Quick Answer

Use a go/no-go gate before build: launch only when ARS payout design, BCRA-related assumptions, and fallback routing are documented and owned. For this pay contractors argentina fx restrictions compliance platform decision, the minimum bar is a complete contractor file (including service agreement and tax inputs), clear approval logs, and pilot payouts that reconcile from internal request ID to provider reference and settlement status. If any of those records are incomplete, defer rollout.

Why this guide exists for platform operators#

Step 1. Start with the decision, not the market story. This guide is for founders and ops leads deciding whether Argentina should ship now. If you have not already committed product, treasury, and support capacity, the real question is not market size or broad LATAM demand. It is whether you can pay contractors in Argentine peso (ARS) while handling FX-related constraints with a level of compliance work and exception handling your team can actually sustain.

That framing matters because a market can look attractive at a high level and still be the wrong next launch. A country can be commercially interesting and operationally premature at the same time. If your team does not have a named owner for onboarding, payout exceptions, and legal escalation, treat that as a red flag before you build anything country-specific.

Step 2. Separate the known controls from the unknown mechanics. Some parts of the problem are clear enough to plan around. ARS is the local currency, and the Banco Central de la República Argentina (BCRA) is the central bank. Contractor compliance, at a minimum, means dealing with local labor, tax, and data-security obligations, and worker classification is a core control because misclassification is a major risk.

These are not abstract concerns. In practice, rollout planning touches contract terms, tax-data collection, payout eligibility, and evidence retention from day one. A useful checkpoint before a go or no-go call is simple: can your team show where classification is reviewed, where tax inputs are collected, and where payout approvals are logged? If that answer is fuzzy, your launch readiness is also fuzzy.

Step 3. Treat BCRA and FX details as items to verify, not assumptions to inherit. What needs counsel or provider confirmation is the exact handling for FX-related questions and payout routing. Do not let a sales conversation or one provider integration stand in for your own documented interpretation. The failure mode here is common and expensive: product assumes one conversion or settlement path will work, ops builds around it, and finance later discovers exceptions that break contractor experience or reconciliation.

Use a hard-evidence rule early. For every payout design you consider, ask for the provider's supported route, the currency steps, the exception cases, and the documents you would need to retain if a payout is questioned later. If a partner cannot explain those pieces clearly, or if counsel has not confirmed the open country-specific points, the country is not launch-ready for you.

That is why this guide keeps the decision first. The basics are grounded in sources updated on Feb 05, 2025 and March 31, 2026, but you still need to verify the country-specific mechanics that make or break actual operations.

Decide if Argentina is launch-ready for your platform#

Argentina is launch-ready only when your team can run onboarding, payouts, and compliance controls with clear ownership and fallback paths. If owners, backup payout routes, and audit evidence are still undefined before build, defer launch.

| Readiness check | What to verify | Action if missing |

|---|---|---|

| Volume, FX, and exception load | Expected contractor volume justifies country-specific support, finance, and legal handling; FX handling and payout exceptions are treated as core operating constraints | Plan manual review capacity before go-live |

| Ownership for onboarding and tax/compliance inputs | Accountable ownership exists for contractor onboarding, tax-data collection, and payout eligibility checks | Prioritize a lower-friction market first if you cannot staff this ownership |

| Provider dependency | At least two rails are available, one for routine payouts and one for edge cases; providers document the supported route, currency steps, exception cases, and required records | Treat launch as conditional until fallback routing exists |

| Pilot evidence | Success criteria are set for payout success rate, exception turnaround, and audit evidence completeness; each pilot payout can retrieve contractor record, service agreement, tax profile inputs, approval log, provider reference, and settlement status | Pause rollout if evidence is incomplete or exceptions do not close consistently |

Step 1. Screen for volume, FX handling risk, and exception load. Start with a blunt filter: does expected contractor volume justify country-specific support, finance, and legal handling? Treat FX handling and payout exceptions as core operating constraints, not edge cases. If your expected manual review load is high, plan that capacity before go-live.

Step 2. Assign ownership for onboarding and tax/compliance inputs. Use a simple rule: if you cannot staff accountable ownership for contractor onboarding, tax-data collection, and payout eligibility checks, prioritize a lower-friction market first. A March 19, 2026 legal overview says Argentina's Labour Modernisation Bill amends the LCT and other labor statutes, and that workers engaged through technological platforms are excluded from LCT scope in that summary. Treat that as a signal that legal interpretation is moving, not as a reason to loosen review or documentation discipline.

Step 3. Pressure-test provider dependency before GTM. If your launch plan depends on one provider route, treat launch as conditional until fallback routing exists. A practical baseline is to use at least two rails: one for routine payouts and one for edge cases. Ask providers to document the supported route, currency steps, exception cases, and required records if a payout is questioned later.

Step 4. Define success before build, then verify in a pilot. Set success criteria upfront for payout success rate, exception turnaround, and audit evidence completeness, then run a small pilot. For each pilot payout, confirm you can retrieve the contractor record, service agreement, tax profile inputs, approval log, provider reference, and settlement status without stitching across multiple tools. If that evidence is incomplete or exceptions do not close consistently, pause rollout.

Gather prerequisites before first contractor payout#

Before you send the first payout in Argentina, lock the record and the owners. If the document set, approval path, or payout traceability is still implied, you are not ready to move money.

Step 1. Build the minimum contractor record. Prepare one payout-ready packet with the contractor profile, signed service agreement, tax profile inputs, and a defined path for any Argentine tax forms you need to collect or validate. Keep this record unified instead of split across onboarding, legal, and finance tools.

Step 2. Assign named owners for classification and approvals. Treat independent contractor classification as a controlled decision, not a shared assumption, because it affects contract terms, IP ownership, invoice handling, and tax reporting. Set clear ownership across legal, ops, and product so classification changes and payout eligibility stay aligned.

Step 3. Confirm payout controls in your stack. Whether you use global payroll software or direct rails, verify idempotency keys, reliable webhook handling, reconciliation exports, and ledger-level traceability before launch. You should be able to follow a payout from internal request ID to provider reference and final settlement status.

Step 4. Log unresolved dependencies before go-live. Record any open BCRA interpretation, payout currency constraints, and provider coverage caveats with an owner and fallback route. Keep at least two rails available, one for routine payouts and one for edge cases, so one blocked path does not stop contractor payments.

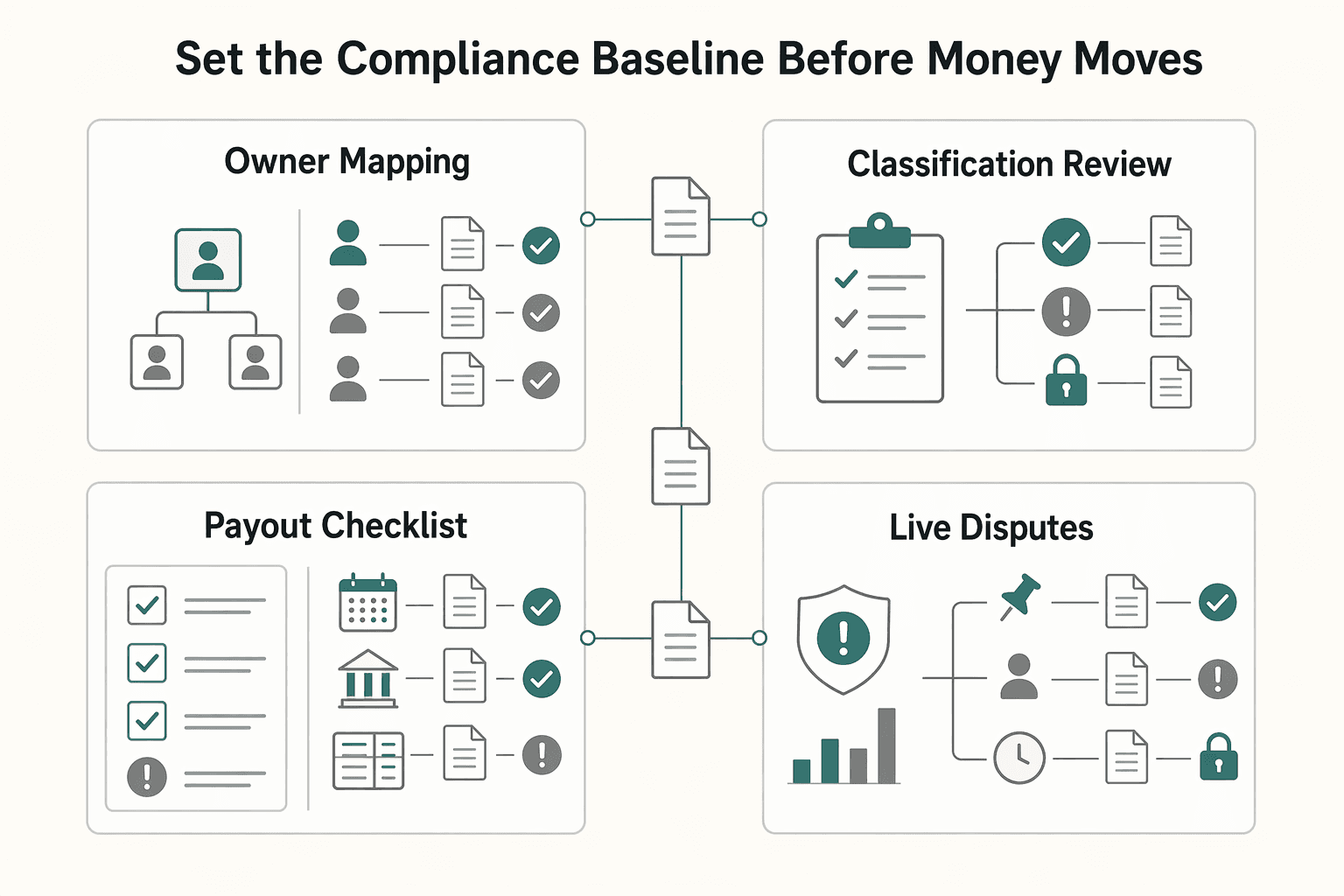

Set the compliance baseline before money moves#

Set the baseline as a release gate, not a policy note. Before the first transfer, you should be able to show who owns each decision, what record supports it, and how exceptions are handled.

| Control | What the record should show | Escalation point |

|---|---|---|

| Owner mapping | Distinct labor, enforcement, and tax lanes in the internal record, for example LCT, MTEySS, and AFIP lanes | Each open item needs an owner, a current view, and an exception log |

| Classification review | Onboarding checks and contract review, then periodic re-validation of independent contractor classification | When role scope or working patterns change, route the file back through legal review |

| Payout checklist | Verified identity, signed service agreement, complete tax data, and an eligible payout route | Eligible means the route is traceable end to end for finance and can produce auditable records, including receipts where available |

| Go-live and disputes | Legal sign-off on classification assumptions before live payouts | Document who can pause payouts, who reviews disputes, and what happens while a file is under review |

-

Map compliance lanes to clear owners. Keep labor, enforcement, and tax steps distinct in your internal record, for example LCT, MTEySS, and AFIP lanes. Even when interpretation is still evolving, each open item needs an owner, a current view, and an exception log.

-

Use classification controls that are reviewed over time. Start with onboarding checks and contract review, then re-validate periodically so your independent contractor classification does not drift from actual working arrangements. When role scope or working patterns change, route the file back through legal review instead of relying on the original approval.

-

Define a minimum compliant payout checklist for ops. Before release, your file should show verified identity, a signed service agreement, complete tax data, and an eligible payout route. Eligible should mean the route is traceable end to end for finance and can produce auditable records, including receipts where available.

-

Require go-live sign-off and a dispute path. Record legal sign-off on classification assumptions before live payouts, and document who can pause payouts, who reviews disputes, and what happens while a file is under review. This keeps payment execution aligned with compliance decisions instead of treating disputes as later cleanup.

For a step-by-step walkthrough, see Gig Worker Tax Compliance at Scale: How Platforms Handle 1099s W-8s and DAC7 for 50000+ Contractors.

Choose payout rails and FX handling based on risk tolerance#

Pick rails based on who carries FX risk and how easily you can explain each payout later. Most teams should use at least two rails: one for routine payouts and one for edge cases.

| Rail | Compliance burden | FX risk | Operational complexity | Recovery speed |

|---|---|---|---|---|

| Bank transfer | Typically document-heavy in your own process | In cross-currency flows, costs can include outgoing wire fees, intermediary fees, and FX spread | Moderate to high, especially when cross-border details need extra review | Often slower when multiple institutions are involved |

| Wallet payout | Depends on provider controls and record exports | Varies by whether payout is handled in ARS or another currency | Moderate, with extra mapping work if exports are thin | Can be faster when provider status and retry paths are clear |

| Platform-managed payout | Day-to-day ops can be lighter, but your compliance file still needs to stand on its own | Centralized conversion can simplify treasury handling, but only if records are complete | Lower inside one system, with concentration risk if you rely on one provider path | Often better with consolidated provider records and support ownership |

Set the settlement objective before you pick the rail#

Define the settlement objective first. If contractor certainty on local purchasing power is required, prioritize ARS settlement designs. If treasury flexibility is the priority, use staged conversion only when quote timing and approval controls are clear enough for finance to reconcile.

Match rail choice to compliance and tax traceability#

Cross-border payout design is not only a payments decision. Your route should support your labor, tax, and currency-conversion controls, and your records should let you trace what was paid, in which currency, and how conversion was handled. For Argentina, document your internal policy assumptions clearly for BCRA- and AFIP-related review rather than relying on provider dashboards alone.

Treat stablecoins as a conditional route#

Use stablecoins only as a conditional route, not a default. Only use them where support, recipient acceptance, and auditability are fully documented in your process. If that evidence is weak, keep a conventional fallback rail active.

Related: How to Pay Contractors in Mexico: SPEI CoDi and SAT Compliance for Foreign Platforms.

Build payout operations that survive failure modes#

Your payout flow should assume failures will happen and prevent them from becoming accounting breaks. In Argentina, where transfer rails can credit quickly across bank and virtual accounts, pre-send controls matter more than post-send cleanup.

| Failure mode | Handling | Control |

|---|---|---|

| Duplicate attempts | Block them from creating a second payout object | Use idempotency keys on payout creation |

| Expired FX quote | Fail before submit | If an expired FX quote is attached, the provider can return a 400 status code, so quote-validity checks should happen before API submission |

| Returned transfer | Require repair notes and a re-initiation rule | Treat it as a separate workflow before re-initiation |

| Unmatched deposit | Trigger reconciliation review before any ledger posting | Treat it as a separate workflow before ledger posting |

| Duplicate webhook delivery | Store processed event IDs, deduplicate duplicate deliveries, and enforce deterministic status transitions | Account for delayed redelivery windows that can run up to three days |

- Set a strict order of operations before release of funds.

Approve contractor eligibility, run compliance gates, create the payout request, consume provider status updates, then post final ledger reconciliation. Before submission, the record should already include contractor ID, settlement currency, approved amount, rail, and FX context when conversion applies. For ARS flows, this is critical because Transferencias 3.0 describes online crediting up to 15 segundos with 24 horas availability.

- Treat each failure mode as a separate workflow.

Do not bucket duplicate attempts, stale FX quotes, returned transfers, and unmatched deposits into one generic error path. Duplicate attempts should be blocked from creating a second payout object, stale FX quotes should fail before submit, returned transfers should require repair notes and a re-initiation rule, and unmatched deposits should trigger reconciliation review before any ledger posting. If an expired FX quote is attached, the provider can return a 400 status code, so quote-validity checks should happen before API submission.

- Make retries replay-safe and callbacks deterministic.

Use idempotency keys on payout creation so retries do not execute the same operation twice. Capture the provider Request-Id from responses, and keep it separate from your internal request ID and payout reference. On webhook intake, store processed event IDs, deduplicate duplicate deliveries, and enforce deterministic status transitions. Also account for delayed redelivery windows that can run up to three days.

- Build an evidence pack per payout cycle and stop batching if traceability breaks.

For each payout, keep the request ID, provider reference, event history, final ledger entries, and exception notes. For Argentina audit readiness, keep the electronic comprobante or other original support you rely on, linked back to the contractor record. Use a hard stop for ARS batches: if you cannot tie request to provider reference to ledger posting, pause batching and fix the root cause first.

Compare Argentina with nearby rollout alternatives#

Sequence by operational certainty, not market narrative. Put Argentina first only when FX and compliance unknowns are already bounded in your operating design. Otherwise, pilot where your rail and regulator map is clearer and exceptions are easier to control.

Build a country sequence table before you commit product time#

Use rail and regulator names as diligence anchors, not as shorthand for easy or hard. The real test is whether you can define a routine payout path, an exception path, and a document set without guessing.

| Market | Rails and regulators to map | What is grounded in this section | Sequencing signal |

|---|---|---|---|

| Argentina | Local bank transfer for local-currency payout; Argentina regulatory and macro review | Argentina is operating with high inflation, recession, and temporary capital controls. Since December 2023, the government has started removing some interventionist policies. Local bank transfer is a strong fit when paying in local currency, and many teams use at least two rails overall. | Launch first only when FX assumptions, local-currency route, and fallback route are documented and approved |

| Peru | Yape, Plin, SBS | This section does not establish operational behavior for these rails or regulator actions | Move ahead of Argentina only if your own review shows a clearer path for onboarding, payout handling, and exceptions |

| Mexico | SPEI, CoDi, SAT | This section does not establish operational behavior for these rails or regulator actions | Move ahead of Argentina only if your team can define payout and compliance handling with fewer open questions |

| Kenya | M-Pesa, Pesalink, KRA | This section does not establish operational behavior for these rails or regulator actions | Move ahead of Argentina only if partner coverage, documents, and failure handling are clearer than your Argentina design |

Readiness check: each country row should name one routine rail, one edge-case route, the authority map, and required documents before first payout. If key fields are still TBD, that market is not launch-ready.

Compare operational load, not market upside#

The core comparison is operator load. In Argentina, macro constraints can directly affect payout design, so FX handling, settlement behavior, and fallback planning need tighter definition before launch.

Assess rails by speed, FX, and settlement characteristics. Local bank transfer is strongest when you can pay in local currency, but most teams still run at least two rails to cover normal flow and edge cases. That raises integration and control work, which is exactly why sequencing should follow evidence, not momentum.

Choose the first launch based on timing and evidence quality#

If your GTM depends on fast onboarding and fewer payout exceptions, launch where your document checks, payout route, and exception ownership are least ambiguous. That may be Argentina, but only if your evidence pack is complete.

For expansion planning, require a one-page country memo with regulator map, payout rails, required documents, and top failure modes. For Argentina, state how temporary capital controls affect your assumptions, what policy-direction changes since December 2023 matter to your setup, and which fallback route you will use if the primary path fails.

If the case for Argentina is mostly LATAM momentum, pause. Sequence by verified operational readiness, then expand with fewer surprises.

For a comparable Latin America payout workflow, see How to Pay Contractors in Peru: Yape Plin and SBS Compliance for Platform Operators.

Common mistakes that create compliance or payout rework#

Most compliance and payout rework comes from locking assumptions too early. When regional guidance or a provider summary becomes your decision record, you often end up rebuilding contracts, payout logic, or finance controls after payouts have started.

Localize your legal and FX assumptions#

Argentina-specific assumptions need their own record. On 6 March 2026, Argentina enacted Labor Modernization Bill No. 27,802 with broad employment-law reforms, including measures intended to clarify presumptions of employment and reduce litigation exposure. Treat that as a trigger to refresh legal interpretation, not as proof that classification risk is resolved.

Do not rely on vendor claims alone for BCRA or ARS-related assumptions. Keep a short internal log for each assumption with source, date, owner, and fallback route if coverage changes or a case is rejected. If you cannot show that log and a backup payout path, your design is still fragile.

Lock classification controls before enabling payouts#

Lock contractor-classification controls before payouts go live. Cross-border contractor payments become complex when fees, tax paperwork, and classification rules intersect, and misclassification risk is the risk that a contractor is later treated as an employee. That distinction affects contract terms, IP ownership, invoice handling, and tax reporting.

Use a clear activation gate: completed contractor profile, signed service agreement, classification review, and tax data before first payout. A common failure pattern is launching first and trying to standardize agreements only after exceptions appear.

Build reconciliation and model flexibility from day one#

Design reconciliation from the start or routine issues become finance fire drills. Payment rails affect speed, FX, and settlement, and currency conversion can materially change payout outcomes.

Track each payout from request ID to provider reference to final ledger entry from your first pilot. Avoid locking into one EOR model or one rail too early; most teams maintain at least two rails, one for routine payouts and one for edge cases. If your contractor mix repeatedly lands in exceptions, adjust the model before scaling.

Conclusion and copy-paste launch checklist#

The decision comes down to inspectability. For a conservative launch, treat Argentina as launch-ready only when your compliance owner, FX policy, and payout operations can all be checked end to end without guesswork. If any part still depends on unwritten assumptions, especially around foreign exchange controls or tax considerations, treat the launch as conditional and keep volume off until the gap is closed.

Use this as a final go or no-go pass before broader release.

- Confirm authority mapping.

Make sure your internal memo or counsel note explicitly maps the labor, tax, and enforcement steps you are relying on. The verification point is simple: one reviewer should be able to open a single record and see who owns classification decisions, what assumptions were approved, and where disputes or edge cases escalate. If that record does not exist, you are not ready.

- Lock the payout rail and FX policy.

Your launch file should name the primary rail, settlement approach, and the exact country-level FX assumptions you are making, plus a fallback route if the preferred path fails. A good checkpoint is whether finance, ops, and product would all describe the same conversion rule and exception path in the same words. The common failure mode is a provider saying a route is workable while your own team has no written fallback for stale quotes, returned transfers, or route unavailability.

- Validate the onboarding evidence pack.

Before the first live payout, confirm that every contractor record contains the service agreement, tax data collected at onboarding, payout-method eligibility, and a named exception route. Do not rely on scattered attachments across email, CRM, and payment tools. If ops cannot produce the file quickly during a review, missing paperwork will show up later as payout delays or rework, not as a clean pre-launch issue.

- Run a pilot batch and reconcile it completely.

Send a limited batch first and require full evidence from request to provider result to ledger entry as an internal launch control. Your checkpoint here is auditability, not speed: request ID, provider reference, final amount, settlement result, and exception notes should all match. If even one payout cannot be tied cleanly from initiation through reconciliation, stop and fix the design before you scale volume.

- Pause expansion when a checkpoint fails.

This matters more than launch timing. The OECD's 2019 framing is useful here: good regulation should meet policy goals without imposing unnecessary burden, which is a reminder not to ship a process that creates avoidable manual risk for your team or contractors. The Lex Mundi 2020 Argentina guide also makes clear that foreign exchange controls and tax considerations for businesses sit squarely inside the operating picture, so unresolved country-specific assumptions are not minor details.

Related reading: How to Write a Payments and Compliance Policy for Your Gig Platform.

Frequently Asked Questions

What are the minimum compliance checks before paying contractors in Argentina?

Start with baseline checks: verified contractor identity, a signed service agreement, and collected tax documentation before payout activation. One source also states Argentine contractors must register with AFIP, so your onboarding record should confirm that status. A practical checkpoint is simple: if ops cannot show the contract, tax record, and payout eligibility decision in one file, do not release funds.

Do contractors in Argentina always need to be paid in Argentine peso (ARS)?

Do not assume that. The grounded sources identify Argentine Peso (ARS) as the country currency, but they do not support a blanket rule that every contractor payout must always settle in ARS. If currency handling is material to your launch decision, treat it as an Argentina-specific legal and provider verification item, especially where provider constraints or central-bank-related rules could affect what is actually possible.

How should a platform reduce FX risk without creating reconciliation complexity?

Use a limited set of payout routes and apply one quoting and settlement rule per route. If treasury flexibility matters, keep tight quote-expiry controls and log the approved FX assumption with the payout record. The failure mode is mixing conversion logic across rails, which makes it hard to match the request amount, provider reference, and final ledger amount.

When should we use an EOR versus direct contractor payouts in Argentina?

Use direct contractor payouts when your compliance process is reliable and your team can manage Argentina-specific exceptions without improvising. Use an EOR when local compliance support is thin or your contractor mix keeps producing edge cases that slow approvals and rework contracts. An EOR is an optional operating model, not something to treat as legally required by default.

What operational controls matter most for payout compliance at scale?

The controls that matter most are usually consistent identity checks, payout-method eligibility checks, and clear ledger traceability. Keep an evidence pack for each payout cycle with the request ID, provider reference, ledger entries, and exception notes. Also set a reporting owner, because one source says contractor payments should be reported to local authorities monthly or quarterly.

When is regional LATAM guidance not enough for Argentina decisions?

As soon as the decision touches classification, tax administration, or FX handling, generic LATAM guidance is not enough. Argentina-specific assumptions should name the relevant authority or operating point, such as AFIP registration, ARS currency handling, or a BCRA-related provider dependency. If a vendor summary cannot tell you what happens in your edge case, pause the launch decision and get country-specific confirmation.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- docs.fcc.gov/public/attachments/FCC-00-202A1.pdftrusted

- downloads.regulations.gov/ITA-2024-0001-0002/attachment_19.pdftrusted

- farmingdale.edu/courses/index.shtmltrusted

- oecd.org/content/dam/oecd/en/publications/reports/201...trusted

- oecd.org/content/dam/oecd/en/publications/reports/201...trusted

- sec.gov/Archives/edgar/data/904851/00011931251909682...trusted

- sec.gov/Archives/edgar/data/1846832/0002070979260001...trusted

- state.gov/reports/2024-investment-climate-statements/a...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Pay Contractors in Peru with Yape, PLIN, and SBS Checks

Treat Peru as a posture decision, not just a rail decision. If you choose a local wallet-style method first, then sort out contractor status, tax data, and evidence later, you may get a smoother payout experience. You also raise launch risk in areas that are much harder to fix once money starts moving.

Pay Contractors in Mexico: SPEI, CoDi, SAT, and CFDI Decisions for Platforms

Mexico contractor payouts usually break for a simple reason: teams launch from a generic Latin America plan, then discover that payout rail choices, tax steps, and operating structure cannot be separated in practice. If you are evaluating multiple rails and operating models at the same time, you need Mexico-specific decisions before you send the first live payout.

How to Pay Contractors in Kenya with M-Pesa, PesaLink, and KRA Controls

Kenya is worth serious consideration for contractor payouts, but you should not greenlight a launch just because M-Pesa is familiar and PesaLink is on the shortlist. The real decision is practical. Confirm which rail fits your contractor base, put local compliance and tax controls in place before money moves, and keep enough evidence to explain each payout later.