Quick Answer

Start by treating the eu dac7 directive as an operations workflow: map each channel, classify every line once, and verify the reporting platform entity for each channel. Keep a year-based evidence pack, then run three internal checkpoints so reconciliation is done before filing pressure. Escalate when records conflict, operator ownership is unclear, or a complex cross-border VAT issue may need a CBR path.

What DAC7 means for freelancers using digital platforms#

Treat the EU DAC7 Directive as an execution problem, not a theory exercise. Your job is to do three things early: identify which income channels need review, set up one record routine you can actually maintain, and escalate complex cross-border cases before they turn into year-end guesswork.

This article stays intentionally narrow: seller-side DAC7 readiness for platform income. VAT frameworks matter here as process context, not as DAC7 determinations. If you opt into an OSS scheme, you register in one Member State of identification. OSS returns sit alongside domestic VAT returns, and supplies covered by your chosen scheme must be declared through that scheme. Use that structure to organize records, not to decide DAC7 scope. If more than one country could reasonably assess the same income stream, escalate early. Work through the article in this order:

- Channel map: list each platform or sales channel, buyer location, EU link, and identifiable platform operator entity so review flags show up before year-end.

- Line classification: use one label system across invoices, platform exports, and books so reconciliation is matching, not relabeling.

- Evidence pack: keep one year folder with account records, platform summaries, and dated submissions or correction requests.

- Reconciliation: compare platform totals against accounting records before filing pressure builds, so missing rows, duplicates, or mixed labels are caught early.

- Escalation: route unclear multi-country or entity-mismatch cases for professional review. If a VAT ruling path such as CBR is being considered, treat that as a complexity signal and get advice under the relevant national ruling conditions.

For broader residency planning, start with The Ultimate Digital Nomad Tax Survival Guide for 2025. For a country-level tax baseline example, see Taxes in Germany for Freelancers and Expats. If you want a clean baseline on the directive before applying these steps, use What Is DAC7? EU Platform Reporting Directive Explained.

How to Use This List and Who It Fits#

Use this list to reduce mismatch risk before you optimize for speed. If your channel map, labels, and evidence trail are not stable first, faster admin usually just creates worse records.

This fits independent freelancers and consultants with platform-linked, cross-border activity: buyers in more than one country, an EU-linked platform, or work touching more than one tax jurisdiction. It is seller-side guidance, not an operator build guide. If all your work is direct invoicing with no platform income, or you need a legal primer first, start with What Is DAC7? EU Platform Reporting Directive Explained.

Use a step only if it passes all four filters:

- Risk first: does this step reduce the chance that platform exports, invoices, and books describe the same income differently?

- Repeatability: can one source record feed multiple outputs without retyping?

- Evidence: can you show what changed, when, and which document supports it?

- Boundary control: are DAC7 interpretation and VAT administration kept on separate tracks? OSS can mean one registration in one Member State of identification, and OSS returns are additional to domestic VAT returns. Those VAT mechanics do not, by themselves, determine DAC7 scope.

A practical way to run the article is in two passes:

- Pass 1: Gap map. Move through every section and log missing operator entities, unmapped income lines, absent tax details, and country links that need review.

- Pass 2: Documented fixes. Close only the flagged gaps and save proof: corrected labels, profile updates, and a dated evidence log.

That sequence helps prevent silent drift when a new platform, a profile change, or a country move pushes exports, invoices, and books out of sync.

You are ready to move on only when a third party could reconstruct what you did from the tracker and evidence log alone, with no meeting required.

1) Confirm Your DAC7 Exposure Before You Do Anything Else#

For DAC7, this first step is a risk screen, not a legal conclusion. The goal is to identify which income channels need review before ambiguity spreads into platform exports, invoices, and bookkeeping.

Start with a clean channel map. Mixed rows tend to break classification and reconciliation later, even when the totals still look fine.

- Split mixed channels into separate rows

Use one row per real income path, not one row per client or platform brand. If a platform introduced the buyer but part of the work was billed directly later, split that into two rows.

- Capture four fields on every row

Every row should include buyer location, platform involvement, EU link, and an exposure flag. Keep the flags operational, such as potential exposure, review needed, or no current exposure signal, so triage stays fast and readable.

- Keep DAC7 notes separate from VAT administration notes

Use VAT context for process planning, not for DAC7 scope decisions. OSS is optional, uses one Member State of identification, and OSS returns are additional to domestic VAT returns. If you use an OSS scheme, you must report all supplies that fall under that scheme through OSS. Treat tools like OSS and VAT Cross-border Rulings as process anchors only. Record unresolved items as Current threshold pending official verification and Current processing timeline pending official verification instead of recycling old figures.

- Escalate patterned ambiguity early

Escalate as soon as you see repeated multi-jurisdiction ambiguity, an unclear platform role, or conflicts between platform exports, invoices, and your books. Every open issue needs an owner and a next action.

If buyer location is unclear because of a mid-year move, or because billing address, tax residence, and work location do not line up, resolve that in parallel with your residency file.

Keep evidence attached to the map as you go. For each flagged row, attach the document that created the question, such as platform terms, a sample payout export, an invoice trail, or a platform profile showing the operator entity. If you later need a VAT Cross-border Ruling on complex cross-border VAT treatment, file it in a participating EU country where you are VAT-registered. Follow that country's national VAT ruling conditions.

Verification checkpoint#

Use this checkpoint before moving on.

Pass only if all four are true:

- every income path has its own row, with platform and direct work split

- every row shows buyer location, platform involvement, EU link, and an exposure flag

- DAC7 notes and VAT notes are kept in separate columns or tabs

- each open issue has an owner and next action

Fail and stop if any of these appear:

- a row still says "platform + direct" without separation

- VAT status is being used as the answer to a DAC7 question

- the platform operator is unclear

- invoices, exports, and books describe the same income differently

If you pass, move to line-level activity classification. If you fail, fix the map first.

2) Classify Every Income Stream by Relevant Activity#

Classify each income line before you total anything. Line-level labels are a practical way to keep reporting mapping, platform summaries, and VAT documentation aligned.

This matters most when revenue is mixed, such as services, digital products, and occasional rentals. The payoff is usually cleaner reconciliation and faster review. The tradeoff is that some edge cases will stay unclear until you compare platform terms, your reporting materials, and country guidance. That is fine. The point is to get to a consistent first pass, then escalate the lines that remain ambiguous.

Use one rule set for every invoice line:

- Activity label: assign one activity label per line using your reporting or platform documentation.

- Tax note: add a short note for possible VAT impact under local rules, and keep any direct-tax follow-up note separate. This is documentation, not a final determination.

- Cross-border marker: tag each line as domestic or cross-border and note the EU Member State link when present.

- Evidence reference: attach a record ID, such as invoice number, platform transaction ID, or payout batch reference.

Create a short label dictionary and use it everywhere. The same activity label should appear in invoices, exported platform rows, and ledger mapping notes. Consistent naming reduces category drift when someone updates one source but not the others. If a label is too vague to survive across those sources, rewrite it before you keep using it.

A simple example shows why this matters. If you sell advisory calls and downloadable templates, split them into separate lines so each line carries one activity label and one tax note. That split can prevent mixed-category totals that look fine in a dashboard but fall apart when you reconcile platform data to books and filings.

Keep VAT context separate from activity classification. Since 1 July 2021, cross-border B2C VAT rules changed. If you use an OSS scheme, you register in one Member State of identification and declare supplies covered by that scheme through OSS VAT returns. Those OSS returns are additional to, not a replacement for, domestic VAT returns. Online marketplaces and platforms facilitating supplies can be deemed suppliers in certain circumstances and have record-keeping duties. The EUR 10,000 threshold and the 150€ low-value-goods limit under the import scheme apply in specific VAT frameworks, not as universal activity-category tests.

Before item 3, check whether any line still bundles two different activities under one description. Bundled lines are a common failure mode because one summary may look acceptable in one reporting path but fail in another. If you cannot explain the label without a footnote, the line probably needs to be split. For envisaged complex cross-border VAT treatment questions, flag the line for possible CBR review instead of forcing a definitive label too early.

Before item 3, confirm the following:

- Every invoice line has one activity label.

- Every line has one tax note and one cross-border marker.

- Every line has an evidence reference.

- No line remains tagged as miscellaneous if it combines distinct activities.

If a line still carries more than one activity, split it before you continue. Once labels are stable, the next step is to tie each channel to the operator behind it.

3) Identify the Reporting Platform Operator in Each Channel#

Once you know what each revenue line is, identify the legal entity operating each channel you use. This is a record-mapping step that keeps requests, corrections, and profile updates aligned with account records.

If you use two marketplaces plus direct invoicing, keep three separate channel records. For each platform channel, store the legal entity name shown in platform documents, the stated jurisdiction, and the support contact path. For direct invoicing, mark that no platform is involved for that revenue line. Do not merge channels just because the brand looks related. Different channels under one brand can still point to different legal entities, and that distinction matters when you are asked to confirm details or correct a profile.

| Channel | Record this now | Why it matters |

|---|---|---|

| Marketplace A | Legal entity name, stated jurisdiction, support channel, account ID | Keeps requests and corrections aligned with account records |

| Marketplace B | Same fields, kept separate even if the brand is related | Prevents merged records when related brands use different legal entities by channel |

| Direct invoicing | Mark no platform involved and keep invoice evidence | Separates non-platform revenue lines while preserving tax evidence |

Use VAT channel data as a cross-check, not as a DAC7 rule test. Since 1 July 2021, the OSS framework applies for covered supplies. If you opt into an OSS scheme, you register in one EU Member State, the Member State of identification, for that scheme. If a channel uses OSS, note the Member State of identification. These VAT details help validate administrative handling, but they are not a standalone test for DAC7 role allocation.

Before item 4, confirm the following:

- Every platform income line links to one channel record ID and one legal entity name.

- One document proof is saved per channel.

- Jurisdiction is populated, including Member State of identification when an OSS registration is stated.

- Support route is recorded with a ticket ID or message log.

Escalate quickly if one brand shows different legal entities across channel documents and account screens. Ask for written clarification and save the response in your evidence pack. If cross-border VAT treatment is complex, consider whether a VAT Cross-border Ruling request is appropriate. Requests are introduced in the participating EU country where the requester is VAT-registered and must follow that country's national VAT ruling conditions.

Set a simple precedence rule for document conflicts. Use the legal entity in formal channel documentation as your working reference, log conflicting screen labels, and attach the support response that resolves the gap. That gives you a clean trail and avoids silent edits that nobody can explain later.

If a platform updates legal notices during the year, log the change date and keep both old and new snapshots. You do not need a long memo. A dated note plus saved documents is usually enough to explain why a channel record changed. Once every channel points to the right legal entity, build the evidence pack around those records.

For a step-by-step walkthrough, see Digital Platform Reporting for Online Marketplaces: MRDP, DAC7, and UK HMRC Duties.

4) Build a Reportable Seller Evidence Pack Before Platforms Ask#

Build the evidence pack before any request arrives. In practice, that is the difference between a routine document request and a scramble.

| File | What to keep | When relevant |

|---|---|---|

| Core records file | Current tax-identification and registration records together | Always |

| Member State of identification file | Registration confirmation for the single Member State of identification and any related change notices | If you use OSS |

| OSS records file | Invoices, required records, and bad debt relief evidence together, aligned with record-keeping and audit topics | For periods where OSS applies |

| Complex-case escalation file | Draft facts and submitted correspondence together | For complex cross-border VAT transactions; if you seek a CBR advance ruling, align the request with national VAT ruling conditions in the country where it is filed |

For cross-border VAT readiness and related record work, speed comes from file quality, not last-minute searching. A practical internal setup is one year-based source folder, updated whenever core tax-identification or registration details change. The file should be boring in the best way: an obvious structure, current documents easy to find, old documents still archived, and a short log showing what changed and when.

Use this structure for the folder:

- Core records file: keep current tax-identification and registration records together.

- Member State of identification file: if you use OSS, store your registration confirmation for the single Member State of identification and any related change notices.

- OSS records file: keep invoices, required records, and bad debt relief evidence together for periods where OSS applies, aligned with record-keeping and audit topics.

- Complex-case escalation file: for complex cross-border VAT transactions, keep draft facts and submitted correspondence together. If you seek a CBR advance ruling, align the request with national VAT ruling conditions in the country where it is filed.

If you use two marketplaces plus direct invoicing, a practical layout is one tax-year top folder, three channel subfolders, and one shared VAT subfolder. Keep channel files in the channel folders. Keep OSS and related scheme files in the shared folder with clear period-based names. That structure is simple enough to maintain and specific enough that someone else can use it without decoding your logic.

A common failure mode is treating the pack as static after onboarding. Avoid that by keeping a dated submission log that records what you sent, to which entity, and when. If a mismatch appears later, that log can shorten resolution time because you can point to the exact document bundle instead of trying to rebuild it from memory.

Set update triggers so maintenance stays predictable. As an internal control, update the pack when your legal name, tax IDs, registration details, or OSS filing setup changes. Small, regular updates are easier than rebuilding the file stack at year-end, and they reduce the chance that one outdated document keeps resurfacing in later requests.

Archive discipline matters too. When details change, move superseded files into a clearly marked archive subfolder instead of deleting them. Current files should be obvious at a glance, and historical versions should remain searchable if a platform or advisor asks what was on file earlier in the year.

Before item 5, confirm the following:

- Core tax-identification and registration records are current.

- If OSS is used, Member State of identification and OSS registration records are saved.

- OSS period files include invoices, required records, and any bad debt relief evidence.

- Submission log entries include date, entity, and document bundle.

With the files in place, timing becomes the next control. A solid evidence pack helps only if you review it before deadlines force rushed decisions.

Related: DAC7 for Platform Operators: Scope, Seller Data, and Controls for EU and Non-EU Platforms.

5) Run a Yearly DAC7 Calendar With Three Checkpoints#

Use three checkpoints each year as a practical baseline. These are internal controls, not statutory DAC7 deadline definitions. That gives you a repeatable review cycle without confusing OSS process timing with separate reporting deadlines.

| Checkpoint | When | Main review | VAT context |

|---|---|---|---|

| Checkpoint 1 | Start of the year | Reconfirm activity mapping from item 2 | Review whether your OSS setup changed, including whether your Member State of identification is still the right fit; in the Union scheme, some choices can bind you for the current calendar year plus the two following years |

| Checkpoint 2 | Mid-year | Compare platform profile fields with your evidence pack, including legal name, tax IDs, and jurisdiction fields where applicable | Confirm OSS administration is covered across registration, declaration and payment, with retained records for potential audits; document your scheme cadence (quarterly for Union/non-Union, monthly for import) |

| Checkpoint 3 | Before filing | Reconcile annual platform summaries against ledger totals and log unexplained variances | For planned complex cross-border transactions, decide whether to prepare a VAT Cross-border Ruling request in a participating EU country where you are VAT-registered |

This baseline helps if compliance work tends to drift toward filing season. The cost is a bit of calendar discipline. The payoff is smaller corrections, better documentation, and fewer year-end surprises. You are not trying to review everything all the time. You are creating three moments in the year when the right questions get asked before the file hardens.

Keep these three reviews as the base layer:

- Checkpoint 1 at the start of the year: reconfirm activity mapping from item 2, then review whether your VAT setup changed. If you use OSS, confirm your Member State of identification and scheme setup are still appropriate, and account for any multi-year binding effect on Union-scheme choices.

- Checkpoint 2 mid-year: compare platform profile fields with your evidence pack, including legal name, tax IDs, and jurisdiction fields where applicable. In the same pass, confirm OSS administration is covered across registration, declaration and payment, with retained records for potential audits, and that supplies in your chosen scheme are being captured through the OSS return.

- Checkpoint 3 before filing: reconcile annual platform summaries against ledger totals and log unexplained variances. For planned complex cross-border transactions, decide whether to prepare a VAT Cross-border Ruling request in a participating EU country where you are VAT-registered, following that country's national VAT ruling conditions.

Add extra reviews only if volume, country spread, or unresolved variances justify them. More frequent review is not automatically better. If the extra cycle does not change decisions or improve evidence quality, it is just more admin.

Put each checkpoint on your calendar with a short agenda and a folder link to the evidence pack. That small step improves follow-through because you are not hunting for files during the review window. Keep the agenda tight. The point is to confirm the map, the profile, and the tie-out, not to reopen every old question from scratch.

Assign an owner to each checkpoint, even if that owner is you. Define completion criteria before the year gets busy, including where outputs are saved and how open issues are tracked. A review is not complete because you thought about it. It is complete when the file, log, and open items are updated where you said they would be.

Before item 6, confirm the following:

- Three dated internal reviews are on your calendar for the current year.

- Each review has a short task list tied to evidence-pack folders.

- OSS scope and return cadence are documented for your scheme.

- Every open variance has an owner, due date, and saved support thread.

Once the calendar is set, the highest-value review is reconciliation. That is where inconsistencies stop being abstract and start showing up in the numbers.

If you are evaluating tooling, see Choosing DAC7 Compliance Platforms Without Overbuilding.

6) Reconcile Platform Reports Against Your Books Before Filing#

Do not treat platform annual statements as filing truth. Treat them as inputs that need to be tested against your books before anything is submitted.

Start from a frozen year-end file for each platform. Include the annual statement export, monthly payout reports, refund logs, fee summaries, your FX conversion method, and a chart-of-accounts mapping table. Then build one reconciliation table per platform and one consolidated view across all channels. If you keep working from live dashboards, it becomes much harder to explain why totals changed between review and filing.

Use this method:

- Include gross transactions, platform fees, refunds, net payouts, and ledger totals in original currency and base currency.

- Post adjustments as separate lines, not by editing source totals. Use labels such as

refund timing,non-platform invoice,currency remeasurement, andclassification correction. - Create two tie-outs from the same table: one to income tax working papers and one to VAT working papers.

- Close with a variance note. If any difference remains unresolved, record owner, due date, and filing impact before submission.

Run reconciliation in the same order every time: verify source totals first, post adjustments second, tie out to working papers third, then close open variances. That fixed sequence reduces missed steps when filing pressure rises. It also makes the file easier for an advisor or reviewer to follow, because they can see what was source data, what changed, and why.

If cross-border sales or services fall within OSS scope, keep a dedicated VAT tab aligned to what you declare through your Member State of identification. For any OSS scheme you use, declare all supplies covered by that scheme via the OSS return, and remember that OSS VAT returns are additional to domestic VAT returns. Do not blend that tab with income-tax categorization. The EUR 10,000 threshold applies only in specific VAT contexts, so note it only where it is actually relevant.

One common failure mode is assuming platform totals equal taxable totals without adjustment. Refund timing, cutoff differences, and off-platform revenue can all drive corrections. Use one hard control before filing: check that platform totals plus direct revenue tie to tax working-paper totals after documented adjustments. If they do not, you do not have a filing-ready number yet, no matter how polished the export looks.

Manual mapping can be tedious, especially when platform labels do not match accounting categories. Keep the final reconciliation file with your OSS records, since OSS includes record-keeping and audit expectations. If VAT treatment remains unclear in a complex cross-border case, assess whether a VAT Cross-border Ruling request is available in a participating EU country where you are VAT-registered and follow that country's national VAT ruling conditions. If multiple companies are involved, one company should submit on behalf of the others.

Finish each reconciliation with a short sign-off note stating what matched, what you adjusted, and what remains open. That note makes the file usable during advisor review and later checks. Once you can explain every variance, you are in a position to choose the lightest compliance setup that still fits your risk.

If you want one workspace for your country ties, filing notes, and evidence checklist before year-end reconciliation, use the Tax Residency Tracker.

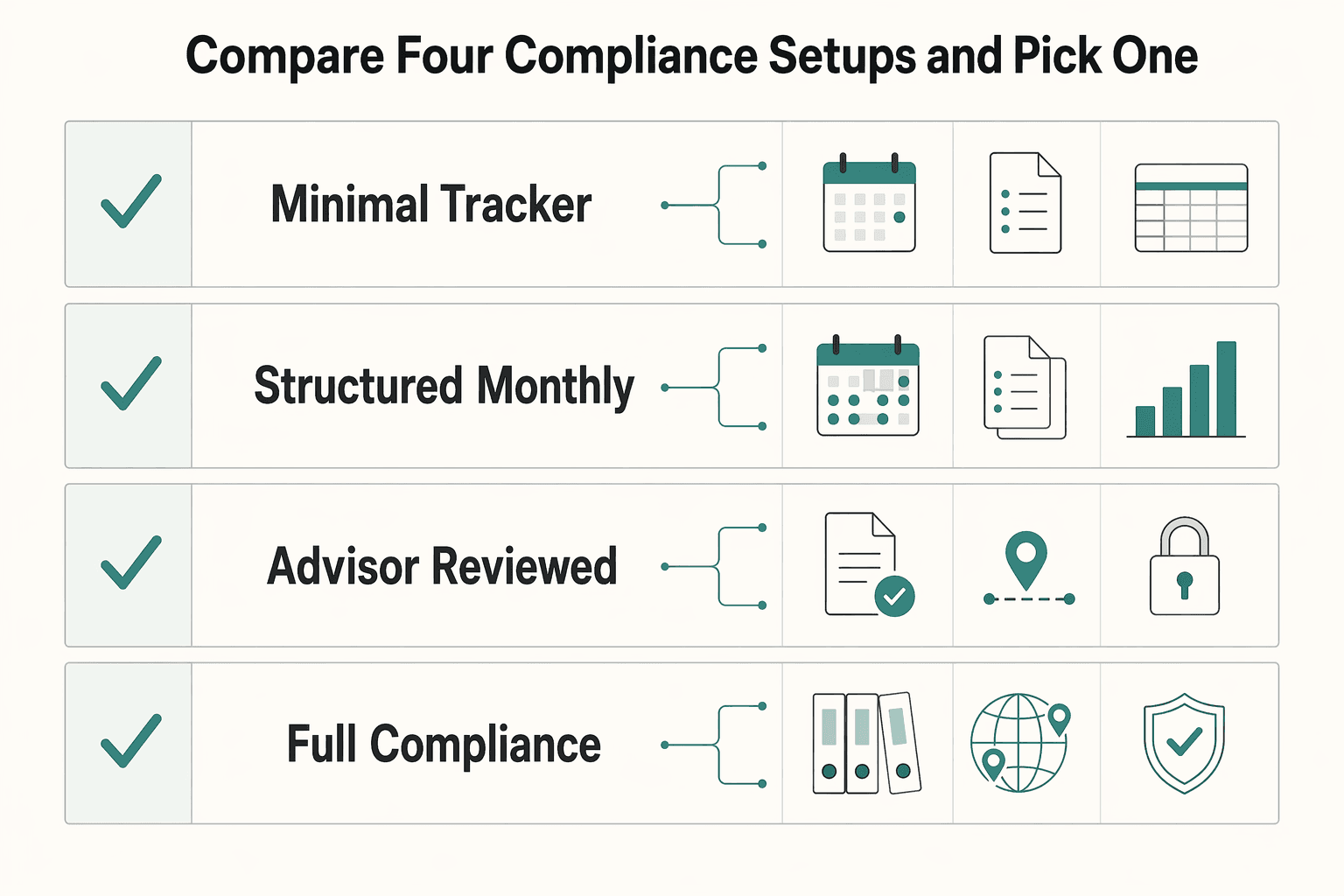

7) Compare Four Compliance Setups and Pick One#

Pick the setup that matches your current complexity, then move up only when the facts justify it. Choosing a setup is an operating decision, not a legal shortcut.

The real question is how much structure you need to keep records consistent without creating overhead you will not maintain. A setup that is too light can break once channels, countries, or currencies multiply. A setup that is too heavy can get abandoned mid-year. The right choice is the lightest option that still gives you clean evidence, workable reconciliation, and a clear escalation path when the facts turn.

Use this selector table. Keep the concepts separate: OSS is an optional filing route for covered supplies, while CBR is an advance-ruling path for complex cross-border VAT questions.

| Setup | Best for | Pros | Cons | Use-case trigger |

|---|---|---|---|---|

| Minimal tracker | One platform, one tax residence | Lowest admin load | Higher error risk if facts change | One platform, one-country tax position, and no unresolved variances after reconciliation |

| Structured monthly close | Multiple platforms or currencies | Better reconciliation history and audit trail | More monthly maintenance | You use OSS and need records that support one Member State of identification, including record-keeping and audit readiness |

| Advisor-reviewed quarterly | Multi-country activity with recurring VAT judgment calls | Stronger control when treatment is less clear | Advisory cost and quarterly prep time | You opted into an OSS scheme and need periodic checks that all in-scope supplies are reported through the relevant OSS return while domestic VAT returns stay on track |

| Full compliance stack | High-volume, high-complexity cross-border footprint | Strong defensibility across jurisdictions | Highest process overhead | Complex cross-border VAT questions across participating countries, including cases where a CBR request may be appropriate under national ruling conditions |

Run this lock-in check before choosing:

- Confirm platform count and country footprint for the current year.

- Confirm OSS records are complete and audit-ready.

- Confirm your OSS return cadence matches your scheme, quarterly for Union/non-Union and monthly for import, and that domestic VAT returns are still covered.

- Confirm whether your Member State of identification choice is binding in your case and whether OSS exclusion risk needs mitigation.

- Confirm whether any complex cross-border VAT issue should be escalated for a CBR path.

Do not treat the setup as permanent. Re-run the lock-in check when your country footprint, channel count, or transaction profile changes. Moving up one tier early can be cheaper than repairing a low-control setup after complexity has already increased.

If two setups seem viable, choose the one that gives you clearer monthly evidence rather than the one that saves a little admin time. In practice, stronger records reduce downstream cleanup effort. Once you know what level of process you are actually running, it becomes much easier to define when outside advice is necessary.

For a platform-side view of DAC7 alongside 1099 and W-8 workflows, see Gig Worker Tax Compliance at Scale: How Platforms Handle 1099s W-8s and DAC7 for 50000+ Contractors.

8) Use Clear Escalation Triggers for Professional Advice#

Use trigger-based escalation, not stress-based escalation. Bring in professional advice when the facts get complex, not when the deadline is already too close.

That keeps low-complexity years efficient and can reduce rework in cross-border years. It can feel overly cautious in a one-country year, but the downside is usually limited. Waiting too long is often the costlier mistake, especially when records already contain mixed channels, unclear platform roles, or unresolved VAT treatment across countries.

Escalate when any of these are true:

- A cross-border transaction involves two or more participating EU countries and the VAT treatment is unclear.

- OSS scope is near or unclear. If you are close to the EU-wide EUR 10,000 threshold or unsure how it applies to your supplies, escalate before filing. If you must choose a Member State of identification among multiple fixed establishments, that choice is binding for the current calendar year plus the two following calendar years.

- Complex cross-border VAT treatment is unresolved. Consider a CBR request for advance treatment on complex transactions involving participating EU countries. Introduce the request in the participating EU country where you are VAT-registered, and follow national VAT ruling conditions there.

- VAT records do not reconcile cleanly. Escalate when OSS registration, declaration and payment records, regular VAT returns, or required record-keeping are inconsistent or incomplete.

If multiple companies are involved in a CBR request, one company should submit on behalf of the others. Keep the escalation packet short and complete:

- Current-year transaction summaries and reconciliation tables.

- Relevant VAT filing records, including regular VAT returns and OSS VAT returns.

- OSS records for registration, declaration and payment, and record-keeping.

- A one-page issue log with trigger, countries affected, open question, and deadline.

Before contacting an advisor, write the issue in one paragraph with the facts, the open point, and the filing deadline. That makes the first conversation more productive and reduces the chance of getting a vague answer that still leaves you uncertain about the next step.

When you do contact an advisor, ask first for a direct yes or no on the immediate filing decision, then ask for the assumptions behind that answer. That keeps the discussion practical and makes follow-up easier if the facts change. The questions below cover the points most likely to remain unclear when you rely on public summaries alone.

Conclusion#

Disciplined records and early escalation can reduce compliance risk.

The throughline is simple:

- Confirm your exposure before you start.

- Classify income lines consistently so reconciliation stays clean.

- Verify the platform legal entity in each channel and save dated evidence.

- Reconcile early, not under filing pressure.

- Escalate unresolved items before they harden into a filing position.

For VAT process handling, keep the OSS and CBR lanes from the earlier sections separate from DAC7 decisions. OSS can simplify multi-country administration through one Member State of identification, but OSS returns are additional to domestic VAT returns, not a replacement for them.

Apply this framework to your residency context with The Ultimate Digital Nomad Tax Survival Guide for 2025 and Taxes in Germany for Freelancers and Expats.

If cross-border treatment, platform entity ownership, or reconciliation still does not resolve cleanly, review the FAQ and escalate to a qualified advisor with your evidence pack before filing.

For related reading, see Freelancer Decisions Under the EU Platform Work Directive.

If your platform, residency, and payout setup still has unresolved edge cases, talk to Gruv to review a compliance-aware operating workflow for your context.

Frequently Asked Questions

Do I need to think about DAC7, VAT, or both?

Treat DAC7 and VAT as separate tracks, even when the same platform income appears in both. Keep VAT points in the VAT column: OSS is optional, OSS returns are additional to domestic VAT returns, and the EUR 10 000 threshold is a VAT threshold in specific cross-border B2C contexts. Keep DAC7 applicability in a separate review column and verify it from official records before you rely on the classification.

If a platform processes the sale, is it automatically the reporting platform operator?

Not necessarily. For VAT, a platform can be treated as a deemed supplier in some cases, and platforms can still have record-keeping duties when they are not the deemed supplier. Do not treat sale processing as proof of DAC7 reporting-operator ownership. Verify the contracting legal entity in platform terms and payout records, save dated evidence, and ask support which entity handles seller reporting. If your remaining issue is non-EU platform scope, review Does Your Non-EU Marketplace Owe DAC7 Tax Reporting in Europe?.

How should I label my freelance activity when public summaries use different categories?

Do not invent DAC7 legal categories from summaries, and do not reuse VAT labels as if they were DAC7 labels. Keep any DAC7 activity taxonomy unresolved until the label is verified from official records; the EUR 10 000 figure is a VAT threshold, not a DAC7 activity test. Use one plain-English internal label per income line, keep it consistent across invoices and books, and attach supporting evidence for lines that may be questioned later.

Why do online explanations use different start dates and deadlines?

Some guides mix VAT milestones with platform-reporting topics, which creates timeline confusion. Keep VAT dates and DAC7 implementation dates in separate source columns, then verify each from official records before use. Record unresolved items as "Current DAC7 implementation timeline pending official verification" and "Current threshold pending official verification."

When should I stop researching and ask a professional?

Escalate when the answer could change your filing position, not when you are near the deadline. On the VAT side, one practical trigger is Union-scheme OSS identification choices that, in specific establishment scenarios, can bind you for the calendar year plus two following years. Another is unclear VAT treatment of a foreseen cross-border transaction where a CBR request may be available under national VAT-ruling conditions in a participating EU country where you file. If records do not reconcile, or the platform role or entity is still unclear, escalate with a tight evidence pack: platform exports, invoices, reconciliation notes, any OSS filings, and a one-paragraph issue summary with deadline.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

Digital Nomad Taxes in 2026 With a Defensible Filing Plan

With digital nomad taxes, the first move is not optimization. It is figuring out where you may be taxable, where filings may be required, and what proof supports that position.

Taxes in Germany for Freelancers and Expats

Low-stress compliance in Germany comes from decision order, not tax tricks. Use this sequence: confirm core facts, apply conservative temporary assumptions, verify the few points that can break invoices or filings, and keep one evidence file that explains each decision.

CCPA for Freelancers Handling California Client Data

Privacy risk is delivery risk for many freelancers who handle client data. The practical move is to assess likely CCPA exposure early and put baseline controls in place before a client issue forces rushed decisions.