Preserve the filer identity inputs used on the form, for example name and TIN, and the asset support for specified foreign financial assets in which the filer has an interest. If accounts were excluded, record the exclusion basis clearly, including when an account is maintained by a U.S. payer.

- Open-issue log and separate FBAR check

Maintain a visible log of unresolved classification or data-quality gaps and escalate before filing when support is incomplete. Keep a separate FBAR determination in the packet. Filing Form 8938 does not by itself remove a separate FinCEN Form 114 obligation.

Assign escalation ownership before issues surface#

Set escalation ownership before filing so unresolved classification questions do not turn into last-minute decisions. A practical internal split is policy, interpretation, and execution.

| Function | Primary responsibility | Boundary |

|---|---|---|

| Compliance | Maintain the internal classification policy for what is reviewed for Form 8966 and what is out of scope, with filing-year examples and exclusions | Policy should reflect that Form 8966 can cover certain U.S. accounts and substantial U.S. owners of passive NFFEs |

| Tax/legal | Own interpretation when facts do not fit the policy cleanly | Escalate before submission with account facts, proposed treatment, applicable tax year, and why the policy did not resolve the case |

| Operations | Own execution after approval | Prepare and transmit only records with clear classification and documented approval; use a hard internal stop when filing assumptions are unresolved |

- Compliance owns the internal classification policy.

Compliance should maintain the rulebook for what is reviewed for Form 8966 and what is out of scope, with filing-year examples and exclusions. That policy should reflect that Form 8966 can cover more than one category, including certain U.S. accounts and substantial U.S. owners of passive NFFEs.

- Tax/legal owns interpretation when policy is not enough.

If facts do not fit the policy cleanly, escalate for interpretation before submission. Keep the escalation pack short and specific: account facts, proposed treatment, applicable tax year, and why the policy did not resolve the case.

- Operations owns execution after approval.

Ops can prepare and transmit only records that have clear classification and documented approval. Use a hard internal stop when filing assumptions are unresolved, so a technically complete submission is not built on an open interpretation issue.

Keep form boundaries explicit during review. Form 8938 must be attached to the annual return and filed by that return's due date, including extensions. Filing Form 8938 does not remove a separate FBAR (FinCEN Form 114) requirement.

Roll out in a sequence that reduces rework#

Confirm applicability and filing artifacts on a small, controlled set before you scale. That helps you avoid rebuilding the process in the middle of filing season.

- Lock applicability first

Treat Form 8938 as a two-gate decision: the filer is a specified person, and the filer has an interest in specified foreign financial assets required to be reported. Document both gates per record, with the tax year and threshold logic used. Keep threshold handling explicit: IRS guidance cites a baseline $50,000 threshold for certain U.S. taxpayers, with higher thresholds in some cases, and Form 8938 instructions set specified domestic entity thresholds at $50,000 at year-end or $75,000 at any time during the tax year.

- Map your data to required form artifacts

Build the data model around what Form 8938 actually captures, including items such as the number of deposit accounts and maximum-value summaries. Preserve traceability from each reported total back to underlying records. Also record out-of-scope outcomes clearly: if no income tax return is required for the tax year, Form 8938 is not required.

- Validate filing-chain readiness before expanding volume

Confirm your process supports the filing chain Form 8938 requires: it must be attached to the annual return and filed by that return's due date, including extensions. Add a version checkpoint each cycle because Form 8938 is continuous-use. Verify the current form and instructions before filing.

- Keep adjacent obligations and date boundaries explicit

Keep Form 8938 separate from other foreign-account filings in reviews and handoffs: filing Form 8938 does not remove a separate FinCEN Form 114 (FBAR) obligation. Keep scope dates visible in rollout notes: Form 8938 applies to taxable years starting after March 18, 2010, and certain domestic corporations, partnerships, and trusts are in scope for tax years beginning after December 31, 2015.

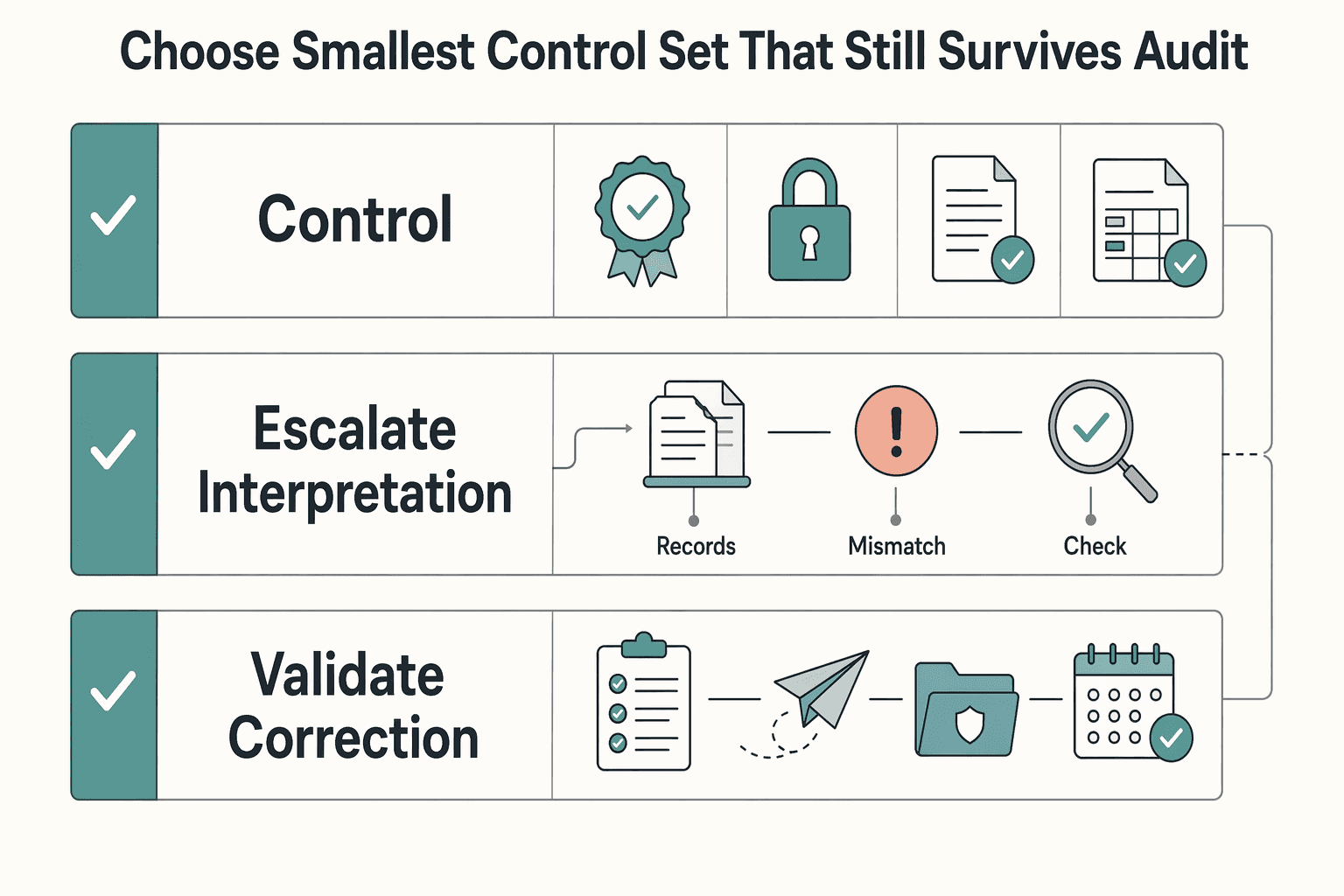

Choose the smallest control set that still survives audit and scale#

Start with the smallest control set you can prove end to end, then scale. That means approved GIIN plus digital-certificate authorization, Form 8966 XML quality checks, retained IDES confirmation evidence, and a tested correction process.

- Match the path to your actual control maturity

Choose the operating path your team can run today, not the one that only looks cleaner on paper. IDES is described as a six-step process, so assign clear owners for authorization, file preparation, transmission, and evidence retention. If any handoff is unclear, narrow scope and close that gap before you expand.

- Install minimum controls around the IRS-defined checkpoints

Start with GIIN authorization, certificate management, IRS-published FATCA XML schema best practices for Form 8966, and IDES transmission evidence. Before upload, files must be compressed and then encrypted. After transmission, retain the IDES confirmation message as part of your filing evidence.

- Escalate interpretation questions before automation

If applicability or threshold treatment is unclear for a tax year, route it to tax or legal first, then automate only approved rules. Keep adjacent obligations separate in your logic: filing Form 8938 does not satisfy FBAR, and if no income tax return is required for the year, Form 8938 is not required.

- Validate correction handling before wider rollout

Confirm your process can correct, amend, and void records using IRS sample correction patterns, and verify DocRefId handling in those flows. Then document your current path and known gaps across GIIN, certificate, XML quality, IDES evidence, corrections, and named escalation owners. Before expanding coverage, confirm your chosen filing path supports your required evidence outputs. If you need to map this baseline to your payout workflow and market/program coverage, talk with Gruv.

Frequently Asked Questions

What does a FATCA reporting platform actually need to do at minimum?

Based on these sources, a practical minimum is to support a defensible Form 8938 decision for each tax year and keep the basis for that decision. That includes threshold logic, including the $50,000 baseline for certain U.S. taxpayers and, for specified domestic entities, $50,000 at year-end or $75,000 at any time in the year, correct tax-year capture, and alignment with what is attached to the annual return.

Which IRS submission steps in IDES cannot be skipped?

These sources do not provide a reliable step-by-step list of IDES actions that can or cannot be skipped. They do confirm that IRS FATCA FAQs cover IDES data format and transmission components, and that IRS materials separate technical IDES topics from broader compliance topics. Verify current IRS technical guidance before finalizing any submission workflow.

Should platform operators run FATCA and CRS in one operating model?

The sources here do not establish that FATCA and CRS must be combined or kept separate operationally. They do show that adjacent obligations remain distinct, including that filing Form 8938 does not satisfy FBAR (FinCEN Form 114). If processes are shared, keep decision logic and evidence clearly separated by regime.

What are the most common FATCA filing failure points in practice?

Key control points: Form 8938 must be attached to the annual return and filed by that return's due date, including extensions, and the filing must match the correct calendar or tax year. Threshold value alone is not the only condition, because if no income tax return is required for the year, Form 8938 is not required.

What should we demand in vendor due diligence before signing?

These sources do not define a formal vendor due-diligence checklist. They only establish Form 8938 control checkpoints such as tax-year handling, threshold applicability, annual-return attachment timing, and the separate FBAR obligation.

When is manual filing still acceptable, and when is automation mandatory?

These IRS excerpts do not set a hard manual-versus-automation rule. Whatever process is used, it still needs to support Form 8938 applicability decisions, threshold basis, tax-year selection, required attachment timing, and separate FBAR consideration.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

FATCA Compliance for Marketplace Platforms: Identifying and Reporting Foreign Account Holders

For marketplace teams handling cross-border payouts, FATCA work is mostly a control-design problem. You need to decide what to implement first, what evidence to keep, and what to escalate before a payout creates avoidable reporting or withholding risk. The practical question is not whether FATCA exists, but which controls actually reduce reporting errors and potential 30% withholding outcomes.

Does Your Non-EU Marketplace Owe DAC7 Tax Reporting in Europe?

Treat DAC7 first as a reporting and data-control problem, not a tax-rate problem. Council Directive (EU) 2021/514 was adopted on 22 March 2021 and entered into force on 1 January 2023. It amended the Directive on Administrative Cooperation so tax authorities can receive and exchange platform seller data across the EU. We recommend starting there so your team does not treat DAC7 like a tax-calculation project and miss the reporting controls that actually fail first.

ICFR for Payment Platforms Under SOX With a Lean Finance Team

**Think small on scope and strict on evidence.** Under SOX pressure with a lean team, the goal is to build defensible ICFR for financial reporting, not to document everything. For covered Exchange Act issuers, management must maintain ICFR and assess effectiveness at each fiscal year-end under Section 404-related SEC rules. ICFR is designed to provide reasonable assurance, not absolute assurance. If you run a lean finance team, we recommend treating evidence quality as the control floor before you add more documentation.