Quick Answer

Choose based on ownership: a Merchant of Record is the party that takes legal and operational responsibility around a sale, not just payment processing. For platform teams, the real call is whether to run that burden in house, outsource it, or split it by market or product line. Verify the boundary in the order form, MSA, or service schedule, and define one authoritative record for disputes, tax evidence, and reconciliation before launch.

Merchant of record liability starts with ownership#

For platform teams, what is merchant of record is not a vocabulary quiz. It is the decision about who stands behind the sale when money moves, taxes attach, refunds reverse revenue, and a card dispute lands after launch. In 2026, the safest starting point is still to map responsibilities before you compare feature lists.

- Treat the label as a responsibility map, not proof that liability vanished.

- Read the order form, MSA, tax schedule, and dispute workflow together before launch.

- Choose one authoritative record for orders, tax evidence, refunds, and chargebacks.

A practical definition here: if the party is standing behind the transaction layer, not only the card rail, it belongs in your MoR review. If you want a baseline definition first, Stripe's merchant-of-record overview is a useful starting point, then pair it with ASC 606 for Platforms: How to Recognize Revenue When You're the Merchant of Record before finance signs off.

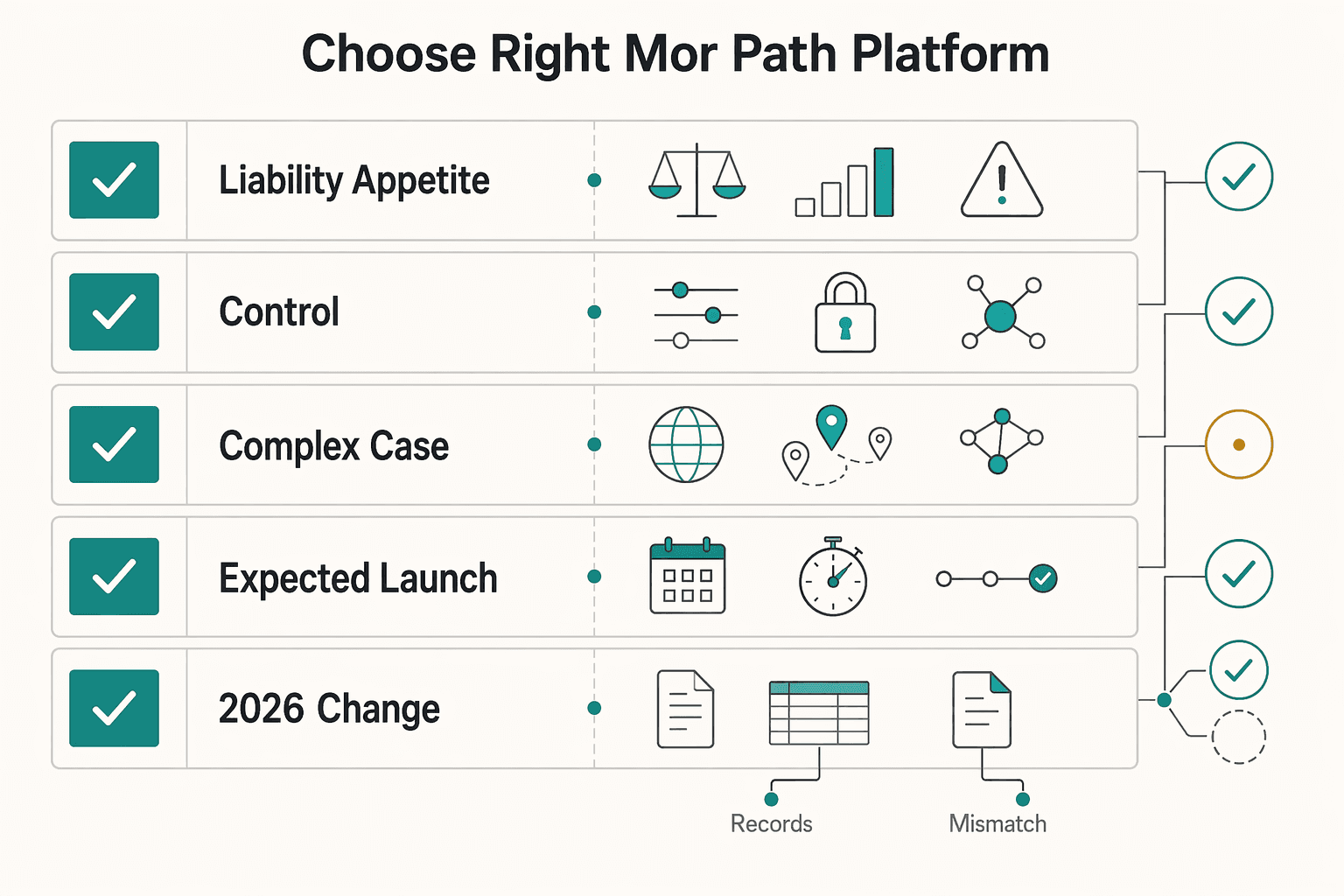

How to choose the right MoR path for your platform#

Once you treat this as an ownership decision, the screening criteria get much clearer. Score each path on liability appetite, control readiness, cross-border complexity, and launch timing before you compare vendors or architecture. If your team cannot reliably run tax, dispute, and compliance processes across the markets you want to enter, lean toward a model that shifts more operating burden and make sure the contract language is explicit enough to survive live operations.

| Criterion | What to assess | Checkpoint |

|---|---|---|

| Liability appetite | The legal and financial load your team is willing to carry when something goes wrong | Confirm in writing who accepts customer payments, calculates and remits taxes, handles chargebacks, and takes legal responsibility |

| Internal control readiness | Whether finance, risk, support, and engineering can operate review and evidence-retention processes without heroics | Look for named owners, documented review steps, and records you can produce during an audit, dispute review, or partner escalation |

| Cross-border tax and payments complexity | Multiple countries, local customer expectations, and different tax treatments | Favor a path that already handles those variations instead of assuming your domestic setup will stretch cleanly |

| Expected launch timeline | Whether the contract boundary is explicit enough to survive live operations | Verify who is the legal seller, who remits sales tax or VAT, who handles refunds and chargebacks, and which export or ledger is the audit record |

| 2026 change pace | How quickly your team can adapt when country coverage, tax rules, or provider terms change | Choose the model whose owners can still update contracts, tax logic, and support playbooks without manual scramble |

Start with contractual ownership#

We use one blunt test: can your team point to the exact clause naming the legal seller, the tax operator, the refund owner, and the dispute owner? If not, the liability boundary is still open. That is true whether the contract says Merchant of Record, processor, payfac, managed payments, or something more creative.

- Who appears as the seller on receipts, invoices, and customer-facing terms.

- Who calculates, collects, files, and remits indirect tax in each market.

- Who handles refund policy exceptions, chargeback evidence, and deadline management.

- Which export or ledger becomes the audit record when systems disagree.

Map the operating record#

MoR selection breaks most often when finance books from one dataset and product teams troubleshoot from another. Decide whether the provider statement, your internal ledger, or a reconciled warehouse table wins when records differ. If that call is not made before launch, every dispute and tax exception becomes a mini forensic project.

For EU consumer digital sales, a current VAT One Stop Shop review belongs in this step because registration, filing, and evidence questions can stay with you even when checkout looks outsourced. If you want a deeper conceptual pass first, read What is a Merchant of Record (MoR) and How Does It Work?.

- Red flag: the provider demo is detailed, but the order form is vague on seller, refund, or tax ownership.

- Red flag: support cannot explain whose name the buyer sees on the statement or invoice.

- Red flag: finance and engineering already rely on different datasets for refunds or disputes.

Merchant of Record vs PSP vs payfac for platform liability#

Start with scope, not branding. Stripe's processor-versus-payfac explanation is useful because it treats processor and payfac as separate provider models. That matters because those labels still do not answer who owns tax, customer billing terms, or post-transaction evidence in your stack.

| Check | Merchant of Record | PSP | Payfac |

|---|---|---|---|

| Plain description | Model to evaluate when transaction responsibilities matter alongside payment processing | Payment provider category used to accept and process payments | Distinct payment provider category from processors, per Stripe |

| Legal seller status | Do not infer from label alone. Verify the order form and MSA | Not established by label alone. Verify merchant agreement | Not established by label alone. Verify program terms |

| Primary 2026 review question | Does the contract name the seller and dispute owner clearly enough to operate under pressure? | Can your team run merchant obligations itself if the PSP only handles processing? | Who owns the program rules, notices, and merchant obligations when the payfac structure is under stress? |

| Tax scope | Verify who calculates, collects, files, and remits | Must be mapped explicitly. Label alone does not answer it | Must be mapped explicitly. Label alone does not answer it |

| Compliance burden | Depends on what stays with you versus the provider | Depends on your retained scope and controls | Depends on program structure and retained scope |

| Cross-border payments | Provider-specific market coverage. Verify supported countries and flows | Provider-specific | Provider-specific |

| Checkout localization | Verify product support in docs and contracts | Verify product docs | Verify product docs |

| Digital wallets | Wallet support is provider-specific | Provider-specific | Provider-specific |

| Card networks | Check who receives operational notices and dispute deadlines | Check acquiring path and notice flow | Check program docs and notice flow |

| Primary record to reconcile | Name the provider export or statement that finance will treat as authoritative | Make your internal ledger primary, with processor reports as support | Name the program ledger or export that prevails when records conflict |

Where MoR starts#

The MoR model is the right path when you want one commercial relationship to cover the transaction layer, not only card acceptance. That usually means the provider is closer to the customer-facing sale, tax handling, and dispute administration than a basic processor integration. The operational question is whether those responsibilities are explicit enough to stand up to refunds, disputes, and audit requests.

Start your review with documents, not only API docs. Ask for the exact clause or schedule that covers refunds, chargeback handling, tax records, and evidence retention. A common failure mode is finance booking from a provider statement while engineering treats webhook events as the truth, then discovering they disagree on refund state or dispute timing.

Where PSP and payfac still leave work with you#

PSP and payfac models can still be the right answer. They just require more discipline about retained responsibilities. If you stay merchant of record yourself, document who owns notices, reserve impacts, refund policy exceptions, and evidence retention before launch. Otherwise the platform will discover the true boundary during its first exception queue.

- Name a ledger owner for authorizations, captures, refunds, and disputes.

- Decide who receives card-network or processor notices and who answers them.

- Keep your tax evidence repository and provider exports tied back to the same order ID.

Before you sign anything, make one practical decision: choose the primary record for disputes, tax, and audit evidence. If the provider is contractually carrying a given obligation, make the named provider statement or export the finance record and keep your internal event log as supporting trace. If you are carrying the obligation, flip that. Your internal ledger is primary, and provider reports are evidence, not truth. For a deeper build-versus-buy frame, read What is a Merchant of Record (MoR)? The Platform Builder's Complete Guide.

Option 1 Be your own MoR#

This is the control-heavy choice, and it only makes sense if your finance and compliance teams are already built for it. If you choose to be your own Merchant of Record, assume you are keeping the end-to-end transaction burden, not just the checkout surface. A PSP can still process payments, but the merchant responsibility stays with your entity unless the contract clearly says otherwise.

Best fit#

Use this when your finance, tax, and risk operations are already mature enough to support the product you want to ship. The upside is product control: you keep pricing logic, support policy, revenue treatment, and checkout changes on your own timeline. You also keep direct visibility into the operational evidence behind every sale.

Control costs you keep#

The hidden cost is ongoing operations, not initial engineering. You own the monthly close questions, refund edge cases, audit requests, and country-by-country tax follow-up that an outsourced model is designed to absorb. We usually see this model work best when reconciliation is already boring, not heroic.

- Read the PSP merchant agreement and service terms and confirm they cover processing only unless the contract explicitly says more.

- Keep your internal ledger authoritative for transaction state, refunds, disputes, and tax evidence.

- Rehearse refund, dispute, and tax exception escalation before launch instead of treating it as future ops work.

The common failure mode is choosing this path for control while underestimating the monthly operating load. If your team cannot already reconcile payment events to refunds, chargebacks, and tax records without stitching together dashboards and CSVs by hand, do not pick this model yet.

- Wait if tax ownership changes every time you discuss a new market.

- Wait if support cannot tell the buyer which entity sold to them.

- Wait if reserve, refund, and dispute reporting still live in separate spreadsheets.

For a step-by-step procurement view, see How to Choose a Merchant of Record Partner for Platform Teams.

Option 2 Use a full-service outsourced MoR#

If your priority is entering new countries quickly without building tax and dispute operations first, this is usually the stronger choice. A full-service outsourced Merchant of Record can take on a wider slice of the daily work around cross-border payments, refunds, chargebacks, tax handling, and payment-related compliance.

| Check | What to verify | Reason |

|---|---|---|

| Responsibility boundaries by jurisdiction | Who handles refunds, chargebacks, tax collection, tax remittance, and compliance obligations in each market you plan to enter | Do not assume the same handoff applies everywhere |

| Coverage and localization scope | The country list, supported payment methods, currencies, and what checkout localization includes in the product you are buying | If you cannot verify coverage before launch, do not treat the provider as a complete liability transfer |

| Evidence and reporting | Sample exports or reporting views that tie your order ID to the provider transaction ID, refund events, dispute status, and tax records | Finance can reconcile without manual stitching |

| 2026 rollout proof pack | The exact fields, sample statements, and support escalation path you will use on day one | A 2026 launch still fails if the contract is broad but the data handoff is vague |

Best fit for speed#

This route fits teams that need faster multi-country launch and do not want to build tax and dispute operations first. Providers such as Paddle and FastSpring position MoR as a way to offload more operational work; the operator test is whether the contract and reporting really back that up. The upside is speed and fewer moving parts inside your own team.

The downside is reduced control. Some checkout behavior, customer-facing policies, and edge-case handling sit inside the provider's product and legal structure rather than your own. That can be a good trade if speed matters more than deep customization.

Contract and reporting checks#

An outsourced MoR is only as real as the paper trail. Ask for sample exports, refund status fields, dispute evidence views, and tax records before launch. If the provider cannot show how your order ID maps to its transaction and adjustment records, finance will rebuild the truth manually. For a 2026 EU or UK rollout, also verify how the provider handles indirect-tax evidence and buyer-location records.

- Require a country-by-country statement of who handles refunds, chargebacks, tax collection, tax remittance, and support escalations.

- Ask what checkout localization includes in the product you are actually buying, not only in marketing copy.

- Make sure the finance export ties your order ID to transaction IDs, adjustments, disputes, and tax references.

Ask for evidence before signing, not after go-live. That includes sample statements, reserve reporting, dispute timelines, and data export access after termination.

- Evidence of how statement descriptors, receipts, and invoices reflect the selling entity.

- Evidence of who receives dispute notices and who must submit documentation.

- Evidence of how tax references and buyer-location records appear in reporting.

We covered the marketplace angle separately in Stripe Connect vs Merchant of Record for Marketplace Liability Decisions.

Option 3 Use a hybrid MoR model by market or product line#

If a fully outsourced setup feels too blunt, a hybrid model is often the practical middle ground. In 2026, this is frequently the most realistic answer for platforms with stable domestic flows and newer international routes where tax remittance, disputes, and compliance would otherwise slow launch.

| Item | What to document | Why |

|---|---|---|

| In-house vs MoR split | What stays in house and what moves to an MoR by market, entity, or product line | The split should be deliberate, not accidental |

| Ownership by segment | Who owns the customer relationship and transaction layer in each segment | Keep those roles explicit so teams are not guessing later |

| Winning report or ledger | Which report or ledger wins when systems disagree | Hybrid models create more than one operational surface, so reconciliation rules need to be written down |

Best fit for uneven risk#

Hybrid works when your risk is uneven. You may keep a stable domestic product in house while routing newer consumer digital sales or experimental markets through an outsourced MoR. The appeal is precision: you are not choosing control or speed once, you are assigning each by segment.

The tradeoff is coordination. A hybrid model only works if the boundary is explicit for each segment: which entity sells, which provider handles the payment and legal transaction layer, who owns tax and dispute operations, and which record finance treats as authoritative.

Hybrid control map#

The model only works when the split is written down by segment, entity, and ledger. Support, finance, and engineering should be able to answer the same three questions for every market: who sells, who refunds, and which record wins.

| Segment example | Typical trigger | What to document | Record that wins |

|---|---|---|---|

| US domestic software / USD | You already run tax and support internally | Your entity as seller, PSP scope, refund owner, and ledger owner | Internal ledger linked to processor IDs |

| EU B2C digital sales / EUR | VAT collection and buyer-location evidence add overhead | Whether the provider or your entity handles VAT collection, OSS reporting, and disputes | Named provider export plus your order mapping |

| UK subscriptions / GBP | Separate tax, refund, and support processes can diverge | Legal seller, tax workflow, support handoff, and dispute deadlines | Contract-named MoR report or internal ledger, but choose one |

| New higher-risk markets / local methods | Localization and exception handling expand quickly | Country coverage, payment method support, escalation owner, and reserve impacts | Route-specific reconciliation file defined before launch |

- Document the segment split by market, entity, or product line.

- Match support scripts and buyer disclosures to the legal seller in each segment.

- Define one escalation path and one winning ledger for each route before launch.

The common failure mode is drifting into a hybrid model accidentally, one contract or one market at a time, without updating ownership maps. This pairs well with ASC 606 Principal vs Agent Decisions for Merchant-of-Record Platforms.

Bottom line for platform teams#

The bottom line is simple: choose the model your team can actually operate when a sale is refunded, taxed, disputed, or audited. For a 2026 launch, we would rather see a slower go-live with a clean ownership map than a fast launch built on implied responsibilities.

- Read the legal documents with finance, product, and support in the same room.

- Pick one authoritative record and test a sample reconciliation before launch.

- Only then compare launch speed against the control you are giving up or keeping.

If you want a budgeting angle next, use the payment fee comparison. If you want a program-specific review, Talk to Gruv.

Frequently Asked Questions

What should a 2026 MoR contract review include?

Review the named legal seller, tax collection and remittance scope, refund and chargeback ownership, reporting access, evidence retention, and what happens to data exports and customer support obligations if the relationship ends. If any of that is implied rather than written, the liability boundary is still open.

Does a Merchant of Record remove all platform liability?

No. An MoR can take defined transaction responsibilities, but your platform can still keep product promises, support workflows, data retention duties, revenue recognition decisions, and any obligations the contract leaves with your entity.

When is a PSP enough for a platform?

A PSP is usually enough when your company is prepared to remain the merchant, manage tax and dispute operations internally, and use the processor primarily for payment acceptance and settlement. If you still need someone else to absorb more of the transaction burden, a PSP alone is usually too narrow.

How should finance and engineering choose the source of truth?

Choose it before launch. If the provider contract carries the obligation, the provider statement or export should normally be the finance record and your internal event log should support it. If your company carries the obligation, flip that rule and make your own ledger primary.

Do cross-border digital sales still need tax mapping in 2026?

Yes. In 2026 you still need to map seller identity, indirect-tax registration and filing responsibility, evidence requirements, and dispute handling by market. A localized checkout or outsourced payment flow does not remove that review by itself.

Can you mix MoR and non-MoR flows inside one platform?

Yes, if the split is deliberate. Document the selling entity, refund owner, support handoff, and winning ledger for each segment so teams do not operate from different assumptions.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- consumerfinance.gov/ask-cfpb/how-do-i-dispute-a-charge-on-my-cre...trusted

- occ.treas.gov/publications-and-resources/publications/comp...trusted

- oecd.org/tax/consumption/role-of-digital-platforms-in...trusted

- oecd.org/en/publications/international-vat-gst-guidel...trusted

- stripe.com/resources/more/merchant-of-recordtrusted

- stripe.com/resources/more/payment-processor-vs-payment-...trusted

- vat-one-stop-shop.ec.europa.eu/index_entrusted

- vat-one-stop-shop.ec.europa.eu/one-stop-shop_entrusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

What is a Merchant of Record (MoR) and How Does It Work?

**Payment chaos drains margin through fee creep, payout uncertainty, and dispute-handling overhead, so build a risk-first get paid system before you optimize growth.**

Merchant of Record for Platforms and the Ownership Decisions That Matter

If you are looking for a **merchant of record for platforms**, the real question is not what MoR means. It is whether handing off enough payment, compliance, and risk work will help you move faster without creating new problems for product, finance, and engineering later.

ASC 606 Revenue Recognition for Merchant of Record Platforms

If you run a Merchant of Record flow, cash movement is not your revenue policy. Under ASC 606, the hard part is that customer payment, processor settlement, and the point when revenue is actually earned can sit on different dates and in different records.