Quick Answer

Tipping features on gig platforms should be designed as a funds-flow and reporting choice, not just a UX prompt. The platform needs to separate optional tips from required charges, set form mapping before launch, collect W-9 or W-8 details when needed before payout, and preserve a traceable record from tip event to adjustment, payout status, tax profile, and ledger outcome.

Why tipping design can make or break expansion decisions#

Treat tipping as a funds-flow decision first and a product feature second. The visible choice is the tip prompt. The harder choice is the operating model behind it: who collects funds, whether the amount is voluntary, when it is released, what tax identity data you hold, and what records you can defend later.

This is why tipping decisions can age badly when they are made as UX choices alone. A local flow can look simple at launch, then become expensive once reporting, reversals, and cross-market rollout catch up.

Tax treatment starts with the money path#

Your tip design affects tax handling from day one because gig workers must report gig income even when no information form is issued. If customers can add gratuity, your system should clearly distinguish an optional tip from a required charge, since the IRS treats mandatory service charges differently from tips.

Before launch, store a clear event flag showing whether the amount was optional or required at checkout. If you may need to file information returns, collect Form W-9 details before payouts begin, not after reconciliation issues appear.

Reporting pain usually appears in reconciliation#

Much of the operational pain shows up in reconciliation, not in abstract policy. Form 1099-K reports gross payment amounts, so refunds, credits, and fees can create mismatches when tip and reversal logic is weak.

| Record element | Capture | Context |

|---|---|---|

| Original tip event | The original tip event | Part of the practical minimum record chain |

| Adjustment or reversal event | Any adjustment or reversal event | Refunds, credits, and fees can create mismatches when tip and reversal logic is weak |

| Payout status | Payout status | Needed to trace the amount through reconciliation |

| Worker tax-profile status | Worker tax-profile status | Relevant if Form W-9 details may need to be collected before payouts begin |

| Ledger mapping | Where the amount landed | Needed for reconciliation and defensible records later |

Do not hard-code a single 1099-K threshold into product logic. Current IRS materials include different threshold statements in different contexts. Your reporting logic should be versioned by tax year instead of embedded as a fixed assumption.

A practical minimum record chain is the original tip event, any adjustment or reversal event, payout status, worker tax-profile status, and the ledger mapping for where the amount landed.

Expansion makes local shortcuts expensive#

Shortcuts that feel manageable in one market can get expensive once you expand. IRS guidance for digital platforms ties operating design to worker classification and required reporting, withholding, filing, and deposits. In the EU, DAC7 adds platform reporting obligations across both cross-border and non-cross-border activities. It entered into force on 1 January 2023, and the first exchange for calendar year 2023 took place at the end of February 2024.

Even where IRS guidance notes that qualifying gig workers may deduct up to $25,000 in tips each year from 2025 through 2028, platforms still need accurate, controllable records.

So the real decision is not just whether to offer tipping. It is which tipping model keeps tax treatment, reporting workload, payout risk, and market portability manageable as volume grows.

You might also find this useful: Music Royalty Tax Compliance: How Platforms Handle 1099-MISC vs. 1099-NEC for Artist Payments.

Start with selection criteria and who this list is for#

Use this list if you operate a marketplace or digital platform in the gig economy and need to choose how gratuities move from customer to contractor under IRS reporting rules and cross-border constraints.

| Criterion | Focus | Grounded detail |

|---|---|---|

| Tax clarity | Traceable, reportable tip income | Section 224 creates a qualified-tip deduction framework; IRS guidance says self-employed workers may deduct up to $25,000 in qualified tips for 2025 through 2028 when those tips are reported on Form 1099-K, Form 1099-NEC, or Form 1099-MISC; gig income still must be reported even if no information return is issued |

| Reporting burden | Match forms to payment flow | Payment card and third-party network payments are reported on Form 1099-K, not Form 1099-NEC or Form 1099-MISC; nonresident-alien contractor payments can shift to Form 1042-S |

| Payout risk | Operate within current controls | If tax-profile collection and exception handling are not ready, simpler payout designs are usually safer than complex gratuity logic |

| Reconciliation effort | Preserve a checkable chain | Prefer models that keep tip event, adjustment, payout status, and tax-profile status tied to reporting outputs |

| Market portability | Support operator-level duties across markets | U.S. portability depends on form-mapping logic; in DAC7-heavy regions, reporting obligations sit with platform operators, including some non-Union operators active in the EU |

Skip this section if you only need personal Form 1040 filing help. This is for operator decisions: worker classification, reporting and withholding workflows, payout behavior, and records that support reporting outcomes. Score each tipping model on the same five criteria:

- Tax clarity

Check whether the model keeps tip income traceable and reportable. Section 224 creates a qualified-tip deduction framework, and IRS guidance says self-employed workers may deduct up to $25,000 in qualified tips for 2025 through 2028 when those tips are reported on Form 1099-K, Form 1099-NEC, or Form 1099-MISC. Taxpayers still must report gig income on their tax return even if no information return is issued.

- Reporting burden

Do not assume one form fits every flow. IRS instructions state certain payment card and third-party network payments are reported on Form 1099-K, not Form 1099-NEC or Form 1099-MISC, and nonresident-alien contractor payments can shift to Form 1042-S.

- Payout risk

Prioritize models your team can operate with current controls. If tax-profile collection and exception handling are not ready, simpler payout designs are usually safer than complex gratuity logic.

- Reconciliation effort

Prefer models that preserve a checkable chain from tip event to adjustment, payout status, and tax-profile status so finance can tie money movement to reporting outputs.

- Market portability

In the U.S., form-mapping logic is central. In DAC7-heavy regions, reporting obligations sit with platform operators, including some non-Union operators active in the EU. Portability depends on whether your model can support those operator-level reporting duties.

For related estimated-tax context, see How to Make a 'Safe Harbor' Estimated Tax Payment.

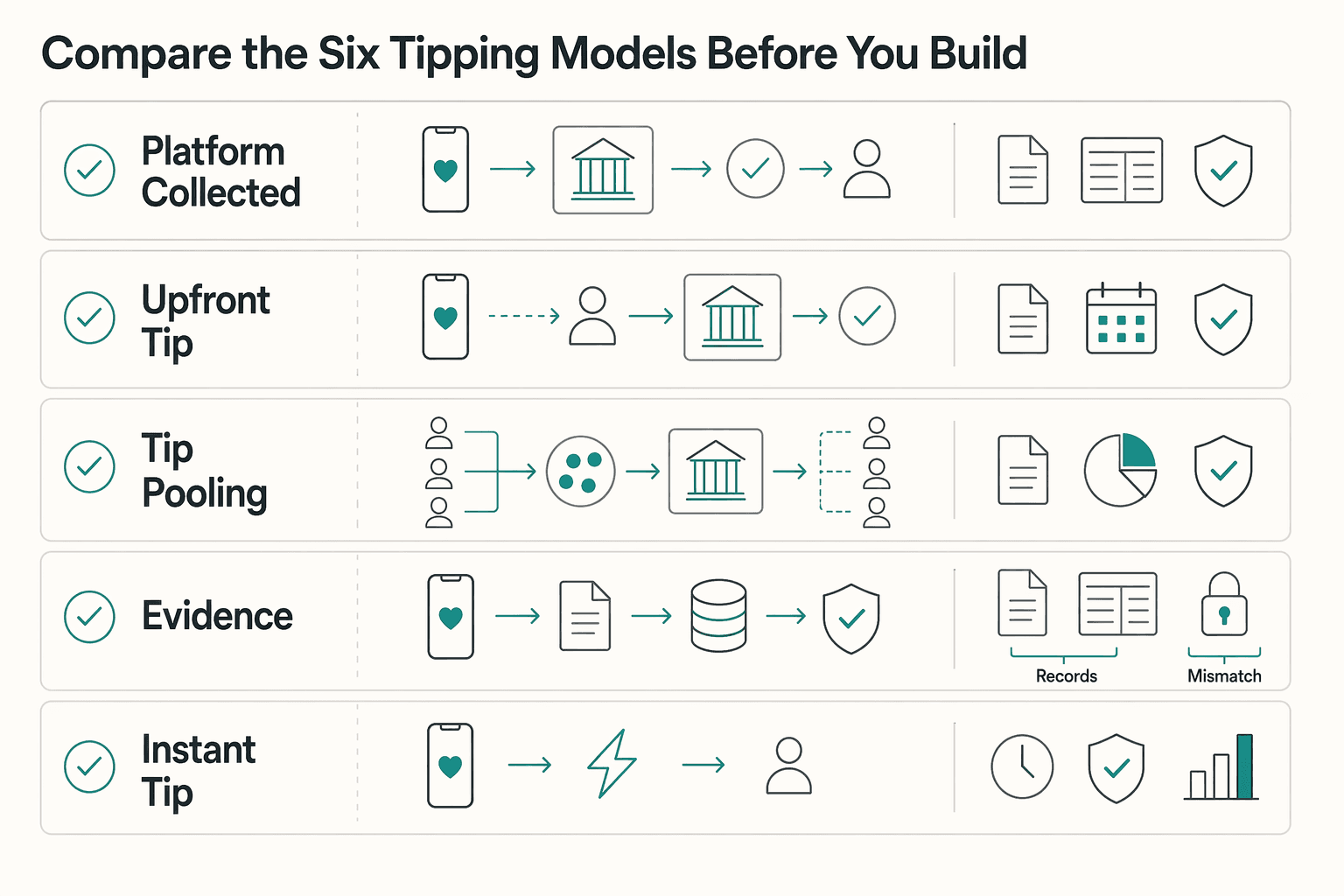

Compare the six tipping models before you build#

If you need a starting point, many early-stage U.S.-first launches begin with platform-collected tips after service completion. If you already run stronger cross-border compliance operations, delayed or batched tip payout with reconciliation can be easier to operate at scale.

This still matters even below filing triggers. IRS FAQs updated January 2026 say TPSOs are not required to file Form 1099-K unless payments exceed $20,000 and more than 200 transactions. Platforms may still issue Form 1099-K below that level, and workers must still report all income. The practical test is whether your model keeps a defensible trail from tip event to payout state to reporting output.

| Model | Best for | Tip timing | U.S. implications (1099-K / 1099-NEC / Schedule SE / Form 1040 support) | Tax/reporting complexity | Payout failure risk | Reconciliation burden | Market portability | Cross-border fit (W-8, DAC7, FATCA, Form 8938 context) |

|---|---|---|---|---|---|---|---|---|

| 1. Platform collected after service completion (Common early-stage choice) | U.S.-first marketplaces needing a clear service-to-tip link | After fulfillment, before release | If settled on payment card or third-party network rails, amounts may be reportable on 1099-K and should not also be reported on 1099-NEC. Can provide clearer worker visibility for Schedule SE and may reduce Form 1040 mismatch support. | Medium | Medium | Low to medium | Good | Moderate. Scales better once W-8 BEN/W-9 collection is reliable; DAC7 reporting obligations can still apply where in scope. |

| 2. Upfront tip at checkout | Standardized services with low cancellation and mature reversal controls | Before fulfillment | Same 1099-K vs 1099-NEC separation, but reversals can complicate gross-to-net mapping and can increase Form 1040 support questions. | Medium to high | Medium | High | Moderate | Moderate if reversal history and tax-profile snapshots are retained. |

| 3. Tip pooling and redistribution by platform | Team or shift-based service models | Collected once, allocated later | Seller-level attribution is harder, which can increase uncertainty around reporting outputs and can raise Schedule SE/Form 1040 support load. | High | Medium to high | Very high | Weak | Weak to moderate. DAC7 is operator-level, and seller reporting workflows still need defensible allocation records. |

| 4. Off-platform tips with platform recordkeeping only | Cash or external-wallet markets where platform does not move funds | Outside platform rails | Platform visibility into settlement is limited. Workers still must report income even if no form is issued, so Schedule SE/Form 1040 support burden can rise. | High | Low on payout rail, high on support risk | High | Mixed | Weak to moderate. Not holding funds does not necessarily remove DAC7 operator duties where applicable; user support complexity can rise across markets. |

| 5. Instant tip payout to contractors | Verticals where immediate access to funds is central and controls are already strong | Immediate or near real time | Form destination depends on rail, but fast release can increase exception-handling pressure. Instant payments are generally final and irrevocable, which can raise post-period correction risk if logic changes after filing preparation. | High | High | High | Moderate | Moderate at best unless W-8/W-9 status and eligibility checks are complete before release. |

| 6. Delayed or batched tip payout with reconciliation (Common in mature multi-country operations) | Platforms balancing release speed with control checks and exception handling | Scheduled release after checks | Can be easier to align held, released, and adjusted amounts with 1099 treatment, with fewer support mismatches for Schedule SE/Form 1040 workflows. | Medium | Low to medium | Low to medium | Strong | Strong. Better fit when W-8 status, DAC7 reporting fields, and account classification checks are part of release review. Keep Form 8938 separate as the taxpayer's filing obligation. |

The table gives you a starting point, but two implementation choices matter more than the label on the model: how you map forms and when you allow payout.

Set your 1099 mapping before launch. IRS instructions state payments reportable on Form 1099-K are not additionally reported on Form 1099-NEC or 1099-MISC. Changing logic after forms are filed creates correction work.

For U.S. onboarding, Form W-9 is the core control point, and IRS guidance says it is the first step for independent-contractor reporting. Where nonemployee compensation is reportable outside 1099-K rails, missing or invalid TIN data can trigger 24% backup withholding. For foreign persons, the parallel checkpoint is Form W-8 BEN.

For cross-border rollout, keep obligations distinct. DAC7 places reporting duties on platform operators, including certain non-Union operators active in the EU, and covers domestic and cross-border activity. FATCA/Form 8938 are separate from DAC7. Form 8938 is attached to the taxpayer's annual return when thresholds are met, generally $50,000 aggregate value, and is separate from FBAR.

Before go-live, test at least three contractor profiles - valid W-9, valid W-8 BEN, and missing tax profile - across a normal tip, a reversed tip, and a held payout. If finance cannot trace the tip event, payout status, tax-profile snapshot, and expected reporting destination in one audit trail, the model is not ready.

Related: Gig Worker Tax Compliance at Scale: How Platforms Handle 1099s W-8s and DAC7 for 50000+ Contractors.

Model 1 Platform-collected tip after service completion#

For U.S.-first launches, this can be a practical starting model if your team can keep a complete record from service completion through payout and reporting.

What the model actually looks like#

The flow is straightforward: the service is completed, the customer adds or confirms a tip, the platform records that tip to the completed job, and payout follows your release rules. Large platforms already run post-service windows, which suggests the model is operationally viable. Uber says riders can tip up to 30 days after a trip, and Instacart says customers can increase a tip up to 14 days after delivery or reduce it within 2 hours.

Why it is workable for U.S. reporting#

It does not remove tax complexity. It can be easier to implement when the tip is tied to a completed service event and reconciliation controls are in place. For U.S. operators, the key reporting split is Form 1099-K versus Form 1099-NEC. IRS instructions state amounts reportable on Form 1099-K are not also reported on Form 1099-NEC or Form 1099-MISC, so you should lock that mapping before launch.

Workers still report tip income on their tax return, including cash and noncash tips. When income is self-employment income, Schedule SE (Form 1040) is used to calculate self-employment tax, and IRS instructions say Schedule SE must be filed when line 4c is $400 or more.

Where this model can create operational pressure#

The main tradeoff is payout timing. A post-service tip window can delay when some tips are final, so your release and communication rules need to be explicit.

Late adjustments also need tight controls. IRS instructions for Form 1099-K report gross amounts without reducing for refunds, fees, credits, or other adjustments. If users can edit tips after payout, finance needs preserved records for the original amount, adjustment timing, and payout state to avoid reconciliation and correction issues.

One more caution: IRS pages currently show different 1099-NEC threshold language, including $600 on one page and $2,000 for payments made after December 31, 2025 on another. Confirm the filing-year rule before hard-coding thresholds.

What to verify before launch#

Do not ship this model until a single audit trail can show all three of these points:

- completed job ID, tip event ID, and payout ID remain linked after edits or reversals

- worker tax profile at payout time is captured

- reporting logic clearly separates amounts expected on Form 1099-K from amounts that could fall under Form 1099-NEC

Need the full breakdown? Read Subscription Billing Platforms for Plans, Add-Ons, Coupons, and Dunning.

Model 2 Upfront tip at checkout before fulfillment#

Use upfront tipping when fulfillment is predictable and your reversal records are strong. Otherwise, cancellations and reassignments can create tax-ops and support friction.

Why teams still choose it#

In high-volume checkout flows, asking for a tip on the same screen keeps the decision in one step. Teams often pilot this in standardized services where pricing and fulfillment are relatively stable.

There is also directional evidence behind testing it. A 2026 SSRN study on DoorDash's December 2023 shift to post-tipping found lower order volume and lower tipping behavior after the change. Treat that as context, not as a universal rule for every vertical.

Where reporting pressure starts#

The hard part is not collecting the tip. It is keeping an auditable record of what happened after checkout when an order is canceled, changed, or reassigned.

Tax obligations do not disappear when records are messy. Gig and tip income are taxable, and workers must report income even when no information return is issued. You also need a clear worker-classification checkpoint because employee and contractor handling differs. If a worker is an employee, cash tips must be reported to the employer and included on Form W-2, with the IRS monthly reporting timing and threshold rules applying to employees.

Failure modes to watch#

A core failure mode is ledger ambiguity: the customer prepays a tip, the service outcome changes, and your systems cannot clearly show whether the tip was retained, reversed, refunded, or reassigned. When that trace is weak, finance, support, and reporting teams can end up with conflicting states.

There is also a marketplace-behavior tradeoff. The same SSRN paper notes reduced upfront incentives can introduce delivery-effort uncertainty in a post-tip model. That helps explain why some teams still prefer upfront prompts in fulfillment-sensitive categories.

Minimum controls before launch#

Keep one transaction trail that covers the original tip amount and checkout timestamp, any order or job status changes after checkout, cancellation or reversal outcomes, the final worker assignment, and the payout state tied to that same trail.

If cancellation rates are volatile, do not default to upfront tipping until reversal logic is consistently auditable for IRS-facing review. This fits best where fulfillment certainty is high and adjustment handling is already mature.

This pairs well with our guide on Permanent Home Test in a Tax Treaty: Meaning, Evidence, and Tie-Breaker Rules.

Model 3 Tip pooling and redistribution by platform#

Use platform-run tip pooling in the United States only if you can consistently show how each pooled dollar was allocated to each final recipient. If you cannot, avoid it until controls are stronger.

This can make sense for team- or shift-based service where the work is genuinely collective. It may support fairness goals and smoother incentives across pooled operations, but it creates a high attribution burden for contractor reporting and worker support.

A pooled share is still tip income to the individual who retains it. Federal tip-pooling regulation treats retained split amounts as that person's tips, and IRS employee guidance similarly treats a worker's share from a tip-pooling arrangement as tip income.

Why support and reporting get harder#

With direct tips, disputes often map to one order and one payout. With pooling, disputes shift to allocation logic: why a worker's share was that amount.

For contractor flows, the reporting problem is recipient attribution, not reporting the same payment flow twice. IRS instructions state payment-card and third-party network transactions reported on Form 1099-K are not also reportable on Form 1099-NEC or Form 1099-MISC. Independent contractors generally report this income through Form 1040 workflows, including Schedule C and, where applicable, Schedule SE when net self-employment earnings are $400 or more. Confirm the current Form 1099-K threshold from the latest IRS publication set before hard-coding numbers, because published thresholds have differed across materials. Unclear allocation records create avoidable disputes.

Common pool methods and required evidence#

| Pool method | How it works | Typical failure mode | Evidence to retain |

|---|---|---|---|

| Equal split | Divide pooled tips evenly across eligible workers in a shift or team | Wrong eligibility snapshot, with missing or extra workers | Shift roster at close, eligibility rules, included tip-event IDs, calculation output, payout IDs |

| Weighted split | Allocate by hours, task counts, or another internal weight | Inputs changed after payout or cannot be reconstructed | Locked source metrics, weighting rule version, timestamped calculation file, approvals, exception notes |

| Role-based split | Predetermined shares by role | Role mismatches or retroactive role edits | Role assignment history, policy version, included orders or shifts, allocation summary, payout mapping |

These are operational methods, not a federally prescribed formula for gig-platform pooling. Your method must be reproducible and explainable.

Section 224 messaging risk#

Section 224 is an income-tax deduction framework for qualified tips, not a blanket exclusion of tip income. IRS guidance says qualified tips can include shared tips, but only when qualified-tip rules are met.

Keep the message narrow. IRS guidance says the deduction may allow up to $25,000 for tax years 2025 through 2028, and eligibility is tied to occupations that customarily and regularly received tips on or before December 31, 2024. Do not present pooled tips as automatically deductible for all worker groups.

Control threshold before launch#

If part of your workforce is employees, keep FLSA employee tip-pool obligations separate from contractor logic. In employee mandatory pool contexts, DOL guidance says collected tips generally must be fully redistributed within the pay period, with required records maintained.

Before launch, verify on sample runs that every pooled tip event is included, the worker roster and eligibility state are captured at allocation time, the rule or policy version is recorded, and each final recipient share has a payout record.

If reassignments, role edits, cancellations, or shift changes can occur after snapshot, set a cutoff timestamp and a documented exception process. If allocations require manual reconstruction, the model is not production-ready.

Related reading: Tax Residency and Co-Living When You Use Outsite.

Model 4 Off-platform tips with platform recordkeeping only#

If tips bypass your rails, treat platform records as support, not as a complete tax record. This can be operationally practical where cash or external wallets dominate, but it gives you less confidence in IRS-facing completeness.

The main constraint is Form 1099-K. It reports payments for goods or services received through payment cards or third-party settlement organizations, and its gross amount reflects payment card and third-party network transactions. Off-platform cash or wallet tips can therefore fall outside the form, and even when tips are part of a 1099-K flow, the form may not separately identify them. Workers still must report gig income on a tax return, including cash and other non-platform payments. Self-employed workers still use Schedule SE (Form 1040) to figure self-employment tax on net earnings.

That shifts the burden from payment orchestration to record discipline and clear worker messaging. State plainly that recipients remain responsible for reporting tip income the platform did not process, and do not imply a Form 1099-K is a full view of all gratuities.

Minimum controls worth having#

At a minimum, keep recurring worker logs or attestations with the date, tip amount, and customer or job context. IRS examples rely on tip logs showing date, customer, and tip amount.

If you use attestation windows, lock edits after each window or maintain a full audit trail of changes so original records can be reconstructed. Keep Form W-9 collection in scope for workers who may receive reportable platform payments outside off-platform tips. If required TIN rules are not met, backup withholding can apply at 24%.

Version your 1099-K threshold guidance. IRS fact sheet FS-2025-08 states a TPSO filing threshold of over $20,000 and over 200 transactions, while older Form 1099-K instructions still show $600 language. Your policy and support copy should reference a dated source.

Model 5 Instant tip payout to contractors#

Use instant payout only when your release controls are already reliable, because the same speed that improves access to funds also leaves less room for error.

Instant rails can deliver funds within seconds, and on RTP the sending institution cannot revoke or recall a payment after submission. That makes release timing both the advantage and the exposure.

Best fit#

This fits categories where immediate access to funds is a priority. It is better suited to mature teams with real-time statusing, idempotent retries, and clear state transitions between tip captured, tip approved for release, and tip paid.

Market demand for speed is real: 86% of businesses and 74% of consumers reported using faster or instant payments in 2023. That does not prove retention lift for gig tips, but it does indicate broad use of faster payment options.

Release gates before first instant payout#

Set explicit gates before you release a first instant tip:

- valid payout destination with a recent success check or equivalent confirmation

- usable tax profile, typically Form W-9 for U.S. persons or Form W-8 where applicable

- no unresolved identity or fraud-review state required by your provider or banking partner

The tax gate is operational, not cosmetic. Form W-9 is used to provide a correct TIN for information-return reporting, and incorrect TIN conditions can trigger 24% backup withholding on reportable payments.

Where teams get burned#

Finality is the core risk. Instant payments are generally treated as final and irrevocable, which increases fraud-prevention and detection pressure. If identity or tax confidence is low, hold the tip in pending status until the W-9 or W-8 issue is resolved.

Instant rails still produce exceptions: payment orders can be rejected and returned. Your product should show clear statuses for completed tips versus failed payouts. Otherwise, the ledger and support outcomes will drift apart.

Non-negotiable controls#

Keep an auditable evidence trail for held and failed instant tips, not just successful ones: release timestamp, tax-document status, identity-review outcome, rail response, and retry history.

A practical rule is simple. Do not use instant payout until both tax-profile confidence and identity confidence are high enough to defend the release decision after the fact. If that bar is not realistic yet, use a batched or hybrid model.

Model 6 Delayed or batched tip payout with reconciliation#

Choose delayed or batched payout when controllability, reconciliation, and exception handling matter more than same-minute access. This is strongest when finance and support need a reliable link between tip events, payout batches, and year-end tax support.

Best fit#

This setup often works best with scheduled payout timing rather than per-tip release. Automatic scheduled payouts can include funds from multiple transactions, and payout reconciliation reports are built to match transactions to each payout batch. That makes batch-level investigations and month-end close easier.

It is also a practical fit for cross-border operations. DAC7 entered into force on 1 January 2023, and non-Union platform operators active in the EU can register and report in one EU country. If you are managing U.S. reporting alongside DAC7 and FATCA workflows, a batch window can give your team time to resolve tax-documentation exceptions before release.

Why reconciliation is the real upside#

The upside is not that batching makes reporting simple on its own. The upside is cleaner alignment between your ledger, payout files, and tax support artifacts.

Form 1099-K reports gross payment volume from payment cards and third-party network transactions, but it does not separately identify tips. Keep your own tip-level record even when processor settlement files are clean. In practice, maintain dated logs with service or order reference, customer reference where appropriate, tip amount, contractor ID, and payout batch ID.

This also makes it easier to separate 1099-K flows from 1099-NEC flows. IRS instructions state that payment card and third-party network payments are not reported on Form 1099-NEC or Form 1099-MISC. Mixing those categories in exports or support tooling creates avoidable cleanup work.

Where teams get burned#

The worker-experience risk is delay without predictability. If timing is unclear, delays feel arbitrary. Set clear payout expectations, including cutoff time, review window, and exception path, in product copy and support macros.

Another failure mode is manual batching without transaction-to-payout mapping. With manual payouts, the provider may not identify which transactions were included in each payout. For cleaner reconciliation, prefer automatic scheduled payouts and persist the payout or batch ID at release.

A practical rule set is to release only after payout frequency is configured, the tax profile is valid, and open exceptions have an owner and escalation deadline. For U.S. persons, unresolved TIN issues can trigger 24% backup withholding on reportable nonemployee compensation. For nonresident payees, some nonemployee compensation is reported on Form 1042-S, and FATCA rules can carry withholding consequences, including 30% on certain U.S. source payments to foreign entities.

In this model, the delay is not the control. Explicit release criteria and enforceable exception timelines are.

Launch checklist for payment flow, tax forms, and audit evidence#

Build this in sequence to avoid rework in reporting and support: tip capture event design, ledger mapping, payout states and holds, Form 1099-K/Form 1099-NEC/Form 1099-MISC extracts, then finance-ops QA before go-live.

| Step | What to include | Grounded note |

|---|---|---|

| Start with the event, not the form | Original tip event ID, reversal link, contractor ID, service or order reference, payout state, and final payout or batch reference at release | Form 1099-K gross amount is not adjusted for fees, credits, refunds, shipping, cash equivalents, or discounts |

| Define the evidence pack before payout release | Payout decision logs, policy-gate outcomes, worker tax profile status, and reconciliation snapshots tied to the extract used for Form 1040 support | If a 1099 is already filed, corrections follow a separate path and incorrect information can cascade into Form 1040-X |

| Test filing-critical edge cases | A U.S. person with valid W-9, a worker with foreign-status documentation, a late-year threshold case, and a tip reversed after an initial reporting snapshot | Schedule SE includes a filing trigger at net earnings of $400 or more; confirm the January 31 1099-K recipient-copy timing |

| Write caveats into product and support copy | Explain what you report and record, and avoid promises about eligibility outcomes | Section 224 provides an income-tax deduction for qualified tips; current IRS guidance states a maximum annual deduction of $25,000 with phaseout over modified AGI of $150,000 ($300,000 joint) |

- Start with the event, not the form

Your tip event model must support reversals, holds, and year-end reporting from day one. Capture, at minimum, the original tip event ID, reversal link if any, contractor ID, service or order reference, payout state, and final payout or batch reference at release.

Keep the mapping traceable to reporting logic. Form 1099-K reports payment app, marketplace, and card flows, and its gross amount is not adjusted for fees, credits, refunds, shipping, cash equivalents, or discounts. If your records cannot separate earned tips from reversed tips, support and finance may not be able to reconcile platform history with gross 1099-K totals. Also version tax-year rules. 1099-K FAQ language currently references the $20,000 and 200 transactions trigger, while 1099-NEC references $600, moving to $2,000 for payments made after December 31, 2025.

- Define the evidence pack before payout release

Set a minimum evidence pack that can support an income, deduction, or credit item in a retrievable way. Include payout decision logs, policy-gate outcomes, worker tax profile status, for example, whether a W-9 or requested W-8 BEN is on file, and reconciliation snapshots tied to the extract used for Form 1040 support.

Tie each pack to a specific reporting version. If a 1099 is already filed, corrections follow a separate path, and incorrect information can cascade into amended individual returns, Form 1040-X. A practical QA check is this: for one contractor, can your team show the full sequence from tip creation to hold or release status, to tax profile at release, to extract row, to support response?

- Test filing-critical edge cases, not just happy paths

Before go-live, run end-to-end tests on contractor files that stress the workflow. Include at least: a U.S. person with valid W-9, a worker with foreign-status documentation, a late-year threshold case, and a tip reversed after an initial reporting snapshot.

Include a Schedule SE check in the same drill. Schedule SE (Form 1040) is used to calculate self-employment tax, and the filing trigger includes net earnings of $400 or more. Also test two operational failures: reversed tips after payout release and held payouts missing a batch cutoff. Then run a mock year-end timeline against the January 31 1099-K recipient-copy timing and confirm support can resolve cases without engineering escalation.

- Write caveats into product and support copy before launch

Document known unknowns now so policy does not drift in case-by-case replies. In product help and support macros, explain what you report and record, and avoid promises about eligibility outcomes.

Be explicit on Section 224 and no-tax-on-tips handling. Section 224 provides an income-tax deduction for qualified tips, but it is not universal across occupations. IRS notice ties eligibility to occupations that customarily and regularly received tips on or before December 31, 2024. Current IRS guidance also states a maximum annual deduction of $25,000, with phaseout over modified AGI of $150,000 ($300,000 joint), and forms remain unchanged for the current tax year. Support copy should therefore clarify that reporting forms may not visibly reflect deduction treatment and that separate filing steps may still apply.

If you want a deeper dive, read Real-Time Payment Use Cases for Gig Platforms: When Instant Actually Matters.

Before go-live, pressure-test your tip flow against payout states, policy gates, and reconciliation exports in the Gruv docs.

The decision that usually saves the most pain later#

If you need to trade some tip-capture upside for stronger reporting and payout control, make that trade early. In early expansion, the safer model is usually the one you can reconcile, explain, and defend when Form 1099 questions, payout disputes, or audit requests arrive months after launch.

That tradeoff runs through every model above. The teams that avoid cleanup later usually make four decisions before they optimize the tip prompt.

1 Define reporting ownership before you pick the tip UX#

Decide who owns reporting for each payment flow before you decide where the tip button goes. Tips are generally taxable income, and gig income must still be reported on a tax return even when no information return is issued, so "we may not hit a threshold" is not a control.

For U.S. rails, separate card and third-party network flows correctly: those payments belong in the Form 1099-K lane and are not also reported on Form 1099-NEC or Form 1099-MISC for the same payments. If your teams cannot answer, plainly, which entity files which form for this tip flow, do not ship the more complex model yet.

2 Put payout gates ahead of payout speed#

Weak identity and tax-profile gates can become costly quickly. Form W-9 exists to provide the correct TIN to a payer required to file information returns, and if TIN data is missing or obviously incorrect, backup withholding must start immediately at 24%.

Treat first-tip payout as a control checkpoint: confirm required tax-form status, TIN formatting, and payout-rail readiness in one decision trail. If any check fails, hold the tip and log the reason. Reconstructing withholding or identity status after release is the failure mode to avoid.

3 Design the evidence pack before launch#

A durable gratuity model needs an audit trail, not just a ledger entry. Your minimum evidence pack should link the tip capture event, payout decision, worker tax-profile status, any hold or release reason, and the reporting extract used for Form 1099 review.

This matters because late or incorrect information returns and payee statements can trigger penalties and interest. It also matters because Form 1099-K threshold references are date-sensitive. One IRS update cites more than $20,000 and more than 200 transactions, while older instructions reference $600 aggregate payments. Verify source date and publication version before freezing logic or writing help-center copy.

4 In early expansion, favor the model that travels cleanly#

When rollout risk is the priority, choose the model with clearer operator-side controls, even if it is less aggressive on immediacy. The operational benefit is cleaner linkage between tip capture, payout decisions, and reporting ownership.

That portability matters even more in cross-border plans. DAC7 places reporting obligations on platform operators and expects operator-side collection and verification. A model built around those controls can be easier to carry into broader compliance regimes, including FATCA and year-end reporting.

For a step-by-step walkthrough, see What Are the Tax Implications of an Honorarium Payment?.

If you are finalizing a tipping model across multiple markets, talk to Gruv to validate operational fit and rollout constraints. ---

Frequently Asked Questions

Is tip income on gig platforms taxable in the United States?

Yes. IRS guidance says gig-economy earnings are taxable whether or not a worker receives an information return. Workers still must report gig income on their tax return.

Does the No Tax on Tips deduction mean tips are fully tax-free?

No. The material here does not establish that tips are fully tax-free or define complete eligibility and filing treatment. Keep copy conservative and avoid promises about outcome.

Why can the same tip flow create different outcomes for employees and self-employed workers?

Because worker classification changes the tax path. For self-employed workers, self-employment tax is calculated with Schedule SE (Form 1040), while for most wage earners employers calculate Social Security and Medicare taxes.

Which forms should platforms expect to manage across Form 1099-K, Form 1099-NEC, and Form 1099-MISC?

It depends on the payment flow, so do not assume one form fits every case. Payment card and third-party network payments are reported on Form 1099-K, not also on Form 1099-NEC or Form 1099-MISC for the same payments. Confirm current-year rules before launch.

When should a platform collect W-8 or W-9 before allowing tip payouts?

The article does not give a universal legal deadline, so do not claim one. Set and document a clear checkpoint before payout so tax-profile status is captured and payout decisions are traceable. For U.S. onboarding, Form W-9 is the core control point, and Form W-8 BEN is the parallel checkpoint for foreign persons.

How should operators explain Payroll tax, Social Security, Medicare, and Self-employment tax differences to workers?

Keep the explanation narrow: self-employment tax covers Social Security and Medicare for people who work for themselves. The article states a 15.3% self-employment tax rate, with 12.4% for Social Security and 2.9% for Medicare, and for 2024 the first $168,600 of combined wages, tips, and net earnings is subject to the Social Security portion. The guidance is not all-inclusive, so edge cases may need additional review.

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.

How to Respond to a Subpoena for Business Records

Move fast, but do not produce records on instinct. If you need to **respond to a subpoena for business records**, your immediate job is to control deadlines, preserve records, and make any later production defensible.

A US Expat's Guide to Investing in UCITS ETFs to Avoid PFIC Issues

The real problem is a two-system conflict. U.S. tax treatment can punish the wrong fund choice, while local product-access constraints can block the funds you want to buy in the first place. For **us expat ucits etfs**, the practical question is not "Which product is best?" It is "What can I access, report, and keep doing every year without guessing?" Use this four-part filter before any trade: