Quick Answer

US expats should use UCITS ETFs only when broker access is confirmed and a repeatable annual PFIC reporting process is in place. The article recommends starting with a simpler Bedrock setup, then moving to a Core UCITS route only if product availability, records, reporting inputs, and preparer support are all documented and sustainable each year.

Escaping the Expat Investor's Catch-22: A Strategic Framework#

The real problem is a two-system conflict. U.S. tax treatment can punish the wrong fund choice, while local product-access constraints can block the funds you want to buy in the first place. For us expat ucits etfs, the practical question is not "Which product is best?" It is "What can I access, report, and keep doing every year without guessing?" Use this four-part filter before any trade:

| Filter | What to assess |

|---|---|

| Compliance risk | Could this choice create a known U.S. tax trap, disclosure issue, or other reporting exposure? |

| Admin burden | What records and account details will you need to keep and review each year? |

| Maintenance cost | What extra platform, advice, fund, or tax prep cost comes with the structure? |

| Implementation effort | Can you actually open, fund, and keep the account working from your country of residence? |

- Compliance risk: Could this choice create a known U.S. tax trap, disclosure issue, or other reporting exposure? The downside is not theoretical. Examples include tax rates up to 100% on gains, loss of 40% of assets to estate taxes, and large fines for non-disclosure.

- Admin burden: What records and account details will you need to keep and review each year? If the filing workflow is hard to describe, it is usually harder to maintain than it first appears.

- Maintenance cost: What extra platform, advice, fund, or tax prep cost comes with the structure? Even small ongoing cost drag can compound over time.

- Implementation effort: Can you actually open, fund, and keep the account working from your country of residence? Access can fail for operational reasons alone, including residency limits and AML friction.

Think in lanes, not upgrades. You can call them Bedrock for situations with unresolved access or reporting uncertainty, Core for setups where access and annual reporting are clearer, and Edge for setups that add complexity and require tighter monitoring. Use these as planning labels, not formal legal categories.

Before moving up a lane, check the basics in writing. Confirm your current country of residence. Confirm broker residency eligibility. Confirm the account classification and constraints shown by your broker. Note what documents you will retain. Stop if any classification, access, or filing step is uncertain, and verify that any guidance fits your individual circumstances. If you need a tax backdrop before deciding, read The Ultimate Digital Nomad Tax Survival Guide for 2025.

Related: How to Amend a Tax Return as a US Expat (Form 1040-X).

The Expat Investor's Dilemma: PFIC vs. PRIIPs#

Your constraint is not just tax or just access. It is the interaction between the two: one set of rules can punish what you hold for U.S. tax purposes, while another can limit what your broker will let you buy where you live.

For U.S. persons abroad, PFIC risk is the core tax-side problem with many non-U.S. funds, and the downside can be severe if you get it wrong. On the access side, local EU/UK retail-product rules can restrict availability in practice, so a product that looks fine on paper may still be blocked in your account.

Use this quick pre-trade check:

| System | What can go wrong | What to confirm before you buy |

|---|---|---|

| U.S. tax (PFIC) | A foreign fund choice can create punitive U.S. treatment and ongoing reporting burden | Whether the holding creates a PFIC workflow you and your preparer can run every year |

| Local retail access (PRIIPs context) | Your broker may not offer the product in your account setup | Whether the exact product is available to your account in your country of residence |

| Account operations | Cross-border onboarding and servicing friction can block execution | Residency status, account permissions, and records you must retain |

Also, do not assume FEIE or FTC automatically solves this investing problem. Cross-border investors can still be exposed to overlapping regimes.

Before placing an order, verify product availability in your specific account and document your reporting path so it stays manageable each filing cycle. If you and your preparer are evaluating PFIC reporting details, review the latest Form 8621 instructions.

If you want the lowest-complexity path, stay in the Bedrock lane and avoid products that trigger this conflict. If you want ETF diversification, move forward only with a clearly defined compliance path.

Related: Form 8621 PFIC Reporting for US Expats Without Guesswork.

For a step-by-step walkthrough, see How to Handle Tax on US Partnership Income as an Expat.

Tier 1: The Bedrock Foundation (Maximum Compliance, Minimum Complexity)#

Start here if you want the lowest-friction path: keep the setup simple, make compliance operations repeatable, and add complexity only after the base works under normal workload.

Build around operational simplicity first#

Tier 1 works when your process is easier to run than to break. Once you add jurisdictions and strategies, the moving parts multiply, so your default should be to keep the structure narrow until your workflow is stable.

| Bedrock checkpoint | Practical default | Why it matters |

|---|---|---|

| Jurisdiction footprint | Keep it as limited as practical | Multi-jurisdiction portfolios are harder to manage |

| Support stack | Confirm access to legal, compliance, company secretary, and fund administration support | These are core operating functions, not optional extras |

| Domicile choice | Treat fund domicile as a deliberate decision, not an afterthought | A suitable domicile is a critical success factor |

| Expansion timing | Add sophistication only after the base process is reliable | Complexity compounds faster than expected |

Use a clear decision rule before adding complexity#

If a new holding or structure increases coordination burden, pause and define who will run each recurring task and how records will be maintained. If you cannot explain the operating path in plain language, stay in Bedrock and defer the change.

In some setups, onshoring can be part of that stability decision if you need clearer economic substance in the jurisdiction where the fund or manager operates.

Keep your compliance workflow auditable#

Your goal in Tier 1 is controlled execution, not chasing every possible product. Keep key account and reporting records together, and review your process on a fixed cadence so complexity does not creep in unnoticed.

For official filing instructions and current limits, use primary IRS pages directly: current limit and FBAR.

We covered related account-opening and relocation issues in Opening a European Brokerage Account as a US Citizen in 2026 and Munich Expat Guide for Remote Professionals in 2026.

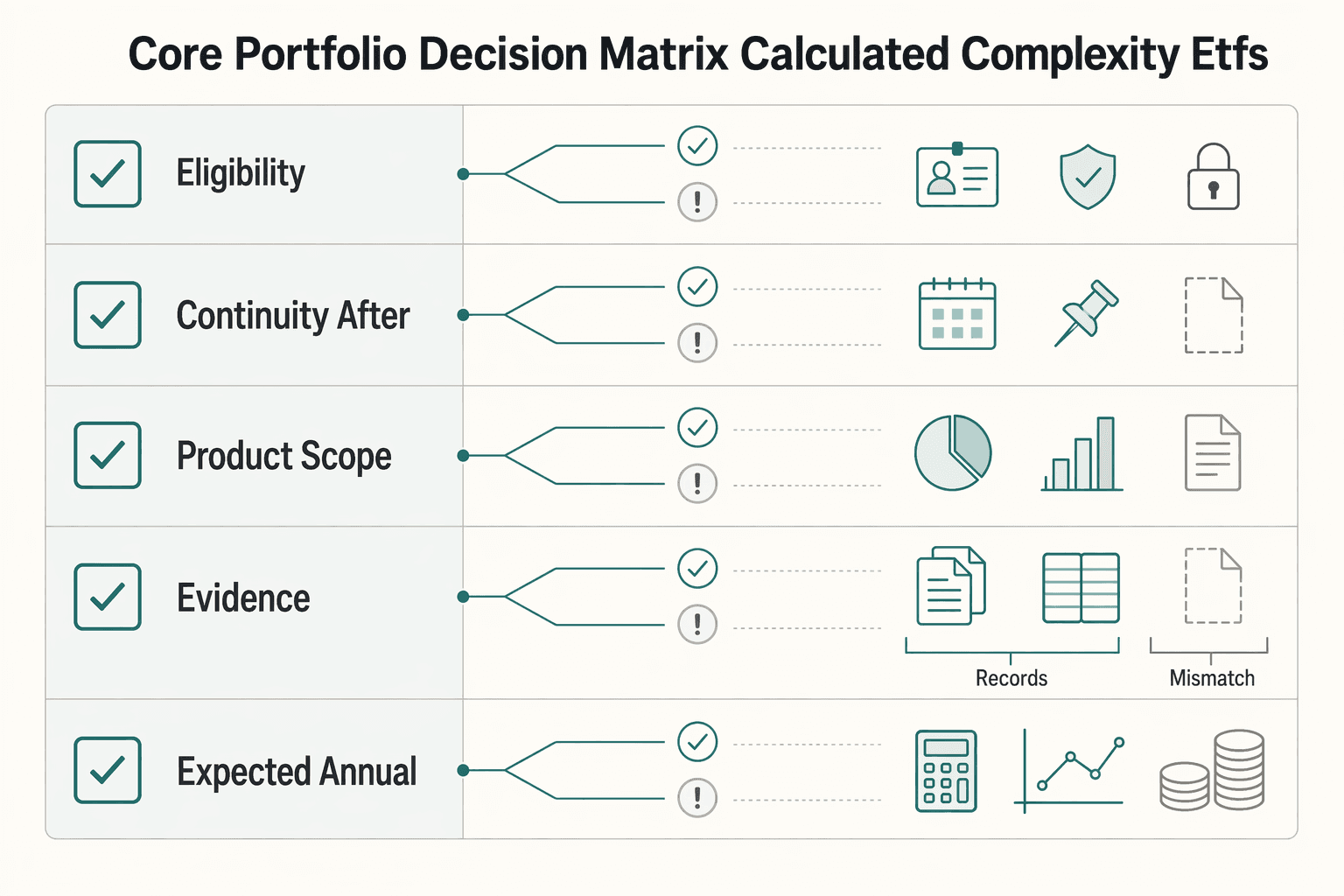

Tier 2: The Core Portfolio Decision Matrix (Calculated Complexity for ETFs)#

Use Tier 2 only after Bedrock runs cleanly: test professional-client access first, and use a UCITS route only when a repeatable PFIC/QEF operating process is confirmed for your account and preparer.

| Decision gate | Professional-client route | UCITS with annual reporting route |

|---|---|---|

| Eligibility | Broker-specific classification required. Verify the current criteria with the broker or advisor for this exact account before relying on the route. If your exact account is approved in writing, proceed. If approval is verbal or still under review, pause. | No client-status gate, but proceed only if reporting inputs exist and your preparer confirms they can use them for your facts. If either is missing, fall back to Bedrock. |

| Continuity after moves or reviews | Confirm whether status survives residence changes, account transfers, and periodic reviews. If continuity is unclear, pause. | Confirm who collects annual inputs, stores them, and delivers them to the preparer each year. If ownership is unclear, fall back to Bedrock. |

| Product-scope fit | Confirm the status unlocks the ETF category you plan to use. If scope is narrower than expected, fall back to Bedrock. | Confirm each intended fund can be supported in your reporting workflow before purchase. If support is uncertain fund by fund, pause. |

| Documentation burden | Keep approval evidence, date, account number, and proof of live trading access. If you cannot document the route, do not allocate until documented and pause. | Keep annual fund reporting packages, statements, lot records, and a preparer-ready handoff file. If that pack cannot be assembled upfront, fall back to Bedrock. |

| Expected annual compliance cost | Verify the current cost and review cadence with the broker or advisor before relying on this route. If either is unclear, pause. | Verify the current recurring prep cost and advisor capacity with your tax preparer or advisor before relying on this route. If either is unclear, fall back to Bedrock. |

| Failure risk | Key risks: status loss, reclassification after a move, or approval that does not match intended products. If one failure would force an unwind, fall back to Bedrock. | Key risks: missing inputs, late handoff, or preparer capacity gaps. If you cannot tolerate that annual dependency, fall back to Bedrock. |

Professional-client route#

This lane works only when access is proven, not assumed. Do not allocate until it is documented.

Pre-trade checklist:

- Written status confirmation for the exact account that will trade.

- Continuity answer for country moves, compliance reviews, and account transfers.

- Product-scope confirmation for the ETF category you actually plan to buy.

Keep the evidence pack with your account records: approval notice, effective date, and proof of instrument availability. If access is ambiguous or temporary, pause new Tier 2 allocation and fall back to Bedrock.

UCITS route#

If professional status is unavailable, this becomes a recurring annual operations lane. Before selecting it, review A Deep Dive into PFIC Rules for US Expats Investing Abroad to validate the compliance path for your situation.

| Owner | Responsibilities |

|---|---|

| Investor | Identify funds, confirm reporting inputs before purchase, keep statements and lot-level records, and maintain a dated tax-year folder. |

| Preparer | Confirm they can use the fund inputs for your facts, define required documents, and set filing-season timing. |

| Shared checkpoint | Lock a handoff date, format, and fallback plan for late or incomplete fund packages. |

Assign ownership before any trade and keep it explicit:

- Investor: identify funds, confirm reporting inputs before purchase, keep statements and lot-level records, and maintain a dated tax-year folder.

- Preparer: confirm they can use the fund inputs for your facts, define required documents, and set filing-season timing.

- Shared checkpoint: lock a handoff date, format, and fallback plan for late or incomplete fund packages.

Fail fast: if reporting inputs are inconsistent, preparer capacity is uncertain, or the annual handoff cannot be described clearly, fall back to Bedrock.

Acc vs Dist and domicile are operating decisions tied to reporting workflow, cash handling, and tax-prep friction, not performance narratives. Verify the current treatment detail with your preparer, broker, or official fund and tax records before using them in the plan.

If you are still comparing where this can realistically be held, see The Best Brokerage Accounts for US Expats. Related: Compliance-First Investment Vehicles for U.S. Expats With Clean Reporting.

Tier 3: The Edge (Advanced Strategies for Maximum Sophistication)#

Use Tier 3 only if you can run it as an operations system, not a product experiment. If Tier 2 already feels heavy, stop there. This tier is optional and only makes sense when monitoring, advisor coordination, and downside planning are already stable.

| Edge checkpoint | What to confirm first | Why it matters |

|---|---|---|

| Platform route | Classify access as DIY (retail) or advisor-led (through an advisor). | Route confusion causes execution and ownership mistakes. |

| Fee clarity | Normalize the full fee stack in plain language before allocating. | Platform terminology and fee structures vary, which can hide real cost and friction. |

| Failure plan | Write down what happens if the setup goes wrong and who owns each response step. | Edge setups have higher downside if decisions are improvised. |

| Strategy disclosure load | Confirm what disclosures and reporting obligations apply to your exact setup. | Advanced strategies can add ongoing compliance overhead. |

Synthetic exposure through options#

Treat this as an execution-heavy lane. Before the first trade, confirm your access route, fee language, and monitoring ownership so you are not making live decisions from a vague support-chat answer.

Keep the process explicit: who monitors positions, who coordinates with your tax advisor, and what your fallback is if platform conditions or liquidity are not what you expected. If that operating checklist is not documented, stay in Tier 1 or Tier 2.

Direct foreign operating-company holdings#

This lane works only if you are prepared for recurring classification and documentation work each year with qualified tax support. If that annual process is not already defined, do not use this as a shortcut around simpler tiers.

Keep your decision rule strict: if evidence quality or advisor readiness is unclear, default back to simpler structures. For PFIC context and tradeoffs, read A Deep Dive into PFIC Rules for US Expats Investing Abroad.

Default to Tier 1 or Tier 2 unless every Edge criterion is met and documented. For a step-by-step walkthrough, see What Is a Qualified Electing Fund (QEF) for PFICs?.

If you want a deeper dive, read Claiming the American Opportunity Tax Credit as an Expat.

Conclusion: From Paralysis to a Confident Action Plan#

The right answer is usually smaller than the menu of options makes it look. Pick the highest tier you can still maintain in a normal year, with ordinary admin time, ordinary broker support, and no heroic cleanup later.

Keep the definitions plain. Product labels, wrapper names, and access terms can vary by broker and account setup. Verify terminology, access, and eligibility directly before buying. If your plan depends on any threshold, minimum, or eligibility test, note the current figure only after you verify it against the relevant broker, advisor, tax source, or official records.

| Tier | Stay here when | Verify before moving up | Common failure mode |

|---|---|---|---|

| Bedrock | You want the cleanest ongoing setup and do not need extra product access to meet your goal | That your current account and plain-vanilla holdings already cover the exposure you need | Chasing a different wrapper when the same underlying portfolio was already available in a simpler form |

| Core | You need a specific fund path badly enough to accept more ongoing coordination | Broker access, product documents, recordkeeping burden, and who handles reporting | Buying based on the ETF label instead of confirming the underlying exposure, costs, and annual admin |

| Edge | You already operate Bedrock and Core cleanly and still need more precision | Specialist support, execution controls, cash handling, and exit rules before the first trade | Using a complex trade to solve an access problem and creating a larger monitoring problem instead |

That middle checkpoint matters. The same underlying portfolio can show up in multiple wrappers or share classes, so verify what you actually own, not just the ticker or share-class label. Also watch the cost trap: ETFs trade intraday, but spreads and commissions can add friction. A cheaper-looking wrapper is not cheaper if execution costs and admin rise with it.

Use this short checklist and keep ownership explicit:

- You: write a one-sentence tier boundary for the next 12 months. Example: "I stay in Bedrock unless broker access and reporting support are both confirmed in writing."

- Broker: confirm the exact product path available in your account, including the actual wrapper or share class you can buy. If a cost or minimum figure comes from an old article, re-check it. Even one source can show inconsistent figures, such as Admiral-share minimums listed as both $10,000 and .04% / $3,000.

- Advisor: confirm, before purchase, who will support recurring reporting and recordkeeping for each holding and what documents you should retain each year.

- Stop rule: if product access is not verified, or the reporting process is not verified, do not buy.

Before you move up a tier, write a one-page operating note for the next filing season. Record the exact account, wrapper, reporting owner, annual document handoff date, and the condition that sends you back to Bedrock if any one of those breaks.

Use the same note to map what happens after a move, broker review, or advisor change. If no one owns the records, no one owns the risk, and Tier 2 becomes harder to maintain than it looked during research.

Keep your upgrade rule just as explicit. Do not add a new fund or structure until access, reporting, and exit conditions are all confirmed in writing. When those three items are clear, the product choice is manageable. When they are vague, Bedrock is still the safer default.

When should I stay in Bedrock?#

Stay there when your current account already gives you workable market exposure and the next tier only adds hassle. If access, product documents, or reporting ownership are still fuzzy, Bedrock is the better choice.

When are us expat ucits etfs worth the extra overhead?#

Only when they solve a real access problem you cannot solve more simply. Before you buy, confirm the broker path, the exact exposure, and the recurring admin burden. Do not upgrade just because an ETF wrapper looks familiar.

When should I escalate to a specialist?#

Escalate when the answer depends on unclear product access, execution costs, or reporting you cannot confidently explain end to end. Broker choice often determines which product paths are practical, so compare that first with The Best Brokerage Accounts for US Expats.

This pairs well with our guide on The Freelancer's Year-End Tax Prep Checklist (US Expat Edition).

Frequently Asked Questions

When should I stay in Bedrock?

Stay there when your current account already gives you workable market exposure and the next tier only adds hassle. If access, product documents, or reporting ownership are still fuzzy, Bedrock is the better choice.

When are us expat ucits etfs worth the extra overhead?

Only when they solve a real access problem you cannot solve more simply. Before you buy, confirm the broker path, the exact exposure, and the recurring admin burden. Do not upgrade just because an ETF wrapper looks familiar.

When should I escalate to a specialist?

Escalate when the answer depends on unclear product access, execution costs, or reporting you cannot confidently explain end to end. Broker choice often determines which product paths are practical, so compare that first with The Best Brokerage Accounts for US Expats. This pairs well with our guide on The Freelancer's Year-End Tax Prep Checklist (US Expat Edition). Want to confirm what’s supported for your specific country/program? Talk to Gruv.

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 5 external sources outside the trusted-domain allowlist.

- nlp.stanford.edu/~lmthang/morphoNLM/cwCsmRNN.wordstrusted

- snap.berkeley.edu/project/14165954trusted

- snap.berkeley.edu/project/10053261trusted

- avca.africa/media/thklrk31/02115-avca-kifc-funds-report_...external

- bankeronwheels.com/ucits-etfs-vs-us-funds-for-non-us-investorsexternal

- bankeronwheels.com/investing-guidesexternal

- bogleheads.org/wiki/Non-US_investor%27s_guide_to_navigating...external

- bogleheads.org/wiki/US_tax_pitfalls_for_a_US_person_living_...external

Educational content only. Not legal, tax, or financial advice.

Related Posts

Digital Nomad Taxes in 2026 With a Defensible Filing Plan

With digital nomad taxes, the first move is not optimization. It is figuring out where you may be taxable, where filings may be required, and what proof supports that position.

PFIC Rules for US Expats Investing Abroad

Start with compliance, not optimization. Screen PFIC risk before you buy, rebalance, or add cash. A common costly mistake is buying a familiar local fund first and checking PFIC classification later.

The Best Brokerage Accounts for US Expats

**Choose your brokerage account as a U.S. expat by prioritizing account viability and day-to-day operability, not headline fees or fancy features.** If you live abroad and want a serious investing setup, the real constraint is simple: will a broker let you onboard cleanly, keep your account working as your address changes, and move money without operational freezes? As the CEO of a business-of-one, your job is to choose systems that keep running even when your location changes.