Quick Answer

Hire contractors in Brazil by treating the process as a classification and recordkeeping control problem. Confirm a real services model based on deliverables and invoices, keep contract, invoice, and payout records aligned, and block first payment until required evidence is complete. If CLT status, identity, tax treatment, or payout setup is unclear, pause and escalate before signature or release.

Hiring contractors in Brazil without creating hidden compliance debt#

If you own compliance, legal, finance, or risk, hiring contractors in Brazil is mainly a classification and recordkeeping control problem, not a sourcing problem. Misclassification risk can create retroactive liability when a contractor or PJ setup operates like employment.

This guide is practical and narrow. It gives decision checkpoints for contractor setup, invoicing, and payout readiness, plus clear escalation points when facts are unclear. The goal is not just to complete a payment, but to show the person was onboarded and paid as a genuine independent contractor with records that match reality.

Treat legal boundary calls in Brazil as escalation decisions, not template decisions. The line is still contested, and the policy debate remains active. In October 2025, Brazil's STF held a major hearing on pejotização with nearly 50 voices from labor, legal, corporate, and academic groups.

Use this as operational guidance, not local legal advice. It does not provide a definitive legal test, so ambiguous cases should go to Brazil-qualified counsel before signature or first payout.

Your core operating check is simple. Is the engagement run through deliverables and invoices, rather than time-based supervision? Contracts and payment records should reflect project outputs, acceptance, and commercial invoicing. If documents and day-to-day reality diverge, your compliance posture is already weakening.

Keep the control mindset disciplined. Confirm the identity and contracting lane, confirm the invoicing and payment lane, confirm payout readiness, and log unresolved issues before release. A transfer that clears with missing records or unresolved treatment is still a control failure.

Success here is specific: first payout only after complete records, a defensible contractor classification, and no employee-like control pattern in practice. If you can produce the signed agreement, classification rationale, invoice trail, and payout confirmation without gaps, you have materially reduced hidden compliance debt.

For a larger platform view, see Gig Worker Tax Compliance at Scale: How Platforms Handle 1099s W-8s and DAC7 for 50000+ Contractors.

Know the legal line before you onboard anyone#

Get the legal line straight before onboarding starts. If the working pattern looks employee-like under CLT, stop and re-check contractor classification before signature.

In Brazil, an autônomo provides services independently, with real control over method and schedule. Employee relationships are different because workers hired as employees fall under the CLT framework. The practical question is simple: are you buying deliverables, or directing the person's routine?

Misclassification risk usually appears in operating behavior, not contract labels. Common disguised employment signals include:

- taking orders as if in a reporting line

- fixed working hours set by the company

- default dependence on company tools

- dependency on a single client

Before first onboarding approval, verify what actually happens in practice. The person should be able to set hours, use their own tools, and work toward services and outputs rather than being treated like full-time staff. If day-to-day instructions start resembling employee-style control, misclassification risk rises.

Your documents should support a real services relationship, and your billing trail should match that model. For tax compliance, a contractor-issued Nota Fiscal (NF-e) is a core record in that trail.

Use a hard stop when delivery oversight starts becoming people management. If the business needs fixed attendance, constant supervision, or exclusive-style dependency, do not try to solve that with contractor paper. Misclassification can lead to back payments, fines, and lawsuits.

For more detail, see Brazil's CNPJ for Foreign-Owned Businesses: When It Is Needed and What It Does.

Use a classification decision table before contract signature#

Use a pre-signature decision table to test facts, not labels. If the facts point to an employment relationship under CLT, calling someone an independent contractor in the contract will not prevent employee classification.

Treat this as an internal control, not a legal formula: assess the four CLT elements (individuality, regularity, compensation, and subordination), and escalate before signature when the pattern is employee-like or unclear. Do not rely on template contractor agreements alone.

| Signal | Independent contractor signs | Employee-like signs | Evidence to collect | Decision rule / action |

|---|---|---|---|---|

| Individuality (CLT element) | Engagement is documented as a services relationship | Facts indicate an employment-style personal work relationship | Contract scope, SOW language, exception notes | Treat as a potential CLT signal and review with the other CLT elements |

| Regularity (CLT element) | Work is organized around defined services/deliverables | Facts indicate ongoing, regular work consistent with employment | SOW cadence, approval logs, operating notes | Treat as a potential CLT signal and review with the other CLT elements |

| Compensation (CLT element) | Billing follows contractor service invoicing | Compensation pattern looks employee-like in practice | Contract payment terms, invoices, nota fiscal records | Treat as a potential CLT signal and review with the other CLT elements |

| Subordination (CLT element) | Provider retains autonomy in how duties are performed | Company imposes orders, policies, procedures, and required reporting | Manager instructions, policy/process records, reporting logs | Treat as a high-priority escalation signal |

| Contract framework and documentation | Engagement is structured under the Código Civil with contractor-issued nota fiscal | Documentation and day-to-day facts point in different directions | Contract terms, SOW, nota fiscal, exception notes | If facts and paperwork diverge, escalate before signature |

| Uncertain case | Signals are mixed | Signals are mixed | Legal review request, risk summary, temporary controls log | Pause and escalate to Brazil-qualified legal review; apply temporary controls before first payout |

For contractor engagements under the Código Civil, your records should read like a services model in practice. Scope should tie to outputs, approval should tie to deliverables, and billing should be supported by contractor-issued nota fiscal. If the evidence starts to look like staff management, escalate before execution.

Need the full breakdown? Read Enhanced Due Diligence for High-Risk Contractors: What Triggers EDD and How to Conduct It.

Draft contractor agreements that match real operating behavior#

The agreement should match the service model you will actually run. If the day-to-day plan depends on fixed hours, method-level manager direction, or staff-like supervision, fix the operating model before signature. Calling someone an independent contractor in the contract does not solve classification risk when the working pattern points the other way.

This is where the decision table turns into practice. The agreement, statement of work, manager instructions, and invoice process should align around the same model: project-based work, contractor control over execution, and payment tied to defined outputs.

Write for outputs, not attendance#

Start with outputs and leave room for contractor execution. Strong agreements describe deliverables, milestones, acceptance criteria, deadlines, and completion standards without turning into role descriptions, coverage schedules, or reporting-line terms.

| Agreement area | Contractor-aligned | Employee-like/risk |

|---|---|---|

| Payment basis | Payment tied to defined outputs | Fixed hours |

| Work definition | Deliverables, milestones, acceptance criteria, deadlines, and completion standards | Role descriptions, coverage schedules, or reporting-line terms |

| Execution control | Contractor control over execution; provider controls schedule and method | Method-level manager direction; fixed windows and task-by-task direction |

| Requirements | Quality, security, or brand requirements for deliverables | Fixed daily availability, time-off approvals, constant status reporting, or broad limits on third-party work |

Keep the distinction clear: output standards fit a contractor model, but employment-style control raises risk. You can set quality, security, or brand requirements for deliverables. Be careful with terms that require fixed daily availability, time-off approvals, constant status reporting, or broad limits on third-party work.

Before signature, run a consistency check between the contract and manager expectations. If the contract says the provider controls schedule and method, but the manager expects fixed windows and task-by-task direction, resolve that mismatch first.

Preserve non-exclusivity in practice#

State non-exclusive engagement plainly, then avoid terms that quietly reverse it. Independent contractor arrangements are presented as project-based and compatible with third-party work, so exclusivity-like restrictions should be limited and deliberate.

You can still protect IP ownership and data-processing terms. The key is not to layer in restrictions that make the relationship function like exclusive employment.

If the same person is being treated as both employee and contractor at the same company, treat that as a classification escalation, not a drafting cleanup.

Align payment and invoicing language with your operating records#

Payment and invoicing clauses should match how finance and operations will actually process the engagement. Keep contract terms, invoice expectations, and payout records consistent so your audit trail supports one coherent model.

If your process captures additional compliance fields, define who provides what and who reviews treatment before payouts begin. Where treatment is unclear, pause and escalate to your compliance owner instead of leaving ambiguous language for operations to interpret later.

Add a re-review trigger before renewal#

Include a change-control trigger so classification is re-reviewed when the operating model shifts. Example triggers are movement from project work to ongoing coverage, increased supervision, staff-like tool dependence, or newly introduced exclusivity.

Assign ownership for that checkpoint and keep a compact evidence pack: signed agreement, current SOW, amendments, acceptance records, invoices, and exception notes. Classification risk can rise after a clean signature when operating behavior changes and nobody re-checks fit before renewal.

Related reading: How Independent Contractors Should Use Deel for International Payments, Records, and Compliance.

Verify tax identity and payer responsibilities before first invoice#

Do not let the first invoice set your tax process by default. Before payment, assign one identity lane, record who approved it, and block submissions with missing or conflicting required data.

Your contract and invoice record must describe the same operating reality. If profile data, invoice identity, and tax-handling notes do not align, the audit trail is weak from day one. Treat CPF, CNPJ, MEI, and ISS as local policy controls that must be defined in advance — confirm the applicable rules with a Brazil-qualified adviser.

Set one identity lane and keep records consistent#

Pick the contractor's lane in intake and keep it consistent across contract, onboarding profile, and invoice. Do not infer identity from bank details, chat messages, or informal descriptions.

Use a hard submission gate for required fields. This follows the documented SSA certificate control pattern: required fields must be complete to submit, and incomplete information can delay or prevent an accurate decision. If records conflict, pause payout, correct the source record, and log who approved the correction.

Separate contractor tax responsibility from payer-side controls#

Regardless of contract wording, set payer-side controls before first invoice: documented review ownership, collected records, consistency checks, and escalation notes.

| Certificate checkpoint | Detail |

|---|---|

| Purpose | Prevent dual social security taxation by assigning coverage to one country and exempting taxes in the other |

| U.S. evidence | SSA issues a U.S. Certificate of Coverage when coverage is assigned to the United States |

| Status values | Received; Pending; Completed |

| Follow-up timing | Allow 90 business days before follow-up |

| Mailing timing | Allow up to two weeks for mailing after issuance |

| Submission limit | Online submission has confidentiality limits |

For cross-border social security treatment, the grounded document here is the Certificate of Coverage under a Totalization agreement. The sources state these agreements are designed to prevent dual social security taxation by assigning coverage to one country and exempting taxes in the other. When coverage is assigned to the United States, SSA issues a U.S. Certificate of Coverage.

If your treatment depends on that evidence, track status and do not assume exemption before the record is complete. The SSA workflow also gives useful timing and state controls: Received, Pending, Completed, allow 90 business days before follow-up, and allow up to two weeks for mailing after issuance. Because online submission has confidentiality limits, keep sensitive identity documents in approved channels rather than ad hoc email or chat.

Treat ISS as a policy gate, not an operations guess#

The supplied sources do not provide ISS rates, fields, thresholds, or filing checkpoints. Define ISS-related fields in your internal Brazil policy, require invoice-to-record consistency, and hold invoices when treatment is unclear.

| Identity lane (defined in your policy) | Required docs before first invoice | Review owner | Escalate when |

|---|---|---|---|

| Lane 1 | Document set defined in your Brazil policy | Finance or tax operations | Missing required document, incomplete field, or identity mismatch |

| Lane 2 | Document set defined in your Brazil policy | Finance or tax operations | Missing required document, incomplete field, or identity mismatch |

| Lane 3 | Document set defined in your Brazil policy | Finance or tax operations, with tax review when unclear | Missing required document, incomplete field, identity mismatch, or unclear tax treatment |

This is an ownership template, not a legal checklist. No complete identity record means no first-invoice approval.

Related: Brazil Platform Operator Tax Controls for CIDE, ISS, and CBS/IBS Transition.

Choose payout rails with control tradeoffs, not speed claims#

Once the identity lane is set, choose payout rails by control quality, not headline speed. Favor options that let your team trace payment status, handle retries consistently, reconcile cleanly, and manage exceptions without losing the audit trail.

If payout volume is high or retries are frequent, prioritize rails and providers that keep status history and decision records clear from request through outcome. Faster movement can still create more operational risk when status detail, failure context, or reconciliation outputs are weak.

Judge the rail by what you can prove later#

Treat rail selection as a safety-versus-velocity decision, not just a treasury optimization. In practice, sources highlight settlement delays and fragmented integrations as scaling burdens, and they emphasize detection during and after execution.

Ask proof questions early. Can you tie each payout request to a unique record, distinguish retries from new attempts, and reconcile payment outputs back to approved invoices without manual guesswork? If not, the rail may look fast but remain expensive to operate.

Controls should work before, during, and after execution. Pre-release checks, in-flight visibility, and post-payment detection are all part of a usable control design.

Compare options by operator consequences#

This comparison is a control aid, not a legal or Brazil-specific rail ranking. The sources here do not establish PIX-specific settlement behavior, fees, limits, or retry mechanics, so validate what your provider actually records and exposes.

| Payout path | What to verify before rollout | Control upside if supported well | Control risk if weak |

|---|---|---|---|

| PIX | Whether the provider preserves clear status history, references, exception records, and reconciliation outputs | Day-to-day operations are easier when request, status, and outcome stay consistently linked | A transfer can complete while evidence and exception handling remain unclear |

| Direct bank integrations across multiple banks | API consistency, status normalization, failure handling, and exception ownership across banks | Supports flexibility and multi-rail operating models | Fragmented APIs can increase manual reconciliation and support burden |

| Cross-border or bank-network rails used for strategic comparison (for example, SWIFT or SEPA-style infrastructure) | Reference continuity, status visibility across handoffs, and reporting outputs | Useful for strategic comparison of control and reporting coverage across rails | Additional handoffs and regulatory complexity can increase operating burden |

If you are deciding between building direct connectivity and buying a provider, treat it as a real build-versus-buy control decision. Building can increase flexibility but often adds integration and operating burden. Buying only helps if the provider exposes the records your finance and compliance teams need.

Payment success can still be a compliance failure#

Payment completion is not compliance completion. You can still fail your internal control standard if required evidence is incomplete or tax-treatment decisions remain unresolved in your policy.

Set a hard release gate before payment execution. Payout status alone should not serve as approval evidence. Keep payout execution dependent on a complete evidence pack, including approved identity lane, record consistency, and required policy decisions. For implementation detail on PIX operations, see How to Pay Contractors in Brazil Using PIX: A Platform Builder's Guide.

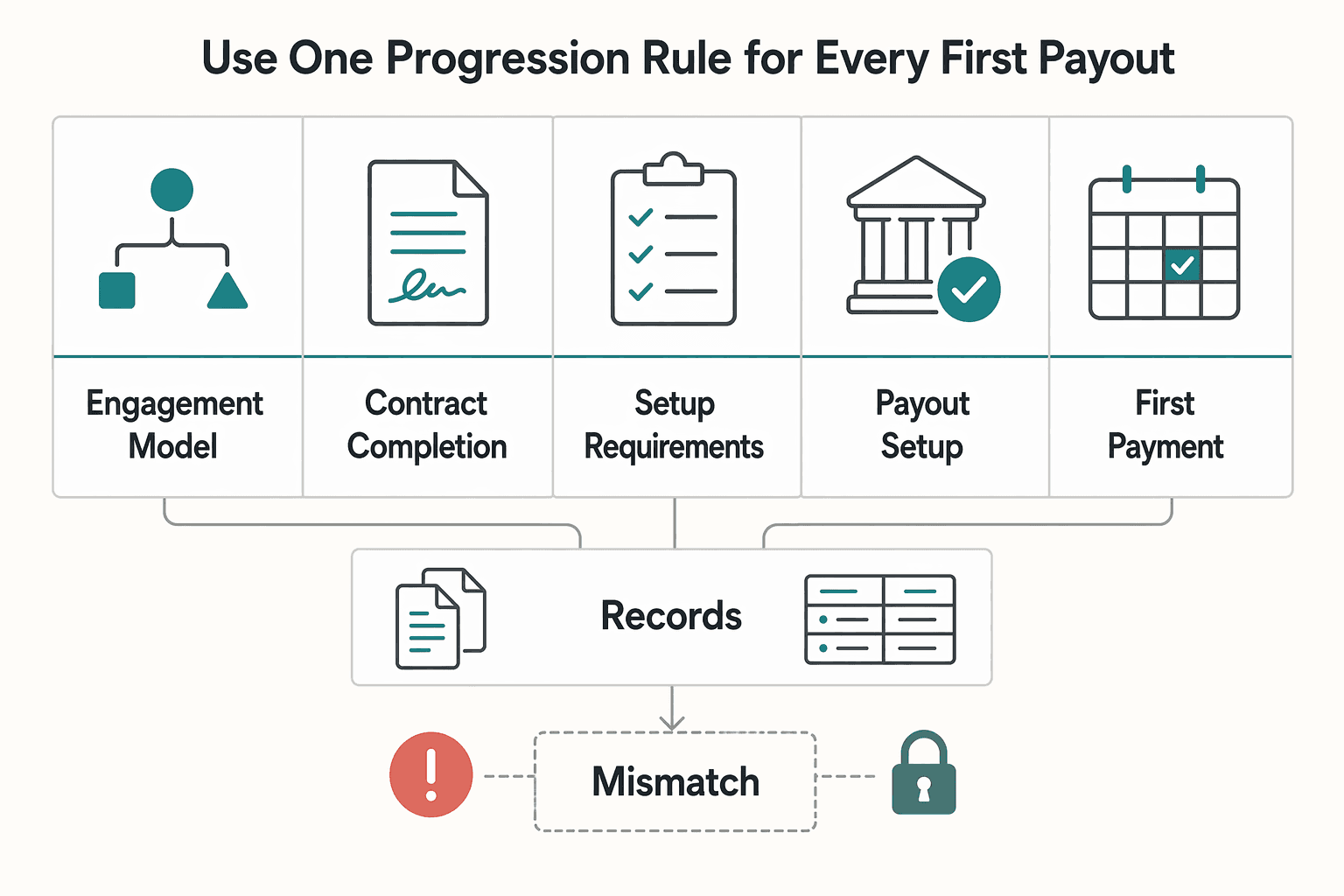

Run onboarding and first payout in a fixed order#

Treat first payout as a release gate tied to onboarding completeness. For Brazil engagements, use a clear internal progression: decide the engagement model early (EOR or your own entity), complete contracts and required setup records, finalize payout setup, then release payment. This is an internal control choice, not a statutory sequence, and it helps prevent funds from moving before the record is complete.

On a DIY path, legal may handle contracts while payments run through a third-party platform. That model works only when handoffs are explicit and owned. If ownership is unclear, unresolved issues can surface at payout time.

Use one progression rule for every first payout#

| Step | Primary owner | What must be true before next step | Record to keep | What blocks progression |

|---|---|---|---|---|

| Engagement model decision | Legal or compliance | Path is confirmed (EOR or own entity) and no open escalation remains | Decision record linked to contractor profile | Unresolved model or compliance escalation |

| Contract completion | Legal | Agreement is fully executed and aligned with the engagement model | Final signed agreement version | Missing signature, stale version, or mismatch with operating model |

| Setup requirements by path | Legal and operations | Required setup steps for the chosen path are complete (for entity setup, this can include notarized Portuguese documents and required registrations, including INSS) | Filed setup artifacts and status notes | Missing required setup artifact or open registration step |

| Payout setup | Payments ops | Payout details are complete and mapped to the approved payee record | Setup confirmation in payout system | Incomplete payout details or broken record linkage |

| First payment release | Finance approver | All prior gates are closed and payment is reconcilable to approved engagement | Approval record and payout status trail | Any open exception from earlier gates |

The key midpoint check is consistency across records. Keep the engagement model, contract, setup artifacts, and payout record aligned before first release.

Name gate owners before money moves#

Set gate ownership before the first invoice arrives. Legal owns engagement-model decisions and contract completion. Operations and finance own setup completion, payout execution, and payment exceptions, but should not approve payment when required evidence is still open.

When facts are unclear, escalate early and seek specialized technical advice rather than making first-payout decisions through ad hoc exceptions. First payout sets the control standard for renewals, retries, and future audits, so avoid informal exception handling in chat or email. Turn this sequence into enforceable gates and status checks in your operating runbook with Gruv Docs.

Hold first payment on missing fields#

Apply a strict internal no-missing-fields rule for first release. If contract evidence is incomplete, setup records are inconsistent, or required signoff is pending, hold payout and log escalation. A completed transfer does not fix an incomplete onboarding record.

Build an audit-ready evidence pack from day one#

An audit trail only helps if it can be retrieved and defended. Once payout gates are in place, a major risk is evidence fragmentation across tools. At that point, you may no longer be able to show why a contractor was approved, which onboarding path was chosen, what invoice was paid, and how failures were resolved.

Keep one evidence pack per engagement, not scattered records across email, chat, drives, and tickets. Use a structured checklist so each review is documented consistently and mapped to the real workflow from intake to payout.

Keep the minimum record set complete#

Keep the minimum record set complete from the start. At minimum, each contractor file should include:

| Evidence item | Minimum content |

|---|---|

| Agreement | Final signed agreement |

| Classification rationale | Classification rationale, including escalation notes |

| Identity and tax records | Identity and tax records used for the approved onboarding path |

| Invoice trail | Invoice trail, including submission and approval record |

| Payout confirmation | Payout confirmation tied to the payee record |

| Exception log | Exception log, including holds, retries, reversals, and resolution approval |

Later reviews test how records connect, not whether one document exists. If contract identity, invoice identity, and payout beneficiary do not align to the approved path, treat it as a control exception and log it formally.

Before closing a payment file, verify identity consistency across contract, invoice, and payout record. If a contractor was reviewed on one path but invoiced or paid through a mismatched record, document and escalate instead of patching it informally in chat.

Trace the full path, including failed payment events#

Your file should trace the full path, not just contract review. That means the original request, onboarding approvals, submitted invoice, payout outcome, and any retry or reversal.

When evidence is split across spreadsheets, tickets, finance tools, and inboxes, disputes turn into manual reconstruction. A completed transfer alone is not enough. You need request-to-outcome traceability, including who handled each exception and what changed.

If the same contractor shows repeated retries or reversals, treat that as a control review trigger, not only a payments issue. Repeated exceptions can signal weak payee setup, inconsistent records, or poor handoffs across legal, finance, and payments ops.

Control sensitive fields and make retrieval deliberate#

Limit full-record access to people who need it, and use masked views for routine operations involving personal data. This reduces unnecessary exposure while keeping the record usable for review, disputes, and inquiries.

Define retention and retrieval expectations in writing. This section does not establish one Brazil-specific retention period for all artifacts. Set internal schedules with legal and tax input, name the source of truth for each record type, and document who can retrieve files and how incomplete records are handled.

An evidence pack is a core control, not extra admin. When legal or tax facts are unclear, record the uncertainty and escalate to qualified professional advice before payout decisions are finalized.

If you want a deeper dive, read The Agency Scaling Blueprint: From Solo Freelancer to Hiring Your First 5 Global Contractors.

Handle failure modes before they become legal exposure#

Use the evidence pack to block payments when core controls fail, not to explain problems after the fact. The highest-risk failures usually begin as routine exceptions: missing compliance evidence, unresolved record inconsistencies, or work patterns that look like employment under CLT.

Treat evidence gaps as release blockers#

If key records do not align across the engagement file, do not release funds. A completed payout does not repair a broken record trail.

Apply the same rule when compliance evidence is missing. If you cannot produce proof of remittances and reporting artifacts (for example, eSocial receipts), treat it as a control exception and escalate. Log the gap, hold payment, and resolve the record before payout.

Watch the real working relationship, not only the contract#

Misclassification risk turns on the real relationship, not just contract wording. A clean agreement does not offset employee-like day-to-day control.

Treat these as red flags in practice:

- company supervision and direction over how work is done, not just deliverable acceptance

- single-client dependency where the worker primarily relies on your company for income

- directed, ongoing work that resembles an employee relationship in practice

These patterns map directly to control and economic dependence. Directed, ongoing work may be treated as employment under CLT, and exposure can include unpaid wages, overtime, severance, FGTS deposits, social security contributions, back taxes, benefits, and fines.

Escalate patterns, not just edge cases#

Escalate when you see repeatable signals, not only isolated errors. Set triggers for ambiguous CLT boundaries, recurring evidence gaps, and repeated exceptions within the same account cohort or manager group.

If one contractor has repeated control-risk signals, review that record. If several contractors in the same cohort show the same pattern, open a broader control review.

Document escalation in the same evidence pack as contract, invoice, and payout records: what triggered review, who approved hold or release, and what remains uncertain. When employee-status boundaries are unclear, pause the next payment or renewal and get Brazil-qualified legal or tax advice before the pattern hardens into legal exposure.

For a step-by-step walkthrough, see Quarterly Tax Payment Calendar for Contractors: All Four Deadlines and How to Calculate Each.

Decide when to use direct contracting, Agent of Record, or Employer of Record#

Use direct contracting when the case is low complexity and your team can maintain classification evidence over time. If classification is uncertain or employment obligations are becoming unclear, consider AOR or EOR instead of carrying that risk internally.

| Model | Control depth | Legal certainty | Operational overhead | Cost visibility in Brazil |

|---|---|---|---|---|

| Direct contractor engagement | Typically the most direct control over onboarding, contract, invoice review, and payout decisions | Lower when facts drift, because you must support contractor classification under the Código Civil | Higher internal burden for contract checks, Nota Fiscal records, and renewals | Varies with your internal process and how well compliance work is tracked |

| Agent of Record | Moderate control, with provider support from onboarding through payment | Can reduce risk in contractor cases, but does not replace strong underlying facts | Can reduce day-to-day contractor administration versus fully direct management | Varies by provider terms and scope |

| Employer of Record | Less day-to-day employer administration on your side | Strong for employee hiring, because the EOR is the legal employer and handles payroll, contracts, and labor-law compliance | Lower internal employment administration, especially without a Brazil entity | Employee-model payroll and compliance obligations still apply |

The legal boundary is the real decision point: contractor services sit under the Código Civil, while employee relationships trigger CLT rules. In the employee case, one EOR source describes the provider as the legal employer that can hire without your local entity. It can create compliant employment contracts and run payroll, tax filings, and contributions.

Your practical checkpoint is whether your team can keep core records current after onboarding: classification rationale, service contract records, and Nota Fiscal records as work patterns change. If you cannot maintain that record trail through renewals, direct contracting is a weak fit even if setup looked simple.

Watch for drift into an employee-like relationship. If the contractor setup starts to resemble employment, pause renewal and escalate model choice. An AOR may support contractor operations. If the role is functionally employment, EOR is the cleaner path.

Be explicit about what automation can and cannot decide#

Use automation to enforce routine controls, but do not let it make final legal classification calls. It should block incomplete records, require required documentation, and keep processing inside approved controls. It should not decide whether a working relationship is employment under CLT.

That line matters because difficult cases are factual, not just procedural. In Brazil, employee status is tied to direction and supervision for pay, while independent contractors are self-employed service providers. Software can flag risk signals, but it cannot conclusively resolve ambiguous or drifting facts.

A practical policy is simple:

- Systems gate routine checks: required fields, required records, approved tools, and traceable workflow controls.

- Humans decide edge cases: conflicting facts, employee-like supervision patterns, or other classification uncertainty.

- Humans own final outcomes: approve, hold, or escalate for legal or tax review, with the reason recorded.

Keep a defensible audit trail for every outcome: classification rationale, key records, process status, exception notes, and any override owner or reason. Without that trail, controls may run, but they are hard to defend.

Do not overtrust consistency from automation alone. Misclassification in Brazil can lead to fines, back taxes, and other penalties, and workers can file labor claims free of charge. If a case raises a real CLT question, pause and escalate to human review.

Build control depth where risk is real, not everywhere#

Strong outcomes come from clear decision checkpoints on classification, onboarding documentation, and payout release controls, not from fast-onboarding claims. Start with one defined Brazil cohort and make the first payout contingent on those checkpoints.

Take the next step in one cohort first: implement a classification table and a first-payout checklist for a defined Brazil group, then expand only after exception handling is stable. If reviewers are re-deciding the same edge cases, your controls are not stable yet.

Put review depth at the real breakpoints#

Do not apply maximum scrutiny to every file. Put deeper review where risk concentrates: unclear contractor status, unclear identity records, or payout setup moving forward before records are complete.

For most teams, three gates are enough to start:

- a documented classification decision before approval

- alignment across contract, invoice, and payee profile on the same legal identity record

- a first-payment hold until required fields and payout approvals are complete

Focus verification on cross-record consistency. If records conflict or payout details change late, stop release, log the exception, and assign clear ownership before funds move.

Pilot one cohort before standardizing#

A one-cohort rollout gives better signal than designing a full process in theory. Use it to find where controls are too loose, too heavy, or repeatedly escalated.

Keep a decision trail from day one: classification rationale, agreement record, identity record, invoice trail, payout confirmation, and notes for overrides or escalations. If a reviewer cannot reconstruct the approval from that file, tighten the control.

Do not treat payout success as proof of decision quality. A transfer can succeed while classification or identity support is still unclear, leaving a weak audit trail.

That caution is practical because one industry source says contractor classification in Brazil remains under Federal Supreme Court review, creating uncertainty for organizations relying on contractors. When facts are unclear, escalate early and document why.

Read deeper where execution detail matters#

For rail tradeoffs across markets, read How to Pay Contractors in Latin America: Brazil Mexico Colombia Argentina Rails Compared. For PIX execution depth, read How to Pay Contractors in Brazil Using PIX: A Platform Builder's Guide.

This pairs well with our guide on Adverse Media Screening for Contractors on Real-Time Payment Platforms.

If you need to validate your Brazil contractor control design before rollout, talk with Gruv.

Frequently Asked Questions

How do you avoid contractor misclassification when hiring in Brazil?

Avoid misclassification by structuring the engagement around deliverables, contractor-issued invoices, and contractor control over schedule and method. Review the facts before signature using the four CLT elements as an internal control, and treat subordination or staff-like supervision as a high-priority escalation. If the documents and day-to-day reality diverge, pause and get Brazil-qualified legal advice.

What is the practical difference between an `independent contractor` and an `employee` under `CLT`?

In practice, an independent contractor provides services independently and controls method and schedule, while an employee relationship under CLT looks more like company direction of the person's routine. The key question is whether you are buying deliverables or directing attendance, hours, and reporting behavior. Fixed working hours, orders in a reporting line, and staff-like supervision raise employee-style risk.

Who is usually responsible for taxes and `social security contributions` when paying contractors in Brazil?

These materials do not establish Brazil's domestic allocation for contractor taxes or social security contributions. One supported point is that under Totalization agreements, coverage can be assigned to one country and exempted in the other, with a Certificate of Coverage used as proof. If your treatment depends on that evidence, track its status and do not assume exemption before the record is complete.

When should a team use `CPF` vs `CNPJ` vs `MEI (Microempreendedor Individual)` in contractor onboarding?

These materials do not state when to use CPF, CNPJ, or MEI, so they do not support a Brazil-specific lane rule. Operationally, choose one approved identity lane in intake and keep it consistent across the contract, onboarding profile, and invoice. If identity type is unclear or records conflict, hold payout and route the case for Brazil-qualified review.

What should be verified before sending the first `PIX` payout to a contractor in Brazil?

Before a first PIX payout, confirm the approved identity lane, complete required fields, and make sure the payout record matches the contract and invoice. Verify that your provider preserves clear status history, references, exception records, and reconciliation outputs. Do not treat payment completion as compliance completion if evidence or policy decisions are still unresolved.

When should we escalate to local legal or tax counsel instead of relying on platform automation?

Escalate when facts are mixed or employee-like, when identity or tax treatment is unclear, or when records conflict before signature, first payout, renewal, or the next payment. Automation should enforce required fields and workflow controls, but it should not make final CLT classification decisions. Repeated exceptions, supervision patterns, or evidence gaps should trigger human review and Brazil-qualified legal or tax advice.

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- eeoc.gov/best-practices-private-sector-employerstrusted

- farmingdale.edu/courses/index.shtmltrusted

- fmc.gov/wp-content/uploads/2019/04/vol01small.pdftrusted

- govinfo.gov/content/pkg/CHRG-109hhrg31362/html/CHRG-109h...trusted

- hammer.purdue.edu/ndownloader/files/52420811trusted

- irle.ucla.edu/old/publications/documents/Informalworkerorg...trusted

- irs.gov/irm/part3/irm_03-012-251rtrusted

- justice.gov/opcl/docs/rec-com-rights.pdftrusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.

How to Respond to a Subpoena for Business Records

Move fast, but do not produce records on instinct. If you need to **respond to a subpoena for business records**, your immediate job is to control deadlines, preserve records, and make any later production defensible.

A US Expat's Guide to Investing in UCITS ETFs to Avoid PFIC Issues

The real problem is a two-system conflict. U.S. tax treatment can punish the wrong fund choice, while local product-access constraints can block the funds you want to buy in the first place. For **us expat ucits etfs**, the practical question is not "Which product is best?" It is "What can I access, report, and keep doing every year without guessing?" Use this four-part filter before any trade: