Quick Answer

Yes. For platform-led pix payouts brazil contractors flows, use Pix as the default when payments are local in Brazilian real (BRL), then apply strict controls before scale: validate provider coverage, gate incomplete contractor records, and separate execution from final reconciliation. Keep TED as a domestic fallback, and move to IBAN/SWIFT routes only when local BRL payout cannot be completed.

How to pay Brazil contractors with Pix using provider validation, BRL controls, and reconciliation evidence#

For many local contractor payouts in Brazilian real (BRL), Pix is often a practical starting rail rather than a later optimization. The real decision is whether your team can use it with enough control to trust it at volume. That means choosing when Pix fits better than TED, DOC, or a cross-border route, and deciding what evidence you will keep when something goes wrong.

Before you start#

Read this as an operator, not as a freelancer picking a withdrawal method. If you own payout speed, reconciliation, finance approvals, or the engineering path that creates and tracks disbursements, your job is to choose the right rail and make its behavior predictable. For Brazil, that means using the same discipline you would use for ledger design or a provider migration, not defaulting to "wire funds and see what happens."

Step 1 Choose the rail based on the payout shape#

Pix sits inside Brazil's payment infrastructure and was created by Banco Central do Brasil. It supports transfers in a few seconds at any time, including non-business days, and moves funds between transactional accounts such as demand, savings, and prepaid payment accounts. That often makes it a strong first option when you are paying locally in BRL and funds availability matters.

That judgment changes as soon as the payout stops looking local. If your operating model depends on international bank routing, foreign currency, or provider coverage that is not confirmed for the recipient account type, do not assume Pix is available just because the contractor is in Brazil. Before launch, verify that your provider supports the exact BRL payout path you plan to use, can return a provider reference for each transfer, and exposes status updates you can reconcile later.

Step 2 Separate payment speed from operating reliability#

Pix can reduce transfer latency compared with older methods such as TED or DOC, which third-party sources describe as taking hours or days. That matters, but it does not remove the rest of the work. You still need ownership for rejected payouts, delayed acknowledgments, duplicate-send prevention, and fallback handling when a transfer cannot complete on the first rail you chose.

A common failure mode is treating "instant payments" as if they also mean instant certainty for finance. They do not. If your product shows "paid" before you have an accepted status and a provider reference, your ops team will end up reconciling exceptions by hand.

Step 3 Decide what you need from the rest of this guide. Use the rest of the guide to make a short set of decisions, not just collect background knowledge. By the end, you should know when BRL plus Pix is the right default. You should also know what data and controls need to be ready before your first live batch, how to route and recover exceptions, and what records finance and audit will expect when they ask you to prove a payout really happened.

That is the lens for the rest of the article. The question is not whether Pix is popular. It is whether your team can run it with enough control to trust the result. If you want a deeper dive, read Invisible Payouts: How to Remove Payment Friction for Contractors Without Sacrificing Compliance. Want a quick next step? Try the free invoice generator.

Decide whether Pix should be your default rail for Brazil contractors#

Use Pix as your default when the payout is local in BRL and fast availability matters; pause that default when the flow depends on international routing or non-BRL settlement.

Pix has been part of Brazil's payment infrastructure since November 2020, and one cited analysis says it now handles 40% of the country's e-commerce payments. Treat that as a strong signal that Pix is a standard local rail, while still validating your provider's exact coverage before launch.

| Contractor type | Currency and routing | Funds urgency | Default decision | What to confirm before go-live |

|---|---|---|---|---|

Autonomo | Local BRL in Brazil | High | Pix | Coverage for this payout path, status tracking, and exception ownership |

Pessoa Juridica (PJ) | Local BRL in Brazil | High | Pix | Same checks; do not assume support matches every account path |

Autonomo or PJ | Local BRL in Brazil | Low to medium | Pix is still the starting point | Whether your team can reconcile outcomes and run fallbacks cleanly |

Autonomo or PJ | Non-BRL or international bank routing required | Any | Evaluate cross-border routing first (IBAN/SWIFT path) | Provider constraints, required routing fields, and return/exception flow |

| Known unknowns | Any | Any | No default until clarified | Provider-specific limits, reversals, and dispute handling |

Speed is not the whole decision. One industry source describes legacy wire/manual batch models as often taking 3-5 days, while real-time rails like Pix are now framed as expected capability; that still does not remove your need for clear status tracking and exception handling.

Keep a visible "known unknowns" row in your decision record, with owner and resolution deadline, so finance does not assume behavior that has not been confirmed. Related: How to Pay US-Based Contractors from Australia.

Prepare compliance and payout data before your first live transfer#

Before your first live Pix transfer, lock down your payout data and review flow so your team does not release money from incomplete or misclassified records.

| Control area | What to define | Timing or check |

|---|---|---|

Autonomo vs Pessoa Juridica (PJ) intake | Split onboarding early and store contractor profile and identifier class as separate fields | Before payout activation; run a pre-live sample check across both paths |

| Tax and invoice evidence | Document where ISS review or NF-e (Nota Fiscal Eletronica) evidence happens | Onboarding, payout review, or reconciliation |

LGPD (Lei Geral de Protecao de Dados) privacy controls | Define who can view full values, who sees masked values, and how long records are retained | Validate access with real user roles across ops tools, exports, and support workflows |

Step 1 Separate Autonomo and Pessoa Juridica (PJ) intake#

Split onboarding early between Autonomo and Pessoa Juridica (PJ), then define the required fields for each path before payout activation. If your process uses CPF and CNPJ, store the contractor profile and identifier class as separate fields so ops does not have to infer document type from free text.

Run a pre-live sample check across both paths. Finance, ops, and engineering should see the same profile class, payout owner, and recipient details for the same contractor record.

Step 2 Decide where tax and invoice evidence enters your flow#

Do not leave tax evidence as an implicit step. If your operating model includes ISS review or NF-e (Nota Fiscal Eletronica) evidence, document where that happens: onboarding, payout review, or reconciliation.

Keep the evidence linked to contractor or payout records, not scattered across chat or email. If ownership is still undecided, treat that as a launch blocker.

Step 3 Document payout-data privacy controls under your LGPD (Lei Geral de Protecao de Dados) approach#

Pix can be initiated with a simple key such as a phone number or email, so payout operations can involve sensitive identifiers. Define who can view full values, who sees masked values, and how long those records are retained across ops tools, exports, and support workflows.

A short policy is enough to start if it is explicit and testable. Validate access with real user roles so full identifiers are only visible where approved.

Related: How Australian Agencies Can Pay US Contractors With Lower Risk.

Build the payout flow in the right order so finance and engineering stay aligned#

After intake is clean, the next control is sequence: treat request sent and paid as different states, and run one ordered flow from eligibility to reconciliation.

| Flow stage | Primary control | Operational note |

|---|---|---|

| Eligibility gate | Confirm the contractor is approved, Pix is present and ready, and the amount is confirmed in Brazilian real (BRL) | Block release when required CPF, CNPJ, or NF-e (Nota Fiscal Eletronica) evidence is missing |

| Creation and status intake | Protect payout creation and callback/event handling | Use one internal payout ID per payable item and deduplicate by provider reference or event identity |

| Completion definition | Treat request sent and paid as different states | A payout can be settled and still not be operationally done if it is missing from reconciliation export or cannot be matched cleanly |

| Post-transfer handling | Model delayed acknowledgments, failures, and reconciliation tasks as first-class stages | Keep the flow explicit: eligibility passed, method ready, amount confirmed, execution attempted, status finalized, export reconciled |

Step 1 Gate eligibility before you create any payout#

Use a hard pre-check before payout creation. Confirm the contractor is approved, Pix is present and ready, and the amount is confirmed in Brazilian real (BRL).

If your process requires CPF for Autonomo, CNPJ for Pessoa Juridica (PJ), or NF-e (Nota Fiscal Eletronica) evidence, block release when any required item is missing. It is easier to stop a bad payout in queue than unwind it after execution.

Step 2 Add idempotency at creation and at status intake#

Protect both entry points: payout creation and callback/event handling. If you only protect execution requests, retries and repeated events can still create duplicate outcomes in your internal records.

Use one internal payout ID per payable item and reuse it on retries. On webhook or status intake, deduplicate by provider reference/event identity so repeated callbacks update the same payout record instead of creating parallel state changes.

This is a platform control choice, but it matters more on a fast rail. Pix is widely used in Brazil; EBANX reported in January 2026 that it is used by more than 95% of Brazilian adults.

Step 3 Define what "done" means in your ledger and ops UI#

Make completion explicit across finance, engineering, and support.

| State | Internal meaning | Store at minimum |

|---|---|---|

| Request accepted | Payout request created | Internal payout ID, contractor ID, BRL amount, timestamp |

| Provider reference received | Transfer attempt acknowledged | Provider reference, request timestamp, raw response/event ID |

| Settled or failed | Final payment outcome reached | Final status, final timestamp, failure reason if any |

| Reconciliation export complete | Included in finance matching export | Export batch ID, export timestamp, ledger link |

A payout can be settled and still not be operationally done if it is missing from reconciliation export or cannot be matched cleanly.

Step 4 Treat post-transfer handling as a real stage#

Execution is not the end of the process. Delayed acknowledgments, failures, and reconciliation tasks happen after send, so model them as first-class stages.

For local BRL payouts, keep the flow explicit: eligibility passed, method ready, amount confirmed, execution attempted, status finalized, export reconciled. This gives finance and engineering shared state definitions and gives support a clear answer when contractors ask for payout status.

We covered this in detail in The Best Way to Pay a Team of Contractors in Latin America.

Compare Pix against TED, DOC, and international rails for real operating scenarios#

For most local Brazilian real (BRL) payouts, use Pix as the primary rail, keep TED as a controlled domestic fallback, treat DOC as exception-only, and route to international rails only when local BRL payout is not possible.

Step 1 Prefer the rail that matches your operating tempo#

Pix is typically the best fit for local BRL payouts where speed and clear status matter. It was launched by the Brazilian Central Bank in November 2020, and a cited Central Bank note reported that by late 2024 it was Brazil's most-used payment method, with 76.4% population usage.

TED (Transferência Eletrônica Disponível) remains a domestic option and is described as a same-day settlement rail, especially for larger amounts. Use it when your provider or treasury flow is bank-account-led, but run it with explicit operational controls for processing windows, acknowledgment timing, and exception handling.

If DOC is available, do not treat it as interchangeable with Pix or TED. The grounding here does not support assuming the same timing or cutoff behavior, so keep DOC behind a documented exception rule.

A practical check is to run one test payout per rail after your usual approval batch time and confirm: expected status path, provider reference returned, and one clear final reconciliation state.

Step 2 Separate payout fees from FX and funding effects#

Do not read "no provider payout fee" as "no payout cost." A local BRL payout can still carry cost from funding and conversion effects outside the provider's payout-request fee.

Keep these as separate ledger lines:

- Provider payout fee policy

- Funding currency vs settlement currency effects

- Any conversion reference used before settlement

This prevents a common month-end mismatch where only provider fees are booked and BRL conversion effects are treated as noise.

Step 3 Route cross-border only when local BRL is unavailable#

Use international rails only when the contractor cannot be paid locally in BRL. Before execution, validate IBAN/SWIFT data quality and provider acceptance up front, instead of treating cross-border routing as a last-minute fallback. If you need a refresher on data differences, use IBAN vs. SWIFT.

| Scenario | Recommended primary rail | Fallback rail | Practical routing logic |

|---|---|---|---|

Marketplace payouts in Brazil | Pix | TED | Default to local BRL via Pix; use TED when Pix readiness or coverage is missing. |

| Creator platform cashouts | Pix | TED | Prioritize fast local BRL payout; keep TED for recipients on bank-transfer paths. |

| B2B contractor payouts | Pix for local BRL, TED when AP flow is bank-account-led | International rail with IBAN/SWIFT when local BRL is not possible | Choose rail based on whether domestic BRL payout is feasible first. |

That hierarchy keeps rail logic clear: local BRL first, domestic bank-transfer fallback second, cross-border only when domestic payout is not possible. For a full process view, see How to Pay International Contractors With Fewer Delays and Disputes.

Set up reconciliation and audit evidence before scaling volume#

Do not scale payout volume until your reconciliation evidence is explicit, consistent, and auditable end to end. The material here does not define Brazil-specific field rules, status-mapping rules, tax-artifact requirements, or SLA thresholds, so your team needs to define and enforce those internally before volume grows.

Step 1 Standardize one evidence pack for every payout batch#

Define one required evidence schema for each payout and each batch, then apply it across all rails and fallback paths. At minimum, make sure your records let ops, finance, and tax answer the same four questions quickly: what happened, when it happened, who it affected, and how it was posted in the ledger. If a record is missing key trace data, treat it as an open operational defect rather than cleanup work.

Step 2 Reconcile by status class, not by net totals#

Do not rely on net-total matching alone. Reconcile using explicit status classes and ledger outcomes so each payout can be traced from operations data to accounting data without guesswork. This guide does not define which status classes or mappings to use, so document your own status-to-ledger rules and review mismatches as exceptions.

Step 3 Attach tax artifacts and auto-open exceptions#

If your process uses NF-e (Nota Fiscal Eletronica) and ISS artifacts, link them directly to payout records so audits do not depend on email or chat history. This guide does not define the required artifact set or SLA timing, so set internal rules for both and enforce them consistently. For related onboarding context, see Hiring Contractors in Brazil: CPF/CNPJ ISS Tax and PIX Payment Compliance, and for adjacent tax context, see A Guide to Tax Residency in Brazil for Digital Nomads.

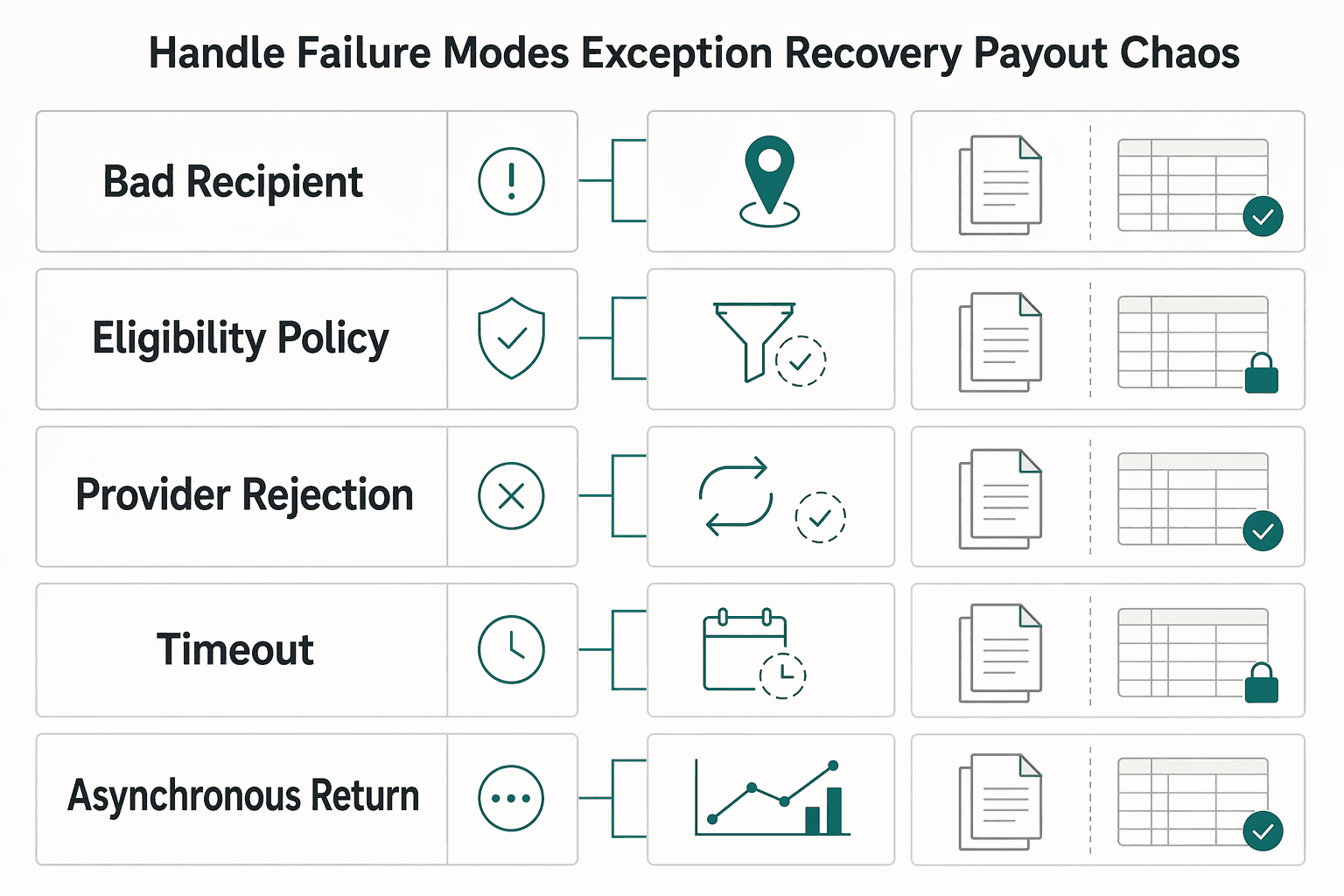

Handle failure modes and exception recovery without payout chaos#

Treat exception recovery as a controlled workflow, not a retry race. On real-time rails, partial failures happen, so the safest path is to classify the issue first, apply a predefined recovery action, and protect auditability and ledger accuracy at each step.

| Exception class | Meaning | Default action |

|---|---|---|

| Bad recipient data | Payee identity or recipient data does not match the intended contractor record (for example CPF/CNPJ path mismatch) | Correct data issues in the source record, then replay |

| Eligibility or policy block | Your internal rules should stop release (approval, compliance, or documentation hold) | Hold policy/compliance blocks for review |

| Provider rejection | The processor returned a clear rejection | For provider rejection with valid payee data, use your approved fallback path (for example Pix to TED/DOC) only if audit trace remains complete |

| Timeout | Outcome is unknown at the moment of failure | Resolve status first and avoid blind auto-retries |

| Asynchronous return | A payout looked accepted first, then funds returned later | Run a defined return-funds flow and reopen liability cleanly |

Step 1 Classify the exception before you retry anything#

Require every exception to be tagged before an operator can act:

| Exception class | What it means operationally |

|---|---|

| Bad recipient data | Payee identity or recipient data does not match the intended contractor record (for example CPF/CNPJ path mismatch). |

| Eligibility or policy block | Your internal rules should stop release (approval, compliance, or documentation hold). |

| Provider rejection | The processor returned a clear rejection. |

| Timeout | Outcome is unknown at the moment of failure. |

| Asynchronous return | A payout looked accepted first, then funds returned later. |

Before any replay, confirm the case shows payout ID, provider reference (if available), identifier class, last status timestamp, and current ledger state.

Step 2 Preassign one recovery action to each class#

Do not decide recovery in the middle of an incident. Map each class to one default action:

- Correct data issues in the source record, then replay.

- Hold policy/compliance blocks for review.

- For provider rejection with valid payee data, use your approved fallback path (for example

PixtoTED/DOC) only if audit trace remains complete. - For timeouts, resolve status first and avoid blind auto-retries.

- For asynchronous returns, run a defined return-funds flow and reopen liability cleanly.

This is a speed-versus-certainty choice: when status is ambiguous, prioritize duplicate-payment prevention over fast replay.

Step 3 Escalate unresolved cases before they hit churn or close#

Set escalation checkpoints by business impact, not queue age. If a contractor-facing payout remains unresolved after first review, escalate to an owner who can decide communication, rail switch, or release hold. If it is still open near close, escalate to finance with the full evidence pack so reconciliation does not break at month end.

A practical ownership split is: ambiguous status to payments ops, identity/compliance mismatches to compliance or onboarding, and returned-funds cases to finance until ledger correction is complete. For the full breakdown, read A Guide to Using Wise for Payroll for International Contractors.

Run a controlled launch and monitor the first month#

Launch in a controlled cohort first, not across all Brazil contractors at once, so you can validate your real payout behavior before scale.

Step 1 Start with a split cohort#

Use a limited live cohort in Brazil, split between Autonomo and Pessoa Juridica (PJ), with the same release criteria for both groups. The goal in month one is signal quality, not volume, so you can spot differences in how your payout paths behave under live traffic.

Verification point: each payout record should expose contractor type, identifier class, internal payout ID, provider reference (when available), and last status timestamp for reconciliation.

Step 2 Track daily outcome metrics#

Monitor daily results for the first month: success rate, time-to-settlement, exception rate, and the share of payouts that required fallback from Pix to TED or DOC.

Pix is built for transfers in seconds and is available 24 hours a day, 7 days a week, including weekends and holidays. If delays or manual interventions trend up, treat that as an early warning even when total completed payouts still look acceptable.

Step 3 Hold a weekly cross-functional review#

Run a weekly finance-and-engineering review and close repeated issues with a named owner and a rule change. Tighten onboarding checks when input quality is the root cause, and update routing logic when execution behavior is the issue.

By the end of month one, you should have fewer manual touches, clearer fallback rules, and cleaner audit evidence.

Conclusion#

Brazil is already operating at a scale where Pix is hard to treat as a niche rail. Reuters reported that since its launch in late 2020, Pix surpassed the combined number of credit and debit card transactions in 2023. That makes Pix a strong rail to test early for local BRL contractor payouts in Brazil, while still pairing speed with clear controls for routing, evidence, and exception handling.

Copy/paste launch checklist#

Step 1. Confirm the contractor path before you confirm the payment method. Lock one onboarding path per payee and make sure the contractor profile, payout instruction, and reconciliation export all use the same core record details. If those records disagree, stop release and fix the source record first.

Step 2. Decide the rail in advance, not at failure time. If you are funding and paying locally in BRL in Brazil, test Pix as your primary route. If that route cannot complete, define and test the fallback path up front with your provider. The red flag is a payout queue that says "Pix preferred" with no tested fallback path.

Step 3. Separate funding from cost. Confirm where BRL comes from and who can explain the full payout cost. Finance should be able to see provider payout fees separately from FX or exchange impact, or you will get false "low cost" assumptions in reporting. A useful verification point is whether one payout batch can be tied back to both a funding source and a fee view without manual thread chasing.

Step 4. Write down ownership for tax and privacy artifacts. Do not leave tax and data-handling responsibilities implied between ops, finance, and legal. Even when the exact obligation depends on your model, you want named owners, retention rules, and a clear answer on who reviews missing or inconsistent artifacts. If nobody owns the exception, it will surface at month end.

Step 5. Make execution duplicate-safe and observable before volume arrives. A fast rail does not protect you from duplicate sends, delayed acknowledgments, or stale status screens. You want controlled retry behavior, provider reference capture, and a defined escalation point when provider status and your internal records do not line up. If you cannot show request accepted, provider reference received, and final status posted, do not call the payout done.

Step 6. Require a reconciliation pack for every batch. At minimum, keep the internal payout ID, contractor record key, amount and currency, payout method used, provider reference when available, status timeline, and posting record. That pack is what turns a quick payment rail into an auditable operation. If any "completed" payout cannot be traced across those records, treat it as an exception, not a rounding error.

Related reading: Brazil's CNPJ for Foreign-Owned Businesses: When It Is Needed and What It Does.

Frequently Asked Questions

Can you pay contractors in Brazil with `Pix` if your platform is global?

Yes, if your payout setup can execute a local Brazilian real (BRL) transfer in Brazil or your provider offers a cross-border Pix product. The key check is provider coverage and operating model, not whether your platform serves multiple countries. A global product does not automatically mean local Pix reach.

Is `Pix` always instant for contractor payouts, or does provider workflow still add delay?

Pix is described as instant and available 24/7 in a secondary source, but that does not make your full payout flow instant every time. Banco Central do Brasil reports Pix transaction data monthly, including transactions settled within and outside SPI, so treat "instant" as a network capability rather than a guaranteed end-to-end processing time in every provider flow.

When should you choose `Pix` instead of `TED` or `DOC`?

If your provider supports multiple rails, Pix is often the first option when faster availability matters, including outside business hours. Keep TED or DOC as fallback options when the Pix route is unavailable for that payout path. Exact handling and eligibility rules depend on provider setup.

What is usually included in payout cost for `Pix` in `Brazilian real (BRL)` versus non-`BRL` flows?

For local BRL payouts, cost usually means whatever your provider charges to execute the payout, not a universal market price. For non-BRL or cross-border flows, separate the transfer fee from FX or conversion cost so finance does not treat them as one line item. One vendor, PagBrasil, markets international Pix with a “small, fixed fee” and FX-rate-lock messaging, but that is a vendor offer, not a rule for all providers.

What contractor data is typically needed for payout readiness, including `CPF` and `CNPJ`?

Pix payouts use a Pix key to route the transfer, such as a phone number or email, and keys are registered in DICT. Beyond that, required contractor fields, including whether CPF or CNPJ is needed, depend on your provider and payout path. The practical verification step is to confirm the key is valid and registered in DICT, or at least passes your provider's validation, before release.

How do `IBAN` and `SWIFT` matter if a contractor cannot be paid locally via `Pix`?

If a payout moves off the local Pix route to international bank rails, follow the routing data rules required by your provider and destination banking path, and validate those fields before execution. See also IBAN vs. SWIFT: How to Know Which Code to Use When Paying International Contractors.

What are the minimum reconciliation records finance should require for audit-ready Brazil payouts?

These sources do not define one universal minimum schema, so treat this as an internal control decision with finance and your provider. Set a standard that lets finance consistently trace payout outcomes to ledger records and provider-side status history.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 1 external source outside the trusted-domain allowlist.

- academia.edu/41404272/Rescuing_Participationtrusted

- bcb.gov.br/en/financialstability/pix_entrusted

- bis.org/publ/bppdf/bispap152_c.pdftrusted

- elibrary.imf.org/view/journals/002/2023/289/article-A004-en.xmltrusted

- oecd.org/content/dam/oecd/en/publications/reports/202...trusted

- sec.gov/Archives/edgar/data/1770883/0000950103210065...trusted

- snap.berkeley.edu/project/10053261trusted

- blog.xtrm.com/posts/2026-global-payout-infrastructureexternal

Educational content only. Not legal, tax, or financial advice.

Related Posts

Hiring Contractors in Brazil: Classification, Invoicing, Payout Controls, and Audit Records

If you own compliance, legal, finance, or risk, hiring contractors in Brazil is mainly a classification and recordkeeping control problem, not a sourcing problem. Misclassification risk can create retroactive liability when a contractor or PJ setup operates like employment.

Invisible Payouts: How to Remove Payment Friction for Contractors Without Sacrificing Compliance

Invisible payouts should make life easier for contractors without hiding the controls your team needs. Contractors should get a predictable, low-friction flow, while internal teams can still enforce and document payout decisions when needed. If you run contractor payouts at scale, you need both outcomes at once. We recommend treating every easy payout as a controlled release path your team can replay later.

IBAN vs SWIFT for International Contractor Payouts on Platforms

If you are scaling international contractor payouts, treat code choice as a release control, not a glossary question. The practical rule is simple: collect the right bank identifiers up front, validate them before approval, and keep enough evidence to explain every submitted, rejected, returned, or retried payout later.