Quick Answer

High-volume platforms handle contractor tax compliance by sequencing controls before automation: classify workers before payout, separate identity from tax status, map each payment stream to the correct reporting lane, run year-end filing in separate validation and correction lanes, and keep audit-ready evidence. Cross-border intake also needs its own lane because Form W-8 collection and DAC7 scope are related but not the same.

How Tax Operations Change at 50,000+ Contractor Scale#

At scale, the hard part is not the acronyms. It is deciding sequence, ownership, and evidence when Form 1099-K, Form 1099-NEC, Form W-8BEN/W-8BEN-E, and DAC7 do not line up cleanly. If you run a high-volume marketplace, put controls in the right order and define clear stop points where legal or tax takes over.

The IRS baseline is straightforward. Gig economy income must be reported on a tax return, including income not shown on common information returns such as Form 1099-K, 1099-MISC, 1099-NEC, or W-2. The IRS also defines digital platforms as businesses that match workers' services or goods with customers through apps or websites. For platform teams, missing or delayed reporting does not remove the underlying tax question.

You can standardize a lot, but not everything. Form 1099-NEC covers nonemployee compensation, while payment card and third-party network payments under section 6050W are reported on Form 1099-K by the payment settlement entity and not on 1099-MISC or 1099-NEC. A practical control is to map each payout type to its tax category and settlement method before reporting automation runs.

Cross-border intake needs its own control lane. Form W-8BEN is submitted to the withholding agent or payer when requested, and Form W-8BEN-E documents foreign entity status for chapters 3 and 4 withholding and reporting. Treat these forms as status evidence, and keep retrievable records of version history, receipt date, and the payer or withholding-agent relationship tied to collection.

DAC7 is not a U.S. 1099 clone. DAC7, Council Directive (EU) 2021/514, entered into force on 1 January 2023, and non-Union platform operators must register and report in one EU country. Because DAC7 creates reporting obligations for platform operators on seller income, assign ownership and document market assumptions before go-live.

This article is for compliance, legal, finance, and risk leads who need controls that hold up under pressure. Standardize the controls that prevent irreversible errors, then escalate year-specific or jurisdiction-specific ambiguity early. That matters even in routine filing logic. IRS materials include different Form 1099-K threshold language in year-specific guidance, so tie policy and filing logic to reporting year, owner, and escalation path.

Who this list is for and how to choose controls#

Use this list if you operate a gig economy digital platform and need to align U.S. information return decisions with domestic and cross-border intake. It fits best when you have mixed employee and independent contractor populations, multiple payout methods, and tax-status or reporting exposure across Form 1099-K, Form 1099-NEC, Form W-8BEN, and DAC7.

Do not use this as a substitute for legal judgment when the same product flow can involve both employee and independent contractor lanes. The IRS treats classification as critical, and the obligations differ. Employee pay can require income tax withholding plus Social Security, Medicare, and unemployment tax, while independent contractor pay generally does not. If your flow can move a worker between lanes, escalate before you automate.

-

Good fit: Use these controls when your main risk is missing classification, tax-status, or payment-method evidence before payout or filing. A practical checkpoint is whether each payout type is mapped to a payment method and reporting branch, including keeping payment card and third-party network transactions in the Form 1099-K lane rather than duplicating 1099-NEC or 1099-MISC logic.

-

Not a substitute for counsel: If one product can treat the same person as an employee in one flow and an independent contractor in another, this list is not enough on its own. Classification mistakes can create hard-to-reverse payroll-tax and reporting consequences.

-

How to score controls: Score each control on four factors: audit defensibility, operational load, dependency risk, and impact on tax return accuracy. Weight audit defensibility heavily, because organized records support return preparation and examination response, and employment tax records generally must be kept for at least four years.

-

What to implement first: Implement controls that prevent irreversible errors before cycle-time automation. In practice, prioritize classification controls, tax-status intake, and payment-to-form mapping first. Add speed improvements after those three are working. For a related template, see How to Write a Payments and Compliance Policy for Your Gig Platform.

Control item 1 classification gate before any payout#

Treat worker classification as a hard stop in your process before first payout. The IRS sequence is explicit: determine the business relationship first, then decide payment treatment. If that step is wrong, you can misroute someone between Form W-2 treatment, with withholding and deposit obligations, and Form 1099-NEC treatment for nonemployee compensation.

Best for mixed roles and role changes#

This gate is especially useful when one platform supports multiple service types or workers can move between roles, because classification depends on facts and circumstances. For federal employment tax, the IRS applies common law rules and looks at three categories of evidence: behavioral control, financial control, and relationship of the parties. That is why labels and self-attest checkboxes are not enough by themselves.

Why this gate pays off#

The main benefit is preventing downstream misreporting. It keeps ambiguous cases out of the 1099 lane until classification is resolved and creates cleaner ownership. Operations collects facts, legal or tax sets decision rules, and payroll or AP executes approved status.

It also helps you avoid a common mistake: using filing thresholds as a classification shortcut. The 1099-NEC reporting threshold, $600, or $2,000 for payments made after December 31, 2025, is a reporting rule, not a worker-status test.

What to require before activation#

Use a gate that blocks payout when classification evidence is missing or contradictory. At minimum, capture:

- service description and payout type

- classification outcome, employee or independent contractor

- evidence across behavioral control, financial control, and relationship of the parties

- reviewer, decision date, and escalation owner

Before first payout, verify that the recorded classification matches the payout branch.

Tradeoff and escalation path#

The tradeoff is maintenance. Facts and circumstances can change, so reopen classification when role conditions change. If status is unclear, escalate to legal or tax review instead of forcing an operations decision. If a formal federal employment-tax determination is needed, use Form SS-8.

Keep the tests separate as well. Tax classification under common law rules is not automatically the same as labor-law classification under FLSA.

Control item 2 tax profile intake that separates identity from tax status#

After classification, separate identity from tax status before payouts scale. Keep one record for onboarding and fraud checks, and a distinct tax profile for withholding and information return decisions.

Why this control matters#

This control is most useful when domestic tax profiles and Form W-8BEN collection sit alongside the same KYC flow. KYC can establish who the payee is, but it does not determine whether you should rely on Form W-9 and TIN data or collect a foreign-status certificate. For foreign beneficial owners, Form W-8BEN is a tax-status document the payer or withholding agent can require, including when no treaty-rate claim is made.

The payoff is cleaner data lineage. At year-end, you can trace 1099-K, 1099-NEC, or 1099-MISC decisions back to tax-status records instead of reconstructing intent from blended onboarding data.

What to collect early vs. before reporting exposure#

Use two-stage intake so activation is not blocked by full tax completion, while reporting lanes still require completed tax status before exposure.

| Stage | Collect |

|---|---|

| Minimum viable profile for activation | Identity verification, country or jurisdiction data needed to branch tax treatment, and a clear lane: domestic profile or foreign-person certificate required. |

| Milestone completion before reporting exposure | Completed Form W-9 data with name and TIN alignment for domestic payees, or completed Form W-8BEN for foreign payees, plus seller information collection and verification aligned with DAC7 obligations. |

If you force every tax field before first earnings, friction rises. If you wait too long, cleanup lands in filing season. Form 1099-K recipient copies have a January 31 deadline, so reminders and remediation need to run before that window.

Lane checks that prevent rework#

Check that tax status matches the payment lane, not just that a profile exists. Payment card and third-party network transactions go to Form 1099-K and are not reported on Form 1099-MISC or Form 1099-NEC.

For domestic payees, validate Form W-9 name and TIN alignment early. If nonemployee-compensation payments proceed without required TIN compliance, backup withholding can apply at 24%.

For foreign payees, do not treat country, passport, or KYC nationality as tax documentation. If Form W-8BEN is required by the payer, collect it, version it, and store it as a tax-status record separate from identity records.

Cross-border detail to keep explicit#

This split also supports DAC7 operations. Platform operators are expected to collect and verify seller information, and non-Union platform operators can still have EU registration and reporting obligations when they have Union activity. Do not use EU incorporation alone as your scope test.

Use a simple operating rule: activate on a minimum profile, but block threshold-sensitive reporting lanes until tax status is complete and verified. For example, if your 1099-K process uses the IRS FAQ test of more than $20,000 and more than 200 transactions, set completion milestones before an account gets close to that point.

For filing workflow details, see 1099-NEC Automation for Platforms to File at Scale Without Manual Errors.

Control item 3 reporting determination matrix tied to transaction types#

Build the reporting matrix from transaction type and settlement rail first, not from worker labels at close. This turns form selection into repeatable logic across payout flows and reduces year-end analyst judgment.

This works best when product, payments, and tax share a stable event taxonomy. It is heavier to set up, and it gets brittle when product names, ledger codes, or settlement rails change without governance.

Start with the payment stream, not the worker label#

Your first branch should usually be the settlement type. In IRS terms, Form 1099-K covers reportable payment transactions (payment card or third-party network transactions), and those payments are not also reported on Form 1099-NEC or Form 1099-MISC for that stream.

Use the matrix below, and map from stable ledger codes and settlement rails, not marketing labels like "creator bonus" or "task reward."

| Event family in your ledger | Candidate form | Decisive check |

|---|---|---|

| Payment card or third-party network settlement | Form 1099-K | Is this a reportable payment transaction in a 1099-K settlement lane? If yes, do not duplicate it on 1099-NEC or 1099-MISC. |

| Direct payment for services to a nonemployee | Form 1099-NEC | Is this nonemployee compensation and not already in a 1099-K lane? |

| Rents, royalties, prizes, awards, or other fixed determinable income | Form 1099-MISC | Does the income type fit a 1099-MISC category rather than compensation for services? |

Version thresholds separately from form logic#

Keep candidate-form logic separate from filing-threshold logic, especially for Form 1099-K. IRS materials here show conflicting threshold text across sources. FS-2025-08 states more than $20,000 and more than 200 transactions. Another IRS instructions page references more than $2,500 in 2025 and more than $600 in 2026 and after. The Form 1099-K page also notes on 17-NOV-2025 that the dollar limit reverted to $20,000.

Operationally, do not hardcode a single permanent 1099-K threshold in the matrix. Store filing year, effective date, source authority, and owner with the threshold rule.

Also keep in mind that a platform or user may receive a Form 1099-K below the stated TPSO threshold. Keep a 1099-K candidate designation at the transaction-stream level, then apply filing-year threshold rules as a separate step.

Make exceptions explicit and reviewable#

A usable matrix includes exception codes, backup logic, and a named escalation owner for each event type. If a payout type or settlement method changes mid-quarter, route it to a needs-review queue before filing output.

Reporting quality follows data quality. At each close cycle, sample every active event family and trace the source event, ledger code, settlement rail, tax-profile lane, and generated candidate form. If the result changes from the prior close cycle, require a reason code and approver.

For mixed-form paper filing, keep outputs separated early. IRS guidance says each information return type needs its own Form 1096 transmittal.

Watch for analyst-override drift. If year-end reclassification becomes routine, the matrix is not controlling decisions. Require mandatory override reasons and resolve open transaction types before recipient-copy deadlines, for example January 31 for Form 1099-K, compress your options.

Related reading: How Independent Contractors Should Use Deel for International Payments, Records, and Compliance.

Control item 4 year end filing operations with correction lanes#

Once your matrix has assigned a payment to Form 1099-K, Form 1099-NEC, or Form 1099-MISC, run year-end in separate lanes: pre-file validation, filing window, and post-file corrections. Route late changes into a tracked correction queue instead of rewriting the main batch.

This makes filing execution more predictable by separating name/TIN mismatches, late profile changes, and output defects into distinct paths. The tradeoff is strict cutoff ownership, which you typically need if you want the correction queue to stay contained.

| Form | IRS paper deadline | IRS electronic deadline | Operational note |

|---|---|---|---|

| Form 1099-NEC | January 31 | January 31 | Also furnish the recipient copy by January 31, so this lane has the least rework capacity. |

| Form 1099-MISC | February 28 | March 31 | Keep timing separate from NEC so later MISC deadlines do not mask NEC misses. |

| Form 1099-K | February 28 | March 31 | Assign ownership clearly: a payment settlement entity must file Form 1099-K for reportable payment transactions. |

Pre-file validation#

Lock data quality and filing method before you submit. IRS TIN Matching is a pre-filing validation service for payers and authorized agents, so use it as a screening step before information returns are filed. Also lock the filing channel early. Starting tax year 2023, 10 or more information returns must be filed electronically. That matters because correction routing depends on how the original return was filed.

Keep an evidence pack for each form lane with the validation extract, exception list, source snapshot date, and approver.

File window#

Run each form as its own lane with a fixed source snapshot. Form 1099-NEC has January 31 deadlines for both IRS filing and recipient copy delivery. Form 1099-MISC and Form 1099-K have February 28 paper and March 31 electronic IRS deadlines.

If a record misses the validation cutoff, move it to a documented exception queue with reason code, owner, and expected disposition. Do not keep reopening the main filing batch.

Post-file corrections#

Use a dedicated correction lane because correction paths differ by filing channel. IRS instructions separate paper and electronic correction workflows. Pub. 1220 is the reference for electronic corrections in FIRE, and returns required to be filed electronically must be corrected electronically. For paper corrections, do not check the VOID box.

Treat TIN and name mismatch notices as timed cases. A CP2100 or CP2100A means the filed payee name or TIN was missing or did not match IRS records. You have 15 business days from the notice date or receipt date to send a B-notice, and backup withholding may apply at 24 percent in specified cases.

For late profile updates, review whether the filed return is inaccurate before amending. Keep the filed record, corrected record, trigger or notice, outreach, and approval together so the correction path is auditable.

Control item 5 cross border boundary setting for W-8 and DAC7#

Set the boundary early: treat Form W-8 collection and DAC7 as connected but separate controls, and publish that split before any new market launch.

U.S. year-end control maturity does not automatically cover EU platform reporting. DAC7 entered into force on 1 January 2023, and it places reporting obligations on platform operators, not sellers. So even if your 1099-K workflow is stable, you still need a separate DAC7 scope and ownership decision.

The boundary matrix you actually need#

Use three columns: globally standardized, market specific, and counsel only. If an item does not fit clearly in one column, do not treat it as launch-ready.

| Decision area | Standardize globally | Varies by market | Escalate to counsel before launch |

|---|---|---|---|

| U.S. foreign status intake | Use distinct intake lanes, typically Form W-8BEN for foreign individuals and Form W-8BEN-E for foreign entities | Local language, onboarding prompts, and evidence retention format | Any assumption that W-8 collection also satisfies non-U.S. reporting |

| Reportability ownership | Keep U.S. information return ownership separate from DAC7 ownership | Local registration and filing mechanics | Whether the operator is in DAC7 scope, including Non-Union Platform Operator analysis |

| Activity mapping | Keep one internal product taxonomy tied to payout events | Map launches to DAC7 activity categories: personal services, sale of goods, property rental, transport rental | Any business line that does not map cleanly to a defined category |

| Filing calendar | Keep one master compliance calendar artifact format | Member-state filing deadlines and exchange timing | Any launch without a named jurisdiction deadline owner |

1. Standardize intake, but keep the promise narrow#

Your global intake standard should answer a narrow question: what evidence do you collect for U.S. withholding and reporting? For foreign individuals, that is commonly Form W-8BEN. For foreign entities, that is commonly Form W-8BEN-E, used to document entity status for chapter 3 and chapter 4 purposes.

Do not treat W-8 intake as DAC7 completion. The regimes are different. W-8 supports U.S. withholding and reporting, while DAC7 is an EU platform reporting framework with separate scope and due-diligence questions.

2. Put DAC7 scope ownership on the operator decision#

DAC7 scope starts with operator status and activity, not seller nationality. EU guidance says the reporting obligation applies to platform operators. It can also extend to certain non-EU operators performing commercial activity in the Union, with Non-Union Platform Operators required to register and report in one EU country.

Before first payout in a market, require a written scope decision that records operator status, activity mapping, and registration approach where relevant.

3. Separate calendars and procedures early#

Keep IRS and DAC7 calendars separate. The EU Commission notes the first DAC7 information exchange for calendar year 2023 happened at the end of February 2024. Ireland's guidance shows the operating pattern: return due by 31 January for the previous calendar year, with exchange by end of February.

Use a dedicated jurisdiction calendar with named owners, filing destination, and escalation contacts. If those fields are unclear, your launch boundary is not complete.

4. Reuse taxonomy, escalate edge cases#

A shared internal taxonomy still helps. OECD model rules emphasize standardization to reduce burden, and that principle is useful operationally. But do not assume "same as 1099, plus Europe." Mixed goods, services, and rental models can require jurisdiction-specific legal interpretation under DAC7.

Keep one global data-capture model, and require written jurisdiction assumptions before enabling payouts in EU-facing markets.

Control item 6 evidence pack design for audits and internal signoff#

Once you separate U.S. reporting from DAC7 scope decisions, make every filed outcome traceable to source evidence. A good evidence pack shortens reviews when the Internal Revenue Service, internal audit, or finance asks not only what you filed, but why.

The tradeoff is concentration of sensitive tax data. If you build this pack, pair it with access limits, retention rules, and a written security program with administrative, technical, and physical safeguards appropriate to your size and complexity.

Minimum pack contents that actually matter#

Use one minimum pack per reportable profile or account, then append filing-season artifacts over time. Keep only what proves the chain from onboarding facts to a filing or non-filing outcome.

| Evidence item | What to keep | Why it matters |

|---|---|---|

| Classification basis | Decision record showing why the payee was routed to one reporting lane rather than another, plus approver or escalation note | Shows the filing lane was chosen deliberately, not by product default |

| Tax profile history | Domestic profile version history or Form W-8 history, including effective dates and any change in circumstances | A payer may rely on a properly completed Form W-8BEN, and W-8BEN validity generally runs through the last day of the third succeeding calendar year unless facts change |

| Filing and furnish artifacts | Filed outputs, recipient statement copy, submission confirmations, and furnishing timestamp | IRS guidance requires filing with the IRS and furnishing statements to recipients, so you need evidence of both |

| Corrections record | Original output, corrected output, reason code or narrative, approval, and channel used | IRS instructions provide correction paths for filed Form 1099-NEC and Form 1099-MISC, and electronic corrections are system-specific |

Four design rules#

- Preserve reconstructability

Publication 1099 says to keep filed information returns, or the ability to reconstruct the data, for at least 3 years. If your system overwrites intermediate profile states or decision logs, routine reviews turn into forensic work.

- Treat profile history as time-based evidence

Do not store only the current profile. Keep the exact version used when payment and filing decisions were made, especially for Form W-8BEN.

- Capture filing and correction channels

For Form 1099-NEC and Form 1099-MISC corrections, keep the exact route used because correction handling depends on the system. This matters more as IRS intake moves to IRIS-only beginning tax year 2026, filing season 2027.

- Keep DAC7 jurisdiction assumptions documented per country

DAC7 places reporting obligations on platform operators, including certain Non-Union Platform Operators that must register and report in one EU country. Retain the written operator-scope decision, activity mapping, and registration assumption, not only seller data.

A practical check is to sample one filed Form 1099-NEC due by January 31 and one corrected return after filing. Then ask a reviewer to trace each to source events, profile version, furnished statement, and approval history without analyst help. If they cannot do it in one sitting, the pack is too thin or too hard to access.

Keep the minimum pack standardized, and handle local retention or filing nuances as jurisdiction add-ons. That keeps the control scalable without assuming one record model fits every market.

Red flags that justify immediate escalation#

Escalate these immediately. Each points to a control break that can turn routine information return work into correction exposure, employment tax risk, or a weak cross-border filing position.

- Repeated mismatch between payout labels and filed Form 1099-NEC or Form 1099-MISC categories

Treat repeated label-to-form mismatches as a taxonomy failure, not a cleanup task. Payment flows reportable on Form 1099-K are not reported on Form 1099-MISC or Form 1099-NEC, and Form 1099-MISC is for categories like rents, royalties, prizes, awards, and other fixed or determinable income rather than nonemployee compensation. Trace filed forms back to source payout labels and your mapping rules. If analysts are routinely overriding categories, or the same label lands on different forms without a written rule, freeze new mappings and escalate.

- Repeated late tax profile updates after the Form 1099-K lock date

A recurring wave of post-lock updates is an escalation trigger because Form 1099-K recipient copies must be sent by January 31. If late changes are frequent, you are repeatedly choosing between stale profile data and exception handling that can drive downstream corrections. Require an exception log tied to the lock date, approval history, and correction path whenever this pattern appears.

- Frequent flips between independent contractor and employee without documented worker classification review

Repeated status flips without written review are a control failure, not just an operations issue. The IRS states there is no single deciding factor for classification, and misclassification can create employment tax liability. For each switch, require a dated classification record, who approved it, and the downstream routing decision.

- DAC7 work starting with no accountable owner and no written jurisdiction assumptions

Do not operationalize DAC7 without explicit ownership and written jurisdiction assumptions. DAC7 entered into force on 1 January 2023, and non-EU platform operators active in the Union may need to register and report in one EU country, so scope cannot be left implicit. Require a written scope decision covering operator status, chosen jurisdiction approach, activity mapping, and where local advice is required.

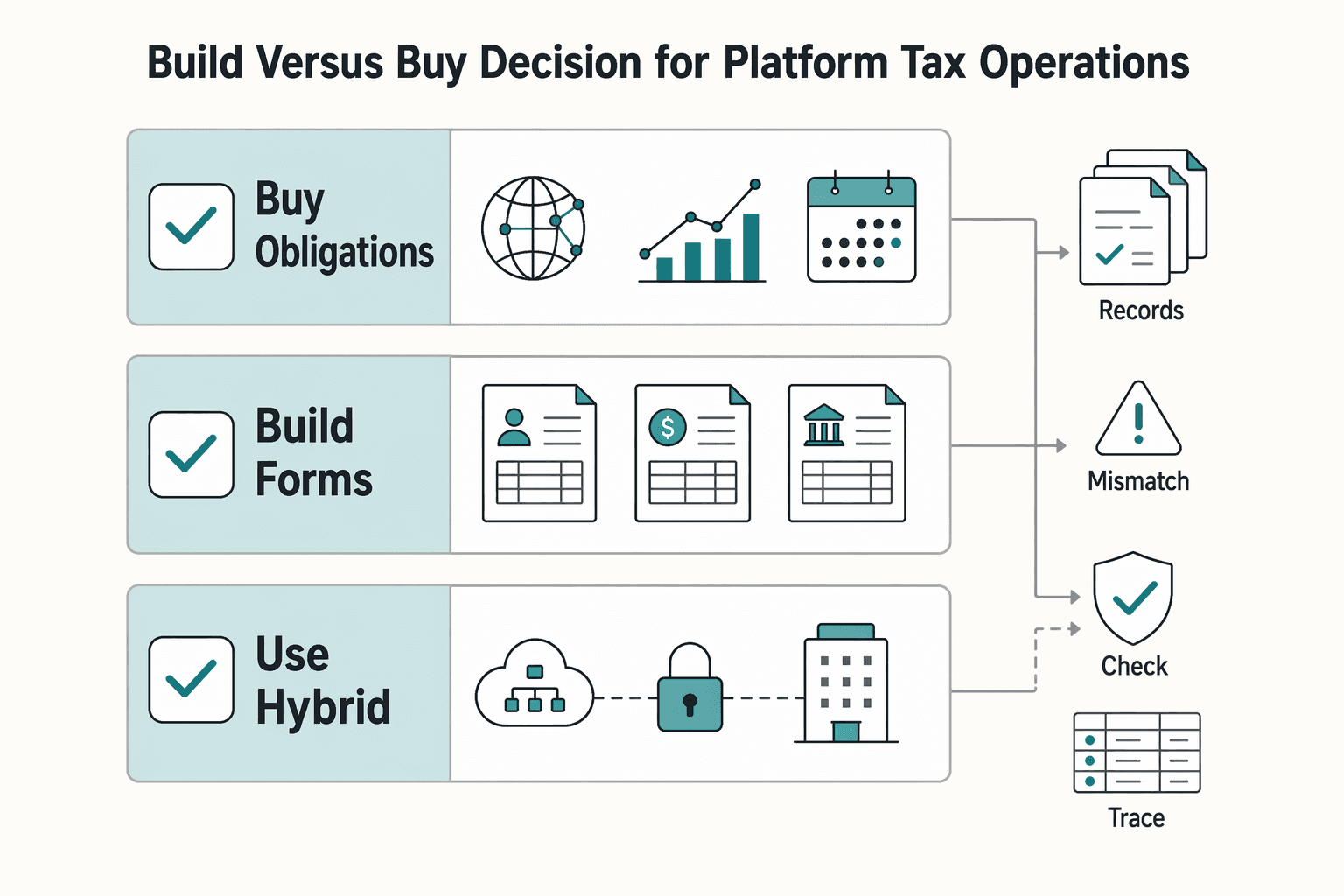

Build versus buy decision for platform tax operations#

Use this rule: buy more infrastructure when obligations are broad and change frequently; build more in-house when forms are limited and your taxonomy is stable. The common failure is treating tax operations as only an engineering backlog problem.

- Buy when your obligations are broad, changing, and correction-heavy

If you are handling Form W-8 intake, Form 1099-NEC or Form 1099-MISC output, possible Form 1099-K obligations for payment settlement entities, and DAC7 expansion at the same time, external infrastructure can be the safer operating choice. The compliance baseline is strict: electronic filing applies at 10 or more information returns, and the IRS states the FIRE System will be retired in tax year 2026 / filing season 2027.

Check whether the product supports the recurring control work. That includes W-8 validity through the last day of the third succeeding calendar year, refresh when circumstances change, correction handling for filed 1099 records, and auditable profile-change history. Ask the vendor to trace one record from onboarding to form determination, filing output, and correction flow. If the process still depends on CSV exports and analyst overrides, risk may not have moved much.

- Build when your forms are limited and your taxonomy is stable

Building internally is defensible when payout types are few, ownership is clear, and jurisdiction variation is low. A typical case is a U.S.-focused model with stable mappings from payout events to Form 1099-NEC or Form 1099-MISC.

This path can fit better when your payout logic does not match vendor assumptions. But the compliance chores stay with you: IRIS readiness, correction workflows, and W-8 change-in-circumstances handling when W-8 forms are in scope. A red flag is building intake screens without automated W-8 validity monitoring or a documented path for missing or incorrect TIN cases, including when reasonable-cause criteria may apply.

- Use a hybrid split only if ownership is explicit

A hybrid model works when you keep determination rules and taxonomy in-house but outsource document collection, filing transport, and recipient delivery. This is practical when U.S. reporting is established and cross-border scope is expanding.

Keep boundary ownership explicit. Under DAC7, platform operators carry the reporting obligation, and non-Union operators may need to register and report in one single EU country. Do not let contracts blur who owns scope decisions, seller-information verification, and jurisdiction assumptions.

For international onboarding and reporting decisions, see Creator Platform Tax Reporting for 1099 and W-8 Expansion Decisions.

If you are weighing build vs buy, map your required payout controls, retries, and audit-trail needs against the Gruv docs.

90 day sequence to deploy without overbuilding#

Use this as an internal sequencing plan: lock hard-to-reverse policy decisions first, then gate payout on usable tax profiles, then prove filing and correction operations in a mock close.

- Days 1-30: lock policy and ownership.

Start by freezing worker-classification policy, payout-event taxonomy, and named owners for IRS reporting and cross-border escalation. Classification should follow evidence of control and independence, not product labels. Document each worker lane with supporting facts, escalation triggers, and signoff rules for mid-year status changes.

Build a payout-event-to-form map with explicit exceptions, including cases where payments reported on Form 1099-K by a payment settlement entity should not also be reported on Form 1099-NEC or Form 1099-MISC. Sanity-check the taxonomy with real scenarios so different analysts reach the same candidate form and escalation owner.

- Days 31-60: implement tax profile flows and payout gates.

Month two should make payout eligibility depend on usable tax profiles, not partial onboarding. Separate identity collection from tax-status collection, and support domestic records and Form W-8 flows with version history and refresh logic.

For Form W-8BEN, enforce the validity window through the last day of the third succeeding calendar year unless a change in circumstances makes the form incorrect. Treat TIN handling as an operational control, since backup withholding can apply at 24 percent when required conditions fail. Validate with test cases for domestic profiles, non-U.S. profiles with W-8, and post-approval changes in circumstances. Confirm payout gating and exception routing in each case.

- Days 61-90: dry-run filing outputs, corrections, and evidence retention.

The final month should prove filing readiness and correction control with production-like data. Dry-run Form 1099-NEC, Form 1099-MISC, and Form 1099-K outputs. Test recipient and filing timelines: 1099-NEC by January 31; 1099-MISC by February 28 on paper or March 31 electronically; 1099-K payee statement by January 31, then February 28 on paper or March 31 electronically for IRS filing.

Do not hard-code a single 1099-K threshold until your tax owner reconciles conflicting IRS-source framing for near-term years and records the decision. Test correction queues for bad TINs, late profile updates, and wrong-form cases, including VOID handling, since incorrect VOID use can prevent correction intake. Finalize evidence retention so a reviewer can trace one worker from onboarding through filed return and correction history, using at least 3 years for general tax records and at least 4 years where employment tax records apply.

As an internal control, do not launch until a mock close demonstrates exception queues, escalation SLAs, and signoff artifacts. If DAC7 is in scope, confirm the cross-border owner can define legal-interpretation boundaries and member-state handling, since reporting is annual by January 31 and national application is not fully uniform.

For deeper implementation detail, see How Gig Platforms Report 1099s for Thousands of Contractors at Year-End and How to Scale a Gig Platform From 100 to 10000 Contractors: The Payments Infrastructure Checklist. For a step-by-step walkthrough, see Gig Worker Financial Wellness: How Platforms Can Offer Savings and Insurance as Benefits.

Conclusion#

For durable compliance at scale, prioritize control order, explicit escalation boundaries, and audit-ready evidence rather than simply collecting more forms. If you cannot trace each filed information return back to the source payout event, the tax profile used, and the decision owner, fix that before adding volume.

-

Put control order ahead of form count. The IRS frames platform operations around classifying workers, reporting payments, and paying and filing taxes, so upstream control failures can be where costly errors start. Keep the sequence tight: worker status, tax profile, transaction mapping, then year-end filing. If your team cannot walk a sample payout through source event, mapped payment type, candidate form, and escalation owner, the gap is control design, not missing paperwork.

-

Standardize the U.S. lane, then hand off cross-border scope deliberately. Form W-8BEN and Form W-8BEN-E document foreign status for U.S. withholding and reporting, but they do not by themselves determine DAC7 scope. DAC7 entered into force on January 1, 2023, places reporting obligations on platform operators, and can require non-Union platform operators in scope to register and report in one EU country, with automatic exchange among EU tax authorities. Treat DAC7 scope, market assumptions, and seller-activity analysis as early legal handoffs, and do not treat country authority manuals as definitive legal advice.

-

Treat audit evidence as a product requirement. Under 26 CFR 301.6721-1, late or incorrect information returns are explicit penalty events, with a general rule of $250 per return and a $3,000,000 annual cap before adjustments or exceptions. Your minimum evidence should support reconstruction of classification basis, profile history, source payment record, filed output, and correction rationale. A useful test is whether one filed record can be reconstructed in minutes rather than days.

Standardize these control items, then treat DAC7 and other cross-border determinations as deliberate legal handoffs instead of late-stage cleanup. Before launch, confirm market-specific compliance coverage and rollout assumptions with Gruv.

Frequently Asked Questions

Is gig income taxable if no Form 1099-K or Form 1099-NEC was issued?

Yes. Gig economy income must be reported on a tax return even if no Form 1099-K, 1099-MISC, 1099-NEC, or W-2 was issued. A missing form does not make the income nonreportable.

What does a platform own versus what the worker owns in tax return compliance?

The platform or payer owns information return duties for reportable transactions, including filing required returns with the IRS and furnishing recipient copies. The worker owns their tax return and must report taxable income whether or not a form was received.

When should a payment be considered for Form 1099-MISC versus Form 1099-NEC?

Use payment type first. Form 1099-NEC applies to nonemployee compensation for services, while Form 1099-MISC covers categories such as royalties, rents, prizes, awards, and other income payments. Payment card and third-party network transactions reportable on Form 1099-K are not reported again on Form 1099-MISC or Form 1099-NEC.

Where does Form W-8 fit in a marketplace onboarding flow?

Put Form W-8 in tax-status collection, not in place of general identity onboarding. It is submitted when requested by the payer or withholding agent and supports foreign-status treatment in the relevant withholding and reporting context. Incomplete or inconsistent W-8 data should not be treated as usable.

Can a U.S. 1099 process be reused for DAC7 without major changes?

No. DAC7 creates separate due-diligence and reporting obligations for platform operators and can also apply to non-Union platform operators performing commercial activity in the Union. Shared controls can be reused where they fit, but DAC7 scope and ownership need a separate compliance design.

What is the minimum evidence required to defend an information return decision?

At minimum, keep copies of filed information returns, or the ability to reconstruct the data, for at least 3 years from the due date. If federal withholding, including backup withholding, was imposed, keep records for 4 years.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.

How to Respond to a Subpoena for Business Records

Move fast, but do not produce records on instinct. If you need to **respond to a subpoena for business records**, your immediate job is to control deadlines, preserve records, and make any later production defensible.

A US Expat's Guide to Investing in UCITS ETFs to Avoid PFIC Issues

The real problem is a two-system conflict. U.S. tax treatment can punish the wrong fund choice, while local product-access constraints can block the funds you want to buy in the first place. For **us expat ucits etfs**, the practical question is not "Which product is best?" It is "What can I access, report, and keep doing every year without guessing?" Use this four-part filter before any trade: