Quick Answer

Use a single worksheet with one send amount, one currency pair, and timestamped quotes, then keep explicit fees separate from conversion impact until the final total. Tag every row as `complete`, `partial`, or `missing`, and treat unverified charges as `unknown` rather than zero. Normalize all rows into one reporting currency, compare effective cost percentage, and approve only comparable entries. After settlement, classify variance as fee drift, rate movement, timing movement, or intermediary deduction before choosing the next route.

Why all-in cost matters more than headline fees#

Headline fees can understate true cost. The figure that protects margin is the net amount that lands with the recipient after conversion, transfer charges, and any downstream deductions.

Cross-border payments can pick up costs after the first quote, so a headline-fee view can create false certainty. Use a total-cost view and keep each cost line separate until final approval. That gives you a clean way to explain the decision to a client, a teammate, or your future self when outcomes differ from the estimate.

Use one repeatable worksheet for every send and keep these lines separate before you total them:

- visible transaction fees

- FX spread or conversion impact

- post-send variance between estimate and settlement

This structure is what makes unlike options comparable. Different payment routes may show price in different formats, but each still resolves to the same question: what did it cost to deliver the funds? One 2026 vendor analysis reported directional ranges of 1-2% cross-border fees, 2-4% FX margins above mid-market rates, and provider differences above 2% on international transactions. Treat those figures as directional context, not planning truth, then validate against your own settled history.

The practical benefit is decision quality under pressure. When an invoice is due and timing is tight, you can still choose based on complete cost rather than the most attractive first screen.

What to prepare before you run the numbers#

Start with one complete input packet. Partial inputs can make estimates look exact, then fall apart when you compare providers side by side.

| Field | What to capture | Notes |

|---|---|---|

| Send amount | Use the same send amount for every quote row | Keep the same fields for every row |

| Expected receive amount | Log the expected receive amount | Expected net amount becomes comparable after normalization |

| Listed fees | Log any route-specific fee lines shown in the quote | Keep route-specific pricing notes separate from core quote rows |

| Stated exchange rate | Log the stated exchange rate | Add a mid-market reference so rate movement is separate from provider fees |

| Payment method | Log the payment method for each row | Some ways to pay are free while others have a fee |

| Timestamp | Capture each quote in one short window | If a quote is missing a field, mark it now rather than fixing it from memory later |

| Completeness | Mark each row complete, partial, or missing | This helps prevent choosing a low quote that is missing key cost inputs |

Your packet should include the invoice amount, payer currency, recipient currency, payment method, and any route-specific fee lines shown in the quote. Keep those fields in one place before you open any calculator. If you collect quotes first and patch details later, you will often forget which assumptions belonged to which quote window.

Then capture comparable quotes in one short window. Pull at least two provider views, then log the same fields for every row: send amount, expected receive amount, listed fees, stated exchange rate, payment method, and timestamp. Add a mid-market reference so you can separate rate movement from provider fees. If one provider quote is missing a field, mark it now rather than fixing it from memory later.

Keep route-specific pricing notes separate from the core quote rows. Wise states fees vary by currency, and some ways to pay are free while others have a fee. On Wise US pricing pages, examples shown include send or convert pricing from 0.57%, a 6.11 USD fixed fee for receiving USD wire and Swift payments, and transfer-fee discounts after 25,000 USD equivalent. Wise also states it uses the live mid-market rate plus an upfront fee. Treat those as row notes, not universal assumptions for every route.

Add completeness fields before you make pricing decisions. Record whether each row is complete, partial, or missing, and note any unresolved route-specific fee or method details. This helps prevent you from choosing a low quote that is missing key cost inputs.

Set one base reporting currency and normalize every quote into it. Without normalization, two quotes can both look favorable because each is framed differently. With normalization, effective cost percentage and expected net amount become comparable.

Before you move to ranking, run one quick packet check:

- each quote has a timestamp from the same capture window

- each row uses the same send amount and currency pair

- each row has a visible confidence state such as

complete,partial, ormissing - each row includes payment method and route-specific fee notes

One packet, one quote window, and one reporting currency turns a quote exercise into a reliable decision input.

Set the payment boundary so your calculation is honest#

Set the boundary before you rank options. If a cost line is undefined or unverified, the estimate is not all-in.

- Define all-in lines in writing.

List sender fee, recipient fee, transfer fee, and FX impact. If relevant, include possible intermediary-bank, foreign-transaction, or ATM/card-access charges as separate lines until verified. Also state what is out of scope for this send so costs are not quietly added later.

- Separate rails before pricing.

Keep card-based rails separate from bank transfer rails. Fee ownership, settlement timing, and disclosure style can differ by rail, so mixed rows create false comparisons.

- Treat unknowns as unknowns, not zero.

If you cannot verify whether a fee is included, add a contingency line marked unknown. Do not let a blank field become implied zero. If margin is tight, pause approval until fee ownership is explicit.

- Mark corridor uncertainty and confidence.

Call out country-pair uncertainty and possible receiving-bank behavior as explicit unknowns. Then label confidence as high, medium, or low based on verified lines.

A useful way to keep this practical is to add a short decision note under each candidate row. Example note style:

- what is verified

- what is assumed

- what is unknown and priced as risk

This boundary step removes avoidable surprises. Without it, teams can end up arguing about outcomes after settlement. With it, uncertainty is visible and priced before release.

If a client asks why your selected route is not the lowest headline-fee option, this section gives you the answer in plain language. You chose the route with the best expected net result under known constraints, not the route with the thinnest top-line number.

Pull comparable quotes from each provider in one session#

Collect quotes in one sitting with identical inputs. If you spread collection across different times or assumptions, you are measuring timing noise, not true price differences.

- Capture snapshots close together in time.

Run each provider quote flow back to back with the same send amount and currency pair. Save each snapshot with a timestamp when available. If a tool does not show a timestamp, log your capture time and treat that row as lower confidence.

- Log the same fields for every row.

Use one template for send amount, delivery amount, listed fees, stated exchange rate, payment method, and quote timestamp. Note whether fees are shown upfront or folded into the exchange rate, then normalize if any row uses a different field set.

- Flag quote completeness before ranking.

Mark each row as complete, partial, or missing. Use partial when the rate is visible but the fee stack is incomplete. Use missing when key fields are absent.

- Apply a freshness gate for final decisions.

Because rates can change, treat stale or undated rows as non-comparable and recapture the full set when needed. Keep discount-eligibility notes separate so row-level ranking stays clean.

A practical capture sequence helps when you are moving fast:

- lock the test case inputs in your worksheet first

- open all quote views in parallel tabs

- capture each row within one short window

- tag confidence immediately after each capture

- freeze ranking until all required rows are complete

Common failure mode: someone updates one row later with a new timestamp and leaves the rest untouched. That mixed set can look precise but is not fully comparable. If one row is refreshed, refresh the full set or mark the table non-comparable.

Do not approve on mixed-quality evidence. Complete missing fields or exclude those rows from final ranking and document why.

Calculate FX impact separately from explicit fees#

Keep conversion impact and explicit fees separate until the final total. Because currency values can shift, combining these too early can hide what is driving total cost.

- Anchor each quote to one reference rate and time.

Use one stated reference rate for the same currency pair and capture it in the same session as provider quotes. Log both timestamps so any drift is visible.

- Track conversion-rate gap as its own line.

Compare each provider conversion rate to the reference rate on the same principal amount. Record the gap as implied FX impact.

- Keep visible charges in a separate fee line.

Record foreign transaction fees and listed transfer charges in their own bucket. A row with a low displayed fee can still end up costing more when conversion impact is higher.

- Confirm whether payout already embeds conversion cost.

Check whether the quoted recipient amount already includes conversion impact. If your worksheet math and the quoted payout do not reconcile within rounding tolerance, mark the row partial and refresh before approval.

When two rows are close on headline fee, this separation can reveal the deciding factor. One route may look cheaper until conversion impact is pulled out and compared directly.

A simple review order helps:

- verify reference-rate timestamp

- verify provider-rate timestamp

- calculate implied conversion impact

- add explicit fee line

- total only after both lines are verified

This also improves post-send learning. If settlement underperforms, you can check whether the gap came from fees, rate movement, or both. Without separated lines, variance is harder to diagnose and your next routing decision is less reliable.

Use one approval rule: if conversion detail is missing, stale, or unclear, do not decide from headline fees alone.

Build an apples-to-apples comparison table before choosing#

Build the table first, rank second. Ranking before the table is complete creates false confidence.

- Step 1: Lock one shared test case before collecting quotes.

Use the same send amount, currency pair, recipient country, payout method, and quote window for each option you compare (for example, Tipalti, Wise, and a card-network path). Add target credit date. A row is valid only when it includes quote timestamp, stated rate, send amount, recipient amount, and listed fees.

- Step 2: Apply one cost formula to every row.

Use total estimated cost = explicit fees + FX markup + expected downstream deductions. Then calculate effective cost % = total estimated cost / send amount. Keep row notes specific and short. For Wise, examples shown include pricing from 0.57%, a 6.11 USD fixed fee for receiving USD wire and Swift payments, and discount eligibility after 25,000 USD equivalent.

- Step 3: Score non-price risk alongside cost.

Add settlement predictability, disclosure clarity, and hidden downstream deductions risk as decision columns. Convert those into one confidence score per row. If cost is close, choose the row with clearer disclosure and steadier settlement behavior.

- Step 4: Rank only after unknowns are resolved.

Do not approve from headline fee percentage alone. Finalize ranking only when rows are complete in the same quote window, or when unresolved items are explicitly priced as risk.

| Rank | Option | Total estimated cost | Effective cost % | Settlement predictability | Disclosure clarity | Hidden downstream deductions | Confidence score |

|---|---|---|---|---|---|---|---|

| TBD | Wise | send fee + any applicable fixed receive fee + other listed charges | Total / send amount | - | - | - | - |

| TBD | Tipalti | all costs shown in the quote window + any stated deduction items | Total / send amount | - | - | - | - |

| TBD | Card-network path (if used) | quoted conversion + stated issuer/network fees + downstream charges | Total / send amount | - | - | - | - |

To keep the table useful month after month, add a short note to each row each cycle that answers two questions: what changed, and why the rank moved. That makes later reviews faster and helps prevent repeating an old mistake when team members change.

If an option wins on cost but loses badly on confidence, call that out directly. A low-cost row with weak confidence is a candidate for controlled testing, not an immediate default for high-priority invoices.

Choose payment rail with explicit if-then rules#

Use if-then rules so rail choice is consistent under pressure. You should be able to explain the choice in one sentence before you click send.

| If | Then | Notes |

|---|---|---|

| Client pays a formal invoice to a bank account | Default to bank wire or account transfer unless card acceptance is required | Card-processing flows can add authorization, issuer fund collection, and merchant reimbursement steps |

| Receiving details are stable and repeat payments are expected | Test Virtual Accounts only where supported | Keep it only if reconciliation gets cleaner with fewer manual fixes and fewer status disputes |

| Collection and payout are platform-managed | Compare Merchant of Record and direct routing using statement-level visibility before rollout | Decide who invoices, who receives funds first, and who releases payout |

| Card rails are used | Treat downstream cardholder-side costs and cross-border variability as risk items | Include possible foreign transaction fee or ATM surcharge behavior as uncertainty |

- If the client pays a formal invoice to a bank account, then default to bank wire or account transfer unless card acceptance is required.

Card-processing flows can add steps such as authorization, issuer fund collection, and merchant reimbursement, so treat timing and final net amount as uncertain until you prove that path in your corridor and invoice pattern.

- If receiving details are stable and repeat payments are expected, then test Virtual Accounts only where supported.

Run a controlled comparison against your current route and keep it only if reconciliation gets cleaner with fewer manual fixes and fewer status disputes.

- If collection and payout are platform-managed, then compare Merchant of Record and direct routing using statement-level visibility before rollout.

Decide who invoices, who receives funds first, and who releases payout. Map each settlement line to your all-in table before switching the default rail.

- If card rails are used, then treat downstream cardholder-side costs and cross-border variability as risk items.

Include possible foreign transaction fee or ATM surcharge behavior as uncertainty rather than assumptions, and account for regulatory, geopolitical, and exchange-rate volatility.

A practical rule card for your worksheet can look like this:

- invoice to bank account and no card requirement: transfer route first

- card required by payer: card route with extra uncertainty pricing

- repeated corridor with stable details: test and keep only if reconciliation improves

- unresolved downstream charges: hold default change and keep current route

This keeps route choice tied to evidence rather than convenience. It also helps prevent constant rail switching, which can create more variance than it removes.

Run pre-send risk checks to avoid holds, returns, and delays#

Before release, run a pre-send gate that validates payment data, compliance readiness, and any required profile documents. Common delay sources include compliance checks and incomplete or incorrect information, so catch issues before you send.

| Check | What to confirm | If not clear |

|---|---|---|

| Beneficiary details | Beneficiary name, account number, country code, and required bank fields match the invoice packet and saved payee record | Stop and fix before send |

| Pre-validation | Run a pre-validation check at initiation for core payment data, with bank-side collaboration where available | If result is warning or fail, stop and fix before send |

| Compliance readiness | Required checks are cleared for the selected route before cutoff | If any item remains pending near cutoff, hold release, reset expected credit timing, and communicate immediately |

| Tax and profile documents | Verify tax or profile validation status where required for this payment type | Verify status before approval |

- Validate beneficiary details before release.

Check beneficiary name, account number, country code, and required bank fields against your invoice packet and saved payee record.

- Run pre-validation and record the result.

Run a pre-validation check at initiation for core payment data, with bank-side collaboration where available. If the result is warning or fail, stop and fix before send.

- Confirm compliance readiness before cutoff.

Treat compliance checks as a release gate. Confirm required checks are cleared for the selected route. If any item remains pending near cutoff, hold release, reset expected credit timing, and communicate immediately.

- Check tax and profile documents where required.

If the provider or payer requires tax or profile validation for this payment type, verify status before approval.

Add one ownership line to each send so responsibility is clear:

- who validates payee details

- who confirms readiness fields

- who approves release timing

- who sends client timing updates when conditions change

This simple ownership split reduces last-minute ambiguity. It can also shorten resolution time when a warning appears close to cutoff.

Common failure mode: all checks are done, but not in one record. The send goes out, then no one can prove what was verified at approval time. Keep the checks, results, and owner names in one place so the release decision is auditable.

Final release rule: send only when all four checks are green in one record.

If you want a deeper dive, read Separating Business and Personal Finances: An Important Step for LLCs.

Execute and capture an evidence pack you can audit later#

After execution, the record becomes your control point. Save enough evidence that another person can reconstruct what happened without guesswork.

- Save one complete record under document and record controls.

For each case, keep the key evidence together in a controlled file.

- Track full status timeline with timestamps.

Log each status transition so the sequence can be followed during audit.

- Reconcile expected versus actual outcomes in the same record.

Include fields for expected outcome, actual outcome, and a clear variance note.

- Maintain a reusable exception log, including complaints.

Track exceptions and complaints in one running log that can support internal audit and information supplied for management review.

To keep this useful, store records in a consistent naming pattern and include a short plain-language summary at the top of each file. Summary fields can include process scope, approval timestamp, expected outcome, actual outcome, and variance source.

A strong record can shorten stakeholder communication. If outcomes shift, you can explain what changed with evidence rather than with a generic apology.

If your record cannot show what changed, when it changed, and what outcome landed, it is not complete.

Reconcile estimate vs actual and improve the next send#

Use reconciliation to improve the next routing choice. Compare each settled transfer to its original quote, classify the variance source, then apply the result to the next send in the same corridor.

- Match estimate to settlement line by line.

Keep quote timestamp, quoted recipient amount, listed fees, quoted rate, confirmation reference, and final bank credit in one record. Classify each gap as fee drift, exchange rate markup drift, timing movement between quote and execution, or unexpected intermediary bank fee. If exchange rate markup was captured at quote time, compare it with the effective settled rate during review. Checkpoint: the classified buckets should add up to the total estimate-versus-actual difference.

- Set tolerance before judging performance.

Define corridor-level tolerance using your own risk appetite, and track it as amount plus percent of send. Use the same tolerance method for small and large transfers so performance comparisons stay fair. If a corridor exceeds tolerance repeatedly, use that as your trigger to test another provider or rail on the next transfer.

- Keep a monthly provider scoreboard.

Score providers on predicted-net accuracy, speed, and variance stability using reconciled sends, not memory.

| Provider | Predicted net win rate | Speed (planned vs actual credit date) | Variance stability | Notes |

|---|---|---|---|---|

| Provider A | % of sends where actual net stayed within tolerance | % on-time settlements | Variance pattern by corridor | Most common mismatch reason |

| Provider B | Same metric | Same metric | Same metric | Flag missing quote inputs |

| Current bank or rail | Same metric | Same metric | Same metric | Track intermediary deductions separately |

- Apply one routing rule to the next send.

For each corridor, choose the provider with best predicted-net win rate and variance stability, then use speed as the tie-breaker when timing is tight. At month end, update thresholds and exception notes so the next transfer starts from observed results.

A useful review rhythm is monthly ranking plus immediate review for large misses. Monthly review keeps the big picture stable. Immediate review stops a repeated error from spreading into the next cycle.

This is where the process turns practical: you are no longer estimating in isolation. You are building a feedback loop from estimate to settlement to next decision.

Related: The Best Web3 and Crypto Job Boards for Freelancers.

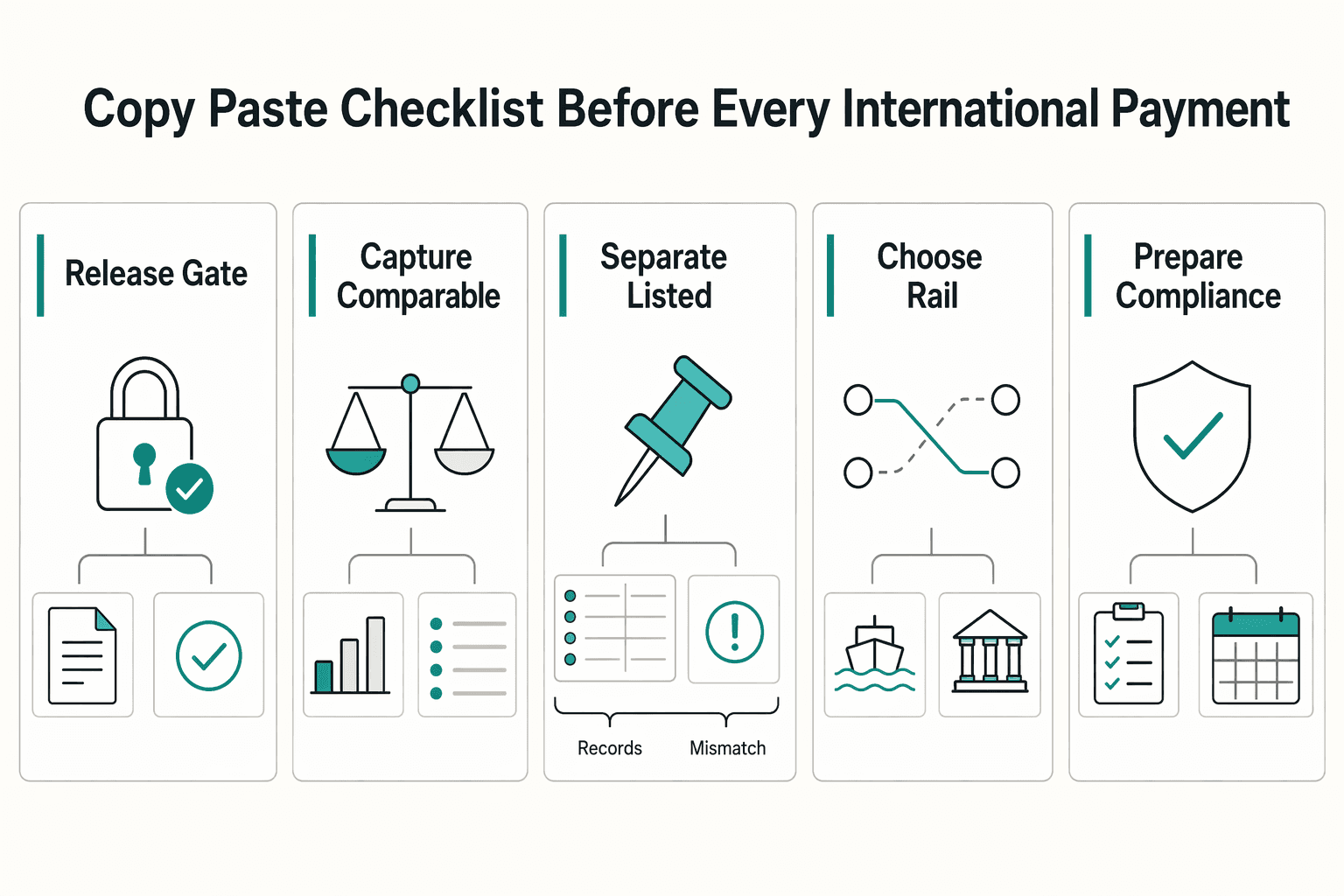

Copy and paste this checklist before every international payment#

Use this checklist as your final pre-send gate each time you calculate international payment cost. The goal is a payment instruction that can be processed cleanly end to end, not an optimistic estimate that breaks at settlement.

- Verify core instruction fields before approval.

Confirm send amount, payout currency, recipient legal name, account details, and required beneficiary identifiers. Match payment draft to invoice and latest approved beneficiary record. Checkpoint: no unresolved field mismatch remains before release.

- Capture comparable quotes in one short time window.

Collect at least two provider quotes with the same amount, currency pair, and intended send time. Add one market-rate reference in the same window, such as a Mastercard currency converter snapshot. Checkpoint: each option is timestamped and directly comparable.

- Separate listed fees from conversion impact.

Record explicit transaction fees on one line and conversion impact on another, then total into all-in estimate. Calculate effective cost percentage against send amount so options stay comparable across corridors.

- Mark unknown deductions before approval.

If any charge is unclear, mark it as unknown rather than zero. Include possible downstream deductions in that uncertainty line.

- Choose rail with an if-then rule, not headline fee alone.

If timing is tight, favor the route with clearer settlement behavior and fewer unknowns. If approval is close to bank cutoffs or holidays, move approval earlier or reset expected credit date.

- Prepare for compliance checks before release.

Treat compliance holds as normal in cross-border payments. Keep payer and recipient data clean, and assign ownership for fast follow-up responses. Checkpoint: no open compliance-data gaps at approval time.

- Save quote, confirmation, and settlement proof together.

Store quote snapshot, provider confirmation reference, and final settlement record in one place, with approval timestamp and owner.

- Reconcile estimate versus actual before next send.

Classify each gap between estimate and settlement, then update provider ranking by corridor. This keeps routing decisions evidence-based and reduces repeat surprises.

Run this checklist every time, even when the payment looks routine. Consistency is what keeps cost control real when timing pressure is high.

Want a quick next step while you price an international payment? Try the free invoice generator.

Frequently Asked Questions

What is the difference between exchange rate and all-in international payment cost?

Exchange rate is the conversion price between two currencies. All-in cost includes the conversion result plus listed transfer fees and any receiving-side fees that affect what arrives. In practice, two options can show similar rates but different all-in outcomes when fees are handled differently. Keep conversion and fee lines separate before totaling. If you compare rates alone, the option that looks cheaper can still deliver less to the recipient.

Which fees are usually hidden even when a provider says pricing is transparent?

Common misses are charges outside the headline number, especially receiving fees and payment-method-specific charges. In Wise US pricing examples, that includes a fixed 6.11 USD fee for receiving certain USD wire and Swift payments, and card withdrawal conditions of 2 free withdrawals each month up to 100 USD, then 1.5 USD per withdrawal. Wise also notes that some ways to pay are free while others have a fee. Treat these as product-specific checks, not universal rules for every country or account type. The practical rule is simple: if a fee can apply but you have not confirmed whether it does, carry it as unknown risk instead of zero.

How do I compare Wise, Tipalti, and card-network tools like Visa or Mastercard fairly?

Use one shared test case with identical send amount, currency pair, payout method, and quote window for every option. Then compare like-for-like fields: listed fee, conversion rate, expected recipient amount, payment method notes, and timestamp. Mark incomplete rows as partial instead of filling gaps with assumptions. Rank only after rows are complete or unknowns are explicitly priced. If two options are close on cost, choose the one with clearer upfront fee and recipient-amount disclosure.

When should I use a rate tool like OANDA vs a fee calculator?

Use a rate tool as a conversion benchmark. Use a provider quote or fee calculator for payable total, because that is where transfer charges and other listed fees appear. A benchmark rate helps with conversion context, but it does not show final recipient amount after all applicable fees. When benchmark and provider outcomes differ more than expected, inspect conversion and fee lines separately before approving.

Why does my recipient get less than the estimate even when the transfer succeeds?

A successful transfer can still settle lower because fees can vary by currency, payment method, and receiving-side fee rules. This is why line-by-line reconciliation matters. If you classify each gap source after settlement, next-send decisions improve quickly. Without classification, every miss looks random and the same corridor problems repeat.

How often should I re-check quotes before approving a cross-border payment?

Re-check in the same decision window immediately before approval. Re-check again if amount, currency, payout method, or selected rail changes. For recurring sends, keep a consistent quoting cadence so month-to-month comparisons stay meaningful. Mixed capture timing creates false variance. If a corridor has shown recent misses, tighten capture timing and increase caution on rows marked partial.

Watch

Calculate the True Cost of International Payments

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

How LLC Owners Separate Business and Personal Finances

For an LLC, separating business and personal money is best treated as a weekly habit, not a one-time bank setup. It keeps records cleaner, cuts month-end cleanup, and creates clearer boundaries as the company grows.

The Best Web3 and Crypto Job Boards for Freelancers

Treat this as a time-allocation decision, not a popularity contest. If you are freelancing between client deliverables, your scarcest resource is focused application time. The right board is the one that helps you reject weak listings fast and spend real effort where there is a real chance of a response.

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.