Quick Answer

Compare rails by corridor readiness, control burden, and exception workload, not headline speed. Keep Same Day ACH in the domestic U.S. lane, treat stablecoin as a full on-ramp and off-ramp design problem, and scale only after live payout evidence holds.

What actually matters when choosing a contractor payment rail#

This article is about payout rails for an international contractor program, not transport infrastructure. The real decision is which markets to open first after you price total payment friction, not just the headline transfer fee.

For founders, Payments Ops, and Finance teams, the useful lens is combined: payout fees, foreign exchange handling, operational speed, and compliance burden. Looking at speed alone can hide the work that creates delays, exceptions, and manual cleanup. The Financial Stability Board still frames the cross-border problem in familiar terms: high costs, low speed, limited access, and insufficient transparency.

Use caution with precise 2026 claims. Public coverage is still thin once you narrow from general cross-border payments to verified contractor payout fee tables by rail, corridor, and provider. In its 9 October 2025 consolidated progress report, the FSB says current quantitative data is still insufficient for a complete picture. It also says satisfactory global improvements are unlikely to align with the end-2027 timetable. In practice, expect gaps in public rail-by-rail speed and FX comparisons.

That does not mean you have to guess. It means using public data as directional input, then validating launch-critical details with your provider or banking stack:

- Which payout route is actually available in the corridor

- Who controls FX and where conversion happens

- What beneficiary data is required to release funds

- How exceptions are reported back to your team

A widely used public methodology supports this multi-factor approach. World Bank remittance pricing measures total cost through transaction fee, exchange rate and margin, and speed of service. As of 18 August 2025, it covers 367 corridors across 48 sending countries and 105 receiving countries, but it remains remittance-focused rather than a contractor payout benchmark table.

Compliance should be part of first-pass market screening, not something you leave for late legal review. FATF’s June 2025 update to Recommendation 16 tightened payment-transparency expectations, including standardized originator and beneficiary information for certain peer-to-peer cross-border payments above USD/EUR 1,000. Even when your exact flow does not map cleanly to that threshold, weak payer or payee data can become an operational bottleneck.

The rest of this piece is built for rollout decisions. It gives you a practical way to compare SWIFT-linked flows, stablecoin paths, and domestic legs like Same Day ACH using the factors that actually change unit economics and support load.

Define the rails before comparing them#

Before you price anything, define each rail at the right layer. If you compare messaging, settlement, and domestic speed tools as if they are the same thing, your fee and timing analysis will be misleading.

SWIFT is not the same thing as settlement#

SWIFT is a messaging service, not the settlement mechanism. It is often used in cross-border wire transfer flows, while the wire transfer is the bank-to-bank movement of money, whether domestic or between a U.S. and an international account. When a provider says it supports SWIFT, ask what SWIFT covers in the flow and which bank or intermediary actually moves and settles funds.

Stablecoin means both sides of the conversion path#

For this article, stablecoin paths include both the asset and the conversion services around it. Federal Reserve analysis of payment stablecoins describes a stablecoin as a crypto asset designed to maintain stable value relative to a reference asset. Contractor payouts can require a stablecoin on-ramp for funding and a stablecoin off-ramp for cash-out where supported. If one side of that conversion path is weak for the payee, your speed expectation can fail at the last mile.

Keep domestic ACH separate from cross border design#

Same Day ACH is a U.S. domestic ACH speed option, not a global rail. It is same-business-day processing within the ACH Network, reaches virtually every bank and credit union account in the United States, and supports payments of up to $1 million. Use it as a domestic leg optimization, not as a substitute for cross-border wire or stablecoin route design.

Payee labels change the requirements#

Payee classification can change which legal terms apply, so keep labels precise early. IRS guidance says independent contractor status depends on the facts in each case, not the label alone. Terms like subcontractor and foreign contractor can be legal-framework specific, so tie them to the jurisdiction and contract structure you are actually using.

If you want a deeper dive, read Same-Day ACH for Platforms: How to Speed Up Contractor Payments Without Wire Transfer Fees.

Separate what is known from what is unknown in 2026#

Make a hard split here: some operating realities are known, and some 2026 planning inputs are still unverified. What is known is that paying an international contractor base creates friction across currencies, tax/compliance, payment speed, reliability, and contractor experience. What is not known at a publish-safe level is rail-by-rail 2026 fee tables, universal foreign exchange (FX) spread ranges, or authoritative settlement benchmarks across providers, corridors, and payout programs.

Two rail signals are solid at a design level. The SWIFT global payment network remains a major cross-border messaging layer, but it is not a clearing or settlement layer. Stablecoin routes are also in scope, but only when the full conversion path works, including both the stablecoin on-ramp and stablecoin off-ramp. Access and regulatory treatment can still be uneven across jurisdictions.

Do not turn those facts into false precision. Public benchmark coverage cited here is not 2026-complete: the World Bank downloadable remittance dataset covers 2011 to Q1 2025, and the site shows a last update of August 18, 2025. Use that as context, not as proof for 2026 corridor-level fee or timing claims.

If your launch case depends on exact fee or speed promises, pause and verify the specific corridor and program. At minimum, confirm:

- Provider fee schedule for the exact country pair and payout method

- FX pricing method or spread disclosure

- Funding cutoff times and expected processing windows

- Payee-side cash-out or bank receipt availability

- Hold, return, and compliance review conditions

A common failure pattern across rail types is assuming one fast or global component makes end-to-end outcomes predictable. Compare rail categories now, but do not lock go-to-market math until provider-specific and market-specific data is confirmed.

Compare rail choices using operational criteria#

Choose rails by operational fit first. Predictability, reconciliation load, and exception handling can matter as much as headline speed or fee claims.

| Rail choice | Cost components to model | Operational latency points | Exception handling burden | Reversibility |

|---|---|---|---|---|

| SWIFT global payment network | Sending and receiving fees, possible intermediary charges, FX conversion charges, internal reconciliation time | Correspondent-bank chain hops and bank processing windows along the path | Medium to high when multiple institutions are involved, because SWIFT is a messaging layer and intermediary banks may sit in the chain | Not standardized across all cases; investigation, return, and recall outcomes depend on banks and payment stage |

| Wire transfer | Bank wire fee, possible intermediary or receiving-bank deductions, FX charges when conversion applies, internal matching and support time | Sender-bank and recipient-bank processing windows, plus intermediary handling when used | Medium, often in tracing deductions, confirming receipt, and resolving rejected details | Product-specific and bank-specific; confirm recall, rejection, and return handling for the exact wire flow |

| Stablecoin route | On-ramp fee, possible network fee, off-ramp fee, conversion spread when cash-out currency differs, internal wallet and cash-out reconciliation | On-ramp funding, transfer processing, off-ramp compliance checks, local cash-out availability | Medium to high; friction is often at on-ramp and off-ramp access, compliance holds, or cash-out | Finality and refund handling are provider-dependent; verify pre-off-ramp and post-off-ramp handling, not just transfer status |

Total cost is not the transfer fee#

Model total cost in three separate buckets:

- Explicit payout fee

- FX cost, meaning the applied exchange rate plus any margin

- Internal ops cost, including reconciliation, contractor support, and exception resolution

That third bucket is often underestimated. In practice, small pricing improvements do not matter much if your team cannot capture them operationally. The more useful question is whether the rail reduces manual work, not just whether it posts a lower fee.

Set the tradeoff first, and pilot stablecoin when liquidity speed is critical#

Start with the tradeoff, not the trend. If predictable bank delivery matters most, a SWIFT-based payout design is often the baseline. If speed to liquidity is critical and you already have strong compliance coverage for on-ramp and off-ramp flows, evaluate stablecoin corridors in a pilot before wider rollout.

Some cross-border stablecoin models are framed as reducing reliance on intermediaries, but only when the full path works in practice, including on-ramp, off-ramp, and local cash-out access.

Same-Day ACH is a domestic leg optimization, not a global replacement rail#

Use Same-Day ACH to improve domestic timing, not to solve cross-border design. Current ACH eligibility excludes international transactions. Public references describe Same-Day ACH up to $1 million today, while $10 million appears as a proposal with a March 19, 2027 proposed effective date.

That makes it useful for domestic funding or treasury timing around your broader cross-border design, but not a replacement for SWIFT, wire, or stablecoin decisions for foreign contractor payouts.

Build a country rollout sequence that reduces regret#

Set country order by execution friction, not market hype. Launch first where local rails are mature and documentation is manageable, then pilot markets with newer rail conditions or higher policy-change risk.

A practical sequence is Mexico and Brazil first, Colombia as a controlled second wave, and Argentina later unless you already have enough volume and support capacity for higher exception handling. Use this as a sequencing tool, not a universal ranking.

A practical Latin America scorecard#

| Market | Payout complexity | FX friction | Compliance overhead | Why it lands here |

|---|---|---|---|---|

| Mexico | Medium | Medium | Medium | SPEI supports near-real-time transfers 24/7, so the domestic leg is strong. Cross-border documentation still drives effort. |

| Brazil | Medium | Medium | Medium | Pix supports transfers in seconds at any time, including non-business days. Domestic speed helps, but cross-border funding, FX, and reconciliation still require control. |

| Colombia | Medium to High | Medium | Medium to High | Bre-B launched in 2025, so production readiness should be validated in pilot rather than assumed. |

| Argentina | High | High | High | Official FX-market rules changed in 2025, including changes effective 14/04/25 under BCRA Communication A 8226, so ongoing rule monitoring and exception planning matter more before scale. |

Local instant rails do not remove cross-border friction. The FSB’s 2025 report says progress has not yet translated into tangible global end-user improvements, and average costs remain sticky.

Apply the same caution to fee claims for 2026. World Bank remittance-price downloads currently cover 2011 to Q1 2025, not 2026. Use sequencing to reduce operational regret, not to chase hard fee claims you cannot verify.

Sequence by friction, then validate with intake quality#

Start with the markets where operations are easiest to control, then prove that your intake data can survive the real payout flow.

- Launch first where domestic rails are already always-on or near-real-time, typically Mexico and Brazil with SPEI and Pix

- Pilot next where rail conditions are improving but still newer in production terms, such as Colombia with Bre-B

- Delay where policy-change risk is more likely to create rework, such as Argentina under recent FX-rule changes

If a country needs heavy exception handling at low payout volume, delay launch and prioritize markets with more established rail and policy conditions.

Before first live payouts, verify data capture quality. FATF’s June 2025 Recommendation 16 update includes standardized information requirements for peer-to-peer cross-border payments above USD/EUR 1,000, such as name, address, and date of birth. If your intake and provider handoff cannot carry required fields reliably, that market is not operationally ready.

Adjust sequencing for payee mix#

Country friction is only part of the decision. Payee mix can also change support and compliance workload. Independent-contractor payouts are tied directly to the person performing the work result. By definition, subcontractor flows add another contractor layer.

That is why sequencing should include both market friction and payee profile. A medium-friction market with mostly direct independent-contractor payouts can be a better first launch than a market with more subcontractor layers. For deeper regional execution detail, see How to Pay Contractors in Latin America: Brazil Mexico Colombia Argentina Rails Compared.

Handle classification and agreement risk before scaling payouts#

Do not scale country payout batches until worker classification, agreement terms, and payout eligibility checks line up. Treating those as separate decisions can create avoidable compliance and reconciliation risk later.

Independent contractor and subcontractor flows do not have the same control surface. In the U.S., federal employment tax status is based on common-law facts across behavioral control, financial control, and the relationship of the parties. A written contract is only one part of that evidence. Misclassification also has real labor consequences, including loss of minimum wage and overtime protections where a worker is legally an employee.

Classification changes what you must verify#

Classification affects required payee, tax and identity data, and pre-payment checks. In practice, verify:

- Direct independent-contractor flows: payee identity and tax record consistency are core controls. In U.S. payer workflows, Form W-9 requires the TIN to match the name on line 1 to avoid backup withholding exposure.

- Subcontractor flows, for example UK CIS: payments must account for subcontractor tax status, first payment requires HMRC confirmation that the subcontractor is known, and verification details must exactly match registered details.

What the contractor agreement must support#

A production-ready contractor agreement should be usable for payouts, not just signed. At minimum, it should make these points clear:

- Identity consistency

The contracting party should match the verified payee identity and tax record used for payout eligibility.

- Basis of payment

The agreement should define what is being paid for and on what basis, so payout execution follows the same contract logic.

- Dispute handling

The agreement should include a defined path for disputes arising under or relating to the contract.

The common failure mode#

A common failure mode is drift between contract records and verified payee details. That mismatch can create name-matching exceptions and questions about whether payment aligns with the contracting party.

The checkpoint before country-level batches#

Before enabling a country batch, require a short pre-release review of:

- Classification outcome and jurisdiction-specific logic used

- Contract readiness on file, for example a signed agreement, tender, or work order where applicable

- Payout eligibility controls, including payee-name consistency and required tax or registration status

For U.S. records, reject obviously incorrect TIN input early, for example not 9 digits or containing non-numeric characters. Backup withholding may need to start immediately when required data is missing or clearly wrong. For UK CIS subcontractor flows, complete HMRC CIS verification before first payment.

Design the money flow so Finance and Ops can trust it#

Once payee identity and eligibility checks are clean, keep the money flow in a fixed sequence: collect funds -> track balance state -> run FX if needed -> execute payouts -> reconcile bank outcomes back to contractor payments. That order keeps payout operations explainable and auditable.

Keep collection separate from payout execution#

Do not collapse collection and disbursement into one control. In a collect-then-disburse model, funds land on the platform side, move through balance states (for example, pending to available), and only then should be used for payout execution.

In Gruv terms, map collection to Virtual Accounts and disbursement to Payouts, with ledger-backed records across both. The key operator point is that a virtual account is a tracking and reconciliation identifier, not where funds are held directly. If that distinction gets blurred, collected funds, held balances, and sent payouts can become harder to reconcile day to day.

Convert currency before you create the final payout#

Run FX against held balances before creating the payout instruction. That keeps a clean record of source currency, conversion event, destination currency, and final disbursed amount.

Avoid pushing FX logic outside the payment record and leaving only a net payout amount in ops tools. That can weaken auditability and slow investigations. For SWIFT-network flows, carry the payment tracking reference through the lifecycle, including UETR where available, so cross-border status can be traced.

Treat retries and webhooks as control points#

Retries and webhook events are not just technical details. They are control points.

Make payout creation idempotent so retries do not create duplicate side effects. An idempotency key lets the API recognize a retry of the same operation and return the same result, and guidance allows keys up to 255 characters.

Use webhook-driven updates as the source for asynchronous payout-state changes, and design for duplicate event delivery. Do not assume exactly-once delivery or perfect ordering. Store the provider payout ID, deduplicate events, and enforce valid state transitions in your payout state machine.

Give operators visible status and exportable evidence#

Finance and Ops need two outputs: clear payout status visibility and reconciliation artifacts they can export. Status monitoring should cover lifecycle states such as pending, in_transit, paid, canceled, and failed. Reconciliation should map bank-received payouts to underlying transactions and support CSV export for accounting workflows.

Your evidence pack should tie together collection reference, internal payment ID, payout ID, FX record (if used), beneficiary details, and network tracking references such as UETR for SWIFT flows. If your team uses Xero, keep finalized, traceable records aligned with accounting and keep full payment-event history available for investigations. For accounting handoff detail, see Xero + Global Payouts: How to Sync International Contractor Payments into Your Accounting System.

Prepare for failure modes before they hit production#

Design exception handling before launch. Otherwise, cross-border payouts can become slow, expensive, and hard to resolve.

Different rails fail in different ways. Cross-border wire transfers can lose clarity across intermediary banks, FX assumptions may no longer hold at release time, and stablecoin flows can still fail at redemption or local cash-out.

Where the rails usually break#

| Rail or step | Common breakpoint | What to verify first |

|---|---|---|

| Cross-border wire transfer | Delays or unclear status across intermediary banks | Tracking reference, beneficiary details, and whether funds are in transit, held, or returned |

| Foreign exchange (FX) step | Rate or funded-balance assumptions no longer match at release time | Whether conversion was completed before payout creation, and whether approval lag changed the expected destination amount |

| Stablecoin off-ramp | Redemption or local cash-out stalls due to banking-path limits | Whether that region and bank can redeem through the available wire or participating banking network path |

Set expectations by rail, not by habit. Domestic Fedwire is immediate, final, and irrevocable once processed, while cross-border payments in correspondent banking networks are generally slower, more expensive, and more opaque than domestic payments.

Treat FX timing as a control point. If payout approval or release is delayed, re-check converted amount and available balance before final submission.

Treat stablecoin routes as policy-sensitive, not friction-free. Stablecoins are designed to maintain stable value, but cash-out can still depend on bank and rail availability, and FATF’s March 2026 stablecoin update highlights illicit-finance misuse risk.

Put control points where failure is easiest to catch#

Catch problems before release whenever possible. Run KYC, screening, and due diligence before payout release. FATF and EU guidance both center these controls, so scale should follow policy readiness, not the reverse.

Pair status monitoring with a defined investigation path. Assign ownership for held or returned funds and for payments stuck between states, with clear rules for cancellation, retry, and escalation. Where U.S. remittance-transfer rules apply, account for the 30-minute cancellation window and the potential investigation timeline that can generally run up to 90 days after a promptly reported error.

Reduce breadth before your queue breaks#

If exceptions outpace your team’s ability to investigate and reconcile, narrow rail or country coverage before expanding into new markets.

For each incident, keep an evidence pack tied to the payout attempt so investigation does not rely on manual reconstruction. Include enough records to reconstruct the payout path and decision history end to end.

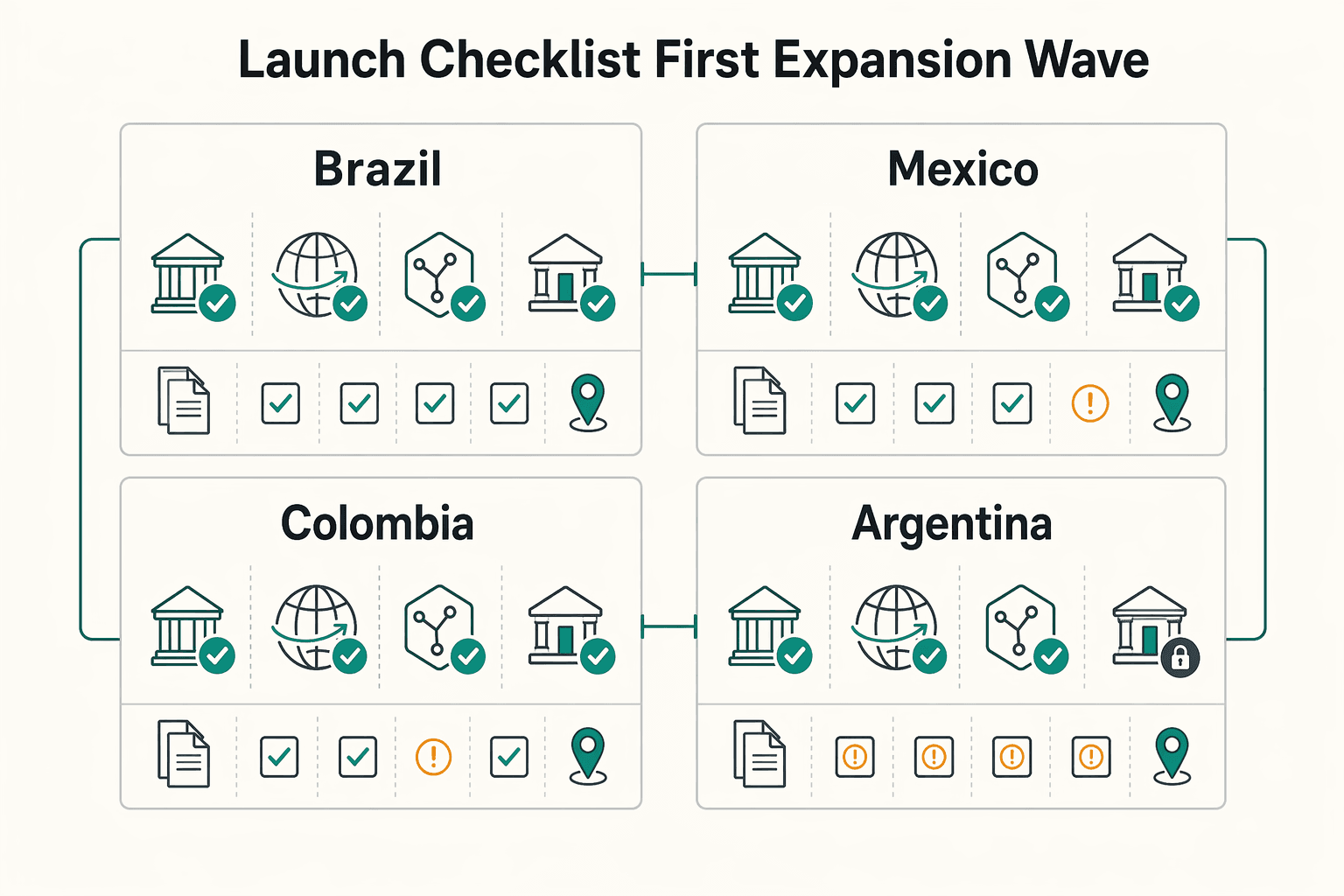

Use a launch checklist for the first expansion wave#

Use launch gates, not assumptions. Open a new market only when your program setup, rail path, and payee records are ready for that specific country flow.

Start with rail eligibility by market. Confirm what your program can actually send through the SWIFT messaging network, any stablecoin route you support, and local bank payout paths. In Latin America, local infrastructure differs by country, so "bank payout supported" is not enough for launch approval.

| Market | Local payout path to verify | What to confirm before launch |

|---|---|---|

| Brazil | Pix | Whether your provider supports contractor payouts to the reachable path, and which beneficiary identifiers and account-name checks are required |

| Mexico | SPEI | Whether local payouts use SPEI, which beneficiary details are mandatory, and how you will monitor payment status after release |

| Colombia | Bre-B | Whether your program can reach the immediate-payment path and what destination account data must be collected up front |

| Argentina | Transferencias inmediatas 3.0 | Whether the destination bank or wallet can receive through the supported path and whether your provider returns usable status data |

Market-by-market verification matters because domestic scheme speed does not automatically become end-to-end cross-border payout speed. SPEI indicates transfers should not take more than 30 segundos, and Transferencias 3.0 indicates crediting in up to 15 segundos. You still need to confirm that provider flow, compliance review, funding, and endpoint handling preserve that experience.

Validate the payee before enabling the rail#

Your second gate is payee readiness. Determine worker classification before enabling contractor payouts. Then confirm your required artifact set is complete: contractor agreement if your program requires one, identity and compliance status, tax identity handling where applicable (such as Form W-9 or Form W-8 BEN), and destination account checks.

Do not treat onboarding and payouts as separate tracks. Before first payout, verify that payee name, country, classification result, tax record, and destination account or wallet record all align to one profile.

Stablecoin routes need an added compliance check. FATF updated Recommendation 16 on 18 June 2025 and included Travel Rule context for virtual assets. Confirm jurisdictional handling, required originator and beneficiary data, and whether local off-ramp or cash-out is available for that market.

Pilot two markets before you widen the map#

Keep the first wave narrow enough to learn. For a first Latin America wave, run a controlled pilot in two markets (for example, Brazil and Mexico), then expand only if pilot evidence supports it. The point is to validate rail coverage, onboarding quality, exception handling, and reconciliation with fewer moving parts before broad rollout.

Define the evaluation plan before first payout. If success criteria are unclear in week one, the pilot is not functioning as a decision gate. For deeper country execution detail, see How to Pay Contractors in Latin America: Brazil Mexico Colombia Argentina Rails Compared.

Set hard go or no-go checks#

Use three go or no-go gates before expansion:

- KPI performance by rail and market on completed pilot volume (for example: payout success, speed, cost, and transparency)

- Time to resolution on failures, with clear ownership for investigations

- Reconciliation completeness, so each payout ties back to funding, any FX step, approval, submission reference, and final outcome

If any gate fails, pause expansion. Incomplete reconciliation at pilot scale is a strong stop signal and becomes harder to unwind as volume grows.

Related: Independent contractor rule overview.

Before scaling beyond a pilot cohort, map your go/no-go checks to a single operational flow in Gruv Payouts so status tracking and exception handling stay consistent.

Track the right metrics every month#

Use your monthly review to make expansion decisions, not to report vanity metrics. To decide whether to expand, pause, or change rail mix, track cost, speed, and control health as separate views.

Start with blended payout cost, then split it into what you can verify: explicit fees and FX effects, with manual operations effort tracked separately from your internal data. Posted transfer fees alone are incomplete, and FX margin can materially change real cost. Keep a monthly check that ties funding amount, FX rate used, amount delivered, and manual handling to the same payout record. If you cannot tie those fields together, your cost view is not decision-ready.

Track speed as a distribution, not an average. Keep time-bucket attainment, for example within one hour and within one business day, plus your own median and tail latency where internal data supports it. That prevents a stable average from hiding a worsening tail.

Track control health as its own monthly dashboard: policy-gated payouts, exception volume, and unresolved cases by international contractor segment. This keeps monitoring aligned with a risk-based control model and makes ownership gaps visible before they scale.

Do not anchor to assumed “2026 public benchmarks.” Public remittance benchmark data was last updated on August 18, 2025. Prioritize your own monthly operating data when re-ranking markets and rail mix.

Conclusion#

The better choice is not the rail that looks fastest in isolation. It is the rail-country mix with the best total operating profile across delivery reliability, compliance friction, reconciliation effort, and acceptable speed.

That standard matches how cross-border payments are being evaluated more broadly: speed, transparency, access, and cost together, not speed alone. In practice, a route is only strong if your team can operate it consistently from payout initiation through receipt and exception handling.

Keep known facts separate from missing benchmarks. As of the FSB’s 9 October 2025 progress report, end-user improvements were still not materially visible at the global level, and quantitative data was still incomplete. Most targets remain set for end-2027. If your expansion case depends on precise 2026 rail-by-rail fee tables or universal settlement benchmarks, validate your corridor assumptions before committing product or go-to-market resources.

SWIFT performance shows why this matters: BIS reports an overall median processing time of less than two hours, but route-level medians range from less than five minutes to more than two days. In some corridors, longer times are associated with capital controls and related compliance processes. Averages can look strong while still hiding route-level tail risk that can drive exceptions and delays.

Your next move should be disciplined. Score, pilot, then scale:

- Score market and route together. For each target country, document rail options, receiving-bank compatibility, likely compliance steps, and the exception load your team can absorb.

- Define pilot checkpoints before launch. Track initiation-to-receipt time, delivered amounts, policy-gated payouts, returns, and time to resolution, and set the evaluation framework in parallel with pilot design.

- Scale only where results hold. Use pilot outcomes to decide whether expansion is warranted, and narrow scope when exception volume exceeds operational capacity.

For teams making 2026 decisions on global contractor payment fees, speeds, and rails, the goal is controlled proof, not false certainty. Test small, learn by corridor, and expand only when both performance and compliance are proven in live conditions.

If you want to validate rail and country fit against your actual compliance and ops constraints, talk to Gruv.

Frequently Asked Questions

What are the main rails for global contractor payouts in 2026?

The core rails in scope are SWIFT-based cross-border bank payouts, bank-wire paths, and stablecoin payout flows. Keep one distinction clear: SWIFT is messaging infrastructure between institutions, not settlement itself. That means payout timing is not determined by SWIFT messaging alone.

What actually drives total payout cost besides visible transfer fees?

Visible transfer fees are only part of total cost. Total cost can also include FX margin and, in some cases, recipient-side fees. Before you label a route "low cost," tie each payout to funded amount, FX rate applied, and amount delivered.

When should a platform choose SWIFT over stablecoin rails?

Choose SWIFT when existing bank connectivity and established institutional usage matter more than testing a newer route. Stablecoin treatment is still evolving across jurisdictions, so rollout certainty can vary by market. If your off-ramp, compliance review, or treasury policy is not already settled, do not force a stablecoin route into production based on headline speed alone.

Is Same-Day ACH a global payout rail or a domestic optimization step?

Same-Day ACH is a domestic optimization step, not a global cross-border rail. ACH is a nationwide batched network, and Same-Day ACH excludes international ACH transactions and has a cited eligibility ceiling of $1,000,000. Use it for a U.S. funding or domestic disbursement leg where it fits, not as a replacement for cross-border rails.

How should we prioritize country rollout across Latin America markets?

Do not force one fixed rollout order for Brazil, Mexico, Colombia, and Argentina without your own payout and exception data. Domestic rail conditions differ by country: Brazil's Pix is available 24/7, Mexico's SPEI supports payments in seconds, and Argentina's Transfers 3.0 cites online crediting within a maximum of 15 seconds. Start where you can verify local bank compatibility, FX handling, and exception rates in a pilot, then expand based on observed results. For deeper country detail, see How to Pay Contractors in Latin America: Brazil Mexico Colombia Argentina Rails Compared.

What data is still missing before we can claim hard 2026 fee and speed benchmarks?

What is still missing is verified 2026 rail-by-rail fee tables by corridor and comparable 2026 settlement-time benchmarks across SWIFT, wire, and stablecoin contractor payout routes. The World Bank remittance data is useful context, but it is a time-bound snapshot that varies over time, and the latest update was August 18, 2025. Broader cross-border target programs also run through end-2027. Before making hard claims, build your own corridor-level evidence pack with effective FX used, delivered amounts, and initiation-to-receipt timestamps.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 1 external source outside the trusted-domain allowlist.

- consumerfinance.gov/consumer-tools/money-transfers-revisions-sep...trusted

- federalreserve.gov/econres/notes/feds-notes/payment-stablecoins...trusted

- irs.gov/businesses/small-businesses-self-employed/in...trusted

- irs.gov/businesses/small-businesses-self-employed/in...trusted

- gov.uk/government/publications/construction-industr...external

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.

How to Respond to a Subpoena for Business Records

Move fast, but do not produce records on instinct. If you need to **respond to a subpoena for business records**, your immediate job is to control deadlines, preserve records, and make any later production defensible.

A US Expat's Guide to Investing in UCITS ETFs to Avoid PFIC Issues

The real problem is a two-system conflict. U.S. tax treatment can punish the wrong fund choice, while local product-access constraints can block the funds you want to buy in the first place. For **us expat ucits etfs**, the practical question is not "Which product is best?" It is "What can I access, report, and keep doing every year without guessing?" Use this four-part filter before any trade: