Quick Answer

Start with a control-first sequence: score evidence quality, match the role to the right hiring model, and release payments only after documentation is complete. For the future of freelance work, this article supports bounded scaling rather than broad assumptions, with checkpoints for country review, classification risk, and finance-ready records. Marketplace speed can help early sourcing, but cross-border growth is safer when approval trails, tax onboarding, and exception ownership are clear before volume increases.

How Freelance Hiring Is Changing Across Borders in 2026#

Before you scale cross-border freelance hiring, make one decision first: are you working from evidence you can actually use, or from broad trend claims that sound bigger than they are? That matters more than the headline. If your records are weak, fast sourcing can turn into compliance gaps or classification risk long before it becomes useful capacity.

When you read about where freelance work is heading, separate platform-scoped signals from market-wide signals. Use a simple checkpoint: does the claim tell you who was measured, where, and when? One widely cited 2025 summary draws on research conducted in November 2024, with 1,900 leaders with talent responsibilities across five countries and 3,300 freelancers from desk-based industries in ten countries. That is credible and useful, but it is still a defined sample, not universal proof for every country, industry, or team size.

Three terms will keep this article grounded. Freelance growth means measured increases in freelancer use within a defined sample, which can inform hiring plans but should not set long-cycle budgets by itself. Platform trust means your finance and compliance setup can hold up when local labor-law exposure or misclassification questions appear across borders. Decision-ready evidence means the source includes enough scope and timing detail for you to judge whether it applies before you commit budget, headcount, or process changes.

That distinction matters because even strong signals are still directional. In the cited research, 91% of companies maintained or increased freelancer use over the prior three years, and 52% explicitly increased it. Useful, yes. A blank check for expansion, no. If a source cannot tell you its sample, geography, and fieldwork date, treat it as directional commentary and keep commitments smaller until your own operating evidence catches up.

Your first gate should be documentation readiness, not demand optimism. Before you add countries, platforms, or freelancer volume, confirm that your current contractor records show who approved each engagement, whether onboarding is complete, and which engagements may be drifting from short-term specialist work into something that looks long-term. That last point is a real warning sign. If local-law risk rises or a contractor relationship becomes persistent enough to look like regular employment, you may need to convert that freelancer to employee status rather than keep stretching the same arrangement.

Use this article as a decision document. First rank evidence by quality, then choose the right hiring model, then pressure-test the operating checks that prevent avoidable failures. If you do those in order, you will get a clearer read on where demand is real, where risk is rising, and what you can scale with confidence.

For a fuller operations view, read Choosing Embedded Finance for Freelance Platforms With an Operations-First Scorecard.

What the current evidence actually says in 2026#

Set your hiring pace by evidence quality, not headline size. In 2026, current data supports targeted tests and bounded expansion, but not market-wide commitments on its own.

Use this rule: the weaker the method disclosure, the shorter your planning cycle and the lower your budget confidence.

| Evidence tier | Use for | Do not use for | Required verification before acting |

|---|---|---|---|

| Tier 1, traceable research | Baseline assumptions, bounded pilots, risk framing | Market-wide 2026 demand conclusions when scope or timing does not match your case | Verify publication date, sample scope, and a traceable artifact, for example DOI 10.3389/fpsyg.2019.02055 from 2019 Sep 12. Treat it as verifiable background, not current-year market proof. |

| Tier 2, contributor analysis or forecast commentary | Hypotheses, watchlists, short sourcing tests | Annual budget setting, country rollout, market-size assumptions | Confirm it is labeled commentary. The Forbes piece (Jan 01, 2026, 03:48pm EST) is contributor analysis framed as predictions, so treat reported metrics as provisional until sample, scope, and method are clear. |

| Tier 3, platform taxonomy or anecdotal sentiment | Role discovery, buyer language, early friction signals | Demand ranking, ROI claims, pay assumptions, market-wide growth claims | Check whether the source is category labeling or narrative reporting. A label like AI & emerging tech is taxonomy context, not demand measurement. |

A Tier 1 source can justify faster movement only within what it actually measured. Even with traceable artifacts, source appraisal still applies; NLM also states that inclusion in its database is not endorsement.

Tier 2 should push you toward smaller tests, not larger commitments. If you reuse a reported metric from commentary, include its source label and treat it as provisional until it has enough source detail to influence planning.

Tier 3 should shape questions, not answer strategy. Use it to spot patterns to test, not to infer prevalence.

Known unknowns: a shared cross-platform dataset with a common 2026 method is not established here, so platform or contributor signals are not market-wide proof. There is also policy commentary with mixed 2025 to 2026 signals and unresolved implementation, plus a concrete tax-status failure mode from small miscalculations after buffer-zone removal, so keep jurisdiction checks country-specific.

For every claim you circulate, put source scope, method clarity, and a confidence label on the same line. If confidence is limited, default to short test cycles and small rollout scope until stronger evidence appears. For a step-by-step walkthrough, see Indian Gig Economy Decisions for 2026.

Where freelance growth is real and where risk is rising#

Treat freelance growth as decision-ready only when the signal is measured, scoped, and matched to your hiring question. Risk rises when teams use broad category totals, commentary, or role hype as if they were budget-grade evidence for your market and role mix.

Use this quick signal-quality filter before anything reaches your plan:

| Signal quality | What it tells you | Use for planning | Use for watchlists |

|---|---|---|---|

| Measured | A scoped result with a defined market and metric. Example: a U.S. estimate of 64 million people, or 38% of the workforce, doing freelance work last year, reportedly up by 4 million from 2022, with $1.3 trillion in annual earnings contribution. | Country-scoped demand confidence, pilot sizing, and timing when your question is also U.S.-scoped. | Check whether the same source updates or revises the measure. |

| Directional | A benchmark with method detail, but not enough to represent your actual cost base. Example: US $28 per hour from a survey of over 2,000 freelancers in 122 countries. | Framing pricing questions and sanity-checking outlier quotes. | Track by specialty, seniority, and country; this is not a universal rate. |

| Anecdotal or broad-category | Large totals that mix work types, or stories that show patterns without prevalence. Example: 154 million to 435 million online gig workers globally, an upper bound for platform-mediated work that includes on-demand roles and micro-tasks, not only service freelancers. | Not for freelancer headcount, margin models, or country rollout decisions. | Spot where platform-mediated work may be expanding or changing shape. |

Assumption drift is the main failure mode. U.S. totals already vary by source, for example 64 million versus about 73 million, so treat them as a range unless methods align. The same drift happens when teams read "online gig workers" as equivalent to service freelancers.

Before you make a decision, require a one-page evidence note that includes:

- publication date and source scope

- geography covered

- method clarity: measured, survey-based, or indicative

- a status line for any current policy or fee still pending official verification

Use a simple freelance-vs-full-time gate: choose freelance first when work is variable, time-boxed, or outcome-based; choose full-time first when continuity and tighter day-to-day control matter more.

Apply the same standard to "winner vs loser" role claims. Treat claims about AI-adjacent roles rising or generalist roles falling as testable hypotheses until your own pricing, fill-rate, and delivery-quality data confirm them.

AI is changing freelance demand faster than most teams can adapt#

Treat AI-era demand shifts as a planning assumption, not a universal rule. The pattern is clear enough to change how you hire, but you still need role-, country-, and platform-level verification before you treat it as decision-grade evidence.

A Wharton-linked study using about 6.6 million marketplace records before and after ChatGPT's late-2022 launch found that total platform earnings and contracts stayed steady, while incumbent freelancers submitted 51% to 62% fewer bids for nearly a year. It also reported contraction in AI-exposed fields like copywriting and translation, while software development and data analytics saw less demand impact but more bidding competition.

Screen the role before you screen the freelancer#

Start with the task, not the title.

| Task profile | What to assume | Hiring implication |

|---|---|---|

| Automation-prone, stable brief, predictable output, low-cost errors | More AI pressure on speed and price | Narrow scope, reduce manual production, and hire for review where possible |

| Judgment-critical, ambiguous brief, interpretation required, high-cost errors | Value sits in decisions and review quality | Pay for scoping, review discipline, and decision quality up front |

This split keeps you from treating two freelancers with the same title as interchangeable when the actual work is not.

Verify capability, not polish#

Portfolio quality alone is not enough. A systematic review covering 2001 to 2024, with a PRISMA-style flowchart, found formal educational qualifications alone are limited predictors of freelance success.

| Signal | What to verify |

|---|---|

| Ambiguity handling | Candidate shows assumptions made from an incomplete brief |

| AI-use transparency | Candidate states which tools were used and what was manually checked |

| Review discipline | Candidate provides a correction log or annotated revision |

| Revision reliability | Second version fixes the identified issue, not just rewrites wording |

Use those same four signals in live tests and paid samples. This shows how the person works, not just how polished the portfolio looks.

Before you use AI speed, quality, or ROI claims in planning, verify the current benchmark from the original source and your own delivery data.

Then tie hiring to outcomes you control: define acceptance criteria at kickoff, track defects after delivery, and monitor rework patterns by task type and freelancer. If speed improves but errors, missed requirements, or revision loops increase, you have moved faster into quality risk.

You might also find this useful: How a freelance video editor can compliantly work for a California-based company while living in Mexico.

How do you decide freelance vs full-time for a role?#

Decide role by role, not by default. In 2026, both models can work, but fit matters more than habit. Use this as a decision framework, not a promise of outcomes, and weigh risk tolerance alongside speed, stability, and handoff cost.

Start with the work, not the worker. If scope is clear, time-boxed, and easy to transfer, freelance is usually the better first test. If the role needs continuity, repeated context, and low tolerance for ownership gaps, full-time is usually the safer fit.

Run a pre-hire filter before you open the role:

- Scope clarity: Can you define deliverables, acceptance criteria, and end points now? If not, tighten the brief first.

- Continuity need: Does this role require steady coverage, institutional memory, or ongoing cross-team decisions? If yes, full-time gets stronger.

- Handoff burden: Will someone have to re-explain context, review heavily, and translate decisions each cycle? If yes, freelance flexibility can get expensive.

- Ramp time: How long until this person can operate with low supervision? Longer ramp often favors full-time continuity.

- Dependency risk: If one person exits, what breaks? If key approvals, relationships, or critical context sit with one contributor, treat that as a contractor-first warning sign.

| Decision criterion | Freelance first | Full-time first |

|---|---|---|

| Speed to start | Usually faster when scope is already defined. | Usually slower to open and ramp, but stronger when the role stays active. |

| Control | Lower day-to-day control unless scope and review checkpoints are tight. | Higher control over priorities, coverage, and direction changes. |

| Knowledge retention | Weaker when context stays in messages or one person's memory. | Stronger when knowledge must stay inside the team. |

| Operational overhead | Lower for short, discrete work; can rise with re-briefing and repeated onboarding. | Higher upfront; often lower per cycle when work is continuous. |

Make the decision auditable: add a short note to the hiring brief with your assumptions, confidence level, and what would trigger a model switch after a pilot. Typical triggers are repeated re-briefing, missed handoffs, or review time growing faster than delivery speed.

Final check before you lock the model: outcomes can vary by role, location, seniority, and demand cycles, so confirm jurisdiction and worker-experience constraints in your operating plan, especially cross-border. Right to Disconnect rules are one example of policy context that can change staffing fit.

Related reading: How Generative AI Is Reshaping Creative Freelance Work.

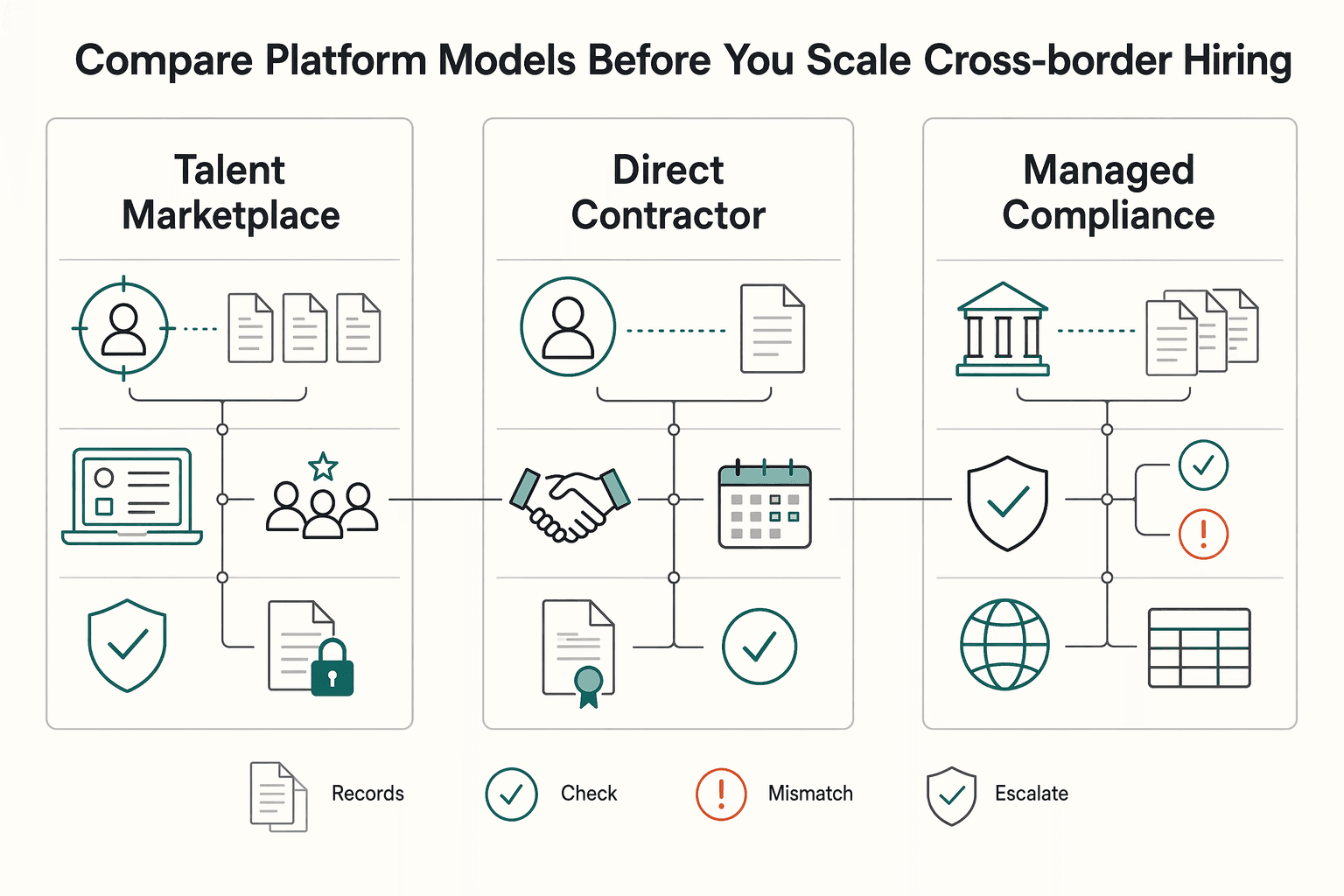

Compare platform models before you scale cross-border hiring#

Choose your model by control and compliance ownership, not by assumed talent quality. You can find strong freelancers in any model; the real difference is who owns sourcing and matching, documentation, and escalation when compliance or payout issues appear.

| Model | Operational fit | Your ownership burden | Common failure modes | Best when / Avoid when |

|---|---|---|---|---|

| Talent marketplace accounts | Useful when you still need sourcing, vetting, and matching support | Moderate: the platform helps with discovery, but you still own scope quality, approvals, and internal controls | Opaque matching process, fee leakage, and weak handoff clarity between platform and your team | Best when demand is uncertain and speed matters. Avoid when you need tight internal evidence trails and repeatable country-by-country controls. |

| Direct contractor stack with Virtual Accounts + Payouts | Useful when hiring is repeatable and you want stronger control of payment operations | High: your team owns country review, process discipline, and record quality | Misclassification exposure, approval gaps, and exceptions that are hard to resolve if process ownership is unclear | Best when you have clear internal owners and stable workflows. Avoid when you do not yet have compliance and exception ownership in place. |

| Managed compliance model (EOR/COR or similar) | Useful when compliance or admin pressure is rising, especially in longer-running engagements | Shared, not zero: provider support helps, but you still must verify coverage and escalation terms | False confidence on coverage, slow escalations, contract-type mismatch, and total landed cost surprises | Best when classification risk and admin drag are limiting scale. Avoid when work is short, simple, and your team can safely run direct contractor operations. |

Pressure-test any option before you scale. For marketplaces, ask how matching works in practice. One documented flow used four steps: requirements call, machine ranking, human shortlist, and interview facilitation. If a provider cannot explain its path clearly, assume extra vetting work will shift back to your team.

Also do not rely on headline-rate comparisons. Total landed cost can change with commissions, currency fluctuations, social contributions, and exception-handling time. If price is a deciding factor, validate the benchmark against current vendor terms and your own delivery data before using it in the model.

What to check before you scale to the next country#

Run this sequence every time before you expand:

| Check | What to confirm |

|---|---|

| Country check | Confirm your model is workable in that country, and name who owns the review. |

| Classification review | Review engagement structure for misclassification risk before contracting, especially for long-running roles that may need employee conversion. |

| Payout and approval evidence readiness | Confirm you can produce a clear trail: approvals, agreed scope, country review, and payout records. |

| Escalation ownership | Assign one internal owner for payout failures, contract disputes, and country-specific compliance questions. |

Keep that order every time you add a country.

Policy risk can change model fit. If local working-time expectations or right-to-disconnect constraints make informal management riskier, use a model with clearer controls and escalation paths. If EU personal data is involved, confirm record ownership and review GDPR for Freelancers: A Step-by-Step Compliance Checklist for EU Clients before expanding.

If you cannot name who owns classification, records, payouts, and escalations in each country, you are not ready to scale.

The operations checklist that prevents payout and compliance failures#

After you choose your hiring model, apply one operating rule every time: do not release payout until records, ownership, and filing responsibility are complete. If any part is unclear, pause the payout or filing and escalate.

| Workflow stage | Required control | What to capture | Who signs off |

|---|---|---|---|

| Onboarding records | Open the evidence pack before work starts | Contractor identity record, contract or scope, tax artifacts, named owner for country review, and any foreign-account or account-control facts that may affect FBAR or VAT review | Hiring owner and finance operations |

| Pre-payout approvals | No payout moves without a complete approval trail | Approval history, payout amount, currency, payout status history, exception notes, and payment route used | Budget owner and finance approver |

| Pre-filing compliance review | Review cross-border payments before filing | Filing responsibility, retained tax artifacts, FBAR screening notes, VAT treatment notes, and account-value evidence, for example periodic statements used to support maximum account value | Compliance or tax reviewer |

Use FBAR screening as a hard gate. A U.S. person with financial interest in or signature authority over foreign financial accounts must file when a single-account maximum or aggregate maximum exceeds $10,000 during the calendar year. For non-U.S.-currency accounts, record the conversion method required by current official instructions and keep the exchange-rate source with the file.

For electronic submission, confirm the required records are present before filing. The Transmitter (1A), Filer Information (2A), and File Summary (9Z) records are required, and missing required XML elements can trigger rejection. If threshold status cannot be determined and there are fewer than 25 accounts, complete the account sections and use item 15a ("amount unknown").

Escalation rule: pause payout or filing and route to compliance review immediately when filer status is ambiguous, account-control evidence is incomplete, threshold status is uncertain, or the current filing deadline is still pending official verification.

Related reading: Freelance Work-Life Balance That Holds Up in Real Weeks.

Common mistakes that make freelance programs expensive and fragile#

At month-close, freelance programs usually fail in predictable ways: cost leakage, compliance exposure, or payout failure risk. Sort issues into one of those buckets first, then fix the operating habit behind it.

| Mistake | Why it breaks operations | What to do instead |

|---|---|---|

| Choosing on headline fees only | The cheapest route can create expensive cleanup when reconciliation is weak, approval history is thin, or payout status cannot be reconstructed. | Score cost together with audit-trail quality, export quality, and your ability to trace who approved what before money leaves. |

| Expanding without a documented jurisdiction review | Filing, account-control, or local handling questions surface after work is done and payment is due. | Require a country-level review note before launch, with a named owner and a clear handoff for downstream obligations. |

| Treating tax and account documentation as cleanup work | Month-close becomes guesswork when filer classification or account evidence is incomplete. | Open the evidence pack before work starts and retain the statements, ownership facts, and account-control notes needed for review. |

| Running ad hoc transfers | One-off routes create duplicate-payment risk, missing approval trails, and inconsistent filing support. | Centralize transfer methods and block retries until the original payment path and status history are confirmed. |

| Impact area | What it usually looks like | Fix first |

|---|---|---|

| Cost leakage | Extra fees, manual cleanup, duplicate retries | Stop choosing tools or routes on price alone |

| Compliance exposure | Missing country review, unclear filer status, weak account evidence | Require documented review before expansion or filing |

| Payout failure risk | Stalled payments, rejected files, unreconciled transfers | Standardize approvals, records, and transfer paths |

FBAR is a common blind spot. If FinCEN Report 114 could apply, verify whether a single-account or aggregate maximum exceeded $10,000, value each account separately, and retain the periodic statements used to approximate maximum account value. For non-U.S.-currency accounts, document the conversion source, and replace any hardcoded deadline language with the current filing rule after checking official records. If you e-file, verify required records such as Transmitter (1A), Filer Information (2A), and File Summary (9Z), because missing required elements can cause rejection.

Stop payouts or filings and route to compliance or finance immediately if documentation is incomplete, filer classification is ambiguous, threshold status cannot be determined cleanly, or required filing records are missing.

For a marketplace-specific angle, see The Future of Freelance Marketplaces in 2026 Favors Curated Channels.

Conclusion#

If the FAQ leaves you with one rule, keep this one: do not scale on trend language alone. When the evidence is mixed, verify before you turn it into policy, budget, or a provider commitment. Your edge is not predicting the market perfectly. It is making sure your controls survive the first payment, the first exception, and the first close.

Follow the four decisions in order#

- Classify role risk

- Choose the model that fits

- Assign named owners

- Pause scale when exceptions repeat until controls are fixed

Start with the role, not the platform. If the work is project-based, variable, and the worker will control their own schedule, rates, and setup, freelance or independent contractor engagement can make sense. If the role depends on long continuity, frequent internal changes, or tight day-to-day control, be much more cautious before treating it as flexible external talent just because the budget is easier to approve.

That first classification matters because freelancers handle their own taxes and often invoice clients directly. Independent contractors are also generally responsible for their own taxes and benefits. In practice, that makes tax onboarding and invoice control practical checkpoints. Before any scale decision, verify that you can collect the onboarding details you need, review an invoice cleanly, and match that invoice to an approved scope and a real payee account. If you cannot do that reliably for one engagement, adding countries or volume will magnify the weakness.

Match the model to the work, not the sales pitch#

Once you know the role profile, choose the operating model that fits the control requirement. A marketplace may help with sourcing speed, but access to a large network is not the same as dependable fulfillment, repeat engagement quality, or clean finance records. Direct relationships can improve continuity and negotiated terms, but they can also put more of the approval, recordkeeping, and payout burden on your team. A Merchant of Record can shift admin burden, but only if you confirm exactly what evidence you still receive and what the provider keeps.

This is where buyers often over-trust convenience. Some views of platform-heavy hiring are optimistic, and some treat platform dependency as a control risk. You do not need to settle that debate in the abstract. You need to test your own operating requirements. If your team needs a durable approval trail, invoice references that finance can reconcile, and clear ownership of payout records, make those requirements part of the buying decision instead of assuming they will be easy to add later.

A useful red flag is any provider discussion that stays at the level of coverage and speed while staying vague on evidence. If you cannot see how approvals, invoices, payouts, and exceptions will be exported and checked, you are not ready to scale. That is not a procurement nuisance. It is a close, filing, and dispute risk.

Make ownership explicit before money moves#

The strongest close is simple: name the owner for hiring approval, payout approval, compliance review, and exception handling before the first release. You want no ambiguity about who checks account ownership, who confirms invoice readiness, who reviews missing records, and who can stop payment when something does not line up. A repeated exception with no clear owner can be an early sign that a freelance program will become expensive and fragile.

Your verification step should be concrete. Ask for coverage by country, the compliance gates that apply before payout, and a finance-ready export sample before you commit. Then have finance review whether that export preserves the fields they actually need, such as approval history, invoice references, payout status, and exception notes. If the sample is incomplete, hard to reconcile, or owned by someone outside your process, pause.

That is the practical finish: classify risk, choose the model, assign owners, and stop expansion when the same exception shows up again and again. Do not add countries or volume until the control gap is fixed. If you want to verify coverage, compliance gates, and finance-ready export proof before signing, contact Gruv and ask for the evidence first.

If you need to confirm country coverage or compare engagement options, talk to Gruv.

Frequently Asked Questions

Is freelance work actually growing in 2026, or just shifting between platforms and direct channels?

The available evidence does not prove market-wide growth on its own. What you can say is narrower: freelance work appears persistent, and channels may be shifting, but that is not the same as confirmed expansion. Before you budget around the future of freelance work, check your own demand signals and repeat-engagement patterns first.

How can I tell whether a freelance trend is real or just online chatter?

Use three evidence tiers. Tier 1 is official datasets and regulator or labor-statistics releases. Tier 2 is platform or company disclosures, such as funding or product announcements, which can show business activity but not labor-market truth. Tier 3 is anecdotal material like a Jan 8, 2024 Medium post, a personal FAQ updated April 29, 2024, or a discussion thread with 153 comments. If a claim shows up only in Tier 3, treat it as directional and keep your pilot small.

Will AI replace most freelancers, or mainly change which skills still command better rates?

There's no quantified answer, so do not plan as if mass replacement or premium-rate protection is already proven. A safer read is that freelance work can include a changing task mix: one freelancer describes days split across longer projects, quick-turn work, research, and admin, and workload can come in waves. Break roles into repeatable tasks versus judgment-heavy work before you change pricing, staffing, or scope.

When should you use a Merchant of Record instead of managing freelancers directly?

No universal cutoff is supported by the available evidence, and Merchant of Record-specific benchmarks still need source verification. What is supported is that freelance operations can create heavy admin load (including invoicing) and that tax mistakes are a real risk if processes are weak. Use that as a trigger to verify your operating model with qualified tax or compliance support before you scale.

What compliance checks matter most first for cross-border freelance hiring?

No universal official sequence for KYC, KYB, AML, and tax forms is supported across jurisdictions, so avoid assuming one platform check covers all of them. A practical first pass is to confirm who owns invoicing and records, retain an accountant if possible, and if you do not, keep meticulous financial records and file away bills and receipts from day one.

What should freelancers and small teams verify before accepting global payouts and tax obligations such as VAT, Form 1099, or FBAR?

Keep clear financial records before money moves, including invoices and stored bills or receipts. Then verify the current filing deadline and current reporting rule with qualified tax or compliance help, rather than relying on memory or an old checklist. If classification or record quality is unclear, pause payout acceptance or filing and route it to qualified tax or compliance review.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- bsaefiling.fincen.gov/docs/FinCENFBARElectronicFilingRequirements.pdftrusted

- bsaefiling.fincen.gov/docs/XMLUserGuide_FinCENFBAR.pdftrusted

- espas.secure.europarl.europa.eu/orbis/system/files/generated/document/en/Fut...trusted

- fincen.gov/reporting-maximum-account-valuetrusted

- fincen.gov/report-foreign-bank-and-financial-accountstrusted

- knowledge.wharton.upenn.edu/article/how-are-freelancers-adapting-to-gen-aitrusted

- oecd.org/content/dam/oecd/en/publications/reports/202...trusted

- pmc.ncbi.nlm.nih.gov/articles/PMC6751263trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

GDPR Compliance Checklist for Freelancers Working With EU Clients

Start by separating the decisions you are actually making. For a workable **GDPR setup**, run three distinct tracks and record each one in writing before the first invoice goes out: VAT treatment, GDPR scope and role, and daily privacy operations.

Right-to-Disconnect Rules for Freelancers in Cross-Border Contracts

If right-to-disconnect rules do not clearly cover your status, your contract has to carry the weight. For freelancers, off-hours boundaries are deal terms, not assumptions.

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.