Quick Answer

A SWIFT code, or BIC, identifies the bank in an international payout, while the IBAN identifies the destination account. For platforms, it should be a release-control field: validate its 8 or 11 character structure, keep institution routing separate from account routing, and hold payouts when beneficiary, bank, or corridor details do not align.

Why this guide exists for platform teams#

This guide exists because SWIFT and BIC data are not just banking labels. In a production cross-border payout flow, they are release-control inputs. A wrong value can stop processing, create extra fees, or trigger follow-up work your team should have prevented upstream.

- Routing data needs operational handling, not glossary-level understanding.

You already know these fields matter. The practical point is that the BIC identifies the financial institution, while the IBAN identifies the account held with that bank. That distinction should shape your payout form, your validation sequence, and your exception queue. If your product collects everything as one loose "bank details" blob, finance ops will spend time fixing issues engineering could have caught earlier.

- Correct format is necessary, but it is not enough to release funds.

A BIC consists of 8 or 11 alphanumeric characters, and that structure carries routing meaning. Validate the code structure, then confirm the account context fits the payout corridor. A valid-looking code tied to the wrong account details is still a bad payout instruction. That kind of failure can lead to non-processed transfers and manual intervention.

- The real goal is decision quality before the wire goes out.

For platform teams, the useful questions are operational: what should you collect, what should you validate automatically, what should trigger a hold, and what should a human verify before an international wire transfer is released? At minimum, your payout payload needs to tie beneficiary identity to destination bank details and the relevant institution identifier. A good checkpoint is whether your team can point to the source of each field, show how it was validated, and explain who can override a failed check.

- This guide stays narrow on purpose.

SWIFT/BIC handling matters because BIC data is used for addressing messages, routing business transactions, and identifying business parties. That makes this a routing-discipline topic first. So the scope here is deliberately practical: how to reduce payout errors, not how to rank providers on fees, delivery speed, or market coverage where current public evidence is incomplete or inconsistent.

- If you run recurring payouts, loose handling gets expensive fast.

One wrong BIC or SWIFT code can mean a failed transfer, extra fees, or a payment that is not processed. Treat SWIFT and BIC handling as a controlled release step with documented validation and evidence, not as a one-time onboarding field that nobody revisits. That is the baseline this article builds on.

For a step-by-step walkthrough, see Crypto Payouts for Contractors: USDC vs. USDT - What Platforms Must Know.

Who should use this shortlist and how to choose#

Use this shortlist if your team runs recurring cross-border bank payouts and wants fewer routing exceptions, clearer release decisions, and audit-ready records.

- Platform founders and product leads

Use it if you own payout onboarding, form design, or release rules. The role split should stay explicit: the BIC identifies the institution, and the International Bank Account Number (IBAN) identifies the account held with that bank. Look for platforms that treat BIC as a structured 8-11 character identifier with separate bank, country, location, and branch components, not a single free-text bank-details field.

- Finance ops and reconciliation owners

Use it when holds, returns, or investigations are eating manual time. Choose systems that preserve traceability for submitted routing data, validation outcomes, check timestamps, and override actions. In practice, for any held payout, your team should be able to retrieve the submitted BIC, IBAN, beneficiary name, and stop reason without raw-log work.

- Engineering teams building validation and holds

Use it when you want to block bad payout instructions before funds move. Format checks are necessary but not sufficient: an 8-11 character BIC can still be wrong in account context. Favor release logic that can hold payouts when identifier syntax passes but account details do not align.

- Teams operating with KYC and AML gates

Use it when payout release depends on risk-based identity verification and AML controls. In U.S. bank-partnered contexts, AML obligations also connect to program, recordkeeping, and reporting requirements under the Bank Secrecy Act. If your main goal is consumer remittance UX, this is not your main decision tool.

If you want a deeper dive, read What is an IBAN and How is it Different from a SWIFT Code?.

SWIFT and BIC basics your team must lock before build#

Lock these definitions into your product spec before implementation: BIC/SWIFT identifies the institution, IBAN identifies the account, and SEPA rules can change the payout path for EU euro flows.

- Treat BIC as the standard term, with SWIFT code as the common operations label.

BIC means Business Identifier Code, and teams commonly collect a "BIC or SWIFT code" interchangeably. Store it as a structured identifier with 8 or 11 characters, not as free text.

- Validate SWIFT/BIC by components, not as one string field.

A SWIFT/BIC contains separate parts: bank code, country code, location code, and optional branch code. Validate each part explicitly in your schema instead of relying on one generic "bank details" input.

- Keep institution routing and account routing separate in specs and UI copy.

The BIC identifies the financial institution; the International Bank Account Number (IBAN) identifies the destination account. If those roles are mixed, valid-looking routing data can still fail in practice. Treat mismatches as review gates.

- Call out SEPA explicitly for EU corridors.

In SEPA (Single Euro Payments Area) payment flows, IBAN is used for account identification, and SEPA technical requirements are set under Regulation (EU) No 260/2012. SEPA is designed to remove domestic-versus-cross-border differences for euro payments across 41 European countries (ECB status: 22 May 2025), so your spec should explicitly distinguish SEPA paths from non-SEPA international wires.

We covered this in detail in MT103 SWIFT Message Explained for Tracing International Wire Transfers.

Five payout routing patterns and when each one wins#

Once you separate institution routing from account routing, pattern choice becomes a tradeoff between reach, control, and exception cost.

- Direct SWIFT wire via your payout provider

Use this when broad bank reach matters most and your team can absorb more exceptions. For almost all international bank transfers, SWIFT/BIC is used to route payment to the correct bank and branch, so this follows standard bank-routing behavior.

Run one strict checkpoint: store BIC as a structured 8 to 11 character identifier, and record whether it is institution-only or institution-plus-branch. If the BIC parses but the beneficiary account context does not, stop and review instead of auto-retrying.

- IBAN-first regional bank payout with SWIFT fallback

Use this when you have a Europe-heavy mix and defined non-EU edge cases. It improves account targeting through IBAN when your release logic clearly separates SEPA and non-SEPA paths.

The tradeoff is added routing logic. Define when IBAN is enough for the route and when BIC fallback is required, since BIC can still appear in SEPA payment instructions. Validate IBAN-country context against the intended corridor before you allow fallback.

- Virtual account collection with downstream bank payout

Use this when reconciliation and finance control are core requirements. Virtual accounts are sub-ledger accounts linked to a physical account, so they can create a cleaner trail from incoming funds to outgoing wire activity.

The benefit is clearer audit traceability; the cost is more integration and treasury coordination. Require a record chain from collection reference to virtual account ID to payout release record, or you lose most of the reconciliation advantage.

- Batch payout orchestration with preflight validation

Use this when payout volume makes manual repair the bottleneck. Payment pre-validation is designed to verify payment information before cross-border initiation and can reduce rejections, returns, and manual intervention.

Validate before release, quarantine bad records, then approve the batch. Keep checks on BIC parts, including location and branch where present, and avoid late edits after signoff.

- Hybrid routing with compliance-triggered holds

Use this when policy control matters more than edge-case payout speed. Routing decisions should include explicit compliance controls, with holds tied to suspicious-transaction policies and procedures.

Make hold logic auditable: record why the payment was held, who cleared it, and what alert or document triggered the pause. This slows some payouts, but it avoids sending first and investigating later.

Comparison table for fast routing decisions#

Use this table when you need a quick decision based on what must be verified before release, where compliance gates apply, and how cleanly you can resolve exceptions later.

| Routing pattern | Required identifiers | Operational burden | Verification preflight | Common failure mode | Compliance gates | Auditability | Best-fit payout scenario |

|---|---|---|---|---|---|---|---|

| Direct SWIFT wire via payout provider | SWIFT code or BIC for bank routing; IBAN where corridor or bank requires account-level targeting | Medium to high; broad reach with more exception handling | Parse the 8- or 11-character BIC into bank code / country code / location code / optional branch code; confirm beneficiary account context matches. Human review: when the code parses but account context is inconsistent, or branch detail is unclear | Valid-looking BIC paired with wrong beneficiary account details | KYC at payee onboarding; KYB for business payees where your program applies it; AML before release | Provider ref: usually available; ledger trace: medium unless you store full payout release records; resolution: use provider reference plus beneficiary record to trace failures and reconcile to bank statements | Mixed global corridors where reach matters more than low-touch operations |

| IBAN-first regional bank payout with SWIFT fallback | IBAN for account routing; SWIFT/BIC fallback when route still needs a bank identifier | Medium; cleaner EU flows, more routing rules | Validate IBAN first, then parse fallback BIC into bank code / country code / location code / branch code if present; compare IBAN country with intended corridor before allowing fallback. Human review: when IBAN country and fallback bank country do not line up | Fallback used too early, masking a bad IBAN-country pairing | KYC before enabling payouts; KYB for business entities where applicable; AML at release, especially on non-routine fallback cases | Provider ref: yes; ledger trace: medium to strong if you store IBAN and fallback decisions; resolution: review route decision, then trace send and return activity | Europe-heavy payouts with a smaller set of non-EU exceptions |

| Virtual account collection with downstream bank payout | Virtual account identifier for funding trace; SWIFT/BIC for outbound bank; IBAN where required for destination account | High; more integration and treasury coordination | Before release, parse outbound BIC into bank code / country code / location code / branch code if present and link it to the collection record, virtual account, and beneficiary account. Human review: required when the funding trail is incomplete | Outbound payout cannot be tied cleanly to the incoming collection event | KYC or KYB at profile creation; for legal entities, beneficial-owner verification where required by your institution; AML before funds-out release | Provider ref: yes for payout, plus internal collection reference; ledger trace: strongest when both sides are linked; resolution: follow collection reference to payout release, then reconcile to statements | Platforms that need stronger audit trails across funds-in and funds-out |

| Batch payout orchestration with preflight validation | SWIFT/BIC for bank routing; IBAN where used in the corridor; batch file identifiers | Medium to high; better at scale with stricter cutoff discipline | Run preflight on every row: parse bank code / country code / location code / branch code, validate IBAN where present, and quarantine failures before approval. Human review: for quarantined rows, not the full batch | Late edits after validation or bulk release of bad records | KYC/KYB completed before a record enters the payable batch; AML screening at batch approval or release | Provider ref: yes at batch and often payment level; ledger trace: strong if batch ID links to payout rows; resolution: isolate failed rows instead of reopening the full batch | Payroll-like or recurring contractor cycles where manual repair is the bottleneck |

| Hybrid routing with compliance-triggered holds | SWIFT/BIC and IBAN as required by route, plus compliance profile status | High; slower on edge cases but tighter policy control | Parse bank code / country code / location code / branch code like other bank routes, then block release until policy gates clear. Human review: required for held cases or risk alerts | Teams retry held payouts without resolving the underlying compliance issue | KYC or KYB complete before release eligibility; AML as an explicit release gate; legal-entity review may include beneficial-owner verification | Provider ref: available once released; ledger trace: strong if hold reason, reviewer, and release decision are logged; resolution: clear hold, then trace payment or return using the provider reference | Higher-risk corridors or programs where policy control matters more than raw payout speed |

Treat the verification column as non-negotiable. A BIC is a structured 8- or 11-character identifier with institution, country, location, and optional branch components, and you should verify it before money is sent abroad. If structure passes but beneficiary context or IBAN-country pairing is off, stop the payout instead of auto-retrying.

Set hard boundaries in the compliance column. KYC and, where relevant, KYB should be completed before a payout profile is release-ready, and legal-entity review may include beneficial-owner verification. Held payouts should always carry a documented reason and clear disposition, not a vague "compliance review" label.

If two patterns still look comparable, use auditability as the tiebreaker. Payment operations includes tracking and attributing funds, resolving failures and returns, and reconciling to statements, so traceability controls usually outperform faster but looser release paths over time.

Data you must collect and validate before payout release#

Do not release a payout until beneficiary identity and bank/account data are complete and consistent.

- Collect a complete minimum payload

Capture the beneficiary's legal name, whether an individual or legal entity, recipient address, receiving bank name and address, account number or IBAN where used in that corridor, and the receiving bank's SWIFT code or BIC. Missing required wire data can delay or return a transfer, so completeness is a release control, not a formality.

- Validate in the right order

Run identifier syntax checks first, then name/ownership checks, then release eligibility. A SWIFT/BIC should be 8 or 11 characters and parse into bank code, country code, location code, and optional branch code. An IBAN is a separate account identifier. It can be up to 32 alphanumeric characters and includes a country code plus two check digits.

- Use name-account checks as a separate gate

A valid format does not prove the payout belongs to the named recipient. After syntax, check beneficiary name against account context. In euro instant-payments, Verification of Payee is an established discrepancy check, with euro area milestones tied to 9 October 2025.

- Stop on cross-field mismatch; review before release

If SWIFT format passes but IBAN-country pairing fails, stop release and route it to manual review instead of auto-retrying. For first live corridors, use dual sign-off between product/engineering for validation logic and finance ops for release controls and exception handling before fully enabling release.

Related reading: What Is Procurement as a Service? How Platforms Can Outsource Vendor Sourcing and Contracting.

Compliance and tax gates to wire into routing logic#

Once routing data is valid, release should depend on policy eligibility, not formatting alone. If compliance or tax status is incomplete, keep the payout on hold even when the SWIFT code or BIC is valid.

| Gate | What to collect or check | Release impact |

|---|---|---|

| KYC / identity and AML | Check policy status before routing status; FinCEN describes CDD as an explicit AML program requirement | Keep the payout on hold when compliance status is incomplete, even if the SWIFT code or BIC is valid |

| KYB and beneficial-owner verification | For legal entities, identify and verify beneficial owners of legal entity customers | Block release while entity review remains unresolved |

| Tax forms | Collect Form W-9 for independent contractors; use Form W-8BEN-E for foreign entities in U.S. withholding/reporting context; connect U.S. nonemployee compensation reporting to Form 1099-NEC workflows where applicable | Collect the matching form before downstream reporting; note the e-file threshold of 10 aggregated information returns effective January 1, 2024 |

| VAT validity and tax residency | Use VIES for a binary VAT validity result (valid or invalid); if you collect CRS-style self-certification, capture all disclosed tax residences | Keep the record available to release controls; use VAT validity as a VAT check, not as tax-residency proof |

- KYC/identity and AML checks should gate release, not happen after send

Treat customer due diligence as part of release logic. FinCEN describes CDD as an explicit AML program requirement, with the final rule effective July 11, 2016, and compliance required by May 11, 2018 for covered financial institutions. In practice, check policy status before routing status: a payout can be bank-valid and still not eligible to send.

- For business payees, run KYB-style entity checks and beneficial-owner verification where supported

For legal entities, go beyond company-name collection. FinCEN's CDD rule added a requirement to identify and verify beneficial owners of legal entity customers. Keep explicit exception states on the payout profile, and block release while entity review remains unresolved.

- Collect the tax form that matches the payee and context before downstream reporting

IRS guidance for independent contractors says the first step is collecting Form W-9. For foreign entities in U.S. withholding/reporting context, Form W-8BEN-E is used to document foreign entity status for chapters 3 and 4. If U.S. nonemployee compensation reporting applies, connect that profile to Form 1099-NEC workflows early, and account for the e-file threshold of 10 aggregated information returns effective January 1, 2024.

- Link VAT validity and tax-residency evidence to the same payout profile

For EU business payouts, VIES provides a binary VAT validity result, valid or invalid. Use that as a VAT check, not as tax-residency proof. If you collect CRS-style self-certification, make sure the profile captures all disclosed tax residences and keeps that record available to release controls.

Failure patterns that create returns and delayed settlements#

Most returns and delays come from two controllable issues: missing account context and unsafe retries. Fix IBAN-aware routing checks and idempotent retry controls before adding more automation.

| Failure pattern | Why it happens | Control |

|---|---|---|

| Valid-looking BIC without enough account context | A SWIFT/BIC confirms structure, not beneficiary correctness; the Account Holding BIC can differ from the payment routing BIC | Use complete payment instructions, including IBAN where applicable; route the payout to review when account context is incomplete or inconsistent |

| Retries without idempotency controls | A delayed or unclear response can lead to a second payout attempt for the same obligation | Store one idempotency key on the payout attempt and reuse it for every retry; align retry timing with key lifecycle rules, such as guidance that keys may be removed after at least 24 hours |

| Post-acceptance failures | A payout can clear preflight checks and still be rejected later for recipient-account issues, incorrect instructions, or unverified recipient status | Capture provider trace/reference data, verify the rejection reason, and update routing details before reopening |

| Urgent exceptions and repeat volume | A one-off urgent payout with conflicting details needs judgment, while recurring batches need consistency | Use targeted finance-ops review for a one-off urgent payout; for recurring batches, enforce preflight data checks, controlled retries, and clear exception records |

- A valid-looking BIC is not enough on its own

A SWIFT/BIC is an institution identifier, typically an 8-11 character code for bank, country, location, and sometimes branch. That confirms structure, not beneficiary correctness. The European Payments Council also notes the Account Holding BIC can differ from the payment routing BIC, so a BIC can look valid and still fail in payment context. Use complete payment instructions, including IBAN where applicable, to reduce delay and return risk. If format checks pass but account context is incomplete or inconsistent, route the payout to review instead of auto-resending.

- Retries without idempotency controls can create duplicates

When responses are delayed or unclear, a new request can trigger a second payout attempt for the same obligation. Idempotency controls exist to let you retry safely without performing the same operation twice. Store one idempotency key on the payout attempt and reuse it for every retry of that same attempt. Also align retry and reconciliation timing with key lifecycle rules, for example provider guidance that keys may be removed after at least 24 hours.

- Post-acceptance failures need exception handling, not blind retries

A payout can clear preflight checks and still be rejected later for recipient-account issues, incorrect instructions, or unverified recipient status. Treat that as an exception workflow: capture provider trace/reference data, verify the rejection reason, and update routing details before reopening. This keeps rework contained and speeds resolution.

- Use judgment for urgent exceptions; use strict controls for repeat volume

For a one-off urgent payout with conflicting details, a targeted finance-ops review can be the fastest way to decide whether evidence is strong enough to send. For recurring batches, consistency matters more: enforce preflight data checks, controlled retries, and clear exception records so the same bad data does not repeat.

Need the full breakdown? Read What is a Virtual IBAN and How Do Platforms Use It to Collect Payments Globally?.

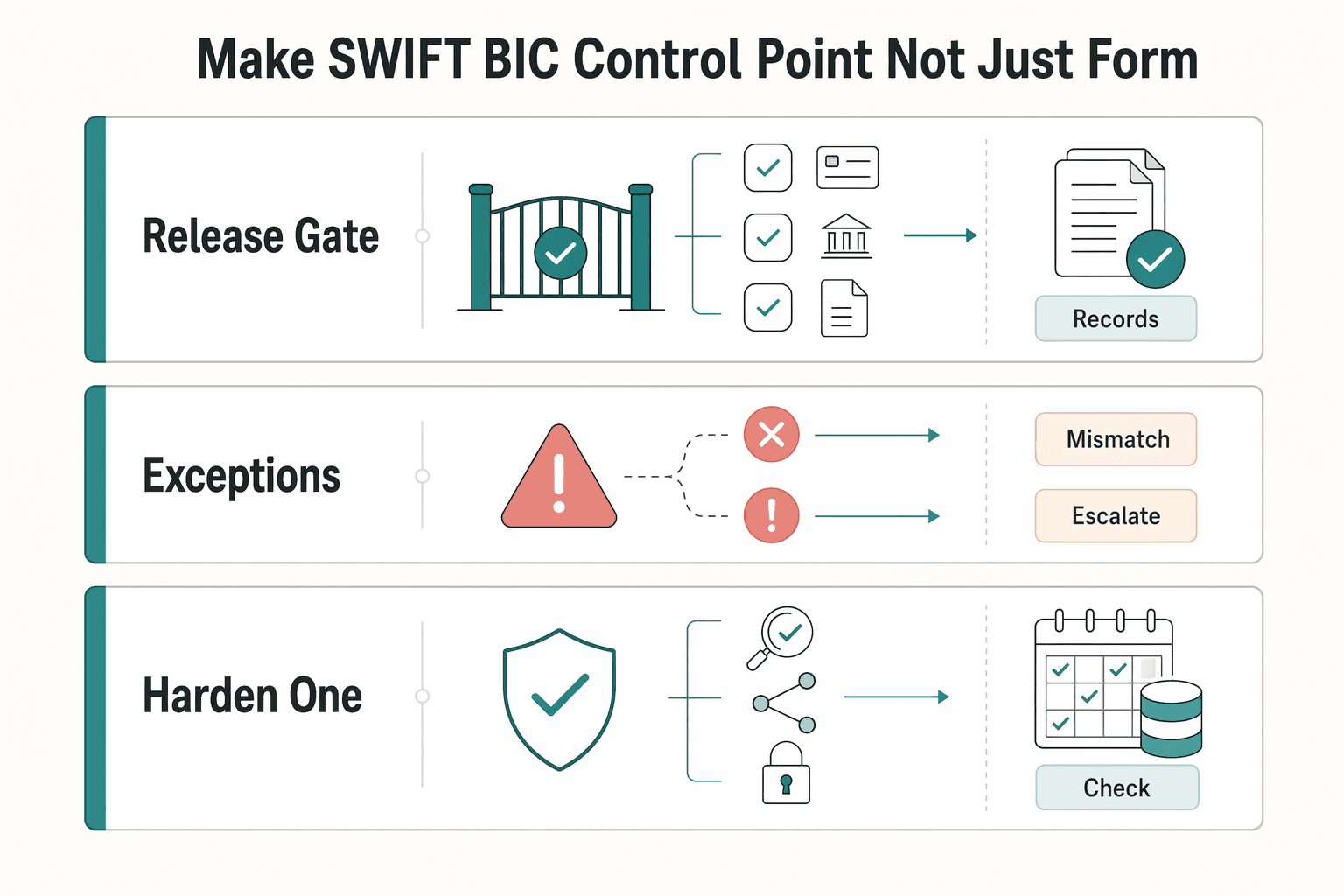

Make SWIFT BIC a control point not just a form field#

Treat SWIFT code/BIC handling as a release control, not passive form metadata. The practical goal is to stop payouts that look complete but are missing the checks and evidence required to release safely.

- Gate routing data before the wire is created.

In corridors where both identifiers are used, validate IBAN and BIC together at preflight, not as a last-step format check. If a required identifier is missing or the instruction does not pass your preflight rules, hold the payout instead of retrying blindly. Store the exact preflight result used at release so ops can show what was checked.

- Put KYC and AML on the release path, not in the exception queue.

Use a risk-based control design, and keep release gating inside it. FATF's 18 June 2025 update to Recommendation 16 focused on safer cross-border payments and stronger financial-crime detection, including monitoring for missing required originator or beneficiary information before processing. For identity, keep risk-based CIP verification on the critical path so unresolved profiles are held for review before send.

- Harden one real route this quarter and make it auditable.

If you change one thing first, implement preflight validation plus release gates for IBAN, KYC, and AML on one live routing path. Map that path against your comparison table and mark three checkpoints: where identifiers are validated, where compliance can block release, and what evidence is stored. One fully controlled route is more useful than broad but shallow coverage.

Frequently Asked Questions

What is a SWIFT code in platform payout operations, and is it different from a BIC?

In payout operations, SWIFT code and BIC are commonly used interchangeably for the same institution identifier. The formal standard is the BIC under ISO 9362. Treat the label difference as naming, not routing logic, and focus on whether the identifier matches the right bank context.

What does each part of a SWIFT/BIC string represent in practical validation terms?

A BIC is made up of a bank code, country code, location code, and an optional branch code. Do not validate it as one text blob. Validate each part so you can check both structure and institution context before release.

When do I need both an IBAN and a SWIFT code for one payout?

For relevant EU cross-border payment flows, guidance references using the IBAN together with the payment service provider's BIC. That does not mean every global corridor requires both. In that EU context, collect and validate both; otherwise confirm corridor requirements before release.

Where should ops teams source and verify SWIFT/BIC data before release?

The strongest source is the account-servicing bank. Only the bank servicing the account can provide the correct IBAN and the related BIC for that account. Use bank-provided beneficiary details as the evidence record, and hold the payout if verified details are not available.

What should a platform validate before sending an international wire transfer?

Start with syntax and structure, including bank code, country code, location code, and branch code where present. Then check account context, especially whether an IBAN is present where applicable and whether IBAN and BIC details align with bank-provided account information. If the BIC passes format but the evidence is weak or mismatched, stop release and route it to manual review.

What is still unknown from public SERP guidance when comparing payout platforms?

Public search results are not a trustworthy basis for audited, apples-to-apples comparisons on fees, settlement timing, or corridor-level support claims. They also do not provide one universal compliance checklist that applies identically across jurisdictions. Use public pages for terminology and feature discovery, then ask providers for corridor-specific documentation, operational requirements, and evidence of what they actually support.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- bis.org/cpmi/publ/brief9.htmtrusted

- bsaaml.ffiec.gov/manual/AssessingComplianceWithBSARegulatoryR...trusted

- ecb.europa.eu/paym/target/target-professional-use-document...trusted

- ecfr.gov/current/title-31/subtitle-B/chapter-X/part-1...trusted

- europa.eu/youreurope/business/taxation/vat/check-vat-n...trusted

- federalregister.gov/documents/2016/05/11/2016-10567/customer-due...trusted

- irs.gov/businesses/small-businesses-self-employed/fo...trusted

- irs.gov/forms-pubs/about-form-w-9trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

IBAN vs SWIFT for International Contractor Payouts on Platforms

If you are scaling international contractor payouts, treat code choice as a release control, not a glossary question. The practical rule is simple: collect the right bank identifiers up front, validate them before approval, and keep enough evidence to explain every submitted, rejected, returned, or retried payout later.

What is an IBAN and How is it Different from a SWIFT Code?

For people handling high-stakes international payments, uncertainty is expensive. Not knowing whether a wire will arrive on time, or at all, pulls attention away from the work and adds avoidable risk. The fix is not another generic template. It is a repeatable process that tells you which details matter, where to get them, and how to check them before money moves.

When Platforms Should Use Wires vs Local Rails for Cross-Border Payouts

Treat rail choice as product logic, not team habit. No rail wins everywhere. SWIFT and local payment rails solve different payout risks, so your job is to route each payout by destination, currency, speed, and cost, not by whichever option sounds more global or more modern.