Quick Answer

Start by building one Residency File that links your co-living agreement, booking history, address updates, and day-count records. In tax residency and co-living cases, reviewers usually assess your behavior pattern over time rather than one contract. Your position gets stronger when new-location ties and prior-location exits are documented on the same timeline, with mismatches corrected early. If work from one place starts looking like an ongoing business base, get professional review before you file.

The Co-Living Tax Playbook: How to Architect a Defensible Tax Residency#

With tax residency and co-living, the aim is not a loophole or a single "perfect" document. It is a consistent evidence trail showing where your life is actually centered.

Residency decisions are fact-driven. California describes residency as a question of fact, and New York guidance similarly focuses on what your records and behavior show over time. Start with one practical move: open a Residency File now, and treat each next step as evidence for that file.

The three tests that often matter most#

Domicile is your permanent-home intent test: where you intend your real home to be. You can have only one domicile, and a prior domicile is not treated as changed until abandonment of the old one and establishment of the new one are shown.

Statutory residency is a rules-based test. In some jurisdictions, it combines day-count rules with an abode or similar connection. Do not assume one global threshold. Current statutory thresholds should be verified from official tax and legal source records before you use them in a plan. Keep the tests separate: U.S. federal substantial presence is its own framework and does not replace state or non-U.S. rules.

Permanent place of abode asks whether you maintain a place suitable for year-round living. Co-living can make this harder because some guidance treats you as maintaining an abode even without owning or leasing it directly.

| Test auditors apply | How co-living complicates it | What evidence you should collect first |

|---|---|---|

| Domicile | Flexible booking and multi-location access can make your life look unanchored | Move timeline, address updates across bank, tax, and government records, proof you stopped using the old address |

| Statutory residency | Frequent travel increases day-count mistakes, especially where counting rules are strict | Day log, passport stamps, flight records, booking confirmations, calendar exports |

| Permanent place of abode | Recurring access to a livable unit may exist without a standard lease in your name | Membership terms, booking history, payment records, occupancy records, operator confirmation of stays |

Pattern beats paperwork#

What often carries the day is the pattern, not any one document. A single booking invoice is weak. Records that line up across time are much stronger.

Strong pattern signals can include repeat presence in the same place, matching address usage across financial and tax records, and old-address usage dropping off. Weak signals can include claiming one home while your filings, banking, and travel records point somewhere else.

Use a monthly control: reconcile your day-count log against passport stamps, booking history, and flight emails. If they conflict, fix the log immediately and verify the counting rules for each jurisdiction.

Start your Residency File now#

Before moving to Pillar 1, your file should already include:

| Residency File item | What to include |

|---|---|

| Residency position memo | A one-page residency position memo naming the jurisdiction you are anchoring |

| Day-count tracker | A live day-count tracker with a note to verify current thresholds per jurisdiction |

| Co-living records | Your co-living membership agreement, booking confirmations, and payment history |

| Old-jurisdiction ties list | A list of old-jurisdiction ties that still need to be closed, updated, or explained |

| Formal proof status | Formal proof requirements pending treaty and source-record verification, for example Form 6166 if a U.S. treaty residence claim becomes relevant |

That is how you turn flexible living into a defensible position. In Pillar 1, you start building the formal and financial evidence that usually carries the most weight.

You might also find this useful: 183-Day Rule Tax Myths That Trigger Residency Filing Mistakes.

Pillar 1: Architecting Your Formal & Financial Ties#

Once you pick your target jurisdiction, the job is to make your records tell one story. In a co-living setup, the problem is often not a total lack of proof. It is the need to replace missing "traditional" proof with documents that still show address use, occupancy, and financial alignment.

Start with official records, but sequence them practically#

The exact order is jurisdiction-specific, but mismatched updates can create avoidable gaps. Use a practical sequence like this, then adjust it to local rules:

| Order | Step | Key note |

|---|---|---|

| First | Collect address evidence you can produce now | Save your membership agreement, booking confirmations, invoices, payment history, and operator communications in your Residency File |

| Next | Update government and tax-facing records where you are eligible | If local rules use minimum-stay or similar criteria, verify the current statutory threshold from official source records before filing |

| Then | Align financial records | Move bank, card, brokerage, insurance, and recurring-account addresses to the same location |

| Last | Decide on business registration | Treat this as a separate risk step, not automatic admin cleanup |

If California is involved, verify state rules directly before you file. California says it conforms to the IRC as of January 1, 2025, also says there are continuing differences, and says it generally does not conform to OBBBA. Its own instructions also say taxpayers should not treat instructions as authoritative law.

Close the all-inclusive proof gap with an evidence matrix#

All-inclusive housing can remove documents reviewers may expect first, so you need substitutes organized by function.

| Common auditor request | Co-living-friendly substitute document | Where to store it in your Residency File |

|---|---|---|

| Lease or tenancy proof | Membership agreement, booking confirmations, operator invoices, dated check-in emails | Housing > Contract and bookings |

| Utility bill at residential address | Bank or card statements using the address, insurance records showing the address, official address-change confirmations | Address usage > Financial statements |

| Proof you actually stayed there | Booking history matched to your day log, support emails confirming stay dates, access or check-in records if available | Presence > Occupancy support |

| Payment trail | Card statements, receipts, monthly invoice ledger | Payments > Housing payments |

| Third-party confirmation | Dated operator letter or support email confirming your stay details | Housing > Third-party confirmation |

A useful guardrail: make "actual use" easy to see. Colorado guidance, while not a residency rulebook, shows a conservative documentation approach: officials look at evidence of actual use, including owner correspondence, and may infer most probable use when records are unclear.

Use the membership agreement as your base, not your only proof#

A membership agreement helps, but it gets stronger when it is paired with records showing who stayed, where, and for how long. If the operator will give you a dated confirmation, make sure it matches your bookings, invoices, and day-count log.

If the operator refuses, build a fallback pack: the agreement, booking exports, invoices, payment receipts, check-in emails, support tickets, and any message confirming stay dates or address. Keep the refusal note too, so your file explains why you relied on substitutes.

Treat business registration as a separate risk decision#

Using the same address for business records can support consistency, but it can also create extra tax or compliance risk depending on local rules and how forms apply. If a filing would publicly list that location as your principal office or business address, stop and get tax advice before you submit it.

Apply the same caution to forms and instructions: use the current version every time you file. The IRS Form 5471 instructions (Rev. December 2025) explicitly direct filers to check for later developments, and Schedule G includes a new question 3b in applicable cases. Keep a note in your file showing which version you relied on and when you verified it.

For a step-by-step walkthrough, see How to handle 'tax residency' if you're stuck in a country due to a crisis.

Pillar 2: Weaving the Fabric of Community & Personal Ties#

Once your address records are aligned, the next question is whether your everyday life moved too. You are not trying to prove a mailbox. You are showing where your personal and economic relations are closer.

Think of this as cumulative evidence, not a one-document test. In jurisdictions like California, residency reviews are fact-pattern based, so if you claim intent, you should be ready to support it with records.

Use a practical signal ladder#

This is a working priority order, not a universal legal ranking.

- High-signal: local care, local professional advisors, and clear records of where your important belongings are kept.

- Medium-signal: recurring local memberships you actually use, such as gym, library, or coworking, especially with local address and payment history.

- Supporting-signal: clubs, volunteering, and cultural or social memberships that a third party can verify.

If you can only do a few things, start with one local healthcare tie, one local advisor tie, and one possessions tie.

| Tie type | Why it matters to an auditor | Best document to save in your Residency File |

|---|---|---|

| Local doctor or dentist | Shows routine life and care moved locally | Patient registration, appointment confirmation, invoice or receipt with provider name and local address |

| Local accountant or attorney | Supports that economic and compliance activity is centered locally | Engagement letter, invoice, payment receipt with firm address |

| Gym, library, or coworking membership | Shows repeat local use and community presence | Membership agreement, welcome email, monthly invoices, entry or booking history |

| Vehicle registration or storage records for belongings | Connects personal belongings to the location | Vehicle registration records, or storage agreement plus recurring invoices and a dated contents list |

Build each tie as action + proof + fallback#

The strongest approach is simple: for each tie, have an action, a document trail, and a backup if the ideal record does not exist.

| Tie | Action | Proof and fallback |

|---|---|---|

| Medical care | Register with a local doctor or dentist | Save intake paperwork, the first appointment confirmation, and billing records; if a visit has not happened yet, keep the registration and scheduled appointment records, and describe it accurately as setup in progress |

| Local advisors | Create a real engagement trail | A paid consultation invoice is usually easier to verify than an informal call; if there is no formal engagement letter, keep the proposal email, invoice, and payment proof together |

| Gym, library, or coworking | Favor memberships that create a local paper trail | If the record is digital-only with no local billing or usage evidence, treat it as weaker support |

| Possessions | Keep records showing where your belongings are actually based | If local vehicle registration is not relevant, storage records can still support your file when paired with the contract, monthly invoices, and a dated contents list |

Fix common mistakes before review#

Weak files often fail in predictable ways, and you can fix them before review.

- Digital-only memberships: add invoices, local address records, or usage logs. Otherwise, classify them as supporting evidence only.

- Unverifiable social claims: keep confirmation emails, receipts, or rosters for clubs or volunteering.

- Mismatched addresses: align profiles and records for care providers, advisors, memberships, and civic records before filing. Driver's license and voting jurisdiction are also location ties, so inconsistencies weaken your story.

If a tie supports your residency position, keep the artifact that proves it.

Related: The Best Digital Nomad Cities for Co-Living.

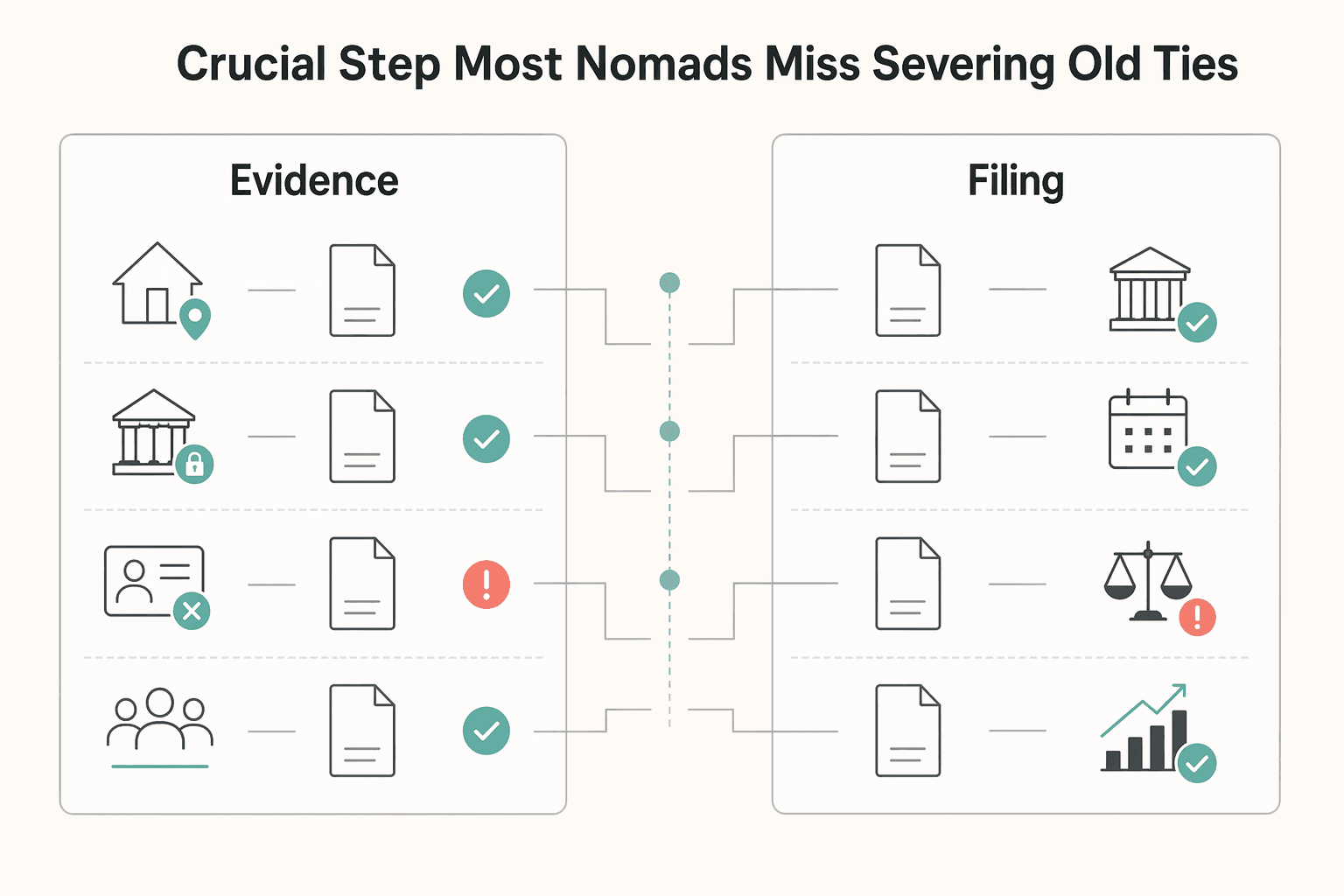

Pillar 3: The Crucial Step Most Nomads Miss - Severing Old Ties#

This is where otherwise solid cases can get weak, but exact tie-severing tests are jurisdiction-specific and need local verification. New ties help, but they may not carry the full argument on their own.

Treat severance as a documented execution sequence:

- Record material changes: keep dated records showing what changed in your old-jurisdiction footprint.

- Update official records where required: keep confirmation artifacts for each completed update.

- Preserve filing documentation: keep the filed return, acceptance evidence, and dated support notes that explain your filing position.

- Maintain an audit trail: keep change confirmations and first records reflecting each update.

| Potential old-jurisdiction signal (verify locally) | Why it can weaken your case | Defensible replacement action |

|---|---|---|

| Records or arrangements still tied to the old location | Can suggest continuing ties under local rules | Update or close what applies and retain dated proof |

| Exit filing documentation is unclear | Leaves move timing and tax position open to challenge | Keep filing, acceptance, and dated support notes together |

| Day-to-day activity still runs through old-location records | Routine life signals may still point to the old location | Reroute records where appropriate and retain proof of changes |

For U.S. citizens, one boundary is non-negotiable: U.S. tax exposure applies to worldwide income and estates even while living abroad. Fully exiting that system requires renouncing or relinquishing U.S. citizenship, and names of people doing so have been published in the Federal Register since 1998. IRS research also describes compliance burden as a major driver of renunciations, not only tax owed.

Escalate to a tax advisor before filing if your facts are complex or you are unsure how your jurisdiction evaluates ties.

If you want a deeper dive, read The 2025 Global Digital Nomad Visa Index: 50+ Countries Compared.

Before you file anything, consolidate your move evidence into one audit-ready timeline with the Tax Residency Tracker.

From Compliance Anxiety to Confident Control#

The goal is not to prove everything at once. It is to keep one consistent, dated record that you and your advisor can review quickly.

Use that file as a control loop: document what is known, flag what is uncertain, and update both before you file.

| Reactive scramble | Controlled process |

|---|---|

| You reconstruct dates from old emails and screenshots | You keep a dated timeline and update it as facts happen |

| Records are fragmented and hard to verify | Records are organized into one reviewable file |

| Your advisor spends time rebuilding the story | Your advisor can validate the position, test gaps, and focus on risk |

Before you call the file defensible, make sure it contains, where relevant:

- a clear chronology of assignment dates and key tax-relevant events

- your home-country tax baseline assumptions for any hypothetical-tax calculation

- records of hypothetical-tax deductions from pay, where this framework applies

- records of employer-side host-country tax filings and compliance steps, where applicable

- one summary page listing unresolved questions and decision points for advisor review

For advisor handoff, split responsibilities clearly:

- You prepare the facts packet: chronology, available records, and unresolved questions.

- Your tax advisor validates internal consistency and confirms how employer-side compliance responsibilities apply in your case.

- Escalate early when cross-border complexity or unexpected liabilities appear, or when home-country vs. host-country treatment is unclear.

If you need a broader operating checklist, use The Ultimate Digital Nomad Tax Survival Guide for 2025 as companion context.

For country-specific context, see Hungary Tax Residency for Nomads and the White Card.

If these tax workflows also affect how you invoice, get paid, and document compliance, review the full Gruv Tools set for your next action plan.

Frequently Asked Questions

How can you prove residency if your co-living rent includes all utilities?

Utilities are not the only way to support residency because this is usually a facts-and-circumstances analysis. Your strongest file usually starts with records you control, such as address updates on financial and government records, with provider-dependent items like a membership agreement or booking invoice serving as support.

What to do next: save dated confirmations for each address change and keep them aligned to your move timeline.

Is a co-living membership agreement enough on its own?

No. It can strengthen your position, but it does not establish residency or domicile by itself. Provider policies vary by location and booking timing, and platform access status is still supplementary evidence.

What to do next: keep the agreement in your file, but anchor your position with government and tax-facing records plus the Pillars 1-3 checklist.

What documents matter most when you are trying to show intent to remain?

Intent is inferred from your pattern of behavior, not one document. New York frames domicile as your permanent, primary home you intend to return to, and Canada gives heavy weight to core ties like dwelling place, spouse or partner, and dependants.

What to do next: keep one dated pack that combines formal records, real-life ties, and old-jurisdiction exit records.

What is the biggest mistake people make with tax residency and co-living?

They build new ties but do not fully sever old ones. That weakens the position when old-home access, official records, or financial activity still point backward.

What to do next: recheck Pillar 3 and confirm you have dated proof for housing exit, civic or identity updates, filing closure, and financial rerouting.

Do day counts decide the answer for you?

Day counts can be decisive in some systems, but they are not universal on their own. For U.S. federal purposes, residency is based on the green card test or substantial presence test, including the 31-day current-year leg and 183-day three-year framework, and any physical presence during a day generally counts. Other systems also use domicile and tie analysis, and New York includes a 184-day statutory rule.

What to do next: keep a reliable travel log and get filing advice early if your year could be dual-status.

Can working from a co-living space create permanent establishment risk for your business?

Yes, in some patterns, but not every work session creates PE. Risk rises when your setup looks like a sustained operating base or when someone habitually concludes contracts for the business. Some treaty contexts also analyze services even without a fixed place, while preparatory or auxiliary activity may be treated differently.

What to do next: treat this as a risk screen and get professional advice before filing if one location starts to look like your business base or if you plan to take a treaty position.

What if your Canadian residency status is still unclear after all this?

That is common when ties are split. Canada explicitly focuses on whether you severed main residential ties, and keeping those ties can keep you in resident treatment.

What to do next: if your facts are mixed, get advice on whether an NR73 or NR74 determination request is appropriate before finalizing your filing position.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- arl.colorado.gov/chapter-6-property-classification-guidelines...trusted

- ftb.ca.gov/forms/2024/2024-1031-publication.pdftrusted

- ftb.ca.gov/forms/2025/2025-565-booklet.htmltrusted

- irs.gov/pub/irs-soi/21rpcitizenshipandtaxes.pdftrusted

- irs.gov/individuals/international-taxpayers/substant...trusted

- tax.ny.gov/pit/file/pit_definitions.htmtrusted

- tax.ny.gov/pubs_and_bulls/tg_bulletins/pit/permanent_pl...trusted

- tax.virginia.gov/residency-statustrusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Digital Nomad Taxes in 2026 With a Defensible Filing Plan

With digital nomad taxes, the first move is not optimization. It is figuring out where you may be taxable, where filings may be required, and what proof supports that position.

The 2026 Global Digital Nomad Visa Index for 50+ Countries

Start with legal fit, not lifestyle filters. The practical order is simple: choose a route you can actually document, then decide where you want to live. That single change cuts a lot of wasted comparison work and stops you from falling in love with places that were never a real filing option.

The Best Digital Nomad Cities for Co-Living

The right coliving city is one you can actually move into on your dates, under terms you can sustain, with a stay path you can realistically keep. Treat this as a relocation decision, not a popularity contest.