Quick Answer

Yes - use real-time adverse media monitoring only when each hit lands in a named case and a payout decision. The article sets a three-way disposition rule: clear, escalate, or hold pending review. It also requires proof before purchase, including entity-match handling, duplicate suppression, and exportable case records. Monthly reconciliation should confirm the case outcome matches the actual payout state.

Why Adverse Media Screening Matters for Real-Time Contractor Payments#

Adverse media screening belongs in a contractor payout stack only if it helps you make or stop a payment decision fast enough to matter. If alerts pile up without a clear owner, you do not have better control. You have a larger audit problem.

- Treat it as a decision input, not a news feed.

Adverse media screening means identifying negative information early from public sources such as news, social media, and court records. In practice, that matters because bad news tied to a contractor or counterparty can expose your platform to fraudulent transactions, money laundering, and account takeover risk. The useful test is operational: if an alert cannot be tied to a named person or business, a current review case, and a payout state, it should not sit in an undifferentiated queue.

- Use it inside AML controls, not beside them.

Negative news screening belongs inside a broader AML framework. For compliance, legal, finance, and risk owners handling cross-border contractor, seller, or creator payouts, the practical question is simple: what changes when a credible alert appears? A workable checkpoint is to require every alert disposition to end in one of three actions: clear, escalate, or hold pending review. If your team cannot say who is allowed to release or block funds after review, tooling is not your first problem.

- Assume monitoring is incomplete and design around that fact.

No team can read every news source in every language across the world, and screening tools still operate within that basic constraint. That is why a risk-based approach matters more than broad claims about coverage. Higher-risk relationships may need closer ongoing review, while lower-risk ones can be revisited periodically. What matters is not more data. It is whether the signal is relevant enough to justify human review before the next payout cycle.

- Plan for overload, false positives, and evidence from day one.

The failure modes are familiar: data overload, false positives, and unresolved cases that drift without a decision. In practice, this can include name-matching issues, duplicate alerts, and weak articles that mention a similar entity but not your contractor. Build the process so analysts verify the entity match first, then assess whether the news changes risk, then record why the case was cleared or escalated. That evidence trail matters later when you review AML decisions, explain payout holds, or defend why a noisy alert did not justify action.

This guide is written for teams working under those constraints. The aim is not to overbuild. It is to help you choose a tool and review approach that reduce financial-crime, reputational, and regulatory-compliance risk without slowing onboarding and payments more than the risk warrants.

Related: FedNow vs. RTP: What Real-Time Payment Rails Mean for Gig Platforms and Contractor Payouts.

Who this list is for and how to choose a platform#

Use this list if you need ongoing name screening after onboarding and must tie alerts to CDD/AML decisions before payouts move. If you only need a one-time onboarding check, a lighter setup is usually enough.

| Selection point | Grounded guidance | What to verify |

|---|---|---|

| Existing relationships | Use this list when screening continues after onboarding and alerts must tie to CDD/AML decisions before payouts move | Tool can re-screen approved contractors, connect new hits to the existing case, and retain disposition evidence |

| Workflow fit | Prioritize one review flow for compliance, legal, and payments ops over broad monitoring claims | Team can answer: is this the same person or business, does the information change risk, and what action follows |

| Directory evidence | Treat rankings and directories as inputs, not proof | Request a sample alert pack, a case export with disposition fields, and a live walkthrough of false-match handling and audit trail ownership |

| Governance | Set hold/release authority before selecting tooling | Name who can place an AML hold, who can release it, and when legal must be involved |

- Use this list when screening continues for existing relationships

Name screening is commonly used against sanctions, PEP, terrorist, adverse-media, and other watchlists, including national, regional, and international lists. The key buying test is practical: can the tool re-screen approved contractors, connect new hits to the existing case, and retain clear disposition evidence over time.

- Prioritize AML/CDD workflow fit over broad monitoring claims

The right tool should help compliance, legal, and payments ops work in one review flow, not just surface articles. You should be able to answer three questions quickly: is this the same person or business, does the information change risk, and what action follows (continue, pause, or escalate).

- Treat rankings and directories as inputs, not proof

Longlists are useful, but they are not procurement evidence on their own. For example, one AML directory view shows 169 results and also discloses referral-fee and sponsored-placement mechanics; a 2025 category mention in a press release can signal market visibility, but not implementation fit. Before you sign off, ask for a sample alert pack, a case export with disposition fields, and a live walkthrough of false-match handling and audit trail ownership.

- Set hold/release authority before selecting tooling

If you cannot name who can place an AML hold, who can release it, and when legal must be involved, fix governance first. Tooling will expose that gap faster, but it will not close it.

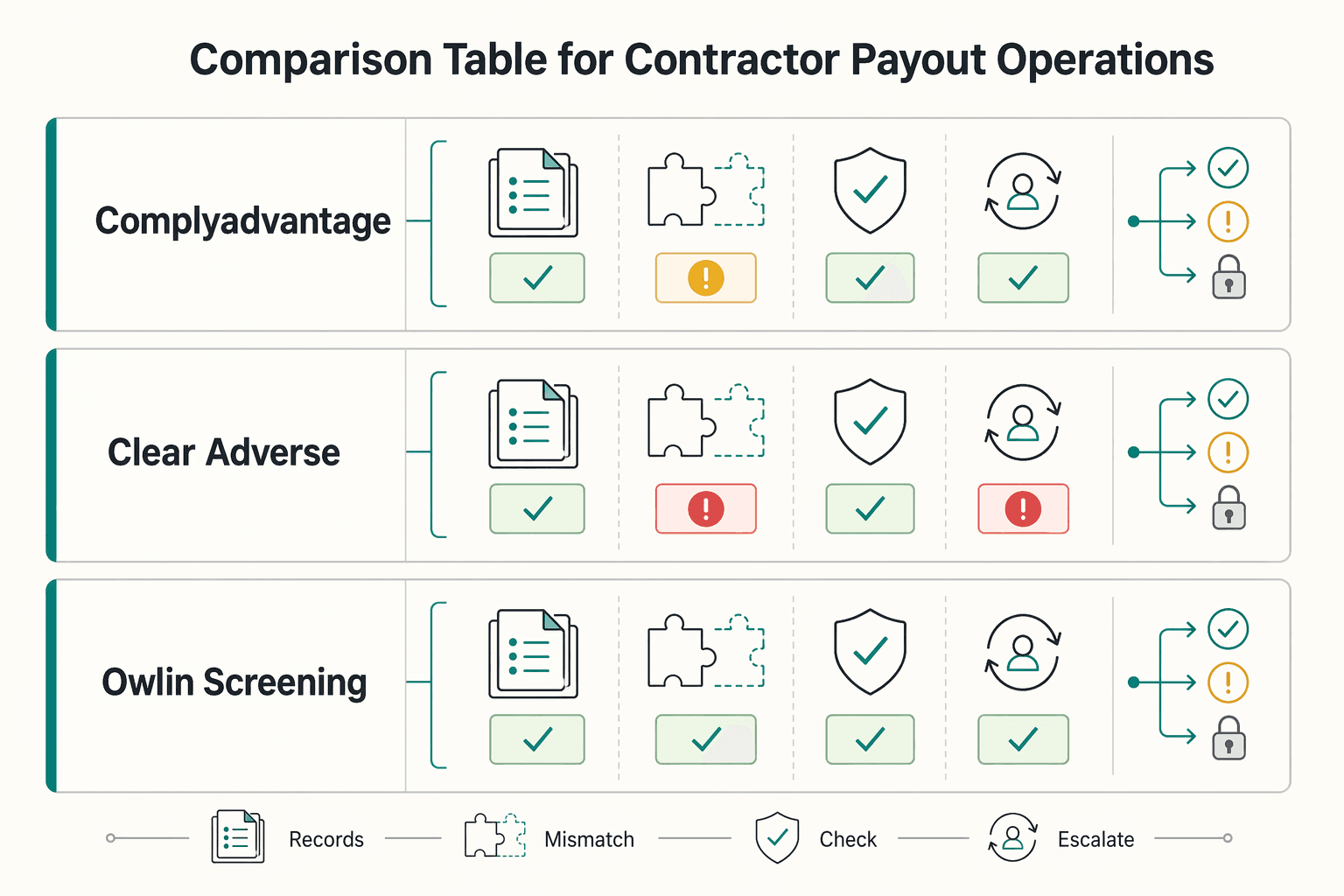

Comparison table for contractor payout operations#

Use this comparison as an evidence checklist, not a product ranking: if a vendor cannot show ongoing monitoring tied to case history and payout decisions, do not sign yet.

Due diligence does not stop at contract signature, and ongoing monitoring remains essential as risk factors change. For payout operations, that means you need proof that adverse media alerts can be reviewed in the same control flow as sanctions and PEP checks, not treated as a separate article feed.

| Vendor | What is supported from supplied material | Ongoing monitoring intent | Onboarding support | Negative-news context depth | Sanctions adjacency score* | PEP adjacency score* | Proof required before sign-off |

|---|---|---|---|---|---|---|---|

| ComplyAdvantage | AML context is supported; product mechanics are not verified here | Not verified | Not verified | Not verified | 0/3 | 0/3 | Demo one contractor from onboarding through re-screening, then export a case with linked adverse media, sanctions context, and disposition fields. |

| CLEAR Adverse Media | Product naming supports adverse-media use case; operational depth is not verified here | Not verified | Not verified | Not verified | 0/3 | 0/3 | Show a live alert pack with entity-match evidence, source context, and whether sanctions/PEP review is handled in one analyst path. |

| Owlin Screening | Screening use case is suggested; product detail is not verified here | Not verified | Not verified | Not verified | 0/3 | 0/3 | Show ongoing alert generation, duplicate suppression, analyst dispositions, and a full case path from hit to clear or escalate. |

*Scores are evidence-based, not quality ratings: 0 = no verified adjacency evidence in supplied material, 1 = adjacency claimed, 2 = shared case handling demonstrated, 3 = demo + export + audit evidence shown.

Before procurement sign-off, close these unknowns explicitly:

- Matching logic: how true matches are distinguished from common-name false matches, including aliases and business identifiers where available.

- API depth: whether you can create and update cases, re-screen existing contractors, and pull dispositions with stable case IDs.

- SLA: written expectations for alert delivery and support response timing.

- Language coverage: evidence in the languages used across your payout corridors.

- False-positive controls: duplicate suppression and common-name stress-test results.

Also require a clear PEP demonstration in case context, including foreign, domestic, and international organization categories. If that adjacency is missing, treat it as a third-party due diligence blocker.

This pairs well with our guide on Vendor Approval Process for Platforms That Screen and Onboard Contractors.

ComplyAdvantage as best for AML-centered due diligence teams#

ComplyAdvantage can be a strong fit if your buying criteria start with AML policy alignment. From the material here, its clearest advantage is that adverse media is framed as part of customer due diligence (CDD), alongside sanctions screening and politically exposed person (PEP) screening, rather than as a standalone news feed.

That matters if your team needs one review logic across onboarding and ongoing monitoring. In ComplyAdvantage's 2026 buyer-guide excerpt, adverse media is described as an essential part of CDD procedures and as a way to surface links to money laundering, terrorist financing, and predicate offenses like drug trafficking and organized crime. The practical value is not just that news exists. It is that adverse media may show risk information that is not yet reflected in official sources.

A practical shortlisting case is when your team wants policy consistency across onboarding CDD, sanctions checks, PEP review, and ongoing risk monitoring. If your compliance team already writes decisions in AML terms, this framing can fit better than treating adverse media as a separate monitoring stream. The supplied material also reinforces a useful procurement lens: breadth, depth, and timeliness of AML data are critical evaluation points. That is the right standard to apply when monitoring continues after onboarding approval.

The limitation is just as important. The excerpts do not confirm contractor-specific triage design, alert precision, false-positive rates, SLA terms, API depth, or payout-control metrics. So this is a conditional recommendation: shortlist ComplyAdvantage for AML-centered due diligence, but do not treat policy fit as proof that it will work cleanly for contractor queues.

Before you sign off, ask ComplyAdvantage to prove four things in one live review path:

- Show an adverse-media hit linked to the same case context as sanctions screening and PEP screening, not as separate disconnected searches.

- Provide a sample evidence pack with case ID, analyst disposition, timestamps, attached source material, and the linked CDD record.

- Demonstrate re-screening of an already approved contractor or counterparty, because onboarding-only checks will not support ongoing AML monitoring.

- Explain how analysts verify an entity match when official sources are still silent, since emerging adverse media is useful only if your team can defend why it was linked to the right person or business.

A real red flag is any demo that stays at the article level and never reaches a documented decision. If the vendor can describe money laundering, terrorist financing, and predicate-offense risk but cannot show how analysts would clear, escalate, or retain that decision inside a case history, you still have a monitoring gap. If your goal is ongoing adverse-media monitoring inside an AML program, that gap matters more than brand fit.

Related reading: How Gig Platforms Report 1099s for Thousands of Contractors at Year-End.

CLEAR Adverse Media as best for legal and investigation-heavy environments#

CLEAR Adverse Media can be a fit when your legal or investigations team already works in Thomson Reuters. In that setup, negative news screening can feed case escalation rather than just add compliance queue volume. That is narrower than an AML-first approach. Here, the draw is product positioning and operating context: Thomson Reuters presents CLEAR Adverse Media explicitly as a "Negative News Screening Solution," which may align better with counsel-led review of risky individuals and businesses than with contractor-payout automation on its own.

The upside is straightforward. Thomson Reuters' adverse media overview says customer news can expose an organization to fraudulent transactions, money laundering, and account takeover. It also highlights the basic monitoring problem of trying to "read every news source in every language across the world." If your risk posture depends on spotting issues before releasing a sensitive payout, that framing is useful. It supports a legal-led escalation path where a media hit triggers deeper review, source validation, and a documented release or hold decision.

The limit is just as clear in the material we have. We do not have proof here of contractor-specific controls, payout gating logic, sanctions or PEP adjacency, false-positive handling, or any SLA. So you should treat CLEAR as a shortlist candidate for investigation-heavy teams, not as confirmed payment-ops infrastructure.

Before you sign off, ask Thomson Reuters to prove three things in one case review:

- Show how a hit is attached to a person or business record, with enough source detail for legal to defend the match.

- Export an evidence pack with article links, timestamps, analyst notes, and final disposition.

- Demonstrate what happens between alert and payout release, because the biggest failure mode is a credible news hit that never becomes an auditable decision.

If your lawyers own escalation authority, CLEAR Adverse Media may fit neatly. If payout operations need precise queue controls, you still need more proof.

For a step-by-step walkthrough, see OFAC, PEP, and Adverse Media Screening Decisions for Payment Platforms.

Owlin Screening as best for real-time alerting in high-volume onboarding#

Owlin Screening can be a strong fit when your priority is real-time adverse media alerting during onboarding and ongoing monitoring after activation. In the available material, Owlin frames this as continuous coverage rather than one-time checks, which suits high-volume queues where manual article-by-article review is not practical.

The core strength is clear: Owlin says its screening scans thousands of credible news sources, adds context to internal alerts, and provides real-time updates on clients and counterparties. It also describes monitoring as continuous, with a 24/7 posture aimed at surfacing red flags early. That is the right profile when risk can change between initial approval and later payouts.

For a fast-growing creator platform, this matters because static onboarding records such as credit ratings or official filings can provide background context but may miss newly emerging issues. Owlin explicitly contrasts live news monitoring with static onboarding data, which is useful when your operational risk is late discovery.

The same constraint applies here. The material does not verify sanctions integration details, PEP workflow integration, measurable false-positive rates, or contractor payout-specific case metrics. If your policy requires one connected decision path across adverse media, sanctions, and PEP controls, treat Owlin as an alerting candidate and validate the missing controls in procurement.

Before approval, ask for a live demo that proves:

- The alert record includes source link, publication time, matched entity fields, and enough context for analyst triage.

- A cleared onboarding record is moved into ongoing monitoring and can trigger new alerts later.

- The review output can be retained as an evidence pack with article references, timestamps, reviewer notes, and final disposition.

Owlin says it supports over 1000 companies worldwide, which indicates adoption, but adoption alone does not prove match quality in your queue. If your bottleneck is triage speed, shortlist it. If your bottleneck is control completeness, keep pressure on end-to-end proof.

Decision rules for triage, payout holds, and escalation#

Treat adverse media as a decision input, not an automatic payout verdict. Escalate immediately for clear financial-crime signals, but keep ambiguous alerts within KYC/KYB review until the match is verified and the decision is documented.

| Review step | Required action | Record |

|---|---|---|

| Validate match | Confirm the alert is tied to your contractor, seller, or counterparty using policy-approved identifiers and check for duplicate internal profiles | Matched fields, source link, and enough context for a second reviewer |

| Classify risk | Assess AML relevance, not headline intensity | Why the signal was treated as material or as weak, old, thin, or ambiguous |

| Choose action | Release with rationale, gate pending KYC/KYB remediation, or escalate for AML review and possible hold | Disposition and escalation owner |

| Log evidence | Keep the alert reference, publication time/date shown, matched identity fields, analyst notes, and disposition in one linked record | Linked due-diligence file |

| Set re-review | Set a re-review date and add recurring checks for duplicate alerts, stale unresolved cases, and missing disposition notes | Re-review date and queue-quality checks |

This control discipline reduces errors in both directions. Fragmented data can create multiple truncated representations of the same client, which increases the risk of wrong-person holds, duplicate cases, and missed connections.

- Validate the entity match first.

Before you react to an article, confirm the alert is actually tied to your contractor, seller, or counterparty using your policy-approved identifiers, and check for duplicate internal profiles that may be replaying the same story as separate hits.

The case file should clearly show matched fields, the source link, and enough context for a second reviewer to follow the same conclusion.

- Classify by AML relevance, not headline intensity.

If reporting indicates potential money laundering, terrorist financing, or closely related financial-crime exposure, escalate to compliance/legal at once and apply a hold only where your AML policy allows it.

If signals are weak, old, thin, or ambiguous, keep payouts gated through KYC/KYB review instead of blanket blocking, and record why you cleared or escalated.

- Use a fixed order of operations.

Run every case in this order: intake alert, validate match, classify risk, choose action, log evidence, set re-review date.

Keep action outcomes consistent: release with rationale, gate pending KYC/KYB remediation, or escalate for AML review and possible hold.

- Close only with a complete evidence record.

A "cleared" label without reasoning is still an audit risk. Keep the alert reference, publication time/date shown, matched identity fields, analyst notes, escalation owner (if any), disposition, and re-review date in one record linked to due-diligence files.

Add recurring checks for duplicate alerts, stale unresolved cases, and missing disposition notes so unresolved queue quality issues do not accumulate into audit risk.

Reporting checklist your team can run every month#

Your monthly report should let any reviewer trace a single path from alert to case to payout state without reassembling evidence across systems.

| Monthly check | What to include | Exceptions or notes |

|---|---|---|

| Evidence pack | Alert log, disposition rationale, linked CDD/AML case IDs, final payout decision, source link, matched identity fields, reviewer notes, and hold/release outcome | Keep one report view |

| Control check | Review both cleared and escalated alerts | Flag records cleared without rationale and holds in compliance notes not linked to the payout record |

| Tax and identity links | Track related contractor records and where they are stored, including W-8, W-9, FBAR, and 1099 artifacts when relevant | Visibility control, not a tax determination based on a news alert |

| FBAR workpapers | Use FinCEN Form 114 precisely; record maximum account values in U.S. dollars, rounded up to the next whole dollar, and value each account separately | Errors in a previously filed FBAR require an amended report |

| Payout reconciliation | Confirm case decisions and payout states match | AML hold should not be released; release with rationale should not remain blocked |

| Explicit exceptions | Surface mismatches between case decisions and payout states | Hold decisions with paid status, released cases still blocked, and missing links between the adverse-media case and transaction records |

- Minimum evidence pack

Keep one report view that includes the alert log, disposition rationale, linked CDD/AML case IDs, and final payout decision. Each record should show the source link, matched identity fields, reviewer notes, and hold/release outcome in the same place.

Run a quick control check on both cleared and escalated alerts. Flag records where a case is marked cleared without rationale, or where a hold appears in compliance notes but is not linked to the payout record.

- Tax and identity cross-links

Track whether related contractor records exist and where they are stored, including W-8, W-9, FBAR, and 1099 artifacts when relevant to your operating model. This is a visibility control, not a tax determination based on a news alert.

If you keep FBAR workpapers, use FBAR rules precisely: FinCEN Form 114 is the Report of Foreign Bank and Financial Accounts, maximum account values are recorded in U.S. dollars and rounded up to the next whole dollar, each account is valued separately, and errors in a previously filed FBAR require an amended report.

- Reconcile policy actions to payout states

Reconciliation should confirm that case decisions and payout states match. If a case is marked AML hold, payouts should not be released; if it is marked release with rationale, it should not remain blocked in an exception queue.

Surface mismatches as explicit exceptions: hold decisions with paid status, released cases still blocked, and missing links between the adverse-media case and transaction records.

Need the full breakdown? Read Gig Worker Tax Compliance at Scale: How Platforms Handle 1099s W-8s and DAC7 for 50000+ Contractors.

Conclusion#

Do not buy the loudest monitoring product and hope it sorts itself out later. The better outcome comes from choosing a tool that fits your contractor payout risk model, then making alert triage, escalation, and payout authority explicit before rollout. That matters even more if you already treat sanctions and PEP screening as part of the same risk-review process as negative news, rather than a separate queue.

- Pick for payout risk fit, not feature claims.

Adverse media screening is useful because it can surface hidden or emerging risk that may not appear on sanctions or PEP lists, and it adds context from negative news, public records, and other open-source information. What matters is whether that context can actually change a contractor decision in time. If your team cannot say which alerts should trigger escalation, deeper due diligence review, or simple closure, the issue is not tooling first. It is control design first.

- Test the whole AML stack together.

Start with the controls you already know you need for your program: due diligence, AML/KYC, sanctions screening, and PEP screening. Then evaluate each vendor on the evidence a reviewer will need to defend a decision, not on marketing promises alone. A practical checkpoint is simple: can your team review the underlying negative news or public-record item, assess whether it truly matches the contractor or business, and record why the case was escalated or cleared? Adverse media helps most when it supports prioritization and faster compliance decisions, not when it creates a second pile of unmanaged alerts.

- Treat unknowns and noise as procurement blockers.

False positives are not a small nuisance. They are a direct analyst-capacity problem, and traditional screening approaches can surface large volumes of irrelevant results that consume review time. With financial crime compliance costs cited at $56.7 billion for the U.S. and Canada in one industry source, wasted review effort is not abstract. What matters is proof. If

Frequently Asked Questions

What is adverse media screening for contractor platforms, and how is it different from basic onboarding checks?

Adverse media, also called negative news, is part of customer due diligence (CDD) and scans official and unofficial news sources plus other public data for risk linked to a business or counterparty. Basic onboarding checks are usually a point-in-time gate, while adverse media adds outside context that can change your risk view after the file is opened. The practical difference is that this control is only useful if the alert can be tied back to the right contractor record and review decision.

Is onboarding-only screening enough, or do we need ongoing monitoring after payout activation?

Onboarding-only checks are usually too thin if your exposure continues after activation. The grounded term that matters here is perpetual KYC: adverse media can support enhanced due diligence and ongoing third-party risk monitoring after a vendor or contractor is onboarded. A simple rule is this: if the relationship stays active, keep watching for new risk signals, because a small report can grow into a much larger issue months later.

What should trigger escalation versus simple alert closure in an AML program?

Escalate when the article appears to match the contractor or business you are reviewing and the content points to material risk such as fraud, money laundering, or account takeover exposure. Close the alert when review shows the item is irrelevant or duplicative, but log the rationale and source link so the decision is reviewable later. The common failure mode is noise: without precise filtering, teams spend time sorting irrelevant alerts and miss the few that deserve deeper review.

Who should own alert decisions across compliance, legal, finance, and operations?

The excerpts do not assign a single required owner, so you should make one person or function explicitly accountable before rollout. What cannot stay vague is escalation and resolution authority: your team needs a named decision owner, named backups, and a clear handoff for execution. If nobody can say who makes the final call on a contested alert, governance is not ready for tooling.

What key vendor details are still unknown before tool selection and contract signature?

Several procurement-critical details remain unproven in the available material: matching logic, API depth, SLA, language coverage, and false-positive performance. Ask each vendor to show a sample alert pack, not just a dashboard, and verify whether a reviewer can see the source article, matched identity fields, filtering behavior, and case export. Treat any answer that stays at marketing level as a contract red flag.

How do sanctions screening and PEP screening fit with negative news screening in one control stack?

The available excerpts do not establish how sanctions and PEP screening should be combined with negative news screening. Treat this as an open control-design and procurement question, and require vendors to show how each signal is reviewed and documented in practice.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- bsaefiling.fincen.gov/docs/XMLUserGuide_FinCENFBAR.pdftrusted

- citap.unc.edu/news/local-news-platforms-mis-disinformationtrusted

- fincen.gov/reporting-maximum-account-valuetrusted

- fincen.gov/report-foreign-bank-and-financial-accountstrusted

- irs.gov/irm/part4/irm_04-032-002trusted

- npsa.gov.uk/insider-risk-mitigation-digital-learningtrusted

- pmc.ncbi.nlm.nih.gov/articles/PMC12894197trusted

- pmc.ncbi.nlm.nih.gov/articles/PMC12116099trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

When Instant Payout Matters for Gig Platform Payments

Instant payout is a tool, not the goal. The real operating decision is where instant timing creates measurable value, where batch timing is enough, and where both should run side by side.

FedNow vs RTP for Gig Platform Contractor Payouts

You are not choosing a payments theory memo. You are choosing the institution-backed rail path your bank and provider can actually run for contractor payouts now: FedNow, RTP, or one first and the other after validation.

Real-Time Payout Tracking for Platforms That Reduces Support Load

Faster rails do not fix unclear payout state. Payout tracking matters when each payout can be followed from authorization through reconciliation, not when disbursement is merely faster.