Quick Answer

A platform files Form 1042-S only if it is the withholding agent for payments to a foreign person. Determine which entity controls payment and withholding, classify each payment as U.S.-source FDAP, ECI, or non-U.S.-source, tie every reportable row to the supporting tax documents, and reconcile Form 1042-S with Form 1042. Reporting may still be required even when no tax is withheld.

When platforms need to issue Form 1042-S#

The core question is simple: is your entity acting as a withholding agent for payments to a foreign person, and if so, does that create a Form 1042-S duty? This guide helps you answer that question, document the support behind it, and escalate early before a weak assumption becomes a filing problem.

If you work in compliance, legal, finance, tax, or risk, you may need to connect policy to what actually happens in the payment flow. For contractor, seller, and creator payouts, responsibility can be split across teams and entities. That is why 1042-S mistakes often start small and surface late.

Start with current IRS materials#

Use IRS definitions and current instructions as your baseline. This is an operational guide anchored to IRS materials, not legal advice. Your team should confirm current filing details in the live Instructions for Form 1042-S before filing.

Identify withholding-agent status first#

Start with withholding-agent status, not platform labels. The IRS says Form 1042-S is used by a withholding agent to report certain income paid to addresses in foreign countries, and IRS guidance says every withholding agent must file. That status turns on control, receipt, custody, disposal, or payment, not on whether the business calls itself a marketplace, processor, or platform.

Your first checkpoint is to identify the entity that actually controls the payment and withholding decision for the flow. If that ownership is unclear, escalate it before anything else.

Define the reporting question before collecting documents#

Define the reporting question before you collect more paperwork. IRS small-business guidance says nonemployee compensation paid to nonresident aliens is reported on Form 1042-S. But "foreign contractor" alone is not enough. You still need to characterize the payment correctly, including whether it is U.S.-source and reportable under the applicable rules.

IRS guidance also says some U.S.-source amounts reportable under chapter 3 or 4 belong on Form 1042-S even when withholding is not required. So zero withholding does not automatically mean zero reporting.

Confirm form year, package, and timing#

Use the current IRS instructions as a control, not as a last-minute check. The IRS tells filers to review the Instructions for Form 1042-S for developments after publication and to make sure the right form is used for the income year.

Before design or filing work starts, confirm:

- the filing-year instructions your team is using

- the form year tied to the income paid

- whether the annual package also requires Form 1042

- if filing on paper, whether Form 1042-T is included as the transmittal form

Timing matters too. IRS discussion guidance says Forms 1042, 1042-S, and 1042-T must be filed by March 15 of the following year. The instructions also state that IRIS will be available beginning January 1, 2026, and must be used to e-file 2026 Forms 1042-S.

The tradeoff is straightforward. If you under-build, you create filing risk. If you over-build, you add process drag. The practical middle path is to build only the checkpoints that prove who had the duty, what the payment was, what documentation supported the treatment, and when specialist review is required.

What to prepare before you touch Form 1042-S#

Do not build Form 1042-S records until ownership, source documents, and payment boundaries are clear. Filing problems often start earlier, when teams assume someone else owns withholding decisions, Form 1042, or recipient statement delivery.

Get your records and ownership model in order before you classify anything.

Assign owners for each duty#

Assign named owners for each duty before any coding starts. At minimum, set one owner for Form 1042-S data preparation, one for Form 1042, and one for recipient statement delivery. If the same entity may be the withholding agent for chapter 3 and chapter 4, tax and legal should align on that position up front.

Checkpoint: for each duty, you should be able to name the legal entity, functional owner, and reviewer. If recipient delivery has no owner, that gap tends to show up late.

Build a complete source file for each foreign payee#

Build a complete source file for each foreign payee before you review rates or income codes. Include the tax profile, payout transaction logs, and applicable forms such as Form W-8BEN-E, Form 8233, and Form W-8ECI.

Having the documents is not enough. You need linkage. If you cannot trace each payment to the payee record and the supporting form, treat that item as unresolved.

Map the control boundary across entities#

Map the control boundary across entities and across the payment flow. Withholding agent analysis turns on control, receipt, custody, disposal, or payment authority, not platform labels. Also check whether any part of the activity could create foreign financial institution (FFI) exposure under chapter 4.

Use an entity-by-entity payment map that shows who contracts, who funds, who releases payment, and who can block or change withholding treatment.

Create the escalation list before classification#

Create an escalation list before classification begins. Include any case where U.S.-source FDAP income status is uncertain, documents conflict, or Form W-8ECI points to a possible effectively connected income path that needs second review.

Do not force coding just to keep operations moving. Reporting can still be required even when no tax is withheld, so unresolved classification issues should pause coding.

If you want a deeper dive, read IRS Form 1042-S for Platform Operators: How to Report and Withhold on Foreign Contractor Payments.

Decide whether your platform is acting as a withholding agent#

Make the call based on control, then document it. "The platform pays" or "the processor handles it" is not enough, because the entity that meets the withholding agent test may need to deposit withheld tax and file the required returns, including Form 1042-S.

Start with the payee in scope#

Start with the payee. Withholding-agent analysis matters only when the payment is to a foreign person. If the payment goes to a U.S. person you know is acting as agent for a foreign person, treat it as a foreign-person payment for this analysis.

Verification point: confirm the payee record, the linked withholding documentation, and the transaction IDs for the payments in scope. If the payment flow and tax forms point to different recipients, stop and escalate before return prep.

Run the control sequence on the real payment flow#

Run the control sequence on the real payment flow, in order:

- Which entity controls or releases payment?

- Which entity applies withholding logic or rate decisions?

- Which entity remits withheld amounts?

- Which entity issues recipient reporting?

Use this sequence because the legal test turns on control, receipt, custody, disposal, or payment. If your entity determines withholding on payments to a foreign person, treat withholding agent analysis as mandatory and document the conclusion, even if another party funds the payment or is called the payer.

Checkpoint: keep a short responsibility memo for each flow with the contracting entity, account-control entity, withholding decision owner, and recipient-statement owner. If any point cannot be supported by contracts, treasury permissions, or payout configuration, the conclusion is not ready.

Compare role names to actual conduct#

Compare role names to actual conduct, but do not let labels drive the result. Labels such as principal, payout facilitator, or delegated processor do not determine withholding-agent status by themselves.

If an entity can release funds, block payments, or apply withholding logic, it may meet the test even when another entity bears the economics. If an entity only follows instructions and does not control withholding decisions, payment release, or reporting, its role may be narrower. Do not assume "processor touches money" means the processor owns tax. Do not assume "nominal payer is elsewhere" means the platform is out. More than one party in a chain can meet withholding-agent criteria for one payment, even though tax is withheld once.

Write the conclusion before building records#

Write down the conclusion before you build Form 1042-S or Form 1042 records. The key question is not just who paid, but who had enough control to be personally liable if withholding was required.

If responsibility boundaries are unclear, escalate to specialist tax or legal review before filing work starts. Escalate especially when contracts split duties across entities, a U.S. intermediary may be acting for a foreign person, or chapter 4 exposure involving an FFI or NFFE may apply.

Related: IRS Form 8233: When Foreign Contractors Claim Treaty Exemptions and What Platforms Must Verify.

Classify payment type before tax treatment decisions#

Get characterization right first. If intake classification is wrong, your Form 1042-S coding, withholding treatment, and recipient reporting will all drift downstream.

Sort payments into source and income buckets#

Sort each payment into one of three buckets: U.S.-source FDAP income, effectively connected income (ECI), or potentially non-U.S.-source. A payment is subject to NRA withholding when it is U.S.-source and FDAP, or certain gains. ECI is treated differently and is not subject to NRA withholding in the same way.

For services, source generally follows where the services were performed. If services were performed partly inside and partly outside the United States, make an accurate allocation instead of forcing a single source by default. Do not use proxy fields as a substitute for actual work location.

Verification point: before setting withholding treatment, confirm that the record supports the payment characterization and where the services were performed.

Apply withholding logic only after characterization#

Apply withholding and Form 1042-S logic only after characterization is set. U.S.-source gross income that is not effectively connected with a U.S. trade or business is usually subject to 30% withholding, subject to exceptions. But not every foreign-contractor payment belongs in that lane.

Early miscoding creates both withholding and reporting risk. Form 1042-S reporting is granular by income type and, where applicable, by tax rate for the same recipient. If your system collapses payments into one generic contractor category, fix that before you file.

Route special categories into separate lanes#

Use IRS-listed special categories as explicit exception lanes. Form 1042-S includes certain specified Federal procurement payments subject to withholding under section 5000C, and distributions of effectively connected income by a publicly traded partnership or nominee.

If a payment involves section 5000C, a publicly traded partnership, or a nominee chain, do not run it through a standard contractor-services process.

Pause automated coding when characterization is unclear#

If source characterization is unclear, pause automated coding and route the case to review. That pause is an internal control choice, but it is safer than defaulting a code when the facts are incomplete.

Final checkpoint: use only current-year income, status, exemption, and limitation-of-benefits codes from the Instructions for Form 1042-S. Misclassification plus stale code selection is a common path to withholding and reporting errors.

Build the payer-payee evidence pack for every reportable payment#

Your evidence pack should answer one question quickly: why did this payment produce this withholding result and this Form 1042-S output? If that chain is not traceable from payee status through source determination to reporting, hold the row before file generation.

Build the pack at the payment-row level#

Build the pack at the payment-row level, not just at the payee-profile level. A withholding agent may need to file Form 1042-S for reportable amounts paid to foreign persons even when no tax was withheld, so each row has to support both reportability and the withholding result.

| Evidence row element | What it should show | Named artifacts to link |

|---|---|---|

| Payee status | Payee status for withholding and reporting, including chapter status where relevant | Form W-8BEN-E, Form W-8ECI, payee master record, chapter 4 status support where applicable |

| Treaty or exemption basis | Why withholding is reduced, exempt, or routed outside the default path | Form 8233 (where applicable), treaty/exemption notes |

| Source determination memo | Why income was treated as U.S.-source, ECI, or non-U.S.-source | Internal source memo tied to payment facts, reviewer sign-off |

| Withholding result | Rate and amount withheld, or reason no withholding applied | Calculation record, exception resolution notes |

| Reporting output | What is reported on Form 1042-S for that payment row | Draft reporting row, income-type code support, tax-rate support, chapter status support where required |

This structure matters because one payee can have different payment types, rates, or documentation within the same year.

Tie each row to named documents#

Tie every row to named documents, not to generic labels such as "tax form on file." Use Form W-8BEN-E for entity beneficial-owner status, Form W-8ECI for effectively connected claims, and Form 8233 for eligible nonresident alien personal-services compensation exemption claims.

Be strict about document scope. Form 8233 is controlled by tax year, withholding agent, and income type, not treated as a permanent profile document. If documentation is stale or mismatched to the payment, treat that as a control failure and route it to review.

When intermediaries or flow-through structures are involved, keep chapter 4 status support in the same row so the reported status code is traceable.

Check freshness and reliability before export#

Run freshness and reliability checks before generating Form 1042-S data files. For Form W-8BEN-E and Form W-8ECI, general validity runs through the last day of the third succeeding calendar year unless a change in circumstances makes the form incorrect sooner.

Your checkpoint logic should cover received date, calculated expiration, and change-in-circumstances review. Require reviewer sign-off before export so the document on file, withholding outcome, and reporting row stay aligned.

Move unreliable documentation into an exception queue#

Move missing, unreliable, or contradictory documentation into an exception queue with a defined internal escalation path. IRS materials do not set one universal queue deadline, but they do require presumption-rule withholding when you know or have reason to know documentation is incorrect.

For chapter 4 withholdable payments, missing reliable documentation can require presuming nonparticipating FFI status. If valid Form W-8 or Form W-9 documentation is not obtained and required presumption-rule withholding is not applied, assessment risk can include 30% chapter 3 or 4 tax or 24% backup withholding. Quarantine and resolve these rows before release.

Keep the evidence pack auditable and restricted#

Keep the evidence pack auditable and access-restricted. Keep records as long as they may become material to Internal Revenue Code administration. While 3 years is the general assessment period, it is not a universal retention rule for every withholding-support record.

Apply strong security measures to tax forms, source memos, and approval records, including role-based access, access logging, and export restrictions. The control target is simple: auditable records with limited exposure, not broad visibility.

You might also find this useful: W-8ECI Explained for Platforms: When Foreign Contractors Have Effectively Connected US Income.

Map withholding outcomes to reporting paths without guesswork#

Do not let the withholding result stand in for the reporting result. For each payment row, map the outcome to a Form 1042-S path, annual-package handling, and an escalation branch.

Build a decision table your team can run#

Use this as the default routing logic:

| Payment outcome | Form 1042-S path | Key control point |

|---|---|---|

| Standard withholding applied | Report on Form 1042-S with withholding reflected on the row | Row ties to source determination, rate logic, and transaction record |

| Reduced or exempt withholding under chapter 3 | Report when the amount is reportable; if tax withheld is less than 30%, include the required chapter 3 exemption code | Confirm support for reduced or exempt treatment and exemption-code population |

| Non-U.S.-source determination | Normally not required on an information return | If voluntarily reported on Form 1042-S, use Exemption Code 03 and keep source support |

| Effectively connected income (ECI) | Route to the ECI reporting path, not the ordinary NRA-withholding path | Require second-review validation because ECI is often subject to reporting even though it is not a chapter 4 withholdable payment |

Practical rule: zero or reduced withholding does not automatically mean "do not report." ECI and non-U.S.-source rows are two places where no-withholding assumptions can create reporting errors.

Force ECI and non-U.S.-source branches through review#

For ECI, confirm the documented basis and route the row through the ECI path before export. For non-U.S.-source, treat "normally not required" as conditional, not absolute. If you report anyway, Exemption Code 03 is the control point to check.

Tie row-level reporting to the annual package#

If Form 1042-S is required, Form 1042 is also required. Use Form 1042-T only when transmitting paper Forms 1042-S to the IRS, and do not use Form 1042-T for electronic Form 1042-S submission.

Before filing, reconcile reportable gross amounts, withholding amounts, and excluded non-U.S.-source rows so row-level outputs and annual totals match.

Add the late-risk and filing-method branch early#

Treat due dates and filing-method rules as a verification step, not a memory test. IRS materials state a general March 15 deadline for Forms 1042, 1042-S, and 1042-T, with a next-business-day rule when March 15 is not a business day. You should still confirm the current-year instructions before filing.

For delays on Form 1042-S, use Form 8809. Do not treat Form 8809 as a Form 1042 extension path. Form 1042 extensions route to Form 7004. For e-file exceptions, handle waiver logic separately. Form 8508 must be submitted on paper, waivers are not automatic, and approved waivers apply only to the current filing year.

IRS pages conflict on the current Form 1042-S e-file trigger, including expanded tax year 2023 language versus the 250-form threshold language. Confirm the controlling Instructions for Form 1042-S and related IRS updates before you choose paper or electronic submission.

Related reading: How to Fill Out Form W-8BEN for a Foreign Freelancer.

Before you operationalize this mapping, align your team on event states, reconciliation outputs, and exception handling in the Gruv docs.

Complete Form 1042-S records with controls auditors can follow#

Use a reproducible record standard. Each Form 1042-S row should let a reviewer reach the same reporting result from the same support.

Build each record so it can be recreated#

Structure records the way IRS reporting is defined: separate Form 1042-S entries by recipient, by income type for that recipient, and by tax rate for that income type. Reporting can still be required even when no withholding was required, so do not treat zero withholding as a reason to skip a record.

For each foreign person entry, keep these linked in one review trail:

- income type classification for the row

- withholding outcome used for the row, including no withholding when applicable

- support used to justify that outcome

Keep recipient fields clean. Boxes 13a through 13h are for one beneficial owner on each Form 1042-S.

Apply second review to high-risk rows#

Use dual sign-off where reporting logic is easy to miscode. Consider preparer and reviewer sign-off before release for rows that include:

- more than one tax rate for the same recipient and income type

- reportable payments with no withholding

- joint-owner allocations, including post-filing split requests

- manual overrides or documentation exceptions

If a joint owner later requests a separate form, amend the originally filed Form 1042-S and reallocate amounts. Across all forms tied to that payment, total reported payment and tax withheld cannot exceed what was actually paid and withheld for the joint owners.

Reconcile before filing and before recipient furnishing#

Run a reconciliation control before IRS submission and again before recipient release. A practical check is to confirm:

- record counts match the expected recipient, income-type, and tax-rate splits

- reported payment and withholding totals match the reporting population

- joint-owner reallocations stay within original paid and withheld totals

Apply extra care when filing volume is large. IRS materials referenced here state a 250-Form 1042-S e-file threshold, separate financial-institution e-file language, and use of the FIRE System for electronic submissions. Confirm the current Instructions for Form 1042-S before you choose the filing method.

Clear a pre-release exception report before release#

Do not release files with unresolved exceptions. Hold a pre-release report that isolates rows with:

- missing or conflicting payee documentation

- mismatched payer or recipient setup that blocks clean reporting

- withholding outcomes that are not supported in the record

- recipient data that appears to include more than one beneficial owner

If support is incomplete, hold or revise the row and document the resolution path before release.

For a step-by-step walkthrough, see Form 1042-S for Foreign Persons With U.S.-Source Income.

Assemble the annual filing package and extension plan#

Once the Form 1042-S population is reconciled, lock the filing sequence. Finalize Form 1042-S first, then add only the annual forms that apply, and do not start filing with open exceptions.

Finalize Form 1042-S as the source file#

Treat Form 1042-S as the anchor for the annual package. Use the final reviewed record set, confirm the correct-year form, and lock record counts and totals before rolling anything into annual filings.

Your release check should be simple: locked Form 1042-S counts, reportable amounts, and withholding totals should match reconciliation, and unresolved exceptions or ownership gaps should be cleared before filing.

Use Form 1042-T only for paper filing#

Use Form 1042-T only if Forms 1042-S are filed on paper, and use a separate Form 1042-T for each type of Form 1042-S. If Forms 1042-S are filed electronically, do not include Form 1042-T.

Set the filing method before generating transmittals so you do not create avoidable rework.

Align the annual return on Form 1042#

If Form 1042-S is required, Form 1042 is also required. Build Form 1042 from the same locked totals used for Form 1042-S so the annual return and information returns stay consistent.

Forms 1042, 1042-S, and 1042-T are generally due March 15 for the prior calendar year, and the due date moves to the next business day when March 15 falls on a weekend or legal holiday.

Define the extension trigger before deadline week#

Set a written trigger for extensions before deadline week so the team is not making filing decisions in a rush. Use Form 8809 to request an extension of time to file Forms 1042-S, and use Form 7004 for an extension to file Form 1042. Form 7004 does not extend time to pay tax.

If you need a hardship waiver from required electronic filing, submit Form 8508 at least 45 days before the due date of the returns.

Keep one uncertainty flag explicit in your control plan. IRS materials show conflicting electronic filing threshold language, including 10-return and 250-Form 1042-S references. Validate the current-year Instructions for Form 1042-S and related IRS updates before release.

Common failure modes and how to recover fast#

Many breakdowns trace to control failures: missing document-to-payment linkage, unsupported responsibility assumptions, or filing before the evidence pack is complete. The fastest recovery is to stop the next release, repair the payment-level decision trail, and then regenerate Form 1042-S and Form 1042 from a clean source set.

Rebuild document-to-transaction linkage#

If you cannot show which document supported each payment on the payment date, treat it as liability exposure, not admin cleanup. IRS practice materials state that a withholding agent that cannot reliably associate a payment with documentation on the date of payment can be liable under IRC section 1461.

Rebuild from each transaction outward. Attach the exact document relied on: Form W-8BEN-E for a foreign entity, Form 8233 for a nonresident alien individual claiming exemption on personal services compensation, or Form W-8ECI when the payee claims the income is effectively connected. Then rerun classification checks, because the wrong document type and the wrong tax treatment often show up together.

A practical gate is simple: each reportable line ties to a transaction ID, the specific tax document, and a reviewer-approved classification result.

Document the withholding-agent analysis before more payouts#

Do not keep paying out if your team assumed a processor, partner, or bank owned the reporting duty without proof. Withholding-agent status turns on control, receipt, custody, disposal, or payment authority over income of a foreign person, not platform labels.

Write a short withholding-agent memo for the exact payout flow and get legal sign-off before the next payout cycle. Name who controls funds, who applies withholding logic, and who issues recipient reporting. Keep the risk explicit: you may still be a withholding agent even if another person withheld, and that exposure can include tax, interest, and penalties.

Re-test broad non-U.S.-source assumptions#

Broad non-U.S.-source assumptions can create deadline mistakes. Re-test each disputed payment type against U.S.-source FDAP criteria, and pause automation on ambiguous cases.

Do not treat zero withholding as proof that reporting is not required. Form 1042-S can still be required even when withholding is not required. For recovery, prepare a short source memo for each disputed payment class covering income type, source conclusion, the document relied on, and the approver. Then escalate edge cases instead of forcing closure.

Enforce package gates before filing again#

If filings were prepared before the evidence was complete, pull them back and restart from a locked source set. Do not relaunch until support is complete for each affected row.

Set clear pre-filing gates: complete evidence pack, final classification, linked withholding rationale, and reconciled Form 1042-S rows by recipient, income type, and rate. Rebuild Form 1042 from that same locked population, because when Form 1042-S is required, Form 1042 is also required. If recovery work threatens the March 15 deadline, use the extension trigger from the prior section rather than filing unsupported records.

This pairs well with our guide on How Gig Platforms Report 1099s for Thousands of Contractors at Year-End.

Use Gruv controls to make reporting defensible at scale#

Use Gruv to enforce evidence collection and reviewer accountability, not to decide tax law. The operating rule is simple: automate only after your decision logic is stable, and keep manual review for gray-area source and withholding cases.

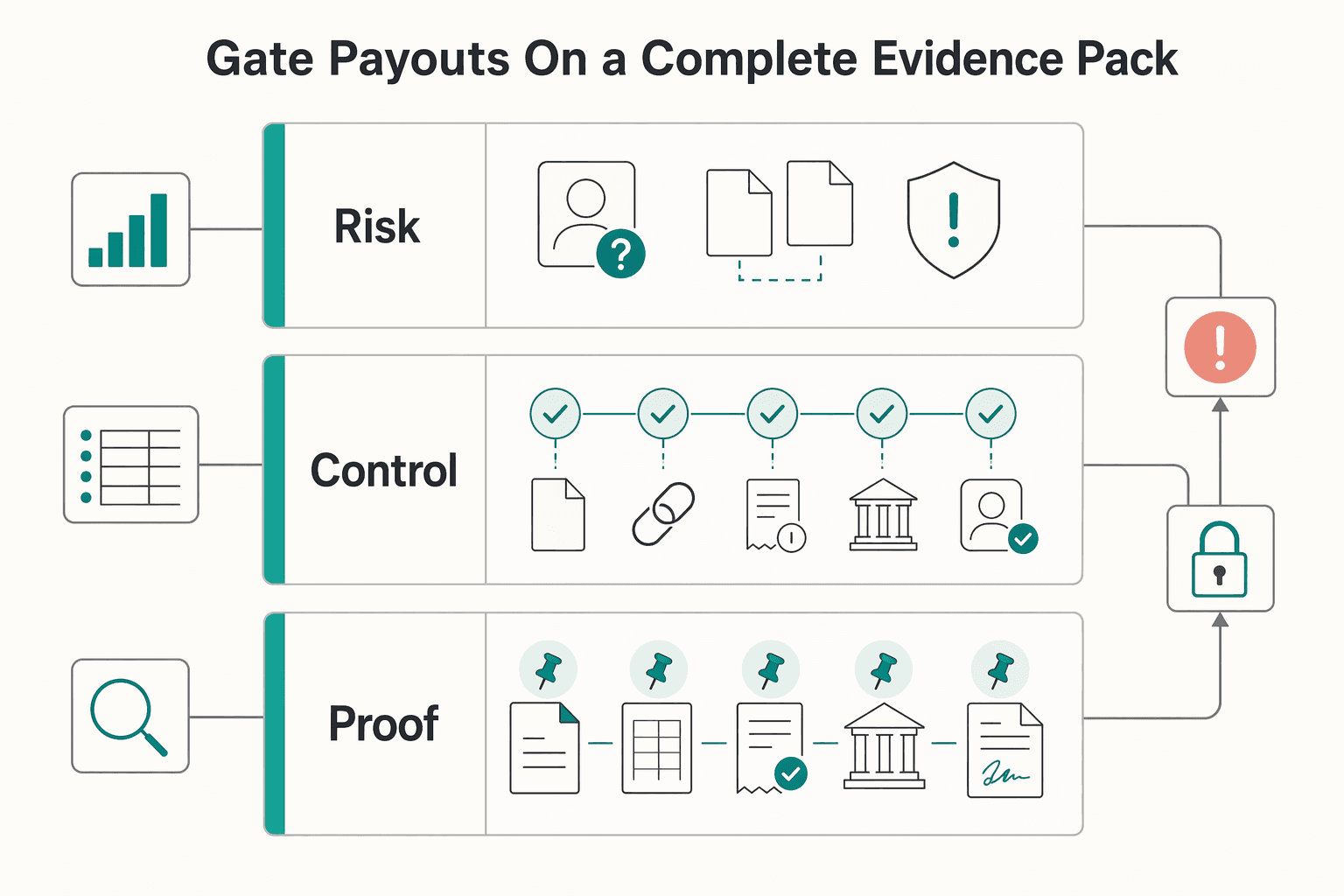

Gate payouts on a complete evidence pack#

Where supported and enabled in your Gruv setup, make payout approval depend on a linked tax record and payment trace. For each reportable foreign payee, require a clear link between the payment line, the document relied on at payment time, the transaction ID, the payer entity, and reviewer sign-off. The control is not just "document on file." It is line-level traceability to the exact record and classification used.

If payee status is unresolved, or the records conflict with the intended treatment, route the payment to an exception path instead of forcing release. That matters because Form 1042-S is filed separately for each recipient, and weak row-level support quickly becomes filing risk.

Tie operational artifacts to filing controls#

Use Gruv audit logs and transaction traceability to show who approved what, when, and against which record version. Pair that with reconciliation exports so you can test whether your Form 1042-S population aligns with the amounts you carry into Form 1042 when applicable and, for paper workflows, with Form 1042-T transmittals by form type.

Before final output, add a checkpoint from the 2026 Instructions for Form 1042-S: when tax withheld is below 30%, confirm that the required chapter 3 exemption code is present.

Keep legal decisions outside the automation boundary#

Gruv can prove that controls ran, but it should not be treated as the tool that determines withholding-agent status. IRS rules turn on control, receipt, custody, disposal, or payment authority, and more than one party can be a withholding agent in the same payment flow. Qualify each setup by market and program coverage, and require tax or legal validation before relying on automated reporting decisions.

Final checklist you can copy into your filing process#

Use this as a pre-filing gate. Do not start a Form 1042-S run until each item below is documented.

Confirm withholding-agent status and chapter 4 questions#

Confirm and document who is the withholding agent, and whether chapter 4 treatment raises FFI questions. The IRS standard is control, custody, receipt, disposal, or payment of income to a foreign person, not whether an entity is labeled a platform. If your entity is the withholding agent, the Form 1042-S filing duty sits there, and a required Form 1042-S also requires Form 1042. If FFI status is unresolved, escalate before filing design is finalized, since IRS materials note cases where 30% withholding can apply unless qualifying status is established.

Confirm each payee has a complete support file#

Confirm that each reportable payee has a complete support file before return data is generated. Match the payee to the form that supports treatment, such as Form W-8BEN-E, Form 8233, or Form W-8ECI, as applicable. If the document is not clearly linked to the payment line that relies on it, treat that row as unresolved and escalate.

Document source and withholding logic at the line level#

Document source and withholding logic at the payment-line level for each foreign person. Form 1042-S reporting can require separate records by recipient, by income type, and by tax rate when more than one rate is used. Your file should let a reviewer reproduce the reporting result from ledger data plus support documents.

Reconcile end to end before filing#

Reconcile end to end before filing. Tie ledger totals and counts to Form 1042-S output, Form 1042-T, if paper Forms 1042-S are transmitted, and Form 1042. For paper submissions, use a separate Form 1042-T for each type of Form 1042-S.

Approve deadline contingencies in advance#

Approve deadline contingencies before risk materializes. IRS filing-cycle references place Forms 1042, 1042-S, and 1042-T on a March 15 due date. If delay is likely, file Form 8809 for a 1042-S filing extension by the return due date.

Pre-plan waiver handling and edge-case escalation#

Pre-plan e-file exception handling and edge-case escalation. If you may need an electronic-filing waiver, use Form 8508. IRS Topic 803 says to submit it at least 45 days before the due date, and FIRE guidance says Form 8508 is paper-only. Because IRS pages can show different e-file threshold references, confirm the current instructions before filing, and route unresolved cases to qualified tax or legal specialists.

If you want to pressure-test your control design and confirm market/program coverage, contact Gruv.

Frequently Asked Questions

Does every platform have to file Form 1042-S, or only entities treated as a withholding agent?

No. Only the entity treated as the withholding agent has the Form 1042-S filing duty for the payment flow in scope. The key issue is which entity actually controls payment and withholding decisions, and reporting can still be required even when no tax was withheld.

When can a platform’s payment flow make it an FFI or otherwise create additional reporting obligations?

This guide does not provide the legal test for when a payment flow makes an entity an FFI, so that issue should be escalated. It does note that chapter 4 exposure should be checked and that if the withholding agent is a financial institution, it must file Form 1042-S electronically. Confirm the treatment with a specialist before finalizing the filing design.

What does Form 1042-S actually report for foreign contractors besides gross income?

Form 1042-S can require separate records for the same recipient by income type and by tax rate. It also reports tax withheld. Each form can include recipient information in boxes 13a through 13h for only one beneficial owner.

If income is treated as non-U.S.-source, do we still issue Form 1042-S records?

Do not use a blanket rule. Non-U.S.-source amounts are normally not required on an information return, but some payments can still be reportable even when withholding is not required. If you voluntarily report a non-U.S.-source amount on Form 1042-S, use Exemption Code 03 and keep source support.

How do exempt or reduced withholding outcomes change what appears on Form 1042-S?

Exempt or reduced withholding does not automatically eliminate Form 1042-S reporting. A separate form is still required for each recipient even if no tax was withheld. If the same income type was withheld at more than one tax rate, split those amounts into separate records.

How do Form 1042-S, Form 1042, and Form 1042-T fit together in one filing cycle?

Form 1042-S is the recipient-level information return, and Form 1042 is the annual withholding tax return tied to that obligation. If Form 1042-S is required, Form 1042 is also required. Form 1042-T is used only when Forms 1042-S are filed on paper.

What details must be confirmed directly in the current Instructions for Form 1042-S before filing?

Confirm the current e-filing requirements, including threshold language, any financial-institution e-filing rules, and the filing system required for that year. Also verify record-splitting rules by recipient, income type, and tax rate where applicable. Check amendment and joint-owner allocation rules so total reported paid and withheld amounts across forms do not exceed actual totals.

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.

How to Respond to a Subpoena for Business Records

Move fast, but do not produce records on instinct. If you need to **respond to a subpoena for business records**, your immediate job is to control deadlines, preserve records, and make any later production defensible.

A US Expat's Guide to Investing in UCITS ETFs to Avoid PFIC Issues

The real problem is a two-system conflict. U.S. tax treatment can punish the wrong fund choice, while local product-access constraints can block the funds you want to buy in the first place. For **us expat ucits etfs**, the practical question is not "Which product is best?" It is "What can I access, report, and keep doing every year without guessing?" Use this four-part filter before any trade: