Quick Answer

Start by giving the payer a complete Form W-8BEN before any payment is made, then keep proof it was accepted. If tax was already withheld, assemble a consistent evidence file from payer records, invoices, and matching identity details, then file through the Form 1040-NR path with the right support documents, including Form 1042-S where applicable. For a refund of over-withheld us tax foreigner issue, consistency and a dated follow-up trail are what keep the claim moving.

For global professionals working with U.S. clients, 30% withholding is more than a tax annoyance. It can hit cash flow, slow payments, and create avoidable admin churn. The good news is that this is usually a process problem you can control.

Treat withholding as part of client operations, not as a surprise. The practical approach has three parts: prevent avoidable withholding up front, recover cleanly when it happens, and manage payer risk before it becomes a year-end mess. This article gives you a workable way to do all three so you can keep your U.S. revenue under control.

Phase 1: Proactive Prevention#

The easiest refund is the one you never have to chase. If Form W-8BEN applies to you as a foreign individual, submit a correct Form W-8BEN before any payment is made or credited. Without usable documentation, withholding can default to 30% on gross U.S.-source FDAP income.

Step 1. Use Form W-8BEN as part of onboarding#

Treat Form W-8BEN as a standard onboarding document, not something you send after a problem appears. Your payer can rely on a properly completed W-8BEN to document your foreign beneficial-owner status and, if you qualify, apply a reduced treaty rate.

Use this form only when your facts fit Form W-8BEN for a foreign individual. If the payer tells you a different withholding form applies, stop and confirm that before you send anything. Send it before the first payment run, then get written confirmation that the payer accepted it.

Step 2. Complete the fields that drive withholding#

Many withholding problems come from fields that are missing, inconsistent, or unclear. Focus on the entries the payer actually relies on:

- Identity and status: your legal name should match the payer's records, and you are certifying foreign individual and beneficial-owner status.

- Permanent residence address: use the address in the country where you are a tax resident for that country's income tax purposes.

- Foreign TIN details: if requested, enter them carefully and consistently with your local tax records.

- Treaty claim details: if you claim a reduced rate, include the treaty country and the specific treaty article/paragraph that supports it.

- Article conditions: where relevant, confirm conditions such as no U.S. permanent establishment.

- Signature and date: incomplete, inconsistent, or outdated forms may not be reliable documentation.

| Service-provider scenario | What to enter | What to verify | Expected withholding outcome |

|---|---|---|---|

| Treaty claim clearly applies | Foreign-status details plus treaty country, article/paragraph, and reduced rate claim | Tax residency, beneficial-owner status, article fit, any LOB requirement, and PE condition if required | Payer may apply a reduced treaty rate if facts and treaty terms support it |

| Treaty claim unclear | Foreign-status details; do not guess article/rate | Treaty text, income-character fit, and whether payer has reason to doubt eligibility | Treaty relief may be rejected until clarified; default withholding risk remains |

| No treaty claim | Foreign-status details only | Form consistency and completeness | 30% withholding may apply on U.S.-source FDAP income |

Step 3. Validate treaty eligibility before claiming a reduced rate#

Do not claim treaty relief on instinct. Before you claim a reduced rate, verify four basics: treaty-country residency, beneficial-owner status, treaty article fit, and permanent-establishment exposure when the article requires that condition.

| Eligibility item | What to verify | When it matters |

|---|---|---|

| Treaty-country residency | Verify treaty-country residency | Before claiming a reduced rate |

| Beneficial-owner status | Verify beneficial-owner status | Before claiming a reduced rate |

| Treaty article fit | Verify treaty article fit | Before claiming a reduced rate |

| Permanent-establishment exposure | Verify permanent-establishment exposure | When the article requires that condition |

| Limitation-on-benefits rule | Check whether a limitation-on-benefits rule applies | If the payer has reason to know the claim is not eligible, treaty rates cannot apply |

Also check whether a limitation-on-benefits rule applies. If your payer knows, or has reason to know, that the claim is not eligible, they cannot apply treaty rates.

Recheck treaty assumptions periodically too. Treaty status can change, and Publication 901 includes recent examples for Hungary, Chile, and Russia.

Step 4. Run a pre-submission QA check before first payment#

Before you send the form, run a quick QA pass:

- Confirm the information across your form and payer records is consistent.

- Confirm your permanent residence address supports your treaty-country claim.

- Confirm foreign TIN details match your local tax documentation, where requested.

- Confirm each reduced-rate claim is supported by the treaty article and your facts.

- Save proof that the payer accepted the form, such as a portal confirmation, ticket ID, or written acknowledgment.

One common breakdown is a missing detail or mismatch that keeps the payer from relying on the form. Build that evidence file now, before you need it.

Set a renewal reminder too. W-8BEN validity generally runs through the last day of the third succeeding calendar year unless your circumstances change earlier. Related: 183-Day Rule Explained: Stop the Tax Myths Before They Cost You.

Before your next U.S. client payment, prepare a reusable withholding packet so your treaty details are consistent each time with the W-8 form generator.

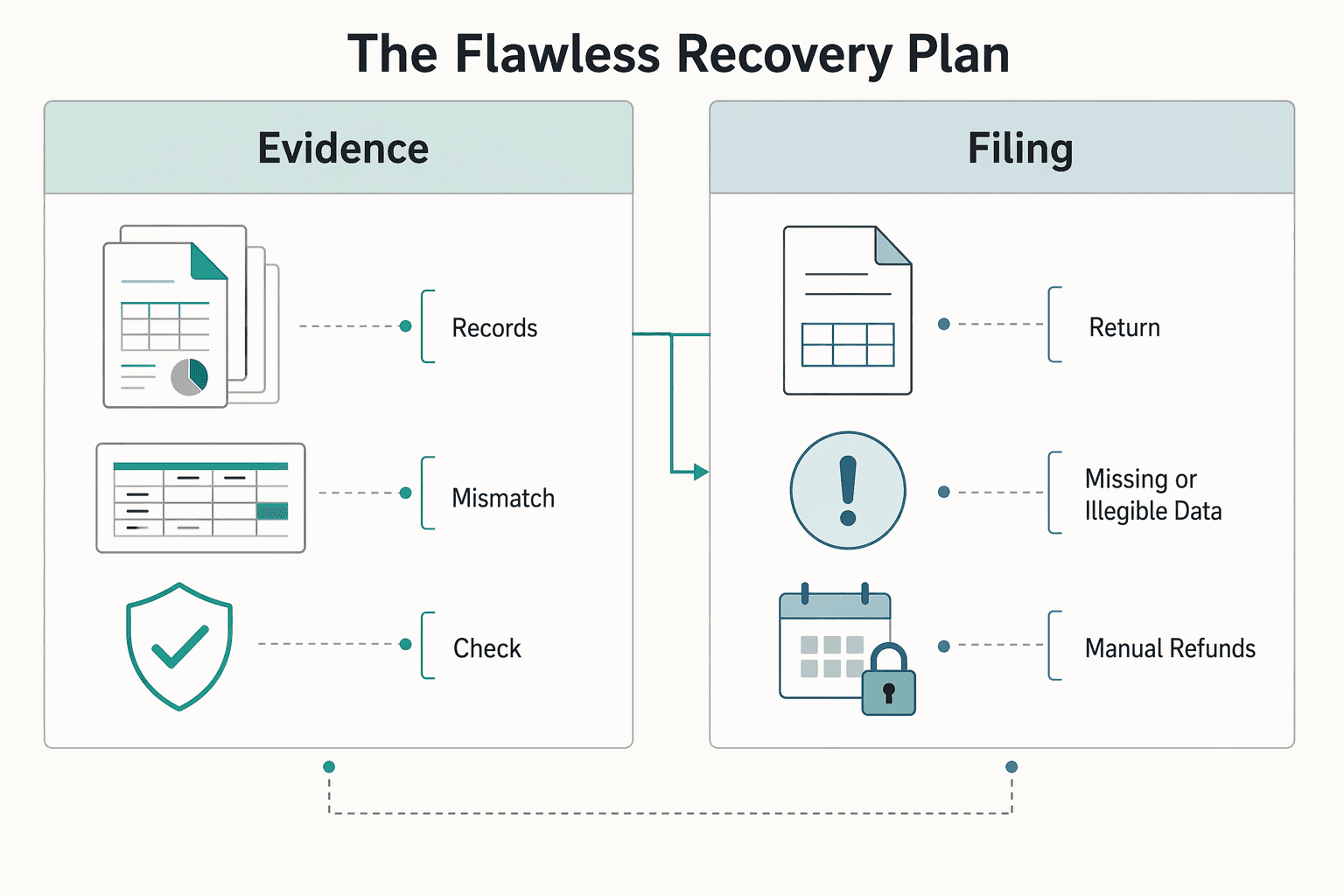

Phase 2: The Flawless Recovery Plan#

Once over-withholding happens, the job is straightforward: give the IRS a clean file it can process without guesswork. From that point on, think in terms of documentation control. IRS processing for Form 1042 withholding returns includes paths for "Missing or Illegible Data" and "Manual Refunds." Consistency across your records is the piece you can actually control.

Assume from the start that delays are possible. The Taxpayer Advocate has identified international withholding relief as an area with delay and hardship risk. Build your follow-up trail right away instead of waiting for a notice.

| Recovery scenario | Key inputs to assemble | Likely friction points | Your next action |

|---|---|---|---|

| You have complete payer documents | Payer withholding records, your invoices/payment records, contract, and your submitted withholding documentation | Name/address mismatches, amount mismatches, unclear or inconsistent fields | Reconcile identities and amounts line by line before filing |

| You are missing payer documents | Your payment trail, invoice trail, contract, and dated requests to the payer for withholding records | Slow payer response, incomplete files, unreadable data | Start a formal document chase now and keep a dated log |

| First-time filing and no taxpayer ID on file | Identity records, tax records, payer evidence, and current IRS instructions for your filing path | Incomplete ID package, identity-data mismatch across documents | Confirm whether ID setup is required for your path, then assemble that package before submission |

-

Gather evidence first. Pull the payer-side withholding records and your own backup records, then check that names, addresses, dates, and amounts line up across the file.

-

Reconcile before you file. Build a simple internal sheet showing each payment, what was withheld, and which document supports each number. Resolve conflicts before you prepare the claim.

-

Assemble the filing package for your verified path. Use the current IRS instructions for your exact situation, include the supporting evidence set, and make sure identity fields match across every document.

-

File against a verified deadline window. Confirm the current IRS claim window for your filing path, then set an internal buffer deadline so missing documents do not cost you the claim.

-

Keep a full post-filing trail. Save what you sent, when you sent it, and every notice or follow-up contact. If processing stalls or a notice is unclear, that record protects you.

If you want a deeper dive, read The Ultimate Digital Nomad Tax Survival Guide for 2026.

Phase 3: CEO-Level Client Risk Management#

Use Phase 2 as the control standard for every new U.S. payer. Confirm who actually controls withholding, lock document duties into the contract, and catch errors before you need Form 1040-NR.

Step 1. Confirm who is the withholding agent before first payment#

Do not assume the contract signer is the tax-reporting party. The withholding agent is the party with control over payment flow, and more than one party can qualify in a chain, with tax withheld only once.

| Payer model | Likely withholding agent | Records you should collect | Who should issue tax forms |

|---|---|---|---|

| Direct client pays you from its own U.S. entity | Usually the U.S. payer making the payment | Contract, invoices, remittance records, your submitted Form W-8BEN, payer receipt confirmation | That payer should issue Form 1042-S when reporting applies and file Form 1042 |

| Marketplace/platform controls payout | Platform or intermediary if it controls payment | Tax-profile screenshots, submitted W-8BEN data, payout ledger, support tickets, payout confirmations | The platform or intermediary with reporting duty should issue Form 1042-S when applicable |

| Mixed chain (agency, client, processor) | Depends on who controls payment/custody | Written confirmation of who pays, who holds funds, legal entities in chain, invoice path, payment notices | Get written confirmation of which entity will furnish Form 1042-S |

Before work starts, get a written answer to one question: "Which entity will pay me, hold my Form W-8BEN, and issue Form 1042-S if required?" If nobody can answer clearly, treat that as a control failure.

Step 2. Put tax duties into contract language#

If tax handling is not spelled out, it usually becomes a problem later. Make it explicit in your MSA, SOW, or onboarding addendum. Use this clause checklist:

| Clause area | Contract should cover | Timing or trigger |

|---|---|---|

| Withholding-agent responsibility | Identify the expected withholding agent and require collection and retention of your Form W-8BEN | Before first payment |

| Form-delivery obligation | Require prompt delivery of any Form 1042-S and require corrected forms | When the original is inaccurate or incomplete |

| Correction workflow | Require written mismatch notice, exchange of supporting records, and corrected recipient form issuance | Within a contract deadline |

| Escalation path | Name finance or legal contacts | For missing, late, or inconsistent documents |

This gives you a contract route if Form 1042-S is not furnished correctly and helps reduce unknown-recipient risk at the maximum applicable withholding rate.

Step 3. Run a repeatable onboarding communication flow#

A short, consistent onboarding package prevents a lot of later confusion. Send these together: the signed contract, your Form W-8BEN, and a brief tax-confirmation note. Ask for written confirmation of:

- Your legal name and country

- Your TIN (if applicable) for treaty-rate treatment

- Which entity will issue Form 1042-S if reporting applies

Store that acknowledgment, whether by email, portal confirmation, or support ticket, with the contract and W-8BEN. If a dispute comes up later, you can show the date, file version, and recipient.

Step 4. QA every Form 1042-S as soon as you receive it#

Treat Form 1042-S as a reconciliation document, not just a year-end form. Check it against your invoices, payment records, and W-8BEN data:

| 1042-S check | Match against | If it fails |

|---|---|---|

| Gross income and withholding amounts | Your ledger | Request a corrected Form 1042-S |

| Income code and tax rate | Payment type and treaty position | Request a corrected Form 1042-S |

| Name, address, country, and TIN fields | Your W-8BEN data | Request a corrected Form 1042-S |

| Required fields, including the unique form identifier | A complete and readable form | Request a corrected Form 1042-S |

If any of those checks fail, start the correction process immediately: "Please issue a corrected Form 1042-S because the recipient details and/or payment amounts do not match the source records we provided."

Ask for a corrected recipient copy, not just an email note. If they say they will fix over-withholding later, ask whether they are still within the adjustment window tied to the extended Form 1042-S filing due date. If not, prepare for the Form 1040-NR refund route. You might also find this useful: A Guide to Dual-Status Alien Tax Returns.

Conclusion: From Anxious Freelancer to Empowered CEO#

Protect cash flow by treating withholding as a repeatable process risk. Prevent problems early, recover quickly when withholding happens, and manage reporting risk on every client. That matters in a system where international withholding relief was identified as one of the 10 most serious taxpayer problems in FY 2025, with long delays and hardships documented in that report.

Step 1. Prevent#

Complete required tax documentation before payment starts, and keep proof that you delivered it. Your core file should include a dated copy, client acknowledgment, and written confirmation of who controls withholding and reporting in the payment chain. If that control point is unclear, treat it as an open risk.

Step 2. Recover#

If withholding happens, start the refund process immediately while records are still easy to pull. Match withheld amounts to invoices, payment records, and reporting documents, then assemble the support package using the process already covered above. Keep a written request trail throughout, including non-responses.

Step 3. Manage#

Run each client with reporting controls, not assumptions. Check the first payment, confirm who issues year-end reporting, and verify final documents against what was actually paid and withheld. That reduces rework and gives you a cleaner path if you need to claim a refund.

| Situation | Immediate action | Expected outcome |

|---|---|---|

| No withholding yet | Finalize documentation delivery and save proof | Lower chance of avoidable withholding |

| Reporting control is unclear | Get written confirmation before the next payment | Clear accountability if issues arise |

| Tax was withheld | Start the refund workflow and collect records now | Stronger claim file with fewer avoidable delays |

| Payer will not correct withholding | Move to the formal escalation step already outlined | Documented formal path forward |

What you do next:

- Prepare now: organize your tax documentation file, delivery proof, and a folder for reporting documents and correspondence.

- Monitor per client: first-payment accuracy, reporting responsibility, and year-end document consistency.

- If withholding happens: request correction, preserve the paper trail, and follow the correct filing lane.

This is how you stay in control. Protect cash flow through consistent execution you can repeat across every U.S. client. For a step-by-step walkthrough, see How to Check the Status of Your Federal Tax Refund.

If you want to run this as a repeatable operating process across clients, move it into a single payouts workflow with visible statuses using Gruv Payouts, where enabled.

Frequently Asked Questions

What if Social Security or Medicare tax was withheld from me by mistake?

Start with the employer, not the IRS. Ask the employer that withheld the tax to refund it first. The outcome depends on payroll records and whether the employer corrects the withholding.

What if the employer refuses or ignores my request?

Move to Step 2. File Form 843, and include Form 8316 when the employer will not issue the refund. The outcome depends on following current instructions and submitting the required attachments.

What proof do I need to send with Form 843?

The documents matter as much as the form. Include a copy of Form W-2 showing Social Security and Medicare tax withheld, plus the employer statement if available. If you cannot get that statement, provide your own written statement explaining what happened and what you requested.

What if I am an F-1 or J-1 student and I am not sure I qualify?

Confirm your status before filing. In this documented context, F-1 and J-1 students are treated as nonresident aliens during the first 5 calendar years in the U.S., and the exemption criteria are tied to Section 3121(b)(19). The outcome depends on your actual status and whether those criteria match your facts.

What if I never received the year-end form from the employer?

Document your requests right away. Ask for the missing Form W-2 and keep records of each request. If no employer statement is available, include your own statement describing what you requested and what was not provided. The outcome depends on how clearly you can prove withholding and failed employer-side correction.

What if this is my first U.S. taxpayer ID setup?

Verify live requirements before you submit anything. The outcome depends on current Form 843 and Form 8316 instructions for your exact case.

Can I use this same process for treaty-rate or federal income-tax withholding issues?

No. This documented workflow is for the payroll-tax lane and does not establish the process for treaty-rate or federal income-tax withholding refunds. Those cases may require a different form set and different rules.

Can I rely on an IRS FAQ page alone?

Use IRS FAQ content for orientation, not as legal authority. The IRS states those FAQ answers are general guidance and not citable legal authority. Your next step is to rely on current official form instructions and your own records.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

Digital Nomad Taxes in 2026 With a Defensible Filing Plan

With digital nomad taxes, the first move is not optimization. It is figuring out where you may be taxable, where filings may be required, and what proof supports that position.

183-Day Rule Tax Myths That Trigger Residency Filing Mistakes

If you are a mobile freelancer or consultant, start here: the "183 day rule tax" idea is not a single universal test. It is a shortcut phrase people use for different residency rules that do not ask the same question. If you mix federal and non-federal residency logic, you can create filing risk even when your travel calendar looks clean.

Filing a Dual-Status Alien Tax Return Without Mismatched Forms

---