Quick Answer

In a tax treaty, a permanent home is a dwelling that is continuously available to you, whether you own it or rent it. It is the first tie-breaker test used when two countries both treat you as a tax resident. If a permanent home is available in only one country, that country generally wins and the analysis usually stops there.

Don't Just Learn the Rule - Master It: Your Playbook for the Permanent Home Test#

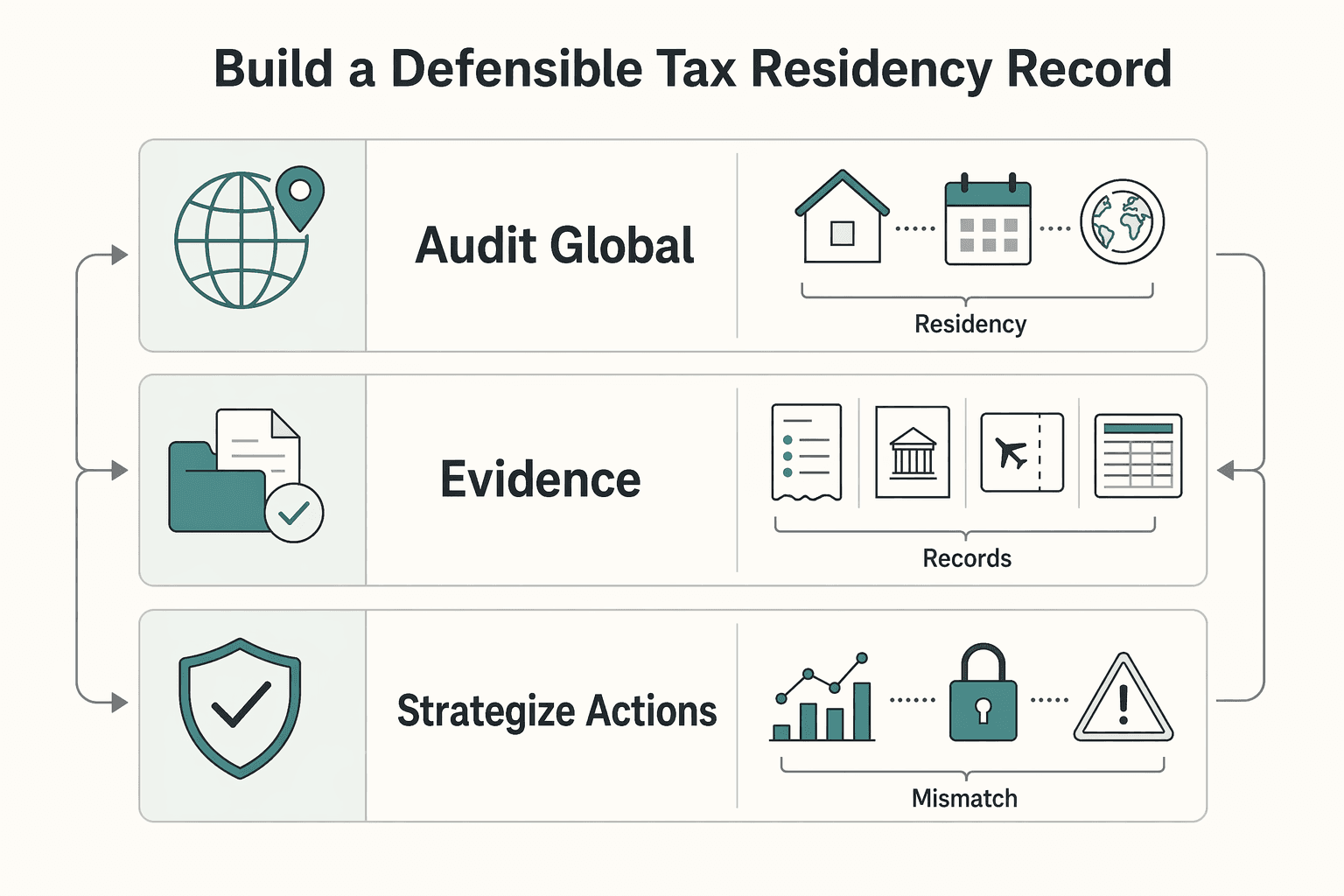

For the elite global professional, "permanent home" is not a term of comfort; it is a high-stakes legal definition that can trigger crippling double taxation. While other guides offer academic theory, this is a strategic playbook. We will transform your compliance anxiety into agency with a clear, three-step framework to audit your footprint, build your evidence, and early control your tax residency.

When you are a resident of more than one country under their domestic laws, you face the risk of being taxed twice on the same income. To resolve this, nations use Double Taxation Agreements (DTAs), and the first tool they deploy is the permanent home test. This is the critical first step in a series of "tie-breaker" rules that determine which country has the primary right to tax you.

Mastering this single concept is the most powerful step you can take to shield yourself from devastating financial surprises. Many professionals operate with a dangerous ambiguity, assuming factors like citizenship or days spent are critical. They are not. The permanent home test takes precedence. If you have a permanent home available in one country but not the other, the analysis often stops there - decisively settling the issue.

This playbook is designed to give you that mastery. We will move beyond definitions to provide a concrete framework:

- Step 1: Audit Your Global Footprint. Critically assess your living arrangements to identify hidden risks.

- Step 2: Build Your Compliance File. Collect the precise evidence needed to build an unshakeable case for your desired tax home.

- Step 3: Fortify Your Position. Early structure your affairs to eliminate ambiguity and strengthen your claim.

This is the path from anxiety to agency. Let's begin.

What is the "Permanent Home" Test, and Why is It Your First Line of Defense?#

To control the outcome, you must first understand the battlefield. When the tax authorities of two countries claim you as a resident, they turn to a tax treaty to resolve the dispute. The tie-breaker rules within that treaty are a rigid, sequential protocol, and the permanent home test is the powerful first step.

The Tie-Breaker Hierarchy Explained#

Think of this as a strict checklist. An authority cannot skip to a test that better suits its interests. Your goal is to win decisively at the earliest possible stage.

The hierarchy is as follows:

- Permanent Home: Does the individual have a permanent home available in only one of the countries? If yes, that country wins the right to tax, and the analysis stops.

- Center of Vital Interests: If a permanent home exists in both countries (or neither), which country is the center of their personal and economic life?

- Habitual Abode: If the center of vital interests is unclear, where do they spend more time?

- Nationality: If the habitual abode is inconclusive, of which state are they a citizen?

- Mutual Agreement: If all else fails, the tax authorities of the two countries must negotiate a solution.

Resolving your case at the permanent home stage is the cleanest victory. It prevents the deeper, more subjective scrutiny into your personal and economic life required by later tests. If you want the next treaty steps laid out in sequence, use Using DTA Tie-Breaker Clauses to Resolve Dual Tax Residency as your companion framework.

Defining "Permanent Home": Availability Over Ownership#

This is where a critical error is often made: "permanent home" is not about ownership; it is about continuous availability. A tax authority seeks to determine where you can live on a lasting basis, not just for a short or occasional stay. You have a permanent home available if you have arranged for a dwelling to be accessible to you at all times, continuously. According to the OECD Model Tax Convention commentary and the IRS guide to claiming tax treaty benefits both frame availability, not simple ownership, as the decisive issue.

This means a rented apartment where you hold the lease is a permanent home, even if you travel most of the year. Conversely, a hotel room, no matter how frequently used, does not qualify because it is transitory.

Here's how different arrangements typically stack up:

| Type of Dwelling | Qualifies as a Permanent Home? | Why? |

|---|---|---|

| Owned House/Apartment | Yes | You have a clear, continuous right to occupy it. |

| Rented Apartment (Leaseholder) | Yes | The lease gives you the legal right to continuous access. |

| Room in a Family Home | Likely Yes | If it is kept for your use and is always available to you. |

| Long-Term Corporate Housing | Maybe | Depends on the terms; if you have exclusive, continuous access. |

| Frequently Used Hotel Room | No | It is considered transitory accommodation, not a permanent dwelling. |

| Owned Property Rented Out | No | It is not "available" to you if a tenant has the right to occupy it. |

Crucial Distinction: "Permanent Home" vs. "Permanent Establishment"#

Finally, let's eliminate a common and costly point of confusion. These terms sound similar but are fundamentally different.

- A Permanent Home relates to your personal tax residency. It is about where you live.

- A Permanent Establishment relates to a business's tax presence. It determines if a foreign company has a taxable presence in another country.

Conflating these can lead you to incorrectly apply business rules to your personal situation or, worse, inadvertently create a taxable presence for your company.

Step 1: Audit Your Global Footprint - Uncover Your Hidden Homes#

Effective risk management begins with a brutally honest self-audit. To a global professional, 'home' is a fluid concept, but tax authorities see it in black and white. You must systematically examine your life through their lens to uncover hidden exposures. This isn't about feelings; it's about facts.

The "Continuous Availability" Litmus Test#

Ask yourself this critical question for every country where you spend time: "If I had to return to Country X tomorrow, is there a specific dwelling I could immediately and freely access for a lasting period?"

This question cuts through the noise. It is not about ownership or frequency of use. It is about your legal right to walk in and live there on a continuous basis.

Scrutinizing Modern Living Scenarios#

Let's dissect the common edge cases that trip up even the most sophisticated professionals:

- The Long-Term Airbnb: A six-month booking could very well create a permanent home. While a short hotel stay is temporary, a long-term arrangement granting you exclusive right to occupy a space provides the stability and accessibility tax authorities look for. The longer the term, the stronger the case.

- The Family-Occupied Property: You own a home in your country of origin, but your parents live in it full-time. Is it "available" to you? Likely not. OECD guidance is clear: if a home is occupied by another party - even family - such that you do not have free access, it is not considered "available." If you would need to displace your parents to live there, you cannot access it freely.

- The Empty Leased Apartment: You hold a 12-month lease in London but only spend 30 days a year there. Does it still count? Yes, absolutely. The test is not a measure of usage; it is a measure of availability. Your legal right to occupy the dwelling, guaranteed by the lease, makes it available 365 days a year.

Actionable Task: Create Your "Footprint Inventory"#

Anxiety thrives in ambiguity. To eliminate it, transform abstract risks into a concrete list. Take 30 minutes to create a simple "Footprint Inventory." This single document will give you more clarity over your international tax exposure than anything else.

Use this template to list every location where you have a potential dwelling. Be ruthlessly objective.

| Country | City | Nature of Access | Continuously Available? (Yes/No) | Justification |

|---|---|---|---|---|

Completing this inventory is your first strategic move. It replaces vague worry with a clear-eyed assessment of your actual ties and forms the foundation for your compliance defense.

Step 2: Build Your Compliance File - The Power of the Paper Trail#

Your Footprint Inventory is the blueprint for the next important phase: building an irrefutable evidence file. In any tax dispute, the burden of proof is not on the tax authority to prove you are a resident; it is on you to prove you are not. A carefully organized file is your primary tool for risk mitigation. Keep the IRS guidance on recordkeeping and Form 8833 treaty disclosures in the same working file you use for annual treaty reviews.

In a residency audit, the burden of proof is on the taxpayer to present clear and convincing evidence of their non-residency. Contemporaneous documentation is crucial as it provides a real-time record of your whereabouts and intentions, which is far more credible than trying to recreate records after the fact.

Use your inventory to guide you. For each country, you will either be establishing ties or demonstrating their absence.

Evidence to Establish a Permanent Home (Country A)#

Your goal is to build an unassailable case that this is your true home base. The documents must show stability and a genuine connection.

- Signed Lease Agreements or Title Deeds: A long-term lease (12+ months) is a powerful demonstration of commitment.

- Utility Bills in Your Name: Gas, electricity, water, and internet bills are powerful indicators of ordinary life.

- Home or Renter's Insurance Policies: Insuring your belongings at a specific address signals you consider it your home.

- Local Council Tax or Property Tax Records: Official correspondence linking you financially to a property is exceptionally strong evidence.

- Bank and Credit Card Statements: Showing a local address on your primary financial accounts helps establish this as your center of life.

Evidence to Disprove a Permanent Home (Country B)#

For countries where you want to sever ties, your documentation must prove a clean break. If UK residence is part of the fact pattern, HMRC's INTM154020 manual is a useful cross-check on how treaty residence tie-breakers are framed.

- Lease Termination Agreements: A formal, signed document ending your rental obligations is your single most important piece of evidence.

- Final Utility Bills: Zero-balance statements showing you have closed your accounts are critical.

- Mail Forwarding Records: Proof that you have officially redirected your mail demonstrates clear intent.

- Evidence of a New Occupant: A signed lease agreement with an unrelated third-party tenant is the ultimate proof that an owned home is not available to you.

Building this file is not a one-time task; it is an ongoing discipline. Every time you sign or terminate a lease, consciously collect and file these documents. This is how you move to a position of command, ready to answer any question with clear, irrefutable proof.

Step 3: Fortify Your Position - Proactive Strategies to Control Your Residency#

Moving from a defensive posture to one of command demands a forward-looking strategy. With your compliance file established, you can shift from proving what was to deliberately shaping what will be. These are the decisive actions of a CEO managing the risks and opportunities of "Me, Inc."

Strengthening Ties to Your Chosen Home#

Your documentation tells a story, but your actions give it credibility. To fortify your claim, demonstrate an undeniable depth of connection.

- Structure Your Lease for Permanence: A rolling month-to-month lease suggests transience. A signed 12-month (or longer) lease is a powerful statement of intent that aligns with the concept of a "permanent home."

- Pass the "Furniture Test": Tax authorities look beyond paperwork to the substance of your life. Do you live out of a suitcase, or have you moved significant personal belongings? Shipping your furniture, books, and artwork is a clear, physical manifestation of establishing a home. It shows you don't just occupy a space; you inhabit it.

Strategically Severing Ties Elsewhere#

Just as important as building ties in one country is methodically cutting them in another. Your goal is a clean break that leaves no room for interpretation.

Use this "Clean Break Checklist" to guide your actions:

| Area of Life | Action to Take | Strategic Rationale |

|---|---|---|

| Property | Sell the property, or sign a long-term lease with an unrelated tenant. | This definitively proves the dwelling is no longer "continuously available" to you. |

| Financial Footprint | Close non-essential local bank accounts and credit cards. | This centralizes your financial life in your new home country. |

| Social & Community | Cancel local club memberships (gym, social clubs). | This demonstrates a departure from the social fabric of the community. |

| Official Records | Surrender your driver's license and cancel voter registration. | These are strong indicators of civic connection that you must formally sever. |

| Communications | Update mailing addresses for all correspondence. | Rerouting your mail shows a deliberate shift of your center of life. |

Navigating the "Dual Permanent Home" Scenario#

It is common to have a permanent home available in two countries simultaneously. This is not a disaster; it is a predictable outcome tax treaties are built to resolve.

When this occurs, the tie-breaker rules simply require you to proceed to the next test: the "Center of Vital Interests." This is a more subjective analysis to determine where your personal and economic relations are closer. Authorities will weigh factors like: From there, compare your facts against What is the 'Center of Vital Interests' in a Tax Treaty? and What Is a Habitual Abode in a Tax Treaty? so you know which evidence matters next.

- Personal Ties: Where does your immediate family reside? Where are your most significant social connections?

- Economic Ties: Where is your primary place of employment? Where are your most substantial investments located?

The early strategies you've just employed - moving furniture, closing accounts, leasing your former property - are precisely the actions that build your case for this next test, making sure you remain in control of the narrative.

Your Next Step: Build a Defensible Tax Residency Record#

The once-intimidating permanent home test is no longer an abstract threat. It is a controllable risk factor, a set of variables that you can now actively and deliberately manage. You have moved from a defensive posture of reacting to confusing rules to an offensive one, where you are the architect of your tax destiny. The power dynamic has shifted. You are in control.

This playbook provides the repeatable, logical path from the anxiety of compliance to the confidence of financial control:

- Audit your global footprint to identify every potential permanent home.

- Build a fortified compliance file with indisputable evidence.

- Strategize your actions to strengthen ties to one location while cleanly severing them from another.

This is how you convert abstract legal principles into concrete actions that protect your assets and provide deep peace of mind. You are no longer hoping you are compliant; you are making sure it.

For a professional whose time is their most valuable asset, the logical next step is to professionalize the execution. The most careful part of this process is the day-to-day logging of your location and travel. Automating this with a dedicated residency tracker removes the significant risk of human error, helpful you to make decisions with complete clarity. It is the final piece of the puzzle, turning your strategic intent into a precise, data-driven reality. If your facts involve a U.S.-Canada tie-breaker, U.S.-Canada Tax Treaty for Freelancers shows how the same documentation logic plays out in a concrete country pair. If you later need formal proof for a treaty claim, How to Get a Tax Residency Certificate as a Digital Nomad shows how to turn that record into an official document request.

Frequently Asked Questions

What counts as a "permanent home" for tax treaty purposes?

A permanent home is any dwelling that is continuously available to you, not just property you own. It can be a house, rented apartment, or rented room if it offers permanence and stability. Temporary accommodation like a hotel stay does not qualify.

How do you prove you do not have a permanent home in a country?

You need documents showing you no longer have a right to a specific dwelling. Strong evidence includes lease termination agreements, property sale documents, a long-term lease to a new unrelated tenant, and final utility bills.

What is the difference between "permanent home" and "center of vital interests"?

These are separate tests in a fixed order. Permanent home comes first and asks whether a dwelling is continuously available to you. Center of vital interests is used only if both countries have a permanent home, or neither does, and it looks at where your personal and economic ties are closer.

Can you have a permanent home in two countries at the same time?

Yes. That is common for globally mobile individuals. When it happens, the treaty moves to the next tie-breaker test to determine residency.

Does a long-term Airbnb or co-living space count as a permanent home?

It can. If a long-term arrangement gives you continuous, exclusive access to a specific dwelling, it is likely to count. A series of short, ad hoc stays would not.

If I own a house but rent it out full-time, is it still my permanent home?

No. If you lease the house to an unrelated third party long-term, it is no longer continuously available to you. The tenant has the legal right to occupy it.

What specific documents are most powerful for proving or disproving a permanent home?

To prove a permanent home, strong documents include a signed long-term lease, utility bills in your name, home or renter's insurance, proof of moving personal effects, and local council or property tax records. To disprove one, use lease termination or property sale agreements, final zero-balance utility bills, a signed lease showing a new unrelated tenant, mail forwarding confirmation, and records showing you surrendered local ties such as a driver's license or club memberships.

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 1 external source outside the trusted-domain allowlist.

Educational content only. Not legal, tax, or financial advice.

Related Posts

Digital Nomad Taxes in 2026 With a Defensible Filing Plan

With digital nomad taxes, the first move is not optimization. It is figuring out where you may be taxable, where filings may be required, and what proof supports that position.

Tbilisi Digital Nomad Guide for 2026 Long Stays in Georgia

Start with sequence, not excitement. If your income depends on delivering work on schedule, secure your legal footing, assemble your documents, and keep month one reversible before you optimize comfort.

Using DTA Tie-Breaker Clauses to Resolve Dual Tax Residency

If two countries can both claim you as a tax resident, the safer move is a treaty position you can prove and keep consistent across filings, not a one-year optimization that may fall apart later. DTA tie-breaker rules help allocate treaty residence, but only after you confirm that dual-residency risk is real under domestic law on both sides.