Quick Answer

Route tax status at onboarding: U.S. persons to Form W-9 and possible Form 1099-NEC, foreign individuals to Form W-8BEN, and foreign entities to Form W-8BEN-E. Check the payment rail early because Section 6050W transactions belong on Form 1099-K, not 1099-NEC. Then enforce payout holds for missing or expired documentation and keep versioned forms, validation timestamps, and hold-release reasons so IRS and finance reviews can be defended.

Tax Form Routing as a Payout Control, Not a Support Task#

Tax form routing is an operating decision, not a creator support task. When it goes wrong, you see payout delays, avoidable withholding, and reporting risk. For creator platforms, the core job is to classify payees before the first payout and keep that logic defensible as volume grows.

The split is straightforward in principle. Form 1099-NEC reports nonemployee compensation. Form W-8BEN is for foreign individuals to establish foreign status for U.S. withholding and reporting purposes. Form W-8BEN-E serves that role for foreign entities under chapters 3 and 4. If your platform or payout stack controls or pays a withholdable payment, you may be operating as a withholding agent, so misrouting is a compliance issue, not just a UX issue.

Major platforms already treat tax collection as a payout gate. TikTok says it must collect tax information before paying creators, and YouTube requires tax info from monetizing creators regardless of location. YouTube also notes that missing tax info can trigger deductions of up to 24% of total earnings worldwide. For many U.S.-source payments to foreign persons, a 30% baseline withholding context also applies. A few early design choices carry most of the operational risk:

- U.S. reporting path: When payments belong in a nonemployee compensation flow, design around Form 1099-NEC and its January 31 filing deadline.

- Foreign individual vs. foreign entity path: Route foreign individuals to Form W-8BEN and foreign entities to Form W-8BEN-E. Valid W-8 documentation can affect backup withholding and Form 1099 reporting outcomes.

- Renewal and continuity policy: Some platforms apply a renewal cycle ending in the third full calendar year after signing, while IRS instructions also describe conditions where Form W-8BEN can remain effective until a change in circumstances. Treat expiry as a policy decision with documented checks, not a blanket timer.

This guide is for founders, payments ops, and product leads planning U.S. and cross-border launches. The goal is practical: choose a reporting model that matches your creator mix, verify forms before payout, and maintain versioned records so withholding and reporting decisions remain defensible. Not every platform payment belongs on Form 1099-NEC or Form 1099-MISC, which is why classification has to happen upstream.

You might also find this useful: Digital Platform Reporting: What Every Online Marketplace Must Report to Tax Authorities Worldwide.

Selection criteria and fit before you choose a model#

Pick the model that matches how you actually pay creators, not the form you wish were simplest. Use this section when you are deciding between a Form 1099-NEC path and a Form W-8BEN or Form W-8BEN-E path before rollout. If you only need individual filing help on Form 1040, this is the wrong scope.

| Criterion | What to assess | Key detail |

|---|---|---|

| Jurisdiction coverage | Whether the model handles only U.S. payees or also foreign individuals and foreign entities | If non-U.S. creators are in scope, include U.S. tax treaty handling and FATCA chapter 4 classification at launch |

| Ops burden | Onboarding, review, and renewal complexity | W-8 paths add treaty and entity-status handling; Form 1099-NEC has a January 31 filing deadline; W-8 forms generally remain valid through the last day of the third succeeding calendar year unless circumstances change |

| Payout continuity risk | How often missing or incomplete tax data can delay payouts | Before first payout, verify payee type, residency, and whether foreign entities completed the relevant Form W-8BEN-E content for chapter 3 and chapter 4 treatment |

| Evidence quality | Whether the model can be defended later to IRS and finance review | Keep versioned forms, timestamps, validation outcomes, and decision rationale for treaty and withholding treatment |

Start with the payment rail. Section 6050W card and network transactions are reported on Form 1099-K, not on Form 1099-NEC or Form 1099-MISC, so the 1099 versus W-8 split is only part of the routing decision. Then use an internal four-criteria check:

- Jurisdiction coverage

Check whether you need to handle only U.S. payees or also foreign individuals and foreign entities. If non-U.S. creators are in scope, include U.S. tax treaty handling and Foreign Account Tax Compliance Act, or FATCA, chapter 4 classification at launch rather than patching it in later.

- Ops burden

Measure your onboarding, review, and renewal complexity. W-8 paths add treaty and entity-status handling. Form 1099-NEC has a January 31 filing deadline, and W-8 forms generally remain valid through the last day of the third succeeding calendar year unless circumstances change.

- Payout continuity risk

Rate how often missing or incomplete tax data can delay payouts. Before first payout, verify payee type, residency, and whether foreign entities have completed the relevant Form W-8BEN-E content for chapter 3 and chapter 4 treatment.

- Evidence quality

Prefer the model you can defend later to IRS and finance review. Keep versioned forms, timestamps, validation outcomes, and decision rationale for treaty and withholding treatment.

If your monetization is U.S.-only and contractor-like, prioritize clean Form 1099-NEC issuance where applicable and fast support resolution over premature global branching.

Comparison of the five operating models for 1099 and W-8 handling#

Pick the model that keeps exceptions, payout holds, and audit evidence manageable at your current stage. What matters is not which form looks simplest at intake, but where the operational weight lands once payouts start.

| Model | Required docs | Renewal burden and likely exception volume | Decision checkpoints | Payout holds and escalation path | Reconciliation and audit artifacts |

|---|---|---|---|---|---|

| U.S.-only contractor | Form W-9; Form 1099-NEC filing by January 31 when applicable, plus required recipient statements | Generally lower renewal burden with no W-8 lifecycle; exception volume can rise if routing changes | Confirm TIN quality; confirm payments are not in the 1099-K carveout, since certain card and network transactions are not reported on 1099-NEC or 1099-MISC | Hold for missing or invalid W-9; first-line support can usually resolve standard intake issues | If multiple payers issue separate Form 1099 records, complexity rises; retain signed W-9, validation results, filing evidence, and furnished-statement evidence |

| Mixed creator | Form W-9 for U.S.; Form W-8BEN for foreign individuals; Form W-8BEN-E for foreign entities | W-8BEN renewals run through the last day of the third succeeding calendar year; exceptions often center on residency/entity routing and treaty inputs | Determine residency and payee type before first payout; use IRS tax treaty tables for treaty claims; add FATCA branch logic when W-8BEN-E applies | Hold for missing residency or entity status, or incomplete treaty inputs; escalate treaty and entity cases to tax ops | Reconciliation can increase when creators receive payer-specific forms; retain routing logic versions, treaty decision records, and hold-release logs |

| Non-U.S.-first | Mostly Form W-8BEN and Form W-8BEN-E; Form W-9 for U.S. exceptions | Renewal burden can be higher; exceptions often cluster around treaty and no-treaty handling | Run treaty-table checks early for reduced or exempt treatment; in at least one platform flow, no-treaty cases prompt a Certificate of No U.S. Activities; W-8 forms go to the payer or withholding agent, not the IRS | Hold for expired W-8s or missing no-treaty documents in flows that require them; escalate to an international tax support queue | Withholding review is often heavier; retain signed forms, renewal controls, and treaty lookup records |

| Entity-heavy agency | Form W-9 for U.S. entities; Form W-8BEN-E for foreign entities; limited Form W-8BEN | Review burden can be high around entity classification and mismatches | Verify entity versus individual status; FATCA chapter 4 classification is mandatory logic; incomplete classification can create 30% withholding risk | Hold for incomplete W-8BEN-E or payer-payee mismatch; escalate to tax ops, and counsel when needed | Reconciliation complexity can be high across payer records; retain form versioning, chapter 4 rationale, and approval notes |

| Rapid expansion | All three intake docs, routed by country, residency, and entity type | Renewal burden can grow quickly; exception volume rises without strict gating | For each launch country, define treaty availability, document path, certificate behavior in local flow, and FATCA logic before go-live | Use hard holds until tax status is complete; triage support between document fixes and treaty or entity exceptions | Reconciliation complexity depends on market structure; retain country policy versions, test evidence, payout-block logs, and 1099 filing and furnishing records |

If non-U.S. creators or foreign entities are already in scope, treat treaty checks, W-8BEN-E, and FATCA routing as launch requirements rather than post-launch cleanup.

For a deeper dive, read How to handle the tax on income from 'crowdfunding' platforms like Patreon.

Best for U.S.-only creator payouts#

This model works when your payouts are genuinely U.S.-only and contractor-based. Collect Form W-9 early and run year-end Form 1099-NEC operations on one calendar.

Why this model works early#

The main advantage is simplicity. For independent-contractor workflows, IRS guidance treats a completed Form W-9 as the first step. Onboarding can stay on one tax-status path instead of branching into residency, treaty, and entity logic.

It also keeps year-end operations tighter. Form 1099-NEC reporting and recipient furnishing both run on the January 31 deadline, which is easier to manage when you are not mixing U.S. and foreign document flows.

What to verify before you commit#

Before you lock this in, confirm that it fits your actual roadmap and not just today's supply mix:

- Collect a completed Form W-9 early in onboarding so TIN collection is in place for information-return reporting.

- Check your near-term market roadmap, not just the current mix. If non-U.S. onboarding is likely soon, this setup is less durable.

- Do not hard-code one 1099-NEC threshold without checking current-year IRS instructions. The source set includes conflicting language, with

$600in one place and$2,000 for payments made after December 31, 2025in another.

Keep records tight even in a U.S.-only flow: completed W-9 documentation and proof that Form 1099-NEC was filed and furnished by January 31.

The real tradeoff#

The weakness is retrofit risk. Once nonresident creators or foreign entities enter scope, routing shifts from W-9 and 1099-NEC toward Form W-8BEN or Form W-8BEN-E, and potentially Form 1042-S. For certain U.S.-source nonemployee compensation paid to nonresident aliens, guidance points to 30% withholding unless treaty reduction applies.

So the main risk is not launch complexity. It is what happens later, when a U.S.-only intake flow does not capture the foreign-status and treaty data needed for smoother international payouts.

This model fits best when creator supply is genuinely U.S.-resident, W-9 onboarding is standardized, and reporting operations are predictable. If foreign creator demand is already showing up, mixed routing is usually the safer starting point.

For a step-by-step walkthrough, see Choosing Creator Platform Monetization Models for Real-World Operations.

Best for mixed U.S. and non-U.S. creator bases#

Use a mixed routing model when U.S. and non-U.S. creators will share one payout flow this year. Set the branch at onboarding: Form W-9 for U.S. persons, Form W-8BEN for foreign individuals, and Form W-8BEN-E for foreign entities.

The benefit is durability. You collect tax-status data before payouts start, so creators enter the right U.S. reporting lane or foreign-person withholding and reporting lane from the beginning.

| Creator status | Intake document | What to verify before first payout | Likely reporting path |

|---|---|---|---|

| U.S. person | Form W-9 | TIN collected, U.S.-person status documented | Form 1099-NEC may apply for reportable nonemployee compensation |

| Non-U.S. individual | Form W-8BEN | Foreign status documented, treaty claim reviewed if made | For nonresident-alien nonemployee compensation, IRS points to Form 1042-S, not Form 1099-NEC |

| Non-U.S. entity | Form W-8BEN-E | Entity status documented, chapter 4 status documented, and treaty residency/treaty position reviewed if claimed | Foreign-entity withholding and reporting path depends on form details and status determination |

The tradeoff is support and review complexity. Treaty handling and chapter 4 FATCA classifications can create specialized exception work. That is especially true for foreign entities, where missing or incomplete chapter 4 documentation can lead to 30% withholding treatment.

If non-U.S. creators are material to this year's growth, build mixed logic now. If not, set a clear trigger before launching in new countries and tie that trigger to tax-form routing, not just go-to-market timing. Keep the operating checkpoints explicit:

- Require tax-status selection before payout activation.

- Hold payouts when payee type and form type conflict, when a Form W-8 is expired, or when treaty information cannot be reviewed.

- Store form version, collection date, validation result, and hold or release reason per creator.

- For the U.S. lane, plan Form 1099-NEC operations with the IRS e-file threshold of

10aggregated information returns for filings required on or afterJanuary 1, 2024. - Track renewal windows: Form W-8BEN and Form W-8BEN-E generally run through the last day of the third succeeding calendar year unless circumstances change earlier.

Once international creators are part of core payout design rather than an edge case, this is usually the cleaner model.

We covered this in detail in Best Platforms for Creator Brand Deals by Model and Fit.

Best for non-U.S.-heavy creator supply#

Choose this model when most creators are outside the United States and your default onboarding path is Form W-8 documentation. Make U.S.-person handling the exception path, not the baseline.

The advantage is focus. You collect foreign-status documentation up front with the right form variant: Form W-8BEN for individuals and Form W-8BEN-E for entities. These forms are not interchangeable, so intake logic should branch on person type before the first payout.

Why this model works#

In an international-heavy supply mix, this model can reduce day-to-day friction by standardizing most creators on one document family with a time-bound renewal lifecycle. For media, affiliate, or publisher networks with broad non-U.S. supply, that usually means less onboarding variance and fewer support loops.

Treaty handling is the main control. When a creator claims treaty benefits on Form W-8BEN or Form W-8BEN-E, validate the claimed article or rate against the IRS tax treaty tables before payout release.

What you still have to manage carefully#

This model does not remove withholding risk. Most U.S.-source income received by a foreign person is subject to a 30% U.S. tax rate, so you still need a clear path for cases where no treaty applies or the treaty does not cover that income type.

If your policy uses extra attestations, such as a Certificate of No U.S. Activities, treat them as internal controls rather than universal IRS requirements for every non-U.S. creator. Define exactly when they apply and whether they affect payout release, withholding treatment, or both.

Form W-8 records also expire. The validity period generally runs through the last day of the third succeeding calendar year. Compute expiration when the form is collected, send renewal reminders early, and hold payouts when a required W-8 is expired.

Reporting path and fit#

For covered income paid to foreign-address recipients, design reconciliation and year-end operations around Form 1042-S. This model is a strong fit for international-first creator networks with periodic U.S.-source payments. Two controls are non-negotiable: the correct W-8 variant at onboarding and payout holds for unsupported treaty claims or expired W-8s.

This pairs well with our guide on Common Reporting Standard (CRS) for Digital Nomads: Self-Certification and Data Mismatch Risk.

Best for entity-heavy agency and network structures#

If agencies, studios, and incorporated creator businesses make up a meaningful share of payouts, use entity-first onboarding from the start. The core split is foundational: foreign entities generally use Form W-8BEN-E, while foreign individuals use Form W-8BEN.

Why this model fits#

Entity-heavy payout flows can create avoidable errors when platforms force individual-only tax logic. In one payout system, you may pay a solo creator, an incorporated agency, and a studio entity. Getting the payee type right before payout avoids rework when money movement is time-sensitive.

Form W-8BEN-E is the IRS form for foreign entities and includes Chapter 4 Status, or FATCA status, so intake needs more than a simple residency branch. The operating advantage is that you separate U.S. versus non-U.S. and individual versus entity rules before money moves.

Where valid foreign-person W-8 documentation is on file, payees may fall outside ordinary Form 1099 reporting. U.S. business payees on a Form W-9 path can still require Form 1099-NEC, which is due by January 31 for nonemployee compensation reporting.

What you need to verify up front#

A common operational risk here is a mismatch between the party you contracted with, the party you are paying, and the party on the tax form. Check that before payout, not after.

- Confirm the actual payee before first payout. In agency and network structures, the campaign counterparty, bank account holder, and tax-form owner may not be the same party unless intake enforces that match.

- Collect the correct form by person type: foreign entities generally use Form W-8BEN-E, and foreign individuals use Form W-8BEN.

- Match the legal entity name across the contract, payout profile, and tax form.

- Review entity treaty claims carefully. IRS materials note that an entity claiming treaty benefits may need to provide a statement that it derives the income for which it claims those benefits.

Where complexity shows up#

The tradeoff is heavier document review, especially around FATCA branching. W-8BEN-E includes multiple Chapter 4 statuses, including FFI variants, and an FFI generally means a foreign entity that is a financial institution.

Plan renewal controls at intake. W-8BEN-E is generally valid through the last day of the third succeeding calendar year unless circumstances change, so track expiration dates as soon as the form is collected.

Related reading: What Is a Tax Home for US Expats and Why It Matters.

Best for fast country expansion with a lean tax ops team#

When you need to enter multiple countries quickly with limited tax review capacity, strict intake gates can be worth the friction. It is often simpler to hold a payout at onboarding than to remediate a bad tax status after creators are already queued for payment.

The goal is not to solve every edge case on day one. It is to open each market with a clear routing branch and a clear hold rule when required tax data is incomplete.

Keep the first routing decision hard to get wrong#

Start with a small set of branches your team can actually support:

- U.S. person: collect Form W-9.

- Foreign individual: collect Form W-8BEN to establish foreign status and, where relevant, support treaty claims.

- Foreign entity: collect Form W-8BEN-E. Entities use this form. Individuals use Form W-8BEN.

If you are launching three new geographies in one quarter, limit early cohorts to branches your review queue can handle. That gives you a documented trail showing the route, document collected, and hold or release reason.

The checkpoint that matters most#

Do not stop at "form uploaded." Verify that the tax document can be reliably tied to the actual payee. Match legal name and payee type across the tax form, payout profile, and contract or account owner record. If documentation is missing or cannot be reliably associated, presumption rules can apply.

For U.S.-source nonemployee compensation paid to a nonresident alien, reporting ties to Form 1042-S and withholding is 30% or a lower treaty rate if applicable. For U.S.-person payments subject to Form 1099 reporting, backup withholding can be 24% when conditions are met.

Operationally, define hold rules so creators are blocked when residency branch, payee type, document type, and treaty selection status do not line up. If your provider captures pre-filing tax confirmation, e-consent, and delivery events for 1099s, retain those timestamps with the tax record. Form 1099-NEC recipient copies are due by January 31.

What you give up for the control#

You may slow early activation, and some creators may get held because they started on the wrong form path. You also need more upfront policy design for U.S. versus non-U.S. routing, individual versus entity handling, treaty review, and automatic holds.

For foreign individuals, Form W-8BEN is generally valid through the last day of the third succeeding calendar year unless circumstances change, so expansion planning needs renewal controls as well as initial collection.

If payout timing is sensitive and your compliance team is lean, this tradeoff can be worth it: controlled onboarding friction now instead of emergency remediation after payouts begin. Need the full breakdown? Read International Inheritance Tax Guide for Digital Nomads.

Tax document collection sequence that prevents payout breaks#

The IRS guidance cited here does not prescribe a required W-8 onboarding order. A practical internal approach is to route first, verify before release, and carry status forward into filing.

| Step | Action | Key detail |

|---|---|---|

| Route before release | Decide which tax document to request and keep payout on hold until the tax record is tied to the payee you will actually pay | The key control is whether the record is complete enough for payout and downstream filing |

| Add two review moments | Use one gate before first payout and another before correction windows | Keep hold reasons explicit so support, payouts, and finance are working from the same status |

| Build for filing rules early | Plan for electronic filing if you expect 10 or more information returns | If an original return had to be e-filed, corrected returns must also be e-filed; electronic filing requires a Transmitter Control Code; scanned files and PDF, PNG, TIF, GIF, JPG, Word, and Excel formats are not accepted |

| Assign escalation ownership | Treat payout blocked and tax form delivery issue as controlled exception paths | Use a named owner and required case evidence so corrections stay in one queue instead of scattered handoffs |

- Route before release

Use your internal routing policy to decide which tax document to request, and keep payout on hold until the tax record is tied to the payee you will actually pay. The key control is whether the record is complete enough for payout and downstream filing.

- Add two review moments

Use one gate before first payout and another before correction windows so stale or changed records do not pass silently. Keep hold reasons explicit so support, payouts, and finance are working from the same status.

- Build for filing rules early

If you expect 10 or more information returns, filing is electronic regardless of form type. If an original return had to be e-filed, corrected returns must also be e-filed. Electronic filing requires a Transmitter Control Code (TCC). Scanned files and PDF, PNG, TIF, GIF, JPG, Word, and Excel formats are not accepted.

- Assign escalation ownership

Treat "payout blocked" and "tax form delivery issue" as controlled exception paths with a named owner and required case evidence. That keeps corrections in one queue instead of scattered handoffs.

Plan the IRS handoff in advance. The IRS recommends submitting the IR Application for a TCC by November 1st and allowing 45 business days for processing. Tax Year 2026 / Filing Season 2027 is the targeted point when IRIS becomes the only intake system for information returns. If you are still on FIRE before that transition, TCC availability is typically within 48 hours of the application's effective date, but invalid electronically transmitted documents can lead to TCC revocation.

Keep annual-return forms separate from onboarding decisions. Form 8938 is attached to an annual return and filed by that return's due date, including extensions, and it must specify the applicable calendar year or tax year.

Before rollout, use a practical dry run of your W-8 intake flow with a W-8 Form Generator where available.

Renewal, exception handling, and edge-case governance#

Edge-case governance gets easier when you separate lanes early. Keep FATCA/Form 8938 exception handling distinct, and treat W-8 renewal mechanics, treaty workflows, and multi-payer Form 1099 operations as counsel-reviewed policy areas.

- Renewal control

Maintain Form W-8 controls under your internal policy and legal guidance. These excerpts do not establish a required Form W-8 renewal frequency or a specific platform workflow, so avoid hard-coding one from this material alone.

- FATCA and foreign-asset exception lane

Route unclear FATCA questions to a Form 8938 review lane and verify whether FBAR is also required. In these IRS excerpts, FATCA reporting is generally through Form 8938, and that requirement is separate from FinCEN Form 114 (FBAR). Form 8938 is attached to the annual return and filed by that return due date, including extensions. For specified domestic entities, filing thresholds in the excerpts are $50,000 on the last day of the tax year or $75,000 at any time during the tax year. IRS also says exceptions may apply, and if a U.S. taxpayer is not required to file an income tax return, Form 8938 is not required regardless of asset value. Failure handling should be explicit because penalties may apply: $10,000 baseline, up to $50,000 for continued failure after IRS notification, and a 40 percent substantial understatement penalty in some cases.

- Treaty disputes and cross-border entity documentation lane

Keep treaty and cross-border entity-document questions in a separate escalation lane. Withholding-rate specifics, platform-specific treaty mechanics, and jurisdiction-specific overrides vary — confirm each with the relevant authority before promising outcomes.

- Multi-payer

Form 1099governance

Treat multi-payer Form 1099 handling as a counsel-reviewed policy topic. Whether consolidation, suppression, or correction into a single Form 1099 is appropriate depends on your situation — confirm with qualified counsel before making definitive commitments.

Evidence pack operators should retain for audits and reconciliations#

If a tax decision cannot be reconstructed later, it will be hard to defend. Retain evidence that shows what you collected, when you collected it, what you decided, and why.

| Evidence item | What to retain | Key detail |

|---|---|---|

| Versioned tax forms and validation results | The exact version of each Form W-9, Form W-8BEN, or Form W-8BEN-E tied to the payee record, along with the validation result | Documentation should generally be obtained before payment; if a payment cannot be reliably associated with valid documentation, presumption rules apply and foreign-payee exposure can default to 30% of gross; keep Form W-9 for four years |

| 1099 furnishing evidence and consent records | Evidence that Form 1099 statements were furnished, including recipient consent for electronic delivery and renewed written consent after technical delivery changes | For Form 1099-NEC, both filing and recipient furnishing tie to January 31; also retain payment and withholding records needed to support reconciliation and tax administration |

| Determination support in one auditable location | IRS tax treaty tables, the treaty text used where needed, internal policy mapping, and validation controls | IRS says treaty tables are not a complete guide and directs withholding agents to consult applicable treaty provisions |

- Versioned tax forms and validation results

Keep the exact version of each Form W-9, Form W-8BEN, or Form W-8BEN-E tied to the payee record, along with the validation result. Documentation should generally be obtained before payment. If a payment cannot be reliably associated with valid documentation, presumption rules apply, and foreign-payee exposure can default to 30% of gross. For U.S. payees, keep Form W-9 in your files for four years.

- 1099 furnishing evidence and consent records

Keep evidence that Form 1099 statements were furnished, especially for electronic delivery. If delivery is electronic, retain recipient consent, and after technical delivery changes, retain renewed written consent. For Form 1099-NEC, both filing and recipient furnishing tie to January 31. Also retain payment and withholding records needed to support reconciliation and tax administration.

- Determination support in one auditable location

Store the reference set for each withholding or treaty determination in one auditable location: IRS tax treaty tables, the treaty text used where needed, internal policy mapping, and validation controls. Do not rely on treaty tables alone. IRS says they are not a complete guide and directs withholding agents to consult applicable treaty provisions. If the reference basis is missing, the decision trail will be harder to defend even when the outcome appears correct.

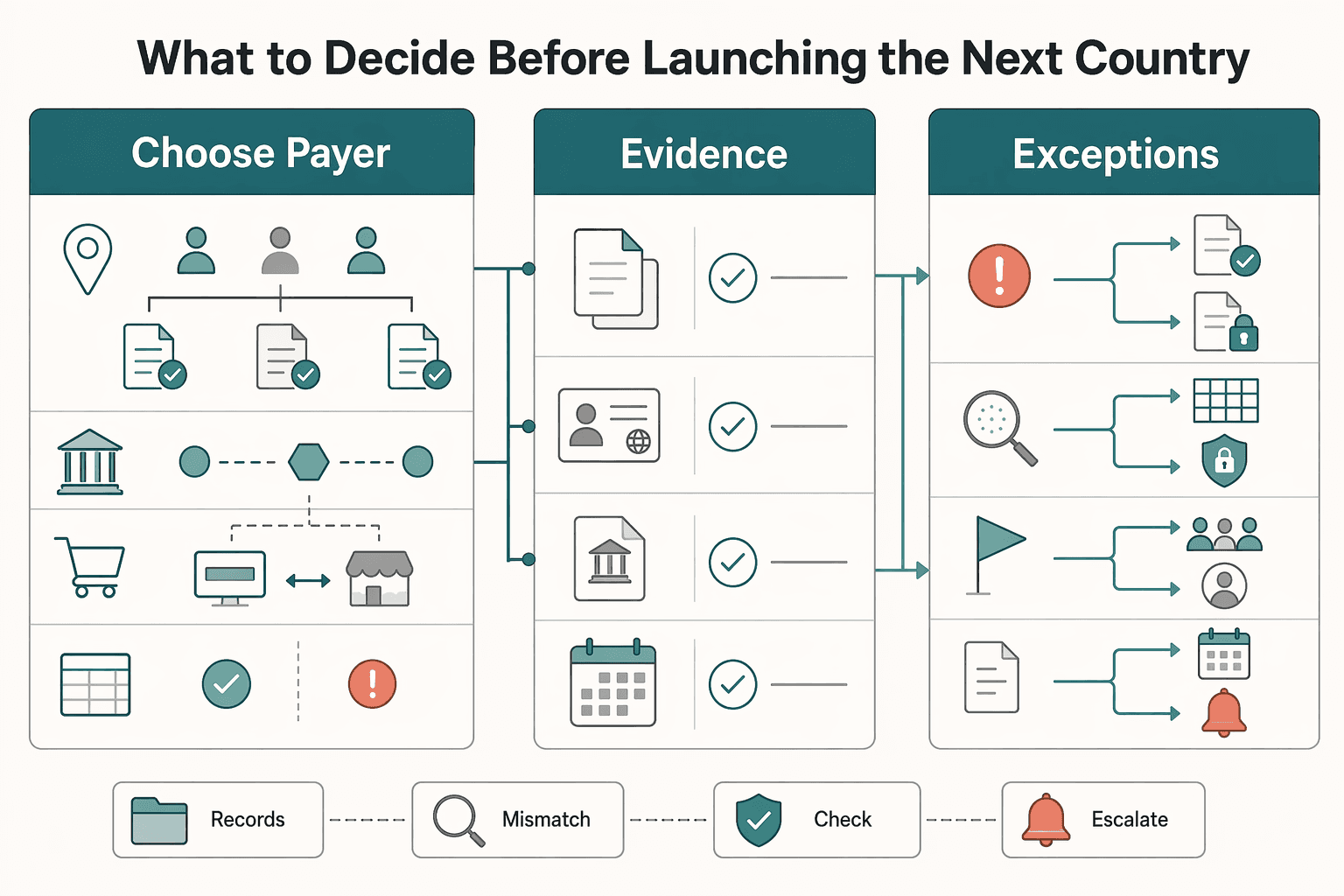

What to decide before launching the next country#

Before you launch a country, lock four decisions: reporting model, tax-document sequence, exception handling, and evidence standards. If any of these gets deferred to year-end cleanup, you are taking on avoidable operational risk.

- Choose a payer and reporting model per country cohort.

Decide whether your creator mix is primarily U.S. persons using Form W-9, foreign individuals using Form W-8BEN, or foreign entities using Form W-8BEN-E. Then confirm the payment rail and payer role, because some transactions are reportable on Form 1099-K instead of Form 1099-NEC or Form 1099-MISC. If you cannot explain that classification clearly, pause launch. Form 1099-NEC filing and recipient delivery are both due by January 31.

- Lock the tax-document sequence before acquisition ramps.

Set the order in product and ops: determine U.S. versus foreign status, collect the matching form, validate required fields, then decide payout eligibility. For U.S. persons, Form W-9 collects TIN and certifications. For foreign payees, the W-8 path documents foreign status and can support treaty-based withholding treatment where applicable. Keep the sequence platform-specific but explicit, because missing or incorrect TINs create backup withholding exposure.

- Define exception rules before exceptions happen.

Write rules for expired W-8s, payee-type mismatches, duplicate tax profiles, and unsupported treaty claims. W-8 lifecycles are not open-ended: Form W-8BEN generally remains effective through the last day of the third succeeding calendar year, and Form W-8BEN-E also has validity and change-in-circumstances lifecycle requirements. Build renewal and failure handling early, especially in non-U.S.-heavy cohorts. Missing tax info can also affect payouts, with at least one major platform warning it may be required to deduct up to 24% of total worldwide earnings when tax info is not provided.

- Set a go or no-go evidence bar and enforce it every launch.

Require retained proof for versioned tax forms, validation outcomes, payout status linked to tax-profile state, and records showing Form 1099-NEC recipient-delivery timing. Because W-8 forms are provided to the withholding agent or payer and not sent to the IRS, your own records are a core control. Use the comparison table and evidence checklist as the gate: if you cannot show the form, validation result, payout decision, and override rationale, delay rollout.

Related: 1099-K Reporting Threshold Changes: What Platform Operators Need to Know After the IRS Delay.

If you want to confirm country coverage, payout gating, and audit-trail requirements for your launch plan, talk to Gruv.

Frequently Asked Questions

Do non-U.S. creators receive `Form 1099`?

Not as a universal rule in the sources used here. In Poe’s creator program, non-U.S. participants use Form W-8 to confirm they are not U.S. persons, and Poe says it is required to issue Form 1042-S to nonresident aliens earning price-per-message payments. If a provider says international creators do not get a 1099, confirm which reporting form applies instead.

What is the difference between `Form W-8BEN` and `Form W-8BEN-E`?

The provided excerpts do not define this difference. They only support that, in Poe’s workflow, creators can download and edit a completed Form W-8 in the Stripe Express Dashboard under Tax Forms. Treat BEN vs BEN-E routing as platform-specific until you verify it in your own tax workflow.

When are `Form 1099` documents typically issued on creator platforms?

These sources do not establish one standard issuance timeline across platforms. They do show that Poe uses Stripe to collect taxpayer information and complete U.S. 1099 filings. They also show that Form 1042-S in that program is prepared by Poe, not through Stripe.

How often should international creators renew `Form W-8`?

The excerpts provided here do not support a single fixed renewal interval across platforms. Use the renewal timing defined by the platform and policy you actually operate under. In the Poe setup, creators can go to the Stripe Express Dashboard under Tax Forms to download and edit a completed Form W-8.

What happens if a creator is from a country without a `U.S. tax treaty`?

These materials do not provide a universal rule for rates, fallback documents, or required forms in that situation. Treat treaty-edge cases as unresolved until you validate the treatment for your platform. The IRS bulletin excerpt also states it may not be relied on as an authoritative interpretation.

Can one creator receive multiple `Form 1099` records?

The provided excerpts do not establish a universal yes-or-no rule. What they do support is that reporting paths can differ by platform and form type. Design your internal process so any statement outcome can be explained from your own payer and reporting records.

What should operators do when platform rules are unclear across providers?

Treat unclear rules as unresolved requirements before you scale. Validate how your platform handles Form W-8, who prepares each reporting form, and when Form 1042-S applies in your operating model. Do not turn one provider’s FAQ language into a universal rule.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

How to Handle Tax on Patreon and Other Crowdfunding Income

Tax season should not feel like a siege. For many creators, it does. The fix is not a bigger spreadsheet or a last-minute scramble. It is a setup you build on purpose, in the right order.

1099-K Reporting Threshold After the IRS Delay: Control Updates for Platform Operators

This is a controls update, not a news recap. If your Form 1099-K program was built around transition-era assumptions, recheck it against the current IRS baseline before you change workflow or code.

Digital Platform Reporting for Online Marketplaces: MRDP, DAC7, and UK HMRC Duties

Digital platform reporting is an operating control, not a year-end cleanup task. For online marketplaces, seller and income data should be collected and verified as part of normal operations, not reconstructed later. If you run a marketplace, you need this data model working before filing season, not after it.