Quick Answer

In 2026, gig economy payment volume trends look positive, but no single verified global payment volume figure is proven. Operators should choose markets based on receiving-side rail coverage, payout reliability, onboarding friction, compliance burden, and treasury readiness instead of headline growth claims. The safer launch sequence is usually the market where cashout works end to end and exceptions can be resolved cleanly.

What Gig Platform Operators Need to Watch in 2026#

Treat gig economy 2026 payment volume trends as an execution question, not a headline-growth story. Some inputs are measurable now, including platform counts, payout-rail behavior, and jurisdiction-specific compliance requirements. What remains uncertain is any single, verified global gig payment volume number for 2026.

That distinction matters because you do not launch into an abstract market. You launch into a specific country, vertical, and payout design with real operational constraints. If you lean on broad market optimism alone, you can choose a market that looks large on paper but is much harder to run in practice.

The evidence base is useful but uneven. A February 2026 ILO brief says current data is still insufficient to accurately estimate the total number of people engaged in digital platform employment. It also says cross-country measurement still needs harmonization.

Even widely cited size signals need careful reading. OECD evidence places gig-platform employment at 1 to 3 per cent of overall employment. World Bank reporting cites up to 12 percent of the global labor market and 545 online gig work platforms, with workers and clients in 186 countries. Read these as boundary markers shaped by scope and definitions, not as one market truth.

The same caution applies to payout rails. Instant payments can make funds available within about ten seconds, and SEPA Instant Credit Transfer can make funds available in less than ten seconds. But availability is not uniform across SEPA jurisdictions. For operators, a rail label is not enough. Local readiness for your payout flow is what matters.

Compliance follows the same pattern. FATF centers a risk-based approach, which means countries adapt AML/CFT implementation to their own legal and operational context. So when demand looks similar across two markets, the better first launch is often the one with clearer compliance execution.

You should also treat legacy growth figures carefully. Mastercard's widely cited estimate projected 17% CAGR to about $455 billion by 2023, which is useful history, not direct proof of 2026 volume. By the end of this article, you should be able to choose a defensible launch sequence based on rails that work, compliance load you can absorb, and market conditions you can validate.

For a deeper look at platform-level payment shifts, see Gig Economy Payment Trends 2026: What Platform Operators Should Expect.

Start with the numbers you can trust#

Start with measured payment behavior and rail readiness, not a single global volume figure. The direction looks positive, but direct 2026 gig-payment evidence is still thin, so older Mastercard figures are context, not forecast proof.

A widely cited benchmark is Mastercard's 2019 study: about $204 billion in 2018 digital gig gross volume, projected at 17% CAGR to about $455 billion by 2023. That is useful history, not measured 2026 volume. Mastercard later noted it was unknown whether those trends would endure, so do not carry that CAGR forward as if it were current fact.

Macro payments data is stronger, but it answers a different question. World Bank Findex shows adults making or receiving digital payments in developing economies rising from 35% in 2014 to 57% in 2021. BIS also reports that cashless payments continue to increase. That supports digital-payment demand, but it does not prove country-vertical conversion quality in a specific market.

| Evidence bucket | What you can treat as known | What stays unknown |

|---|---|---|

| Gig market size | Mastercard historical benchmark to 2023 | Precise global gig payment volume for 2026 |

| Payment adoption | Findex digital-payment growth; BIS cashless trend | Your platform's country-vertical conversion quality |

| Rail readiness | Brazil Pix up 52% in 2024 and 47% of non-cash payments by Q4 2024; FedNow reported nearly 1,600 participating institutions (Year in Review 2025), and participant reporting was updated 3/23/26 | Whether those rails work end to end for your payout flow |

| Europe | SEPA Instant exists | Uniform availability across all SEPA jurisdictions |

Keep a simple evidence log with four fields per datapoint: source, date, geography, and the operational decision it supports. The practical checkpoint is receiving-side coverage for your target bank mix, not just whether a rail exists. For more context, see The Future of Work is Freelance: Trends to Watch in 2026.

Build the mental model from rails to revenue#

If rapid contractor cashout is part of your offer, prioritize markets where payout flows work end to end in production, not markets where an instant rail exists only on paper. Account-to-account payments move funds directly between bank accounts, and instant schemes can reduce latency, but only when receiving coverage, disbursement operations, and return handling work reliably for your users.

| Rail | Speed/finality signal | Operational caveat |

|---|---|---|

| SEPA Instant | Designed for funds availability in less than ten seconds | Availability is not uniform across SEPA jurisdictions |

| Pix | Transfers happen in a few seconds at any time, including non-business days | Those infrastructure traits are not proof that your payout experience is ready for your bank mix and support model |

| FedNow | Went live on July 20, 2023; designed for 24x7x365 processing; settlement through the service is final | Requires active handling of payment and return messages, including required payment-status responses (pacs.002) in defined cases |

| RTP | Credit transfers are described as final and irrevocable | Includes return-of-funds messages for errant and fraudulent payments after initiation |

Rail existence is not payout performance#

A rail does not translate into payout performance until contractors can receive funds consistently, trust the timing, and resolve failures cleanly. SEPA Instant is designed for funds availability in less than ten seconds. Brazil's Pix states transfers happen in a few seconds at any time, including non-business days. FedNow went live on July 20, 2023 and is designed for 24x7x365 processing.

Those are strong infrastructure traits, but they do not prove your payout experience is ready for your bank mix and support model. If fast cashout is part of the promise, reliability should come before launch breadth.

Finality changes who owns the problem#

On instant rails, settlement finality becomes a product and operations requirement, not just a back-office detail. FedNow states settlement through the service is final. RTP documentation cited by the Federal Reserve describes credit transfers as final and irrevocable.

Finality does not remove exception handling. RTP includes return-of-funds messages for errant and fraudulent payments after initiation, and FedNow requires active handling of payment and return messages, including required payment-status responses (pacs.002) in defined cases. If you do not design for those states, users will experience them as payout failures.

What you should verify before expansion#

Before you add a country because it has A2A or instant rails, verify the operating details that determine whether cashout actually works:

- Receiving-side coverage for the banks your contractors actually use

- User-level completion timing, including nights and weekends

- Exception behavior for rejects, mistaken payments, and fraud-related returns

- Reconciliation evidence, including transaction IDs and message states your ledger and support team can trace

If two markets look similar on demand, prefer the one where you can prove payout reliability and exception recovery in live tests. Keep your product language precise too. The Federal Reserve distinguishes instant payments from other speed improvements such as same-day ACH.

For cross-border contractor flows, see The State of Global Contractor Payments 2026: Fees Speeds Rails and Trends.

Compare country and vertical attractiveness before launch#

Treat market selection as an operations decision first. When demand looks similar, choose the country-vertical pair with lower onboarding friction and clearer settlement behavior. Rail presence matters, but launch outcomes are often shaped by whether contractors can onboard, get paid, and resolve failures without overwhelming support and compliance. Use one scoring sheet so product, legal, and GTM are making the same tradeoffs from the start.

| Market candidate | Rail maturity signal | Expected dispute burden | Contractor concentration | KYC complexity | KYB complexity | AML complexity | Initial launch read |

|---|---|---|---|---|---|---|---|

| Euro area × freelancer marketplace | SEPA Instant is reinforced by the EU Instant Payments Regulation adopted 13 March 2024. Euro-area receiving/sending deadlines are 9 January 2025 and 9 October 2025. As of Nov 2024, SCT Inst had 2,627 participants and 73% share, but availability is still not uniform across SEPA jurisdictions. | Score from your own refund, complaint, and payout-recall patterns by job type. | Score from your own applicant density and active-worker distribution by country. | Medium for individual contractors because identity verification must be risk-based at account opening. | Low to High depending on sole traders vs legal entities. | Medium to High where sanctions-screening and verification-of-payee operations increase workload. | Good candidate when tested coverage is strong for your bank mix and supplier base is mostly individuals. |

| Brazil × delivery or service marketplace | Pix transfers in seconds at any time. Official stats show +170 million individuals (about 80% of population) and +7 billion transactions in January 2026. | Score from cancellation, non-fulfillment, and support-contact patterns in your model. | Score from your own city-level worker supply and repeat activity. | Medium for high-volume individual onboarding. | Can be lower if onboarding is mostly natural persons. | Medium because participation includes eligibility/supervision conditions and AML-related internal controls. | Strong cashout fit if your provider can support real receiving coverage and 24x7 exception handling. |

| U.S. × contractor platform paying individuals and businesses | RTP emphasizes final settlement anytime, every day. It reported 125 million transactions totaling $405 billion in Q4 2025 and over 1,130 participants as of December 2025. | Score by payment trigger type (milestone, adjustment, mistaken payment) since support load differs. | Score from your own acquisition funnel by state, metro, and trade. | Medium for individuals under customer identification procedures. | High when legal entities are common because beneficial owners must be identified at account opening. | High when mixing individuals and businesses with heavier monitoring and investigation needs. | Attractive only if you can prove receiving-side reach for your bank mix and fast failed-transfer investigations. |

Read this as a gating tool, not a ranking toy#

The rail signal tells you whether instant payout is plausible. The KYC, KYB, and AML columns tell you whether activation is sustainable at your target cost. If you score demand alone, you may overcommit to markets that look large but stall in onboarding, entity checks, or sanctions operations.

Use this tie-break rule before GTM spend#

If two markets tie on demand, pick the one with lower onboarding friction and clearer settlement behavior. That rule is conservative by design and can help you avoid spending into markets where signup volume is high but activation and payout support degrade.

Verify before greenlighting launch#

For each country × vertical candidate, track the same three pilot checkpoints:

- Pilot payout success rate on real contractors and real receiving accounts, segmented by institution

- Median payout completion time, including nights and weekends

- Investigation turnaround for failed transfers, measured from ticket creation to useful resolution

Keep evidence for every failed or delayed payout: payout reference, transaction ID, initiation timestamp, completion or reject timestamp, investigation open and resolve time, and reason code or support explanation. Track onboarding rejection reasons for identity and business verification separately. A fast rail with messy exception handling is still a slow launch.

Related reading: How to Calculate the All-In Cost of an International Payment.

Choose payout and collection architecture that can survive scale#

If your promise depends on fast contractor cashout, choose an architecture that keeps collection, payout, and payment-state visibility aligned from day one. In practice, that often means a ledgered model such as Virtual Accounts plus local payout rails, with webhook-driven status tracking built in. Card-led collection with batch disbursement can still work, but timing gaps and reconciliation load can increase as payout volume grows.

| Architecture | Where it fits | What it buys you | Main operational failure points |

|---|---|---|---|

| Virtual Accounts + local payout rails | Marketplaces that need clear inbound attribution and faster contractor payouts | Virtual Accounts use a virtual sub-ledger under one physical account, improving cash visibility while reducing physical account sprawl. Combined with local rails, this can make collection-to-payout matching cleaner and liquidity easier to track. | If status events or references are weak, your ledger can drift from bank state and failed payouts turn into manual investigations. |

| Card-led collection + batch ACH disbursement | Platforms collecting by card, then paying U.S. contractors on scheduled runs | Familiar setup and broad collection acceptance. ACH remains material in U.S. flows: Same Day ACH reached 1.4 billion payments and $3.9 trillion in 2025. | ACH is batch-based, not always-on. Same-day deadlines such as 10:30 a.m. ET, 2:45 p.m. ET, and 4:45 p.m. ET can create cutoff pressure, treasury timing gaps, and support friction when users expect immediate cashout. |

| Card-led collection + instant payout rails such as RTP or FedNow | Platforms that want card acceptance but tighter payout timing | RTP and FedNow are positioned for real-time availability at any time of day, any day of the year, which can support more precise funding and cash-flow management. | Faster settlement raises exception-handling requirements. For RTP credit transfers, settlement is described as final and irrevocable once settled. Weak account validation or retry controls can become customer-facing incidents quickly. |

Where ACH still sits in U.S. flows#

Design as if ACH will remain part of your U.S. stack. FedACH is explicitly batch-based, and Same Day ACH still operates on defined windows rather than continuous settlement, so those timing constraints are structural.

In marketplace operations, ACH often remains in the mix for scheduled disbursements where timing windows are acceptable. Its scale and growth reinforce that reality: Same Day ACH volume rose 16.7% year over year from 2024 to 2025, and value rose 21.4%. The core decision is not ACH vs no ACH. It is where ACH timing is acceptable and where it conflicts with your cashout promise.

If you need contractor access to funds at night or on weekends, RTP or FedNow can help reduce how much cash you park early just to meet later batch windows. That benefit only matters if payment-state changes are visible quickly and reconciled correctly.

MoR can simplify ownership, but it changes who absorbs the mess#

Treat Merchant of Record as an architecture decision, not just a legal label. The MoR is the entity with legal responsibility for a transaction, and in platform designs that can be the platform or connected accounts depending on configuration.

An MoR-heavy setup can reduce fragmentation when you want one party to own customer-facing transaction responsibility. But it is not a full handoff. In certain marketplace charge models, refunds, disputes, and associated fees are still debited from the platform balance.

Direct platform settlement can give more control over ledger design, payout timing, and reconciliation logic. It may be a better fit when you need contractor-level balance ownership, hold logic, or custom release rules, but only if your ledger, event intake, and investigation handling are mature.

If refund or return risk is high, optimize for observability first#

When refund or return risk is high, favor the architecture with stronger reconciliation and webhook-driven status visibility from day one. Speed alone does not prevent operational breakdowns.

At minimum, tie each inbound collection and outbound payout to one traceable record chain: platform ledger entry, provider payment ID, bank reference, initiation timestamp, latest status timestamp, and final disposition. Webhook endpoints are useful here because they are designed for asynchronous payment events, which helps keep internal state current as payment status changes outside user sessions.

A common failure mode is missing evidence, not rail choice. If support cannot quickly confirm whether a payout is pending, settled, rejected, refunded, or disputed from one record path, teams end up rebuilding truth in tickets and spreadsheets. Under growth, that is usually what turns a workable model into an unstable one.

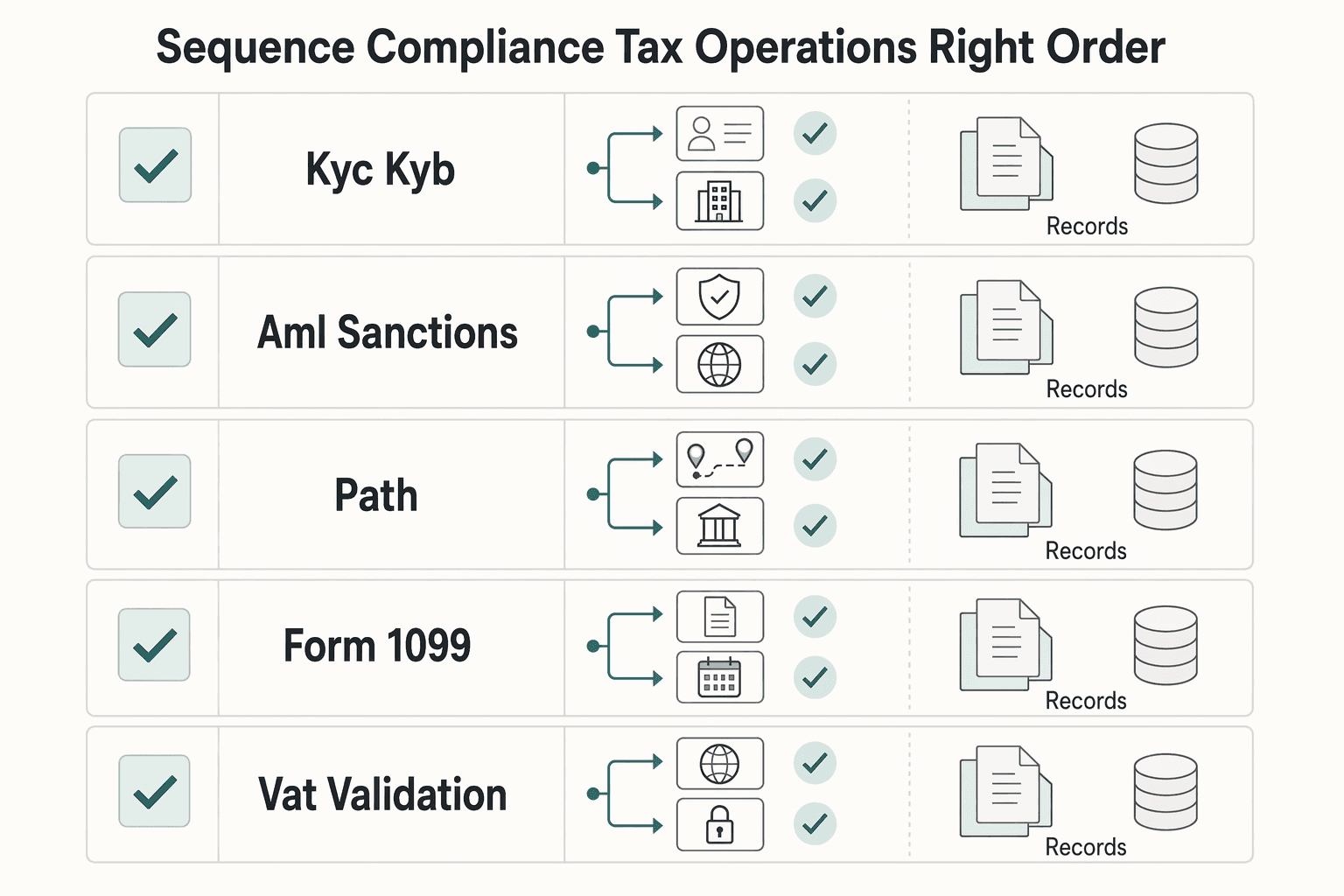

Sequence compliance and tax operations in the right order#

Do not scale high-velocity contractor payouts until compliance and tax onboarding are reliable end to end. As an operating sequence, start by confirming who you are paying with KYC or KYB, then run AML and sanctions checks, and collect the tax artifacts you will depend on later.

| Workstream | When to handle it | Why it matters |

|---|---|---|

| KYC or KYB | Start by confirming who you are paying before payout activation | When checks happen after funds start moving, teams can face more freezes, manual holds, and support escalations |

| AML and sanctions checks | Put them in front of payout activation | The article says to run AML and sanctions checks before scale and track where applicants stall |

| W-8 or W-9 path | Set it early and collect tax artifacts during onboarding | Keep form status tied to the same operational record path as payee identity and payout state |

| Form 1099 readiness | Treat it as a data-integrity outcome, not a year-end task | Fragmented payee profile, tax form state, payment history, and correction history can turn reporting into a reconciliation project |

| VAT validation | Use it as an explicit gate where tax status affects operations | Store the result with the payee record and make support visibility immediate |

Start with payout gating, not tax cleanup#

Put KYC, KYB, AML review, and sanctions screening in front of payout activation. When those checks happen after funds start moving, teams can face more freezes, manual holds, and support escalations instead of controlled onboarding outcomes.

Track more than pass or fail. You need clear visibility into where applicants stall so you can fix prompt clarity, document flow, and escalation routing before rollout pressure increases.

Sequence tax artifacts before payout volume makes remediation expensive#

Collect tax artifacts during onboarding, not after payouts are already active. For contractor-heavy flows, set the W-8 or W-9 path early, and keep form status tied to the same operational record path as payee identity and payout state.

Treat Form 1099 readiness as a data-integrity outcome, not a year-end task. If payee profile, tax form state, payment history, and correction history are fragmented across systems, reporting can turn into a reconciliation project.

Treat VAT validation as a market gate where it affects operations#

Use VAT validation as an explicit gate in markets where tax status changes invoicing, settlement treatment, or required documentation. Decide when validation happens in onboarding, store the result with the payee record, and make support visibility immediate so finance does not need to rebuild the trail.

Use one expansion rule and enforce it#

If compliance onboarding completion is below pilot target, pause geographic expansion and fix identity and document workflows first. The leading indicators can include payout-eligible completion without manual rescue and exception-resolution time. If those are weak, adding markets can multiply failure paths instead of growth.

Rework treasury assumptions for always-on payout expectations#

If you support instant payouts, treasury has to run as a continuous liquidity operation, not an end-of-day cash sweep.

Always-on rails raise the bar for funding readiness. FedNow requires immediate recipient fund availability 24/7, and TIPS provides final, irrevocable instant settlement on a 24/7/365 basis. In practice, payout capacity depends on where liquidity sits, how fast you can replenish it, and how quickly you detect settlement exceptions.

Fund for the rail you actually use#

Set funding policy by corridor and rail, not with one global treasury rule. RTP positions are backed by prefunded balances held at the Federal Reserve Bank of New York. FedNow supports liquidity management transfers and provides access to intraday credit during its business day. TIPS requires participants to keep enough liquidity on the dedicated cash account for continuous instant settlement.

The operating implication is direct. In prefunded models, payout headroom is constrained by the prefunded balance. In top-up models, missed or delayed replenishment is a key risk during demand spikes.

Use controls that match settlement behavior#

Once funding is corridor-specific, your controls need to match the settlement model. Three usually matter most:

- Payout windows by corridor: Release automatically only in windows that match each rail's funding mechanics and your operating coverage. FedNow liquidity controls include concepts like time-window constraints and transaction limits, which map well to corridor-level release rules.

- Liquidity concentration where available: Notional pooling can net balances across accounts or entities without physically converting currencies, but it is not universally available.

- Alerts on settlement gaps: Alert on low prefunded balances, failed top-ups, and payouts that remain neither settled nor returned inside the expected corridor window.

A rail can be technically live while usable payout capacity is still constrained by funding setup and replenishment reliability.

Buffer logic should differ by payout pattern#

Use different buffer logic for different payout patterns, and validate the settings with pilot data. High-frequency, low-ticket gig payouts often need buffers designed for burst volume and potential exception traffic. Retries, returns, and delayed status events can create a gap between projected wallet balances and actually available funds.

Low-frequency, high-ticket contractor payouts carry concentration risk. On RTP, the per-transaction limit can reach $10 million, so a small number of large payouts can consume available capacity quickly even when transaction count is low.

Reconcile against ledger truth, not wallet projections#

Treat your authoritative ledger plus rail messages as the source of truth after retries and reversals. Reconcile payout state against outbound payment messages and return or status events. FedNow uses ISO 20022 message types such as pacs.008 for credit transfer and pacs.004 for payment return, and RTP supports real-time reconciliation with ISO 20022 data.

If a retry is initiated before the first attempt is conclusively settled or returned, route it to manual review or a suspense balance to prevent projection drift.

For the labor-rule side of platform risk, see The Department of Labor's New Independent Contractor Rule (2026).

Decide when platform consolidation helps and when it hurts#

Consolidation can help when one provider preserves your core controls across the corridors you operate. It can hurt when one integration removes retry safety or leaves you with no workable fallback in weaker corridors.

Consolidate around controls, not vendor count#

Start with control integrity by market and rail, not procurement simplicity. If retries are not idempotent, or timeouts cannot be clearly separated from delayed status updates, consolidation can increase duplicate-payment and investigation risk instead of reducing it.

A practical check is whether your retry keys, payment references, timestamps, and return or rejection events remain usable for incident review across all markets. That includes partner-bank or local-processor paths where status timing can vary by corridor.

If you operate in an EU-regulated chain, DORA-related direction is explicit: ICT third-party risk strategy should account for multi-vendor design (Article 6(9)). Even outside direct scope, this logic is useful. Resilience decisions are safer when designed up front, not retrofitted after scale.

Compare one-provider vs multi-provider by corridor depth#

Judge consolidation corridor by corridor, because cross-border quality is uneven.

| Decision lens | One-provider model is stronger when... | Multi-provider model is stronger when... |

|---|---|---|

| Corridor performance | Your key corridors are consistently served and predictable. | Performance and outcomes vary materially by corridor. |

| Local rail depth | One provider has real local payout and return handling on both ends. | Depth differs by market, so coverage and exception handling need alternatives. |

| Fallback resilience | Non-instant and contingency paths are still available when needed. | Primary and secondary routing is required to avoid single-path dependency. |

Global averages can hide risk. The World Bank tracks 367 corridors and reports a 6.49% global average remittance cost, while the ECB notes many corridors remain poorly served and nearly one-quarter are above 3% cost. If your corridor outcomes vary, use primary and secondary routing and validate failover behavior before committing to single-provider dependency.

In the U.S., ACH still processed 35.2 billion payments worth $93 trillion in 2025, so consolidation planning should include non-instant fallback capacity where it matters.

Stablecoins fit some programs, not your whole map#

Treat sterling-denominated systemic stablecoins as program-specific, not universal corridor infrastructure. The Bank of England consultation published on 10 November 2025 sets a high bar: nominal value stability, strong legal claim, and redemption at par in fiat, with final rules expected in 2026.

For consolidation decisions, test issuer dependence explicitly: who issues, where par redemption is enforceable, and how you reroute if the issuer is unavailable. The ECB warns expansion can increase reliance on a limited set of dominant private issuers, so keep stablecoin routes ring-fenced and retain a non-stablecoin path for the same corridor where required.

For a step-by-step walkthrough, see Indian Gig Economy in 2026: Treat Platform Income as Variable Until Settlements Prove Stability.

Spot red flags that invalidate growth projections#

Growth projections are not decision-grade if they assume instant, fully digital behavior and frictionless activation from day one.

Red flag 1: You model instant payout as the default market behavior. Cash use is still material, and some flows still run on batch rails. The ECB reports cash remains the most-used instrument at point of sale and person-to-person in the euro area, U.S. consumers still average seven cash payments per month, and ACH remains a batched service. If your model assumes faster payouts will immediately shift volume, validate that by rail and funding method in pilots first.

Red flag 2: You count rails without validating exceptions and finality. Rail availability alone is not readiness. Settlement finality means a transfer is only final when it is unconditional, enforceable, and irrevocable. RTP is final and irrevocable, while ACH includes reversal constraints for erroneous entries within 5 banking days, and some consumer error claims can surface up to 60 days after statement delivery. Keep a per-rail matrix for finality status, return paths, reversal windows, and investigation ownership before you trust launch assumptions.

Red flag 3: You under-scope KYC, KYB, and tax document work. Onboarding and tax workflows are launch dependencies, not post-launch cleanup. U.S. CIP requires core identifying data such as name, date of birth for individuals, address, and identification number, and legal-entity onboarding requires identifying and verifying beneficial owners. Tax intake also matters early: Form W-9 collects TIN data, and independent-contractor payments may trigger Form 1099-NEC reporting. Because IRS threshold language differs across pages, verify the current date-specific source before you model compliance effort.

If your first-market plan does not include KYC, KYB, tax-document capture, and exception handling, treat the forecast as optimistic rather than operational.

Run a 90-day operator checklist before committing GTM spend#

Do not commit GTM spend until a 90-day pilot shows that payouts, onboarding, compliance, and reconciliation work under real operating conditions.

| Pilot phase | Main focus | Key checks |

|---|---|---|

| Weeks 1 to 3 | Controlled corridor pilot | Test the exact payout path you plan to sell, plus fallback rails such as ACH where relevant; track completion time, failure reasons, manual intervention rate, and onboarding drop-off at the CIP step |

| Weeks 4 to 7 | AML and tax operations | Harden internal controls and escalation paths; collect W-9 and W-8BEN documents at onboarding and review reject reasons and resubmission patterns |

| Weeks 8 to 10 | Treasury and reconciliation stress | Simulate a payout that times out after submission, retry with the same Idempotency-Key, and confirm one economic result instead of duplicate payouts |

| Weeks 11 to 13 | Go or no-go decision | Set explicit thresholds for payout reliability, onboarding completion, and support ticket load; if a threshold misses, hold expansion, fix the failing step, and rerun the pilot |

Weeks 1 to 3#

Start with a controlled pilot in one or two target corridors and test the exact payout path you plan to sell, plus fallback rails such as ACH where relevant. In the U.S., test always-on behavior separately from ACH timing. FedNow is designed for near real-time transfers at any time, while ACH runs on defined processing and settlement windows.

Track per-rail behavior before you look at headline volume: completion time, failure reasons, manual intervention rate, and onboarding drop-off at the CIP step. Avoid calling the experience instant if only one leg is instant or fallback adds delay.

Weeks 4 to 7#

Before you widen access, harden AML and tax operations. Your AML program needs internal controls. Make the escalation path explicit enough that suspicious activity triage does not stall, especially with SAR timing that generally starts at 30 calendar days and cannot be delayed beyond 60 days when no suspect is identified.

Collect W-9 and W-8BEN documents at onboarding, not after first payout. Review capture quality using common reject reasons and resubmission patterns, and pause expansion if document friction is driving onboarding failure.

Weeks 8 to 10#

Now stress treasury and reconciliation with ambiguous failure scenarios. Simulate a payout that times out after submission, retry with the same Idempotency-Key, and confirm you get one economic result instead of duplicate payouts.

Keep an audit trail with payout intent ID, retry count, rail, and final state so finance and support can reconcile to the same ledger outcome.

Weeks 11 to 13#

Make the go or no-go decision only after setting explicit thresholds for payout reliability, onboarding completion, and support ticket load. If a threshold misses, hold expansion, fix the failing step, and rerun the pilot before increasing acquisition spend.

If you are turning this checklist into launch gates, map payout status handling, retries, and reconciliation workflows in the developer docs.

Conclusion#

The winning move in 2026 is usually not the biggest headline market. It is the next market where your payout rails, compliance stack, and treasury posture can handle real operating volume without breaking activation or overloading support.

Treat 2026 payment-volume signals as a confidence spectrum. The World Bank notes there are no reliable data sources to size online gig work precisely, and its estimate spans 154 million to 435 million workers. So use global volume claims as directional context, not budgeting-grade certainty.

Use macro payments growth as backdrop, not proof of platform payout readiness. The ECB reported 77.7 billion euro-area non-cash payments in H1 2025, up 7.7% year over year. Nacha reported 35.2 billion ACH payments in 2025, up 4.9%. But those figures do not confirm that your payouts in a specific country and vertical will clear fast, reconcile cleanly, or activate users at acceptable cost.

Your execution constraints are more concrete than market-size narratives. EU instant-credit-transfer rollout for euro-denominated transfers in the European Union is being pushed by the Instant Payments Regulation adopted on 13 March 2024. U.S. instant-rail operations can carry around-the-clock operating expectations. Settlement models that clear obligations individually can reduce settlement risk but increase liquidity needs, so treasury readiness is a launch gate, not a back-office detail.

Compliance also has to be gated market by market. FATF standards are not implemented identically across countries, so compliance and onboarding burden can vary even when demand looks similar.

A practical next step is to:

- Build a scored market shortlist using observed rail behavior, onboarding friction, compliance burden, and treasury fit.

- Run a time-boxed pilot (for example, 90 days) with explicit checkpoints: payout success rate, median completion time, failed-transfer investigation turnaround, onboarding completion, and support ticket load.

- Apply a hard go or no-go gate before full rollout.

In that pilot, verify returns, reversals, and timeout-and-retry behavior, not just first-payout success. Model mixed-rail reality too, since U.S. flows may still rely partly on ACH even when the product promise emphasizes faster cashout.

If reliability holds, scale. If it does not, quarantine the assumption. The credible path in 2026 is to scale what you can verify and avoid treating payment optimism as payout readiness.

For a vendor-risk and rollout view, read Choosing a Safer Fintech Stack in 2026.

Frequently Asked Questions

What are gig economy 2026 payment volume trends, and what is still unproven?

The defensible view is that activity looks meaningful, but a precise global 2026 gig payment volume is still unproven. Current data is still insufficient to accurately estimate total digital-platform employment. Use worker and platform ranges as context, not as a budgeting-grade baseline.

Is gig payment growth in 2026 established, or mostly inferred from broader payments data?

It is mostly inferred, not firmly established. Broader digital-payment growth and cashless trends support the direction of travel, but they do not prove platform-specific payout growth by country, corridor, or vertical. Treat your own rail performance and payout outcomes as the hard evidence.

How should operators compare countries when payment rails differ?

Compare countries on observed payout behavior, not on rail labels alone. SEPA Instant, Pix, RTP, and Same Day ACH have different timing and exception patterns. In pilots, prioritize receiving-side coverage, measured success rates, completion times, and failure recovery before you scale.

Which payment capabilities should platforms prioritize first in 2026?

Prioritize payout reliability, onboarding quality, and reconciliation that can handle retries and failures cleanly. If fast cashout is core to your offer, use instant or account-to-account rails where you can operate them consistently, with a fallback path where needed. Do not promise instant delivery if any required step can still delay funds.

What does always-on treasury mean in day-to-day marketplace operations?

It means treasury runs as a continuous liquidity operation instead of an end-of-day process. Always-on payout rails require funding readiness, balance monitoring, and clear controls for retries, returns, and settlement gaps. Day to day, teams need corridor-level funding rules and fast visibility into exceptions.

Do stablecoin rails materially improve cross-border gig payouts in most markets or only selected programs?

For now, they fit selected programs more than a default rollout across most markets. The article says systemic stablecoin rules are still being finalized in 2026 and warns that issuer dependence and rerouting need explicit testing. Corridor-by-corridor validation remains necessary, with a non-stablecoin fallback where required.

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- census.gov/library/stories/2025/07/nes-gig-economy.htmltrusted

- ecfr.gov/current/title-31/subtitle-B/chapter-X/part-1...trusted

- ecfr.gov/current/title-31/subtitle-B/chapter-X/part-1...trusted

- fdic.gov/news/financial-institution-letters/2024/fil2...trusted

- federalreserve.gov/paymentsystems/fednow_about.htmtrusted

- federalreserve.gov/paymentsystems/files/interest_on_rtp_joint_b...trusted

- irs.gov/forms-pubs/about-form-w-9trusted

- irs.gov/businesses/small-businesses-self-employed/re...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.

How to Respond to a Subpoena for Business Records

Move fast, but do not produce records on instinct. If you need to **respond to a subpoena for business records**, your immediate job is to control deadlines, preserve records, and make any later production defensible.

A US Expat's Guide to Investing in UCITS ETFs to Avoid PFIC Issues

The real problem is a two-system conflict. U.S. tax treatment can punish the wrong fund choice, while local product-access constraints can block the funds you want to buy in the first place. For **us expat ucits etfs**, the practical question is not "Which product is best?" It is "What can I access, report, and keep doing every year without guessing?" Use this four-part filter before any trade: