Quick Answer

Start with the rail your bank or provider can actually send on today, not the one with better headline appeal. For most teams, that means one real-time rail plus ACH fallback at launch, then expansion after live proof. FedNow has documented 24x7 availability and published 2026 fee lines, while RTP shows stronger public reach signals and explicit immediate finality. Decide with operator checkpoints: routing validation, idempotent send behavior, off-hours ownership, and reconciliation quality.

How to choose between FedNow and RTP#

You are not choosing a payments theory memo. You are choosing the institution-backed rail path your bank and provider can actually run for contractor payouts now: FedNow, RTP, or one first and the other after validation.

Neither rail is directly available to your contractors. FedNow is available to U.S. depository institutions, and the Federal Reserve does not provide payment services directly to businesses or consumers. RTP is financial-institution infrastructure, and institutions can connect directly or through Third-Party Service Providers. For a gig platform or marketplace, the practical decision is which bank, processor, or embedded-payments partner can support your payout flow with acceptable coverage, support, and reconciliation.

This guide helps you choose a starting rail, validate the assumptions that matter at launch, and decide when a second rail is worth the added complexity. If instant payouts are a targeted retention feature, your path may differ from a marketplace trying to broaden real-time availability across a wide payee base.

Treat "real-time" as rail behavior, not a universal day-one product promise. The Federal Reserve frames instant payments as immediate end-user funds availability, at any time, with near real-time interbank settlement. Your product outcome still depends on send-side access, recipient institution reach on the selected rail, and your ability to run controls when money movement continues outside business hours. Before you commit to a launch path, confirm four operator facts with your bank or provider:

- which rail or rails they currently support for outbound payouts

- whether recipient reach is based on live routing data or point-in-time participant snapshots that can lag

- what payment status and exception detail they return

- who owns off-hours support when urgent payouts fail or stall

Keep the starting scope tight. Capabilities, participation, and coverage vary by institution and provider, and shared standards do not guarantee identical implementation behavior. Use this guide as an operator guide. Pick a starting rail, validate the bank or provider route behind it, and add the second rail only when the results justify the extra operational surface area.

This pairs well with our guide on Choosing Global Contractor Payment Rails in 2026 Without False Precision.

FedNow and RTP at a glance for platform operators#

Start with the rail your bank or embedded-payments provider can run well today, not the rail with the cleaner headline. RTP has stronger public reach and finality signals, while FedNow has clearer public fee lines and explicit liquidity tooling. Neither rail alone supports a universal instant-payout promise.

| Operator criterion | FedNow Service | RTP Network | What it means for a platform |

|---|---|---|---|

| Participation requirements | Available to depository institutions eligible to hold accounts at the Reserve Banks | Open to any federally insured depository institution and certain other FIs; no ownership or membership in The Clearing House required | You still access the rail through a bank or provider, so confirm their actual outbound capability |

| Network status | Live since July 20, 2023 | Launched in 2017 | RTP has a longer live history; FedNow is fully live, not pilot-only |

| Settlement behavior | Known: instant payment infrastructure, available continuously | Known: payments clear and settle individually in real time with immediate finality; settlement is final and irrevocable | Treat both as high-control rails; RTP finality is explicitly documented here |

| Availability | 24-hour business day every day, including weekends and holidays | Known real-time infrastructure; this pack is more explicit on FedNow availability wording | If you market instant payouts, your support model must cover nights, weekends, and holidays |

| Liquidity handling | Known: liquidity management transfer capability; 2026 LMT origination fee is $1.00 per item | Confirm with your provider | FedNow gives you a documented treasury control to validate with your bank |

| Messaging | Uses ISO 20022 for customer credit transfers, requests for payment, and more | Includes ISO 20022 standard messages plus proprietary messages for sign-on, sign-off, and echoes | Shared ISO 20022 does not mean identical implementations or engineering effort |

| Transaction limit | Network transaction limit increased from $1 million to $10 million effective November 2025 | Up to $10 million per transaction | Both support high-value use cases on paper; confirm operating limits with your provider |

| Public pricing visibility | Known: 2026 customer credit transfer origination fee is $0.045 per item; participation fee listed as $25.00 per RTN per month, discounted to $0.00 in 2026 | Compare directly with your provider | Do not assume cost parity just because both are instant rails |

| Public reach data | Verify current count with the Fed or TCH | Over 1,130 participants as of December 2025; reaches 71% of U.S. DDAs, with technical reach close to 90% of DDAs | RTP gives stronger public reach signals, but technical reach is distinct from direct participant reach |

| Product promise | Can support instant payouts where send-side access and recipient institution path are live | Same | Message instant payouts as eligibility-based, not universal |

| Support load | Known always-on service context; exception detail is provider-dependent | Known immediate finality context; exception detail is provider-dependent | Always-on rails and immediate-finality flows require clear support and exception handling |

If treasury setup is your main blocker, FedNow deserves a hard look because LMT support and 2026 fee lines are publicly documented. If reach validation is your blocker, RTP gives you more concrete public numbers to pressure-test in diligence.

Known vs unknown#

Here is the clean split. Known: FedNow runs every day, including weekends and holidays. Known: RTP settles individually in real time with immediate finality, and submitted payments are irrevocable. Known: both rails use ISO 20022 in some form, but shared ISO does not guarantee identical implementation.

| Topic | Status | Detail |

|---|---|---|

| FedNow availability | Known | Runs every day, including weekends and holidays |

| RTP settlement | Known | Settles individually in real time with immediate finality, and submitted payments are irrevocable |

| ISO 20022 use | Known | Both rails use ISO 20022 in some form, but shared ISO does not guarantee identical implementation |

| RTP fees vs. FedNow fees | Unknown | This evidence set does not provide an apples-to-apples RTP fee comparison against FedNow's published 2026 fees |

| FedNow participant count | Unknown | Verify current count with the Fed or TCH |

| Universal contractor coverage | Unknown | Confirm contractor-level coverage with your rail provider |

Unknown in this evidence set: an apples-to-apples RTP fee comparison against FedNow's published 2026 fees. Also unknown: a single current FedNow participant count and any universal contractor-level coverage claim for either rail. If a provider says "near universal reach," ask whether they mean direct live reach, technical reach, or static participant snapshots.

Before launch, ask for two artifacts: a current routing or participant validation method and sample status or error payloads for failed or rejected payments.

What changes in the product and ops layer#

For contractors, both rails can support instant payouts, but only as a conditional promise. Use messaging like "available for eligible bank accounts" until you have live success data by bank cohort and a fallback path.

Implementation effort is easy to underestimate. Shared ISO 20022 does not remove implementation work: the evidence set confirms RTP proprietary message handling and that ISO 20022 implementations can differ across services.

That is the real decision point. Treasury posture, controls for irrevocable money movement, and support maturity matter more than the headline that both rails are real-time. If those capabilities are still maturing, start with one rail, prove routing and incident handling, then add the second when added reach or resilience justifies the extra complexity.

For a side-by-side with ACH, see FedNow vs RTP vs ACH: Which Real-Time Payment Rail Should Your Platform Use?.

Stop mixing up instant payouts and real-time rails#

Instant payouts are your product promise; real-time payments are rail behavior. If you treat them as the same thing, product commitments will outrun actual bank access, routing coverage, and ops readiness.

A team can promise "get paid fast" before the money movement stack can deliver it consistently. Instant payout features are eligibility-based, not universal from day one. FedNow and RTP are institution-level real-time rails with participation and operating constraints, not consumer payout products.

That distinction matters in practice because contractors see the ETA in your app, not your rail diagram. FedNow is explicit that there is no consumer app and that send or receive depends on whether the other institution is also signed up. RTP is also FI-driven infrastructure. If your UX says "instant for everyone" but your provider only supports certain cohorts or routes, you create support load and expectation risk.

What to verify before you promise speed#

Before you market instant payouts broadly, require segment-level evidence, not coverage headlines:

| Evidence | What to request |

|---|---|

| Routing validation | Current routing or participant validation method by destination institution |

| Outcome data | Success and failure rates by bank cohort or payout segment |

| Status detail | Sample reject and status payloads so product and support teams know what "not eligible" looks like |

Do not treat rail availability as payout eligibility. FedNow participant snapshots are updated irregularly, and universal contractor coverage claims cannot be confirmed without checking live participation directly with your provider.

The operator rule#

Never market "instant" globally until you can verify rail-path success rates and fallback behavior by segment. If a segment cannot reliably clear on your supported path, show a different ETA and route to fallback instead of letting marketing language outrun operations.

If you want a deeper dive, read Real-Time Payment Use Cases for Gig Platforms: When Instant Actually Matters.

Where FedNow and RTP differ in day-to-day operations#

FedNow and RTP are both real-time rails, but they do not create the same operating work. If your team treats them as interchangeable because both use ISO 20022, support and finance can absorb the mismatch first.

| Operator question | FedNow Service | RTP Network | Why it changes daily operations |

|---|---|---|---|

| Who runs it, and in what network context? | A Federal Reserve instant payment service for U.S. depository institutions, with Boston Fed program leadership context and a stated role alongside private-sector providers | A private instant payments network operated by The Clearing House, which is owned by large commercial banks | Bank-partner coordination, escalation paths, and change communications can run through different governance contexts |

| Does shared ISO 20022 mean the implementations match? | Uses ISO 20022, but not identically to RTP | Uses ISO 20022 and also proprietary administrative messages for sign-on, sign-off, and echoes | Shared standards help with common language, not message parity or identical exception handling |

| What does liquidity look like? | Settlement occurs in the participant's master account and does not require prefunding | Sending participants must monitor their Current Prefunded Position and provide supplemental funding when needed | Finance sign-off can be different, especially for off-hours payout volume |

| What should you expect from onboarding and compliance? | Formal testing and certification were part of launch readiness before July 20, 2023 | Has its own technical documentation and operating rules, including rules effective January 1, 2026 and specified compliance by April 16, 2026 | You need rail-specific readiness checks, not one generic real-time checklist |

Shared ISO 20022 helps, but it does not flatten the work#

ISO 20022 gives product, engineering, and providers a shared message vocabulary, but it does not make FedNow and RTP operationally identical. Message-level differences still matter in production.

ASC X9 highlights concrete differences, including RTP using pacs.008 for Payment Returns while FedNow uses pacs.004. RTP documentation also includes proprietary administrative messages for connectivity. Before sign-off, require a rail-specific message map plus sample reject, return, and status payloads so support is not diagnosing failures from payout-screen symptoms alone.

Where the differences show up in real teams#

A common split point is onboarding. FedNow launch readiness included formal testing and certification, with 57 early adopter organizations completing that process before go-live, while RTP has its own technical stack and operating rules. Ask for rail-specific certification, connectivity, and exception-test steps through your bank or provider, not a generic "real-time supported" answer.

Another split point is support escalation. Because the operator contexts differ, one incident template may not be enough. Capture destination institution, timestamps, message IDs, raw network or provider status, and internal ledger references. For RTP-related issues, include the liquidity snapshot at send time to cut avoidable escalation cycles.

Finance sign-off can become a bottleneck. RTP requires ongoing prefunded-position monitoring and supplemental funding when needed, while FedNow states settlement occurs in the participant's master account without prefunding. Approve launch only after ownership is clear for after-hours liquidity actions on RTP and bank or provider settlement coordination on FedNow.

Pick the rail your bank and provider can onboard, support, and fund with the fewest unknowns now. Add the second rail once your team can run two distinct exception and finance motions reliably.

We covered this in detail in The Gig Economy in 2026: Payment Volume Trends Contractor Growth and Platform Consolidation.

Should you launch with one rail or both#

Launch one rail first, stabilize real-time support, exception handling, and finance operations, then decide whether the added reach or resilience of a second rail justifies the extra overhead. Consider dual-rail earlier when payout speed is a priority and you already operate across multiple bank or provider paths, but only if ownership is clear before launch.

| Checkpoint | What to confirm |

|---|---|

| Support staffing | Define who covers nights, weekends, and holidays; FedNow participation guidance calls out continuous-availability expectations |

| Failure triage SLA | Set internal first-response and escalation targets, then test reject and return scenarios so teams can isolate root cause quickly |

| Liquidity management | Assign an owner by rail; for FedNow, confirm how your bank or provider handles liquidity management transfers and funding operations |

| Routing logic ownership | Engineering should own deterministic routing, fallback behavior, and duplicate-send prevention |

The rails do not ask the same things of your team. FedNow went live on July 20, 2023, while RTP launched in 2017. RTP participants must complete a compliance self-audit at least once each calendar year. FedNow guidance expects near-continuous availability and a strategy to maintain sufficient liquidity at all times for institutions that send credit transfers or provide settlement or funding services. Before you decide on one rail or both, confirm those four checkpoints and make sure the owners have tested their part of the process, not just approved it in a planning doc.

Consider dual rail only after those four areas are fully owned and operationally tested. If they are not, start with one rail and expand after operations are consistently clean.

Liquidity design for always-on settlement#

Moving from ACH to instant settlement shifts treasury from a banking-day batch process to a 24/7 operations function. Do not widen real-time payout eligibility until your team can reliably forecast, fund, monitor, and rebalance liquidity outside business hours.

ACH gives you more timing slack. It is a batch, store-and-forward rail with value-dated settlement. It processes payments 23¼ hours every banking day, settles four times each banking day, and does not currently settle on weekends or federal holidays. FedNow is designed for uninterrupted 24x7x365 processing, and RTP documentation requires participants or funding agents to monitor Current Prefunded Position and provide supplemental funding, including during Fedwire off-hours.

| Rail | Settlement timing | Funding model that matters operationally | Treasury implication |

|---|---|---|---|

| ACH | Batch, value-dated settlement on banking days | Liquidity and reconciliation cadence follows banking-day settlement windows | Plan around file cutoffs and banking-day schedules |

| FedNow Service | Continuous 24x7x365 instant settlement | Settlement occurs in the participant's master account and does not require prefunding; Liquidity Management Transfer (LMT) supports moving funds between eligible settlement accounts | You still need off-hours liquidity coverage, alerts, and a fast top-up path |

| RTP Network | Real-time settlement with finality | Participants or funding agents must monitor CPP and provide supplemental funding | Prefunded balance discipline is central, especially nights and weekends |

Use a cohort model based on payout behavior. Predictable recurring contractor cohorts are often easier to start with because lower variance can make funding assumptions easier to validate against observed intraday demand. More volatile cohorts should start with tighter eligibility and clear exposure limits, with ACH fallback for overflow or non-urgent payouts.

Order of operations#

- Forecast by cohort, daypart, and weekend pattern, separating stable payouts from volatile cash-out demand.

- Fund according to your actual bank or provider setup. For FedNow, confirm whether LMT is used and which settlement accounts are in scope. For RTP, confirm who monitors CPP and who executes top-ups.

- Monitor with off-hours alerts tied to runway against expected send volume, not only current balance.

- Rebalance before balances become critical. FedNow end-of-day accounting records support reconciliation, so keep intraday monitoring in place.

- Set escalation thresholds before expanding eligibility. If available funding drops below your approved floor or top-up response misses SLA, pause new real-time payouts and route to ACH where allowed.

Caveat

Coverage, account reach, and funding mechanics vary by institution and program configuration. RTP reports reach to 71% of U.S. demand deposit accounts, while FedNow participation is still expanding. Confirm the operating model in your contracts and implementation documentation before widening access.

For the full breakdown, read Continuous KYC Monitoring for Payment Platforms Beyond One-Time Checks.

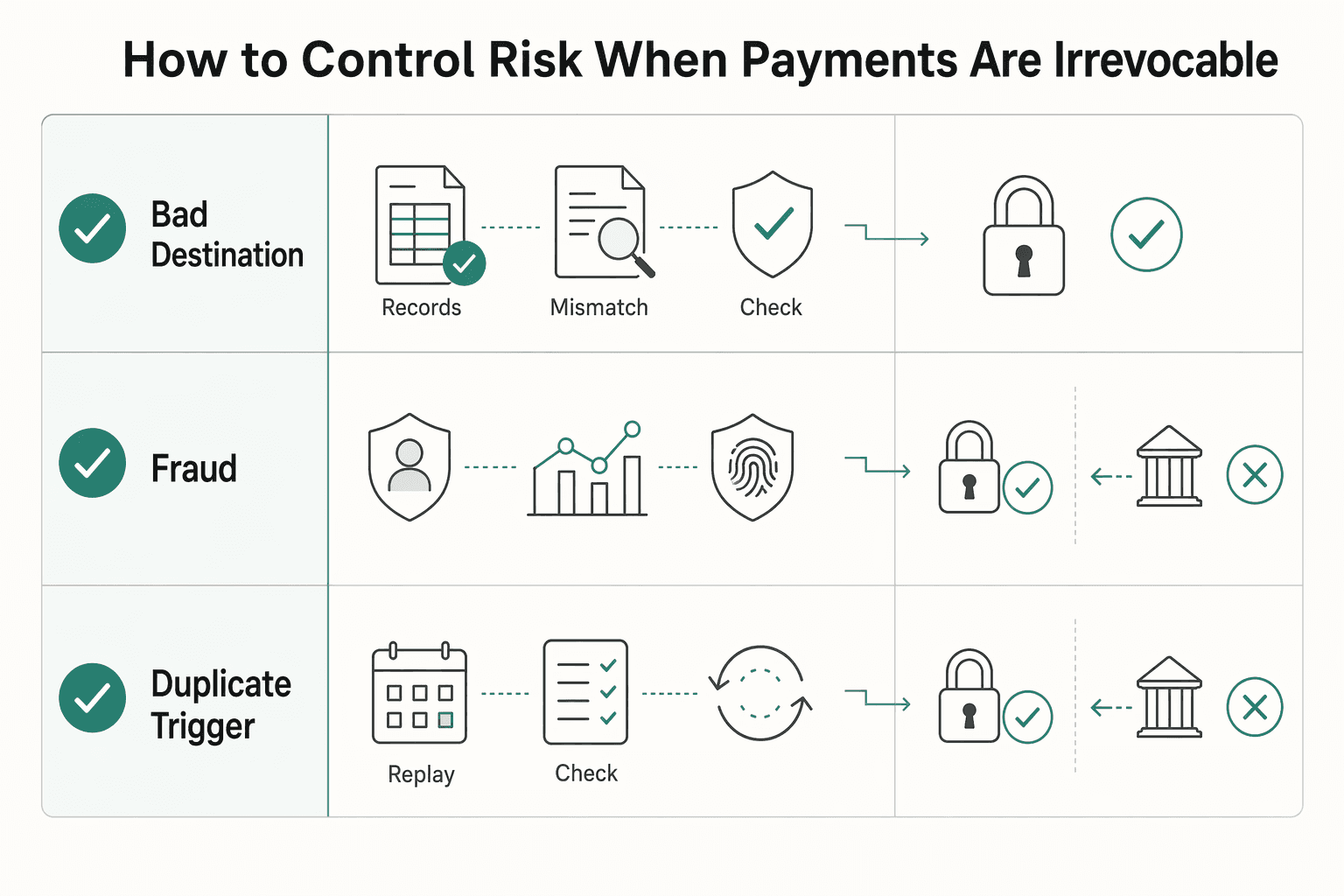

How to control risk when payments are irrevocable#

On FedNow and RTP, risk control should happen before send, because once a payment is sent it is final and the payer cannot cancel it. RTP also allows a message to request return of funds, but that is not a guaranteed recovery path.

| Risk event | Why it is harder on irrevocable rails | Pre-send control | Post-send action |

|---|---|---|---|

| Bad destination data | Funds may be withdrawn immediately after settlement | Verify recipient identity and payout account details before enabling real-time payouts; add stricter review when payout details change | Open an incident immediately, capture account-change and approval history, and issue documented return requests where available |

| Fraud | Finality and speed reduce time to detect and stop loss | Put fraud controls early in the flow, ideally during authentication, then apply risk-based identity and due-diligence checks before release | Route to a dedicated fraud queue, preserve authentication and device evidence, and escalate with clear severity rules |

| Duplicate-trigger incidents | A second payout cannot simply be canceled after send | Enforce idempotent payout creation and approval logic for repeated or unusual events | Link related payout events, isolate the trigger path, and retain processor, ledger, and webhook records for audit |

Pre-send controls that matter most#

Put your strongest controls upstream of payout release. If identity or risk profile is not sufficiently verified under your risk-based CIP or CDD framework, keep that user off real-time rails until verification is complete.

For FedNow programs, use value and velocity controls by customer segment where available, with tighter settings for newer or higher-risk profiles. In practice, a new recipient, recent credential reset, changed payout details, or unusual payout behavior can trigger lower limits, additional review, or secondary approval.

Post-send controls for when prevention fails#

Some incidents will still pass through, so run a dedicated real-time incident lane instead of a generic support queue. Separate misdirected payment, suspected fraud, duplicate send, and dispute cases so each follows the right escalation path.

Attach a complete evidence pack to each payout event: profile state, payout-method change history, authentication logs, approval records, timestamps, amounts, external references, and support interactions. For FedNow-related operations, Federal Reserve exception tooling can support case handling and documentation exchange.

Related reading: How Gig Platforms Can Use Earned Wage Access (EWA) as a Contractor Retention Tool.

Design contractor payout choices without creating support chaos#

The cleanest operating model is tiered: use real-time only where the route is actually available, and keep ACH for the rest. For contractor payouts, eligibility should be based on segment and destination, not on a universal instant promise.

| Payout path | When to use it | What you promise the contractor | Operator check that matters |

|---|---|---|---|

| Real-time rail | Contractor is in an eligible segment and the payment path supports instant receive | Funds are expected to be available in real time, any time of day, when the route is available | Confirm your sending institution or provider can send on the chosen rail and the recipient institution can receive |

| ACH fallback | Destination is not eligible for instant receive, or the payout is lower priority | Processed on business-day ACH timing, not always-on instant timing | Use ETA language tied to ACH processing and settlement windows |

| Hold or review first | Routing capability is unclear, payout details just changed, or controls require another check | Payout is under review before release | Do not downgrade silently; record why the payout did not go real-time |

Support chaos usually starts when teams market speed as universal and then run into participation and bank-routing limits. FedNow availability depends on institutions on the payment path signing up, and RTP reach is broad at 71% of U.S. demand deposit accounts but still not universal. If you promise instant before confirming route success by bank and segment, support becomes the fallback.

In the UX, lead with outcome and ETA, not rail branding. Customers may never see the rail name, so clear status updates matter more: whether the payout is in review, sent in real time, queued for ACH settlement, or delayed by an inquiry or exception.

When a payout falls back from instant to ACH, log the routing decision and reason in the payout record. That gives support a concrete answer for payment inquiries instead of a generic processing message.

Integration and reconciliation checkpoints before go-live#

Do not launch until engineering, finance, and ops can trace the same payout from trigger to settlement with the same IDs. If retries can create duplicate sends, callbacks can replay state changes, or product shows "paid" while finance cannot reconcile, you are not ready.

| Function | Required checkpoint | What to verify before go-live | Red flag |

|---|---|---|---|

| Engineering | Idempotent sends and replay-safe events | Every payout create or update call requires an idempotency key, duplicate webhooks are suppressed, and state transitions are deterministic | A retry creates a second payout or moves a terminal payout back to pending |

| Finance | Reference mapping and reconciliation | Internal ledger entries map to provider references and payout records, with intraday checks and a defined end-of-day exception review process | Finance cannot tie a bank payout back to underlying contractor transactions |

| Ops | Clear incident ownership and recovery paths | Named owners for callback failures, wrong-destination claims, duplicate-event incidents, and return-of-funds handling where available | Support opens a ticket but no team owns the next action |

Engineering checks that actually prevent duplicate money movement#

Require idempotency keys on every payout create or update call across your embedded payments stack. This is what makes retries safe instead of expensive. Run an intentional retry test and confirm you get the same logical outcome, not a second payout. If your provider retains idempotency keys for a limited window, for example 24 hours in one common implementation, make sure your own dedupe record covers longer retry paths.

Treat duplicate and delayed webhooks as normal. Providers can redeliver undelivered events for up to 3 days, so handlers should store event IDs and suppress duplicate processing. Keep payout transitions monotonic, for example created, submitted, sent, failed, under_review, so late events cannot push a payout backward in state.

Finance checks that keep the ledger honest#

Finance should be able to map each internal payout ID to the provider settlement reference and to the underlying transaction records. The point is not only confirming that funds moved, but proving what was included, what adjustments applied, and what remains unresolved.

Set up two views before go-live: intraday reconciliation and end-of-day exception review. Intraday checks catch drift early. End-of-day review should surface unmatched payout IDs, amount mismatches, payouts marked sent without matching ledger closure, and callbacks with no corresponding ledger record.

Ops checks for finality and exceptions#

Define an ownership matrix for each failure mode: provider timeout, duplicate callback, wrong-recipient claim, and post-sent payout inquiry. For RTP and FedNow operations, treat submitted instant payments as final and irrevocable. RTP recovery can use Request for Return of Funds messaging (camt.056 with camt.029 response), which is not the same as a sender-side reversal. FedNow also supports exception message types such as request for return of funds and request for payment cancellation, but ops should still assume funds are not routinely unwindable after submission.

If Gruv is in this layer, confirm what your setup exposes instead of assuming it. Check that you can retrieve audit-ready records, payout status history, provider references, timestamps, retry outcomes, and policy-gate decisions where enabled. The go-live standard is simple: engineering, finance, and support can inspect one payout and reach the same conclusion without translating across tools.

Related: The Future of Contractor Payments: Embedded Finance Real-Time Rails and Programmable Money.

Use this checkpoint to map idempotency, status events, and reconciliation fields in your own flow, then compare implementation details in the Gruv docs.

Hidden costs and failure modes teams miss#

A common cost shift is operational, not just per-transaction pricing. When you move contractor payouts from batched ACH to always-on instant rails, you also take on 24/7 support expectations, tighter liquidity discipline, and harder recovery when money is sent in error.

In practice, the rail decision is not just about speed. It is about whether your team can operate final, always-on payouts without creating avoidable support and treasury strain.

| Rail | Direct cost signals you can verify | Operational staffing and support burden | Treasury overhead | Integration maintenance | Failure recovery effort |

|---|---|---|---|---|---|

| FedNow Service | 2026 customer credit transfer origination fee is $0.045 per item. Liquidity management transfer origination fee is $1.00 per item. General participation fee is $25.00 per RTN per month, discounted to $0.00 in 2026. | Can be higher than ACH because FedNow runs 24x7x365, so incidents and payout questions can surface outside business hours. | Can be higher. Always-on settlement requires explicit liquidity management, and FedNow includes liquidity management transfers for that purpose. | Moderate to high. You need rail-specific controls and ongoing limit and risk-setting review. | High. FedNow describes payments as final and irrevocable, so mistakes are harder to unwind. |

| RTP Network | Public sources reviewed here do not show a simple per-item operator fee. Connection can involve third-party service providers and other partners, adding vendor-management overhead. | Can be higher than ACH because RTP runs around the clock, including weekends, holidays, and after hours. | Can be higher. Real-time settlement reduces room for delayed funding. | High. Partner coordination plus ongoing maintenance against RTP Rules and technical specs in the document library. | High. RTP settlement is final and irrevocable, and sending institutions cannot revoke or recall a payment once submitted. |

| ACH | FedACH 2026 discount item fee is $0.0035 per forward or return item, with a $0.0010 surcharge for SameDay forward items. | Often lower. ACH is an efficient, low-cost batched payment rail and often aligns with business-hours exception handling. | Often lower. Batch timing can give finance more room to fund, review, and reconcile. | Often lower for teams already running ACH workflows. Rules still apply, but cadence is batch-based. | Lower to moderate. ACH reversals are allowed only under certain circumstances, which is a different recovery profile from irrevocable instant rails. |

One non-obvious tradeoff is support intensity. Faster settlement can raise support load if controls are thin. Once you promise immediate funds, exceptions can become live incidents, and weak controls can shift work into manual review instead of reducing it.

Check the date on your limit and risk assumptions before launch. FedNow communications have shown time-sensitive differences. One 2025 communication noted a default transaction limit of $100,000, while a later communication says the network transaction limit increased from $1 million to $10 million effective Nov. 12, 2025. If product, treasury, and engineering are working from different assumptions, eligibility rules and payout messaging can drift.

Red flags before launch#

- No explicit owner for liquidity management, including off-hours coverage

- No escalation design for irrevocable-payment mistakes, duplicate-trigger incidents, or wrong-destination claims

- No measurable launch gates for success rate, reconciliation match rate, exception aging, and support response

- No current evidence pack for rail limits, provider dependencies, and rule or spec versions in use

If instant rails do not clearly improve retention, unlock payout-critical use cases, or solve a real contractor experience problem, do not roll them out broadly. Phase by cohort, keep ACH in the mix, and expand only when operating evidence supports it.

A 30-day rollout sequence for gig platforms#

Keep the first 30 days narrow and evidence-led: prove one rail, one fallback path, and one support model can operate cleanly under live payout conditions before you expand. Treat this as an internal rollout cadence, not a regulator-mandated timeline.

| Week | Primary decision | What you need to verify | Hold signal |

|---|---|---|---|

| 1 | Pick the first rail and eligible contractor cohort | Named institution or provider path, send capability, participation requirements, fallback cohort | You cannot confirm actual send access or contractor eligibility by bank path |

| 2 | Prove controls in test | Idempotent send behavior, duplicate-event handling, exception paths, ACH fallback messaging | Unknown-status payouts, duplicate-send risk, or support cannot explain post-failure outcomes |

| 3 | Pilot with a limited cohort | Daily success rate, support contact volume, reconciliation quality, treasury variance against liquidity assumptions | Manual exceptions rise, reconciliation drifts, or off-hours funding behavior surprises finance |

| 4 | Decide whether to expand | Payout timing SLAs, incident handling speed, reconciliation sign-off, product-owner approval | Recurring incidents remain open, timing promises are inconsistent, or finance has unresolved breaks |

Week 1 decision and scope#

Start with one rail and one tightly defined contractor cohort. The practical first choice is usually the rail your bank or provider can support cleanly now.

Confirm access through your actual institution or provider path, not network headlines. FedNow access is institution-mediated, the Federal Reserve does not provide payment services directly to businesses, and institutions can join FedNow in receive-only mode first. RTP onboarding can be direct or through third-party providers. In both cases, get written confirmation of send capability and date-stamp it.

Keep the first cohort operationally simple: stable payout patterns, clean account data, and a clear need for faster funds. If you use RTP reach figures, treat them as date-sensitive and secondary to your own path validation.

Week 2 controls and testing#

Use week two to break your payout flow in test before production does. FedNow includes a customer testing environment in onboarding, and RTP technical documentation is built for institutions and tech firms planning integration. Prioritize two controls:

- Idempotent requests: retries must not create duplicate payment operations.

- Webhook deduplication: consumers should handle repeated event delivery without duplicate ledger movement or false alarms.

Run explicit irrevocable-payment drills. RTP settlement is final and irrevocable, and submitted payments cannot be revoked or recalled by the sending institution. Test wrong-recipient data, duplicate triggers, and delayed acknowledgments.

Test ACH fallback as a real user path. Same Day ACH is faster ACH within business-day windows, not a 24x7 instant rail, and ACH erroneous-entry reversals run on a different timeline, including a defined 5 banking day window.

Week 3 pilot launch#

Keep the pilot small enough to inspect every exception the same day. Review daily across product, ops, engineering, and finance, and track three daily views:

- Success and failure outcomes by primary rail path and fallback path

- Support contacts tied to payout timing, missing funds, and duplicate concerns

- Treasury variance against liquidity assumptions

Watch reconciliation closely. For FedNow, settlement occurs in the participant master account and does not require prefunding, but you still need to validate off-hours funding and monitoring assumptions under real load.

If send outcomes look healthy while reconciliation degrades, pause expansion. Unmatched references, delayed exception clearing, and support tickets ahead of confirmed payment state are scale blockers.

Week 4 scale gate#

Treat week four as a go-or-hold decision, not a calendar milestone. TCH launch guidance supports phased launches before full general availability and advises legal and compliance review of risks. Require an evidence pack with:

- Success and failure dashboard for the pilot period

- Incident log with root cause and current status

- Reconciliation sign-off from finance

- Product-owner decision note: expand, hold, or narrow scope

Expand only when reconciliation, incident handling, and payout timing SLAs are consistently met. If not, hold and fix, and keep ACH in the mix for non-eligible or lower-priority payouts.

For a step-by-step walkthrough, see Tipping and Gratuity Features on Gig Platforms: Payment and Tax Implications.

Conclusion#

Choose the rail your team can operate

Frequently Asked Questions

Is `FedNow Service` or `RTP Network` better for contractor payouts on a marketplace?

Neither is universally better for every marketplace. FedNow Service is Federal Reserve instant payment infrastructure for eligible depository institutions, and RTP is The Clearing House real-time payment infrastructure used by financial institutions. A practical first rail is often the one your bank or provider can send on now, with clear support coverage and a workable escalation path for unknown payout states.

Do we need both real-time rails at launch, or can we start with one?

You can start with one rail. One rollout option is one real-time rail plus ACH fallback before adding routing complexity. Add the second rail when your controls are stable and institution-path eligibility differences justify it.

What does `irrevocable payments` mean for fraud and payout error recovery?

It means mistakes are harder to unwind after send. On RTP, sending institutions cannot revoke or recall a payment once submitted, and FedNow settlement is final when the debit or credit is recorded or on Advice of Credit. Your controls need to be strong before send, with measures such as account verification, duplicate-send protection, and support playbooks built for operational recovery rather than simple reversal.

What is the practical difference between `instant payouts` and `real-time payments`?

Instant payout is the user promise, while real-time payments describes rail behavior. The Federal Reserve definition ties instant payments to immediate funds availability for the end user with near real-time interbank settlement. Do not market universal instant payouts unless you can validate routing success by recipient bank path.

When should we keep `ACH` in the mix instead of forcing real-time for everyone?

Keep ACH for lower-urgency flows and segments where real-time exception handling is not yet reliable. Same Day ACH still runs on processing windows, with examples like 10:30 AM ET submission and 1:00 PM settlement rather than continuous 24x7 processing. ACH can still be practical when urgency is lower, since Nacha reports most ACH volume settles within one banking day or less.

What must product, engineering, finance, and ops verify before go-live?

Before go-live, each function should validate a specific control set tied to payout reliability and incident handling. Product should verify ETA language and fallback messaging. Engineering should verify idempotent sends, duplicate-event handling, and deterministic payout states. Finance should sign off on reconciliation and off-hours monitoring for continuously available rails. Ops should maintain written send-capability confirmation through the institution path, clear incident ownership, and the governing operating materials for FedNow participants and RTP execution.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 4 external sources outside the trusted-domain allowlist.

- bsaaml.ffiec.gov/manual/AssessingComplianceWithBSARegulatoryR...trusted

- ecfr.gov/current/title-31/subtitle-B/chapter-X/part-1...trusted

- federalreserve.gov/paymentsystems/fednow_about.htmtrusted

- federalreserve.gov/paymentsystems/fednow_faq.htmtrusted

- explore.fednow.org/resources/readiness-guide-participant-availa...external

- frbservices.org/binaries/content/assets/crsocms/financial-se...external

- frbservices.org/financial-services/fednow/organizationsexternal

- theclearinghouse.org/payment-systems/rtp/institutionexternal

Educational content only. Not legal, tax, or financial advice.

Related Posts

When Instant Payout Matters for Gig Platform Payments

Instant payout is a tool, not the goal. The real operating decision is where instant timing creates measurable value, where batch timing is enough, and where both should run side by side.

Future Contractor Payments Depend on Market-Ready Operations

Treat contractor payouts as a market-entry decision, not a speed feature. The real test is whether a country and payout program can run cleanly on day one and still hold up in reconciliation and reporting when exceptions happen.

FedNow vs RTP vs ACH for U.S. Platform Payout Routing

For many U.S. platforms, the right move is not picking a single winner between ACH, RTP, and FedNow. It is routing each payout to the rail that fits the job. Use ACH for predictable, non-urgent flows, and instant rails when speed changes the outcome and you are ready for tighter controls.