Quick Answer

Start with the IRS-hosted treaty packet: for us india dtaa independent personal services, confirm Article 4 residence first, then classify your facts under Article 15 or Article 16. Build one evidence file that ties contracts, travel, invoices, and payment records to the same filing period, and keep Form 8938 and FBAR conclusions separate. If that chain does not reconcile, pause DIY filing and seek specialist review.

How the US-India DTAA Applies to Freelance Services#

Start with the treaty text before you decide anything. For us india dtaa independent personal services, use this order. Open the U.S.-India Tax Convention PDF, then the Technical Explanation. The Technical Explanation states that it is an official guide to the Convention.

Then make the lane decision in sequence, not from contract labels or form pressure. First, confirm your treaty residency position under Article 4 (Residence). Next, classify your service facts under Article 15 (Independent Personal Services) or Article 16 (Dependent Personal Services). After that, draft invoices, filing narratives, and any relief position so they all reflect the same fact pattern.

Use this article the same way:

- Check source hierarchy first and trust only summaries you can trace back to treaty materials.

- Confirm your treaty lane from facts, not assumptions.

- Build a baseline evidence file early: your residency position, service documents, invoices, payment records, and the treaty passages you relied on.

- Set an escalation trigger now: if residency is unclear, records conflict, or your conclusion is hard to map to treaty text, pause and get specialist review.

For orientation only, the Convention and Protocol were signed on September 12, 1989, and the treaty lists a general effective date under Article 30 of 1 January 1991. That context helps, but your filing position still depends on the treaty articles and Technical Explanation language that fit your facts.

The operating rule for the rest of this guide is simple: tell one consistent story across residency, contracts, invoicing, and filings. A quick check is to compare the same service period across those records and fix mismatches before filing. If you want a broader workflow, use our digital nomad tax guide. You might also find this useful: Understanding the Independent Personal Services Article in Tax Treaties.

Start with the right legal sources before you decide anything#

Use a consistent source order before you interpret anything. Start with the IRS India treaty documents page, then the treaty PDF, then the Technical Explanation, and only then use secondary summaries for context.

| Source | Use | Detail |

|---|---|---|

| IRS India treaty documents page | Start here | Says complete treaty document texts are available in PDF; page reviewed 08-Aug-2025 |

| India Income Tax Treaty PDF | Read first after the source page | Linked from the IRS India treaty documents page |

| India Technical Explanation PDF | Read after the treaty PDF | Linked from the IRS India treaty documents page |

| Treaty timeline details | Record key dates from treaty materials | Signed September 12, 1989; entered into force December 18, 1990; general effective date under Article 30: 1 January 1991 |

| Secondary explainers | Use last | Only after key claims map back to treaty instruments |

Begin on the IRS India treaty documents page. It says complete treaty document texts are available in PDF. It links the India Income Tax Treaty PDF and India Technical Explanation PDF. The page also shows a last reviewed date of 08-Aug-2025.

Save those details so your position is traceable, then follow the same sequence each time:

- Confirm you are in the IRS India treaty document set.

- Read the India Income Tax Treaty PDF first, then the India Technical Explanation PDF.

- Record treaty timeline details from treaty materials, including the signing date (September 12, 1989), entry-into-force date (December 18, 1990), and general effective date under Article 30 (1 January 1991).

- Use secondary explainers only after key claims map back to treaty instruments.

Keep signing and entry-into-force dates separate in your notes. They mark different milestones, not a contradiction.

Resolve scope before detail. If residency is unclear, settle treaty residence first, including Article 4 tie-breaker analysis in dual-resident scenarios, before you move into article-level interpretation.

Treat secondary content as interpretation, not authority. If a precise claim cannot be tied to treaty text or the Technical Explanation, treat it as unverified and keep it out of your filing logic. Also check saving-clause context before relying on treaty relief, because a contracting state may still tax its residents or citizens. Escalate early if any of these show up:

- Your notes mix signing and legal-effective dates without explanation.

- A secondary source makes a precise claim you cannot find in treaty documents.

- Your records do not show which passages support your conclusion.

One extra control is worth using. For each important statement you plan to use in a form narrative, capture the treaty passage first, then write your own plain-language summary under it. If your summary includes detail that is not visible in the treaty passage or Technical Explanation, treat that detail as provisional. Remove it from the filing draft until you confirm it. That keeps commentary in the right place and prevents overconfident wording.

Build the mental model before tactics#

Before you touch forms, build a one-page decision map that separates treaty lineage, article lane, residency gate, and relief objective.

| Decision block | What to write now | What to avoid |

|---|---|---|

| Treaty lineage | Primary treaty documents used first, secondary materials used only for orientation | Treating orientation material as treaty authority |

| Article lane | Provisional lane based on facts (Article 15 vs Article 16) | Picking a lane from a heading alone |

| Residency gate | Whether residency facts are clear enough to proceed | Forcing article analysis while residency is unresolved |

| Relief objective | The exact relief outcome you are testing | Drafting form language before logic is stable |

Keep the lineage note short#

Your lineage note should stay brief: which primary treaty documents you relied on first, and which secondary guides you used only for context. As an orientation checkpoint, the OECD 2025 update lists separate commentary entries for Article 15 and Article 16, so treat them as distinct analytical lanes, not interchangeable labels. That is context, not binding law for this treaty.

If your residency facts are still split across countries or dates, pause there and resolve them first before forcing a treaty position.

Choose a path from facts, not headings#

Before any relief claim, write a short self-classification memo. It should cover the service facts, the control pattern, and the gap between contract wording and what actually happened in practice:

- Service facts: what you delivered, where you performed it, and how the work pattern actually looked

- Control pattern: who set hours, methods, review rights, and day-to-day direction

- Contract reality: what the contract says versus what happened in practice

The goal here is not a final legal conclusion. It is a defensible provisional lane, the facts that support it, and the items still open.

Mark unresolved risk instead of smoothing it over#

If fixed base or PE exposure is unclear, say so directly. The materials here do not provide treaty-specific thresholds, so do not invent bright-line tests. Instead, mark unresolved items in your lane memo, such as repeated use of one location, local meeting patterns, or signing authority you have not verified.

If you cannot reconcile lane, residency, and relief logic in one memo without gaps, stop DIY filing and escalate to qualified U.S. and in-country Indian advisers.

Decide your likely treaty position in the right order#

Work in sequence, not by urgency: confirm residence, classify services, run a preliminary fixed-base screen, then map relief. If one step conflicts with another, pause before finalizing your filing position.

| Step | Focus | Key note |

|---|---|---|

| 1 | Article 4 gate | Confirm your residence position for the relevant period and document that basis before finalizing your filing position |

| 2 | Service classification | Choose between Article 15 (Independent Personal Services) and Article 16 (Dependent Personal Services) based on actual facts, not just contract wording |

| 3 | Fixed-base screen | This material does not include full fixed-base criteria, so avoid absolute conclusions when facts are mixed or records are incomplete |

| 4 | Relief mapping | Build a preliminary map of where income may be taxed and where relief may apply, then check saving-clause limits before final conclusions |

Step 1 is the Article 4 gate. Since the convention applies to persons who are residents of one or both contracting states, confirm your residence position for the relevant period and document that basis before you finalize your position. Use the same period labels everywhere so month ranges, invoice ranges, and filing periods line up.

Step 2 is service classification by actual facts. Article 15 and Article 16 are separate lanes, so choose the lane your actual delivery pattern supports, not the one your contract heading suggests. If contracts and delivery records point in different directions, document the conflict and resolve it before you draft final narratives.

Step 3 is the fixed-base screen. Treat it as a caution point. This material does not include full fixed-base criteria, so avoid absolute conclusions when facts are mixed or records are incomplete. A forced conclusion here can create rework across treaty notes and filing records.

Step 4 is relief mapping. Build a preliminary map of where income may be taxed and where relief may apply, then align your filing artifacts to that map using the full treaty text and your facts. Also keep in view that treaty benefits are not absolute, since Article 1(3) allows a contracting state to tax its residents and, by reason of citizenship, its citizens.

A practical checkpoint is a two-column draft before final filing. In one column, list each key fact used to support your treaty lane. In the other, list each filing location where that fact appears. If a key fact appears in one place but disappears in another, fix the mismatch before submission.

Decision rule: if residency evidence and service classification point in different directions, do not file until the position is reconciled with a cross-border professional. Related: US-Australia Tax Treaty Independent Personal Services for Freelancers.

Test fixed base and Permanent Establishment exposure with real scenarios#

Stress-test your facts before filing. Repeated, locally anchored delivery can increase taxable presence risk, including potential fixed base or Permanent Establishment concerns.

Use this contrast to pressure-test your file before you decide whether your records support a lower-risk or higher-scrutiny posture:

| Scenario | What your records usually show | Review posture |

|---|---|---|

| Short remote consulting, no local setup | Work performed mostly outside India, limited travel, invoices tied to remote milestones, no recurring local work location | Lower apparent fixed base and Permanent Establishment pressure, but still requires complete records |

| Repeated in-country delivery | Regular client-site presence, recurring workspace use, invoices tied to on-site execution, repeated local-facing activity | Higher scrutiny risk and stronger need for specialist review before relying on treaty relief |

Treat the following as risk signals, not automatic legal conclusions:

- Recurring physical workspace use in India across months.

- A local operational footprint that supports ongoing delivery, not occasional visits.

- Repeated client-facing presence tied to core service performance.

- Contract language says remote advisory work while calendars and invoices show regular in-country execution.

Build one fact timeline that reconciles contracts, travel, and billing. Include contract start and change dates, entry and exit dates, meeting logs, and invoice periods. Then map each invoice to where services were performed. If any billed period cannot be matched to both a location record and contract scope, mark it unresolved and pause the treaty narrative.

Anchor interpretation to treaty records and to the substance of how work was performed. A carefully worded contract, or the absence of a formal office by itself, is not enough to rule out Permanent Establishment risk.

A practical failure mode is partial matching. For example, travel and contracts may be reconciled while invoice descriptions are not, or invoices and contracts may be reconciled while meeting logs are not. Do the full match in one pass. If an on-site week appears in meeting logs, make sure invoices and contract scope language can explain it without contradiction. If they cannot, treat the item as open and hold filing until resolved.

The tradeoff is practical. An aggressive reading may reduce near-term tax friction, but it can also increase audit and dispute risk when facts are mixed. If your timeline, records, and service narrative do not align, reconcile them with a cross-border specialist before filing.

This pairs well with our guide on The Role of a Permanent Establishment in International Tax.

Build a documentation pack that survives review#

A documentation pack is ready only when a reviewer can verify, quickly, what is documented in the file set, what is missing, and what remains unknown. If any required link is missing, pause filing.

| Audit question | Where it is documented | How it supports your filing position |

|---|---|---|

| What was agreed, and from when? | Signed master agreement, referenced Statements of Work, referenced appendices/exhibits/attachments, and the Effective Date | Anchors service scope and timeline from the contract record |

| Who are the parties? | Agreement header party names and business address details | Provides a concrete identity checkpoint |

| Is service scope fully evidenced? | Statements of Work referenced by the master agreement | Missing SOWs mean service-level evidence is incomplete |

| Are treaty-specific filing rules proven here? | Not established by these excerpts | Keep treaty tests, withholding rules, and filing thresholds as open items until separately verified |

Minimum viable evidence pack#

At minimum, keep:

- Signed master agreement with Effective Date and party identity details.

- Every referenced SOW available in your file set, or an explicit gap note if any are missing.

- Every appendix, exhibit, or attachment referenced as accepted in the agreement.

- One index that cross-references related files and clearly marks missing documents.

- One short "unknowns" note for treaty-specific requirements not established by these excerpts.

Use the agreement's Effective Date as your index anchor. In the provided contract excerpt, that anchor is May 7, 2025. If services are defined in one or more SOWs, missing SOWs mean the service-evidence chain is incomplete.

Index the pack so reconciliation is fast#

If you want fast review, indexing matters. Use one consistent naming pattern, for example: YYYY-MM-DD_DocType_Client_Period_v01_XREF-ID.

Each file should carry the same four fields so a reviewer can sort the pack without guessing:

- Date + document type

- Version marker (

v01,v02) - Effective or covered period

- Cross-reference ID shared across related records

If a file uses XREF-MSA-2025-05-07, the related SOW and referenced attachments should use that same ID. Also index referenced appendices and exhibits instead of leaving them outside the pack.

Verify in one fixed sequence#

- Identity

Confirm party names and entity details match across the agreement and its referenced documents. The agreement header is a concrete checkpoint because it contains party identity details.

- Period and scope

Match the Effective Date and your covered period, then confirm scope statements are supported by available SOWs. If records conflict or SOWs are missing, stop and resolve the issue before filing.

- Cross-reference completeness

Verify each referenced appendix, exhibit, attachment, and SOW is present in the indexed pack. If a referenced file is absent, the pack is not review-ready.

- Narrative consistency and uncertainty

Read memo claims line by line against the contract file set. If a memo claim is not document-backed, or depends on treaty-specific rules not shown here, treat it as unresolved.

Apply one rule throughout: if any link fails, stop and escalate. Typical triggers are missing SOWs, missing referenced attachments, conflicting party details, or memo language that cannot be traced to the file set. Do not treat this SEC contract excerpt, the 2021 Senate hearing record, or the 1967 IMF policy article as operative filing instructions for current treaty compliance.

Execute India-side treaty relief without last-minute chaos#

To reduce last-minute issues, prepare one reconciled package before submission. If forms and schedules are built in isolation, contradictions are harder to catch and fix.

Anchor each claimed item to one chain: treaty position, tax-position logic, and supporting records. If the same income is described differently across forms or schedules, stop and fix the mismatch.

Use a simple reconciliation sheet so every claimed item ties back to one record set. Include four fields:

- Claimed item or amount

- Where it appears in your filing set

- Short note on treaty-position logic

- Source record reference: invoice, payment proof, contract section, or memo

Before submission, run a line-by-line check across your filing set and the evidence pack. Keep wording, period coverage, and identity details aligned everywhere.

Keep authority boundaries clear. These extracts do not provide definitive India-side procedural mechanics, so confirm current filing instructions before submission. For U.S. withholding and reporting checkpoints in this evidence set, rely on Publication 515 (2026): determination of amount to withhold, when to withhold, Forms 1042 and 1042-S reporting obligations, and liability for tax.

Treat weaker references carefully during final checks. One secondary source in this set is inaccessible, so do not use it to resolve filing ambiguity when primary instructions are available. If another source warns that parts may include unverified LLM-generated content, do not rely on that summary to close a filing gap.

As an internal review workflow, you can use a simple sequence: draft, reconcile, then finalize. Draft with provisional notes, reconcile against your evidence pack, then finalize only after every line item has a clear record tie-out. That helps reduce last-minute edits that introduce accidental inconsistency between forms and schedules.

Decision rule: if any one form or schedule cannot be reconciled to your treaty position and records, do not file yet.

Cover the U.S. forms freelancers most often miss#

The common miss here is straightforward: Form 8938 and FBAR (FinCEN Form 114) are separate U.S. reporting decisions, and each needs its own documented conclusion.

Keep the same discipline across both filings: one fact pattern, one asset register, and no contradictions across forms.

Keep the two filing decisions separate#

Form 8938 is filed with your annual income tax return and is due with that return, including extensions. FBAR is a separate FinCEN filing requirement. You may need both, and the penalties are separate if you miss each one.

Do not hardcode a single threshold in your notes. Leave the threshold unresolved until you verify it for the filer profile, filing status, and current IRS instructions, then record the source you used.

| Filing decision | Who files | Where filed | Assets in scope | Record evidence to keep |

|---|---|---|---|---|

| Form 8938 (specified individual) | Specified individual, if the verified threshold is met for that filer profile and filing status | Attached to the annual income tax return | Specified foreign financial assets, including foreign financial accounts and certain non-U.S. financial interests held for investment | Account statements, ownership support, valuation support used for threshold testing, acquisition/sale notes, and any exception memo |

| Form 8938 (specified domestic entity) | Certain domestic corporations, partnerships, and trusts formed or availed of to hold specified foreign financial assets, if the verified threshold is met | Attached to the annual tax return | Same Form 8938 asset category | Entity and ownership records, valuation support, filer-type analysis, and exception rationale |

| FBAR (FinCEN Form 114) | Separate foreign-account reporting determination; some filers need this in addition to Form 8938 | Filed separately as FinCEN Form 114 | Foreign accounts subject to FBAR reporting | Account inventory, ownership/authority notes, and written inclusion/exclusion logic |

Run one asset register workflow#

The practical move is to run one asset register for both decisions instead of two separate checklists. For each account or asset, track:

- legal owner, and entity owner where relevant

- asset type and institution or issuer

- valuation basis used for your threshold analysis

- Form 8938 treatment

- FBAR treatment

- exception or exclusion rationale

- whether the asset was acquired or sold during the year

This is what makes your file review-ready. Form 8938 includes inventory and lifecycle checkpoints, such as account-count fields and whether assets were acquired or sold during the year, so your register should tie directly to those entries.

If you are not required to file an income tax return for the year, document that and record why Form 8938 is not filed for that year. If your return obligation is still unclear, run that determination first using a broader residency workflow like The Ultimate Digital Nomad Tax Survival Guide for 2025.

Escalation rule: if you cannot reconcile asset classification, verified threshold profile, and Form 8938 or FBAR treatment in one consistent register, stop DIY and get specialist review before filing. Related reading: A Freelancer's Guide to the US-Germany Tax Treaty.

Know the red flags that mean stop DIY and hire a specialist#

Escalate when your facts or filings are not consistent enough to support one treaty position.

| Red flag | What is unclear or inconsistent | Action |

|---|---|---|

| Form 8233 treaty terms unclear | You cannot clearly apply the treaty terms needed to complete Form 8233 correctly | Get specialist review before filing |

| Residency facts unclear | Possible dual-residency issues require Article 4 analysis | Get specialist review before filing |

| U.S. office or fixed base possible | You may have an office or fixed base available to you in the United States | Get specialist review before filing |

| Form 8233 process inconsistent | Separate forms by tax year, withholding agent, and type of income are not being handled | Get specialist review before filing |

| Forms and withholding do not align | Your forms and withholding position do not align with the treaty terms you are claiming | Get specialist review before filing |

| Relying on summaries | You are relying on summaries instead of the treaty text, Technical Explanation, and current Form 8233 instructions | Get specialist review before filing |

Red flags that should trigger specialist review before filing:

- You cannot clearly apply the treaty terms needed to complete Form 8233 correctly.

- Your residency facts are unclear, including possible dual-residency issues that require Article 4 analysis.

- You may have an office or fixed base available to you in the United States.

- Your Form 8233 process is inconsistent, including not handling separate forms by tax year, withholding agent, and type of income.

- Your forms and withholding position do not align with the treaty terms you are claiming.

- You are relying on summaries instead of the treaty text, Technical Explanation, and current Form 8233 instructions.

Treaty-based withholding relief exists, but it is conditional and form-driven. If exemption is not secured, withholding can default to 30% under section 1441. If your facts cannot be explained as one coherent, fact-based position across those materials and your filings, pause and hire a specialist.

When you do escalate, hand off organized records and a clear list of unresolved questions so a specialist can focus on the key issues quickly.

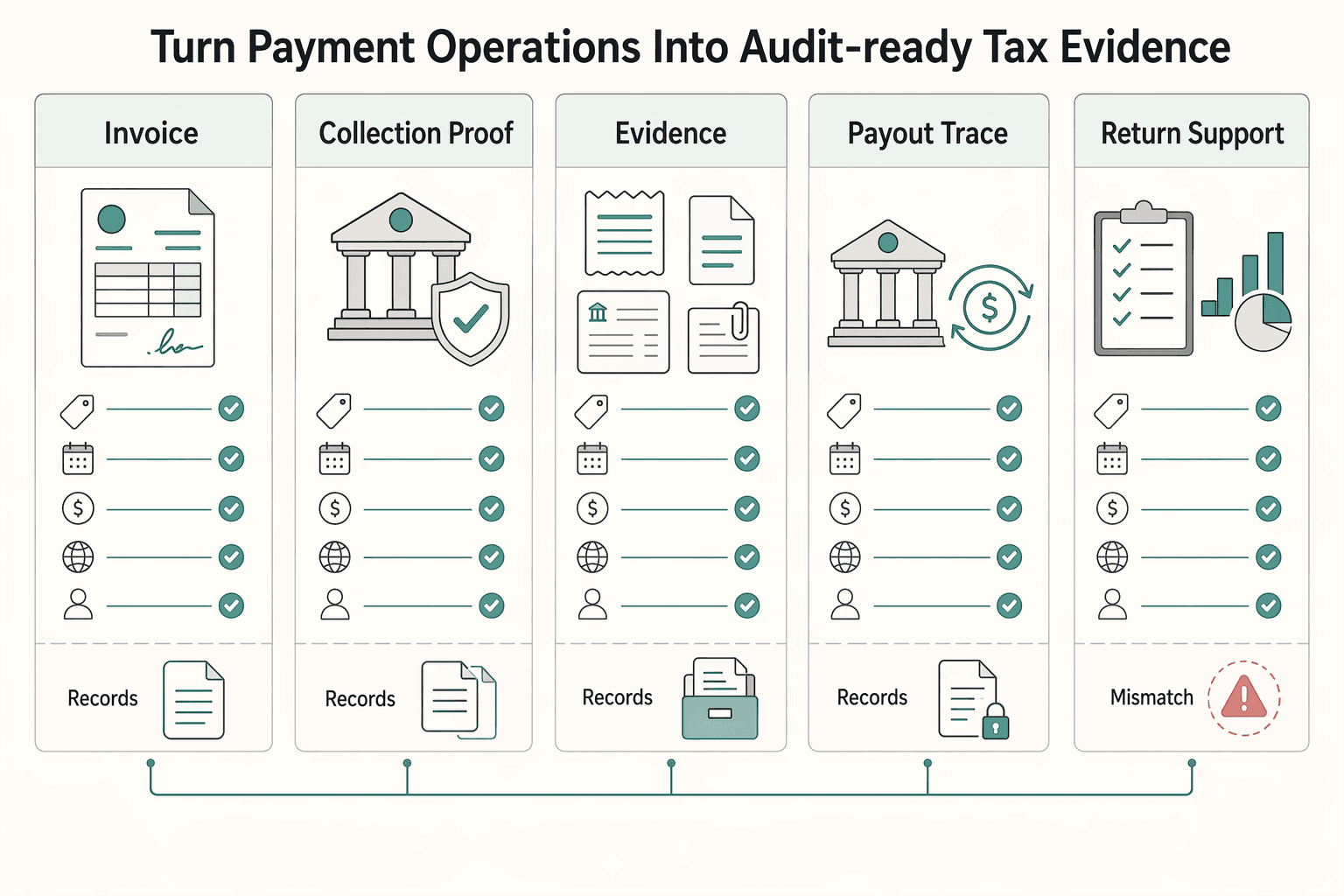

Turn payment operations into audit-ready tax evidence#

Money flow often decides whether a technically good position survives review. Set one practical standard: a reviewer should be able to follow money from invoice to filing position in one pass.

Use one traceable chain for each engagement: invoice, collection, payout, and ledger record. Keep IDs, dates, amounts, currency, and payer or payee names consistent across each record type, because mismatches can undermine an otherwise defensible tax position.

Build the evidence pack around matching fields so the same facts repeat cleanly across every record:

| Record | What should match across the pack |

|---|---|

| Invoice | Invoice ID, service dates, legal payer name, amount, currency |

| Collection proof | Date received, amount received, payer reference |

| Payout record | Date, amount, account owner, transfer reference |

| Ledger export | Invoice ID, payer/payee history, service date mapping |

| Return support docs | Identity details and narrative language consistent with the same records |

Keep foreign-asset reporting on a separate track, tied to the same underlying records. Form 8938 is attached to the annual income tax return for certain U.S. taxpayers when specified foreign financial assets exceed the applicable threshold. Those assets include foreign financial accounts maintained by a foreign financial institution and certain foreign investment assets not held in a financial account. Account classification matters, because some accounts are excluded from Form 8938 reporting.

Use explicit threshold checkpoints. IRS guidance includes a $50,000 trigger for certain taxpayers, but you still need to verify the rule that matches your filer profile. If no income tax return is required for the year, Form 8938 is not required for that year.

Before filing, run this checkpoint list:

- Confirm each foreign account is either reported where required or documented as out of scope.

- Reconcile balances used for threshold testing to underlying records.

- Confirm Form 8938 inclusion status is documented.

- Lock a read-only copy of the final evidence pack before submission.

A monthly close discipline can make year-end filing much easier. Reconcile invoice IDs, payment proofs, and ledger exports each month, then archive a dated snapshot. By filing season, you should be reviewing complete packs, not rebuilding missing links from old emails and bank notes. That helps reduce last-minute errors and rework.

For a step-by-step walkthrough, see Assessing Services PE Clause Risk Under Tax Treaties for Cross-Border Consultants.

Conclusion#

For a us india dtaa independent personal services filing, the goal is consistency, not a clever interpretation. Keep the same operating stance throughout: use primary sources first, classify conservatively, and make sure your records, treaty reading, and filed positions all align.

Before filing, do one final source check on the IRS India treaty documents page, then verify your position against the treaty text and the Technical Explanation. If your Article 15 conclusion sounds plausible in a summary, but you cannot tie it to treaty text or show how Article 4 residence supports it, treat that as a no-go.

Before you file, use this final go or no-go sequence:

- Confirm the current IRS treaty page status, and save the exact treaty PDF and Technical Explanation you relied on.

- Confirm your Article 4 residence memo still matches your filing-year facts, especially if domestic-law tests could make you resident in both states.

- Reconcile service classification, contracts, invoices, travel timeline, and payment records into one treaty narrative.

- Reconcile U.S. reporting positions with your India-side filing position, and review Publication 901's treaty-based disclosure item when your position reduces tax.

- Escalate anything you cannot explain clearly in writing.

Contradiction chains can create filing risk even when one document looks complete. If your residency facts, classification, and filing narrative still do not match cleanly, pause submission and get specialist review before filing. For mobility record hygiene, use this companion digital nomad tax guide. If you want a second review of your evidence pack and treaty position, Talk to Gruv.

If your treaty position is still unclear after your contradiction check, talk to Gruv to pressure-test your compliance workflow.

Frequently Asked Questions

What should I open first before deciding a treaty position?

Open the IRS-hosted India treaty PDF first. Use its Table of Articles to confirm Article 4 (Residence), Article 5 (Permanent Establishment), Article 15 (Independent Personal Services), Article 16 (Dependent Personal Services), and Article 25 (Relief from Double Taxation) before you rely on any summary. Save the exact PDF version you used and log page references in your evidence pack. For broader planning context, use this companion digital nomad tax guide.

Does Article 15 mean freelancer income is always taxed only in the country of residence?

Not necessarily. Article 15 is a treaty lane, not an automatic residence-only outcome. The treaty also separately names Article 25 on relief from double taxation, which is a reminder not to force the full result from one heading alone. Map your facts to the treaty text and keep a short memo explaining why your Article 15 position fits that filing period.

Do I need to check residence before I decide between Article 15 and Article 16?

Yes, check residence first. Article 4 is a separate Residence article, so your residence facts should be consistent before you finalize services classification. Prepare a dated residency memo and keep the same story across contracts, invoices, payment records, and the return narrative. If Spain is part of your setup, compare that workflow with this guide to the autónomo system for freelancers in Spain.

How do I choose between Article 15 and Article 16 in practice?

Choose the lane using facts, service type, and evidence, not contract labels alone. Article 15 and Article 16 are separate treaty articles, so your classification should match how the work was actually performed. If your records support both lanes, or you cannot explain your choice clearly, escalate before filing.

What should I do if fixed base or Permanent Establishment exposure is unclear?

Treat unclear exposure as a filing risk that needs resolution. Article 5 is separately titled Permanent Establishment, so build a timeline that aligns work location, dates, contracts, invoices, and payment timing. If location evidence and money records do not reconcile, pause DIY and get specialist review.

Why is the article title alone not enough for a U.S. filing position?

Because treaty headings are labels, not the full analysis. The treaty packet also identifies the Saving Clause as Paragraph 3 of Article 1, which is a clear reminder to read beyond titles. Trace each key sentence in your filing narrative to saved treaty text, or remove that sentence.

Which document checkpoints and dates should I keep in my file?

Keep the exact treaty PDF you relied on as your primary checkpoint document. The IRS-hosted packet states the convention was signed at New Delhi on September 12, 1989, and gives a general effective date under Article 30 of 1 January 1991. Store a read-only copy with highlighted passages and a short note on why that version supported your filing-year position.

Can I rely on blog summaries or advisory articles if they are easier to read?

Use summaries as commentary, not primary authority. Your filing position should still trace back to treaty text and your own records without guesswork. If a summary gives a conclusion you cannot tie to primary materials, treat it as a prompt to verify, not a rule to file on.

When should I stop DIY and hire a specialist?

Stop DIY when you cannot classify income cleanly, your residence story conflicts across records, or your result depends on treaty mechanics you cannot tie to primary text. The 2025 National Taxpayer Advocate report highlights severe compliance burdens and long delays and hardships in IRS processes, so unresolved contradictions can become expensive. Bring a specialist your treaty excerpts, contracts, travel timeline, invoices, payment proof, and contradiction log so they can review the facts quickly.

Try a related tool

Tomás breaks down Portugal-specific workflows for global professionals—what to do first, what to avoid, and how to keep your move compliant without losing momentum.

With a Ph.D. in Economics and over 15 years of experience in cross-border tax advisory, Alistair specializes in demystifying cross-border tax law for independent professionals. He focuses on risk mitigation and long-term financial planning.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

Digital Nomad Taxes in 2026 With a Defensible Filing Plan

With digital nomad taxes, the first move is not optimization. It is figuring out where you may be taxable, where filings may be required, and what proof supports that position.

Tbilisi Digital Nomad Guide for 2026 Long Stays in Georgia

Start with sequence, not excitement. If your income depends on delivering work on schedule, secure your legal footing, assemble your documents, and keep month one reversible before you optimize comfort.

Spain Autonomo System for Freelancers Who Want Compliance Control

Low-stress compliance comes from predictable execution, not tax-shortcut bets. Keep filings clean, document decisions, and set escalation triggers before deadlines.