Quick Answer

Start by locking your legal and operating controls before you recruit: define IP transfer terms, cap liability in a defensible way, require signed scope changes, and document a reserve policy tied to your real cost exposure. In this agency scaling blueprint, you then systematize delivery with SOPs and a shared knowledge base, and only then add cross-border contractors through role-based vetting, access controls, and payment documentation.

Scale after you harden what already works. Before you write a job description, lock down the parts of the business that usually break first under growth: contracts, cash, worker status, delivery documentation, and how work gets reviewed. This blueprint is about adding capacity without adding avoidable risk.

Phase 1: Fortify Your Foundation (De-Risk Before You Scale)#

Before you hire anyone, reduce the three risks that can sink a growing practice quickly: legal exposure, cash strain, and worker classification mistakes. If any one of those is still loose, pause the hiring plan and fix it now.

Growth turns small ambiguities into expensive facts. A vague IP clause becomes an ownership dispute. Thin reserves turn one late client payment into a payroll problem. A casual contractor setup can trigger tax, labor, or permanent-establishment questions once you cross borders.

Tighten the contract before you add people#

Your client agreement is the first control to fix because vague paper gets more expensive once more people touch the work. At a minimum, it should answer three practical questions: when IP transfers, how liability is capped, and how scope changes get approved.

| Contract point | What to define | Article note |

|---|---|---|

| IP transfer | State exactly when IP transfers | In both the U.S. and UK, copyright assignment generally needs a signed writing to be effective; say whether ownership transfers only after final payment, on milestone payment, or on another named trigger. |

| Liability cap | Cap liability in a structure you can defend | A cap tied to fees paid for the specific project can be one contract design, but some regimes restrict exclusions; in the UK, you cannot exclude liability for death or personal injury resulting from negligence. |

| Scope changes | Make scope changes bilateral and signed | Use a written change order that updates scope, price, and timeline, signed by both sides. |

- State exactly when IP transfers. Do not rely on implication. In both the U.S. and UK, copyright assignment generally needs a signed writing to be effective. Your clause should say whether ownership transfers only after final payment, on milestone payment, or on another named trigger. Verify that your signed contract, SOW, or separate assignment actually satisfies the formality in your jurisdiction.

- Cap liability in a structure you can defend. A cap tied to fees paid for the specific project can be one contract design, but it is not universally valid in every form. Some regimes allow parties to limit damages by agreement, while others restrict exclusions for certain losses. In the UK, for example, you cannot exclude liability for death or personal injury resulting from negligence.

- Make scope changes bilateral and signed. Each SOW should describe deliverables, timing, dependencies, and acceptance criteria in clear, objective, measurable terms. If the client asks for more, route it through a written change order that updates scope, price, and timeline, signed by both sides. The common failure mode is familiar: teams start "just one extra thing" work, then lose margin and evidence when a dispute follows.

Use this quick checkpoint. Open your current MSA and latest SOW. Confirm you can answer, in one minute, "Who owns draft work, when does final IP transfer, what is the liability cap, and how is extra work approved?" If that answer is fuzzy, have counsel review the document set before you scale.

Set a reserve target and pick a cash method you will actually keep running#

Do not treat a six-month reserve as a universal rule. Set your runway target from your actual exposure: fixed monthly business costs, contractor commitments you are about to add, client concentration risk, and payment timing. If one client represents a large share of revenue, or your sales cycle is lumpy, your target should be higher. If you have stable retainers and low fixed burn, it may be lower.

Park that reserve somewhere boring and liquid. FDIC deposit insurance covers deposits up to $250,000 per depositor, per ownership category, per insured bank. That matters if your reserve is material. Also remember that money market funds are mutual funds, not insured bank deposits. If you cannot meet your own documented reserve condition yet, pause hiring.

| Approach | Best fit | Operating discipline required | Common failure mode |

|---|---|---|---|

| Percentage buckets | Early stage owner who needs simple guardrails | Move each receipt into named accounts consistently | Percentages stop matching reality as margins or tax exposure change |

| Rolling forecast | Variable revenue, larger projects, uneven collections | Weekly cash review and forward visibility | Forecast gets stale and decisions keep using old assumptions |

| Hybrid | Owner wants both habit and forward visibility | Bucket rules plus recurring forecast updates | You maintain the buckets but ignore the forecast warnings |

Screen contractor risk as a cross-border question, not a label#

Once your cash position can absorb a miss, review the people model. A signed contractor agreement does not settle status, especially when the work crosses borders.

| Review factor | What to ask | Article note |

|---|---|---|

| Control | Do you control how the work is done? | Control is one of the four tests that show up in many approaches. |

| Integration | Is the person woven into your business like staff? | Integration is one of the four tests that show up in many approaches. |

| Economic dependence | Do they depend on you economically? | Economic dependence is one of the four tests that show up in many approaches. |

| Permanence | Does the relationship look indefinite rather than project based? | Permanence is one of the four tests that show up in many approaches. |

| Tax presence | Could this arrangement create tax presence? | Check fixed-place or dependent-agent permanent establishment, or U.S. Effectively Connected Income issues if facts point to a U.S. trade or business. |

| Local labor-law triggers | Are there local labor-law triggers, registration duties, or legal presumptions of employment? | For country cutoffs, verify the current threshold before you rely on it. |

Review the whole relationship using four tests that show up in many approaches: control, integration, economic dependence, and permanence. Ask whether you control how the work is done, whether the person is woven into your business like staff, whether they depend on you economically, and whether the relationship looks indefinite rather than project based.

U.S. federal analysis is in transition in 2026. On February 26, 2026, the Department of Labor announced that it is proposing to rescind the 2024 approach it says it is no longer applying in investigations. A separate DOL page still lists the 2024 final rule as effective March 11, 2024. Treat that as a live-change area, not settled ground.

For cross-border hires, add two more checks. First, could this arrangement create tax presence, including a fixed-place or dependent-agent permanent establishment, or U.S. Effectively Connected Income issues if facts point to a U.S. trade or business? Second, are there local labor-law triggers, registration duties, or legal presumptions of employment where direction and control facts exist? For country cutoffs, verify the current threshold before you rely on it.

Your pre-hiring gate is simple. Contracts updated and signed. Reserve policy documented. Cash method running for at least one full cycle. Classification review completed with a short written memo for each role. If one of those is missing, you are not ready for Phase 2.

If you want a deeper dive on classification, read What to Do If You've Been Misclassified as an Independent Contractor.

Phase 2: Systematize for Leverage (Build Your "Operations OS")#

After your legal and financial base is stable, leverage comes from consistency. If work quality still depends on you personally in every step, adding people adds complexity faster than capacity. Build an operations system that lets others execute your standard clearly.

Create Your Minimum Viable SOPs (Standard Operating Procedures)#

Start with the recurring workflows your business depends on right now. The goal is handoff, not perfect documentation.

Before hiring, write clear step-by-step SOPs for:

- Client onboarding

- Project kickoff

- Final deliverable handoff

For each SOP, define:

- Inputs needed

- Step order

- Owner for each step

- Completion standard

This gives contractors a usable path for execution and reduces avoidable back-and-forth.

Productize Your Core Service Offering#

If every engagement starts from scratch, your system resets every time. Define a repeatable offer structure so sales, scope, and delivery begin from a known baseline.

| Custom model | Productized model |

|---|---|

| New scope each time | Predefined offer structure |

| Delivery plan rebuilt per project | Repeatable delivery pattern |

| Review standards vary by engagement | Shared review criteria |

Productizing does not mean identical client work. It means your operating model is defined enough to run consistently.

Choose a Lean, Integrated Tech Stack#

Keep your stack lean so your team knows where the source of truth lives. Cover the essentials with one primary system per function:

- Project execution

- Team communication

- Finance operations

Then standardize usage rules across the team. Consistency in tool use matters more than adding more apps.

Build a Knowledge Base, Not Just a Task List#

A task list tells people what is next. A knowledge base shows how to make decisions when edge cases appear.

Store your SOPs and operating references in one maintained location, including:

- Core SOPs

- Client communication templates

- Brand and voice guidance

- Examples of acceptable output quality

When people can resolve common questions from the system instead of routing everything through you, your operations model is doing its job. For a related walkthrough, read The Solo Agency Blueprint for Productized Services and Subcontractor Control.

Phase 3: Scale with Control (Leverage a Global Team)#

Use a contractor-first model only when the work is genuinely independent and output-based. If you need fixed hours, close day-to-day supervision, or a role that is embedded in your core delivery long term, move earlier to an employer intermediary or direct employee path.

Control without micromanagement means your Operations OS does the controlling: clear outcomes, SOPs, quality standards, review checkpoints, and evidence of completion are defined before work starts. If you cannot define the role that way, the bottleneck is role design, not hiring.

Choose the engagement model that matches the work#

Choose based on how the work is performed, not the label in the contract. If the role requires independence and project-based deliverables, a contractor can fit; if it requires tighter supervision, fixed schedules, or long-term integration, reassess before classifying the role as contractor.

If you are U.S.-based, use IRS control/independence evidence as the baseline check across behavioral control, financial control, and relationship factors. Also date-stamp your policy notes: DOL's worker-status framework changed in 2024 and has a proposed update announced on February 26, 2026.

| Model | Compliance burden | Flexibility | Control level | Admin overhead |

|---|---|---|---|---|

| Independent contractor | Lower payroll-tax handling, but classification risk remains with you | High | Lower day-to-day control | Low to medium |

| Employer intermediary (for example EOR, or in some U.S. cases CPEO/PEO-style) | Medium; provider may handle some withholding/reporting/payment functions, but responsibility split must be verified | Medium | Medium to high | Medium |

| Direct employee | Highest; employer withholding/payment obligations generally apply | Lower | Highest | Highest |

Vet with a scorecard, not gut feel#

Use the same scorecard each time and require evidence in four categories before you assign client work:

- Capability evidence: two relevant samples, what they personally owned, and one paid test task with a scope limit verified against contract records, HR policy, or approved operating rules before use.

- Communication reliability: response quality, deadline consistency, and whether they clarify before executing.

- Process fit: willingness to follow SOPs, naming standards, approval steps, and review gates.

- Risk flags: portfolio inconsistencies, refusal to sign core terms, pressure to skip documentation, or early requests for broad access.

A technically strong specialist who will not follow your delivery method can still harm margins and client trust.

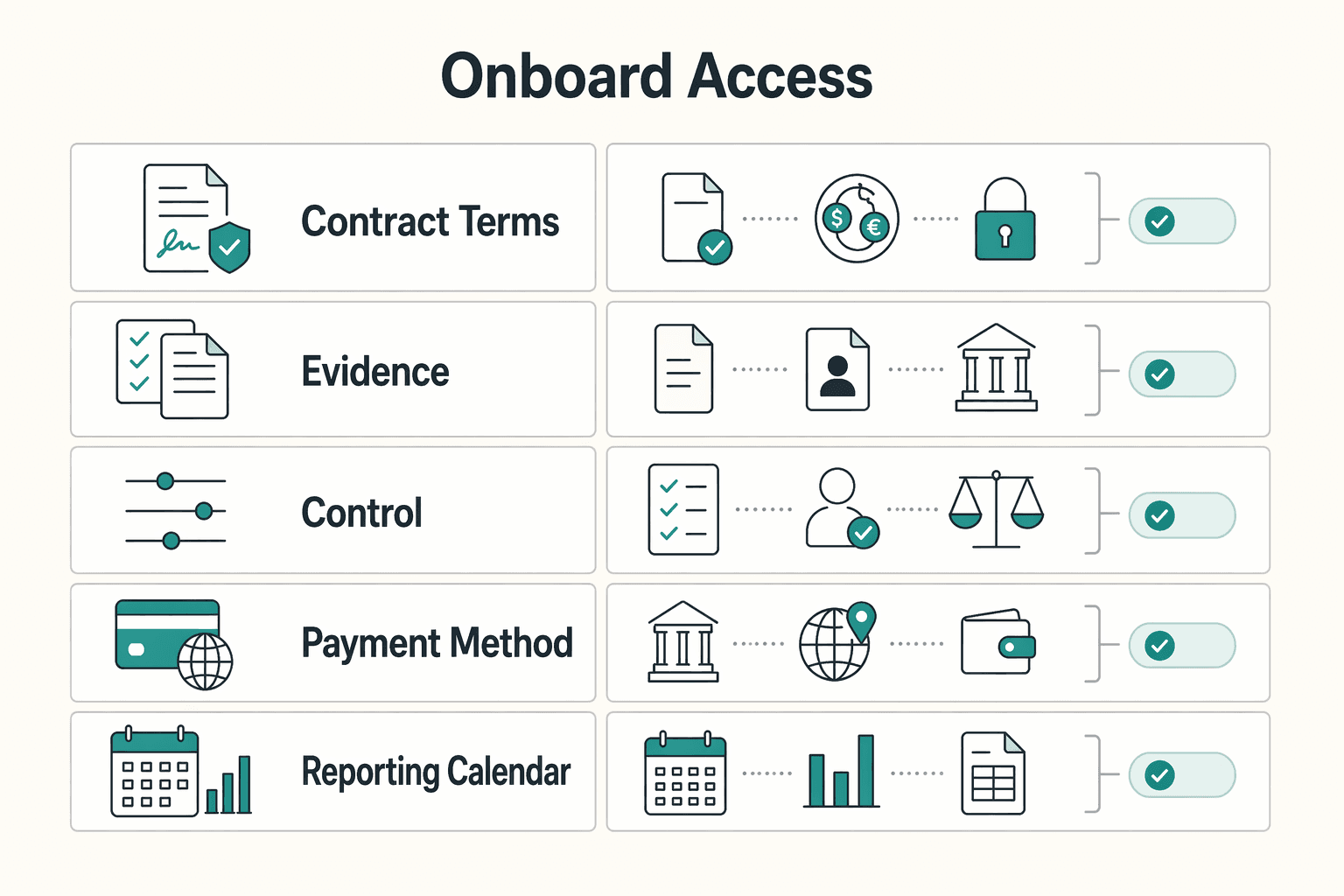

Onboard access, standards, and payments like a real operator#

Treat onboarding as an operational control point. Before first delivery, complete this checklist:

| Workflow step | What to confirm | Article note |

|---|---|---|

| Contract terms | Signed scope, deliverables, payment terms, and currency terms before work starts | Run a documented compliance workflow every time. |

| Tax documentation | Collect required forms before payment | For U.S. contexts, W-9 for U.S. payees; W-8BEN for foreign individuals where applicable. |

| Invoice controls | Match invoice to contract terms, approved deliverables, and reviewer sign-off | Use approved deliverables and reviewer sign-off before payment. |

| Payment method and FX decision | Choose by corridor and transaction needs, not habit | Cross-border costs and speed vary by route, intermediaries, and payment method. |

| Reporting calendar | Track applicable filing deadlines | For U.S. contexts, 1099-NEC by January 31; 1042/1042-S/1042-T by March 15 where required. |

| Jurisdiction checks | Exact country-specific withholding, registration, and labor requirements verified from source records | Verify country requirements against counsel/adviser records, official source records, or approved operating rules before use. |

| Record retention | Keep a clear audit trail of contract, forms, approvals, payment confirmations, and method/FX decisions | For OFAC-regulated scope, keep records examinable for at least 10 years. |

- Tool access: grant only role-required access (least privilege), with elevated permissions only after proven need.

- Security baseline: require MFA for sensitive systems and include security literacy in onboarding.

- SOP orientation: confirm they can execute your onboarding, kickoff, and handoff SOPs.

- Communication norms: define channels, update cadence, escalation path, and response expectations.

- Quality standards: define acceptance criteria, revision boundaries, and approval authority.

- Confidentiality and data handling: confirm signed terms and practical handling rules before production access.

- Review checkpoints: run a probation-style review after first assignment and again before expanding scope or permissions.

For cross-border payments, run that compliance workflow every time. The essentials are already in the checklist above: signed scope and currency terms before work starts, required tax forms before payment, invoice matching and reviewer sign-off, route-level payment and FX decisions, a reporting calendar, country checks after local verification, and a clear audit trail.

Do not assume one rail is always cheapest or fastest. Cross-border costs and speed vary by route, intermediaries, and payment method, so you need route-level decisions, not one default setting.

For more on the first hire process, see Hiring a Subcontractor for the First Time Without Costly Surprises.

Conclusion: Scale Your Resilience, Not Just Your Headcount#

Do not scale just because demand is there. Scale when your business can absorb mistakes, keep delivery stable, and maintain records you can explain under review. Growth can magnify mistakes and produce uneven outcomes, so your blueprint should be a coordination tool, not a guarantee.

By this point, you should have three things in place:

- Phase 1: baseline risk controls you can point to, including signed terms, cleaner records, and a habit of checking legal and tax exposure before adding complexity.

- Phase 2: a repeatable operating setup for delivery, with defined outputs, standards, checkpoints, and evidence of completion so work does not depend on your live intervention.

- Phase 3: capacity you can add without losing control, including clear engagement models, least-privilege access for sensitive systems, and required payment/tax documentation where applicable.

Before you hire the next person, run one hard checkpoint on yourself. Can you describe the role's output, review method, and access level in writing? Can you tie each invoice to the contract, approved deliverable, currency, FX approach, and payment date? If the role requires close day-to-day supervision, reassess whether your current engagement model still fits.

Your next move is simple: tighten the gaps you just found, then scale one role at a time. Keep your calendar aligned to filing and reporting obligations in the jurisdictions you operate in, and confirm deadlines with qualified advisors. If your next challenge is day-to-day contractor management, read How to Manage a Global Team of Freelancers. Turn that into your next onboarding and review checklist.

For a step-by-step walkthrough, see The US Solopreneur's First-Year Blueprint: From Wyoming LLC Formation to Filing Your First Expat Tax Return.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 2 external sources outside the trusted-domain allowlist.

- fdic.gov/resources/deposit-insurance/understanding-de...trusted

- irs.gov/businesses/small-businesses-self-employed/in...trusted

- irs.gov/individuals/international-taxpayers/effectiv...trusted

- gurkhatech.com/the-agency-scaling-blueprint-a-systematic-mo...external

- gurkhatech.com/the-agency-scaling-blueprint-a-systematic-mo...external

Educational content only. Not legal, tax, or financial advice.

Related Posts

What to Do If You've Been Misclassified as an Independent Contractor

Treat this as a protection problem first, not a label debate. If your work was treated as an independent contractor arrangement even though the relationship functioned differently, your first goal is to protect pay, rights, and records while you choose the least risky escalation path. You can do that without making accusations on day one, which often keeps communication open while you document what happened.

How to Manage a Global Freelance Team Without Compliance Gaps

If you want to manage a global freelance team without constant cleanup, use the same intake-to-payout process for every engagement and save an artifact at each gate. Common failure points are instinct-based classification, vague scope, and payments approved in chat with no audit trail.

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.