Quick Answer

Choose the stack that proves operations under stress, not the one with the strongest demo. In fintech trends 2026, use a two-pass decision: first remove vendors missing written scope, fallback behavior, ownership clarity, and auditable records, then score remaining options by persona fit. Before procurement, run a limited pilot with a simulated failure and require reconciliation output plus an unresolved-risk log.

Start Here With the 2026 Buyer Lens#

Use fintech trends 2026 as a buying filter, not a prediction game. You are choosing the vendor that can earn trust, show clear control ownership, and keep operations stable when conditions are uncertain.

For this review cycle, this lens is grounded through February 2026. The operating environment remains complex across regions, shaped by geopolitical tension, regulatory intervention, and uneven macro conditions. Treat compelling claims as unproven until you can inspect execution evidence.

This lens works for three buyer types:

- If you are a freelancer, prioritize reliability and clear ownership without heavy procurement overhead.

- If you run a small team, prioritize fewer operational surprises and explicit support accountability.

- If you run embedded finance, evaluate both customer experience and underlying controls.

Use the rest of this article in a simple sequence:

- Filter signals: keep recurring 2026 patterns and ignore one-off feature hype.

- Test checkpoints: request evidence across strategy, sourcing, diligence, integration, and separation execution.

- Gate rollout by proof: advance only when outputs are demonstrated, not just promised.

When you ask for proof, ask for artifacts that show how the capability is executed and who owns outcomes when something fails. Failure often is not about bad intent. A compelling opportunity can still stall when conviction weakens under cost and risk pressure.

Start a lightweight diligence log on the first call:

| Demonstrated capability | Unverified claim | Promised follow-up artifact |

|---|

That one page keeps your shortlist honest and makes every later comparison faster.

Related: The 'Right to Disconnect': How New Laws are Affecting Freelancers.

Build the Mental Model Before You Compare Vendors#

Do this first: write your own scope and decision rules before you score any vendor. If you skip it, you can end up grading narrative quality instead of operating capability, and ownership gaps can stay hidden until later.

Trend coverage is useful context, but it is not proof. A practical reading for 2026 is simple: innovation can rise with risk, and automation can still underperform when service quality is weak. Treat polished claims as incomplete until scope, ownership, and exception handling are explicit.

Force terminology into written scope#

Do not debate Open Banking, Open Finance, or embedded finance in the abstract. Ask each vendor to define the term it is using in writing, then map that claim to concrete scope in your environment.

A simple one-page capability map can include three fields:

- Data boundary

- Payment action

- Ownership line

If any field is blank, treat the claim as incomplete and pause scoring until it is filled.

Compare in layers, not one blended score#

Use the same comparison structure for every vendor so a strong UI demo is less likely to hide weak controls.

| Layer | Example artifact to request | Likely internal owner | Possible failure mode |

|---|---|---|---|

| Customer experience | Flow walkthrough for key actions, including exception paths | Product or operations | Happy-path demo only and exception handling is unclear |

| Policy | Written decision logic and escalation path | Finance, risk, or compliance | Rules are informal and outcomes vary by person |

| Money movement | End-to-end transaction lifecycle with status changes and handoffs | Finance ops or payments owner | Initiation is clear, but exception ownership is not |

| Evidence | Exportable records tied to a transaction outcome | Controller, ops, or audit-facing owner | Records are partial or hard to reconcile |

Use one evidence pack and check completeness#

Before ranking, ask every vendor for one bounded evidence pack. The point is reviewability. Bounded artifacts are easier to challenge and compare. For context, the Coalition Greenwich 2026 trends page also points to a bounded artifact via its downloadable report (7 pages; 0 graphics).

Minimum pack:

- Current capability map

- Sample policy decision trail

- Reconciliation output tied to a real or realistic transaction outcome

If key artifacts are missing, outdated, or deferred, treat the vendor as incomplete and hold final ranking.

Validate rails with scenarios, not promises#

For cross-border or multi-rail scope, test scenario behavior, not feature claims. Run concrete exception cases and require named ownership for detection, communication, resolution, and decision-trail export.

This is where the automation-versus-service tradeoff becomes visible in practice. Use 2026 trend coverage as a pressure test, not a shortcut: written scope first, layered evidence second, scenario validation third.

For a step-by-step walkthrough, see The Race to Zero on FX Fees Is a Losing Bet for FinTech Buyers.

Cover the Table Stakes Every Credible Platform Needs in 2026#

Before you spend time on a pilot, set a hard gate. If a vendor cannot prove baseline trust controls, named ownership, and audit-ready evidence, do not advance it. The goal is not to score roadmap slides. It is to confirm that cross-functional reviewers can assess the same artifacts and clearly see who owns approvals, exceptions, and incident evidence.

This gate is practical, not arbitrary. The OECD's March 2026 update keeps the focus on oversight, protection against fraud/scams/misuse, and complaints handling and redress. For buyers, that translates into a simple standard: if control ownership and escalation accountability are unclear, the platform is not ready for real money movement.

| Requirement | Evidence artifact | Disqualifying gap |

|---|---|---|

| Onboarding and identity-check controls are documented before financial services are turned on | Current onboarding policy, a sample review path, and a dated description of what is checked and when | The vendor says checks exist but cannot show the decision path or when controls apply |

| Compliance ownership is named, not implied | Owner list with role names, approval authority, and escalation contacts | Ownership sits with a generic team label or shifts depending on the issue |

| Third-party risk management covers external dependencies | Responsibility map across involved parties for approvals, exceptions, and incident handling | The vendor cannot show who acts first when a partner blocks, delays, or rejects activity |

| Escalation accountability produces usable records | Sample case record with alert, reviewer action, outcome, and exportable evidence | Exceptions are handled informally, or records cannot be tied back to a transaction outcome |

Before advancement, compile one diligence packet for cross-functional review. For example, include the control artifacts above, a clear decision trail, and one sample escalation record.

Then run two checks. Confirm every artifact is current and has a named owner. Test one failure case, not only a happy path. Fast onboarding and broad 2026 narratives can be useful, but fully autonomous payments remain limited. If human edge-case review and recorded decision evidence are missing, stop there.

Separate AI Signal From AI Theater in Finance Operations#

Treat any AI feature as non-production until it is explainable, reviewable, and auditable. The test is straightforward: if a case is challenged, reversed, or audited, can your team reconstruct what happened and why?

That matters in 2026 because the sector is shifting from hype toward execution. The ECB's 23 March 2026 framing of AI as a general-purpose technology is a practical lens here. Value comes from improving real production processes, not from one impressive feature.

Split use cases into two risk tiers before you pilot:

- Low-impact assistive tasks: draft summaries, document classification, queue sorting, analyst recommendations.

- Higher-impact decisioning: approvals, holds, limits, or any output that changes money movement, compliance outcomes, or customer outcomes.

If a use case falls into the higher-impact tier, keep a human in the loop.

| Failure mode | What breaks in operations | Buyer evidence to require |

|---|---|---|

| AI appears in dashboards but not in the real workflow | Teams report usage, but decisions and handoffs still happen outside the product | Decision logs tied to real cases, plus records showing where reviewers used or rejected the output |

| Model behavior is opaque | Reviewers cannot explain why a case was flagged, cleared, or prioritized | Case-level decision logs, reviewable reason traces, and exportable records for audit review |

| No override or escalation path | Incorrect outputs persist, exceptions stall, and ownership becomes unclear | A documented override path, a sample escalation trail, named approvers, and exportable case history |

Keep a manual review lane open through the pilot, then gate expansion on explicit acceptance criteria:

- AI output is compared against final human decisions.

- Overrides and exceptions are traceable to the underlying case record.

- Unresolved drift blocks rollout expansion until the vendor can explain behavior and export usable evidence.

In finance operations, explainability and auditability are not premium extras. They are baseline proof that an AI feature is ready for production.

Treat Fraud and Compliance as Product Requirements, Not Legal Footnotes#

Fraud and compliance should be tested as product behavior, not treated as legal text sitting outside the product. Evaluate how controls work across onboarding, transaction checks, payout release, and post-settlement review.

In practice, that means verifying how controls run in the workflow, not how policies read on paper. Compliance in 2026 is broader than identity and fraud checks alone, and key features such as onboarding and dispute handling are expected to follow strict rules from the start. If a vendor cannot show that code enforces limits, logs actions, and adapts to regional requirements, treat it as an operating gap.

Use this table to judge evidence quality by stage:

| Stage | Documented ownership | Traceable decision trail | Exception handling | Audit readiness |

|---|---|---|---|---|

| Onboarding | Named role owns KYC reviews and unresolved identity cases | Record shows trigger, reviewer, and final disposition | Failed or incomplete verification has a defined manual path | Exportable logs include country-specific settings used |

| Transaction checks | Named owner for AML and suspicious-activity triage | Alert history ties trigger, actions, and outcome to the case | Triggered cases and duplicate alerts have a clear escalation route | Logs show limits or rules applied and actions taken |

| Payout release | Named approver or policy owner for holds and releases | Release decision links to prior checks, overrides, and timestamps | Holds can be escalated or rerouted without losing case history | Approval records remain reviewable after settlement |

| Post-settlement review | Named owner for disputes, reversals, and retrospectives | Full history is preserved from first event to closure | Reopened cases and corrections keep attribution | Retained trail is exportable for review |

If you hear "our compliance team handles that," push for stage-level ownership. You should know who triages suspicious-activity alerts, who can override a hold, and how that override is recorded.

Run a short failure drill during diligence#

Use a short drill to see whether the operating story holds up when something goes wrong.

- Request three real case walk-throughs: one KYC review, one AML or suspicious-transaction case, and one payout-hold escalation.

- Follow escalation end to end: who touched the case, what triggered review, and where each decision was recorded.

- Confirm attribution fields are visible: reviewer, timestamp, trigger or rule, manual override if used, and outcome.

- Verify recovery behavior: what happens when an alert is cleared in error, a payout hold is incorrect, or a check must be rerun after settlement.

You are not testing model internals. You are testing whether exceptions stay visible, attributable, and recoverable.

For cross-border programs, require evidence that regional variance is handled in product settings, not only in policy PDFs. A 2026 analysis describes a regulatory patchwork with "50 competing rulebooks" and warns that state-law variance can split one national product into "50 different variants." Before contract signature, ask for three artifacts: a clean resolution, an escalated case, and the export format for logs or case history. If those artifacts are missing, keep the vendor off the shortlist until it can provide the operational record.

For a more specific look at platform selection, see How Freelancers Choose a Compliance-First Fintech Platform.

Decide if Stablecoin Readiness Is a 2026 Must-Have or a Distraction#

Treat stablecoin readiness as optional until a live corridor pilot shows a net operational gain after compliance effort is included. If you cannot show that with settlement records, exception handling, and clear market-level ownership, it is a distraction, not a differentiator for your 2026 stack.

Start with supervision and regulatory reality, not the demo. On March 11, 2026, the FDIC said supervision reform remains a top priority and involves more than publishing new rules. So if a vendor positions stablecoins as payment plumbing, test how oversight, controls, and partner responsibilities work once money moves. If it references the GENIUS Act, require a written legal assessment for your use case and target markets before treating it as rollout support.

Keep scope narrow at first. Stablecoins may be useful in a specific corridor pilot, but broad rail replacement is hard to justify before operating evidence exists. One 2025 market view described the stack as issuers, wallets, compliance, analytics, and on or off-ramps. Treat that as a chain of counterparties and controls where unclear ownership at any point becomes your outage or audit risk.

Require a named responsibility map before any pilot#

Before rollout, require a market-by-market map naming ownership for vendor operations, issuer relationship, custody or wallet control, sanctions and AML review, transaction monitoring, incident response, reconciliation, and off-ramp settlement. If you hear "that sits with our partner," ask who handles exceptions, who approves holds or releases, and where those decisions are logged.

| Responsibility area | Map requirement |

|---|---|

| Vendor operations | Name ownership in the market-by-market map |

| Issuer relationship | Name ownership in the market-by-market map |

| Custody or wallet control | Name ownership in the market-by-market map |

| Sanctions and AML review | Name ownership in the market-by-market map |

| Transaction monitoring | Name ownership in the market-by-market map |

| Incident response | Name ownership in the market-by-market map |

| Reconciliation | Name ownership in the market-by-market map |

| Off-ramp settlement | Name ownership in the market-by-market map |

Ask for concrete proof: one corridor diagram, one exception case history, one reconciliation output tied to a settled transaction, and one escalation path with named owners. A fast happy-path demo is not enough if accountability disappears when transfers stall or must return to a fallback rail.

| Check | Evidence artifact to request | Disqualifier rule |

|---|---|---|

| Cost outcome | Live corridor pilot showing all-in current-rail vs stablecoin-path cost, including fees, treasury handling, off-ramp charges, and manual review effort | No-go if savings disappear after compliance work and exception handling are included |

| Settlement reliability | Timestamped pilot records from initiation to final settlement, with exception counts, retries, and unresolved cases | No-go if performance improves only on the happy path or exception recovery is unstable |

| Compliance burden | Market-specific control matrix for onboarding, sanctions screening, monitoring, reporting, case ownership, and audit-log export | No-go if control ownership is unclear by market or decision trails cannot be exported |

Keep first production scope tight: one corridor, one segment, one fallback bank rail, and explicit rollback rules if settlement fails or review queues spike. Expand only after repeatable live-corridor evidence and stable exception handling confirm documented ownership for key workflows. Roadmap slides and future [decentralized finance] ambition are not production readiness.

Compare Money Movement Architecture, Not Just Dashboard Screenshots#

If your corridor pilot passed the economics test, choose based on traceable money movement, not interface polish. Keep the vendor that can show how money, state, and ownership move across the stack in records your finance and operations teams can review.

Across 2026 trend coverage, payment teams are prioritizing data quality, interoperability, and agnostic architecture. Use those as diligence tests, not marketing claims. A platform can claim interoperability while still hiding key handoffs in manual casework, side spreadsheets, or support-only actions.

Use buyer-grade pass or fail checks#

Focus the test on the points where state changes, exceptions appear, and accountability can blur. Treat the checks below as buyer-defined diligence criteria, not universal standards.

| Architecture area | Buyer pass/fail check | Example evidence | Disqualifier |

|---|---|---|---|

| Collection to recorded balance | Show how incoming funds move from receipt to balance or payable state, including holds, retries, and rejections when applicable | Event trail | Balances change in the UI, but there is no clear event path for why or when |

| Event delivery and exceptions | Show what happens when events succeed, stall, retry, or fail, and who owns the next action | Failure handling record | Only happy-path proof is available, or failed events disappear into support queues |

| Commercial and operating boundary | Clarify ownership for tax, invoicing, liability, and market-specific handling across partners and transaction types | Responsibility matrix | Ownership shifts across documents or defaults to "our partner handles that" |

| Accounting and operational truth | Tie sample accounting records to movement outcomes and resulting balance impact | Reconciliation artifact | Finance cannot explain differences between accounting records and movement outcomes |

Test interoperability where teams usually lose visibility#

Do not accept "we integrate with everything" as proof. Ask how data and state move across four boundaries: ledger, payments execution, risk or compliance review, and reporting. Confirm which identifier survives each handoff, which state changes write back, and whether holds, releases, returns, or reversals are visible outside the originating tool.

Use concrete prompts. If risk review stops a payment, does the ledger reflect that hold state right away? If a return or failure occurs, does reporting show intermediate states and final disposition, or only the endpoint? If operations intervenes, is that action in the same trace as the original payment, or isolated in a separate case tool?

Apply the same standard to agent-assisted flows. Guardrailed, agent-assisted execution is moving into production, while fully autonomous payments remain limited. Ask where human intent is set, what guardrails apply, and how the platform separates legitimate agents from fraud.

Set one clear acceptance test when possible: review one successful trace and one failed trace, ideally in the same session. For each, ask for timestamps, named ownership at key handoffs, and final disposition details where the platform provides them. If the story only closes after switching between product screens, support notes, and verbal explanation, treat that as an architecture gap.

Finish with finance-led validation. Have your team attempt to reconcile a sample record set to final movement outcomes, and document where vendor guidance is still required. If matching depends heavily on vendor intervention, translated fields, or special exports, flag implementation risk.

Score Vendors by Persona So Tradeoffs Stay Honest#

Set persona-level minimum controls before you do any weighted scoring. If a platform fails one must-have for freelancers, finance or AP, or ops or developer, cut it first and score only the survivors.

That keeps tradeoffs honest. Finance leaders focus on cost per transaction, cash timing, and hidden manual work. Risk teams track fraud, disputes, and policy drift. Technology leaders focus on outages and brittle integrations. A blended score too early can hide real operating risk.

Use one scorecard with pass/fail first, then scoring#

Use the same evidence standard for every vendor: successful and failed workflow traces with clear ownership and final disposition.

| Persona | Must-have control (pass/fail gate) | Business impact lens | Required proof | Disqualifier signal |

|---|---|---|---|---|

| Freelancer | Clear in-product payout status changes and a named owner for holds, returns, or corrections | Cash timing, trust, support burden | A real payout completion path and an exception path, including who acts and where status changes appear | Status is only a label, or exception handling sits in email, support notes, or verbal explanation |

| Finance/AP | Records that reconcile movement outcomes to balances, payables, and exceptions | Margin, cash flow, close effort, hidden manual work | Sample records finance can match to final outcomes without vendor intervention, plus clear ownership for exceptions | Matching depends on custom exports, translated fields, or vendor-only interpretation |

| Ops/developer | Observable integrations with modular orchestration and clear outage or retry behavior | Integration durability, migration effort, outage exposure, provider flexibility | An automated path and a failed path showing surviving identifiers, retries, write-backs, and recovery ownership | Only happy-path API proof, retries vanish into support, or provider changes effectively require a rebuild |

After a vendor passes the gate, scoring differences are expected. Keep them evidence-based, not demo-based.

AI claims should meet the same bar. If a vendor claims agentic AI value for compliance, AML, fraud, identity, or analytics, score that only after it shows clean data pipelines, shared metrics, and a consistent operating model in real workflows.

Verify digital-asset tax readiness as an operational workflow#

If digital-asset tax workflows are in scope, run a dedicated product walkthrough from transaction capture to draft tax record, then test incomplete, disputed, and correction scenarios. If Form 1099-DA matters for your program, verify status visibility, correction handling, and accountable ownership in product, not as a future partner promise.

Treat off-platform spreadsheets, email approvals, or unowned handoffs as incomplete support.

Keep the decision sequence short#

Keep the process tight:

- Set persona minimum controls and eliminate any vendor that fails one.

- Score only remaining vendors using the same evidence session.

- Recheck premium claims, especially AI and digital-asset tax workflows, only where workflow proof and ownership are visible.

- If scores are close, choose the vendor with stronger cross-persona evidence quality and failure-path proof.

When scores are nearly even, pick the platform whose bad day is easier to understand and operate.

Use Red Flags to Eliminate Risky Platforms Early#

Eliminate vendors on control risk before you score features. If a platform cannot show clear ownership, verifiable evidence, and human intervention controls, remove it from the process.

The bar is not paper compliance alone. Diligence should test whether issues can be caught and stopped earlier, with real-time accountability and clear human escalation when automation fails.

Start with control boundaries, not product polish#

Run a boundary-and-ownership test first. Before a vendor advances, require a written verification pack and explicit control ownership that shows who owns onboarding checks, ongoing monitoring, exception review, and when to pause work or expand validation.

Do not accept this verbally. Onboarding alone is not enough for ongoing risk control. If ownership is vague or undocumented, treat it as a red flag until resolved.

Require one verification pack up front, not in fragments. It should include supporting records and a clear note on how figures were cross-checked. If access is restricted, data is incomplete, or reporting is only rounded numbers, pause diligence or expand validation immediately.

| Red flag | Required proof | Elimination trigger |

|---|---|---|

| Unclear ownership of onboarding and ongoing monitoring controls | Written control map with a named owner and escalation point | Ownership is verbal, vague, or changes based on who answers |

| Restricted or low-quality diligence evidence | Verification pack provided up front, including supporting records and cross-check method | Read-only access is blocked, records are incomplete, or reporting is only rounded numbers |

| Automation claims without exception proof | One real example showing alert, review, human intervention, and final decision | Only happy-path automation is shown, or no accountable manual intervention is demonstrated |

| Repeated issues framed as one-off customer behavior | Evidence of earlier detection thresholds and earlier manual intervention when patterns repeat | Incidents keep repeating without control-framework changes |

Treat automation claims with the same evidence standard. You are looking for proof of early detection and early manual intervention, not roadmap language or "AI will handle it" claims. If repeated issues are framed only as customer behavior, that points to control-framework weakness.

Use a short review protocol and cut fast#

Use a short protocol and keep the decision binary:

- Collect all evidence packs together, including the verification pack and one real exception record.

- Run one joint review with finance, risk or compliance, and engineering or ops.

- Log each red flag as pass or fail with a one-line rationale and missing proof.

- Disqualify immediately on any unresolved red flag. Do not carry it into weighted scoring.

This keeps polished demos from outranking control evidence and gives you a safer shortlist faster.

If embedded finance is part of your stack decision, Choosing Embedded Finance for Freelance Platforms With an Operations-First Scorecard offers a practical evaluation framework.

Before final scoring, pressure-test your checklist against real status flows, retry behavior, and reconciliation outputs in the Gruv docs.

Execute in the First 90 Days Without Breaking Finance Ops#

Treat your first rollout window as a proof gate. Scale only after launch readiness, budget alignment, and quarterly priorities are documented and jointly reviewed. In 2026, the real tradeoff is still speed versus proof, and trust does not survive a ship-now-fix-later approach.

Before expanding volume, have a cross-functional team review the same three checkpoints together:

- Launch readiness for the product path in scope, including how exceptions and risk signals are handled.

- Budget and priority alignment for current operating goals, with clear owners for open issues.

- Fraud and risk readiness across teams, since fraud pressure can move earlier in transaction flows.

If regulated products are in scope, make compliance and reporting readiness an early checkpoint, not a cleanup task. Treat vendor claims as unverified until your team confirms them in your own operating context.

| Rollout stage | What must be true | Who signs off | What blocks promotion |

|---|---|---|---|

| Limited pilot | Documented checkpoints are complete, controls are active, and key risks are understood on initial scope | Cross-functional reviewers confirm readiness together | Missing checkpoint evidence, unresolved risk, or unclear ownership |

| Broader production use | Results stay consistent as usage grows, with issues logged and tracked to resolution | Same reviewers reassess readiness together | Repeated unresolved issues or new risks without a mitigation plan |

| Higher-volume expansion | The operating model remains stable under higher demand and regulatory expectations | Joint approval is recorded in the gate log | Any disputed checkpoint, open critical risk, or unresolved compliance question |

Keep every gate auditable. If evidence is missing or disputed, freeze expansion, log the owner and remediation, and rerun the same gate before moving to higher volume.

Handle Country and Program Variance Without Guesswork#

Do not sign until you can show, in writing, how variance is handled for each market and launch program. Use this as a working diligence frame, not a legal taxonomy. The sources support documented scope, precision, and ROI checks; they do not, on their own, validate country-by-country legal or regulatory requirements.

Before signature, run more than one scenario per market and per program, then treat any mismatch across product, legal, and support as unresolved risk until it is resolved in writing. This protects you from broad demos and generalized claims that may not hold up in your specific operating path.

| Check area | What you should request before signing | How you verify this | Red flag that should pause signature |

|---|---|---|---|

| Market scope | A market sheet that lists included, excluded, and conditional markets for your exact product path | Compare the market matrix to the signed order form or contract scope exhibit | Sales claims broad coverage, but signed scope is still generic |

| Program fit | A written description of supported customer types, use cases, and policy constraints for your first launch program | Match product docs and sandbox or pilot output to your real onboarding and exception scenarios | Demo works for one path, but your customer type or edge cases are not confirmed in writing |

| Operational ownership | Written support and escalation ownership for normal and exception flows | Check the support plan or support exhibit, plus named owners and handoff rules | Commitments live in email or marketing copy, not executable documents |

| Evidence and ROI | Proof of reviewable output for outcomes, plus ROI evidence for the proposed setup | Review pilot output, sample reports, reconciliation artifacts, and a short ROI case tied to the same path | AI efficiency or margin-scale claims appear without evidence tied to your program |

The last row is a major diligence signal. In 2026 diligence, feature coverage is not enough on its own. You also need evidence of customer ROI and scalable AI-enabled margins for the path you will actually run. If reviewable output is missing, assume ramp risk is higher because integration and change management may carry more of the load.

Use a short pre-sign checklist#

Use a short checklist and make every item produce a document you can review later. Treat it as an internal operating control, not a substitute for legal advice:

| Checklist item | Documented output |

|---|---|

| Create one market sheet per target market | Scope, constraints, enabled product path, and your named owner |

| Create one program sheet per launch use case | Customer type, transaction pattern, internal risk-policy notes, and required evidence |

| Run at least two scenarios for each market-program pair | Sandbox or pilot output for one normal case and one exception case |

| Log every contradiction across product, legal, and support | A contradiction log entry with mismatch, source document, named owner, and due date |

| Make a written go or no-go decision | A decision note that accepts documented variance or blocks signature until resolved |

Do not let references substitute for proof. In niche B2B markets, your buyer pool may be only 5,000 to 15,000 people in a country, and relationship-led pipeline has a ceiling. When a vendor says, "others like you run this," ask for the market sheet, program sheet, and written mismatch resolutions for your path.

Related reading: When Freelancers Outgrow Spreadsheets and Need an AI Virtual CFO.

Choose the Safer 2026 Stack and Next Step#

Choose the vendor that proves control quality under stress, not the one with the longest feature list. The safer call is evidence quality over feature volume, because outsourcing execution does not outsource your accountability when money movement, data access, or exception handling fails.

That standard should hold even when the product looks modern and the demo is smooth. Third-party use can reduce your direct control and introduce new risk, so ownership, fallback behavior, and monitoring cadence should be explicit in writing. For critical activities, monitoring should be more frequent and more complete. Your selection standard should follow a full third-party risk lifecycle: planning, due diligence and selection, contracting, ongoing monitoring, and termination.

Use three buyer tests before you pick#

Before final selection, require clear answers to three questions: can this vendor keep your operation running through disruption, can you trace decisions and payments after the fact, and can it prove where your exact program is live today.

| Buyer test | What you should require in the walkthrough | What should make you pause |

|---|---|---|

| Continuity readiness | One severe-but-plausible disruption scenario using your real flow, plus stated tolerance for disruption, fallback route, retry behavior, and named escalation owner | No written fallback path, no owner for manual recovery, or vague answers about rail, partner, or data-source outages |

| Control traceability | One end-to-end example with raw event trail, timestamps, status changes, manual override record if used, and reconciliation evidence tied to final ledger or export | Screenshot-only demos, no exception log, no way to explain decision changes, or AI outputs that are not reviewable for reliability, accountability, and explainability |

| Market and program scope proof | Written scope confirmation showing where the feature is live now, for which customer type or program, with exclusions, dependencies, and fallback behavior by jurisdiction | Sales assurance without written limits, one market presented as proof for all markets, or stablecoin claims that ignore cross-jurisdiction AML context or June 2025 payment-transparency changes |

Continuity readiness can be under-tested. The vendor should walk you through a severe-but-plausible disruption and show mitigation, not just promise resilience. If it cannot name who owns recovery, you still have a sales answer, not an operating answer.

Scope proof is where late-stage mistakes happen. If you depend on U.S. consumer-authorized data sharing, the CFPB final rule was released on October 22, 2024, and compliance dates are phased from April 1, 2026 to April 1, 2030. If your program touches EU regulated entities, DORA has applied since 17 January 2025. If a vendor tells one generic open banking story without program-level applicability, treat it as incomplete diligence.

For stablecoin or other virtual-asset-connected flows, apply stricter proof standards. FATF updated Recommendation 16 on 18 June 2025, and implementation remains uneven across jurisdictions. Ask for corridor-level and program-level proof, not global claims. If the response is still generic instead of written live coverage, treat it as a verification gap.

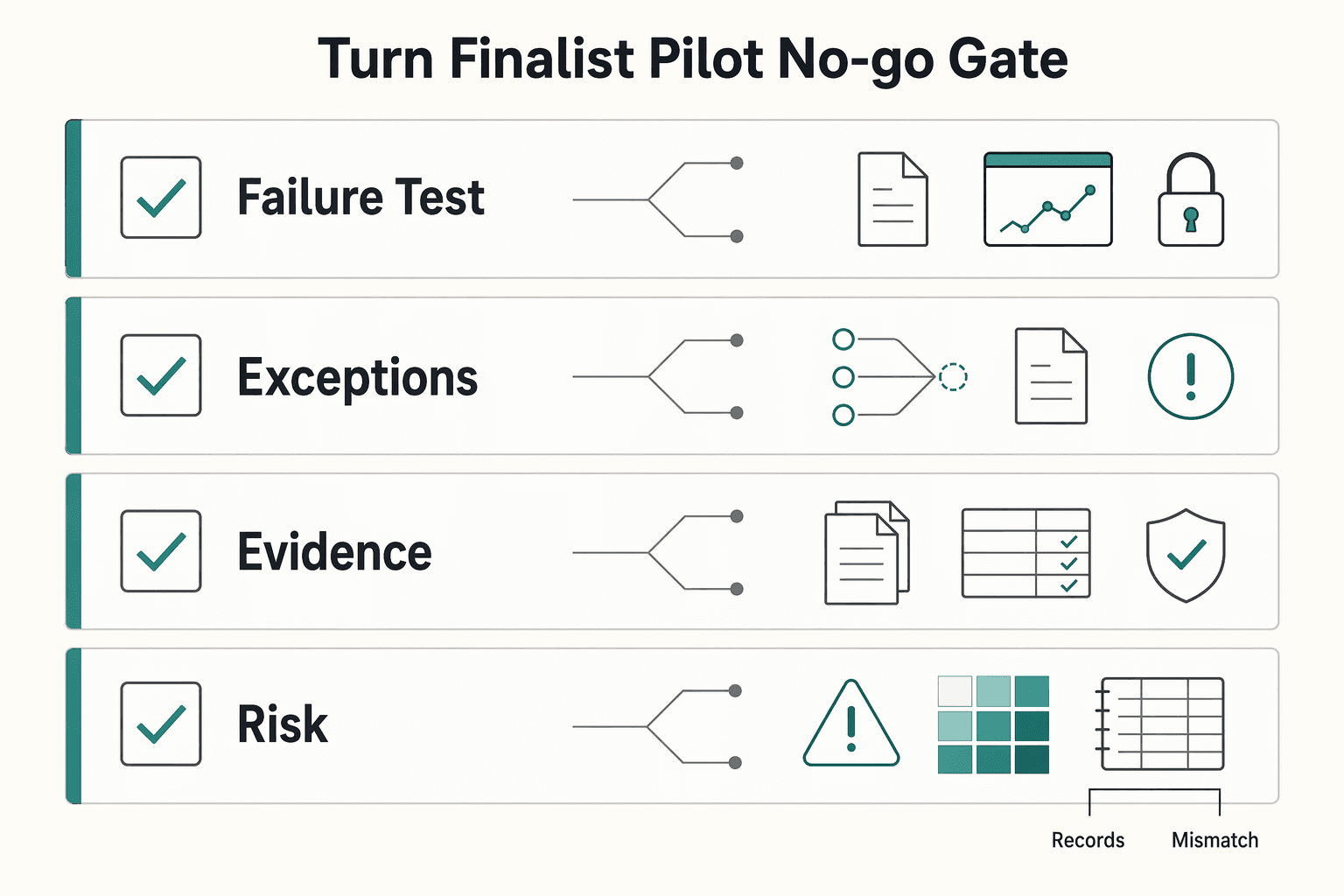

Turn the finalist pilot into a go or no-go gate#

When two vendors remain, run a short pilot designed to expose ownership gaps early. Do not let it become a soft launch with undefined success criteria.

| Required output | What it must show |

|---|---|

| Failure test result | One forced failure case in your real or simulated flow, observed behavior, fallback trigger status, and whether recovery stayed inside your disruption tolerance |

| Escalation owner | A named role, response path, and contact method for payment delay, return, screening hold, and data-feed failure |

| Reconciliation evidence | One normal transaction and one exception transaction tied to status history, ledger movement, and exported records your finance lead can review |

| Unresolved-risk log | Each open issue, owner, workaround, acceptance decision, and target closure date |

Require these outputs before signoff:

- Failure test result for one forced failure case in your real or simulated flow, including observed behavior, fallback trigger status, and whether recovery stayed inside your disruption tolerance.

- Escalation owner with a named role, response path, and contact method for payment delay, return, screening hold, and data-feed failure.

- Reconciliation evidence tying one normal transaction and one exception transaction to status history, ledger movement, and exported records your finance lead can review.

- Unresolved-risk log listing each open issue, owner, workaround, acceptance decision, and target closure date.

One failure mode to watch for is passing the happy path, then stalling on one rejected payment, one delayed return, or one manual override with logs. Another risk is split ownership where support owns tickets, compliance owns policy, and no one owns the customer outcome. If that is still unclear after the pilot, you do not have enough control to proceed.

Make your next step operational#

Run a scenario-based walkthrough with your own payout, refund, hold, and outage cases. Require written scope confirmation for your exact market, program, customer type, and fallback path before procurement review starts.

If ownership is still unclear, or fallback behavior is still verbal instead of documented, pause selection. The safer stack is not the one that promises the most. It is the one that proves, in writing and in test evidence, how your operation keeps working when the normal path fails.

If your shortlist is down to finalists, request a market-and-program coverage review for your exact payout corridors via Gruv.

Frequently Asked Questions

What are the most important fintech trends in 2026 for small teams and freelancers?

For your shortlist, treat three signals as filters: Open Banking is baseline, AI is shifting from novelty to expected utility (especially in fraud defense), and stablecoin claims need corridor-level proof. These are procurement checks, not stand-alone reasons to buy. Request a capability map that shows, in your signed scope, where Open Banking, AI decisions, and any stablecoin rail actually operate.

Is AI in fintech a must-have now, or should you wait?

AI is now expected in many fintech workflows, but use it first where it improves a real review step, queue, or fraud control you already run. The risk is not just a wrong output. It is an unreviewable decision with no owner, override, or audit trail. Ask for one approved case, one false positive, and one manual override with logs, timestamps, and named ownership.

How do you evaluate whether stablecoin-ready features are actually usable for your business?

Start with your real corridor, customer type, and fallback path, not the demo path. Stablecoins may help in specific flows, but cross-border friction can remain because AML and KYC expectations differ by jurisdiction, and stablecoins do not remove all operating friction. For programs involving permitted payment stablecoin issuers, confirm AML program ownership, then treat each jurisdiction's requirements as pending until they are verified against current regulatory, vendor, and program records before use. Require written ownership for monitoring, screening, returns, and outages.

What capabilities are table stakes in a modern fintech platform in 2026?

Assume Open Banking support is table stakes, then evaluate scope, ownership, auditable evidence, and fallback path. A polished dashboard does not offset weak reconciliation, vague escalation, or unproven exception handling. Request a signed scope exhibit, a support ownership document, and sample evidence from one normal flow and one exception flow.

Which trends are hype for your use case and which are worth immediate budget?

Treat claims as hype when they are not tied to your jurisdiction, program, and first operating phase. Fund capabilities that remove current manual work or risk in your live flow, and treat stablecoin readiness as conditional on corridor-level validation. Ask each vendor to map every claimed benefit to one measurable operating step and disqualify claims that stay generic.

How can you compare vendors quickly without missing compliance and operational risk?

Run a two-pass process: disqualify first on scope, ownership, fallback path, and auditable evidence, then score survivors on fit and cost. This keeps exception-path risk in scope before feature-led scoring. Require one diligence packet per vendor with market sheet, program sheet, support ownership, and pilot output including a forced failure case.

What should you verify first if you plan to support cross-border payouts this year?

Verify live corridor coverage first, then confirm compliance boundaries, return handling, delay handling, and fallback behavior for your exact program. Do not assume one setup works across all markets. Request one market sheet per target corridor plus tests for one normal payout and one exception payout with reconciliation output.

What is the fastest disqualifier when a vendor sounds promising but still feels risky?

If the vendor cannot provide written scope, ownership, fallback path, and auditable evidence, stop the process. References and strong demos do not replace clear operating accountability when money movement fails. Ask for the exact documents your finance, ops, and support owners need to sign off, and treat any unresolved gap as a no-go.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- airc.nist.gov/airmf-resources/airmf/3-sec-characteristicstrusted

- bis.org/fsi/fsisummaries/op_resilience.htmtrusted

- congress.gov/crs-product/R47997trusted

- consumerfinance.gov/rules-policy/final-rules/required-rulemaking...trusted

- consumerfinance.gov/personal-financial-data-rightstrusted

- ecb.europa.eu/press/key/date/2026/html/ecb.sp260323_1~1e06...trusted

- fdic.gov/news/speeches/2026/update-reforms-regulatory...trusted

- federalregister.gov/documents/2024/11/18/2024-25079/required-rul...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

GDPR Compliance Checklist for Freelancers Working With EU Clients

Start by separating the decisions you are actually making. For a workable **GDPR setup**, run three distinct tracks and record each one in writing before the first invoice goes out: VAT treatment, GDPR scope and role, and daily privacy operations.

Right-to-Disconnect Rules for Freelancers in Cross-Border Contracts

If right-to-disconnect rules do not clearly cover your status, your contract has to carry the weight. For freelancers, off-hours boundaries are deal terms, not assumptions.

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.