Quick Answer

Choose the path that removes your biggest constraint. For merchant of record for platforms, an MoR can shift Seller of Record liability and reduce day-to-day burden around VAT, GST, refunds, and chargebacks, while a PSP model keeps more control and more responsibility in-house. The practical decision is not branding; it is whether your team can own tax remittance, dispute handling, and audit evidence across markets without creating finance and support drag.

How to evaluate a merchant of record for platforms on compliance fit, not just payment handling#

If you are looking for a merchant of record for platforms, the real question is not what MoR means. It is whether handing off enough payment, compliance, and risk work will help you move faster without creating new problems for product, finance, and engineering later.

That matters because each transaction includes far more than a card payment. It sits inside a complex web of financial processes, legal obligations, and regulatory requirements. An MoR is not just about taking payment. It is about who is set up to handle the surrounding work when you sell across markets or face disputes.

Platform teams feel this quickly because the stack can fragment. 31% of internationally operating companies use four or more solutions across payments, tax, and compliance workflows. Once you are stitching together multiple tools across those workflows, the choice stops being abstract. It becomes an operating decision with real downstream cost. This guide is built around three practical questions:

- Which path fits your current constraint

We compare common options, from outsourced MoR to more in-house ownership. The separator is not branding. It is which side carries the day-to-day burden once payment, tax, and risk work starts piling up.

- Where responsibility actually starts and stops

MoR vendors are often positioned as a way to offload operational work, and MoR software is often framed as handling transaction processing, payments, compliance, and fraud, risk, and chargeback functions. The key distinction is that "handles" does not mean "solves everything." You still need a clear line between what the provider owns, what your platform owns, and what your sellers or internal teams still need to do.

- What to verify before you commit engineering time

A costly failure mode is starting integration before ownership is written down. If you do one thing early, make it this: require a responsibility matrix that names who owns payment operations and dispute handling before any build starts. If a provider cannot describe those boundaries clearly, treat that as a red flag.

The thread through the rest of this article is simple. If your bottleneck is the operational load around payments and compliance, an MoR model may remove enough burden to justify the tradeoffs. If your bottleneck is control over product and economics, you may be better off keeping more ownership and accepting the extra load.

Who this list is for and how to choose the right path#

Use this list if you run multi-party marketplace payments and need to reduce payment and compliance complexity without slowing growth.

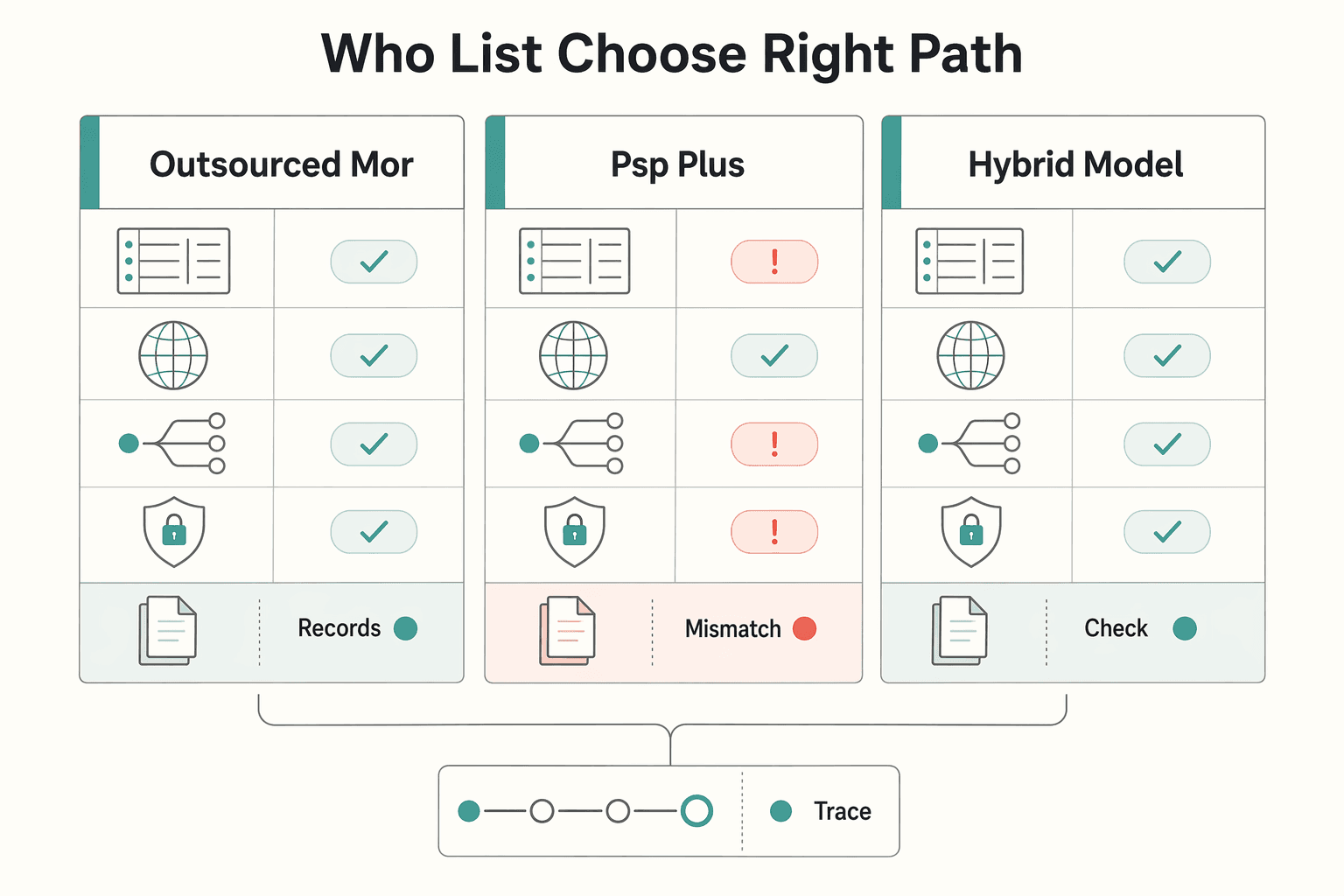

| Path | Best for | Key benefit | Key tradeoff |

|---|---|---|---|

| Outsourced MoR | Teams prioritizing speed and lower internal payment/compliance workload | Launch across regions quickly while shifting transaction liability and operational burden | Less flexibility for custom checkout behavior, unusual pricing rules, and platform-specific payout design |

| PSP plus in-house seller ownership | Teams prioritizing control and able to own seller responsibilities in-house | Maximum product and operations flexibility over checkout behavior, routing logic, fee design, ledger, and reconciliation | Your company remains the seller, so legal and operational responsibility stays with you |

| Hybrid model | Teams using a controlled transition with an existing PSP lane that is stable | Reduces change risk by not moving every market at once and preserves working embedded payments logic in core lanes | Dual-lane complexity can create policy drift in refunds, disputes, support, and reporting |

- Best fit for this evaluation

This guide is for founders, product leads, finance ops, and engineering owners managing more than a basic checkout. If you handle sellers, split funds, cross-border customers, or market-specific payout logic, focus on operating fit over brand familiarity: business model, target regions, product complexity, and internal team bandwidth.

- When to skip a full MoR review

If you only need a standard PSP checkout for a single-store model and do not have cross-border VAT/GST or payout complexity, a full MoR evaluation is often unnecessary.

- How to choose the path

Compare options on four criteria: liability transfer (Seller of Record scope), speed to launch, control over checkout and payout flows, and audit burden under regulatory compliance. If your core risk is tax/compliance execution, bias toward MoR. If your core need is deep checkout control or custom economics, evaluate Payment Service Provider plus in-house ownership.

Before you shortlist providers, ask for draft contract language defining Seller of Record responsibilities and sample transaction/finance exports for reconciliation and audit review. If legal review uses FederalRegister.gov material, verify it against an official Federal Register edition.

If you want a deeper dive, read ASC 606 for Platforms: How to Recognize Revenue When You're the Merchant of Record.

If you need a quick next step, try the free invoice generator.

Option 1 outsourced MoR for fastest global launch#

If your main goal is to launch across regions quickly while shifting transaction liability and operational burden, outsourced MoR is usually the strongest first path.

- Best for: teams prioritizing speed and lower internal payment/compliance workload over deep customization.

- Key pros: avoids building a full in-house payments stack and offloads significant operational work tied to payments, taxes, and customer disputes.

- Key cons: less flexibility for custom checkout behavior, unusual pricing rules, and platform-specific payout design.

- Concrete use case: a creator platform entering new regions that needs MoR liability coverage before building a larger internal tax, risk, and finance-ops function.

An outsourced MoR handles transaction processing, payment collection, and payment-related compliance. Teams usually choose it to simplify operations and reduce risk. In practice, this model helps you move faster without taking on the full execution burden of cross-border tax and payment operations from day one.

Do not assume coverage is identical across providers. Scope and commercial terms vary, and published pricing examples can differ (for example, 4% + 40c US, +1.5% intl, +0.5% subs versus 5% + 50c). Treat public rates as examples and run margin modeling before you sign.

Before integration starts, require a written ownership matrix for Seller of Record duties, including:

- who owns sales tax, VAT, GST, refunds, chargebacks, and payment-regulation compliance

- which exceptions stay with your team

- what transaction/payout exports and escalation paths support reconciliation and audit review

Option 2 PSP plus in-house seller ownership for maximum control#

Choose this path when control is the priority and your team can own seller responsibilities in-house. A PSP helps you collect payments, but your company remains the seller, so legal and operational responsibility stays with you.

When this option is right#

This is the better fit when payments behavior is part of your product, not just checkout plumbing.

- You need custom checkout, routing, margin logic, or a Stripe Connect-style marketplace architecture.

- You want direct control over ledger and reconciliation design instead of relying on a provider default export model.

- You can support that control with in-house finance, legal, and risk ownership across your markets.

- You see potential upside from lower baseline processing fees and are ready to own the operating burden that comes with it.

Decision rule: if you cannot name owners today for sales tax handling, tax remittance, dispute response, and compliance workflows, this option is usually premature.

What you gain#

You gain maximum product and operations flexibility. You can shape checkout behavior, routing logic, and fee design around your model, then map transaction data to your own ledger and reconciliation process.

What you still own#

A PSP facilitates payment. It does not, by default, take on VAT or sales-tax calculation, payment disputes, or the broader compliance burden that comes with being the seller.

Before integration, confirm clear ownership for:

- seller responsibilities by market, including tax handling and remittance

- dispute operations and exception handling

- finance outputs needed for reconciliation and close

Verification checkpoint: get sample PSP exports early and map them to your real finance process before your data model is locked.

Option 3 hybrid model for phased platform scale#

Use a hybrid model as a controlled transition, not a permanent mixed-ownership setup. Keep your existing PSP lane where it is stable, and add an MoR lane only where operating conditions create more coordination overhead.

For cross-border platforms, this can reduce change risk because you are not moving every market at once. You preserve working embedded payments logic in core lanes while you phase rollout in higher-friction lanes.

Where this model earns its keep#

The main benefit is containment. You can limit migration blast radius by changing fewer markets at a time, with fewer simultaneous changes to routing, support flows, and finance handling.

It also protects product logic that already works in core markets, especially when payout timing, fee behavior, or routing is tightly coupled to platform workflows.

Where teams get hurt#

The tradeoff is dual-lane complexity. You now need consistent handling across two operating paths, and policy drift can show up quickly in refunds, disputes, support, and reporting.

That risk increases as your payment footprint expands across contexts like in-store, online, and peer-to-peer flows. Data asymmetries, entrenched market power, and gatekeeping of critical infrastructure are enough reason to assume consistency will not happen by default.

Non-negotiables before you launch#

Use this model only with explicit market-by-market boundaries and one shared audit evidence template across both lanes. At minimum, include:

- market and legal entity by transaction lane

- provider handling each payment path

- exact export/report used for reconciliation and close

- support escalation path and evidence owner for exceptions

Verification checkpoint: run the same order, refund, and dispute scenarios in both lanes, then compare the actual evidence outputs. If one lane produces weaker transaction detail or exception trails, fix that before launch.

If you cannot maintain one ownership matrix and one audit-pack standard across both lanes, stay single-model longer.

What the MoR owns and what your platform still owns#

Start with one rule: for each responsibility, separate legal accountability from operational execution. A Merchant of Record is the legal entity selling to the end customer, and its coverage is broader than PSP-only payment processing, but it is still contract-scoped.

| Responsibility | Legal liability under Seller of Record | Operational execution | Common misread | Verify before launch |

|---|---|---|---|---|

| sales tax | May sit with the MoR where Seller of Record scope is explicit | Can be handled by provider workflows, while your team still handles close/reconciliation needs | "MoR solves tax everywhere" | Confirm covered jurisdictions and notice handling in contract language |

| VAT | Contract-dependent; do not assume inclusion from MoR label alone | Process can be provider-led, with platform teams still needing usable outputs | "VAT is automatically covered in all markets" | Confirm country scope and required evidence outputs |

| GST | Contract-dependent; separate from VAT assumptions | Execution may be shared depending on market and setup | "If VAT is covered, GST is too" | Confirm market list and fallback owner for out-of-scope regions |

| tax remittance | Can be included where contract says collection/remittance is in scope | Provider may remit, but your team still needs proof for controls | "Collection implies remittance proof will be automatic" | Require remittance evidence format, timing, and escalation path |

| refunds | Not automatically transferred by MoR status | Often shared between provider operations and your support policy | "Provider owns every refund outcome" | Define first-responder, approval rules, and handoff timing |

| chargebacks | Not automatically transferred by MoR status | Provider may run dispute flow, but platform evidence can still be required | "Disputes are fully outsourced" | Define evidence deadlines, packet owner, and failure escalation |

| PCI compliance | Do not infer from MoR label alone | Depends on your checkout/data-flow design | "MoR removes all PCI scope" | Document whether card data touches your stack and residual obligations |

| statement descriptor handling | Not established by MoR status alone | Implementation-specific; support still needs buyer-facing handling | "Descriptor behavior is guaranteed by default" | Test live descriptors and document support scripts/escalation |

Separate accountability from action#

Treat each row as two assignments: who is legally accountable under Seller of Record terms, and who actually performs the task day to day. This is where teams avoid rework from vague ownership assumptions.

The checks that catch bad assumptions early#

For every row, lock three items before launch:

- Contract language

Find the exact clause that defines Seller of Record scope by market or program. If a duty is not explicit, treat it as unconfirmed.

- Support handoff rules

Define who gets the first case, who can act, and when it escalates to the provider.

- Failure escalation paths

Name the owner or queue for missing evidence, unresolved disputes, tax notices, and descriptor confusion.

Related: What Is a Merchant of Record? How It Shifts Liability for Platforms.

Finance and accounting checks before you sign#

Before you sign, make sure finance can clearly defend four things: your ASC 606 position, your audit evidence pack, edge-case behavior for refunds and chargebacks, and jurisdiction-by-jurisdiction regulatory compliance scope.

| Check | Confirm | Evidence or test |

|---|---|---|

| ASC 606 position | How the setup affects revenue recognition under ASC 606 and the principal versus agent framework | Assign an owner for the policy memo, confirm auditors can review the contract set, and define close procedures that match Seller of Record scope |

| Audit artifacts | What you will receive for close and audit, including transaction-level exports, dispute evidence, tax documents, and reconciliation fields | Require explicit contract language and validate with sample outputs before signature |

| Refund and chargeback edge cases | Behavior for partial captures, reversals, partial refunds, multiple refunds on one order, and cross-border scenarios | Define who submits evidence, what your team must provide, and how lifecycle status is reported back for reconciliation |

| Compliance duties by jurisdiction and program | In-scope jurisdictions, where coverage differs, what evidence proves performance, and who receives notices | Require contract language that names scope by market and program |

- Lock the ASC 606 position before procurement closes.

A Merchant of Record setup can change how you assess revenue recognition under ASC 606 and the principal versus agent framework, so treat this as an accounting decision, not vendor shorthand. Assign an owner for the policy memo, confirm auditors can review the contract set, and define close procedures that match the actual Seller of Record scope by market or program. For a deeper walkthrough, use ASC 606 principal vs agent.

- Put required audit artifacts in the contract.

Do not rely on sales-call assurances. Require explicit language on what you will receive for close and audit, including transaction-level exports, dispute evidence, tax documents, and reconciliation fields linking orders, refunds, fees, taxes, and payouts to your ledger. Validate with sample outputs before signature.

- Test refund and chargeback edge cases before launch.

Confirm behavior for partial captures, reversals, partial refunds, multiple refunds on one order, and cross-border scenarios. For disputes, define who submits evidence, what your team must provide, and how lifecycle status is reported back for reconciliation.

- Define compliance duties by jurisdiction and program.

MoR coverage is often described as broad, but scope can vary by market and program. Require contract language that names in-scope jurisdictions, where coverage differs, what evidence proves performance, and who receives notices when issues occur.

You might also find this useful: What is a Merchant of Record (MoR) and How Does It Work?.

Implementation sequence for the first 90 days#

Use a strict order: lock ownership first, design integration second, prove finance controls in a pilot third, then launch market by market. This reduces the contract, tax, and PSP rework that shows up when teams start ad hoc.

| Phase | What to do | What to finish with |

|---|---|---|

| Freeze the ownership map | Map the flow from charge to invoice, payout, refund, dispute, and ledger entry, then mark where MoR, PSP, and Seller of Record duties change | One responsibility matrix shared by finance, legal, ops, and engineering, with named owners per market where needed |

| Design integration | Define API/webhook behavior with idempotent retries, replay handling, and reconciliation outputs that connect invoices, payouts, refunds, fees, taxes, and disputes to a stable transaction record | Test sample payloads and exports so one order can be traced end to end without manual stitching |

| Run a controlled pilot | Pilot real VAT/GST, invoice generation, refund paths, and dispute handling, then run a finance close simulation and reconcile pilot activity to settlements and ledger postings | Use the same evidence pack you will use after launch |

| Launch by market | Roll out in stages with testing scripts, rollback triggers, documented rollback procedures, and daily cutover communication | Define stop criteria such as invoice failures, settlement mismatches, missing tax outputs, or dispute-notice gaps, and run a weekly exception review in the first weeks |

- Freeze the ownership map before anyone writes production code.

Map your current flow from charge to invoice, payout, refund, dispute, and ledger entry, then mark where MoR, PSP, and Seller of Record duties change. In a true MoR model, the merchant becomes the seller to the customer and takes seller-side duties, including invoicing, acquirer-facing merchant role, and VAT/chargeback liability. End this step with one responsibility matrix shared by finance, legal, ops, and engineering, with named owners per market where needed.

- Design integration for retries, evidence, and ledger traceability.

Define API/webhook behavior with idempotent retries, replay handling, and reconciliation outputs that connect invoices, payouts, refunds, fees, taxes, and disputes to a stable transaction record. Before build signoff, test sample payloads and exports to confirm one order can be traced end to end without manual stitching.

- Run a controlled pilot, then simulate close.

Pilot real VAT/GST, invoice generation, refund paths, and dispute handling so you can verify responsibilities in practice, not just in contract language. Then run a finance close simulation and reconcile pilot activity to settlements and ledger postings using the same evidence pack you will use after launch.

- Launch by market with explicit rollback controls and exception review.

Roll out in stages with testing scripts, rollback triggers, documented rollback procedures, and daily cutover communication. For each market, define stop criteria such as invoice failures, settlement mismatches, missing tax outputs, or dispute-notice gaps. In the first weeks, run a weekly exception review for chargebacks, refund mismatches, and tax anomalies.

Do not do a full launch until finance, ops, and engineering sign off on the same responsibility matrix and evidence pack.

Conclusion#

Choose the model that removes your actual bottleneck. If speed to launch and compliance liability are what keep stalling the work, outsource to a Merchant of Record with tight boundaries. If checkout control and custom economics matter more, keep ownership with a PSP stack and accept that the extra tax, dispute, and support load stays with you.

- Pick outsourced MoR when liability is the problem

A MoR is the legal entity authorized to accept online payments for products or services, and it is commonly described as assuming financial liability for the transaction while handling end-to-end payment duties. In practice, that often means one provider takes on accepting payments, refunds, sales tax compliance, and local financial regulations that a PSP does not usually cover on its own. What matters is not nicer checkout copy. It is who stands behind the transaction when refunds, tax handling, or regional compliance questions show up.

The tradeoff is real. You may give up some flexibility in how checkout or pricing edge cases are handled, and some providers come with fee or churn concerns. Before you sign, verify the contract by market and by duty. If the agreement is vague on where coverage starts and stops, treat that as a red flag, not a paperwork detail.

- Pick PSP plus in-house ownership when control is the problem

A Payment Service Provider facilitates payment processing, but that is not the same as taking the broader VAT, sales tax, or dispute scope. If you want tighter control over checkout behavior and commercial design, this path can be right. The benefit is freedom, but freedom comes with more operational ownership.

This model breaks when the platform wants custom control but has not assigned real owners for tax, refund, and dispute duties. If your team cannot name who owns sales tax, VAT, refunds, disputes, and the evidence finance will need later, you are not ready for this route yet. A common failure mode is shipping payment flows that engineering can support while finance and support are left manually stitching together what happened after the charge.

- Do not launch either model without proof, not promises

The winning move is a signed responsibility matrix, tested edge-case evidence, and a phased launch plan that finance, product, and engineering all approve. This matters more than any vendor demo because the risk sits in exceptions, not happy-path transactions. Test ugly cases early, especially refunds and disputes, and confirm you can pull the records your teams will need when something goes wrong.

If you remember one rule, make it this: choose by constraint, verify by document, and launch by market only after the ownership map is clear. Vendor messaging can blur the line between MoR and PSP. Your contract, your evidence, and your internal signoff are what keep that blur from turning into expensive rework.

Frequently Asked Questions

What is a merchant of record for platforms in one sentence?

It is a third-party legal entity that takes responsibility for the full transaction process, not just the payment processing step. In practice, you are not only buying checkout infrastructure. You are shifting who stands behind the transaction.

How is MoR different from a Payment Service Provider in day to day operations?

A PSP handles payment processing, while a Merchant of Record is positioned as handling the full payment flow and taking transaction liability. In practice, that can change who owns the broader work around tax handling, compliance in scope, refunds, and chargebacks, not just who moves the money. A red flag is any provider that can demo a successful payment but cannot show who owns the later refund, dispute, and tax trail.

Can a platform be its own Seller of Record and still use a third party PSP?

Yes. Seller of Record and Merchant of Record are often used interchangeably, but they represent different responsibilities and potential liabilities, so a platform can keep seller ownership while using a PSP for processing. If you choose that route, make sure you can name the owner for tax, refunds, chargebacks, and the finance evidence pack before you build.

Does MoR always cover sales tax, VAT, GST, refunds, and chargebacks in every market?

No. MoR providers are commonly described as handling tax collection and remittance, regulatory compliance, checkout localization, and more, but that scope does not automatically apply the same way across every market or program. Verify the contract by jurisdiction, ask what is included market by market, and request sample outputs so you can see what finance and support will actually receive.

How is Stripe Connect different from a full MoR model for marketplaces?

The deciding factor is still contractual responsibility: unless the agreement explicitly transfers end-to-end transaction responsibility and liability, you should assume you retain more of it. That can still be a valid model, but it usually means your team retains more operating work.

What should we verify before choosing a provider for multi party marketplace payments?

Check three things in writing: the responsibility matrix by market, the exact scope of tax and compliance coverage, and who handles refunds and chargebacks when something goes wrong. Then ask for sample transaction exports and trace one order through charge, settlement, refund, and dispute. If your finance team cannot reconcile that path without manual stitching, or if the provider cannot explain coverage by market, keep evaluating.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 1 external source outside the trusted-domain allowlist.

- federalregister.gov/documents/2012/04/03/2012-5317/swap-dealer-a...trusted

- irs.gov/pub/newsroom/Initial%20Assessment%20and%20Pl...trusted

- occ.gov/topics/laws-and-regulations/enforcement-acti...trusted

- occ.treas.gov/publications-and-resources/publications/comp...trusted

- one.oecd.org/document/DAF/COMP(2025)2/en/pdftrusted

- stripe.com/resources/more/merchant-of-recordtrusted

- supremecourt.gov/opinions/23pdf/22-277_d18f.pdftrusted

- checkout.com/blog/what-is-a-merchant-of-recordexternal

Educational content only. Not legal, tax, or financial advice.

Related Posts

ASC 606 Revenue Recognition for Merchant of Record Platforms

If you run a Merchant of Record flow, cash movement is not your revenue policy. Under ASC 606, the hard part is that customer payment, processor settlement, and the point when revenue is actually earned can sit on different dates and in different records.

ASC 606 Principal vs Agent Decisions for Merchant-of-Record Platforms

For merchant-of-record teams, the **ASC 606 principal vs agent merchant of record** call is a high-stakes judgment, not a presentation preference. It can move revenue from gross to net and raise the level of judgment finance, audit, and compliance teams need to defend.

What Is a Merchant of Record? How It Shifts Liability for Platforms

For platform teams, **what is merchant of record** is not a vocabulary quiz. It is the decision about who stands behind the sale when money moves, taxes attach, refunds reverse revenue, and a card dispute lands after launch. In 2026, the safest starting point is still to map responsibilities before you compare feature lists.