Quick Answer

For most small SaaS teams, paddle vs stripe should be decided by risk ownership and operating capacity, not checkout polish. Paddle is often safer when you need lower weekly tax and dispute workload through a Merchant of Record model, while Stripe is stronger when you need deep control and can staff ongoing billing, tax, fraud, and dispute operations. Pick the setup your team can run reliably every week.

You need a payment stack that gets you paid on time not just a prettier checkout#

Paddle vs Stripe is a risk-ownership decision first, so choose the setup that keeps cashflow stable when tax, refunds, and disputes show up together. If you are the CEO of a business-of-one, you are not just picking a checkout. You are deciding who carries the operational burden when things get messy.

A Merchant of Record is the legal seller to the customer. In that model, the MoR carries core liabilities, including collecting tax and handling refunds and chargebacks. Paddle positions itself as an authorized reseller in this model.

Stripe supports multiple modes. Some Stripe setups can place Stripe in the merchant-of-record role, for example, Stripe Managed Payments. Other Stripe configurations can put merchant-of-record duties on your account, and in some Connect setups platforms can be responsible for covering losses.

You can finish this decision in one sitting if you produce three outputs:

- A risk-first framework for tax, disputes, and payout interruptions.

- A role-ownership map that names a real owner for each recurring task.

- A go or no-go checklist you can reuse for every new subscription management workflow.

| Decision area | What to decide now | Safe default when data is incomplete |

|---|---|---|

| Tax and VAT | Who registers, calculates, collects, files, and remits | Choose the model that reduces weekly compliance load until you have finance ops capacity |

| Chargebacks and disputes | Who gathers evidence, executes refunds, and owns escalation | Pick the path with fewer moving parts first |

| Merchant-of-record status | Which exact Stripe or Paddle product mode you will run | Do not assume Stripe is always or never MoR. Confirm per configuration |

| Subscription lifecycle management | How much billing logic you must customize now | Start simpler, then add modular control when your team can run it reliably |

If you do not have clear ownership for VAT and disputes, the work piles up fast and payment risk rises. If you lock in clearer ownership first, you protect cashflow and can layer in customization later.

Use this go or no-go gate before you commit:

- Go if you can name one accountable owner for tax, disputes, and loss handling.

- Go if your team can run the required controls every week, not just during launch.

- No-go if merchant-of-record ownership still feels ambiguous in your chosen configuration.

- No-go if you need assumptions to make the model work.

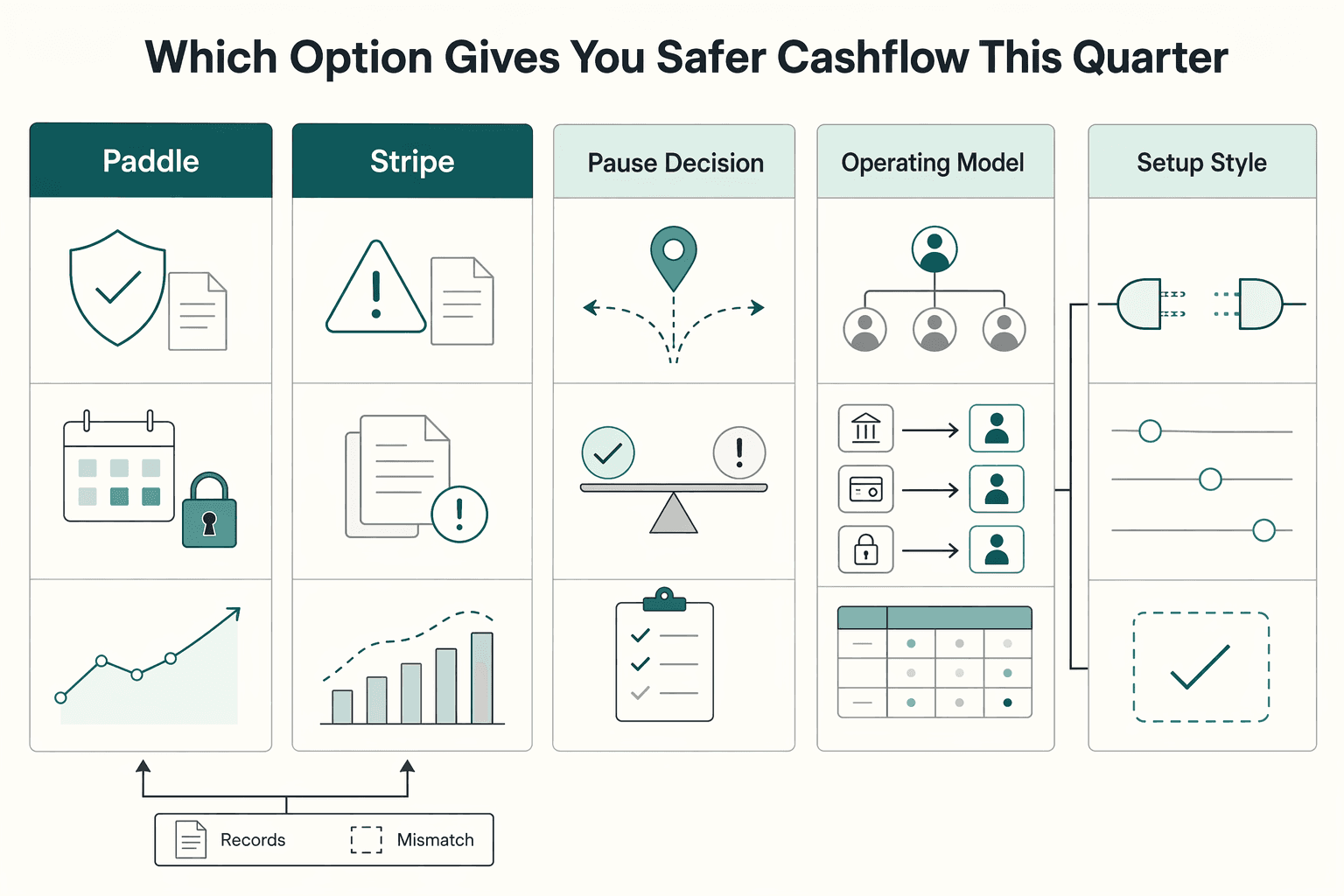

Which option gives you safer cashflow this quarter#

For this quarter, safer cashflow comes from choosing the model that removes the most weekly risk work from your team. Start with the comparison below, then decide based on who will actually run tax, disputes, and payout controls in real time.

| Decision | Use when |

|---|---|

| Paddle | You need lower compliance and dispute overhead right now. |

| Stripe | You can staff ongoing tax, fraud, and dispute operations for more control. |

| Pause the decision | Your MoR ownership still feels unclear in your exact configuration. |

| Criteria | Paddle | Stripe |

|---|---|---|

| Operating model | Authorized reseller model where Paddle acts as Merchant of Record (MoR) for supported sellers | Modular payment processing stack. In some setups, such as marketplace patterns, your platform takes MoR responsibility |

| Setup style | Centralized workflow for checkout, billing, and compliance-related tasks in supported flows | Composable products designed to run together or separately |

| Tax posture | MoR model carries core tax and compliance obligations in supported flow | Your team enables Stripe Tax to calculate and collect tax, then owns process design for registration and filing decisions, with support across 100+ countries |

| Dispute posture | MoR model carries core liability in supported flow and can reduce internal handling load | Your team manages disputes and refunds. Stripe Radar adds AI risk evaluation, custom rules, and granular risk scoring |

| Best fit pattern | Lean SaaS payments teams that want faster ownership transfer | Builder-heavy teams that want deeper control over subscription management and risk controls |

Merchant of Record means the legal seller to the customer, plus the party that carries key payment liabilities. That ownership line usually decides cashflow safety faster than any checkout-style debate.

Do not treat headline fee snippets as the whole cost picture. Include add-ons, dispute effort, and operator time before you choose.

Treat comparison posts from Chargeblast and UniBee as directional input, not proof. Use them to generate questions, then validate against your own transaction profile, support burden, and operating capacity.

Verdict for this quarter:

- Choose Paddle when you need lower compliance and dispute overhead right now.

- Choose Stripe when you can staff ongoing tax, fraud, and dispute operations for more control.

- Pause the decision if your MoR ownership still feels unclear in your exact configuration.

What changes when you choose Merchant of Record instead of a payment processor#

Choose Merchant of Record when you want liability transfer for covered payment and compliance tasks, and choose a payment processor when you want deeper control with explicit internal ownership. The practical difference is not philosophical. It decides who is on the hook when VAT questions, chargebacks, and disputes land in the same week.

A Merchant of Record (MoR) is the legal seller that carries payment and compliance responsibility. A payment processor facilitates transactions, but your business usually keeps legal and operational accountability for key workflows. Exact ownership depends on your contract terms and enabled product configuration. That difference usually determines who owns VAT, chargebacks, and disputes when pressure hits.

| Workstream | MoR pattern (Paddle model) | Payment processor pattern (Stripe Payments + Stripe Billing) |

|---|---|---|

| VAT and sales tax | Paddle acts as seller on record and handles collection and payment in its reseller model | Your team configures tax tooling, including Stripe Tax where enabled, and owns tax process decisions and controls |

| Chargebacks and disputes | For Paddle processed transactions, disputes are raised against Paddle | Your team runs dispute and refund operations and must maintain response playbooks |

| Subscription lifecycle management | More of the recurring billing lifecycle is handled in the provider's integrated flow | Stripe Billing supports recurring billing and subscription lifecycle management, with more internal rule and exception decisions |

| Fraud and risk operations | Can be more bundled into the provider operating model | Your team keeps more fraud and risk process ownership in Stripe Payments and related tooling |

Use this lightweight RACI checklist before launch:

- R runs the task day to day.

- A owns the outcome and signs off.

- C advises on edge cases.

- I gets status updates.

- For VAT, chargebacks, and disputes, assign one named person for each RACI role before you process live payments.

When enabled and where supported, Stripe Managed Payments can shift MoR responsibilities to Stripe for eligible businesses, but availability is not universal. Stripe Tax can calculate and collect tax across 100+ countries, yet your exact obligations still depend on your enabled setup and jurisdiction footprint.

Decision rule: pick MoR for faster operational relief today. Pick processor control only when your team can absorb the extra weekly decision load. If you want a quick next step, try the free invoice generator.

Where your real costs appear after month two#

Real cost shows up in add-ons and weekly operations, so evaluate total effort, not just headline processing fees. The cost you feel after month two is usually a mix of fees and operator time. Model both.

| Hidden cost source | Operational effect |

|---|---|

| Failed retries | Can trigger manual outreach and recovery work. |

| Chargebacks | Can create fee exposure and pull time from product work. |

| Unclear subscription lifecycle management rules | Can cause rework across support, billing, and reconciliation. |

Published pricing gives you a starting point, not a final answer. Paddle lists a pay-as-you-go fee of 5% + 50 cents per checkout transaction and says that plan has no migration, monthly, or hidden extras. Stripe lists 2.9% + 30 cents for successful domestic card transactions at base processing, then adds optional layers like Stripe Billing, Stripe Tax, and Stripe Radar.

| TCO line item | Paddle | Stripe |

|---|---|---|

| Headline processing | 5% + 50 cents per checkout transaction | 2.9% + 30 cents per successful domestic card transaction |

| Recurring billing layer | Confirm whether your subscription workflow needs extra tooling | Stripe Billing adds 0.7% of billing volume |

| Tax layer | Confirm tax workflow scope in your contract | Stripe Tax Basic adds 0.5% per transaction where you're registered to collect taxes; Tax Complete starts at $90 per month with a 1-year contract |

| Fraud tooling | Budget internal review time and support handling | Stripe Radar pricing includes 5 cents per screened transaction, with a higher tier listing 7 cents per screened transaction |

| Disputes overhead | Budget evidence prep and customer communication labor | Published dispute-management pricing includes $15 per dispute blocked, $29 per dispute resolved, and Smart Disputes at 30% of the disputed amount |

| Reconciliation labor | Budget monthly close and exception handling time | Budget monthly close and exception handling time plus add-on coordination |

The hidden costs usually show up in routine work, not launch week:

- Failed retries create manual outreach and recovery work.

- Chargebacks create fee exposure and pull time from product work.

- Unclear subscription lifecycle management rules create rework across support, billing, and reconciliation.

Month-two cost is not always "the checkout broke." It is often support chasing edge cases and finance closing late because billing rules were never nailed down.

If you choose Stripe for control, approve add-ons and assign owners before launch. If you need simpler forecasting this quarter, choose the model with fewer moving parts.

Who handles risk controls and compliance work every week#

Your payment system stays reliable only when you assign one accountable owner for each weekly control, and Paddle vs Stripe changes that ownership map. Fees matter, but ownership is what keeps you out of the ditch.

| Control area | Paddle model | Stripe model |

|---|---|---|

| VAT and tax compliance | In a Merchant of Record setup, Paddle carries tax-related risk for covered transactions, and your team tracks exceptions and reporting cadence | In standard Stripe setups, your team owns tax operations through Stripe Tax setup and ongoing compliance workflows; in Managed Payments, Stripe can act as merchant of record |

| Fraud monitoring | Set an internal reviewer for alerts and policy exceptions, then confirm provider-side responsibilities in your contract | Assign a fraud owner to tune Stripe Radar rules, review risk signals, and approve rule changes |

| Disputes handling | Name an internal owner for customer communication and evidence readiness, then verify formal liability and process terms | Your seller team counters claims with evidence, while issuers decide outcomes |

| Payout controls | Document payout timing terms and escalation contacts in your runbook | If you use Stripe Connect, set payout controls like delay_days only where your configuration allows it and where your account owns fraud and dispute liability |

| Billing continuity | Keep a single owner for plan changes and renewal QA | Use Stripe Billing runbooks for recurring payment changes and migration sequencing |

Small teams need minimum controls, not perfect controls:

- Set a policy gate for every new market. Do not launch until the VAT validation owner and approval owner both sign off.

- Set a fraud gate. No rule change ships without a rollback note and audit trace.

- Set a disputes gate. Define the evidence SLA, escalation owner, and final decision checkpoint.

- Set payout monitoring windows after go-live, because initial payouts can take longer in early live periods.

For migration readiness, run this mini-checklist:

- Complete data handoff mapping for customers, plans, and renewal dates.

- Protect billing continuity with anti-double-billing sequencing.

- Define rollback triggers before cutover.

- Watch the post-import window closely, including scheduled-state and cancellation windows where applicable.

Competitor comparison pages often skip this runbook layer, and you should not either. Choose the model you can staff every week, then scale control depth after your operators are hitting clean weekly execution.

What usually breaks first for small teams and how to prevent it#

Breakages start with ownership gaps, not checkout design, so lock tax, chargeback, and dispute controls before you optimize UX. Pressure-test your setup against the failure modes that hit cashflow first.

| Failure mode | Why it hurts cashflow fast | Prevention action you run every week |

|---|---|---|

| Unclear VAT ownership | Tax decisions stall and risk exposure grows when ownership is unclear | Name one accountable tax owner. If you run a Paddle Merchant of Record setup for covered transactions, confirm contract scope and exceptions. For other setups, document who owns tax decisions and sign-offs. |

| Unmanaged chargebacks | A formal dispute can reverse payment flow immediately and trigger dispute-fee exposure that hits your balance | Monitor dispute-created events in real time, assign one responder, and define transfer-reversal steps early if you use platform models. |

| Weak disputes evidence follow-through | Missed deadlines can auto-lose the case, and weak evidence structure hurts response quality | Keep an evidence pack template. Present events chronologically, group receipts, communications, policies, and logs, then submit before deadline. |

| UX-first decision making from Reddit or r/SaaS threads | You optimize conversion while control gaps keep draining margin | Treat Reddit and r/SaaS UX advice as directional only. Promote UX changes after you prove reliability in tax, disputes, and reconciliation. |

This is how it fails in the real world. One SaaS founder has publicly described early chargeback pain before building stronger process discipline. The pattern is familiar: no owner tracks evidence deadlines, no clear escalation path exists, and one dispute can turn into a cashflow problem.

Use these safe defaults if you operate alone:

- Choose lower operational burden first, then add modularity after you run controls consistently.

- Create one owner for VAT, one for chargebacks, and one backup for disputes.

- Write a one-page incident runbook for holds, delayed settlements, and escalation paths.

- Review one weekly risk dashboard before any checkout or subscription management experiments.

If you want more control later, earn it with process discipline first.

Which platform should you choose for your exact scenario#

Choose Paddle when you need Merchant of Record ownership to offload core liability areas, and choose Stripe when you need deep billing control and can operate it with discipline. Use your risk map as the decision input, not feature checklists.

| Scenario | Recommended platform | Why this fit is safer | What you must staff or verify |

|---|---|---|---|

| Solo creator or tiny SaaS team with limited ops time | Paddle | A Merchant of Record model is a legal ownership model, and that model can take on core liabilities such as tax, refunds, and chargebacks. | Confirm MoR scope in your contract, including where it applies and any exceptions. |

| Developer-led team with complex pricing, usage logic, or negotiated plans | Stripe | Stripe Billing supports simple recurring billing, usage-based billing, and contract-driven models. Stripe Radar gives default fraud protection and supports business-specific rules. | Assign explicit owners for Stripe Billing configuration, Radar rule reviews, and disputes operations. |

| Team moving from one stack to another | Staged transition | Stripe migration guidance is staged, which supports phased transition planning instead of an instant full cutover. | Run migration in stages with hard success gates and rollback triggers before full cutover. |

If your team cannot consistently run tax compliance checks, dispute evidence handling, and rule tuning, Paddle can be a safer default. If your team can run those control loops and needs custom subscription management behavior, Stripe can be a strong long-term fit.

If you transition, do it in stages. Set up the target billing integration first. Migrate customer and payment processor data in controlled phases, then import subscriptions after your monitoring gates pass.

If you are moving from a legacy Paddle setup, keep the existing integration running during validation. Cut over only after the new flow proves stable.

Go no go checklist you can run today#

| Checklist item | Requirement |

|---|---|

| Ownership | We named an owner for tax compliance and an owner for chargebacks and disputes. |

| Contract boundaries | Our contract clearly defines responsibility boundaries for Merchant of Record or payment processor tasks. |

| Stripe staffing | If we choose Stripe, we have clear staffing for Stripe Billing changes and Stripe Radar rule governance. |

| Subscription testing | Our subscription management logic is tested for plan changes, renewals, failed payments, and cancellations. |

| Migration plan | Our migration plan uses staged validation, explicit success criteria, and a rollback trigger. |

| Weekly review | Our weekly review covers payouts, refunds, disputes, and reconciliation. |

| Pause rule | If any item is false, we pause signing or migration and fix ownership first. |

If you want a broader short list before final commitment, review The Best Payment Gateways for SaaS Businesses.

Choose the system you can run reliably and audit without stress#

Choose the model your team can execute every week, because reliable operations protect cashflow better than ambitious architecture. The cleaner decision is the one where the ownership map matches your actual operating capacity.

In practice, this comes down to responsibility boundaries. A Merchant of Record (MoR) model assigns legal payment responsibility to the MoR entity. A payment processor model typically leaves more day-to-day control and accountability with your team.

Paddle positions its MoR model around handling payments, tax, and compliance work. Stripe can operate as a payment processor or, in eligible flows, as MoR through Managed Payments. Define your configuration explicitly, because an unclear MoR setup can create avoidable compliance and financial risk.

Use this final decision filter in the table below.

| If this describes your team today | Safer first choice | Why this wins now |

|---|---|---|

| You run lean ops time and need simpler weekly risk handling | Paddle | You offload more transaction-liability operations in an MoR structure, including chargeback handling flow at the platform level. |

| You need deep custom billing logic and control surfaces | Stripe | You gain flexibility for complex billing and risk controls, but your team must run disputes, policy, and ownership loops with discipline. |

| You plan to scale into multiple regions or models | Stage your rollout | Confirm region and product coverage for your launch markets first, then expand after you validate controls and monitoring. |

If nobody can own VAT, disputes, and chargebacks every week, choose the lower operational burden first. Protect continuity.

Run this final go no go check before you commit#

- Name one owner for VAT, one for chargebacks and disputes, and one backup.

- Document whether you operate as MoR or payment processor in each flow.

- Verify country and product coverage for your exact launch regions before signing.

- Confirm your dispute response workflow, evidence standard, and escalation path.

- Test payment lifecycle events end to end before migration day.

- Set rollback triggers and a monitoring window for the first live cycle.

Compare your current flow against this checklist, then request access or talk to sales to confirm coverage where supported. For implementation depth, read The Best Payment Gateways for SaaS Businesses, Stripe vs. PayPal for International Freelancers, and Value-Based Pricing: A Freelancer's Guide.

Frequently Asked Questions

Is Paddle or Stripe cheaper once you include add-ons, dispute work, and internal ops time?

Headline rates only start the math. Paddle lists a 5% + 50¢ per-checkout rate, while Stripe commonly shows 2.9% + 30¢ per successful charge and can add +1.5% for international cards, +1% for currency conversion, and dispute-related fees (for example, $15.00 for disputed payments). Total cost in SaaS payments depends on your transaction mix and the time your team spends running payment operations week to week.

What is the practical difference between a Merchant of Record and a payment processor?

In a Merchant of Record (MoR) flow, core transaction responsibility is handled in that model by the MoR, including dispute handling in Paddle's MoR setup. A payment processor gives you payment rails and tooling, but your team typically owns more operating process. Stripe Tax can automate major tax workflows, but automation does not change liability ownership by itself.

Who handles chargebacks and disputes better for a small SaaS team with no finance ops hire?

If bandwidth is tight, Paddle can reduce direct dispute handling load because chargeback disputes in its MoR flow are raised against Paddle. With Stripe, your team must run an active dispute process and meet required response deadlines, usually within 7 to 21 days depending on network rules. If you do not respond before the deadline, you automatically lose the dispute.

When should I choose Stripe even if Paddle seems simpler?

Choose Stripe when you want processor-level control and you can staff the operational workload consistently. In practice, that means owning dispute responses to deadline, balancing checkout friction with risk-signal collection, and planning for payout timing and possible reserve holds.

Does checkout UX matter more than compliance and risk ownership?

No. You need both. Stripe guidance explicitly frames this as a balance: collect enough information for accurate risk assessment without overloading checkout.

What should I verify before migrating recurring billing from one platform to the other?

Use a phased migration plan, not a one-step cutover. Move new customers first, then migrate existing customers with a clear card-update process and ownership plan. Define success gates and rollback triggers before you migrate live subscriptions.

How do I avoid payment delays and avoidable holds during the first 90 days?

You cannot eliminate delays and holds completely in the first 90 days, so plan cashflow around that reality. Stripe notes initial payouts are typically scheduled 7-14 days after your first successful payment and that reserve balances can temporarily restrict payouts; Paddle documents scheduled monthly payouts (sent by the 15th in that flow) rather than on-demand withdrawals. Keep a cash buffer, monitor payout status weekly, and document escalation steps before issues appear.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 2 external sources outside the trusted-domain allowlist.

Educational content only. Not legal, tax, or financial advice.

Related Posts

Value-Based Pricing for Freelancers Under Real Payment Risk

Value-based pricing works when you and the client can name the business result before kickoff and agree on how progress will be judged. If that link is weak, use a tighter model first. This is not about defending one pricing philosophy over another. It is about avoiding surprises by keeping pricing, scope, delivery, and payment aligned from day one.

The Best Payment Gateways for SaaS Businesses

**Choose your gateway stack by cashflow risk first, then optimize for features and price.** If you want the best payment gateway for SaaS, start where money can stall, not where brand buzz is loudest. You are the CEO of a business-of-one, which means a payout delay or a payment hold is not an inconvenience. It is an operating event.

Stripe vs. PayPal for International Freelancers

**For an international Stripe or PayPal choice, pick the payment gateway that cuts your cashflow exposure first, then optimize fees.**