Quick Answer

Start with classification and country documentation, then pick the rail that proves clean reconciliation on a live payout. To pay contractors in Latin America with fewer surprises, verify contractor status, collect required forms where applicable, and confirm beneficiary details before sending. Approve expansion only when the quoted amount, invoice, provider confirmation, and final received funds align, with a documented fallback path for failed transfers.

Start with payout risk, not convenience#

If you need to pay contractors in Latin America without cashflow surprises, start with risk, not convenience. Cross-border payouts can break on delays, hidden FX loss, or compliance friction, so the cheapest-looking option is not always the safest one to run.

-

Judge payouts by what the contractor actually receives. SWIFT fees can run $25-$50 per transfer in some cases, and FX markup can still reduce the landed amount, including an example where $1,000 USD ends up near $940 after fees and conversion. The useful test is whether you can estimate the final received amount before you release the batch.

-

Treat failure recovery as a core feature. Some transfers can take 3-7 business days, and a common failure mode is missing or mismatched local bank details. Validate recipient data before sending, including local account formats such as CLABE where relevant. Use providers that confirm delivery through a dashboard or webhook, not a vague "processing" status.

-

Run each country as its own operating environment. Mexico, Colombia, and Argentina do not share one payment or compliance rulebook. Classification, tax handling, payout operations, and compliance requirements vary by country. For example, contractors in Mexico issue electronic facturas under CFDI 4.0 standards, and tax-registration responsibility should be verified per engagement because sources conflict.

That country split applies to worker setup too. Here, contractor status depends on autonomy, financial independence, and no legal subordination, so misclassification and invoicing or compliance errors are live risks. Keep payment operations and classification decisions connected.

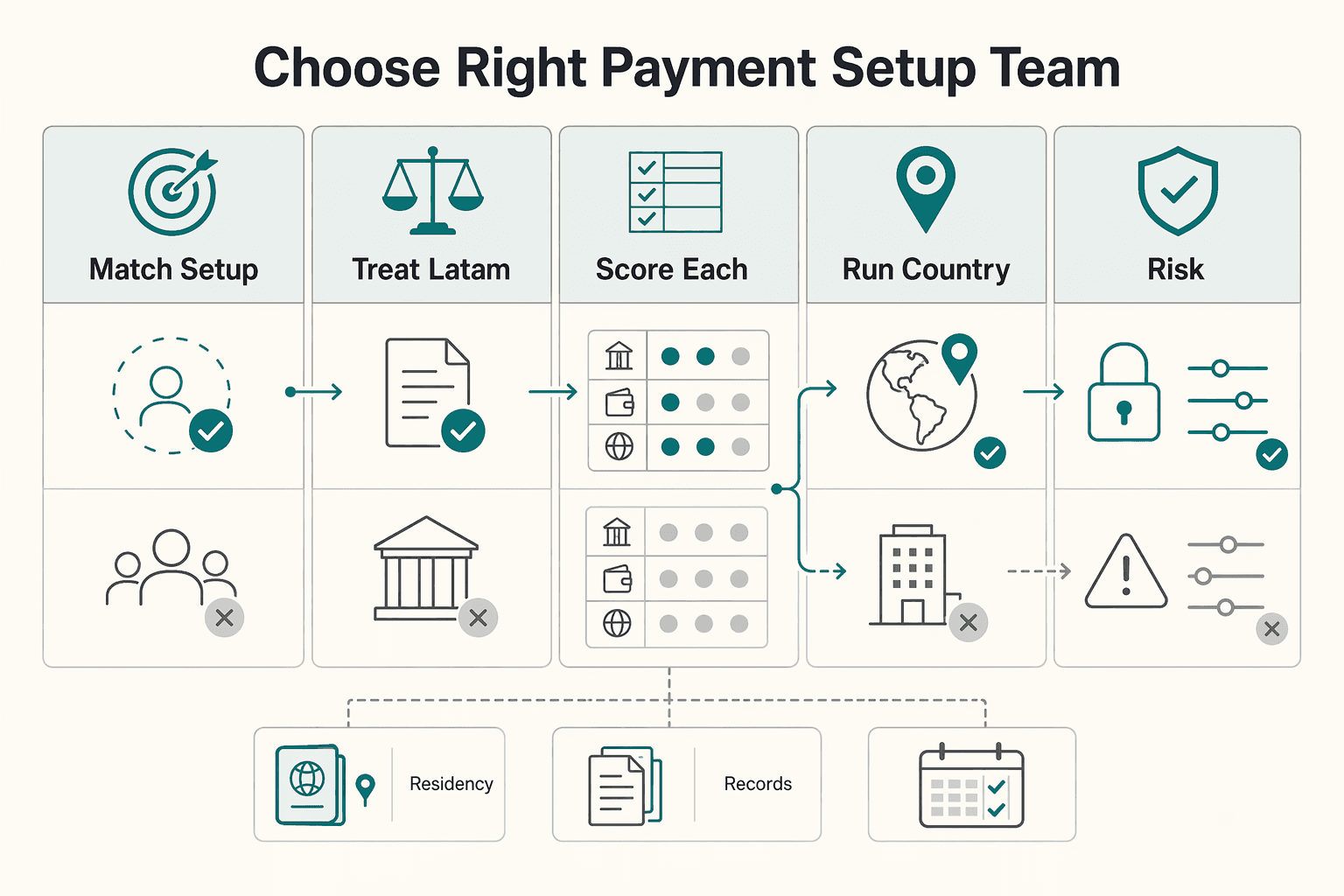

How to choose the right payment setup for your team#

Choose the legal model first, then the payment rail. If you are paying contractors across borders, confirm independent contractor classification before you compare banks, wallets, or platforms.

- Match the setup to the worker relationship.

Use this path for independent contractors, not full employment. If the role is really employment, an Employer of Record (EOR) is a different model. It is the legal employer in-country and handles payroll, taxes, benefits, and compliance.

- Treat LATAM as country by country, not one setting.

LATAM spans 33 countries with different contractor laws, tax rules, currency differences, and payment preferences, so one regional policy is not enough. Even within one market, a source notes 4 approaches to paying a contractor. Use that as a reminder to localize before you pick a rail.

- Score each option on five criteria every time.

Compare labor-law fit, tax handling, currency handling, local payment preferences, and fee or delay tradeoffs. A SWIFT wire transfer uses the Society for Worldwide Interbank Financial Telecommunication network, but wire routes still bring fee and delay tradeoffs tied to bank procedures.

- Run a country-specific pre-payment check before the first payout.

For a United States to Mexico contractor payment, one concrete checkpoint is to verify classification, use a locally compliant contract, and collect Form W-8BEN before payment. Use that as a pattern, not a template copied unchanged into other countries.

- If misclassification risk is high, fix that first.

Correct the contract and compliance position before you optimize rails, vendors, or payout steps. The decision rule is simple: resolve classification risk first, then optimize payment operations. For broader process controls, see How to Manage and Pay a Global Team of Contractors Compliantly.

The real cost stack behind every contractor payout#

Once classification is settled, landed cost is the real decision point. The number that matters is not the advertised send fee. It is what leaves your account, how conversion is handled, what gets deducted in transit, and what the contractor can actually use.

A rail can look cheap at initiation and still cost more in practice. Compare every method on the same fields, even when a provider cannot fully disclose the path up front.

1. Compare on landed cost, not just the send fee#

| Method | Platform fee | FX spread visibility | SWIFT or wire transfer charges | Return fees | Contractor-side withdrawal costs |

|---|---|---|---|---|---|

| Bank transfer | Bank-specific; confirm before sending | May be unclear from headline pricing; confirm rate source | Bank-specific; confirm all wire/transfer charges before sending | Confirm with sending and receiving banks | Confirm whether contractor pays to access or move funds locally |

| SWIFT | Bank-specific; confirm before sending | Confirm who sets conversion rate and when conversion happens | Confirm whether charges beyond the initial instruction apply, and who applies them | Amount not supported here; confirm before use | Confirm recipient-bank or local access costs |

| Wise | Transfer fee varies by route and currency; published pricing starts from 0.57% | Wise says it uses the mid-market rate and shows fee plus exchange-rate breakdown before confirmation | Wise lists 6.11 USD for receiving USD wire and Swift payments | Confirm per route and support outcome; no universal amount in source material | If the contractor uses a Wise card, fees depend on where the card was issued; help guidance says 2 free withdrawals or up to 200 EUR/month before extra fees, but not as a universal rule |

| PayPal | Not publicly documented; confirm corridor-specific pricing | Not publicly documented; confirm before approval | Not publicly documented; confirm funding and transfer charges | Not publicly documented | Confirm wallet-to-bank or cash-out costs borne by contractor |

| Payoneer | Not publicly documented; confirm corridor-specific pricing | Not publicly documented; confirm before approval | Confirm whether bank or withdrawal rail adds charges | Not publicly documented | Confirm local withdrawal or transfer-out cost for contractor |

| Unknowns to confirm | Ask for exact route pricing, not generic pricing-page claims | For Mexico, Colombia, and Argentina, confirm whether conversion happens at send, receipt, or withdrawal | Confirm settlement timing and whether local banking steps change the fee path | Confirm who pays if details are wrong or transfer is rejected | Confirm how quickly funds are usable and whether contractor-side conversion changes final amount |

The comparison pattern matters more than the brand names. Bank transfer, SWIFT, PayPal, and Payoneer can all work, but if the full price path is unclear, you are estimating instead of budgeting. The source material is clearer on Wise than on the other options here, but the fee is still route-dependent and can change.

2. The same invoice can land very differently by method#

Keep the same invoice amount constant across rails, then compare what actually arrives. A bank transfer or SWIFT payout can look simple on your side, but the received amount can still vary when conversion details or contractor access steps are unclear.

Wise provides the clearest pre-send checkpoint in the material for this guide. It says you see fee and exchange-rate details before confirmation, and it says it uses the mid-market rate. That does not prove it is always the lowest-cost option in every corridor. It does mean you can price the payout more transparently before release.

Volume can change outcomes too. The same source says discounts apply after 25,000 USD sent in a month, and the threshold resets on the first. If your volume sits near that line, payout timing around month-end can change effective cost.

Contractor access costs matter as well. The provider notes ATM-side conversion can apply an unfavorable rate. If an ATM offers to convert, declining that conversion is usually the safer choice.

3. Approve the next batch only after a four-way match#

Approve the next batch only after one completed payout reconciles from start to finish:

- Match the invoice amount to the payment instruction you intended to send.

- Match the quote or pre-send screen to provider confirmation, including fee and FX details shown at approval time.

- Match provider confirmation to the contractor's actual received amount.

- Record any gap between expected and received funds, including conversion, transfer charges, or contractor-side access costs.

This keeps small pricing changes from compounding. Wise explicitly says some fees change and points users to its fee calculator for current route costs, so old screenshots are not a safe approval basis.

For Mexico, Colombia, and Argentina, keep unknowns explicit until verified: settlement timing, conversion point, and usable received funds. If any of those remain unclear, pause the next batch until the first payout has a clean received-amount record.

We covered this in detail in The Best Way to Pay an Offshore Development Team in Ukraine.

Best payment methods for LATAM contractor teams#

Use two defaults, not one: keep a bank rail for formal invoice payouts, and keep a digital option for contractors who prefer a different receive path. Do not scale any method until one real payout fully reconciles: invoice, approval view, provider confirmation, and usable received amount.

| Method group | Use in article | Checks or caveats |

|---|---|---|

| Bank transfer and SWIFT | Use when the priority is formal payout records tied to invoices, statement-level evidence, and consistent payment references | Capture beneficiary details, invoice number, and your internal payout ID on every instruction; if the contractor receives through Wise, it lists a fixed 6.11 USD fee for receiving USD wire and Swift payments |

| Wise and PayPal | Wise provides a pre-send pricing view; PayPal can still be usable | Wise says it uses the mid-market rate, shows fees upfront before confirmation, starts from 0.57%, and states there are no subscriptions or plans; PayPal approvals should use the fee view from your own account because the referenced fee page is for U.S. resident accounts and shows Last Updated: February 19, 2026 |

| Deel and RemoFirst | Treat vendor claims as unverified until they work in your own process | Pricing, compliance features, and country handling are not verified in the source material; confirm you can retrieve the records needed for payout operations and later audits |

| Abillio Pro with Airtm or card rails | Evaluate only when your current route repeatedly fails your payout or withdrawal process | Not verified here: coverage or capabilities for Mexico, Colombia, or Argentina; confirm send and receive currency, beneficiary type, withdrawal path, and exception-handling evidence before rollout |

| USDC on Solana where supported | Use only when the contractor explicitly wants it and both sides can document acceptance | Not supported here: claims that it is cheaper, faster, or easier to run compliantly than other rails; record invoice linkage, wallet address, network, transaction hash, and contractor confirmation that funds are usable |

Bank transfer and SWIFT#

Use bank transfer or SWIFT when your priority is formal payout records tied to invoices. This can be a cleaner option for teams that need statement-level evidence and consistent payment references.

A practical risk here is reconciliation, not just fees. Capture beneficiary details, invoice number, and your internal payout ID on every instruction, then verify what was actually received before you release a batch. If the contractor receives through Wise, it lists a fixed 6.11 USD fee for receiving USD wire and Swift payments. That gives you a practical landed-cost checkpoint.

Wise and PayPal#

In the material for this guide, Wise provides a pre-send pricing view. It says it uses the mid-market rate, shows fees upfront before confirmation, and lists send pricing from 0.57% on a route-dependent basis. It also states there are no subscriptions or plans.

Do not rely on old pricing assumptions. The same provider says some currencies and payment methods can see fee increases after reviews, so recheck live pricing before approvals. It also says discounts start after 25,000 USD sent in a month, or the equivalent, which can affect effective cost at higher volumes.

PayPal can still be usable, but scope your checks correctly. The referenced PayPal fee page is for U.S. resident accounts, and PayPal defines an international transaction as sender and receiver in different markets. The page shows Last Updated: February 19, 2026. For approvals, use the fee view from your own account and transaction type.

If a contractor uses a Wise card, note the allowance: 2 free withdrawals or up to 200 EUR per month before extra ATM charges. They can use View ATM fees to check allowance and reset timing, and the provider recommends declining ATM-offered conversion rates.

Deel and RemoFirst#

Pricing, compliance features, and country handling for these vendors are not verified here.

Treat vendor claims as unverified until they work in your own process. Before you commit, confirm that you can retrieve the records you need for payout operations and later audits.

Abillio Pro with Airtm or card rails#

Use alternate rails only when your current route repeatedly fails your payout or withdrawal process. That can justify evaluation, but only with corridor-specific validation.

Coverage or capabilities for Abillio Pro, Airtm, or specific card routes in Mexico, Colombia, or Argentina are not verified here. Confirm send and receive currency, beneficiary type, withdrawal path, and exception-handling evidence before rollout.

USDC on Solana where supported#

Use this only when the contractor explicitly wants it and both sides can document acceptance. Claims that USDC on Solana is cheaper, faster, or easier to run compliantly than other rails are not supported here.

If you allow it, tighten controls: record invoice linkage, wallet address, network, transaction hash, and contractor confirmation that funds are usable on their side. Validate with a small pilot before full-amount payouts.

If you want a step-by-step walkthrough, see this guide: How to Use Deel to Pay a Global Team of Contractors for a US-Based Agency.

Country checkpoints before your first payout#

Run Mexico, Colombia, and Argentina as separate launch checks, not under one LATAM policy. If you cannot clearly map the documentation path, receive path, and fallback path for a country, pause that country's first batch.

| Country | First focus | What to confirm before rollout |

|---|---|---|

| Mexico | Confirm the contractor's documentation path before optimizing for speed or fees | Ask in writing which invoicing and payment-documentation requirements apply; also confirm receive currency, beneficiary setup, and whether your rail matches what the contractor can actually use |

| Colombia | Treat delay handling as a first-launch requirement | Ask how incoming international funds are usually handled and what the provider may request if a transfer is held or delayed; prepare a resend-ready evidence pack tied to your payout ID |

| Argentina | Confirm the usable receive and conversion path before the first live amount is sent | Check what currency the contractor can receive, where conversion would happen if needed, and whether that fits your available rail; if the preferred route does not match your workable payout rail, switch methods before rollout |

Before country-specific checks, do two things every time: confirm contractor identity and restricted-party screening, and keep a backup payout rail for edge cases.

Mexico#

Start by confirming the contractor's documentation path before you optimize for speed or fees. Ask in writing which invoicing and payment-documentation requirements apply to their setup.

Do not assume one answer fits every contractor. Also confirm how currency handling works on the payout path: receive currency, beneficiary setup, and whether your rail matches what the contractor can actually use.

Colombia#

Treat delay handling as a first-launch requirement, not a later fix. Ask the contractor how incoming international funds are usually handled, and what their provider may request if a transfer is held or delayed.

Prepare a resend-ready evidence pack tied to your payout ID, for example the invoice and transfer reference plus any details your provider requests. This can cut rework if clearance issues appear.

Argentina#

Confirm the usable receive and conversion path before the first live amount is sent. Check what currency the contractor can receive, where conversion would happen if needed, and whether that fits your available rail.

If their preferred route does not match your workable payout rail, switch methods before rollout. A backup rail matters here so a "successful send" does not turn into an unusable payout.

The pause rule#

If country documentation requirements are unclear, stop that country's first batch and resolve them before scaling. A low apparent transfer cost is not enough on its own, because FX spreads, intermediary deductions, and failed-payment rework can be the bigger risk.

Use public country explainers as prompts, not final approval, especially when publication dates are older. Keep a per-contractor country note with documentation items, receive rail, fallback rail, and delay-handling notes.

This pairs well with our guide on The Best Way for a German Agency to Pay a US-Based Freelancer.

Contract and classification controls that prevent expensive mistakes#

A major risk is classification and contract design, not just the transfer itself. If your agreement says "independent contractor" but the working model looks like employment, legal and financial risk rises.

1. Write the classification test before payment terms#

Set your independent-contractor criteria in writing before you finalize payout terms. In Mexico, contractor status is tied to autonomy: the person is self-employed and not under your direct control or supervision.

Keep a short classification note with the contract so your team can explain how the role works in practice. If your company is U.S.-based, the IRS 20-Factor Test can be a secondary check.

2. Match payment language to a contractor relationship#

Your payment clause should read like a commercial services arrangement, not payroll language. Define invoice timing, accepted payout methods, and required payment documentation. Also set tax-form checkpoints before first payment where applicable, including forms such as W-8BEN or W-8BEN-E.

3. Localize contracts instead of forcing one LATAM template#

Do not rely on one template for every country. Contracts should be localized to each country's legal and language requirements and aligned to local invoicing, tax, and payment rules. For Mexico, frame the relationship as a commercial contract basis under civil or commercial rules, not as labor-law employment terms.

4. Add an escalation path for misclassification drift#

Risk does not end at signature. Include an internal escalation path for cross-border engagements so teams know who reviews classification concerns and which documents must be gathered during review.

If the facts stop matching contractor status, escalate immediately instead of trying to solve the issue through invoice or payout fixes later. For a practical response path, link your contract owner to What to Do If You've Been Misclassified as an Independent Contractor.

Payment terms that protect cashflow before work starts#

Clear payment terms before kickoff can reduce avoidable payment delays and compliance friction. Define when invoices are submitted, what must be on them, and what evidence releases payment before work begins.

1. Billing cadence and overdue rules#

Set one billing cadence and document the operating details in the contract: invoice submission date, due date, any late-fee policy, and what happens operationally if payment is overdue. Keep this practical. Name who reviews disputes, how quickly questions are raised, and when new work pauses pending resolution.

Treat "work pauses if overdue" as a contract and process signal, not something automatically enforceable across all Latin American jurisdictions. The goal is to remove ambiguity before a late invoice turns into a larger delivery and cashflow problem.

2. Invoice data standards and transfer references#

Use a written invoice data standard from day one. As an internal baseline, require legal name, country, payment rail, payout currency, and the reference details needed to execute and trace a bank transfer or wire transfer. If you also require internal IDs such as PO or project codes, document that up front.

For Mexico, add a stricter pre-work check: contractor invoices typically require electronic facturas, usually in Spanish, and must comply with CFDI 4.0. Available guidance also lists SAT registration and RFC as prerequisites. Confirm this before kickoff so payment does not stall at invoicing.

3. Milestone release and change approval#

Milestone terms should define release conditions, not just percentages. Specify what counts as completion, who approves it, what deliverables are required, and when acceptance or rejection must happen.

Then add a written change-approval rule: scope changes need approval before extra work starts, with any budget or timeline impact documented. This keeps invoice approval tied to clear records and helps limit confusion later.

Need the full breakdown? Read The Best Way for an Australian Agency to Pay a US-Based Contractor.

Monthly execution checklist from invoice to confirmed receipt#

If you want fewer payout misses, run one fixed monthly sequence and keep status in one tracker, not scattered across inboxes and screenshots. The control point is traceability from invoice to confirmed receipt.

- Collect and validate before you batch

Collect invoices first, then validate them against your agreed terms and required payout details. At minimum, confirm beneficiary name, amount, account details, and payment method before anything enters the batch. If a required field is missing or inconsistent, hold it out of the batch until corrected.

- Approve in batches, not one by one

After validation, group payments and run a batch approval check for errors or duplicates before release. Batching cuts handling load and lowers error exposure compared with processing each payment separately. In a one-by-one flow, even a normal cycle can become 15 separate transactions, each with its own processing time and chance for error. If your provider says batched payments are usually processed within one business day, treat that as planning guidance, not a promise.

- Build a proof pack for every payout

For each contractor, keep one proof pack with the invoice, transfer reference, payout status, and a short reconciliation note. Add provider confirmation artifacts such as receipts, timestamps, and downloadable reports. If an invoice includes supporting documentation, store it in the same record so payout evidence stays complete and easy to audit.

- Run exceptions daily and keep one status record

During payout week, review exceptions daily: duplicate-attempt checks, typos in beneficiary details, and missed invoices. Track each payout in one shared status flow: invoice received, validated, approved, sent, provider confirmed, exception open. If an issue appears, log the original instruction, issue type, corrected details, and retry approval so the same issue does not repeat next cycle.

Before your next payout batch, use this payment fee comparison tool during approval prep.

What breaks most often and how to recover fast#

When a cross-border payout fails, a safe response is to pause retries and investigate one case from start to finish before sending again. Before any retry, keep one evidence checkpoint: the original instruction, the provider's stated failure reason, and updated beneficiary data if anything changed. Failure modes are not ranked and resolution SLAs are not provided here, so treat this as a control process, not a timing promise.

Use this triage sequence:

- Transfer-path check (transfer risk)

Confirm what happened to the first instruction and capture core references: transfer ID, amount, currency, send date, and an internal tracking ID. In FDIC Section 11.1 terms, treat this as transfer risk in international activity.

- Beneficiary-data check

Verify beneficiary details against the latest contractor-confirmed bank record, then update your internal record before retrying.

- FX check (foreign exchange risk)

Reconfirm invoice currency, approved send amount, provider conversion details, and expected received amount. If conversion assumptions changed, reapprove on current terms before release.

- Identifier continuity check

Carry one consistent payout identifier across internal records and provider notes so support and the contractor can reconcile the payment quickly.

If escalation is needed, define an internal handoff and retry-control process. At a policy level, FDIC Section 11.1 frames this as risk mitigation, including exit strategies, rather than a payout-specific ladder.

For repeat exceptions, keep a simple corridor log modeled on the Country Risk Exposure Report idea from FDIC Section 11.1 so recurring route-level risk is visible early.

When to use card or stablecoin rails instead of bank rails#

Use a non-bank rail only when you can document the full path: how funds move, how failure is detected, and how recovery works. If your team cannot document that, do not make that rail your default for LATAM contractor payouts.

- Use card payouts for speed-sensitive access

Use card payouts when faster access is the main need and coverage is confirmed on the exact route. Treat speed comparisons as corridor-specific, not universal: traditional bank rails are described in the 2-5 or 3-5 business day range, and faster-payment guidance frames rail choice as finding the most viable option. Before going live, confirm card eligibility and a fallback bank path.

- Use stablecoin rails only with a complete evidence trail

Use stablecoin rails only when policy allows, contractor acceptance is explicit, and compliance checks are recorded from start to finish. The speed case is directional: blockchain payments are described as settling in under 3 minutes, and one LATAM case study describes a USD-funded flow where workers receive funds in a wallet, then use a virtual card or withdraw to a local bank. Document wallet details, approvals, and the off-ramp path before making it routine.

- Keep bank transfer as default when your process favors familiar banking records

If your payout operations are built around bank-based records and reconciliation, bank transfer can remain the default. Keep the tradeoff explicit: sources describe cross-border bank costs around 2-7%, and one case study cites 3-10% losses when FX spreads and wiring fees stack up. Use that tradeoff to decide where faster alternatives are worth the extra controls.

- Make recovery readiness the deciding test

Default to the rail your team can recover on cleanly. For card or stablecoin rails, define who confirms receipt, which reference ID is stored, what proof is acceptable, and which fallback rail is used if a payment fails, stalls, or is reversed. If that recovery process is missing, keep bank transfer as the default and use alternate rails by exception.

How to vet payment vendors without getting trapped by marketing#

Use proof-based checks, not demos, before you move contractor payments at scale. If Deel, RemoFirst, Airwallex, Payoneer, or Abillio Pro cannot answer the same operating questions with evidence, keep volume limited until they can.

- Use one checklist for every vendor

Review each vendor against the same three areas: pricing transparency, payout status depth, and dispute handling. This keeps the comparison fair because payment options can carry different cost and risk tradeoffs. Ask each vendor to show a real payout timeline, the statuses visible after initiation, and what proof you receive if a transfer is returned, reversed, or disputed.

- Demand corridor-specific proof

Treat corridor evidence as required, not optional. Payment preferences differ by market, so ask for proof for each target country separately: supported routes, expected receipt windows, common failure points, and fallback steps when the first attempt fails. If the evidence is only global claims or examples from another market, treat the review as incomplete.

- Separate included features from add-on costs

Get written scope before signing. Confirm what is included versus extra cost for support levels, FX handling, reversals, and compliance documentation, since local options can add both complexity and cost. Also ask what payout records and transaction evidence you receive by default versus as a paid add-on.

- Run a pilot with pass-fail metrics

Require a pilot with measurable success criteria before full rollout. Use simple pass-fail metrics: first-pass success rate, median time to confirmed receipt, support response time, payout-record completeness, and time to resolve a forced exception. If a vendor markets "human support in less than 2.5 minutes" or "integration with less than 10 lines of code," treat those as pilot checks to verify, not assumptions.

You might also find this useful: How to Pay US-Based Contractors from Australia.

Conclusion#

The best way to handle contractor payouts in Latin America is the method your team can run consistently every month, with clear terms, visible status, and clean records. If you cannot explain payment terms, total landed cost, payout status, and retry handling in one place, do not scale yet.

- Choose operability over demo optics.

A common rail like a SWIFT bank transfer can feel safer because it is familiar, but familiar does not mean low-friction. SWIFT fees can run more than $40 per transaction in some cases, and low transparency can make missed or postponed payments harder to trace.

- Prove one corridor with one monthly checklist before expanding.

Keep the evidence pack simple and repeatable: invoice, approved amount, transfer reference, provider confirmation, and receipt confirmation. The core control is reconciliation: quoted amount, invoice amount, provider confirmation, and final received amount should match before you add volume.

- Treat exceptions as part of the method, not an edge case.

Cross-border payouts can include deductions or delays, and those issues affect trust and compliance handling. Before any retry, confirm the original instruction, the stated failure reason, and the updated payment details so reconciliation stays clean.

- Use stricter tooling when control needs justify the tradeoff.

Worldwide employment systems can combine contracts, payments, local tax compliance, and onboarding, which can improve legal and admin coverage. The tradeoff is cost and flexibility: quoted pricing can be $300 to $700 per month per worker, and many tools still depend on conventional bank rails.

- Decide from operating evidence, not marketing claims.

The right choice is the one that gives your team clear documentation, status visibility, and predictable handling when payouts fail. Reliability is whether you can close each month with payouts matched, explained, and audit-ready.

Related reading: The Best Way to Pay an Indian Development Agency from the US.

If you want a payout setup with policy gates, status tracking, and reconciliation-ready records where supported, review Gruv Payouts.

Frequently Asked Questions

What is the best way to pay contractors in Latin America if I care most about reliability?

There is no single best rail across LATAM, because the right method depends on the contractor’s country, banking setup, and your company setup. Reliability usually comes from validating each country’s payment-method fit before scaling. Where available, local rails can reduce the delay and cost patterns common with international wires.

Which payment methods are most common across LATAM and how do I choose between them?

Bank transfers, digital wallets, and digital payment platforms are all common, but preferences vary across LATAM’s 33 countries. Choose based on corridor fit and fee transparency, then compare total landed cost before scaling. For example, PayPal cross-border costs can approach nearly 9% in some cases. Wise is described as using the mid-market rate with a clear fee often under 1%, and local systems like SPEI show why local infrastructure matters.

How can I reduce payout delays and unexpected cross-border fees?

Use a repeatable pre-send check: quoted amount, invoice amount, provider confirmation, and final received amount should all reconcile. Confirm whether FX uses the mid-market rate or includes markup, and get return and reversal handling in writing before volume increases. This makes fee risk visible before it becomes a margin problem.

What are the biggest compliance risks when paying independent contractors?

The main risk is treating payment as only a transfer process instead of a contract-and-local-law process. Proper contracts and local compliance reduce misclassification risk, so fix weak classification or vague scopes before scaling. If needed, review What to Do If You've Been Misclassified as an Independent Contractor. In Mexico, confirm the contractor can issue electronic facturas compliant with CFDI 4.0 and has an RFC from SAT, and remember withholding treatment varies by classification and residency.

How should I compare Deel, RemoFirst, Payoneer, Airwallex, and other vendors fairly?

Use one evidence standard for every vendor: pricing transparency, payout status visibility, dispute handling, and country-level operability for your actual corridors. Separate included features from add-on costs, especially around FX handling, reversals, support, and compliance documentation. Then run a pilot with pass or fail metrics before full rollout.

What country-specific details should I confirm first in Mexico, Colombia, and Argentina?

Start with the country where requirements are most explicit in your workflow evidence. For Mexico, verify SAT registration, RFC, and electronic facturas that meet CFDI 4.0. For Colombia and Argentina, validate method fit and local compliance requirements before first live payouts, and in Argentina review contractor terms against the LCT context.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- doit.maryland.gov/contracts/DoIT-Contracts/Documents/Statewide...trusted

- ecfr.gov/current/title-19/chapter-I/part-24trusted

- elibrary.imf.org/display/book/9781597822268/ch08.xmltrusted

- fdic.gov/risk-management-manual-examination-policies/...trusted

- federalreserve.gov/publications/files/cbem-7000-202602.pdftrusted

- gsa.gov/buy-through-us/purchasing-programs/multiple-...trusted

- niehs.nih.gov/health/topics/agents/air-pollutiontrusted

- oecd.org/content/dam/oecd/en/publications/reports/201...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

How LLC Owners Separate Business and Personal Finances

For an LLC, separating business and personal money is best treated as a weekly habit, not a one-time bank setup. It keeps records cleaner, cuts month-end cleanup, and creates clearer boundaries as the company grows.

What to Do If You've Been Misclassified as an Independent Contractor

Treat this as a protection problem first, not a label debate. If your work was treated as an independent contractor arrangement even though the relationship functioned differently, your first goal is to protect pay, rights, and records while you choose the least risky escalation path. You can do that without making accusations on day one, which often keeps communication open while you document what happened.

How to Pay International Contractors With Fewer Delays and Disputes

Paying international contractors reliably starts with compliance setup before the first invoice. Missed registration or filing steps turn routine payouts into delays and penalties.