Quick Answer

Choose based on ownership, not interface: in stripe connect vs merchant of record, Connect usually means more control with more internal responsibility, while a Merchant of Record path is evaluated to shift more transaction burden outward. Use one checkpoint first: confirm who is named for tax notices, disputes, refunds, and buyer support in signed documents and buyer-facing artifacts. If that owner is unclear, your team is not ready to compare costs or launch scope.

How to choose between Stripe Connect and a Merchant of Record on liability ownership, not checkout features#

The core choice in stripe connect vs merchant of record is not checkout UX or payout speed. It is who carries the legal and operational burden when a transaction goes wrong, when tax obligations expand, or when your marketplace starts selling across more regions.

That distinction matters because payment acceptance is only part of the job. Stripe's own merchant-of-record material describes digital commerce as sitting on "a complex web of financial processes, legal obligations, and regulatory requirements" behind every purchase. A merchant of record is a specialized entity used to manage those responsibilities. Some provider descriptions go further and describe it as the legal entity responsible for the transaction, including payment processing, tax compliance, fraud prevention, chargebacks, and regulatory obligations.

Stripe Connect sits on a different part of the stack. Connect is Stripe's platform and marketplace product for onboarding, embedded components, and payouts. Stripe also positions it as tooling that can reduce how much you need to staff for fraud, tax forms, risk, and onboarding compliance. Useful, yes, but that is not the same as saying liability has been outsourced. That is the first checkpoint to keep straight.

If you are building marketplaces or embedded payments, the practical question is simple: where do you want responsibility to live before scale makes the answer expensive? For some teams, the right call is to keep more control and accept the extra ownership that comes with a Connect-led setup. For others, the better move is to evaluate a merchant-of-record path because broader tax handling and reduced operational exposure matter more than owning every layer.

A good early test is to force the decision into one sentence before product and engineering get too far ahead. "Are we the party owning transaction liability, or is a Merchant of Record doing that?" If your team cannot answer that cleanly, you are not comparing products yet. You are still deciding your liability architecture.

One more nuance matters for the rest of this guide. Merchant of record and seller of record are not interchangeable labels. Stripe's own explanation says they represent different responsibilities and potential liabilities, which means finance, legal, and payments ops should not treat them as wording choices. That becomes more important as ecommerce-driven retail sales are projected in one cited forecast to reach $3.8 trillion by 2027. As volume and geographies expand, tax, disputes, and support ownership usually needs to be explicit.

The rest of this guide is built for that decision, not vendor slogans. The goal is to help founders, product, finance, and engineering leaders choose who owns what, verify the gaps, and avoid discovering after launch that no one actually agreed on tax, chargebacks, or customer issue handling.

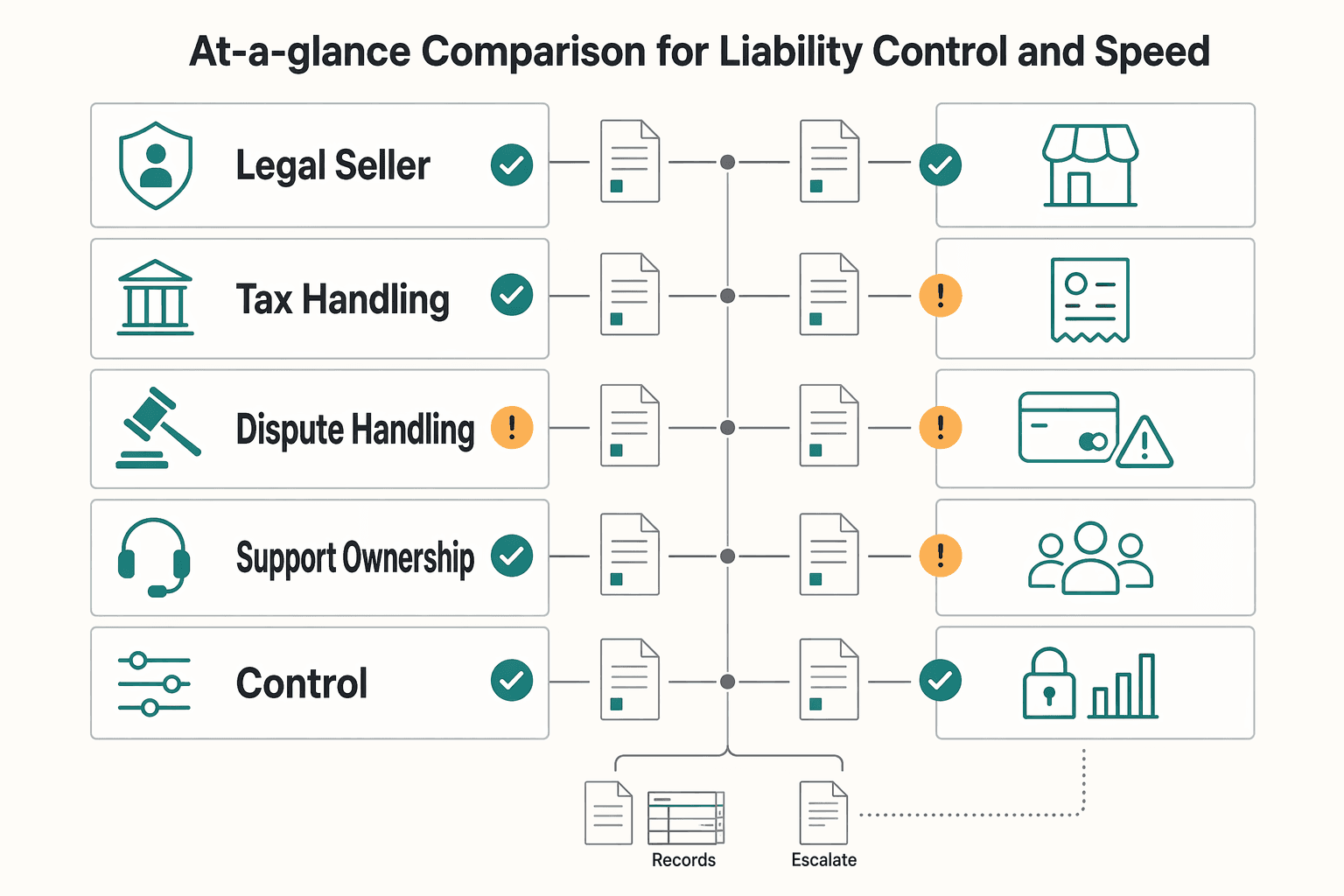

At-a-glance comparison for liability, control, and speed#

If you want more product and integration control, a Connect-led path is usually the better fit. If you want faster operational coverage by shifting more responsibility outward, a merchant-of-record path is usually what teams evaluate. Treat both as directional until your actual contracts and eligibility terms are confirmed.

Stripe's payments material frames payments as a network with defined participants and processing flow. For decision-making, use one practical test first: when a transaction issue happens, who is named, who receives it, and who must act?

| Criteria | Stripe Connect-led ownership | Stripe Managed Payments ownership under a merchant-of-record model |

|---|---|---|

| Legal seller role | Not confirmed as a universal rule in the provided excerpts. Verify whether your platform or connected accounts are the contracting seller in your setup and documents. | Not confirmed in the provided excerpts as a blanket rule. This model can imply more centralized transaction ownership, but agreement terms still decide it. |

| Tax handling | The excerpts do not support a definitive default owner for registration, collection, filing, or notice handling. Map these responsibilities explicitly between platform and connected accounts. | The excerpts do not confirm exact tax scope, jurisdiction coverage, or exclusions. Verify coverage and any residual platform obligations. |

| Dispute handling | Do not assume tooling means ownership transfer. Confirm who receives notices, submits evidence, and carries financial exposure. | The excerpts do not confirm full dispute boundaries. Confirm escalation paths for refunds, customer communication, and evidence handling. |

| Support ownership | Usually needs clear internal routing across buyer, seller, and platform support flows. Confirm first-response and escalation ownership. | Often considered for broader operational coverage, but the excerpts do not prove full support outsourcing. Confirm what remains with your team. |

| Integration control | More direct control over onboarding, payment flows, payout logic, and product experience, with more operating burden. | Typically less direct control if responsibility is more centralized, with potential speed gains if terms and eligibility fit. |

| Responsibility when failures happen | Accountability may sit with platform, connected accounts, or both, depending on implementation and agreements. | The model is often evaluated to move more accountability outward, but not necessarily all of it. Keep a written owner-by-process matrix. |

| Known unknowns | Exact commercial terms are not confirmed in the Stripe, Dodo Payments, Reddit, and r/SaaS excerpts referenced for this article. | Exact pricing, eligibility constraints, supported business types, and country coverage are also not confirmed from those excerpts. |

| Practical read | More control and configuration freedom, with more operational burden. | More outsourcing and potentially faster operational coverage, with less direct control and stricter dependency on confirmed terms. |

Use documents, not product labels, to settle ownership. Before launch, keep a short evidence pack with signed agreements, a platform/connected-account/MoR responsibility matrix, and named owners for disputes, refunds, tax notices, and buyer support.

What changes when you choose the liability owner#

The biggest change is accountability: you are deciding which entity is expected to carry key transaction responsibilities and liabilities when something breaks. Stripe's own material states that merchant of record and seller of record are different roles with different liability implications, so this is an operating-model decision, not a feature toggle.

In practical terms, do not infer ownership from product naming alone. Stripe also has Connect documentation specifically on understanding merchant of record, which is a signal to verify responsibility explicitly in your Connect structure and agreements.

| Area | What changes | What to verify before launch |

|---|---|---|

| Sales tax, VAT, GST | Ownership can materially shift with the liability model you choose. | Who is named to register, calculate, collect, file, and respond to notices in each jurisdiction. |

| Chargebacks and disputes | First-response and loss-handling responsibility may sit in different places. | Who receives notices, who submits evidence, and which balance absorbs losses. |

| Customer-facing merchant identity | Legal and operational ownership must match what buyers and sellers see. | Which entity is shown in terms, receipts, checkout disclosures, and support routing. |

| Internal team load | Work may move between internal execution and partner oversight. | Named owners, escalation path, and sign-off across product, ops, finance, and support. |

Run one tax-notice scenario and one chargeback scenario end to end before go-live. If your team cannot point to the contract language, receipt entity, notice recipient, and dispute flow, liability ownership is still unresolved.

Finance follow-up is mandatory, not optional cleanup. Start principal-versus-agent and ASC 606 review as soon as you narrow the liability model, and do not infer revenue presentation from checkout UX or payout mechanics alone. See principal vs agent revenue recognition and ASC 606 for Platforms: How to Recognize Revenue When You're the Merchant of Record.

The non-obvious cost picture beyond processor fees#

If you cannot staff ongoing tax and dispute operations, lower headline fees can be misleading. This decision is not just processor pricing; it is operating design.

The direct fee math already branches quickly. Stripe's standard pricing page lists 2.9% + 30¢ per successful domestic card transaction, plus 0.5% for manually entered cards, 1.5% for international cards, and 1% when currency conversion is required. In Connect, one model has Stripe set and collect processing fees from users, and the platform can avoid listed additional account, payout-volume, tax-reporting, and per-payout fees. In the "you handle pricing" model, Stripe lists $2 per monthly active account and 0.25% + 25¢ per payout sent.

Managed Payments is not a single clean replacement line item. Stripe's support material describes a 3.5% fee per successful transaction, in addition to standard Stripe processing fees, and also notes country and payment-method variation plus additional charges for subscription payments. If you run recurring revenue, model that separately before assuming this route is simpler or cheaper.

| Cost area | Connect-led cost pattern | Merchant-of-record / Managed Payments cost pattern | What to verify before modeling total cost |

|---|---|---|---|

| Payment processing | Standard Stripe fees apply; Connect costs vary by billing model. | Managed Payments adds 3.5% per successful transaction on top of standard processing, with country/method variation. | Country, payment method mix, card mix, FX exposure, subscription treatment. |

| Tax operations | More responsibility can remain with platform and connected accounts. | More transaction-level burden may be centralized externally, but oversight still stays in-house. | Who receives notices, who responds, and what evidence is available. |

| Dispute operations | Intake, evidence, and loss handling can be split across parties. | Some burden may move outward, but handoffs still need clear ownership. | Who gets first notice, who submits evidence, and SLA expectations. |

| Support operations | Buyer and seller issues can bounce if ownership is unclear. | Merchant identity can be more centralized, but routing still needs definition. | Receipt wording, checkout disclosures, refund path, escalation contacts. |

| Internal team load | More day-to-day coordination across finance, ops, support, and product. | More vendor-management overhead, potentially less daily execution if setup is clean. | Named owners, sign-off flow, monthly exception review. |

Hidden costs usually show up as rework and delay, not a neat fee line. If ownership between platform and connected accounts is unclear, chargeback handling and transaction reconstruction can consume support and finance time repeatedly. Unresolved chargebacks create a second drag: notices land with the wrong team, evidence is late, and reconciliation slows.

You will also see pricing concerns in Reddit and r/SaaS threads, especially for Stripe Managed Payments. Use those threads as diligence prompts, not pricing truth: the provided excerpts do not validate forum-quoted pricing beyond Stripe's own support article.

A practical rule: if you cannot name owners for tax operations, dispute operations, and support escalations, treat "lower fees" as incomplete math. Before you compare options, get four items: the exact Connect billing model, a country-specific fee sheet, subscription-pricing treatment if relevant, and a sample dispute and tax-notice routing path.

Implementation checkpoints that prevent expensive rewrites#

Expensive rewrites usually happen when teams build checkout first and sort out ownership later. Use this order instead: decide liability owner, design checkout and payout flows around that owner, then implement reconciliation and auditable records.

Payments operations are ongoing workflows, not a one-time integration. They include onboarding, disputes, refunds, reconciliation, and incident response, and those workflows involve edge cases, policy constraints, and cross-system coordination. If ownership is unclear at design time, rework shows up later in support, finance, and incident handling.

| Checkpoint | Connect-led path | Merchant-of-record path | Required launch artifact |

|---|---|---|---|

| Ownership model | Define internal responsibility boundaries for platform and connected accounts. | Confirm provider responsibility assumptions in writing. | Owner-by-process matrix |

| Checkout and payout design | Align buyer and seller flows with your documented ownership model. | Align buyer-facing flow and internal operations with documented provider handoffs. | Approved journey map |

| Exception handling | Assign clear escalation owners for disputes, refunds, and incidents. | Define where provider handling stops and internal handling starts. | Exception escalation map |

| Reconciliation and audit trail | Ensure transactions and status changes are traceable across systems. | Keep the same traceability standard even when a provider handles more front-line activity. | Finance and ops evidence pack |

Stripe Connect checkpoints#

For a Connect path, treat connected-account onboarding as an operations checkpoint, not just an API task. Define what "onboarded" means for your marketplace, which account data your teams need, and which events change payment or payout status.

Next, document responsibility boundaries by workflow so support, finance, and operations are using the same ownership model. Then assign one escalation owner per exception type so routing is clear when a dispute, refund, or incident occurs.

Merchant of Record checkpoints#

For a merchant-of-record path, avoid assumption-led design. Keep eligibility and product coverage as open items until they are confirmed in writing.

Be explicit about operational handoffs. Even if a provider takes more transaction-level responsibility, your team still needs controls for reconciliation, incident response, and customer communication.

If your model includes recurring, usage-based, or sales-negotiated billing, confirm how those billing patterns map to your operating model before go-live.

The evidence pack to require before go-live#

Do not launch on verbal alignment alone. Require:

| Artifact | What it includes |

|---|---|

| Owner-by-process matrix | Onboarding, disputes, refunds, reconciliation, incident response, support, and payout issues |

| Exception escalation map | First responder, escalation path, and final system of record |

| Finance and ops evidence pack | Sample transaction records, transaction-to-ledger mapping, and a traceable log of status changes and approvals |

Include PCI scope in the same launch gate. Any business that handles card payments must maintain PCI compliance, and the effort can range from a short questionnaire to an enterprise-level security program.

If written ownership, written coverage assumptions, and auditable workflows are not in place before build, pause and close those gaps first.

Failure modes competitors gloss over#

The biggest failures in this decision are ownership failures, not coding failures. If you have not verified who is acting as Merchant of Record in your actual configuration, contracts, and buyer-facing flow, treat downstream support, tax, and dispute decisions as unproven.

The first trap is binary thinking about Stripe. Teams often assume Stripe is always, or never, the merchant-of-record provider, then design operations around that assumption. Use a concrete check instead: signed documents, receipt language, buyer-facing support contact, refund path, and your owner-by-process matrix should all point to the same owner. If they do not, your architecture is still ambiguous.

Mixed ownership is where ambiguity turns expensive. A platform can own product experience while connected accounts own parts of transaction responsibility, but only with explicit handoffs. If support, disputes, and reconciliation each land on different teams without a clear written boundary, cases will bounce and escalations will pile up.

| Failure mode | What to verify now | What breaks if you skip it |

|---|---|---|

| Assuming Stripe is or is not the merchant-of-record provider | Written confirmation of the commercial model, plus receipt, refund, and support-contact examples | Wrong tax, support, and compliance ownership from day one |

| Platform and connected accounts split duties informally | One named owner per process for chargebacks, refunds, customer communication, and reconciliation | Cases bounce between teams, deadlines get missed, buyers get conflicting answers |

| Accepting performance claims without method | Ask how claims were measured, for which cohort, and whether methodology is published | Vendor selection based on confidence signals instead of operational proof |

| Approving architecture without written owners | Signed matrix for tax, disputes, and support, with backups and system of record | Launch with unresolved liability and no clean escalation path |

This research set also has evidence-quality limits. A reader-supported publication dated Aug 24, 2025 can be useful context, but it is not formal methodology documentation by itself. The captured Quora page is unreliable on its face, so it should not be used to resolve liability ownership.

A practical filter is to evaluate claims using payment-processing RFP criteria: security and compliance, customer support and account management, pricing structure, and reliability and uptime. Those categories force the conversation from demo flow to operating reality.

Red flags that mean you are not decision-ready#

| Red flag | Artifacts or proof named |

|---|---|

| Your team cannot name, in writing, who owns tax notices, disputes, and buyer support | Tax notices, disputes, and buyer support |

| The buyer receipt, refund policy, and support inbox point to different entities | Buyer receipt, refund policy, and support inbox |

| Someone says "the provider handles that" but cannot show the exact document, handoff point, or internal record | The exact document, handoff point, or internal record |

If any one of these is true, pause. Ownership uncertainty is a build blocker that usually reappears later as compliance confusion, finance rework, or missed dispute deadlines.

Scenario-based recommendations for marketplace builders#

Use Stripe Connect when your priority is marketplace control over multi-party money movement. Use a merchant-of-record path when operational simplicity and liability outsourcing matter more, and treat Stripe Managed Payments as a candidate only after Stripe confirms support for your model.

Stripe's own payout guidance is direct: "If you're running a marketplace, use Stripe Connect." That aligns with scenarios where you need to take a platform fee, pay out sellers or service providers, and split payments across multiple seller accounts. If you are only selling your own products or services, a regular Stripe account can be enough.

| Your situation | Better fit | Why | Verify before build |

|---|---|---|---|

| You need platform fees, payouts, and payment splits across multiple seller accounts | Stripe Connect | Built for marketplace-style, multi-party money movement | Written owner-by-process matrix for disputes, tax notices, refunds, and buyer support |

| You want less internal operational handling and more outsourced responsibility | Merchant of Record | Better direction when simplicity matters more than deep control | Written confirmation of eligibility, product scope, commercial terms, and buyer-facing handoff points |

| You run both embedded payments and marketplace payouts | Split only by segment | Can work if ownership boundaries stay explicit and auditable | Separate receipts, contracts, support inboxes, and reconciliation views by segment |

Mixed models are where teams usually create avoidable escalation risk. If one segment uses connected accounts and another uses a merchant-of-record provider, keep boundaries explicit in buyer-facing artifacts and internal records before launch.

Team maturity is the practical tie-breaker. Lean early-stage teams should usually bias toward operational simplicity, while teams with mature finance, support, and reconciliation capabilities can absorb Connect's ongoing complexity for added control.

For a step-by-step walkthrough, see How to Choose a Merchant of Record Partner for Platform Teams.

A decision checklist you can use this week#

Use this checklist before build kickoff: if these four artifacts are not written and owned, delay launch.

| Checklist item | What to include | Key detail |

|---|---|---|

| Write the liability sentence first | "We are platform-led via Stripe Connect" or "We outsource merchant liability to a Merchant of Record for eligible sellers." | Verify that the same sentence matches checkout copy, receipts, refund policy, seller onboarding, and support macros |

| Build a responsibility matrix with named owners | Sales tax, VAT, GST, chargebacks, and customer support | Assign a legal owner, day-to-day operator, escalation contact, and backup |

| Pressure-test the finance model before commitments | Pull in ASC 606 and principal-vs-agent stakeholders before pricing pages, contracts, or forecasts are locked | Connect: $2 per monthly active account and 0.25% + 25¢ per payout sent; Managed Payments: 3.5% per successful transaction in addition to standard processing fees such as 2.9% + 30¢ for domestic cards |

| Assemble the go-live evidence pack | Ownership matrix, escalation paths, a reconciliation plan for charges, payouts, refunds, disputes, and tax entries, plus an unresolved-unknowns list | Keep Stripe, Dodo Payments, and Reddit notes split into "verified" and "unverified" |

For related reading, see Stripe Atlas vs Firstbase.io for US Formation Without Compliance Surprises.

Conclusion#

The practical move in stripe connect vs merchant of record is to decide who owns the sale before you compare product knobs. Pick the liability architecture first, then choose the Stripe product path, checkout shape, and payout design that fit it.

That sounds simple, but it is where teams avoid the most cleanup. A Merchant of Record is the legal entity authorized to sell to customers and take the associated financial liabilities. In one Stripe-vs-MoR comparison, Stripe is framed as more flexibility with more responsibility. The merchant-of-record path is framed as less operational burden with a different pricing model. Those are not just feature differences. They are business model differences.

So the recommendation is straightforward. If your team wants tighter control over seller experience, payouts, and customer flow, and you can staff ownership for tax, compliance, fraud prevention, and customer-facing operations, choose the Connect route and document exactly what sits with the platform versus connected accounts. If you care more about outsourcing liability and reducing day-to-day operational burden, evaluate a merchant-of-record path where supported. But verify the exact product configuration, eligibility, and contract language before anyone assumes responsibility has moved.

The most important checkpoint is not technical. It is documentary. Before build or launch, your team should be able to produce a signed responsibility matrix that names owners for sales tax, VAT, GST, chargebacks, refunds, and customer support. Pair that with an escalation map and a reconciliation plan. If those documents are vague, your implementation is not ready, no matter how polished the checkout looks.

One failure mode is worth repeating: role confusion creates real cost. Stripe notes that confusion over payment entities can lead to inefficient setups, higher processing fees, and a greater risk of failed transactions. In practice, this can show up when support says one party owns refunds, finance books another party as the seller, and ops discovers too late that tax notices or disputes are landing in the wrong queue.

A clean close to this decision usually includes three things:

- Write one sentence stating your target model: platform-led ownership via Connect, or outsourced ownership via a Merchant of Record.

- Create a verified unknowns list for anything public materials do not settle yet, especially commercial terms, seller eligibility, and product coverage assumptions.

- Assemble a go-live evidence pack with the responsibility matrix, escalation paths, reconciliation plan, and finance sign-off items.

If you can leave this article with those artifacts in hand, you do not just have an opinion about Connect versus a merchant-of-record path. You have a decision your product, ops, and finance teams can execute with fewer surprises.

Frequently Asked Questions

What is the actual difference between Stripe Connect and a Merchant of Record for marketplaces?

The practical difference is responsibility allocation and how much operational burden is outsourced. From these sources, the exact owner of tax, disputes, refunds, and support is not fixed by product name alone; it depends on your Stripe configuration and contracts.

Is Stripe “not MoR,” or does Stripe Managed Payments count as a merchant-of-record option?

Stripe Connect by itself should not be treated as automatic merchant-of-record coverage. In this comparison, Managed Payments is a Stripe path to evaluate, but public snippets here do not prove liability transfer on their own. Verify your exact product configuration, seller eligibility, and contract language before teams operate as if responsibility moved.

Who handles tax, fraud, disputes, and support under each model?

These snippets do not assign a universal owner for every function. You need a written ownership matrix across contracts and operations so finance, support, and ops teams follow the same handoffs for customer communication, exceptions, and reconciliation.

When should a platform choose Connect-led ownership over MoR outsourcing?

Choose Connect-led ownership when you want tighter control and can staff the operational work that comes with it. The pricing page matters here: in the Connect model where you handle pricing, Stripe lists $2 per monthly active account plus 0.25% + 25¢ per payout sent. A monthly active account is one that receives payouts in that month. If owners for tax notices and disputes are still undefined, slow rollout until they are explicit.

What is still unknown from current public snippets about pricing, eligibility, and implementation constraints?

A lot of the commercial detail is still not decision-ready from public snippets alone. Managed Payments lists a 3.5% fee per successful transaction, and Stripe says that fee is in addition to standard processing fees such as 2.9% + 30¢ for domestic cards, but you still cannot infer an all-in rate without country, payment method, and product context. Stripe also notes that some local methods are only available to eligible sellers, and country-specific pricing pages can override listed payment-method examples like Klarna’s 2.99% to 5.99% range.

How does this decision affect ASC 606 and principal vs agent revenue recognition workstreams?

This grounding pack does not establish ASC 606 conclusions. Treat principal-versus-agent outcomes, fee presentation, and revenue recording policy as accounting questions that need finance review before launch decisions are finalized. For a deeper accounting lens, see ASC 606 for Merchant-of-Record Platforms: Principal vs Agent Revenue Recognition.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- albanyoregon.gov/mnt/html/citycouncil/bcc/archive/2025/cdc_20...trusted

- docs.stripe.com/connect/merchant-of-recordtrusted

- docs.stripe.com/global-payouts/pricingtrusted

- ellsworthmaine.gov/wp-content/uploads/2019/10/10212019-Regular-...trusted

- oecd.org/content/dam/oecd/en/publications/reports/201...trusted

- online.ogs.ny.gov/purchase/snt/awardnotes/7900823234MerchantRe...trusted

- sec.gov/Archives/edgar/data/1594805/0001594805260000...trusted

- stripe.com/connect/pricingtrusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Paddle vs. Stripe: A Comparison for SaaS Founders

**Paddle vs Stripe is a risk-ownership decision first, so choose the setup that keeps cashflow stable when tax, refunds, and disputes show up together.** If you are the CEO of a business-of-one, you are not just picking a checkout. You are deciding who carries the operational burden when things get messy.

ASC 606 Revenue Recognition for Merchant of Record Platforms

If you run a Merchant of Record flow, cash movement is not your revenue policy. Under ASC 606, the hard part is that customer payment, processor settlement, and the point when revenue is actually earned can sit on different dates and in different records.

ASC 606 Principal vs Agent Decisions for Merchant-of-Record Platforms

For merchant-of-record teams, the **ASC 606 principal vs agent merchant of record** call is a high-stakes judgment, not a presentation preference. It can move revenue from gross to net and raise the level of judgment finance, audit, and compliance teams need to defend.