Quick Answer

Start by automating intake, validation, routing, and evidence capture, then keep legal interpretation manual. For payment teams, regtech compliance technology payment platforms automate regulatory reporting is most effective when each filed value can be traced to a payout event, tax form record, approver, and timestamp. Focus first on deadlines and documentation risk, including Form 1099-NEC timing, then add clear escalation triggers for uncertain FATCA or privacy-scope decisions.

How RegTech Fits Into Payment Platform Compliance#

RegTech can automate regulatory reporting for payment platforms, but it should not replace legal judgment. The hard part is often not finding the rules. It is keeping up with changes across jurisdictions and producing a defensible record from onboarding through payout.

In the FCA's definition, RegTech is technology used to address regulatory challenges in financial services. For payment platforms, that can include tax reporting workflows, financial-crime controls, and evidence assembly when a regulator or auditor asks how a filing was produced. The Financial Stability Board has also noted that adoption rose as requirements increased, and that the value is better compliance outcomes and risk management, not just efficiency.

Cross-border complexity is often where these implementations are tested first. The BIS notes there is no single, complete international rulebook for cross-border payment services, and jurisdictions regulate and supervise banks and non-banks differently. At the same time, both remain anchored to FATF financial-crime standards. FATF's 18 June 2025 update to Recommendation 16 also introduced standardized information requirements for certain peer-to-peer cross-border payments above USD/EUR 1,000.

The same pressure shows up in reporting deadlines. Form W-9 is used to provide a correct TIN to payers filing IRS information returns. Form 1099-NEC is due by January 31, and Form 1099-MISC is due by February 28 for paper or March 31 for electronic filing. Under the cited U.S. banking rule, SAR filing is required no later than 30 calendar days after initial detection. Different regimes, same lesson. Missing fields or untracked exceptions can become filing risk very quickly.

This article keeps a narrow scope on purpose: automate collection, validation, routing, timestamps, and evidence packaging, while escalating ambiguous legal interpretation to legal or compliance. That boundary matches how the authorities frame supervision. Technology can support the work, but judgment still sits with people.

This article covers five things:

- Selection criteria: how to evaluate coverage, evidence quality, escalation controls, and integration depth.

- Side-by-side comparison: six capability categories tied to required data and escalation ownership.

- Best-for recommendations: practical fit for lower-volume teams and multi-market payout platforms.

- Escalation triggers: when automation should stop and legal or compliance should take over.

- Implementation sequence: a phased rollout that prioritizes filing and evidence risk before optimization.

If you cannot trace a reported value to the underlying payout event, supporting document, and approver timestamp, your reporting automation may not be audit-ready yet.

Who this list is for and how to choose#

This list is for teams that own reporting risk at a payment platform and need better control over how obligations are executed and evidenced. It is not for teams looking for software to make final legal judgments on ambiguous rules. Use automation for collection, routing, validation, and evidence, and keep interpretation and contested edge cases with people.

- Fit

This section is for compliance, legal, finance, and risk owners managing AML, FATCA, and tax reporting obligations in payment flows. It is most useful when your team already knows which filings and controls apply, but cannot consistently prove how a reported value, Form W-9 record, or other information-return input was collected, checked, approved, and retained. If you are accountable for AML implementation under a risk-based approach, you are in scope.

- Non-fit

Do not use this list if your goal is a fully automated legal-interpretation engine for GDPR, Dodd-Frank, or PSD2-era reporting requirements. Tools can surface obligations and route issues, but they do not remove the need for human intervention and legal review on judgment calls.

- Selection criteria

Evaluate options through four filters: regulatory reporting coverage, evidence quality, control architecture, and escalation controls. Coverage means support for your actual obligations, not just a long jurisdiction list. Evidence quality means clear source records, approver identity, and an auditable history. Control architecture and escalation controls mean clear compliance ownership, documented procedures, independent audit coverage, and reliable handoffs when automation reaches its limit.

- Decision rule

If reporting ownership still runs on email and spreadsheets, prioritize control and evidence tooling before advanced analytics. The test is simple: can you show who received the alert, who owned the action, what data changed, and which artifact supports the filing decision? If not, analytics may polish weak inputs rather than reduce risk.

Related: Music Royalty Tax Compliance: How Platforms Handle 1099-MISC vs. 1099-NEC for Artist Payments.

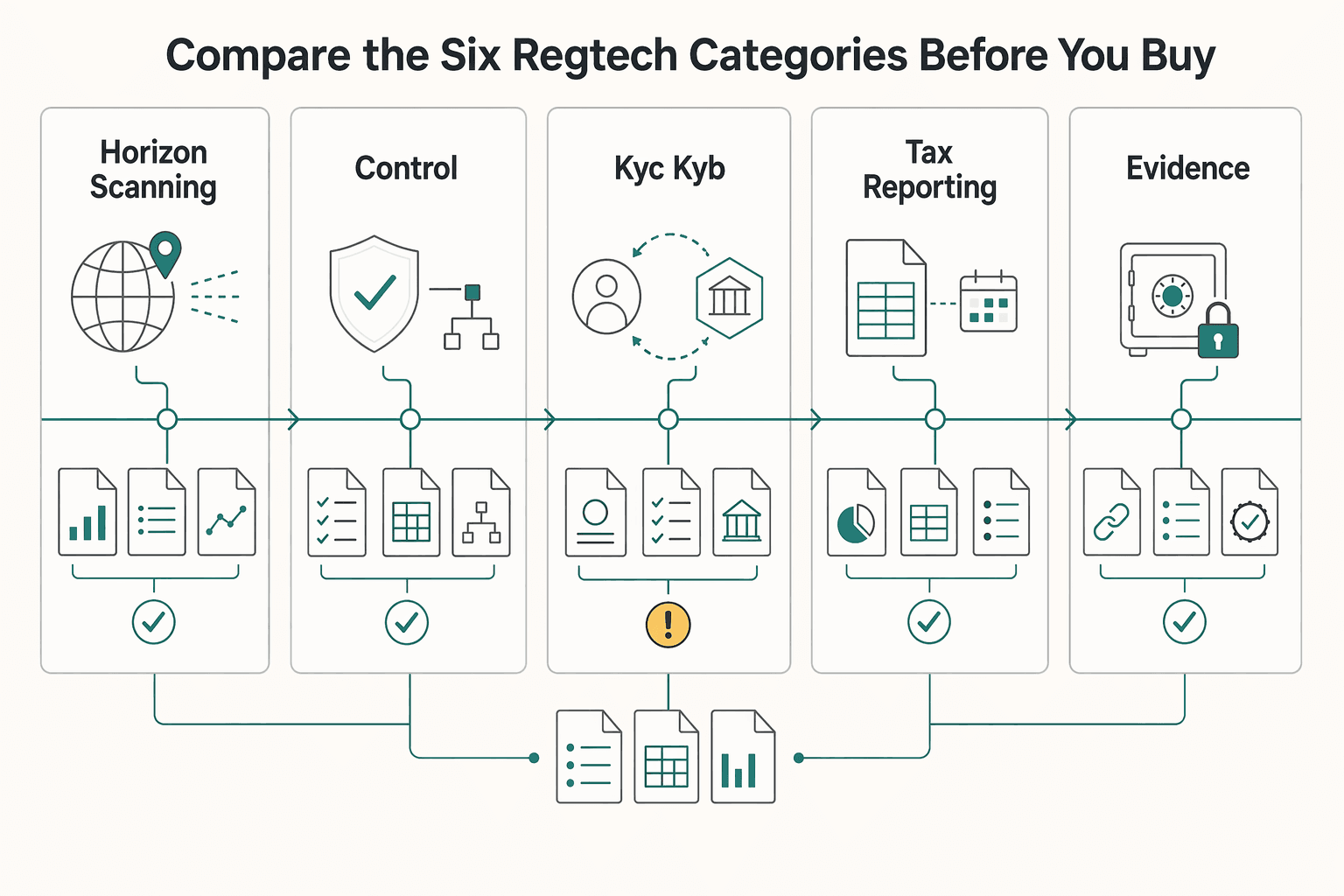

Compare the six RegTech categories before you buy#

If you need to reduce reporting risk quickly, do not buy for breadth first. Start with the category that prevents missed filings, missing source records, and ownerless exceptions in your payout flow. These six categories are a practical buying lens for payment platforms, not a regulator-mandated taxonomy.

| Category | Best for | Key pros | Key cons | Core data needed | Escalation owner |

|---|---|---|---|---|---|

| Horizon scanning | Teams missing updates that affect payout rules, AML obligations, FATCA steps, or FinCEN filing duties | Can surface change early, route notices by jurisdiction or product, and reduce reliance on inbox memory | Alert noise grows quickly if filters are weak; does not make final legal judgments | Jurisdiction, product scope, legal entity, regulated activity map, change log | Legal or regulatory counsel |

| Policy and control mapping | Platforms with written rules that still cannot show which control satisfies which obligation | Can connect obligations to owners, approvals, and evidence; exposes gaps between policy text and implemented practice | Setup is heavy when controls vary by market; stale mappings create false confidence | Obligation inventory, control library, owner list, policy versions, evidence links | Compliance owner for the control |

| KYC, KYB, and AML orchestration | Payout programs where release depends on identity checks, customer risk, and AML gating | Can apply risk-based checks consistently, capture review history, and reduce manual handoffs | False positives add friction; edge cases still need human review | Customer and business identity data, verification results, sanctions or monitoring hits, payout status, case notes | AML officer or designated day-to-day compliance lead |

| Tax reporting workflows | Platforms collecting W-8BEN or W-9 data and preparing 1099-NEC, 1099-MISC, FATCA-related records, or Form 8938/FBAR review triggers | Can improve collection completeness, validate required tax fields before payout, and support filing prep and corrections | Bad upstream data still produces bad filings; Form 8938 and FBAR are separate obligations | TIN or foreign-status data, W-9, W-8BEN, payee type, payment classification, reportable amounts, filing status | Tax operations with tax counsel for edge cases |

| Evidence and audit trail tooling | Teams that can submit reports but cannot prove where values, forms, and approvals came from | Can create lineage from source event to filing artifact, with exportable timestamps and retention support | Requires disciplined event naming and retention rules; weak integrations break traceability | Source transaction IDs, form versions, approval timestamps, user identity, export history, retention tags | Compliance operations or internal audit |

| Case management | Organizations with repeated exceptions such as W-9 mismatches, AML alerts, SAR review, or payout holds | Can make ownership visible, track status, centralize rationale and attachments, and support SAR-related escalation lanes | Adoption stalls when legal, operations, and compliance split ownership | Case triggers, severity, assignee, due dates, linked forms, linked transactions, disposition notes | Operations manager for triage, then legal or AML for final review |

These categories solve different problems. Horizon scanning spots change. Policy mapping proves accountability. KYC, KYB, and AML orchestration routes or blocks risk. Tax workflows improve filing readiness. Evidence tooling helps defend what was filed. Case management keeps exceptions from dying in email.

For many payment environments, start with tax reporting workflows and evidence and audit trail tooling. Late or incorrect information returns can trigger IRS penalties, and intentional disregard has no maximum penalty cap. E-filing applies as of tax year 2023 if you file 10 or more information returns. The practical question is whether your data and approvals are structured enough for filing season.

Before you add optimization layers, use two quick checks:

- Trace one reported output, such as a 1099-NEC or 1099-MISC amount, back to payment records, payer or payee classification, form on file, approver, and export timestamp.

- Confirm foreign-account logic is separated correctly. Form 8938 and FBAR are separate obligations, and FBAR is FinCEN Form 114, not an IRS filing. IRS examples include different thresholds, such as $50,000 for certain Form 8938 filers versus aggregate value over $10,000 for FBAR context.

Retention also needs to be explicit in the tool design. IRS instructions call for keeping filed information returns, or reconstructable data, for at least 3 years, while BSA records have a five-year baseline. In practice, that means storing versioned W-9 and W-8BEN records, correction history, and approver identity, not just final output files.

A practical sequence is straightforward: start with the categories that reduce missed filings and unverifiable evidence, then expand into optimization. For many teams, that means tax reporting workflows plus evidence tooling first, then case management, then broader horizon scanning, policy mapping, and deeper orchestration.

For a reporting-specific example, read FATCA Compliance for Marketplace Platforms: Identifying and Reporting Foreign Account Holders.

Use this table as a control-design checkpoint. Map each category to your current payout flow, escalation owner, and evidence artifact. Then validate API and webhook fit in the Gruv docs.

Regulatory change monitoring tools#

Add this category after filing readiness and evidence controls are stable. Its job is to improve intake, classification, and ownership of new obligations, not to replace legal judgment on PSD2, GDPR, or Dodd-Frank.

FCA frames RegTech as technology that helps address regulatory challenges in financial services, and horizon scanning is a recognized part of regulatory change management. The operational failure you are trying to avoid is simple: a relevant update is seen, but nobody maps it to the right product, jurisdiction, and reviewer.

Best fit#

This category is strongest when your team keeps missing updates tied to legal anchors already in scope, such as:

- EU payments: Payment Services Directive, Directive (EU) 2015/2366 (25 November 2015).

- Privacy scope: GDPR Article 3 can apply to some non-EU entities offering goods or services to people in the Union, including where no payment is required.

- US oversight context: Dodd-Frank (Public Law 111-203, July 21, 2010).

When those obligations affect multiple product lines, manual tracking can become a material operating burden, especially at high rule volume.

What to automate first#

Start with routing discipline, not legal analysis. Set a clear internal routing target, and treat that as an operating target, not a software guarantee.

At minimum, each alert should be tagged with:

- jurisdiction

- legal entity

- product or payment flow

- obligation type

- review owner

- due date or review window

Classification features across jurisdictions and sectors can help, but routing still depends on your own product map and ownership model.

A useful checkpoint is an end-to-end notice-stream test, such as FINRA notices. Ingest the notice, tag it correctly, assign an owner, and retain the timestamp, original text, and disposition.

Main tradeoff#

The upside is broader coverage and faster handling. The downside can be alert fatigue if jurisdiction and product filters are weak.

If your team cannot classify alerts reliably by jurisdiction and product, keep legal triage manual while automating intake, deduplication, and assignment first. Ambiguous interpretation of GDPR territorial scope, PSD2 applicability, or Dodd-Frank impact still needs named legal or compliance review.

For each material notice, keep a compact evidence pack: original notice, tags, owner, review date, impacted flow, and disposition.

Related reading: What Non-Compliance Costs Gig Platforms Before Market Expansion.

Policy and control mapping systems#

If you can document obligations but cannot show which control addressed each requirement, this is the next category to add. The goal is not better policy prose. It is making ownership and evidence retrievable before release instead of reconstructed after a challenge.

This category closes the gap between written policy and operating proof. Regulators are clear that written policies and procedures alone are not enough. Practices have to match them. A mapping system helps you show that link across policy, operations, and audit records.

Best fit#

Use this when the recurring issue is: "we know the rule, but we cannot show the exact control, owner, and evidence behind the reporting outcome." That problem usually surfaces in release reviews, internal audit requests, or regulator inquiries.

It is especially valuable when compliance risk crosses business lines, entities, and jurisdictions. In those conditions, manual mapping can become hard to maintain, especially when KYC, KYB, and AML controls differ by market.

What to map first#

Start with one material obligation tied to a real release or reporting decision, then map the minimum record set:

- Obligation anchor

The requirement tied to the relevant jurisdiction, entity, and payment flow.

- Primary control owner

The individual or individuals responsible for day-to-day execution. For AML programs, 31 CFR 1020.210 requires designated compliance responsibility.

- Evidence artifact

The record showing the control actually operated, such as a review outcome, case disposition, test output, or retained decision record.

- Approval trail

The signoff showing who approved the control design or release decision, and when.

This is an operating choice, not a universally mandated format. It is useful because it forces a hard release question: can you show the control working, or can you only describe it?

Main tradeoff#

The benefit is clearer accountability and a stronger audit posture. The cost is setup complexity when similar controls are executed differently across markets and systems.

A common failure mode is stopping at policy text and broad control labels. FCA findings, published 11/11/2025, flagged firms that could not clearly explain how identified risks were being managed and mitigated. If your map cannot answer that with a named owner and a control record, it is incomplete.

Verification checkpoint#

Run one release-readiness trace before you scale. Take a single high-impact obligation and confirm you can retrieve the owner, latest execution evidence, and approval history without manual reconstruction across teams.

Also verify that independent testing is mapped where required. Under 31 CFR 1020.210, AML programs require both designated responsibility and independent testing for compliance. If owners are mapped but testing evidence is not, the framework is still incomplete.

KYC KYB and AML orchestration layers#

Use KYC, KYB, and AML orchestration when payout release depends on several risk gates and exception paths, not one isolated check. The point is to make one defensible release decision by connecting identity verification, beneficial-owner checks, sanctions or monitoring outcomes, and payout context in a single flow.

This becomes valuable when eligibility rules differ by program, entity type, or market. If reviewers have to piece together onboarding records, screening results, and transaction alerts across separate tools before deciding whether funds can move, orchestration is usually the missing control layer.

Best fit#

This is the right fit for payout processes where individuals or businesses must clear identity and risk checks before execution, and exceptions need to be routed with context. Under 31 CFR 1020.220, a Customer Identification Program includes risk-based identity verification procedures. Under 31 CFR 1010.230, covered institutions must have written procedures to identify and verify beneficial owners of legal-entity customers. EU customer due diligence also includes ongoing monitoring and transaction scrutiny throughout the relationship, not just at onboarding.

In practice, that matters because risk can change after onboarding. Orchestration keeps later monitoring outcomes tied to the payout decision instead of leaving them scattered across systems.

What good orchestration actually does#

- Applies risk-based gates before release

It checks whether required KYC, KYB, and AML conditions are met for the relevant program, then holds or routes exceptions instead of relying on manual memory of policy branches.

- Escalates with usable context

Reviewers can see the trigger, prior verification status, beneficial-owner findings, monitoring or sanctions hits, and current payout details in one case. For rejected transactions under OFAC rules, 31 CFR 501.604 requires enough detail to identify the transaction, including items like reference numbers, account numbers, and dates.

- Keeps monitoring proportionate to scale and risk

FCA guidance states that transaction-monitoring design depends on business nature and scale, and that some smaller firms can monitor effectively with manual procedures.

Main tradeoff#

The benefit is fewer missed policy gates and less manual stitching across tools. The cost is operational friction when false positives, duplicate entities, or weak tuning send too many cases into review queues.

BIS guidance is useful here: ongoing monitoring should help detect suspicious activity and reduce false positives. If alerts increase but case quality does not, control quality has not improved. Siloed monitoring can be a failure mode, especially in cross-border, multi-program environments where decisions need shared context.

Decision rule#

Use a lighter model when complexity is limited, and move to configurable policies as complexity becomes structural.

- Lower volume, narrow jurisdiction set: often start with simpler rules, manual review, and clear hold reasons. Confirm each hold maps to the exact identity, beneficial-owner, or monitoring condition.

- Higher volume, multi-market operations: often invest in configurable risk policies, per-program routing, enhanced due-diligence paths for higher-risk cases, and senior-management reporting on monitoring performance and remediation.

Before rollout, run one end-to-end payout trace on a real business account. You should be able to retrieve the identity-verification result, beneficial-owner record, latest monitoring outcome, reviewer disposition, and release or hold action without manual reconstruction.

Tax document and filing support tools#

Use tax document and filing support tools when the control gap is collection quality and filing readiness, not document storage. Once identity and risk checks are in place, you still need the right tax record to support payout eligibility decisions and prepare reporting correctly.

The value here is cleaner intake and fewer filing surprises across W-9, W-8 BEN, 1099-MISC, 1099-NEC, FATCA/Form 8938, and FBAR (FinCEN Form 114) steps. The tradeoff is direct: if payee type, TIN data, payment category, or foreign-account facts are wrong upstream, software will scale the error.

Where these tools fit best#

This category fits teams that tie tax profile completeness to payout release. Form W-9 supports collecting the payee TIN for information-return reporting, and Form W-8 BEN supports foreign beneficial-owner intake for U.S. withholding and reporting context.

Treat the tool as a control layer, not a passive vault. It should gate payout readiness on form presence and completeness, keep versioned document history, and preserve an auditable correction trail.

It also helps to separate form collection from reporting classification. Collection is one decision. Mapping payments to the right return is another. Form 1099-NEC reports nonemployee compensation. Form 1099-MISC covers other categories, including at least $10 royalties or broker payments in lieu of dividends or tax-exempt interest, and at least $600 in categories such as rents, prizes and awards, other income payments, and medical and health care payments.

The lifecycle checkpoints that matter#

A workable tool should support the full lifecycle from intake through retention evidence.

| Checkpoint | What the tool should handle | Operator detail that matters most | Common failure mode |

|---|---|---|---|

| Collection | Gather the correct form at onboarding, for example W-9 for U.S. payees or W-8 BEN for foreign beneficial owners | Capture submission date, payee identity, and exact form status before payout release | Wrong form selected and not caught until filing season |

| Validation | Enforce completeness and obvious mismatches before payout eligibility | Missing or incorrect TIN data can trigger withholding obligations on certain reportable payments | Forms are collected but required fields are not enforced |

| Correction loop | Route pre-filing and post-filing corrections with explicit workflow | 1099-MISC and 1099-NEC corrections require correct handling; misuse of the VOID box can invalidate remediation | Corrections handled as ad hoc edits without QA |

| Filing prep | Build outputs by lane, destination, deadline, and delivery requirement | From tax year 2023, 10 or more information returns must be e-filed; Form 1099-NEC is due January 31; recipient statements must also be furnished | Teams submit to IRS but miss recipient delivery or e-file rules |

| Retention evidence | Preserve source documents, status changes, and submission records | FBAR processes include recordkeeping duties, so account record trails must be recoverable | Final files saved without usable source-history evidence |

Separate filing lanes before they get conflated#

Keep IRS and FinCEN lanes separate. Form 8938 does not replace FBAR, and FBAR (FinCEN Form 114) is filed with FinCEN, not the IRS.

That separation should show up in queue design and submission logic. FBAR is filed through the BSA E-Filing System and is due April 15 with an automatic extension to October 15. It applies when aggregate foreign financial accounts exceed $10,000 at any time in the calendar year. Do not collapse these into one generic foreign-reporting status.

What to verify before go-live#

Before rollout, run two end-to-end traces: one U.S. payee expected in a 1099-NEC lane and one account with foreign-person documentation such as W-8 BEN. You should be able to retrieve the original form, each status change, correction requests, current payout eligibility, and final reporting bucket without manual reconstruction across teams.

If your process still depends on email attachments, shared drives, and year-end CSV cleanup, move collection and correction controls earlier in onboarding before expanding filing automation. Intake quality and correction evidence are the core controls here.

Regulatory reporting and evidence repositories#

If your team can file reports but cannot reliably defend them during an inquiry, the gap is evidence lineage. A good repository should let you prove which event, records, decisions, and export produced each submission without rebuilding the story from inboxes and shared drives.

The upside is stronger traceability from source event to filing. The constraint is operational discipline. This works best when event labels, retention rules, and version history are consistent and enforced.

What a good repository actually stores#

You need a linked evidence chain, not a document dump.

- Event record

Store the originating trigger with a stable ID, timestamp, actor, and affected record so the filing can be traced back to source data.

- Decision and approval history

Preserve who reviewed, what was decided, when it was decided, and what evidence was available at that moment.

- Reporting artifact

Keep the exact exported file or submission dataset plus supporting documentation tied to that event.

That structure matters because some regimes explicitly treat supporting documentation as part of the filed record and require retention for 5 years from filing. In SEC books-and-records contexts for covered firms, regulators may require both the record and its audit trail in a usable electronic format. For specified Rule 17a-4 records, preservation can run 6 years, with the first 2 years easily accessible.

The control detail that separates usable evidence from shelfware#

The core test is whether history survives change. For covered SEC entities, recordkeeping can be handled through WORM preservation or an audit-trail approach that still allows recreation of the original record after modification or deletion. Even where those exact rules do not apply, that is a useful benchmark for repository design.

Before go-live, test one completed reporting case and confirm you can retrieve the original source record, each status change, approvals, and final export without cross-team reconstruction. Then change a noncritical test field and verify the prior state is still reconstructable.

Where teams usually fail#

A common failure is naming and retention drift. If event labels are inconsistent across teams, lineage breaks quickly and filed outputs become hard to defend.

The second failure is applying one retention period across all reporting lanes. Retention obligations are perimeter-specific, so legal or compliance still needs to map which rule applies to which lane before you scale automation.

For a step-by-step walkthrough, see HMRC Reporting Rules for Platforms for UK Marketplace Operators.

Case management and escalation tooling#

Case management works best when exceptions are frequent and you need consistent ownership, deadlines, and escalation paths. Use it to automate intake and routing for AML alerts, tax-form mismatches, and cross-border payout holds. Before rollout, set ownership across legal, compliance, and operations so escalation does not drift between teams. In U.S. AML contexts, regulators expect designated individuals responsible for coordinating and monitoring day-to-day compliance, not just a queue.

- AML and suspicious activity cases

Automate case creation when monitoring flags patterns for review, but keep SAR filing judgments with trained staff. In U.S. bank SAR rules, reporting can hinge on transactions involving or aggregating at least $5,000. Filing is due within 30 calendar days from initial detection, or up to an additional 30 calendar days if no suspect is identified, capped at 60 calendar days. Build deadline-aware routing with attached evidence: alert reason, transaction history, account profile, prior reviews, and timer start date. Activity at or near the $10,000 CTR threshold alone is not enough to require filing a SAR.

- Tax-form mismatch and withholding cases

Open cases automatically when TIN data is missing, a W-9 conflicts with account data, or foreign-entity documentation is incomplete. Some outcomes are rule-driven once facts are confirmed, including potential 24% backup withholding in specified IRS cases and 30% FATCA withholding for certain undocumented foreign entities. Keep a compact evidence pack: form version, validation failure, outreach history, and payout impact. Do not collapse FATCA and backup-withholding logic into one rule just because both can pause money movement.

- Cross-border and privacy-impact holds

Auto-create cases for unresolved jurisdiction conflicts, sanctions-related geography signals, or payout restrictions that may have legal effect on the user. Where GDPR Article 22 safeguards apply, do not make final legal-impact decisions solely through automation because people may have the right to human intervention. Define explicit triggers for legal interpretation, not just risk scores. Before launch, verify operations can reassign a case to legal without losing decision history or attachments.

Integration requirements before rollout#

Before rollout, verify that the integration is replay-safe, ledger-linked, and audit-retrievable under real retry conditions. A polished demo does not matter if production retries can create duplicate actions, stale decisions, or reporting gaps.

- Idempotent write handling

Any API action that can change money movement, account status, or reporting records should be idempotent per provider. Your spec should show how keys are generated, stored, and aged. Stripe keys can be up to 255 characters and may be pruned after they are at least 24 hours old. PayPal uses PayPal-Request-Id for POST idempotency. Adyen keys are valid for a minimum of 7 days. Treat "we support retries" as insufficient unless duplicate-request behavior is clear for each provider.

- Replay-safe webhook consumption

Webhook consumers should assume retries and deduplicate explicitly. Stripe can resend undelivered events for up to 3 days, and undelivered-event recovery returns only the last 30 days, so you need more than a happy-path listener. Run a replay test by sending the same event multiple times and confirm one business side effect, a traceable audit record, and success responses on duplicates so retries stop. If you process snapshot payloads, fetch current resource state before acting because payload data can be stale.

- Ledger-backed event linkage

Compliance events should map to the transaction and ledger references finance uses, including reconciliation workflows such as dispute handling. For each event-driven decision or status change, you should be able to trace the external event ID, internal transaction or ledger ID, account ID, decision timestamp, and actor or service. Without that linkage, teams can see different states and still fail to prove what caused the business outcome.

- Retention and reconstruction of reporting evidence

Retention controls should prove retrieval and reconstruction, not just storage. Under 31 CFR 1010.430(d), required records must be retained for 5 years and remain accessible within a reasonable period of time. For IRS information returns, keep filed copies or reconstructable data for at least 3 years. Ask vendors what exports are available, which join keys persist, and whether filed output can be rebuilt from transaction records. A practical proof test is tracing one reported item from event intake, to current-state fetch, to ledger entry, to approval trail, to filed output.

For a broader platform view, read Why RegTech Creates a Compliance Moat for Gig Platforms.

Common implementation failures and how to avoid them#

Many failures come from implementation quality, not tooling alone. A safer order is to tailor controls to your actual payout model, set governance before tooling, and prove quality in a narrow pilot before scaling.

- Copying generic FinTech templates

Generic templates fail when they do not match your real payout flow. If you use specialized payout structures, map controls to those realities instead of using a default checklist. FATF's risk-based approach is the anchor: implementation should be adapted to your particular circumstances. Use a hard checkpoint: trace one reportable event from onboarding data to payout decision to filed output, and confirm decision owner, evidence used, and ledger linkage.

- Buying compliance software before defining ownership and evidence standards

Software does not fix unclear accountability. The OCC's compliance management system framing starts with governance, policies and procedures, monitoring and testing, and audit, not tooling alone. Before rollout, define for one obligation the named owner, evidence standard, and escalation trigger. Without that, you risk storing unresolved exceptions instead of producing defensible decisions.

- Scaling before a narrow pilot proves reporting quality

Expand only after a pilot shows measurable control quality. A time-bounded pilot approach is consistent with how the BoE/FCA tested Digital Regulatory Reporting in a six-month pilot. For a controlled start, limit scope (for example, one jurisdiction and one reporting obligation), then scale only when error rates improve, reconciliations are stable, and audit reconstruction is reliable. This matters because the FCA has said reporting data is not always consistent, timely, or of sufficient standard to be useful.

- Automating through unresolved legal ambiguity

When obligations are unclear or conflict, pause automation changes and document assumptions first. Keep an assumption log tied to each rule decision, then escalate for specialist legal review before further automation. This is a control issue, not a speed issue. The EBA said on 28 July 2025 that over half of serious compliance failures in EuReCA involved improper RegTech use, and pointed to weak expertise and oversight as recurring causes.

Conclusion#

Treat RegTech as controlled automation for regulatory reporting, not as a substitute for legal judgment. Technology can improve compliance outcomes and efficiency, but accountability stays with management, and that responsibility does not disappear when third-party tools are involved.

- Keep the operating model explicit

Automate structured tasks, but keep interpretation, exceptions, and final accountability with named people. Use one clear owner for the obligation, one approver for exception decisions, and one evidence set that shows what happened and when. Without that, you have speed, not control.

- Start with one high-risk reporting lane

Prioritize the lane where missed deadlines, weak source data, or poor evidence would cause the most harm, then automate in sequence. This follows a risk-based approach: allocate effort to the highest-risk area first. In practice, that can be a U.S. tax lane with a hard January 31 deadline for Form 1099-NEC, or a BSA lane where records must be retained for five years.

Define the lane before expanding tooling:

- obligation and jurisdiction

- source records and required fields

- owner, reviewer, and escalation path

- filing output and retention evidence to preserve

- Scale only after one lane is defensible end to end

Compare your current process against the earlier comparison table, then build a phased plan based on your market coverage and risk profile. Narrow footprints may need proportionate controls; higher-risk or more complex operations usually need stronger evidence lineage, clearer escalation ownership, and tighter links between transaction records and filing outputs.

Use phase one as a verification checkpoint: trace one report from source event through validation, approval, filing artifact, and retained record. For tax intake, that can include how a Form W-9 was collected, checked for completeness, corrected, and tied to the information-return workflow. If one lane is not defensible, adding more lanes can multiply exceptions instead of reducing them.

For the next step, see How to Build a RegTech Stack for Payment Platforms: Tools and Vendors by Compliance Function.

If your next step is a pilot in one high-risk reporting lane, align legal, compliance, and ops owners first, then contact Gruv to confirm market/program coverage and rollout constraints.

Frequently Asked Questions

What is RegTech for payment platforms in practical terms?

It is technology used to improve compliance outcomes in reporting workflows, not just speed. In payout operations, that can include collecting, validating, routing, filing, and evidencing reporting data with a clear approval trail. The practical value is better control over onboarding records, tax form data, filing prep, and who approved each decision.

Which parts of regulatory reporting can we automate safely right now?

Start with structured, repeatable steps: intake, completeness checks, deadline tracking, case routing, reconciliations to ledger events, and filing mechanics where batch submission is supported. The BSA E-Filing system supports individual or batch filing, and the IRS requires e-filing once you reach 10 or more information returns. A good control test is tracing one return end to end and confirming data lineage, ownership, timestamps, and filing output.

What should remain manual for legal and compliance teams?

Keep legal interpretation, exception approval, and ambiguous scope decisions under human ownership. That matters most when obligations conflict or depend on qualitative or expert judgment. Human review should also focus on reporting quality, not just whether a submission was sent.

Can RegTech replace compliance staff or only reduce manual load?

It should reduce manual load, not replace accountable compliance judgment. The control standard is effective challenge: qualified reviewers should critically assess automated outputs instead of accepting them by default. If a tool promises no-review compliance, treat that as a control risk.

How does RegTech reduce reporting errors in multi-market operations?

It can reduce errors by standardizing required data, evidence fields, and approval records before deadlines compress decision time. That consistency can lower the risk of missed forms, duplicate filings, and classification mistakes across jurisdictions. It also helps teams keep separate obligations separate, including FinCEN Form 114 (FBAR) and Form 8938, which may both apply.

What should we implement first if we are still using spreadsheets and email?

Start with one recurring obligation where deadlines and evidence requirements are clear, then add ownership and exception routing around it. Tax-form data intake and validation is a practical first lane because upstream data defects can quickly create downstream filing problems. In some cases, bad payee tax data can also trigger 24 percent backup withholding exposure.

What escalation triggers should send a case to legal counsel?

Escalate when the obligation is unclear, jurisdictions appear to conflict, or you cannot classify the account or payment with confidence before a deadline. Timing matters in SAR workflows: the base window is 30 calendar days from initial detection, with only an additional 30 calendar days if no suspect is identified. Escalate early when facts could create overlapping obligations, including whether FBAR and Form 8938 both apply.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.

How to Respond to a Subpoena for Business Records

Move fast, but do not produce records on instinct. If you need to **respond to a subpoena for business records**, your immediate job is to control deadlines, preserve records, and make any later production defensible.

A US Expat's Guide to Investing in UCITS ETFs to Avoid PFIC Issues

The real problem is a two-system conflict. U.S. tax treatment can punish the wrong fund choice, while local product-access constraints can block the funds you want to buy in the first place. For **us expat ucits etfs**, the practical question is not "Which product is best?" It is "What can I access, report, and keep doing every year without guessing?" Use this four-part filter before any trade: