Quick Answer

In 2026, treat platform income as variable until your own settlement records show repeated, traceable net receipts that can survive a delayed payout without hitting essentials. Use growth numbers only for market context, split location-based work from project-based services, budget from settled receipts, cap exposure to any one platform, and pause expansion if you cannot trace funds from invoice or task to final receipt.

Why Platform Income Should Stay Variable Until Settlements Stabilize#

Treat platform income as variable until your own settlement records prove otherwise. If one delayed or partial payout would make you miss fixed monthly obligations, cap your exposure now and postpone scale.

That matters more than any headline about the Indian gig economy. The market context is real: the NITI report cited by PIB estimated 77 lakh workers in 2020-21 and projected 2.35 crore by 2029-30. But those figures are planning context, not cash flow proof. Even the headline percentages need labels. 6.7% refers to the non-agricultural workforce, while 4.1% refers to total livelihood. Use growth data to understand direction, not to underwrite your rent.

| Signal | Useful for | Cannot prove | What you should use instead |

|---|---|---|---|

| Workforce growth estimates | Market direction and category interest | Your payout reliability | Your last 3 to 6 settlement cycles |

| Platform dashboard earnings | Near-term pipeline visibility | Cash actually received | Reconciled settled amount in bank or wallet |

| Digital payments growth | Payment adoption context | Faster issue resolution | Your own exception and delay history |

| Positive market reports | Segment demand clues | Income stability across categories | Category-specific win rate, deductions, and settlement timing |

The rule is simple: controls before volume. Put these three checks in place before you accept more work from any platform or channel:

- Exposure cap: limit any one platform or payer to the share of income you can afford to see delayed.

- Verified-settlement budgeting: budget from net settled receipts, not from app balances or expected payouts.

- Stop signal: if essential expenses depend on funds you cannot trace from invoice to final receipt, pause expansion.

Build your evidence pack for outcomes, not record-keeping for its own sake. Keep the invoice trail so you can prove what was billed and when. Save FX evidence where relevant so you can explain the difference between quoted and applied conversion rates, along with fee lines. Track payout status until you know whether a payment settled, failed, or went partial, and who owns the complaint path if something breaks. Run a weekly exception review for anything outside the normal cycle. Keep a dated policy log so when a platform, bank, or payment partner changes rules, you can link that change to the transactions it affected.

That becomes important quickly. RBI complaint guidance expects facts backed by documents, and NPCI says complaint resolution sits with the member bank or institution. If you handle export receipts, map invoices to remittance references early because DGFT's eBRC tooling is built around invoice and remittance artifacts, not memory.

Before you compare numbers, fix one more thing: this market is not one uniform bucket. Category precision comes first, because NITI separates gig work into platform and non-platform groups.

If GST registration affects how you plan and price variable income, see GST Registration Decisions for Indian Freelancers.

Define the Indian gig economy before using the numbers#

Start with a hard split: do not treat local fulfillment work and project-based professional services as one category. If you merge them, you can misprice work, misread cash flow risk, and set the wrong exposure limits.

In this context, gig work is broad and includes flexible, short-term work, but for planning that definition is too loose. Use a practical classification lens before you use any statistic.

Separate the operating models first#

| Dimension | Location-based | Project-based |

|---|---|---|

| Work type | Location-based task execution | Project-based service delivery |

| Income pattern | Frequent task payouts | Milestone or invoice-linked receipts |

| Dispute exposure | App/rating frictions | Contract/payment-timing frictions |

| Pricing leverage | Mostly externally set pricing | Direct negotiation room |

This matters because gig workers are not a homogeneous group. The 2024 IDInsight study discussed by IDR was about two-wheeler, location-based delivery work in India, so use those findings for that segment only.

A common decision error is importing one segment's risk pattern into another. For example, automated delay penalties and rating reduction are grounded risks in delivery-platform contexts; they are not a universal proxy for every gig model.

Match the metric to the decision#

Use each number only for the decision it can support.

| Metric type | Use this metric for | Do not use it for |

|---|---|---|

| Location-based delivery/transport findings | Segment conditions, volatility, and delivery-specific dispute exposure | Pricing project services or forecasting invoice collection behavior |

| Project-service income data | Milestone/invoice budgeting, client concentration, pricing assumptions | Estimating app-driven delivery penalties |

| Broad policy estimates (for example, NITI Aayog, Economic Survey) | Category size context and directional market interest | Monthly cash budgeting, payout reliability assumptions, exposure caps |

| Studies split by active vs inactive workers | Participation and retention signals with clearer scope | Assuming all sampled workers are equally active earners |

In the cited 2024 study, "active" meant at least one delivery in the prior three months; "inactive" meant not driving for the platform in the prior nine to 18 months. If you skip that split, you can read retention dynamics as current earning strength.

Validate the source before it enters planning#

Before any number goes into your sheet, label five fields:

- Source class: policy brief, survey, academic study, platform report, or journalism

- Scope: delivery workers, platform workers, freelancers, or mixed categories

- Geography: India-wide, city-specific, or other

- Period: the actual collection window

- Decision use: budgeting, pricing, exposure limit, or context only

Paste this at the top of your model: "Scope: [segment] in [geography], using [period] data, for [decision only]." Keep it fixed, then read the next section's growth claims inside that scope.

Related: The High-Earning Indian Freelancer: A Demographic and Skills Analysis.

What the growth data says and what it cannot prove#

Use each growth figure for one specific decision, not as a blanket truth for your plan. Historical trends, local interviews, strike reporting, and long-range projections can all inform decisions, but only within the segment, geography, period, and use they actually cover.

The secondary-data line from 2.52 million in 2011-12 to 6.8 million in 2019-20, with 16.78% CAGR, supports a historical expansion signal. It does not establish a current 2026 worker count or your likely monthly receipts, pricing leverage, or payout timing. The $1847 billion by 2032 figure is also useful, but only as a projection for long-range context, not as current measured market size.

Apply the same filter to experience-based material. The 2025 study of 23 gig workers in Delhi is non-probability qualitative research, so use it to map risk categories such as economic stability, platform policies, job security, flexibility, and inconsistent work options, not national totals. Similarly, the report of more than 2,00,000 platform-based delivery workers on strike is a segment stress signal, not proof that all project-based freelance work is equally unstable.

Match evidence type to planning use#

| Evidence type | Appropriate use | Misuse risk |

|---|---|---|

| Secondary-data research or synthesis | Historical direction, category expansion, sector mix | Treated as a live baseline for your current revenue plan |

| Qualitative local research | Worker-experience risks and operational friction categories | Presented as nationally representative demand or earnings evidence |

| Policy publication | Directional context, category framing, policy attention | Used as a scope-matched forecast for your exact segment |

| Media synthesis | Event flags, labor tension, platform changes to verify | Repeated as settled fact without method, sample, or scope checks |

| Platform-reported figures | Segment behavior insight when method and coverage are clear | Assumed to represent all workers or the full market |

Validate before any number enters planning#

- Source type: Label it first (research, policy publication, media synthesis, or platform-reported figure).

- Scope: Confirm who is actually counted; do not treat unlike worker segments as interchangeable.

- Period: Separate observed history from forecast horizon.

- Geography: Keep local samples local unless you have support to generalize.

- Decision use: Assign one role only: market context, base-case input, upside boundary, or downside stress.

Keep one definition check in your workflow: in the IDInsight material referenced by IDR, "active" means at least one delivery in the prior 3 months, while "inactive" means no driving in the prior 9 to 18 months. If you skip those labels, you can misread participation categories as current earning strength.

For forecasting, tie your base case to current, scope-matched, validated inputs. Use historical growth lines to sanity-check direction, long-horizon projections as an upside boundary, and insecurity, policy/platform friction, and labor-tension signals as downside stress inputs. If a figure does not match your defined scope, treat it as context only until the current validated input is verified from source records.

Where growth is concentrated and why that matters for risk#

If your work is growing through convenience apps, treat that as activity volume, not proof of reliable take-home income. In this market, a lot of visible expansion is concentrated in platform-mediated, convenience-led services such as delivery, ride-hailing, beauty, domestic care, and field tech support.

Names like Swiggy, Zomato, Blinkit, BigBasket, and Zepto are useful as category markers, not as a model for all freelance work. That model is typically task-based, paid per gig, and structured around independent-contractor arrangements. Do not use it as a proxy for project-based consulting, design, writing, or software work, where pricing control, client terms, and payment flow work differently.

| Factor | Local fulfillment via apps | Professional project work |

|---|---|---|

| Payout predictability | Task-linked and cycle-variable | Usually tied to invoice or milestone terms |

| Dispute exposure | More small settlement exceptions to monitor | Fewer but larger scope or payment disputes |

| Pricing leverage | Lower when platform rules set structure | Higher when you set scope and terms |

| Revenue stability | High task volume can still settle unevenly | More stable when contracted across clients |

Your operating check is simple: validate net settled outcomes, not task counts or dashboard activity. A high-activity week can still underdeliver if credits arrive late, land short, or include adjustments you need to chase. Track what actually settles to your bank or wallet against statements, including reversals, deductions, and unpaid items.

Use this monthly risk-control framework:

- Track app income and project income separately.

- Use segment-specific assumptions for payout timing and volatility.

- Maintain a backup channel so one platform does not carry fixed obligations.

Once you separate visible volume from settled cash, the next decision is clearer: should platform income stay variable, or is it stable enough to include in core revenue planning?

For a step-by-step walkthrough, see Future of Freelance Work in 2026 for Cross-Border Hiring Decisions.

Should you rely on platform income as your primary revenue stream#

Treat platform income as core revenue only after it passes a fail test: one delayed payout, hold, or account issue from your largest source must not disrupt essentials. If that test fails, keep that channel in your variable bucket, even in a busy month.

| Platform | Timing detail | Note |

|---|---|---|

| Upwork | Billing cycle runs Monday 00:00 UTC to Sunday 23:59 UTC | Five-day security period applies |

| Fiverr | Revenue becomes available after 14 days | 7 days for eligible tiers |

| Freelancer.com | Milestone funds can remain locked | Until release or dispute completion |

Under India's legal definitions, gig and platform work sit outside a traditional employer-employee relationship, so do not assume salary-like payment regularity. Platform timing rules are part of the operating model: Upwork runs Monday 00:00 UTC to Sunday 23:59 UTC billing cycles and then applies a five-day security period; Fiverr says revenue becomes available after 14 days (or 7 days for eligible tiers); Freelancer.com milestone funds can remain locked until release or dispute completion.

| Decision lens | Single-platform heavy | Multi-channel mix |

|---|---|---|

| Speed to volume | Usually faster because demand is already aggregated | Slower ramp because you source work across channels |

| Pricing power | Lower when platform terms shape job economics | Better when you can price by scope, client, or niche |

| Payout risk | Higher if one hold, deactivation, or dispute blocks most inflow | Lower if one channel delay does not stall the month |

| Operational overhead | Simpler day to day | Higher admin load across clients, statements, and follow-ups |

Use a practical stress test, not a headline estimate:

- Pick your biggest current source and model one delayed-payout cycle using that platform's real hold mechanics.

- If you need a cutoff, mark the current policy threshold as pending verification rather than inventing a universal rule.

- Check whether essentials still clear from other settled cash, without borrowing or rolling payments.

If that answer is no, do not reclassify platform income as core.

Keep your monthly concentration review short and evidence-based:

- List all income sources and identify the top source by settled amount, not booked work.

- Record payout lag from completion to usable funds.

- Track deductions, revised charges, reversals, and fee changes.

- Log open disputes, cancellations, and held milestones with ticket IDs or platform references.

- Apply action triggers: choose Reduce exposure if one source can affect essentials or if lag/disputes worsen; choose Hold steady only when settlements stay clean across repeated cycles and one delay no longer breaks the month.

This failure mode is real. Uber's India terms allow charge revisions and termination of access, and its community-guideline enforcement can remove account access. That does not mean every platform behaves the same; it means sole-platform dependence creates a real failure mode. Keep a payout paper trail for each cycle: completion date, platform statement, deduction lines, dispute reference, and final bank or wallet credit.

Write your stop rule now: if payout uncertainty starts touching rent, payroll, debt, or other essentials, freeze additional dependence on that platform and route new revenue through diversified channels before scaling again.

Build your cross-border money operations before volume grows#

Set up your cross-border payment operations before you scale volume, or routine delays will turn into delivery risk, reconciliation noise, and longer disputes.

| Rail | Timing | Cross-border note |

|---|---|---|

| UPI | Real time | Domestic speed does not automatically carry into cross-border payouts |

| NEFT | 24x7 in 48 half-hourly batches | Domestic speed does not automatically carry into cross-border payouts |

| RTGS | 24x7 for domestic transfers | Domestic speed does not automatically carry into cross-border payouts |

India's domestic rails are fast, but that speed does not automatically carry into cross-border payouts. UPI is real time, NEFT runs 24x7 in 48 half-hourly batches, and RTGS is 24x7 for domestic transfers. Cross-border flows still face structural limits on cost, speed, access, and transparency, and recent global KPI updates still show uneven progress across corridors. Use a simple rule before you promise any receipt timeline: verify the exact corridor, currency pair, settlement path, and current provider or bank eligibility. Even India-Singapore UPI-PayNow is corridor-specific, and participating bank availability can change over time.

Treat your evidence pack as a live operating record, not month-end cleanup. For each transaction, capture invoice reference, collection reference, conversion reference, payout reference, timestamped status changes, applied FX rate, fees, and final net receipt. Keep this in one shared transaction record across finance and delivery, and assign one owner to update exceptions until closure. If you keep only the final bank credit and lose intermediate IDs, shortfalls and delays become much harder to resolve.

| Breakpoint | Likely cause | Early warning signal | Immediate action |

|---|---|---|---|

| Collection received, no onward movement | Corridor or account constraint | Status stalls after receipt | Re-check route eligibility and open a provider ticket with all reference IDs |

| FX amount differs from expectation | Quote expired or fees applied | Net amount falls outside tolerance | Pull conversion record and compare approved rate vs applied rate |

| Payout pending beyond expected window | Downstream bank or provider hold | No final credit confirmation | Stop re-promising timelines and escalate before reporting cut-off |

Run month-end in a fixed sequence: invoice issued, funds collected, conversion completed, payout settled, exceptions closed, then reporting. Do not report with open exceptions unless they are explicitly tagged and carried, or the next cycle will be spent unwinding prior-period noise. If you want fewer handoffs, Gruv is one optional way to keep invoicing, FX, payouts, and records in one flow. Next, make ownership explicit: who runs the compliance checks that prevent avoidable holds and freezes?

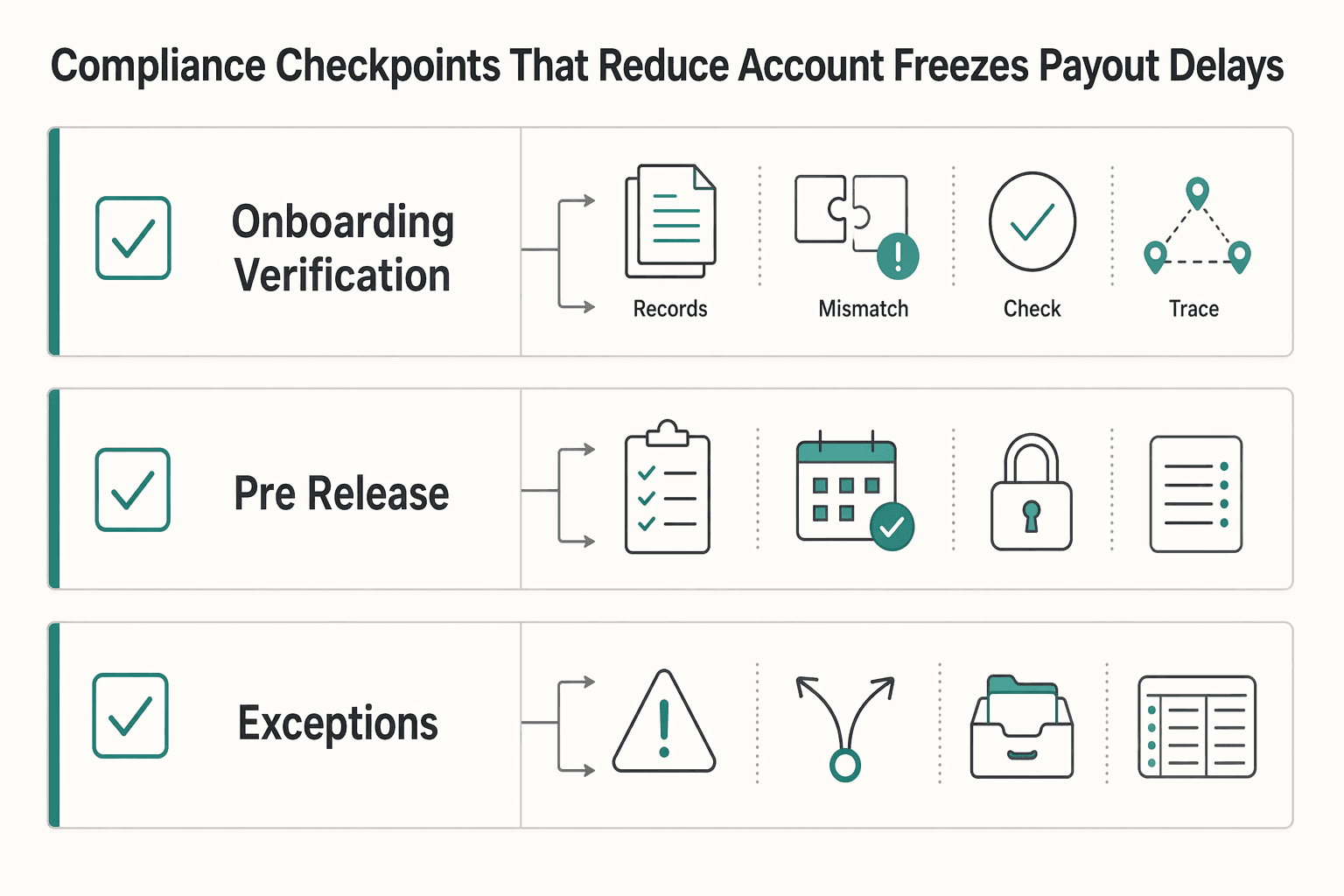

Compliance checkpoints that reduce account freezes and payout delays#

Your payout reliability depends on compliance ownership, not payment-rail speed alone. A fast route still fails when verification is incomplete, an account is paused, or a provider places settlement on hold.

Run the same three checkpoints every time: onboarding verification, pre-release eligibility, and exception routing with a decision log.

| Checkpoint | Required evidence | Common failure mode | Corrective action |

|---|---|---|---|

| Onboarding verification | KYC record, identity and address match, tax-profile artifacts, consented CKYCR pull where applicable, masked account record | Transactions start before mandatory KYC is complete, or records are stale and fragmented | Stop release, refresh from CKYCR or KYC Identifier where available, complete missing fields, and timestamp approval |

| Pre-release eligibility | Invoice, payout reference, beneficiary details, current provider status check, route/corridor eligibility confirmation, approval log | Existing setup is assumed to be valid, or a new account requirement is missed and payouts pause | Recheck provider status and route rules before release; if requirements changed, hold payout until the evidence pack is complete |

| Exception routing | Hold reason, settlement report, status history, requested documents, reviewer notes, decision log | A flagged payout drifts between teams, ownership is unclear, and release happens without clear basis | Move it to one named queue, assign owners, collect missing evidence, and set escalation timing after you confirm the current aging limit from policy or source records |

Use a simple role model so flagged payouts do not move without accountability. Your primary owner gathers evidence and records the first decision. Your backup approver releases only when the file is complete. Your escalation owner handles aged or disputed exceptions and is the only person who can approve an override after rationale is documented.

Treat this as ongoing control, not a one-time onboarding task. RBI requires on-going due diligence, and the June 12, 2025 KYC update noted large pendency in periodic updation. Monitor concrete trigger categories: new payout destinations, corridor changes, unusual timing, sudden value-band shifts, missing tax-status information, new document requests, and provider states like settlement hold or paused payouts. When risk signals shift, hold, review, and document the rationale before release.

Give one check extra weight: verify your provider's current RBI status before onboarding or expansion. Cross-border facilitators are under RBI regulation through the PA-CB regime, and the RBI PA status list as of 16.03.2026 includes entities that cannot onboard new merchants until advised otherwise.

Keep exception review short and recurring. Review open holds, missing documents, and aging items on a fixed cadence, then escalate unresolved cases instead of forcing release to hit a deadline. Once these controls hold, move to the next risk: what to price into contracts when market conditions turn volatile.

Red flags from quick-commerce competition you should price into every contract#

Treat quick-commerce speed pressure as margin risk, not free upside. If a client, platform, or channel starts treating rapid hyperlocal fulfillment as the baseline, update your contract terms before you accept more volume.

Assume tighter speed expectations will raise execution risk unless the commercial terms change too. When response windows shrink, your downside usually comes from extra coordination, more edge-case handling, and more time spent proving what was delivered.

Keep the operating-model context tight. NITI Aayog's June 2022 report describes platform activity across transport, retail, personal care, and home care, and explicitly asks readers to check references and footnotes when claims are unclear. Use that as your checkpoint: signals from retail delivery may inform your risk screen, but they are not automatically transferable to every platform segment or freelance service in 2026.

Match each speed promise to three items in the same contract: compensation, dispute pathway, and scope boundary. If responsiveness tightens, raise rates, define completion evidence, and state what is out of scope when delays come from client inputs or platform-side changes.

| Signal | Why it matters to your margin | Evidence to collect | Default response |

|---|---|---|---|

| Tighter turnaround or instant-response expectations | More standby exposure and higher failure risk | Written response-time ask, revision history, task timestamps, acceptance criteria | Reprice |

| Pay model changes with short notice or vague logic | Realized pay becomes harder to forecast | Prior and current rate cards, notice emails, settlement statements, payout deltas | Reprice or decline |

| Rising disputes, reversals, or deductions without clear rule mapping | Admin load rises while net revenue falls | Dispute log, deduction codes, screenshots of terms, dated support replies | Narrow scope or decline |

| Open-ended coverage asks across more zones, hours, or task types | Capacity drifts beyond the original pricing basis | Contract version, expanded coverage requests, staffing assumptions, exception records | Narrow scope |

Write escalation as policy language, not tribal knowledge. Example: verify the current consecutive-cycle trigger from platform, contract, or policy records before use; if net realized pay, deduction frequency, or unresolved disputes worsen across that verified window, pause new volume on that channel, collect written clarification, and require approver signoff before restart. Keep dated settlements, task logs, notices, and decision records so the pause is auditable.

For renewals and new deals, keep one safeguard non-negotiable: if responsiveness expectations tighten, rates, scope limits, or revision clauses must tighten in the same agreement.

Related reading: High-Earners vs. Low-Earners: A Breakdown of Platform Choices for Indian Freelancers.

The takeaway for a lower-risk next step#

Treat growth as demand, not safety. You should scale only when your own operating evidence is stable, because strong market activity can coexist with payout uncertainty, unilateral rule changes, and uneven worker protection.

Recent reporting shows that tension. On 31 December 2025, Swarajya reported over 7.5 million orders and more than 4.5 lakh active delivery partners, while BBC later reported a New Year's Eve strike involving about 200,000 gig workers. BBC also reported protections tied to workers who clock 90 days on platforms each year, but described the push to stop 10-minute deliveries as not yet fully in place. So policy direction matters, but implementation and day-to-day outcomes can lag.

Use this go/pause standard before adding volume:

- Go only when concentration exposure is tolerable. If one platform or client still carries too much of your monthly cash needs, hold growth.

- Go only when contract changes are survivable. If ratings, scope, deductions, or termination can shift without clear notice and you have no protection in writing, pause.

- Go only when payout reliability is proven in your records. Check invoice or task ID, payout reference, settlement date, and net amount received across consecutive cycles.

- Go only when exception resolution is working. If the same dispute reason repeats, ages badly, or has no named escalation owner, do not add volume.

Set the hard trigger as policy now: before using it, verify the essential-obligation definition and consecutive-cycle trigger from policy, contract, or source records; then pause expansion when payout uncertainty, unexplained deductions, or unresolved exceptions threaten that verified obligation for that verified window.

Record every scale, hold, or pause decision with date, rationale, evidence checked, and next review point so you correct early instead of after losses compound.

For the TDS side of freelancer payments, see A Guide to TDS (Tax Deducted at Source) for Payments to Indian Freelancers.

Frequently Asked Questions

What counts as the Indian gig economy in 2026?

In 2026, the core definition is work done outside a traditional employer-employee relationship, with platform work arranged through an online platform outside that relationship. For planning, split location-based work from remote online or project-based services because the operating risks differ. Do not import delivery-market assumptions into project work without checking your own payout traceability and dispute pattern.

How large is this workforce, and why do the numbers keep changing?

The commonly cited figures are estimates and projections, not a settled 2026 census. The NITI-linked numbers are 7.7 million for 2020-21 and 23.5 million projected for 2029-30, and the report says it uses an indirect approach and still needs better direct worker data. Use those figures for context only, then separate platform task work from project-based services before comparing growth, earnings stability, or bargaining power.

Does growth mean work is getting more formal and safer?

No. The Code provides for a Social Security Fund for gig and platform worker welfare, and aggregator contributions are framed at 1 to 2 percent of annual turnover, capped at 5 percent of payments made or payable, with the start of central contribution dependent on notification. Compliance may be evolving, but day-to-day payout reliability and worker protections can still differ sharply by segment.

What should you make of protests, strikes, or delivery-sector stress signals?

Treat protests, strikes, and delivery-sector stress as segment-specific pressure, not as a universal verdict on all freelance work. Location-based platform services face different speed, safety, and pay-structure pressures than remote project work. Use those headlines as a cue to review exception handling and contract scope, not as proof your consulting or creative work has the same economics.

Can platform work be your primary income source?

Yes, but only after your records show stable concentration risk, payout traceability, and exception handling. Task-based platforms can change rules, deductions, or service expectations faster, while project-based services may give you more room to define scope and completion evidence. If one delayed settlement would disrupt essentials, keep that income in your variable bucket.

What should you set up first to reduce payment and compliance risk?

Start with documents and ownership, not more tools. Keep a clean chain from invoice or task record to payout reference, settlement date, net amount received, and any exception note, and assign one named person to own compliance updates and account changes. NEFT is available round the clock as a domestic fallback, but national payment growth does not guarantee your individual payout timing. Also verify the live law status where you operate before assuming what applies.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- academia.edu/1308432/Becoming_other_From_social_interacti...trusted

- consilium.europa.eu/de/documents-publications/library/library-bl...trusted

- consilium.europa.eu/de/documents-publications/library/library-bl...trusted

- digitallabour.ilo.org/legislation/platform-based-gig-workers-regis...trusted

- ecommons.cornell.edu/server/api/core/bitstreams/38d23bff-2206-4bf...trusted

- ilo.org/digital-labour-platformstrusted

- pib.gov.in/PressReleasePage.aspxtrusted

- pmc.ncbi.nlm.nih.gov/articles/PMC6380453trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Indian Freelancer Payment Analysis That Protects Net INR

For freelancers in India, the number that protects cash flow is the net INR credited to your bank, not the USD amount on the invoice. Start from that outcome and work backward through every payment decision.

High-Earning Indian Freelancers by Demographics and Skills

A useful Indian freelancer market analysis starts with one practical move: classify each number before you trust it. Put every claim into one of three buckets - market projection, platform activity, or worker outcome, then decide whether it changes what you do now.

Cybersecurity for Freelancers Who Need Reliable Client Delivery

If you want reliable delivery, start with continuity, not tools. In practice, that means protecting the accounts, devices, files, and payment paths you need to deliver work, communicate with clients, and recover without making the disruption worse. Incidents often hit operations before they look like an IT problem.