Quick Answer

For third party settlement organizations, the current federal Form 1099-K filing baseline is more than $20,000 in gross reportable payments and more than 200 transactions. Platform operators should treat this as a controls update: confirm the latest IRS source and date, identify superseded phase-in thresholds, pause net-new automation until policy is reapproved, and keep filer-role, counting, and evidence decisions traceable.

Why platform operators should revisit 1099-K controls now#

This is a controls update, not a news recap. If your Form 1099-K program was built around transition-era assumptions, recheck it against the current IRS baseline before you change workflow or code.

The planning baseline changed. In IR-2025-107 (issued Oct. 23, 2025), the IRS released Fact Sheet 2025-08, which says the One Big Beautiful Bill retroactively reinstated the reporting threshold that applied before ARPA. For third party settlement organizations, IRS FAQs say filing is not required unless both tests are exceeded: more than $20,000 and more than 200 transactions. The same fact sheet says these FAQs supersede FS-2024-03.

That creates a practical risk for teams that implemented to the delay path. The IRS had announced a tax year 2023 delay of the new $600 threshold and a planned $5,000 threshold for 2024. Notice 2024-85 then described 2024 and 2025 as a final transition period with phased amounts of $5,000 (2024), $2,500 (2025), and $600 (2026 and after). If your policy docs, monitoring rules, or reporting specs still point to that sequence without reconciling the later IRS update, your controls can drift out of alignment.

Before you touch code, run a governance check. The goal is operational clarity, not theory.

- confirm which IRS sources and dates your current policy, specs, and tickets cite

- flag stale anchors, such as unreconciled FS-2024-03 or transition-phase thresholds

- pause net-new automation changes until the legal baseline is reapproved internally

You should come away with:

- decision checkpoints to confirm the current federal baseline before workflow changes

- ownership boundaries across compliance, tax, finance ops, and engineering

- a quarter-by-quarter checklist for thresholds, exceptions, approvals, and filing readiness

These IRS materials define the Form 1099-K reporting baseline and the PSE filing role; they do not spell out your internal ownership model or release controls. If you want a quick exposure check before redesigning controls, use 1099 Reporting Threshold Checker: Does Your Platform Need to File?. For related planning issues, see Creator Platform Tax Reporting for 1099 and W-8 Expansion Decisions.

Lock the legal baseline before changing any workflow#

Lock your legal source of truth before you change workflow or automation. As an internal control rule, not an IRS mandate, if your policy, specs, or tickets conflict with current IRS wording, pause net-new automation changes and issue a controlled policy update first.

Form 1099-K is an IRS information return for certain payment transactions, and a payment settlement entity (PSE) files it for reportable payment transactions, including payment card and third party network transactions. Confirm that filing framework first, then tune threshold logic.

Use IRS.gov as your primary authority. For the current federal baseline, anchor to IR-2025-107 and Fact Sheet 2025-08. For third party settlement organizations (TPSOs), FS-2025-08 says filing is tied to exceeding both tests, more than $20,000 and more than 200 transactions. Fact Sheet 2025-08 also says it supersedes FS-2024-03.

Put dates on every source before you rely on it. The IR-2025-107 newsroom page says news items may not be updated and tells readers to verify dates. Fact Sheet 2025-08 says FAQs may be updated or modified, and if FAQ text is inaccurate for a taxpayer's situation, the law controls.

The common failure mode is mixing IRS materials from different dates. Older Form 1099-K instructions still show $600 language, so keep a dated evidence pack for each decision: IRS URL, publication date, saved artifact, and an internal note identifying which source controls. You might also find this useful: KYB for Platform Operators Without Losing Legitimate Business Clients.

Reconcile the timeline so your controls match today not last year#

Use one dated timeline for threshold logic, or old transition assumptions will leak back into current controls. If Tax Ops and Engineering are using different source dates, pause the release and reconcile first.

Maintain one internal table for Form 1099-K history, and label each row by source tier and status so teams can see what is current, what is superseded, and what is still uncertain.

| Period | Key development | Source tier | Status for current controls |

|---|---|---|---|

| Mar. 11, 2021 onward | IRS later described the ARPA-era rule as requiring TPSO filing once payments to a payee exceeded $600 | IRS primary guidance | Superseded |

| Calendar year 2022 | IRS treated 2022 as a transition period | IRS primary guidance | Superseded |

| Nov. 21, 2023 update for tax year 2023 | IRS treated 2023 as an additional transition year and said reporting was not required unless payments were over $20,000 and transactions were over 200 | IRS primary guidance | Superseded |

| Nov. 26, 2024 relief and Notice 2024-85 phase-in | IRS used a planned phase-in of $5,000 for 2024, $2,500 for 2025, then $600 for 2026 | IRS primary guidance | Superseded |

| July 4, 2025 law change reflected in Fact Sheet 2025-08 | IRS says OBBB retroactively reinstated the pre-ARPA threshold, so TPSOs are not required to file unless both $20,000 and 200 transactions are exceeded | IRS primary guidance | Confirmed |

| Late secondary commentary still describing broad 2026 $600 reporting | Non-IRS summaries may still repeat the old phase-in story | Non-IRS commentary | Uncertain, do not use without IRS reconciliation |

For current controls, use the latest IRS baseline. Fact Sheet 2025-08 supersedes FS-2024-03 and states the TPSO trigger as exceeding both $20,000 and 200 transactions. If your specs still treat the 2024 to 2026 phase-in as active authority, mark that logic superseded and update it.

Require each row to carry the source title, publication date, saved artifact, source tier, and an internal note explaining why it is active or no longer controlling. Before any threshold-related release, have the compliance lead approve the exact timeline version used by Tax Ops and Engineering. That is an operational control, not a legal requirement, and it helps keep policy-code mismatches out of production.

Decide whether your entity is the filer before counting transactions#

Decide the filing entity first, then apply threshold counting. Counting belongs to the entity with the Form 1099-K reporting duty, because a payment settlement entity must file for reportable payment transactions.

The IRS framework turns on legal and settlement obligations. IRS instructions describe a third party settlement organization as the central organization with the contractual obligation to make payments to participating payees. Treasury regulations also tie settlement flow to who submits the instruction to transfer funds to the participating payee account.

Start with contracts, then confirm operations#

For each affiliate, align these facts to the same legal entity:

- who has the contractual obligation to pay participating payees

- who submits the settlement instruction to transfer funds to the participating payee account

- who can produce the information needed for Form 1099-K reporting

If those answers split across entities, treat filer status as unresolved and escalate. No single operational factor is a universal test.

Do not generalize filer status across affiliates#

Run the analysis affiliate by affiliate. Legal structure can change TPSO treatment, and entities with similar services may still land in different positions.

Use exclusions carefully. IRS instructions state that healthcare networks, in-house accounts payable departments, and automated clearing houses do not qualify as TPSOs.

Document the filer rationale before implementation#

Create a short filer memo before you lock reporting logic. Include the contracting entity, settlement-flow mapping, the reporting inputs, and which entity can produce the filing artifact.

Also record which IRS source controls the decision. The 03/2024 instructions still contain older $600 TPSO language, while FS-2025-08 states its FAQs supersede earlier FAQ versions. If your evidence trail breaks across affiliates, route it to tax counsel before implementation. Related reading: Accounts Payable Automation for Dummies for Platform Operators.

Standardize payee and transaction classification logic#

Once you confirm the filing entity, lock classification logic in one place. Use a canonical ruleset for payee documentation and a separate ruleset for Form 1099-K transaction scope, and treat missing or contradictory records as unresolved until internal review.

Use one canonical payee taxonomy#

Use one canonical payee taxonomy so Compliance, Tax, and Engineering are working from the same document status.

| Payee profile | Canonical document state | What the state establishes |

|---|---|---|

| U.S. person payee | Form W-9 on file | Payee provided documentation used to provide a correct TIN for information return filing |

| Foreign individual payee | Form W-8BEN on file | Payee represented foreign individual status to the payer or withholding agent |

| Foreign entity payee | Form W-8BEN-E on file | Payee represented foreign entity status |

Avoid loose labels like "tax form received" or "international seller." Anchor classification to the actual form state on file. If records are missing or contradictory, keep tax status unresolved and route the record to manual review before final reporting status is set.

Classify transactions first, apply thresholds second#

For Form 1099-K, classify in-scope transactions first, then apply threshold logic as a separate layer. IRS scope is based on payment card and third-party network transactions, and filing can be triggered when goods or services payments are received through a payment settlement entity.

That separation matters because IRS source versions still differ. The 03/2024 instructions still state a $600 TPSO rule for post-2022 years. FS-2025-08 and IR-2025-107 reflect the reinstated pre-ARPA standard of more than $20,000 and 200 transactions. If thresholds are isolated, you can update threshold logic without rewriting transaction classification.

Keep amount logic aligned to gross reporting. Form 1099-K is described as gross payments without adjustments for fees, credits, refunds, shipping, cash equivalents, or discounts.

Prevent duplicate counting and keep a defensible trail#

As an internal control, design counting logic so replayed or duplicated events do not inflate totals. Retries, webhook redelivery, and backfills should not create new reportable counts if the underlying event is the same. Keep machine-readable evidence for each classification update:

- rule version and effective date

- approver and owner

- prior and new classification outcomes

- reason for the change, including source reconciliation when IRS materials conflict

If you cannot reproduce which rule version produced a result, threshold and classification decisions become hard to defend later. For more on adjacent controls, see How to Handle Currency Gain and Loss Reporting for a Multi-Currency Platform.

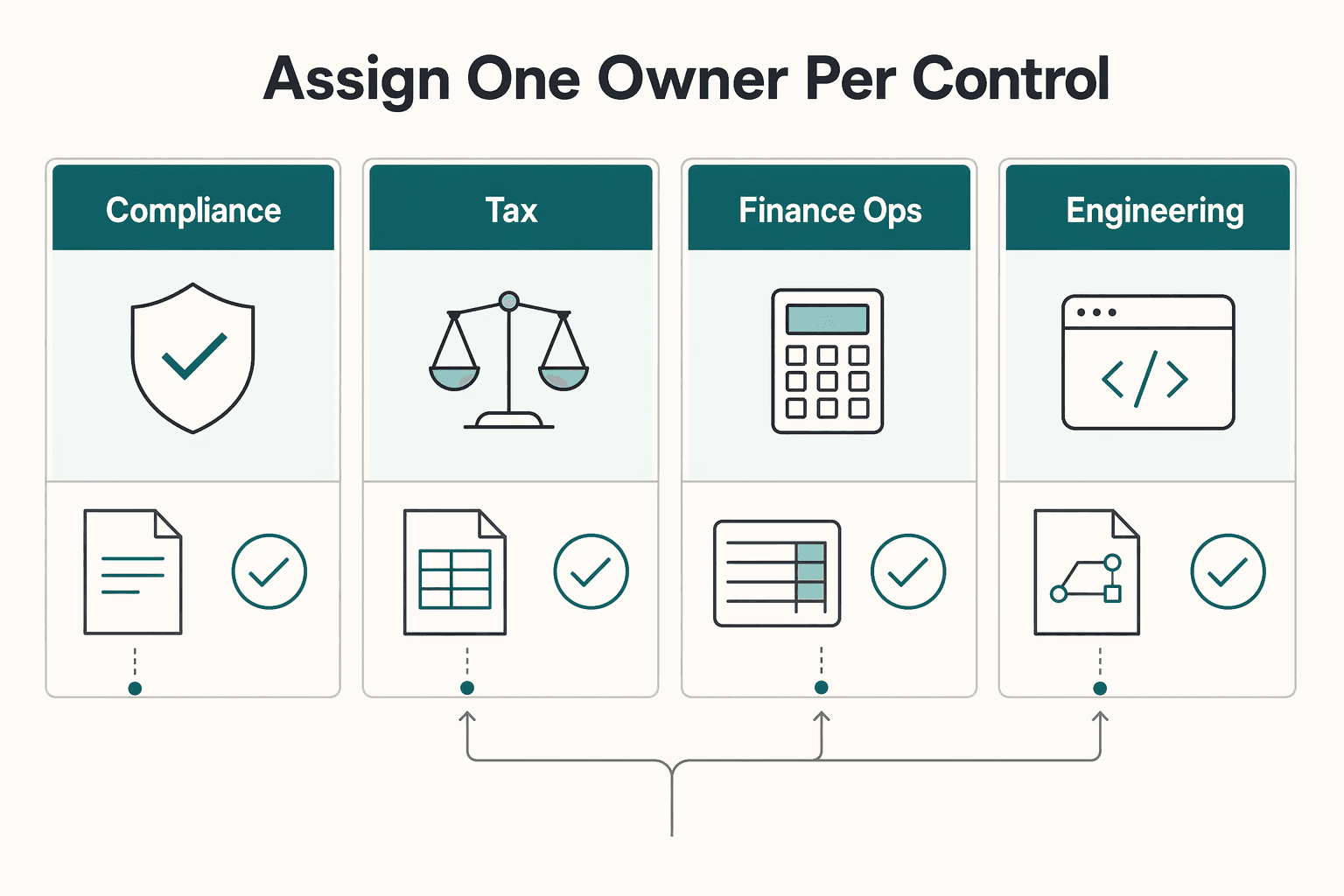

Build a role-owned quarterly control checklist#

Put your Form 1099-K controls on a quarterly calendar with named owners. When IRS source language is not fully aligned across publications, traceable ownership and approvals make decisions easier to reconstruct later.

The source mismatch is the control risk. FS-2025-08 and IR-2025-107 reflect a TPSO baseline of more than $20,000 and 200 transactions, while the 03/2024 Form 1099-K instructions still show $600 TPSO language. That is why ownership has to be explicit.

Assign one owner per control, not one team per problem#

A quarterly checklist works best when each control has one primary owner and a clear downstream consumer.

| Role | Core owner actions for 1099-K readiness | Evidence to retain |

|---|---|---|

| Compliance | Confirm the IRS source set used internally, record whether policy follows FS-2025-08 / IR-2025-107 or another approved interpretation, and own exception policy for unresolved payee or transaction status. | Dated source snapshots, policy memo version, approval record, exception taxonomy |

| Tax | Approve filer position and threshold logic, review threshold-near populations and document-status exceptions, and verify year-end calendar against Jan. 31 payee statements, Feb. 28 paper filing, and March 31 e-file deadlines. | Threshold memo, deadline calendar, signoff log, escalation notes |

| Finance Ops | Reconcile gross payment totals to reporting outputs, monitor document-collection quality for Form W-9 and Form W-8 records, and manage queues for unresolved TIN or classification issues. | Reconciliation files, exception queue aging, document-quality checks, payee outreach logs |

| Engineering | Maintain versioned rules for transaction counting and payee state, require approval before production tax-logic changes, and verify duplicate or replayed events do not inflate reportable counts. | Test results, rule version history, deploy approvals, raw-to-output reconciliation samples |

You do not need a large committee. You do need one policy owner who can state, in writing, which IRS source controls today and why.

Review threshold-near and exception cohorts every month#

Quarterly ownership is not enough on its own. A practical operating pattern is a monthly review of:

- payees approaching the threshold your policy currently applies

- records in exception queues because payee or transaction status is unresolved

State the active rule assumption at the top of the report, with source date. If you are waiting on counsel because of source conflict, say so plainly. IRS newsroom pages can go stale, and IRS FAQ language includes a caveat that if an FAQ is inaccurate for a case, the law controls.

Before you circulate the monthly report, confirm:

- threshold logic version matches the policy version in force

- counts are reproducible from raw ledger events without duplicate-event inflation

- exception queues separate missing documents, contradictory documents, and transaction-classification issues

If those checks fail, treat the report as not decision-ready.

Add internal release gates before any tax-logic deploy#

Treat release gates as an internal control choice. Do not ship production tax-logic changes without reconciliation evidence and policy-owner signoff, especially when threshold assumptions are changing over time. At minimum, require:

- expected results reproduced from a known sample set

- raw event totals, counted transactions, excluded transactions, and final reportable outputs tied to a specific rule version and effective date

- policy approval attached when threshold handling changes

Code defects and ungoverned cross-team changes can both create reporting errors. If reconciliation evidence or policy signoff is missing, hold the release.

Make W-9 and W-8 quality a cross-team handoff#

Document quality has to be shared across teams, not trapped in onboarding. Form W-9 supports correct TIN collection for information returns. Missing or incorrect TIN conditions can trigger 24% backup withholding in applicable cases. Form W-8BEN and Form W-8BEN-E support different foreign payee profiles, so a generic "W-8 received" state is not enough.

Use a simple handoff model across teams:

- Compliance defines acceptable document states.

- Finance Ops tracks missing, unreadable, or contradictory records.

- Tax reviews edge cases that can affect reporting or withholding treatment.

- Engineering ensures canonical states feed reporting logic and exception queues.

Each quarter, sample both "complete" and "exception" records against underlying documents or source data to verify the stored status is real. When rule language is moving, traceability at policy boundaries is what keeps control fixes from turning into filing problems.

If you are turning that role matrix into real operating controls, use Gruv's docs to align event-level workflows, approvals, and audit-trail handling.

Assemble a year-end evidence pack before filing season pressure#

A Form 1099-K filing position is only as defensible as the evidence behind it. Build the pack before January so an independent reviewer can see which rule you applied, which IRS sources you relied on, and how totals were produced from raw events. A minimum pack can stay compact, but it should be dated, versioned, and internally consistent.

| Evidence artifact | What it should answer | Minimum detail to retain |

|---|---|---|

| Policy memo | What rule did we apply, and why? | Current threshold assumption, source hierarchy, approval date, policy owner |

| Timeline version | Which guidance periods were treated as superseded vs current? | Version number, effective dates, source dates, signoff |

| Filer-role rationale | Why is this entity the filer, or not? | Entity analysis, operational facts, escalation notes if unresolved |

| Counting logic spec | How were transactions counted or excluded? | Rule version, inclusion and exclusion logic, duplicate-event treatment |

| Reconciliation outputs | Can totals be traced from raw events to final output? | Raw gross amounts, counted transactions, exclusions, final reportable totals |

Attach source snapshots, not just links. IRS states FAQ updates are dated and prior versions are maintained on IRS.gov, so retain the exact IRS.gov materials used in decisions, including IR-2025-107 and Fact Sheet 2025-08 (both dated October 23, 2025). If you used the IRS "About Form 1099-K" page, keep the captured page state, including its 31-Mar-2026 last-reviewed date.

Describe source authority carefully in the memo. FS-2025-08 says its FAQs supersede FS-2024-03, and it also says FAQs are not used by the IRS to resolve a case. Record that distinction directly: FAQs informed operations, while controlling law and higher authority remain separate. If a non-IRS summary conflicts with IRS primary guidance, treat the non-IRS summary as secondary until reconciled.

Add the filing calendar and unresolved exceptions#

The evidence pack should also show when decisions had to be made. Include execution deadlines in the timeline: payee statements by January 31, paper filing by February 28, and e-file by March 31. Those dates show when approvals, reconciliations, and exception clearing needed to happen.

Keep a live exception log with at least:

- case ID or payee ID

- issue type

- current owner

- target disposition date

- whether the case affects filing eligibility, classification, or totals

Avoid logs that only say "open" or "pending." You need enough detail to distinguish missing documentation, filer-role uncertainty, transaction-classification ambiguity, and reconciliation breaks.

Test whether the pack is actually defensible#

Run a mock walkthrough before filing season pressure hits. This is an internal control choice, not an IRS requirement, but it tells you whether the pack is usable. Give an independent reviewer the policy memo, source snapshots, counting spec, and sample reconciliation. If they cannot reproduce totals from raw ledger events, the pack is not audit-ready.

A common failure is misalignment across artifacts: the memo cites one threshold source, logic uses another rule version, and reconciliation outputs do not match the final population. Resolve those mismatches while records are still easy to trace.

Keep the file as long as it may be material to tax administration, rather than treating it as a one-time filing attachment.

For a step-by-step walkthrough, see 1099-NEC vs 1099-K Platform Filing Starts With Settlement Path.

Handle cross-border overlap without mixing regimes#

Form 1099-K and Form 1042-S are separate compliance tracks, not substitutes for each other. Form 1099-K is a payment settlement entity return for reportable payment transactions, while Form 1042-S is used by a withholding agent to report certain income and amounts withheld in foreign-person cases. If you collapse them into one decision tree, you risk the wrong document request, owner, or filing path.

For the U.S. scope of this guide, keep the federal 1099-K trigger logic anchored to the IRS FAQ position: gross payments exceeding $20,000 and more than 200 transactions. A 1042-S workflow answers a different question tied to foreign-person withholding and reporting, not a relabeling of a 1099-K record.

Separate document logic at intake#

Branch early between Form W-9 and Form W-8BEN states in onboarding and tax profiles.

- Form W-9: used to provide a correct TIN to a requester filing IRS information returns.

- Form W-8BEN: provided by a foreign beneficial owner to a withholding agent or payer for U.S. withholding and reporting purposes.

Avoid a single "tax form received" flag. Keep distinct states such as requested, received, validated, expired, conflicting, and override so reviewers can see why a profile moved between document paths and when.

Keep ownership clean#

Centralize shared controls, then keep filing rules modular.

- Centralize: identity checks, address normalization, audit logs, document storage.

- Modularize: W-9 and 1099-K logic and approvals separately from W-8 and 1042-S logic and approvals.

That gives you one audit trail without cross-jurisdiction contamination. Example: the March 15, 2027 due date for e-filing 2026 Form 1042-S belongs in the 1042-S calendar and queue, not inside 1099-K production planning.

If your foreign-payee volume is material, treat IRS Form 1042-S for Platform Operators: How to Report and Withhold on Foreign Contractor Payments as its own implementation track.

Do not fold UK rules into the U.S. article#

This guide is U.S.-focused. If your program also operates in the UK, run HMRC Making Tax Digital in a separate rulebook, evidence pack, and calendar. HMRC states that Making Tax Digital for Income Tax applies from 6 April 2026 for sole traders and landlords over £50,000, and that MTD for VAT requires digital records and software filing.

In practice, centralize shared infrastructure if useful, but isolate filing-regime rules by authority so U.S. threshold changes do not leak into UK logic, and UK fields do not drive IRS document requests.

If you want a deeper dive, read Making Tax Digital (MTD): What UK Platform Operators Need to Know About HMRC's Digital Reporting Mandate.

Set explicit escalation triggers for specialist review#

Escalation should be mandatory when filer ownership is unclear, IRS baseline guidance conflicts with secondary summaries, or cross-border reporting may apply. These scenarios can lead to wrong filer decisions, incomplete evidence packs, or missed non-1099 obligations.

Escalate entity-role ambiguity before assigning 1099-K ownership#

If affiliates split marketplace and payout functions, pause and escalate before assigning Form 1099-K responsibility. IRS instructions tie third party settlement organization status to the entity with the contractual obligation to make payments to participating payees, and the payment settlement entity is the filer.

Use a document-based checkpoint, not a verbal one. Review payee terms, processor agreements, intercompany contracts, and settlement-flow maps to confirm who holds the payment obligation and who can produce 1099-K records. If more than one affiliate appears to act as filer, require specialist signoff before implementation.

Escalate when IRS primary guidance and summaries diverge#

For current-year operations, treat IRS.gov primary guidance as the baseline and escalate any material mismatch with vendor summaries, blogs, or older newsroom writeups. IRS Fact Sheet 2025-08 states its FAQs are general and may not fit a taxpayer's specific facts, and that the law controls if FAQ text is inaccurate for the case.

A practical trigger is any broad $600 claim for 2026 that conflicts with IR-2025-107 and FS-2025-08, which describe a reversion to $20,000 and 200 transactions. Also escalate when internal guidance relies on potentially stale newsroom content, since the IRS notes news releases may not be updated after publication.

Escalate cross-border indicators outside the 1099-K lane#

Escalate early when facts suggest overlap with FATCA, Form 8938, FBAR, or FinCEN reporting. These are separate regimes, not extensions of a 1099-K workflow, and the IRS states Form 8938 and FBAR can both be required.

Use concrete triggers such as:

- Indicators that may bring Form 8938 into scope, with a general baseline of $50,000.

- Foreign account exposure where aggregate value exceeds $10,000 at any point in the year, which can trigger FBAR filing to FinCEN (due April 15, with automatic extension to October 15).

If either trigger appears, log the exception and route it for specialist review before changing filing logic.

Related context: Foreign Exchange Risk for Platform Operators and the Decisions That Cut FX Exposure.

Fix the failure modes competitors usually skip#

Many failures here come from control design, not unclear law: stale threshold assumptions, spreadsheet-only counting, and tax-document status that never reaches payout decisions. If any of those exist, fix that control chain before tuning anything else.

Retire delay-era assumptions first#

Start with current IRS primary guidance, not delay-era summaries. FS-2025-08 (Oct. 2025) says the One, Big, Beautiful Bill retroactively reinstated the pre-ARPA TPSO trigger. It frames the trigger as exceeds $20,000 and the number of transactions exceeds 200, which differs from the ARPA-era description of more than $600 regardless of transaction count.

A direct red flag is internal policy text or rule comments that still rely on the older $600 framing without reconciling to IR-2025-107 and FS-2025-08. A second red flag is reliance on the 03/2024 Instructions for Form 1099-K without resolving versioning. Those instructions still include a $600 statement, and they also direct readers to later-enacted legislation at IRS.gov/Form1099K.

Run one same-day alignment check across three artifacts: signed policy, production threshold logic, and outbound Form 1099-K logic. If those do not match, treat near-threshold reporting as unreliable until they do.

Move counting logic out of spreadsheets#

If counting logic lives only in spreadsheets, your Form 1099-K output is hard to defend. Because Form 1099-K is an information return, count-and-amount logic should tie to tested system rules on ledger or settlement events, not only month-end manual exports.

The risk is not just arithmetic mistakes. Manual workflows can drift in scope by including retries, replayed events, duplicate adjustments, or mixed transaction types that were never meant to count, and workbook-only exclusions may never make it into reporting code.

The IRS also states some payees may still receive a Form 1099-K below the federal TPSO threshold. That is another reason to avoid single-constant suppression logic.

Make document status operational#

Incomplete Form W-9 and Form W-8 capture is a reporting and withholding control issue, not just onboarding friction. The IRS says Form W-9 provides the correct TIN to a requester that must file an information return. Backup withholding guidance says the payer must begin backup withholding immediately on reportable payments if no TIN is provided.

That does not create a universal payout-block rule for every missing form. It does mean payout workflows should flag missing or contradictory tax-document status as an exception before payment is treated as clean. For foreign persons, capture the relevant Form W-8 before defaulting into domestic documentation assumptions.

Repair in a controlled sequence#

The IRS materials here do not prescribe one universal remediation workflow, but fixes usually hold up better when you do them in a clear order instead of ad hoc:

- Pause nonessential tax-rule changes while you reconfirm IRS baseline assumptions and filer logic.

- Reconcile raw transaction data against prior Form 1099-K logic, especially near thresholds and in manually adjusted cohorts.

- Reclassify edge cases such as duplicate events, personal reimbursements that should not be on Form 1099-K, and unresolved W-9/W-8 status.

- Re-enable changes with policy-owner approval, tested rule evidence, and an exception log for unresolved items.

Skipping a defined sequence can hide defects and weaken the evidence trail you may need later.

Execute a 30-day implementation sequence#

Use the next 30 days as a controlled reset, not a tax-tech sprint. The objective is to align policy, code, and filing evidence to current IRS.gov guidance before filing deadlines turn small mismatches into filing defects.

Week 1#

Start by fixing your source-of-truth timeline. Lock one internal memo to the current IRS baseline: FS-2025-08, IR-2025-107 dated Oct. 23, 2025, and the related FAQ page last reviewed 22-Jan-2026. Reconcile that timeline against American Rescue Plan Act of 2021, Notice 2024-85, and the One, Big, Beautiful Bill signed July 4, 2025.

Assign one owner each from Tax, Compliance, and Engineering, and require a signed timeline marked current or superseded. Flag any artifact that still cites the phased 2024 bulletin path, $5,000 for 2024, $2,500 for 2025, $600 for 2026 and after, without explaining why later OBBB-era guidance changed the operating baseline.

Week 2#

Harden payee classification and transaction counting rules, since reporting errors can start there. For Form 1099-K, the IRS currently states the TPSO trigger as exceeds $20,000 and the number of transactions exceeds 200, so your inclusion and exclusion logic should be tested against ledger or settlement events, not report exports.

Build an exception taxonomy for unresolved entities and contradictory tax-document states. At minimum, separate unclear filer role, duplicate or replayed events, unresolved domestic versus foreign documentation, and manual adjustments that move totals near threshold. If filer role is unclear, route it to counsel review before tuning thresholds.

Week 3#

Run a dry run as if filing season starts today. Produce draft payee outputs, threshold cohort reports, and an evidence pack with the policy memo, rule version history, reconciliation results, and IRS.gov source snapshots.

Add cross-border flags, but keep regimes separate. If a case points to Form 1042-S, confirm whether Form 1042 is also required, because the IRS states it is when 1042-S is required. Use this week to catch a failure mode where aggregate totals look right but cannot be reproduced from raw events.

Week 4#

Close with leadership signoff, a documented escalation matrix, and a locked quarterly control cadence. The matrix should name who sets policy, who approves production changes, and who owns unresolved exceptions, with checks against Jan. 31 payee-statement timing and March 31 electronic filing timing.

Document reliance and approval details before you finalize. IRS news releases say to verify publication dates, and IRS FAQs are not final legal authority if the law applies differently in a specific case. Record what you relied on, who approved it, and when.

What to do next to reduce surprises this year#

This is a controls update, not a one-time threshold announcement. Lock one approved record for your legal baseline, filer-role owner, and counting logic for Form 1099-K. If any of that still sits in email threads, slides, or ad hoc spreadsheets, you still carry avoidable filing-season risk.

Start with the baseline you can defend from dated IRS primary sources. For current federal TPSO treatment, anchor your memo to IRS materials tied to IR-2025-107 (Oct. 23, 2025), Fact Sheet 2025-08, and your freshness check on the About Form 1099-K page (last reviewed 31-Mar-2026). Keep the retrieval date and approver name with that source set. IRS news pages warn they may not be updated after release, and the FAQ package says the FAQs are not in the Internal Revenue Bulletin and that the law controls if FAQ language is inaccurate for a case.

Assign one named owner for filer-role determination and document the rationale. The IRS states a payment settlement entity must file Form 1099-K, but responsibilities can be split across marketplace, payments, and treasury entities. Where facts are mixed, get legal or tax review before you change automation.

Make counting logic reproducible from source records, not just report exports. A practical check is to have an independent reviewer trace one payee from source records to annual gross amount and transaction count using payment app reports, merchant statements, or equivalent records. If that result cannot be reproduced, the control is not ready.

Keep the evidence pack boring and complete#

Under review, a consistent artifact set matters more than polished narrative. At minimum, keep:

- policy memo with current IRS baseline and source dates

- filer-role rationale for each relevant entity

- rule version for payee classification and transaction counting

- reconciliation output showing totals can be rebuilt from source records

- exception log with owner, status, and deadline

Escalate ambiguity before filing season compresses choices#

Escalate early when regime boundaries are unclear. If a payee population may require Form W-8 and Form 1042-S treatment, keep that path separate from domestic Form W-9 intake and Form 1099-K logic. Escalate the same way if internal materials still cite older phase-in thresholds without reconciliation to current IRS language.

Be careful with vendor product claims#

Use vendor pages as operational inputs, not legal conclusions. Vendor documentation itself notes that state criteria can differ from federal rules and that threshold information can change. Examples like $600 in Vermont, Massachusetts, Virginia, and Maryland or Illinois over $1,000 and four or more transactions show why federal-only assumptions can fail. For any product, verify scope by jurisdiction, applicable tax workflows, and preserved evidence if your position is challenged.

Need the full breakdown? Read What Is Negative Churn? How Platform Operators Achieve Revenue Expansion Without New Customers.

If your team needs a program-fit review for 1099-K, W-8/W-9, and payout control design before filing season, contact Gruv.

Frequently Asked Questions

What is the current Form 1099-K threshold after the IRS delay changes?

For TPSOs, the current federal filing trigger is gross reportable payments over $20,000 and more than 200 transactions. The IRS ties that position to Fact Sheet 2025-08 and IR-2025-107. The IRS also says a TPSO may still send a Form 1099-K below those thresholds.

Did the $600 rule get reversed, and what should operators rely on now?

Yes. The IRS says the One Big Beautiful Bill retroactively reinstated the pre-ARPA federal TPSO threshold framework. That is why current IRS FAQs point to $20,000 and 200 transactions instead of more than $600 regardless of transaction count. Verify publication dates on the IRS pages you rely on.

What changed between IRS delay phases and the later rollback signal?

IRS transition relief described phased thresholds of more than $5,000 for 2024, more than $2,500 for 2025, and more than $600 for 2026 and after. The IRS later said the 2025 FAQ package supersedes the earlier 2024 FAQ package after the OBBB-era reset. Keep one signed internal timeline marked current and treat prior phase-in timelines as superseded.

How should platform operators validate whether they are the filing entity?

Start with the rule that a payment settlement entity must file Form 1099-K, then test your actual payment flow against that role. For payment card transactions, the IRS says the merchant acquiring entity that transfers funds to the participating payee reports the gross amount. Document the role decision and keep it in your filing evidence, especially when responsibilities are split across entities.

How should teams adjust controls this quarter without overbuilding?

Keep scope tight: update the threshold baseline, validate counting from raw events or settlement data, and monitor payees near the trigger. Preserve rule versions, approvals, and exception logs instead of starting a broad tax product rebuild. Run that cadence against Jan. 31 payee statements and March 31 electronic filing timing.

What is still uncertain from public summaries and requires specialist review?

Some uncertainty remains because the IRS says these FAQs are informational and will not be relied on or used by the IRS to resolve a case. Use specialist review when filer role is ambiguous, when materials still cite older phase-in thresholds without reconciliation to 2025 IRS guidance, or when documentation is contradictory. If you cannot show which IRS.gov source you relied on and when, escalate.

When does a 1099-K workflow need coordination with IRS Form 1042-S processes?

Coordinate when the payee may be a foreign person or onboarding contains valid Form W-8 documentation. The IRS says foreign persons with valid W-8 documentation are exempt from Form 1099 reporting, and payments subject to NRA withholding are reported on Form 1042-S with a Form 1042 filing. Keep W-9 and W-8 decision paths separate so one intake flow does not blur two different reporting regimes.

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.

How to Respond to a Subpoena for Business Records

Move fast, but do not produce records on instinct. If you need to **respond to a subpoena for business records**, your immediate job is to control deadlines, preserve records, and make any later production defensible.

A US Expat's Guide to Investing in UCITS ETFs to Avoid PFIC Issues

The real problem is a two-system conflict. U.S. tax treatment can punish the wrong fund choice, while local product-access constraints can block the funds you want to buy in the first place. For **us expat ucits etfs**, the practical question is not "Which product is best?" It is "What can I access, report, and keep doing every year without guessing?" Use this four-part filter before any trade: