Quick Answer

Use a risk-first workflow: finalize an outcome-based contractor contract, collect the correct IRS form before money moves, confirm Australian tax and super treatment on its own merits, and pay through a trackable rail with clear FX and fee visibility. For an australian agency pay us contractor setup, fintech transfers are often practical for recurring invoices, while business-critical engagements may warrant a higher-control platform. Keep contract, invoice, and remittance records together from the first payment.

Beyond the Handshake: Crafting an Ironclad Partnership Agreement#

Put a signed written contractor agreement in place before work starts and before you approve the first invoice. It should do four jobs: clarify contractor status, set IP ownership, spell out payment and dispute mechanics, and make exits clean.

Do not rely on the contractor label alone. Classification disputes turn on the contract's actual terms, and both Australian and US guidance focus on control, especially who controls how the work is done. Draft for the relationship you intend to run in practice.

The exposure is real if you get this wrong. Sham contracting is unlawful in Australia. The ATO/FWO release published on 13 March 2026 cites penalties up to $19,800 for individuals and $99,000 for businesses with fewer than 15 employees. For businesses with 15+ employees, it cites the greater of $495,000 or 3 times the underpayment amount. Separate from sham contracting penalties, incorrect treatment can also trigger tax and super exposure, including Part 7 penalties of up to 200% of the super guarantee charge.

The four clauses that matter most#

- Status and scope clause

State that the US professional is engaged as a genuine contractor, then define the work by services, deliverables, milestones, or results. Write to outcomes, not prescribed methods or fixed day-to-day control. If your draft dictates exact hours, daily supervision, or step-by-step execution, tighten it.

- IP ownership clause

State exactly who owns IP created during the engagement. In Australia, contractor-created IP defaults to the contractor unless your contract says otherwise. If you use US "work made for hire" language, make sure any required express written agreement is in place so ownership is not left ambiguous.

- Liability, payment, and dispute clause

Make the commercial mechanics easy to follow: how much is paid, when, how it is paid, what counts as acceptance or completion, and how disputes are handled. This is the clause that prevents invoice stand-offs when approval expectations are fuzzy.

- Termination and offboarding clause

Define how the engagement closes out and what must happen before the contract is treated as finished. Keep closeout terms clear so final invoicing and dispute handling are straightforward.

Clause matrix#

| Clause | What to include | Risk if missing |

|---|---|---|

| Status and scope | Genuine contractor statement, services/results, milestone-based scope, outcome-focused drafting | Reclassification risk and weaker defense if challenged |

| IP ownership | Explicit ownership language for contractor-created IP | Contractor may retain default ownership under Australian IP rules |

| Liability, payment, and disputes | Amount, timing, method, acceptance/completion conditions, dispute process | Payment delays, invoice stand-offs, and unclear resolution path |

| Termination and offboarding | Clear closeout terms, completion conditions, and final invoice process | Messy exits and disputes over what is still owed |

Before first invoice contract QA checklist#

Before you approve the first invoice, run a clean QA pass against the signed agreement and onboarding file:

| Area | What to confirm | Timing |

|---|---|---|

| Written agreement | Both parties signed the written agreement | Before the start date |

| Scope | Scope is outcome-based; remove fixed-hours or method-control language unless reviewed | Before you approve the first invoice |

| IP ownership | The IP clause clearly states ownership for contractor-created work | Before you approve the first invoice |

| Payment and disputes | Amount, timing, method, and acceptance/completion conditions are completed | Before you approve the first invoice |

| Closeout | The contract states what must be completed before the contract is treated as finished and final invoicing can proceed | Before you approve the first invoice |

| W-8BEN | Collect a completed W-8BEN if your withholding analysis requires it | Before first payment |

- Confirm both parties signed the written agreement before the start date.

- Check that scope is outcome-based; remove fixed-hours or method-control language unless reviewed.

- Verify the IP clause clearly states ownership for contractor-created work.

- Complete payment and dispute fields: amount, timing, method, and acceptance/completion conditions.

- Confirm closeout language states what must be completed before the contract is treated as finished and final invoicing can proceed.

- If your withholding analysis requires it, collect a completed W-8BEN before first payment.

If you only make one improvement, make it this: make sure the contract matches the real working relationship. Clear terms do not fix bad practices, but vague terms make a defensible contractor engagement much harder.

Once the paper is right, the next risk is how you run the engagement day to day. If you want a deeper dive, read Separating Business and Personal Finances: An Important Step for LLCs.

Avoiding the Misclassification Minefield#

Use this as a records-and-status self-audit. There are no specific legal tests here for control, independence, or financial risk, so treat those areas as case-specific.

- Control over the work

Specific control thresholds are not provided in the sources here. Use this as an internal consistency check only: make sure your contract terms and day-to-day working arrangement do not contradict each other, and escalate unclear cases for legal review.

- Independent business status

Check whether the person is operating as a business in their own right. The ABR states that individuals carrying on an enterprise can be entitled to an ABN, and that if someone is engaged as an employee for an activity, they are not entitled to an ABN for that activity. The ABR also states that a sole trader is legally responsible for business debts and for their own super, and for any workers they employ. For non-resident businesses, records may instead reflect ATO simplified GST registration: an ARN (12-digit identifier), quarterly GST lodgment and payment, and limited registration restrictions, including that they cannot issue tax invoices or claim GST credits.

- Financial risk and commercial boundaries

Specific financial-risk thresholds are not provided in the sources here. Treat this as case-specific too, and make sure your records match the arrangement as it operates in practice.

| Signal | What is supported | Risk if mismatched | Fix |

|---|---|---|---|

| ABN entitlement | Individuals carrying on an enterprise can be entitled to an ABN; employees are not entitled to an ABN for that activity | Status on file may not match the activity | Correct the status and records for the activity |

| Sole trader obligations | Sole traders are legally responsible for debts and for super (their own and workers they employ) | Responsibilities may be assumed incorrectly | Document and align responsibilities with the setup |

| Simplified GST registration (non-resident) | Registrants receive an ARN, lodge/pay GST quarterly, and cannot issue tax invoices or claim GST credits | ABN-style handling may be applied to limited registration | Align invoicing and GST handling to simplified registration rules |

Run these misclassification prevention checks:

- Verify your records match actual business status.

- Confirm whether the identifier on file is an ABN or, where applicable, a 12-digit ARN.

- If simplified GST registration applies, confirm quarterly lodgment/payment and limited-registration constraints.

- Flag control and financial-risk issues as unresolved.

If these checks hold up, the next control is simpler: confirm payment setup documentation before money moves. We covered related payment setup issues in The Best Way to Pay an Indian Development Agency from the US.

The Compliance Secret Weapon: The W-8BEN Form#

Treat the W-8 step as part of onboarding, not post-payment cleanup. Collect the correct IRS status form before the first payout, confirm that it matches the payee, and store it with the contractor file.

Do not request W-8BEN by default for every cross-border payment. The form depends on who the payee is: W-8BEN for foreign individuals, W-8BEN-E for foreign entities, and W-9 for U.S. persons. The payee gives the form to you as the payer or withholding agent, and you retain it in your records.

| Form scenario | Which form applies | Who completes it | Common mistake to avoid |

|---|---|---|---|

| Foreign individual contractor | Form W-8BEN | The individual contractor | Requesting this from a U.S. person who should provide Form W-9 |

| Foreign company or entity contractor | Form W-8BEN-E | The entity | Letting an individual submit the entity form |

| U.S. person contractor | Form W-9 | The U.S. person contractor | Treating every international payment as a W-8 case |

- Request before first payout.

Build this into onboarding so the right form is in place before income is paid or credited.

- Review for completeness and fit.

Confirm the form matches the payee type, whether individual, entity, or U.S. person, and is not obviously incomplete.

- File in your records, then handle Australia separately.

W-8 documentation supports U.S. withholding and reporting records, but it does not answer Australian tax or super questions. Worker classification still drives Australian obligations, and contractor and supplier records should be retained for 5 years.

- Treat missing or stale forms as payment risk.

If a requested W-8BEN is not provided, withholding consequences can apply. These can include the 30% foreign-person withholding rate or backup withholding under section 3406. W-8BEN is generally valid through the end of the third succeeding calendar year, unless a change in circumstances makes the form incorrect earlier.

In practice, a simple four-step routine is enough for most teams:

- Request the correct IRS status form with the contract pack before first payment approval.

- Review that the form matches payee status and is complete.

- File it with the agreement, invoices, and payment proof in the contractor compliance folder.

- Renew W-8BEN on a change in circumstances or at the IRS validity endpoint.

Once the U.S. form is filed in your records, you still need a separate Australian decision on tax, super, and related obligations. For a step-by-step walkthrough, see The Best Way for a German Agency to Pay a US-Based Freelancer.

Your Australian Obligations, Simplified#

Do not treat offshore delivery or a completed W-8BEN as clearance on the Australian side. PAYG withholding, superannuation, and exact record-retention requirements are not resolved here for your specific arrangement, so verify each area separately and keep an audit file showing how you made each decision.

Non-resident status and offshore work can matter, but only after the worker arrangement and payment facts are documented. Nothing here states that a W-8BEN determines Australian PAYG, super, or GST outcomes.

| Obligation area | When it applies | When it does not apply | Evidence to retain |

|---|---|---|---|

| PAYG withholding | When Australian withholding rules apply to the actual arrangement. Verify directly. | Do not assume it is excluded just because the contractor is U.S.-based or works offshore. | Signed agreement, classification review note, invoices, contractor details, any tax advice |

| Superannuation | When Australian super rules apply to the actual arrangement. Verify directly. | Do not assume it is excluded just because the contract says "independent contractor." | Contract, scope of services, classification memo, payment records, any legal or accounting advice |

| GST registration | When GST registration is required based on your business activities. If required, register within 21 days. | The ATO states not every business or enterprise must register for GST, so do not assume yes or no without checking. | ABN record (standard pathway), or ARN details (simplified pathway), GST registration notice with effective date, BAS records if registered, internal note on why registration was or was not required |

| Record keeping | Keep a file that shows who you paid, why you treated them as a contractor, and how tax treatment was handled. | It does not become optional because the contractor is overseas. | Full audit file, with retention period verified separately for your case |

Do not stop at "we have a W-8BEN." Your control is to make sure the contract party, invoice party, and tax form party align. Keep a short written note on classification and Australian tax treatment, including adviser confirmation where used.

GST needs extra care because the ATO material here is specific. $75,000 appears here as a GST turnover figure, but the list shown is truncated, so do not treat that as the only trigger. What is clear is that, if registration is required, it is time-bound and penalties may apply if you fail to register when required. For non-residents, standard and simplified GST registration have different capabilities; simplified registration is limited and does not allow tax invoices or GST credit claims. Keep the ATO notice showing the effective date.

Build an audit file, not a loose folder#

The safest move here is not more paperwork for its own sake. It is one file that lets another reviewer reconstruct your decisions quickly.

| File item | Details |

|---|---|

| Agreement | Signed contractor agreement and any scope changes |

| Tax status form | Relevant tax status form from onboarding, for example W-8BEN |

| Payment records | Invoices and proof of payment |

| Identity details | Contractor identity and business details |

| Review note | Your classification and Australian-obligations review note |

| GST support | GST registration records, BAS support, ARN details, or adviser correspondence where relevant |

At minimum, include these items in the file:

- signed contractor agreement and any scope changes

- relevant tax status form from onboarding, for example W-8BEN

- invoices and proof of payment

- contractor identity and business details

- your classification and Australian-obligations review note

- GST registration records, BAS support, ARN details, or adviser correspondence where relevant

Then use this operating checklist to close the loop:

- Confirm the agreement reflects the actual contractor relationship.

- Collect and file the relevant tax status form before first payment.

- Verify PAYG, super, and GST treatment separately instead of inferring from offshore status.

- Store the decision note, invoices, and payment proof in one audit file and retain it for the verified required period.

Once compliance is documented, choose a payment method that will not undermine the controls you just built. Related: What to Do If You've Been Misclassified as an Independent Contractor.

Choosing Your Payment Rails: A Framework for Risk vs. Cost#

Choose your rail by downside risk first, then optimize cost. Here, a delayed, returned, or held payment usually costs more than small FX or transfer-fee savings.

For many recurring contractor payouts, Tier 2 fintech rails are a practical default. Move to Tier 1 when a payment failure would be expensive to unwind. Use Tier 3 when policy or recipient constraints require it. Treat Tier 4 as a last-resort convenience option.

| Tier | Rail | Settlement predictability | FX transparency | Hold or dispute exposure | Compliance tooling | Reconciliation quality | Best-fit use case |

|---|---|---|---|---|---|---|---|

| 1 | Specialized contractor platform or EOR | Provider-dependent; request written payout timing and exception handling | Provider-specific | Provider-dependent; review reserve, reversal, and dispute terms | Provider-dependent; verify onboarding, approvals, and record outputs | Can be cleaner when contract, approval, and payout sit together | High-value, long-term, or business-critical contractor payments |

| 2 | Fintech transfer service such as Wise | Predictable when set up early. Wise provides a transfer tracker; USD timing varies by rail: ACH 0-3 working days, wire same day or following working day, SWIFT 1-6 working days | Wise says it uses the mid-market rate; check current fees at send time | Lower disruption than consumer wallets, but verification can pause a transfer. Wise says checks can take 5-14 working days | Batch payments by CSV or XLSX, up to 1,000 transfers per batch file, plus downloadable statements for up to 365 days | Strong for recurring payouts and month-end audit trails | Regular contractor payments where cost and visibility both matter |

| 3 | Direct bank international transfer | Usable, but less predictable. Westpac says files are typically processed in 1-3 business days and can take longer | Often less transparent because overseas or correspondent bank charges may apply | Returns are possible if details are wrong, and overseas banks may deduct fees | Bank payment tracking may be available in online channels | Adequate if your finance team already reconciles from bank records | Infrequent payments or bank-policy-driven transfers |

| 4 | Consumer wallet or speculative rail | Lower predictability for professional payouts when timing matters | PayPal says its conversion includes a retained spread over a base rate | Highest disruption risk. PayPal says disputes place funds on temporary hold, and rare holds can last up to 21 days | Provider policies vary; confirm hold and dispute workflow upfront | Harder to run as a stable recurring pay rail | Small, non-critical one-off payments only, if both sides accept the risk |

Tier 1 Specialized contractor platforms and EORs#

Use this tier when payment failure has a high business cost. It fits core contractors, high monthly amounts, or engagements where finance, legal, and account teams need one auditable trail.

It stops making sense when provider overhead outweighs the risk you are trying to control. Before you commit, get written payout timing, exception handling, and reporting details, and file them with the onboarding records. If hold, reversal, or approval flow is unclear, treat that as a warning sign.

Tier 2 Fintech transfer services like Wise#

For many agencies, this is a strong balance of cost and control. Wise says it uses the mid-market rate, provides in-account transfer tracking, and allows transfer-history downloads for up to a 365-day period. Batch files also support recurring operations at scale.

This tier works for planned, repeatable payouts. It breaks when setup is left too late. Wise states transfers can pause until verification finishes, and that process can take 5-14 working days. Complete verification before urgent deadlines and do not assume first-transfer speed will match later cycles.

A practical setup check is the recipient rail. Wise says USD receiving details can include an account and routing number, and that senders can pay domestically in the US or via SWIFT.

Tier 3 Direct bank transfers#

Use this tier when policy requires bank-to-bank rails or the contractor cannot receive through fintech options. It works, but cost and the final received amount can be less predictable.

The common failure mode is wrong beneficiary data. Westpac notes incorrect details can cause returns, and CommBank states overseas banks may deduct processing fees. Verify payee details against the agreement and current invoice, then send remittance details immediately so the contractor can reconcile receipt.

Tier 4 Consumer wallets and speculative rails#

Use this only when both sides explicitly accept disruption risk. PayPal states FX conversion includes a retained spread, and disputes, claims, and chargebacks can trigger temporary holds, with rare cases lasting up to 21 days.

For routine contractor obligations, this is usually the wrong default. ASIC describes crypto-assets as inherently risky, complex, and highly speculative, which increases disruption risk for time-sensitive pay cycles.

Execution checklist#

Use the same release discipline every time:

- Before first payment: Confirm contract party, invoice party, and payee details match; collect Form W-8BEN when requested by you as payer; confirm it is still valid unless circumstances changed; complete provider verification before any urgent due date.

- For every transfer: Retain invoice, transfer confirmation, amount sent, FX detail shown at send time, beneficiary details used, tracker or bank status, and exception notes. Keep contractor and supplier records for 5 years.

- If delayed or held: Check tracker or bank status first, confirm whether verification or payee-detail errors are blocking release, and notify the contractor before resending. If timing is critical, escalate with the provider and move the next cycle to a more predictable tier.

If you need a quick check on common edge cases, use the FAQ below before you release the first payment. You might also find this useful: How to Pay US-Based Contractors from Australia.

Before you lock in a rail, run your typical invoice sizes through a side-by-side cost check using the payment fee comparison tool.

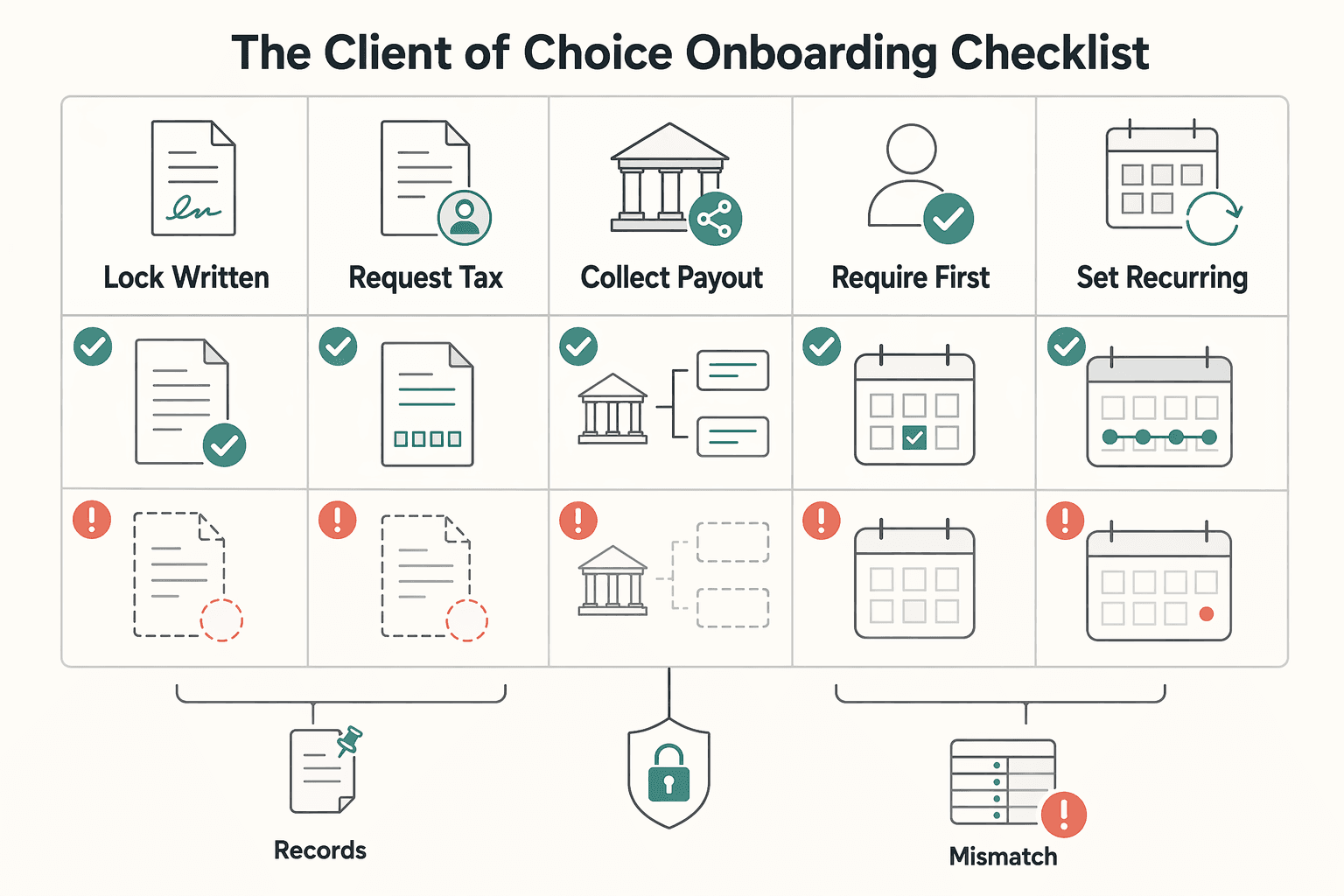

The "Client of Choice" Onboarding Checklist#

Treat onboarding as a release gate. Do not send the first payment until one owner can show a complete file, a verified payout path, and a contractor who knows what happens next.

| Step | Owner | Required artifact | Completion signal |

|---|---|---|---|

| Lock the written agreement before work starts | The person managing the engagement | A signed contract file that states scope, contractor status, and how much, when, and how you will pay | Both sides have signed |

| Request the tax form that actually fits the worker | Finance or accounts payable | The received tax form plus a short note on why that form applies | The form is complete, legible, and filed before first payment |

| Collect payout details through your payment provider, then verify them against your file | Finance | Beneficiary details, payout method, and a verification note that matches the invoice name and agreement | Payout method is verified and ready for release |

| Require the first invoice and pay to the agreed terms | Accounts payable | First invoice, remittance advice, and payment confirmation record | Transfer shows delivered and the contractor confirms receipt |

| Set the recurring payment rhythm before the second invoice | Finance with the engagement manager | Agreed timing, method, approval cutoff, and contact for payment questions | Both sides can point to the next payment date and process |

- Lock the written agreement before work starts.

Owner: the person managing the engagement. Required artifact: a signed contract file that states scope, contractor status, and how much, when, and how you will pay. Completion signal: both sides have signed. Why this reduces risk: a written contract is less risky than a verbal one, and it gives you a clear record if the relationship later drifts toward sham contracting, which is illegal.

- Request the tax form that actually fits the worker.

Owner: finance or accounts payable. Required artifact: the received tax form plus a short note on why that form applies. Completion signal: the form is complete, legible, and filed before first payment. Why this reduces risk: it prevents one-form-fits-all handling. If the worker is a U.S. person, use Form W-9. Use Form W-8BEN only for a foreign beneficial owner when requested by the payer or withholding agent. If the form is incomplete, pause setup and return it for correction.

- Collect payout details through your payment provider, then verify them against your file.

Owner: finance. Required artifact: beneficiary details, payout method, and a verification note that matches the invoice name and agreement. Completion signal: payout method is verified and ready for release. Why this reduces risk: verification catches detail mistakes before funds move. If details fail verification, cancel and recreate with corrected details if transfer status allows it. If funds do not return after a few business days, contact your bank to trace the payment.

- Require the first invoice and pay to the agreed terms.

Owner: accounts payable. Required artifact: first invoice, remittance advice, and payment confirmation record. Completion signal: transfer shows delivered and the contractor confirms receipt. Why this reduces risk: invoices and amounts paid are part of the ATO record set you need to keep. If the first payout is delayed, do not resend blindly. Timing depends on provider and rail; Wise states a local bank transfer can take up to 2 business days, and a Swift transfer can take 4 to 5 business days.

- Set the recurring payment rhythm before the second invoice.

Owner: finance with the engagement manager. Required artifact: agreed timing, method, approval cutoff, and contact for payment questions. Completion signal: both sides can point to the next payment date and process. Why this reduces risk: predictable timing reduces one-off exceptions and keeps expectations clear.

For Australian record-keeping, keep the contract, form decision note, invoices, amounts paid, and payout proof together for 5 years.

Go / no-go before release

- Go only if the contract is signed, the tax form decision is documented, and the first invoice matches the agreement.

- Go only if payout details are verified and you know what to do if the transfer is delayed, fails, or needs correction.

- No-go if any file is missing, the form is incomplete, or the contractor has not received a clear payment timeline and contact point.

This pairs well with our guide on How to Pay US-Based Freelancers from the UK.

When you want this checklist to run as a repeatable operation with compliance gating and status tracking, review Gruv Payouts.

Frequently Asked Questions

What about Form W-8BEN?

There is nothing here confirming that Form W-8BEN is required for this scenario. Treat this as case-specific and confirm the current requirement with qualified tax advice before payment setup. Keep any form used and the written advice you relied on.

Do I need Australian GST registration for this arrangement?

It depends. If your GST turnover reaches $75,000, the ATO says you must register within 21 days, and penalties may apply if you do not. Before registering, you need an ABN for standard GST registration; non-residents using standard registration must lodge BAS and pay GST monthly or quarterly. If simplified GST applies, you do not get an ABN, cannot issue tax invoices, cannot claim GST credits, and must lodge and pay GST quarterly. Keep the ATO registration notice with the effective date, or your simplified registration details.

Do I have to pay super for a US contractor?

Not automatically. The ATO says your tax and super obligations vary based on whether the worker is an employee or an independent contractor, so check the actual working relationship before first payment. Keep your signed agreement, scope, invoices, and classification notes.

What is the most reliable way to pay a US contractor from Australia?

Use a method with clear fee and FX visibility, trackable status, and usable payout confirmations, then apply it consistently. Keep the transfer confirmation, beneficiary details used, and remittance advice for each payment.

How do I avoid misclassifying a contractor?

Assess the real working arrangement, not just the contract label. The ATO states obligations vary by worker status, and incorrectly treating an employee as a contractor can lead to penalties and charges. If the working arrangement changes, reassess the classification and get advice before continuing with the same setup.

Who pays currency conversion fees?

The provided ATO excerpts do not set a default rule for who bears currency conversion costs in this scenario. Define payment currency, FX-cost ownership, and what counts as full payment in your agreement before the first invoice, then verify the final send amount when you pay. Keep the relevant contract clause and the fee or FX screen shown at payment time.

What should I do if a transfer is delayed, failed, or held?

Do not resend until you can confirm what happened to the first payment. Check payment status and internal records, verify beneficiary details against the invoice and agreement, open a provider support case, and update the contractor on next steps. Keep the case ID, timestamps, screenshots, and any corrected payout details.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- ato.gov.au/businesses-and-organisations/international-t...trusted

- ato.gov.au/businesses-and-organisations/hiring-and-payi...trusted

- business.gov.au/people/contractors/prepare-a-contracttrusted

- copyright.gov/circs/circ30.pdftrusted

- irs.gov/individuals/international-taxpayers/forms-fo...trusted

- irs.gov/forms-pubs/about-form-w-8-bentrusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

How LLC Owners Separate Business and Personal Finances

For an LLC, separating business and personal money is best treated as a weekly habit, not a one-time bank setup. It keeps records cleaner, cuts month-end cleanup, and creates clearer boundaries as the company grows.

What to Do If You've Been Misclassified as an Independent Contractor

Treat this as a protection problem first, not a label debate. If your work was treated as an independent contractor arrangement even though the relationship functioned differently, your first goal is to protect pay, rights, and records while you choose the least risky escalation path. You can do that without making accusations on day one, which often keeps communication open while you document what happened.

How to Pay US-Based Contractors from Australia

Engaging U.S. talent can be a smart growth move for an Australian business. But paying a cross-border contractor is not just an admin task. If you handle it reactively, you create compliance risk, unnecessary cost, and record gaps that are hard to repair later.