Quick Answer

Require destination-specific bank fields before money moves: IBAN identifies the beneficiary account, while SWIFT/BIC identifies the receiving bank, and many routes need both. For international contractor payouts, collect destination country first, validate required identifiers before a payout batch is eligible, and hold items with missing or malformed data. Keep request logs, provider responses, and payment references so rejected, returned, and retried payouts can be reconciled without guesswork.

International contractor payouts fail on details, not intent#

If you are scaling international contractor payouts, treat code choice as a release control, not a glossary question. The practical rule is simple: collect the right bank identifiers up front, validate them before approval, and keep enough evidence to explain every submitted, rejected, returned, or retried payout later.

The distinction matters because it drives routing and validation. An International Bank Account Number, or IBAN, is the standardized identifier for the beneficiary account. A SWIFT code, also called a BIC code, identifies the receiving bank for an international transfer.

In operations, teams get into trouble when a contractor record is missing a required field, when a digit is mistyped, or when ops releases a batch before data and compliance checks are complete.

That pattern is common: incorrect beneficiary details can send a payment into limbo, and delays can come from compliance holds, sanctions screening, currency restrictions, or issues at correspondent banks, not just technical outages. For a platform, that means payout design has to cover more than speed. Your intake model, approval states, audit trail, and exception path matter as much as the transfer rail itself.

Two checkpoints usually pay for themselves quickly. First, validate the beneficiary payload before a payout is eligible for release: destination country, account identifier such as IBAN where applicable, and SWIFT code or other bank-routing detail where required. Second, preserve request-level and provider-level evidence after submission. Request logs for successful and failed API calls help engineering trace integration problems, while provider responses and payment references help finance reconcile outcomes and explain retries.

At scale, the friction is not one payment. It is batch behavior. One bad record can create queue holds, manual review work, or finance exceptions when a contractor was marked paid internally but rejected externally. If you operate in European corridors, standardized exception labels such as SEPA reason codes can also improve triage because they distinguish rejected, returned, and stopped payments instead of leaving ops with a generic failure bucket.

So the useful comparison is not just IBAN versus SWIFT, but definitions versus controls. The better operating choice is to build documented checks that tie contractor records, invoices, and payout execution together, then make release conditional on passing those checks. The rest of this guide turns that into concrete decision rules: when to require IBAN, when SWIFT is enough, when you need both, and what finance, ops, and engineering should verify before money moves. Related: Xero + Global Payouts: How to Sync International Contractor Payments into Your Accounting System.

IBAN vs SWIFT at a glance for platform payout decisions#

For payout decisions, treat IBAN and SWIFT/BIC as complementary controls, not interchangeable fields: IBAN identifies the beneficiary account, and SWIFT/BIC identifies the beneficiary bank or branch.

| Decision point | IBAN | SWIFT / BIC | What your product should do |

|---|---|---|---|

| Purpose | Identifies the beneficiary account | Identifies the receiving bank or bank branch | Keep separate fields and separate validation rules |

| Scope | Account-level identifier | Bank-level or branch-level identifier | Do not let one substitute for the other |

| Required fields | IBAN, plus beneficiary legal name and destination-country context | SWIFT/BIC, plus beneficiary legal name and destination-country context | Collect both when the destination route or provider requires both |

| Commonly used | Common in IBAN-based markets, including many European flows | Common in cross-border bank routing globally | Make field requirements conditional by destination and provider |

| Typical failure mode | Invalid format/control digits, or missing IBAN where required | Wrong or missing bank/branch identifier where required | Block before release instead of discovering errors after submission |

| Who owns validation in-product | Product defines required-field logic; engineering enforces checks; ops/finance handle exceptions | Product defines required-field logic; engineering enforces checks; ops/finance handle exceptions | Keep ownership explicit, not hidden in manual review |

| Can this be optional | Sometimes, where destination rails and provider do not require it | Sometimes, where destination rails and provider do not require it | If the destination rail requires IBAN and you only collected SWIFT, hold payout before submission |

| Evidence to store | Beneficiary account details, destination-country context, validation result | Provider response, submitted bank identifier, payment reference and other audit-ready reconciliation references | Preserve evidence for submitted, rejected, returned, and retried payouts |

The rule is straightforward: required fields should be driven by destination and provider requirements, then enforced before release. A single "bank details" field is not enough for cross-border contractor payouts.

In European corridors, apply tighter checks. In the SEPA context, Regulation (EU) No 260/2012 references mandatory IBAN/BIC use where necessary, and the SEPA region covers 41 countries. This section is not a country-by-country legal matrix, so implement route-specific rules for the destinations you actually support.

Verification should happen pre-send, not after a failure: validate IBAN format and control digits, and where both fields are required, verify BIC together with IBAN as part of one release gate.

What each code actually controls in routing#

IBAN and SWIFT/BIC control different routing layers, so they are not substitutes. IBAN identifies the beneficiary account, while SWIFT is a secure financial messaging network and BIC is the institution identifier used in that messaging context.

| Routing job | IBAN | SWIFT / BIC |

|---|---|---|

| What it identifies | The customer account at a financial institution | The beneficiary institution (and, in some flows, other institutions in the route) |

| Where it matters | Account-level destination accuracy | Institution-level message delivery and routing |

| What to verify before release | Format and control digits | Presence and structure of the BIC (8 or 11 characters) |

This distinction matters because cross-border wire instructions can include routing details for an intermediary institution, a beneficiary institution, and the beneficiary. A valid IBAN alone does not identify the institution route, and a valid BIC alone does not identify the beneficiary account to credit.

In practice, "IBAN vs SWIFT" is often the wrong framing. Some payment instructions include both IBAN and BIC fields, and EU policy text promotes standardization around both identifiers. If your provider or destination route requires both, validate both and hold release when either is missing.

One limit to keep in mind: the available evidence here does not establish corridor-level differences in settlement speed, fee impact, or country-specific exceptions. Use destination and provider requirements as your release gate, not assumptions about timing or cost.

When to use IBAN, SWIFT, or both in real payout scenarios#

Use a destination-led rule: collect the banking fields required for that country, and do not release a payout when that set is incomplete.

| Payout scenario | Collect before payout approval | Why this is the right minimum | Operator checkpoint and likely failure |

|---|---|---|---|

| Europe-focused contractor payout | International Bank Account Number (IBAN) and SWIFT code or BIC code | IBAN identifies the beneficiary account, and cross-border instructions often still include a bank identifier | Validate IBAN format/control digits and confirm BIC is 8 or 11 characters. Exception: some SEPA payments explicitly state BIC is not required, so avoid a universal BIC rule for every SEPA route. |

| Non-IBAN destination | SWIFT code plus local bank details required by that market | Some countries use SWIFT for international transfers instead of IBAN | Run pre-send checks against market-specific fields. Common misses include local routing identifiers (for example, FEDWIRE for US payments or NCC in some destinations). |

| Mixed global contractor base | Country-aware intake that switches required fields by destination | One static bank form creates avoidable failures across IBAN and non-IBAN markets | Require destination country before bank-field capture. Common failure: collecting an IBAN-style field for a non-IBAN destination and finding the mismatch at payout time. |

| Marketplace with frequent new payees | Destination-specific required set plus pre-send validation before payout eligibility | New payees usually create the most data-entry mistakes | Do not treat "bank details saved" as "ready to pay." Hold first payout until account identifier, bank identifier/details, and country-specific routing fields pass validation. |

Decision rules that hold up in production#

If the destination uses an IBAN-based format, require IBAN first and usually collect SWIFT/BIC before payout approval. Relax that only when the provider or route explicitly marks BIC as not required, as documented for some SEPA payments.

| Destination case | Minimum fields | Release rule |

|---|---|---|

| IBAN-based destination | Require IBAN first and usually collect SWIFT/BIC before payout approval | Relax only when the provider or route explicitly marks BIC as not required, as documented for some SEPA payments |

| Non-IBAN but globally connected destination | Collect SWIFT and the local routing details that market requires | Validate before batching |

| Mexican peso payments | You may need the beneficiary's 18 digit CLABE | SWIFT plus free-text account details alone may still be incomplete |

If the destination is non-IBAN but globally connected, collect SWIFT and the local routing details that market requires, then validate before batching. In practice, international instructions may require the beneficiary name, account number or IBAN, the bank's BIC, and any destination-country routing code.

Match the field set to the destination before money moves. For Mexican peso payments, for example, you may need the beneficiary's 18 digit CLABE; SWIFT plus free-text account details alone may still be incomplete.

The tradeoff is worth being explicit about#

Stricter upfront capture adds onboarding friction, but missing or incorrect beneficiary or bank data can delay international wires. For operators, that usually means exception handling and manual follow-up after payout initiation.

A practical rule is: collect destination country first, render only required banking fields for that destination, and mark payees payout-ready only after validation passes. This keeps the decision framework accurate: not "IBAN or SWIFT," but destination-led collection, with both used together when the route requires both, plus local routing data where needed.

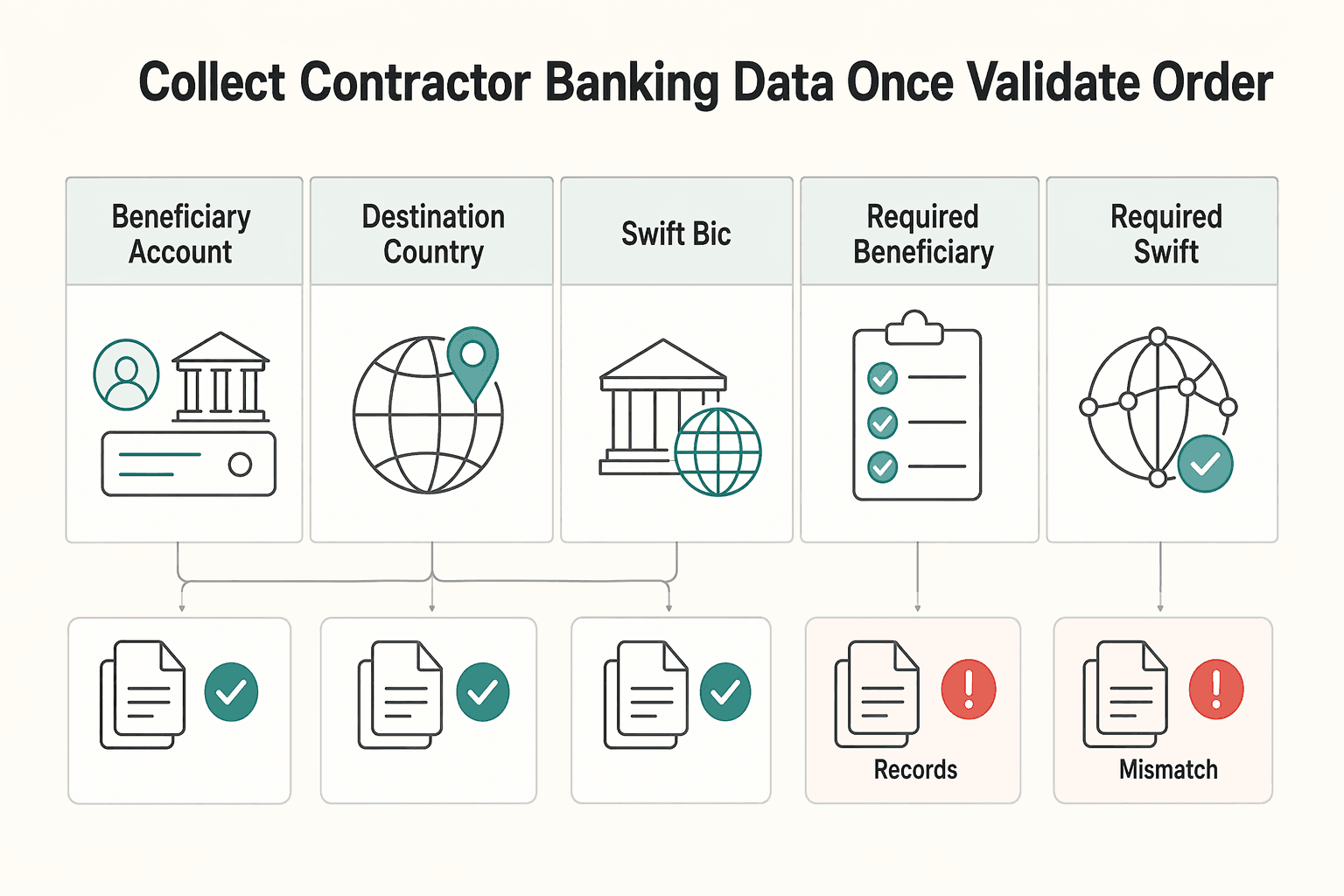

Collect contractor banking data once and validate it in order#

Use a destination-first intake flow, then gate payout eligibility on validation evidence. Capture a baseline payload for each payee: beneficiary account name, beneficiary account identifier, destination country or region, and SWIFT/BIC when that route requires it.

| Field | When it belongs in the baseline | Route note |

|---|---|---|

| Beneficiary account name | Baseline payload | Pre-send checks commonly cover recipient name |

| Beneficiary account identifier | Baseline payload | Show IBAN where used, or local account details where IBAN is not used |

| Destination country or region | Baseline payload | Collect destination first because required payout fields vary by recipient bank country or region |

| SWIFT/BIC | When that route requires it | Pre-send checks commonly cover SWIFT/BIC |

That baseline is a starting point, not a universal field set for every corridor. Required payout fields vary by recipient bank country or region, so collect destination first, then show the right account identifier for that market: IBAN where used, or local account details where IBAN is not used.

Keep the validation sequence strict:

- Collect required fields.

- Validate format and country fit.

- Run beneficiary checks before marking a payee as payout-eligible.

Pre-send checks commonly cover recipient name, address, account number, and SWIFT/BIC. For some IBAN payments, name-check controls compare the recipient name with account-holder details. In product terms, "bank details saved" should never equal "ready to pay."

Handle data with the same discipline. Show masked values in UI, make stored account data unreadable at rest (for example with encryption, truncation, or tokenization), and retain reconciliation evidence such as validation outcomes, timestamps, override actions, and available itemized payout receipts.

| Condition | Default action | Why |

|---|---|---|

| Destination country or region missing | Block payout creation | You cannot determine required fields without corridor context. |

| Required beneficiary account identifier missing or invalid for that destination | Block payout creation | This is a core routing field, whether IBAN or local account number. |

| Required SWIFT/BIC missing for the selected route | Block payout creation | The beneficiary bank cannot be identified correctly for routes that require it. |

| Name-check or beneficiary check returns a mismatch | Warn and route to manual review | Strong error/fraud signal, but not universal across all routes and can produce mismatches. |

| Non-critical field discrepancy that the route does not require | Warn | Escalate only if your provider later flags it as required. |

The rule is simple: block on missing routing essentials, warn on reviewable mismatches, and do not unlock payout eligibility until validation evidence exists. For a step-by-step walkthrough, see How to Handle Termination of an International Contractor.

Put compliance and release gates before payout batches#

Validated bank details are necessary, but they are not enough to release a payout batch. Before submission, check each payee's live verification and risk state and decide item by item whether funds can move.

Use three gate buckets: Know Your Customer (KYC), Know Your Business (KYB) when the payee is a business, and AML controls that include sanctions screening. Providers can restrict flow of funds based on verification status, and accounts can move into restricted states when onboarding, risk, or verification requirements are still open. Treat release gating as a pre-submit control, not a one-time onboarding check.

| Gate | Status | Batch action | What ops should see |

|---|---|---|---|

| KYC or KYB | Complete | Eligible to submit | No action needed |

| KYC or KYB | Pending | Hold item from batch | Exact missing information or verification step still due |

| KYC or KYB | Failed or restricted | Block item | Reason code, affected capability, owner, and next remediation step |

| AML or sanctions screening | Clear | Eligible to submit | Screening timestamp or clear status |

| AML or sanctions screening | Pending review | Hold item from batch | Case status and who must review |

| AML or sanctions screening | Match, failed, or restricted | Block item | Escalation path and compliance contact |

Make the if-then logic explicit in both product and batch jobs. If KYC, KYB, or AML is pending, hold the item and surface the exact remediation task to ops or the payee. If status is failed or restricted, block release until it is resolved. If your provider exposes practical requirement details, show those instead of a generic "compliance issue."

Apply the same discipline to retries. When creating or submitting payout-side API objects, use an idempotency key so timeouts or dropped responses can be retried without performing the same operation twice. Also persist the key per payout item or batch attempt, keep the provider response, and prevent accidental fresh-key retries for the same logical payout.

Reduce payout failures with a clear exception path#

The fastest way to reduce payout failures is to triage exceptions in order: keep the raw provider signal, classify it as invalid data or delay/transient, then route it to the right owner.

Common failure modes should stay visible as codes, not flattened into a generic "failed" label. Hard data errors include invalid IBAN format, invalid or incorrect account identifiers, and incorrect bank identifier/BIC format. You may also see beneficiary-bank rejections, which require code-level review before choosing the next step. Separate those from non-final delay signals like pending credit, where processing continues but credit may not happen the same day.

Triage in order#

| Step | What to capture or classify | Operational result |

|---|---|---|

| Capture the raw signal first | Provider status, reason code, timestamp, payout reference, and any return code shown in the reference field; for SCT Inst failures, the specific R-transaction reason code | Keep the provider-native signal intact |

| Classify into an action bucket | Invalid data such as invalid IBAN or malformed BIC; warning or delay statuses such as WARN or G002 ACSP | Route invalid data to contractor detail correction and hold release; route warnings or delays to controlled retry or timed review |

| Route by owner | Finance, engineering, or compliance | Finance handles rejected vs returned outcomes and reconciliation; engineering handles validation defects, retry logic, and provider/transient issues; compliance handles KYC, KYB, AML, or sanctions blocks |

- Capture the raw signal first. Store provider status, reason code, timestamp, payout reference, and any return code shown in the reference field. For SCT Inst failures, keep the specific R-transaction reason code.

- Classify into an action bucket. If the code indicates invalid data, for example invalid IBAN or malformed BIC, route to contractor detail correction and hold release. If the status indicates warning or delay, for example

WARNorG002 ACSP, route to controlled retry or timed review. - Route by owner. Finance handles rejected vs returned outcomes and reconciliation. Engineering handles validation defects, retry logic, and provider or transient issues. Compliance enters when KYC, KYB, AML, or sanctions status blocks movement.

For each exception, retain the masked beneficiary details, submitted SWIFT/BIC values, exact provider response, and internal decision. This prevents guesswork later when "rejected" and "returned" require different reconciliation actions.

Statuses that survive handoffs#

| Internal status | What it means | Typical next action |

|---|---|---|

| Pending review | Non-final warning, delay, or unclear provider response | Wait for propagation or review with provider trace |

| Blocked by compliance | KYC, KYB, AML, or sanctions state prevents movement | Resolve compliance requirement before resubmission |

| Submitted | Accepted by provider and in process | Monitor for completion, rejection, or return |

| Rejected | Payment was not accepted or was rejected before completion | Inspect code, fix data if needed, then resubmit |

| Returned | Funds came back after submission | Reconcile return, inspect return code, recollect details if required |

| Reconciled | Ledger and payout outcome agree | Close exception with audit trail intact |

Keep two fields per payout item: the provider-native code and your normalized class. Finance gets a stable operating model, while engineering and ops keep the exact signal needed to decide whether to update data, retry, or reconcile a return.

Tie payout execution to accounting and tax records#

Use your payout ledger as the single source of truth for payout state and evidence. Finance can still reconcile in Xero where they use it, but ops and engineering need one record that survives status changes, returns, and year-end tax review.

| Payout moment | What finance should see | What evidence to keep |

|---|---|---|

| Submitted | A transaction reference ready to sync into accounting | Internal payout ID, provider reference, timestamp, masked beneficiary details |

| Completed | A settled transaction ready for bank reconciliation matching | Statement line or bank feed reference, amount, currency, completion status |

| Returned or rejected | An exception item, not an overwrite of the original payout | Provider-native reason code, return timestamp, reconciliation note |

| Year-end reporting | Tax document state linked to payee and payout history | W-8 BEN or W-9 on file, Form 1099-NEC eligibility/output where applicable |

If finance uses Xero, map syncs so each imported bank statement line matches an existing transaction in Xero. That matching step is the core reconciliation check, and reconciliation reporting is what you use to isolate balance mismatches. Avoid marking a payout as done based on provider status alone before the bank line and accounting transaction are both present.

Apply the same discipline to tax-adjacent records. Keep Form W-9 when a payee provides a correct TIN, and Form W-8 BEN when a foreign person provides it to the payer or withholding agent. Track Form 1099-NEC status separately from payout status.

If your product exposes tax support data, keep exportable history for FBAR and FEIE support without implying automatic eligibility. FBAR is a separate annual report for qualifying U.S. persons when aggregate foreign financial accounts exceed $10,000 at any time during the year, due April 15 with an automatic extension to October 15. FEIE under Form 2555 is conditional. Related reading: How to Build a SaaS Marketplace That Manages Subscriptions and Contractor Payouts.

Make the code choice a release decision, not a glossary fact#

Treat IBAN vs SWIFT as a release control: choose the identifier set by destination, then enforce it before batch submission.

Returned payouts are usually a data-quality problem, not an acronym problem. If incorrect destination details drive returns, your job is to stop bad records from becoming sent records.

| Release decision | Use when | What must be valid before release | Block condition |

|---|---|---|---|

| IBAN-led | The destination requirement says IBAN is needed | Beneficiary account captured as an IBAN, format checks passed, destination country matches the route | Required IBAN missing or invalid |

| SWIFT-led | The destination does not use IBAN but the route requires a SWIFT code | SWIFT code plus the local bank or account details required for that market, all complete and validated | SWIFT code missing, malformed, or paired with incomplete local banking details |

| IBAN + BIC/SWIFT | The destination or payment context expects both identifiers | IBAN, BIC or SWIFT code, and verification status all clear before approval | Either identifier missing, mismatched, or the payee is still pending verification |

EU cross-border payment context is a clear example where both IBAN and BIC are referenced. Rules like that belong in onboarding and release logic, not in training notes. If you support those corridors, collecting only one field is a predictable exception queue later.

Field capture alone is not enough. Apply release gates so payouts or payments stay disabled until required checks pass. Your pre-flight should confirm both: the destination has the right identifier set, and the account is still eligible for release. If verification is pending or failed, hold before submission.

Store the rule that approved release, not just raw bank fields. Keep destination country, whether release used an IBAN-led, SWIFT-led, or dual-identifier rule, and verification state at approval time. When a payout is returned, finance and engineering can investigate from evidence instead of debating whether the record looked complete.

If you are entering new corridors, build the destination rule matrix before scaling volume. Clear routing rules, strict intake validation, and release holds prevent more operational pain than another glossary walkthrough.

Frequently Asked Questions

Do I need IBAN or SWIFT for international contractor payments?

Not always the same one. IBAN identifies the beneficiary account, while a SWIFT code identifies the receiving bank, and depending on the country and bank context you may need one or both. If the destination route is IBAN-based, do not release the payout with only a SWIFT code on file.

Can a transfer be sent with a SWIFT code but no IBAN?

Sometimes yes, because some international transfers need only one of the two codes. But that is not a usable default for ops, since some routes require both and some cross-border payment contexts in Europe expect IBAN plus BIC. If your validation cannot confirm that SWIFT-only is acceptable, stop the item before batch release.

When should a platform require both IBAN and BIC code at onboarding?

Require both when your supported destination requirements say both are needed. EU cross-border payment contexts are the clearest documented example. The tradeoff is a little more onboarding friction, but it can reduce avoidable returned payouts from bad destination details.

What fields should we validate before releasing payout batches?

At minimum, validate the recipient’s bank account number or IBAN, plus the recipient’s SWIFT or BIC code where applicable. Check format, completeness, and whether the combination matches the destination you are trying to pay into. If either required field is missing, the batch item should stay blocked, not move to submitted.

What happens operationally when IBAN or SWIFT details are wrong?

Bad destination details commonly lead to returned payouts. When that happens, do not overwrite the original payout as if nothing happened; capture the provider’s return reason, move the item into an exception state, and send it through a contractor update flow or manual review. Blind retrying with the same bad data can lead to repeated failures.

How do verification checks change payout timing?

Verification state can directly delay release because providers can pause payouts when required information is missing or unverified. Treat pending or failed verification as a hold condition before submission, not as a problem to clean up after the fact. That keeps you from mixing compliance exceptions with ordinary payout failures.

What should we store for audit-ready proof of each payout decision?

Keep the beneficiary details used for the payout, whether the account identifier was an IBAN or account number, the SWIFT or BIC captured, the provider reference, timestamps, and every status change from hold to submit to complete or returned. If a payout is sent back, store the return reason from the provider record. That evidence pack is what lets finance, ops, and engineering agree on why a payout was released, blocked, or reversed.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- bis.org/publ/bppdf/bispap167.pdftrusted

- docs.stripe.com/global-payouts/manage-payoutstrusted

- docs.stripe.com/error-codestrusted

- ecb.europa.eu/paym/target/target-professional-use-document...trusted

- ecb.europa.eu/paym/target/target-professional-use-document...trusted

- eur-lex.europa.eu/EN/legal-content/summary/cross-border-paymen...trusted

- irs.gov/individuals/international-taxpayers/foreign-...trusted

- irs.gov/forms-pubs/about-form-w-9trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

What is an IBAN and How is it Different from a SWIFT Code?

For people handling high-stakes international payments, uncertainty is expensive. Not knowing whether a wire will arrive on time, or at all, pulls attention away from the work and adds avoidable risk. The fix is not another generic template. It is a repeatable process that tells you which details matter, where to get them, and how to check them before money moves.

Xero + Global Payouts: How to Sync International Contractor Payments into Your Accounting System

Treat this as a disbursement-sync problem, not a receivables setup task. Xero has clear ways to help customers pay invoices and, in some cases, to pay certain supplier bills. That is not the same as running outbound contractor payouts across countries, currencies, and payout methods end to end.

What Is a SWIFT Code? How Platforms Use BIC Codes to Route International Payouts

This guide exists because SWIFT and BIC data are not just banking labels. In a production cross-border payout flow, they are release-control inputs. A wrong value can stop processing, create extra fees, or trigger follow-up work your team should have prevented upstream.