Quick Answer

Use a status-gated approach for india equalisation levy foreign platforms digital advertising services: monitor announcements, but change billing only after legal confirms enacted Indian law text and effective timing. Keep the advertising levy track separate from the non-resident e-commerce operator track, run sandbox tests before release, and preserve rollback paths. The safest immediate action is to document source type, approvers, and current treatment while you prepare reversible configuration changes.

India Equalisation Levy Changes Are Real but Operational Certainty Still Depends on Legal Status#

Treat any reported change as a trigger for a controlled review, not a switch straight into production. If you handle the India advertising levy question for a foreign platform, the real job is deciding when legal status is firm enough to change billing, tax, and customer-facing controls. Otherwise, you create a second problem while trying to solve the first.

- Use headlines to escalate, not to go live

Reuters reported on March 25 that India will scrap the 6% tax on online digital advertisements, and Times of India reported abolition of the online-ads levy from April 1. That is important as an early signal, especially for compliance, legal, finance, and risk owners who need to brief leadership quickly. The practical rule is narrower. Do not treat reporting language as proof that your production tax logic should change on that date. Start with a basic check. Confirm which source you are relying on, save a dated copy, and record whether it is media reporting, commentary, or primary law text. The failure mode is familiar. A team updates invoices based on announcement momentum, then has to unwind tax treatment, credit notes, and reconciliation when the legal effective date or scope turns out to be narrower than expected. Key differentiator: speed matters for internal awareness, but legal status controls production changes.

- Separate the 6% online advertising levy from the 2% e-commerce operator levy

This is where many avoidable errors begin. Commentary and press coverage often focus on the 6% levy on online advertising services introduced in 2016, while tax commentary also describes a separate 2% equalisation levy on consideration received by non-resident e-commerce operators for e-commerce supply or services. Those are not the same rule set, and you should not collapse them into one India digital tax bucket. If your platform sells digital advertising services into India, check how your products are mapped in billing and tax. A useful operator test is whether the invoice line, product code, and tax rule all identify advertising specifically, or whether they sit inside a broader "platform services" category that could also catch marketplace or e-commerce activity. Key differentiator: scope comes before status. If you are looking at the wrong levy, even a legally correct update can still be operationally wrong.

- Build the evidence pack before interpretation is challenged

If there is uncertainty, prepare the paper trail now rather than after a tax notice or internal audit request arrives. Keep a dated interpretation memo, the exact source snapshots you reviewed, named approvers, and the billing or tax-engine ticket showing what changed and when. If you decide not to change controls yet, document that too. You do not need a huge file. You do need enough to show that your position was reasoned, time-stamped, and tied to the legal status of the relevant levy. Key differentiator: audit defensibility depends less on having the fastest answer than on showing why your answer was reasonable at the time.

You might also find this useful: How Foreign Companies Can Comply With India's DPDP Act.

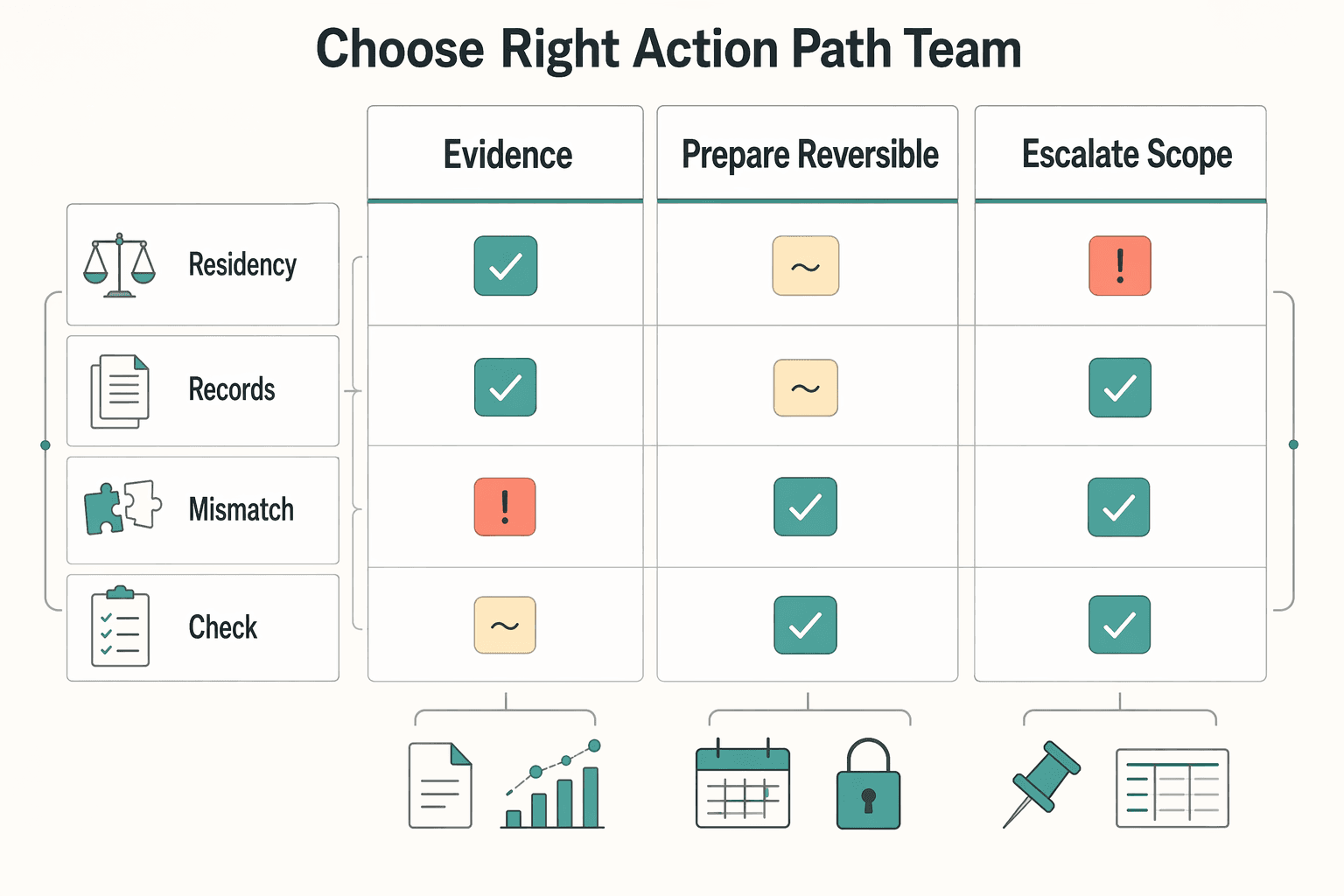

How to Choose the Right Action Path for Your Team#

If you own tax operations for a non-resident enterprise, choose the path you can defend later, not the one that feels fastest now. Use four filters on every decision: legal reliability, implementation effort, reversibility, and audit defensibility.

| Action path | Use when | Key differentiator |

|---|---|---|

| Hold production, brief leadership, document the basis | Inputs are reporting, commentary, or partial legal material and the legal position is still unclear | Strongest audit defensibility; slowest operational pace |

| Prepare reversible changes, but do not publish yet | You expect movement and want faster implementation without treating momentum as legal effect | Best balance of effort and reversibility |

| Escalate scope review when exposure is not clearly narrow | India revenue model is not cleanly limited to one exposure type, or product lines are bundled | Highest upfront effort; strongest protection against scope-mapping errors |

- Hold production, brief leadership, document the basis

Use this when your inputs are reporting, commentary, or partial legal material and the legal position is still unclear. It is the most defensible option when you need to avoid hard-coding a position you may have to unwind. Save the exact source version reviewed, label the source type, and record who approved the temporary hold. Key differentiator: strongest audit defensibility, slowest operational pace.

- Prepare reversible changes, but do not publish yet

Choose this when you expect movement and want faster implementation without treating momentum as legal effect. In practice, that means sandbox rule edits, draft invoice language, and dated change tickets that stay out of production. Keep a clear release gate so "ready to deploy" does not become "deployed by assumption." Key differentiator: best balance of effort and reversibility.

- Escalate scope review when exposure is not clearly narrow

Do this if your India revenue model is not cleanly limited to one exposure type or if product lines are bundled. The available research notes broader scope discussions under the Indian Finance Act 2020 and limited clarity, so classification errors are a practical risk. Request line-by-line product mapping and keep it with your interpretation memo and approval trail. Re-check that mapping regularly as part of ongoing risk review. Key differentiator: highest upfront effort, strongest protection against scope-mapping errors.

Related: A Guide to VAT MOSS for UK Freelancers Selling Digital Services to the EU.

Best Evidence Sources to Confirm Status Before You Change Billing#

Do not change billing based on headlines or commentary alone. For production changes, use official legal text plus official legislative status as your go-live gate; treat other sources as signal or interpretation support.

| Source type | Legal authority | Update speed | Contradiction risk | Action threshold |

|---|---|---|---|---|

| Finance Bill, 2025 text | Primary for legal wording | Medium | Medium when summaries run ahead | Use for legal sign-off only when text is clear |

| Indian Parliament records | Primary for formal stage/status | Medium | Low to medium | Use to confirm formal progress before tax-engine changes |

| Reuters-style reporting on U.S. reciprocal tariffs context | Signal only, not legal finality | Fast | High | Use for leadership pre-briefs and contingency planning only |

| Specialist tax commentary and policy analysis | Interpretation support, not final authority | Fast to medium | Medium to high | Use for scenario memos and issue spotting, not go-live approval |

For commentary, keep source discipline tight. KPMG (updated March 16, 2026) states its material is general information, subject to change, and should be applied with tax-adviser input. Brookings is a January 2017 working paper, useful background but not enacted law text; it describes the levy as applying from June 1, 2016. ClearTax (updated May 27th, 2025) is useful plain-language context, including that the levy was introduced in 2016. If a source page does not provide usable substantive text, for example only "Just a moment...," exclude it from your approval pack.

If legal text or legislative status conflicts with commentary, hold production, log the contradiction, and escalate. We covered related platform questions in The Best Platforms for Selling Digital Products.

Best Decision Paths for Invoicing and Tax Engine Changes#

Use a three-state gate, not a one-step switch: announced, passed, and effective. Your billing decision should follow confirmed legal status, not policy momentum.

| State | Billing action | Withholding treatment | Customer communication |

|---|---|---|---|

| Announced | Keep current transaction-based controls for online advertising services. Prepare only reversible config changes (drafts/feature flags). | Keep current treatment; do not change deductions from announcements alone. | "We are monitoring legal developments; no invoice treatment change is currently in effect." |

| Passed | Test proposed logic in sandbox with India scenarios, but do not move to production until legal confirms scope and effective date. | Keep current treatment unless legal confirms a treatment is already operative. | "The measure has passed; invoice treatment remains unchanged pending effective-date confirmation and implementation review." |

| Effective | Deploy one dated release across invoicing, tax rules, and reconciliation reporting, with rollback conditions documented. | Apply approved treatment from the confirmed effective date. | State what changed, the effective date, and whether treatment is prospective only. |

1. Announced means prepare, not switch#

When the signal is a press statement, transition language, or political-compromise framing, keep production unchanged. The U.S. Treasury release dated June 28, 2024 describes an extension of a political compromise through June 30, 2024 and ties it to continuing G20/OECD multilateral negotiations, which points to ongoing uncertainty rather than immediate domestic billing effect.

Your action here is reversible preparation only: draft rules, draft customer language, and tests in non-production. If your approval pack does not include the relevant India law text plus status confirmation, you are still in announced.

2. Passed means sandbox first, then legal sign-off#

A passed measure is closer to change, but it can still leave scope or timing questions open. Run parallel validation in sandbox and require legal sign-off before any production tax-logic update.

Keep the evidence packet practical: test invoices, tax-calculation logs, and reconciliation comparisons showing current versus proposed treatment. If legal cannot confirm what changes, from when, and for which service class, keep production on the current rule.

3. Effective means dated deployment with rollback conditions#

Once status is confirmed effective, deploy as a controlled, dated change set across invoicing, tax rules, and reconciliation reporting. Record the operative date, legal basis reviewed, and whether treatment is prospective.

Include rollback conditions in case formal clarification later changes scope or start-date interpretation. If that happens, pause further changes, preserve the evidence file, and issue corrected downstream reporting only after re-approval.

4. Keep the advertising levy separate from the non-resident e-commerce operator regime#

Treat this as a mandatory scope check. The Equalisation Levy on online advertising services (described by Brookings as applying from June 1, 2016) should not be merged into a single toggle with the separate non-resident e-commerce operator regime referenced in Finance Bill, 2020 and Finance (No. 2) Bill 2024.

Use a hard control before go-live: require the exact service type and exact legal basis to be named in the change ticket. If your catalog mixes advertising with marketplace or broader digital supplies, split invoice logic first, then apply regime-specific treatment.

For a step-by-step walkthrough, see How to Get a PAN Card as a Foreign National in India.

Best Sign Off Sequence Across Tax Legal Finance and Product Ops#

Use a tax -> legal -> finance -> product ops and engineering sequence as an internal control, not a statutory requirement. It helps you avoid customer-facing invoice changes before your India position is clearly documented.

| Step | Focus | Checkpoint |

|---|---|---|

| Tax counsel first | Start with a short memo grounded in what you can support; keep strict scope discipline | State clearly whether your conclusion is limited to online advertising services |

| Legal second for residual risk | Have legal assess remaining controversy risk, including potential double-taxation exposure | Use a one-page sign-off that names the service, billing entity, and any unresolved issue |

| Finance third before invoice behavior changes | Approve posting logic, month-end reconciliation treatment, and credit-note handling before product ops changes invoice behavior | Require sample entries, a reconciliation bridge, and one test case that crosses the planned change date |

| Product ops and engineering last with controlled release | Promote only after tax, legal, and finance approvals are documented | Require named approvers in the change ticket, then run a timed checkpoint after first cycle close |

- Tax counsel first

Start with a short memo grounded in what you can support: the levy is described as running from June 1, 2016, introduced in 2016, and commonly discussed as aimed at business-to-business digital transactions. Keep strict scope discipline and state clearly whether your conclusion is limited to online advertising services. If current status is still interpretive, say that plainly instead of treating it as already operative.

- Legal second for residual risk

After tax frames the position, have legal assess remaining controversy risk, including potential double-taxation exposure. The goal is a concise risk note on whether the planned invoice treatment could still be challenged even if your levy interpretation is consistent. A practical checkpoint is a one-page sign-off that names the service, billing entity, and any unresolved issue.

- Finance third before invoice behavior changes

Finance should approve posting logic, month-end reconciliation treatment, and credit-note handling before product ops changes invoice behavior. If finance cannot show pre-change versus post-change reporting treatment in the ledger and close pack, hold the release. Require sample entries, a reconciliation bridge, and one test case that crosses the planned change date.

- Product ops and engineering last with controlled release

Promote only after tax, legal, and finance approvals are documented. Use idempotent controls and audit logs so repeated deployments do not duplicate tax outcomes. Require named approvers in the change ticket, then run a timed checkpoint after first cycle close to confirm invoice outputs, tax logs, and reconciliation totals match the approved position.

This pairs well with our guide on US-India DTAA Independent Personal Services for Freelancers.

Best Evidence Pack to Keep if Your Position Is Challenged Later#

Keep one dated, versioned evidence pack that shows what you relied on, what you treated as background only, and what remained uncertain at the time of decision.

| Artifact | What to keep | Purpose |

|---|---|---|

| Dated position memo | Decision date, owners, scope, and the exact materials reviewed; keep updates as new versions | Shows how your position changed over time instead of replacing prior reasoning |

| Audit pack with decision artifacts | Source snapshots, approvals, change tickets, and reconciliation outputs that show pre-change and post-change behavior | Shows what supported the decision and records if a source could not be verified |

| Source-type and contradiction log | Label each source by type so reviewers can see what is legal authority versus context | Shows authority level and contradictions |

| Residual-risk appendix | Open questions, escalated issues, and who owns follow-up | Keeps prior approvals, assumptions, exceptions, and unresolved items together |

- Dated position memo

Maintain a short memo with the decision date, owners, scope, and the exact materials reviewed. Keep updates as new versions so the file shows how your position changed over time instead of replacing prior reasoning.

- Audit pack with decision artifacts

Store the supporting record with source snapshots, approvals, change tickets, and reconciliation outputs that show pre-change and post-change behavior. If a source could not be verified, record that explicitly; for example, one source in this research trail returned "Access Denied - WAF Rule Reached."

- Source-type and contradiction log

Label each source by type so reviewers can see what is legal authority versus context. For example, the EY/FICCI document dated March 2025 is a media-and-entertainment industry report, not tax-law text, and the LawEcon page (last updated August 15, 2025) discusses digital competition regulation and notes limited evidence on competition outcomes.

- Residual-risk appendix

Keep a standing appendix for unresolved or escalated issues, including open questions and who owns follow-up. The goal is fast retrieval under challenge: one file with prior approvals, assumptions, exceptions, and unresolved items.

Need the full breakdown? Read Brazil's CNPJ for Foreign-Owned Businesses: When It Is Needed and What It Does.

Best Ways to Handle Edge Cases After Repeal Signals#

Do not apply one broad billing change across every India flow based on a repeal signal alone. Handle edge cases separately by contract line, service period, legal basis, and reporting audience.

- Require line-level mapping for mixed-service contracts

For bundled contracts, change treatment only after mapping each invoice line to the underlying service, pricing basis, delivery period, and billing entity. Avoid contract-level switches when one agreement includes different service types. Keep the line mapping with the dated interpretation memo so the record shows what was sold and why each line was treated that way.

- Keep retroactive adjustments on original-period logic unless counsel confirms a different approach

For credit notes, true-ups, rebates, and late pricing changes, default to the treatment tied to the original service period. Before posting any retroactive item, check the original invoice date, service period, and adjustment date together. If counsel supports a different treatment, record that advice and preserve invoice-level references.

- Split advertising and non-resident e-commerce exposure into separate control tracks

If your group has both exposure types, keep separate controls, approvals, and testing for each legal basis. Do not assume one status change resolves both. In practice, this means separate rule ownership, separate reconciliations, and separate memo sections.

- Use conditional language in United States parent reporting

If legal status in India is still conditional, say that clearly and consistently in parent reporting. Align memo language, quarter-end decks, and control narratives so teams do not overstate certainty. Resolve wording conflicts before sign-off, especially where summaries compress nuance.

Related reading: EU DAC7 Directive for Freelancers Using Digital Platforms.

Best Mistakes to Avoid When Headlines Move Faster Than Law Text#

Treat commentary as a prompt to investigate, not a trigger to change production logic. Most avoidable errors happen when teams act on headlines before they have enforceable text and a reversible implementation path.

- Treating advocacy or media as if it were enforceable law

Material like an October 2025 submission responding to comments for the 2026 National Trade Estimate Report can inform risk monitoring, but it is not Indian statutory text or binding tax-authority guidance. Keep billing and tax logic unchanged until legal can tie the change to enacted text and approve implementation.

- Collapsing separate regimes into one "India DST" rule

Keep the advertising track and the non-resident e-commerce track separate in controls, ownership, and reporting. If your internal basis points to Finance Bill, 2016 for one track and Finance Bill, 2020 for another, do not merge them into one generic rule for convenience.

- Removing controls without rollback readiness

Do not delete tax-engine logic unless rollback is fully documented and testable. Preserve rule IDs, test evidence, reconciliation queries, downstream report mappings, and withholding-tax dependencies so a disputed period does not force an emergency rebuild.

- Assuming one tax change resolves all characterization risk

Do not treat a transaction-tax change as automatic closure for royalty-income characterization questions. Keep levy treatment and characterization analysis separated in your evidence file so you can defend each position independently.

The Practical Next Move for Most Foreign Platforms#

For most teams, the practical next move is status-gated: prepare now, but change production only when legal can cite enacted Indian law text.

- Gate on law, not commentary

Separate inputs into two buckets: sources that can support a production tax change, and sources that are monitoring context only. A 2026 NFTC submission to the USTR NTE process is policy context, not enacted Indian tax law. The same applies to older technical commentary like the EY note dated 17 Aug 2020: it helps with history and scope, including the 2% EL description for non-resident e-commerce operators, but it does not confirm current legal effectiveness by itself. If legal cannot point to effective Indian law text, keep production treatment unchanged and mark the issue as "watch, not deploy."

- Build reversible changes before release

When legal sees a possible change, prepare the operational layer in a controlled way before touching customer-facing output: a dated interpretation memo, saved rule IDs, sample invoice tests, and pre-change/post-change reconciliations. Keep levy tracks separate in your logic rather than collapsing distinct rules into one "digital tax" bucket. Use a simple release standard: sandbox first, production second, rollback always.

- Use one traceable control owner across decisions

If your exposure spans India Equalisation Levy, Indian GST, and cross-border payout operations, assign one accountable owner for the decision trail. That owner should keep legal interpretation, finance posting logic, and ops changes tied to the same effective-date decision and evidence pack. Keep three artifacts current: the status memo, tax/legal/finance approvals, and a contradiction log for gaps between commentary and law status. For GST scope context, see GST for Digital Marketplace Platforms: Australia Canada India Compared.

If you want a deeper dive, read RBI Payment Aggregator License: What Foreign Platforms Need to Operate in India.

Frequently Asked Questions

Is India’s equalisation levy on digital ads still in force for non-resident enterprises?

The status-safe answer is that you should not treat it as repealed unless you can point to enacted Indian law text. What is clearly grounded is that India introduced the levy in 2016, and Brookings describes it as applying from June 1, 2016 to specified services provided by non-residents. If your exposure is online advertising, keep production treatment unchanged until legal confirms an effective repeal, not just a reported one.

What is the operational difference between the advertising levy regime and the non-resident e-commerce operators regime?

They are not the same regime, and your controls should stay separate. The 2016 version was introduced for specific advertising services, while the 2020 expansion covered e-commerce transactions and is commonly described as a 2% levy on online sales of goods and online provision of services by non-resident e-commerce operators. In practice, this can require separate rule logic, invoice mapping, and exception reporting, because a platform may be out of scope for one track and still be exposed on the other.

Why do some sources link repeal to U.S. reciprocal tariffs while others emphasize OECD Pillar One?

Those are different narratives around the same policy area, not the legal switch that makes a tax change effective in India. Pillar One references usually come from the wider OECD and BEPS debate involving over 135 countries and jurisdictions, while tariff references are often part of trade and diplomatic reporting. Use both as context for leadership briefings, but not as your go-live trigger.

What should a foreign platform change first in systems when repeal is reported but timing is unclear?

Start with evidence and reversibility, not billing output. Freeze a dated interpretation memo, capture source snapshots, and prepare a sandbox change using an effective-date field, saved rule IDs, and sample invoice tests before touching production. Keep legacy rule paths reversible until legal timing is clear.

Does repeal remove all India Digital Services Tax risk for cross-border platforms?

No. A reported change to one levy does not automatically remove potential exposure under other EL provisions. It also does not eliminate the need to review separate exposure for non-resident e-commerce operators under the later expansion.

What evidence should we retain in case India tax authorities challenge our interpretation later?

Keep a file that shows both your legal reasoning and your system behavior. A practical pack includes a dated memo referencing the 2016 levy framework and any later law text you relied on, approval records from tax, legal, and finance, change tickets, and pre-change versus post-change reconciliations. Add a contradiction log for commentary versus formal law status so support is available if challenged later.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- brookings.edu/wp-content/uploads/2017/01/equalisation-levy...trusted

- digitalcommons.law.uga.edu/cgi/viewcontent.cgitrusted

- downloads.regulations.gov/USTR-2025-0016-0026/attachment_1.pdftrusted

- elibrary.imf.org/display/book/9781484315224/ch011.xmltrusted

- ftb.ca.gov/file/personal/residency-status/part-year-and...trusted

- ftb.ca.gov/file/personal/residency-status/index.htmltrusted

- home.treasury.gov/news/press-releases/jy2436trusted

- htu.edu/wp-content/uploads/2025/08/Huston_Tillotson_...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

GST Digital Marketplace Platform Comparison for Australia, Canada, and India

This comparison is an operator guide for Australia, Canada, and India. It is about control decisions, not software selection. The real question is who owns GST decisions, invoice issuance, audit trail quality, and launch readiness in each market.

How Foreign Platforms Should Scope RBI Payment Aggregator Licensing in India

For many foreign platforms, the first India decision is scope, not speed. You need to identify the correct RBI Payment Aggregator - Cross Border, or PA-CB, route before launch work spreads. RBI introduced this category on 31 October 2023. The PA Directions took effect on 15 September 2025.

VAT MOSS and Non-Union OSS for UK Freelancers Selling to the EU

If you sell digital services from the UK to EU customers, treat UK VAT MOSS as historical and [Non-Union OSS](https://vat-one-stop-shop.ec.europa.eu/one-stop-shop_en) as the current route to assess. You cannot use UK VAT MOSS for sales made from 1 January 2021 onwards. For UK sellers who are not established and have no fixed establishment in the EU, the relevant OSS branch is the **Non-Union scheme**.