Quick Answer

Start by locking invoice currency and stating that payment is complete only when the full invoiced amount reaches your designated account. That rule, plus a side-by-side payout-path cost check, removes much of forex risk for freelancers before money moves. Next, decide whether holding foreign balances solves a real operating need or just adds admin burden. If you are a U.S. person, verify FBAR (FinCEN Form 114) and possible Form 8938 requirements before balances grow.

Beyond the Exchange Rate: A Freelancer's Guide to Mastering Forex Risk#

Your problem is not just getting a bad rate on payday. It is invoice value drifting between issue and settlement, payouts landing at amounts you couldn't predict, and account choices that create reporting exposure. That is what forex risk for freelancers looks like in practice.

Foreign exchange risk is your exposure when a foreign currency moves against your home currency. In practice, it shows up in more than one place. If rates change between the transaction date and the settlement date, your home-currency result can rise or fall. Providers can also affect your net payout. Some providers state that their transaction exchange rate is adjusted regularly and includes a currency conversion spread on top of a base rate. So two freelancers can invoice the same amount and still keep different totals because their payment route is different.

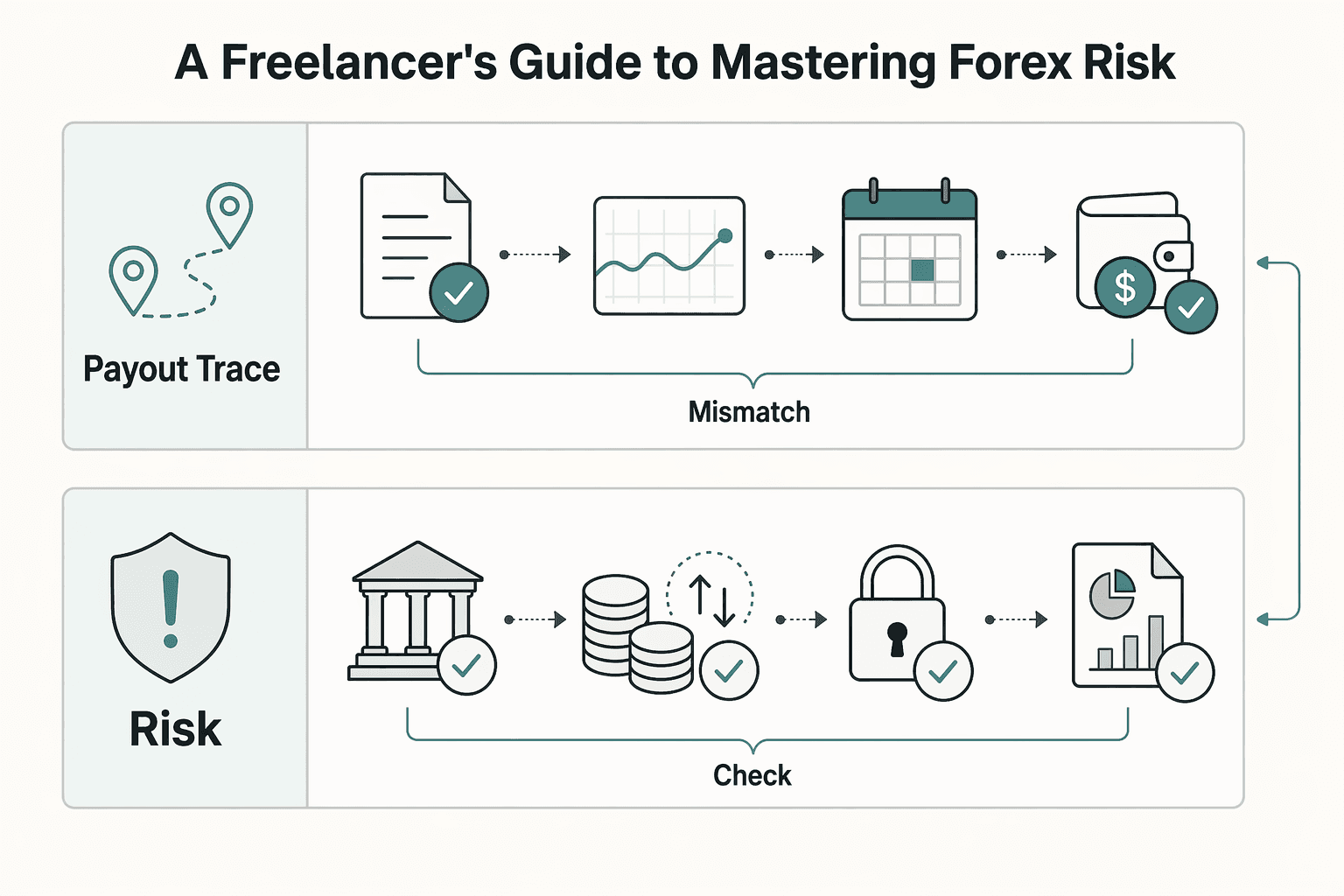

Use this guide as a three-part risk map. Each part ties to a different decision:

- Transaction risk: What can change this invoice before cash settles? Focus on rate movement, settlement timing, and conversion spread in your payout route.

- Operating-model risk: What in your workflow can increase uncertainty? Focus on how you invoice, where you receive funds, and how many conversion steps sit between payment and your business account.

- Compliance risk: What reporting burden comes with the accounts you hold? For a U.S. person, FBAR is generally a live checkpoint if aggregate foreign financial account value exceeds $10,000 at any time during the calendar year reported. Do not assume every wallet counts. Verify account classification before you hold larger foreign balances.

This split matters because each tier supports a different decision. Tier 1 helps you choose invoice currency, payment method, and conversion point for more predictable settlement. Tier 2 helps you tighten your invoicing and account workflow so exchange-rate moves and timing are less likely to surprise monthly cash flow. Tier 3 helps you decide what to hold and what to report so convenience does not turn into a compliance problem.

If a client wants to pay in a foreign currency, treat that as a contract-stage decision. Get advice before finalizing terms; do not leave it as a back-office detail. The next sections give you reusable checks: first what to verify before invoicing, then how to compare payout routes before accepting one, and finally what to check before holding foreign balances.

If you want a deeper dive, read A guide to currency options for 'hedging' against forex risk.

Tier 1: Tactical Defense - Securing Every Cross-Border Transaction#

This tier is about payment control. Decide invoice currency and payout setup before money moves so you reduce conversion loss, settlement uncertainty, and hidden-fee erosion. If you cannot receive and hold the client's currency without forced conversion, default to invoicing in your home currency.

The key choice here is not just invoice currency. It is who absorbs rate movement, where conversion happens, and whether the payout route adds hidden cost.

Choose the invoice currency with the payout path in mind#

Choose currency by scenario, then verify the exact receiving account and when conversion happens. Labels are not enough.

| Client scenario | Invoice currency | Payout path to confirm | Who carries rate-move risk | Practical default |

|---|---|---|---|---|

| Small, one-off project | Your home currency | Route settles directly in that currency | Client | Best for certainty and fewer moving parts |

| High-value, long-term client wants local-currency billing | Client currency | Multi-currency account that can receive and hold that currency without forced immediate conversion (for example, a Wise-style setup) | You until conversion | Use when lower client friction is worth managing conversion timing |

| Platform/marketplace payout required | Depends on platform terms and your receiving setup | Confirm whether conversion happens on receipt, withdrawal, or both | Depends on platform terms | Use only after mapping the full path from platform balance to bank |

If your receiving setup auto-converts on arrival, you are not controlling conversion timing, even if the invoice is in the client's currency.

Price the payout path, not just the invoice amount#

Do not judge a route by the invoice total alone. Price the full payout path with a simple total-cost framework:

transfer/platform fees + FX spread + forced-conversion impact + payout-timing impact

Use this before each invoice so you compare like-for-like payout routes, not marketing claims. Save the fee page, FX disclosure, remittance instructions, and receiving-account details with your invoice records. That makes shortfalls easier to trace later.

Make payment completion explicit in the contract#

Put this in your agreement so payment expectations are explicit.

- Intent: payment is complete only when the full invoiced amount reaches your designated account.

- Baseline wording: "Payment is considered complete only when the full invoiced amount is received in the freelancer's designated account."

- Fallback wording if there is pushback: state that the client is responsible for transfer and conversion charges required for you to receive the invoiced amount in the agreed currency.

- Legal note: add jurisdiction-specific phrasing after legal review before relying on it in signed contracts.

Pick a payment method by fit, not brand#

Start with the route that fits the job, then check how that route handles deductions, conversion, and control. What matters is not the logo on the checkout page. It is how the money actually moves.

| Method | Best use case | Fee transparency | Access timing | Compliance implications |

|---|---|---|---|---|

| Direct bank transfer | Larger clients with formal AP workflows | Can vary by route; intermediary deductions are possible | Can vary by route and banking chain | Document deductions and conversion points |

| Multi-currency receipt account | You accept client currency and choose conversion timing | Often clearer, but verify exact conversion mechanics | Depends on whether funds are truly held in that currency | Reporting/admin burden depends on jurisdiction |

| Platform/marketplace payout | Client will only pay inside a platform | Posted fees may not reflect the full payout path | Depends on platform release and conversion terms | Platform balance structures can add operational complexity |

Decision rule before every invoice: confirm what currency lands, which account receives it, whether conversion is optional or automatic, and who pays transfer and conversion costs. If any answer is unclear, simplify the route or price that uncertainty into the job.

For a related legal-operational angle, see Permanent Establishment Risk: A Guide for US Freelancers with a Single Large Client in Germany.

Before you lock your payout route, run your likely methods through this payment fee comparison and keep the output in your client onboarding checklist.

Tier 2: Strategic Operations - Building a Forex-Resilient Business Model#

At this tier, the goal is predictability: revenue behaves more consistently across currencies because your setup is better, not because you got lucky on timing.

Focus on three controls. First, check how concentrated your currency exposure is. Then look at how long receivables stay exposed before conversion, and decide when contract terms may need review if exchange moves materially change deal economics.

Use client mix as a natural hedge, but verify the match#

Diversification helps only if currency inflows and outflows actually offset in amount and timing. If they do not, you still carry meaningful net exposure.

| Exposure pattern | Assumptions to verify | Likely outcome to verify | Operator note |

|---|---|---|---|

| Concentrated | Most revenue in one foreign currency; most costs in your home currency; conversion happens after payment lands | Full exposure to that pair until conversion | Highest sensitivity to one rate move |

| Partly diversified | Revenue split across two currencies; costs still mostly in your home currency; conversion timing differs by client | Partial offset, but swings can still be material if one currency dominates | Better than concentration, but not a true hedge unless timing also lines up |

| Diversified and matched | Revenue spread across multiple currencies; some recurring costs paid in one of those currencies; only net surplus is converted | Lower net exposure when inflows and outflows genuinely match | Strong natural-hedge setup if records confirm the match |

Watch for fake diversification. Invoicing in multiple currencies does not reduce risk if you convert everything immediately without a matching outflow strategy.

Turn contract structure into an operating policy#

Shorter exposure windows are the core control. Under IAS 21, rates at transaction date and settlement date can differ. That difference creates exchange differences.

| Control | What to set | Article note |

|---|---|---|

| Upfront funding | Require upfront funding before work starts | For fixed-price platform work, pre-funded milestones are one baseline control |

| Paid checkpoints | Break delivery into smaller paid checkpoints | Less revenue remains exposed at any one time |

| Conversion timing | Convert on receipt, convert on a fixed schedule, or hold only what you need for known foreign-currency expenses | Set conversion timing rules in advance |

| Payout timing | Verify payout timing by contract type before committing to your own cashflow dates | Platform timelines can differ across help pages and contract models |

For longer engagements, put the rule in writing rather than deciding ad hoc each time:

- Require upfront funding before work starts where available; for fixed-price platform work, pre-funded milestones are one baseline control.

- Break delivery into smaller paid checkpoints so less revenue remains exposed at any one time.

- Set conversion timing rules in advance, for example convert on receipt, convert on a fixed schedule, or hold only what you need for known foreign-currency expenses.

- Verify payout timing by contract type before committing to your own cashflow dates. Platform timelines can differ across help pages and contract models.

Add a fair renegotiation trigger for long contracts#

Longer contracts need a review mechanism, not an assumption that the starting rate will hold. A hardship-style structure works well: if performance becomes excessively burdensome due to an unforeseen event, either side can request review.

Keep it symmetrical and explicit. Define at signing what exchange-move conditions allow either party to request a repricing review and how that review is handled. Treat this as a fairness clause, not a one-way increase, and have local counsel validate the wording before you rely on it.

Stewardship checklist#

Keep the operating review simple, but do it deliberately and on a regular cadence.

- Recheck your currency mix on a regular internal cadence using actual invoice, payout, and expense data.

- Keep records for contract-date rate reference, invoice date, settlement date, and conversion confirmation on larger foreign-currency jobs.

- Re-verify platform payout, hold, and dispute rules whenever cash planning depends on them.

- If timing controls are not enough for recurring exposure, evaluate formal hedging tools such as forward contracts, and start with A Guide to Currency Hedging for Freelancers.

- Before relying on any platform workflow, review the operational terms in Analyzing the Terms of Service for Upwork and Fiverr: What Freelancers Miss.

Related reading: A Guide to Index Fund Investing for Freelancers.

Tier 3: Compliance Fortification - Eliminating Catastrophic Risk#

If holding a foreign balance gives you conversion flexibility but adds reporting duties you cannot manage cleanly, do not hold it. At this tier, the priority is a defensible setup: clear account structure, complete records, and year-end reporting you can support.

Tier 2 was about shortening exposure windows. Once you hold foreign currency longer, the administrative and reporting stakes go up too. The decision has to work operationally, not just on rate timing.

Benefits and obligations#

A multi-currency account can add flexibility: you may receive payments in the invoice currency, convert later, and pay matching foreign expenses. The tradeoff is more reporting checks and more documentation if your treatment is reviewed.

| Setup choice | Flexibility benefit | Compliance obligation | Main red flag |

|---|---|---|---|

| Home-currency account only | Simple reconciliation and fewer moving parts | Usually lower added reporting burden | Forced conversion on receipt can increase rate exposure |

| Dedicated business multi-currency account | Hold client funds in original currency and convert on your schedule | May add foreign-account reporting analysis depending on balance levels, provider structure, and jurisdiction | Opened for convenience without a recordkeeping process |

| Multiple foreign accounts with mixed business and personal use | High flexibility | High tracking and reconciliation burden; greater risk of incomplete reporting | Commingled flows make ownership and purpose hard to prove |

Do not assume every account, wallet, or platform balance is treated the same. Verify current rules for your jurisdiction and provider structure before optimizing for conversion timing.

Set up accounts so reporting is obvious#

The cleanest setup is usually the simplest one. Separate business and personal flows, keep an inventory of every account that can hold client funds, and document ownership and jurisdiction for each one. If needed, use Separating Business and Personal Finances: An Important Step for LLCs as your baseline.

| Inventory field | What to track |

|---|---|

| Legal owner | Track legal owner |

| Account purpose | Track account purpose |

| Jurisdiction | Track jurisdiction |

| Open and close dates | Track open and close dates |

| Currencies held | Track currencies held |

| Where statements are stored | Track where statements are stored |

At year-end, keep statements and balance records so you can reconstruct what was held, where, and by whom.

Track rate differences like tax evidence#

Rate differences are not only a cashflow issue. They are also a reporting issue. Treatment depends on your facts and jurisdiction, so confirm current treatment with a qualified advisor.

| Stage | Date detail | Rate or proof |

|---|---|---|

| Invoice | Invoice date | Invoice rate |

| Receipt | Date funds were received or made available | Receipt-date rate |

| Conversion | Conversion date if later | Conversion rate |

| Statements | Each step | Supporting statements |

For each foreign-currency invoice, keep the invoice date and rate. Also keep the date funds were received or made available, the receipt-date rate, the conversion date if later, the conversion rate, and supporting statements for each step. IRS Publication 525 is a practical checkpoint for timing questions, including constructively received income, assignment of income, advance payments, and self-employment tax.

Quick decision check before you hold foreign balances#

Before you hold funds in foreign currency, ask three blunt questions:

- Does this reduce real payment friction, or am I just taking a timing bet?

- Does this add reporting duties I have not verified yet, including any filing triggers in my jurisdiction?

- If reviewed at year-end, do I already have the ownership, balance, and rate records to support my position?

If the first answer is weak and the next two are uncertain, convert sooner and keep the setup simpler. You might also find this useful: A Guide to Invoice Factoring for Freelancers.

Conclusion: You Are the CEO of Your Financial Destiny#

You do not need to predict exchange rates to reduce forex risk. You need three habits that show up with every new client: set up each transaction well, structure your client mix to reduce exposure, and check compliance before convenience turns into reporting risk.

At the transaction level, lock in the basics before work starts: invoice currency and payment terms. For smaller one-off projects, invoicing in your home currency shifts currency fluctuation risk to the client. For high-value or long-term clients who want to pay in their currency, agree only if your multi-currency account can receive and hold funds without forced immediate conversion.

At the operating level, reuse the same checks across clients instead of reinventing the process each time. Compare quoted costs with final bank credit and track real settlement timing. That is the practical shift from reacting after the fact to controlling the process earlier: steadier cash flow and fewer payment surprises.

At the compliance level, treat foreign balances as an ongoing responsibility, not a side note. Holding balances can support operations, but it also brings balance monitoring, record retention, and possible foreign account reporting work such as FBAR reporting. If ownership and review cadence are unclear, simplify the setup before balances grow.

For the next week, run this sequence:

- Review contract terms for invoice currency and payment conditions, especially on longer projects.

- Map each payment route you use: visible fees, conversion points, settlement timing, and final bank credit.

- Confirm who owns compliance monitoring for foreign balances, recordkeeping, and whether foreign account reporting obligations may apply.

If you want deeper execution detail, continue with A Guide to Currency Hedging for Freelancers. Also review Analyzing the Terms of Service for Upwork and Fiverr: What Freelancers Miss.

For a step-by-step walkthrough, see A Guide to SEPA Transfers for European Freelancers.

If you want this risk process to run in one place, review Gruv for freelancers for invoicing, conversion, and payout workflows where supported.

Frequently Asked Questions

Do I need to worry about FBAR or FATCA if I hold foreign currency as a U.S. freelancer?

Potentially, yes. Check this before you hold balances for rate timing. If your foreign accounts cross the applicable filing threshold, you may need to file FBAR (FinCEN Form 114) through the BSA E-Filing System, and Form 8938 can be a separate requirement attached to your annual tax return. Do not assume an account is irrelevant because it produced no taxable income. Verify whether you need FBAR, Form 8938, or both, plus the current penalties for noncompliance.

Which payment route usually gives me the cleanest FX outcome?

Usually, it is the route with the fewest surprises, not the one with the lowest advertised fee. Judge routes by total mechanics: fee visibility, conversion-rate transparency, payout timing reliability, and control over payout currency. Use this side-by-side check, then run one real invoice and compare quoted costs with final bank credit before you standardize. | Route | Fee visibility | FX spread transparency | Settlement speed certainty | Control of payout currency | Compliance/admin burden | Best use case | | --- | --- | --- | --- | --- | --- | --- | | Wise account or transfer | High; Wise describes a small upfront fee | High; Wise says it uses the live mid-market rate | Verify by route before use | Medium to high; you can hold 40+ currencies | Moderate if you hold balances and keep records | Direct client payments where you want clear conversion math | | PayPal balance and withdrawal | Mixed; visible fees may not show full conversion cost | Lower; PayPal says its conversion rate includes a spread it retains | Depends on withdrawal path and destination | Medium; PayPal can automatically open a new currency balance | Moderate; balance handling and provider structure need review | Clients who require PayPal or convenience-first flows | | Stripe multi-currency settlement | Good, but setup-dependent | Strong if you accrue and settle in the same currency | Varies by country/industry; initial payout is typically 7-14 days after first live payment | High if you configure separate supported bank accounts per settlement currency | Higher; requires currency-specific bank account setup | Ongoing card billing and repeat volume needing payout control |

What should my client contract say about exchange risk?

Keep it simple. Cover three things: invoice currency, the payment-complete point, and a renegotiation trigger for long projects. State that payment is complete only when the full invoiced amount reaches your designated account in the invoice currency, then define when rate movement triggers a repricing discussion. Validate the wording for your governing law and jurisdiction before you reuse it.

Is a multi-currency account worth it, or is it just extra complexity?

It is worth it when it removes real operational friction, such as matching foreign income and foreign expenses without repeated conversions. The tradeoff is more reconciliation, statement retention, and possible reporting obligations once balances cross the applicable filing threshold. Use it when flexibility solves a repeated operating problem. Avoid it when you are mainly making a rate-timing bet without strong records.

What is the “withdrawal penalty” on freelance platforms and marketplaces?

It is the gap between invoiced earnings and usable cash after payout fees, conversion spread, and payout friction. The risk is margin leakage that is easy to miss when costs are split across multiple steps. Use platform withdrawals for small, convenience-driven jobs. Do not make them the default for larger or repeat invoices unless you have measured the leakage and priced for it.

Can I rely on Form 8938 instead of FBAR if I already report foreign assets on my tax return?

No. Form 8938 does not replace FBAR, and FBAR is not filed with the IRS. Treat this as a two-check process: verify whether you need FBAR, Form 8938, or both, then calendar April 15 and the automatic FBAR extension to October 15.

Try a related tool

Ethan covers payment processing, merchant accounts, and dispute-proof workflows that protect revenue without creating compliance risk.

Sources

- beta.trade.gov/articletrusted

- beta.trade.gov/articletrusted

- bsaefiling.fincen.govtrusted

- irs.gov/businesses/small-businesses-self-employed/re...trusted

- irs.gov/businesses/corporations/foreign-account-tax-...trusted

- kings.edu/pdf/Catalog2014-2015.pdftrusted

- sec.gov/Archives/edgar/data/1210677/0001193125260767...trusted

- trade.gov/foreign-exchange-risktrusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

How LLC Owners Separate Business and Personal Finances

For an LLC, separating business and personal money is best treated as a weekly habit, not a one-time bank setup. It keeps records cleaner, cuts month-end cleanup, and creates clearer boundaries as the company grows.

Currency Hedging for Freelancers Without Guessing the Market

Treat hedging as a cash-flow control choice, not a bet on FX market movements. The goal is to reduce foreign exchange risk that appears between transaction start and settlement. For freelance work, that means protecting what you keep after payment arrives, conversion happens, and funds are withdrawn.

What Freelancers Miss in Upwork and Fiverr Terms of Service

Use this manual when a client request touches platform rules and you need a clear call fast. It is built for **upwork fiverr terms of service** decisions where speed matters, but traceability matters more.