Quick Answer

Yes. In most situations, honorarium payment tax is treated as taxable income even if Form 1099-MISC never arrives. Start by tying payer data to your records, then classify from facts: a one-off award-style amount may be reported on Schedule 1 (Form 1040) line 8i, while recurring service revenue can require Schedule C and possibly Schedule SE. If your year includes state mobility or foreign accounts, run those checks as separate compliance lanes before filing.

Start Here If You Just Got an Honorarium#

Use a conservative default: treat an award-style payment as taxable and reportable, and do not assume a missing form removes your filing duty. This article is a decision path for income reporting, not a loophole guide.

If you work across countries, scope the issue first. You need to know how the payment was reported, what documents support that treatment, and where cross-border facts can change the analysis. We will focus on Form 1099-MISC, Schedule 1 reporting for award-style payments, possible Schedule C forks, and social-tax edge checks.

A useful anchor is the IRS award example for a Segal AmeriCorps Education Award. In that example, the payment is taxable in the year paid. If it is $600 or more, you should receive Form 1099-MISC. The amount is shown in Box 3, Other Income, and is reported on Schedule 1 (Form 1040), line 8i, Prizes and awards. The same example says reporting can still be required even if you do not receive Form 1099-MISC.

Before you classify anything, do a quick records check:

- Confirm whether you received

Form 1099-MISCand whether the amount matches your records. - Save the payer message, event details, payment memo, and any invoice or agreement.

- Note whether the payment looks like a one-off award-style receipt or part of an ongoing service relationship.

Do not assume the label decides the treatment. "Honorarium" can cover different fact patterns, and the line between Other Income and business income can be fact-specific. If the facts are mixed or the classification materially changes your tax outcome, get advisor review before filing.

If you work across countries, keep one boundary clear: Totalization agreements and a Certificate of Coverage can matter for social-tax exposure. Run that check separately from your payment-classification and reporting analysis.

Build the Right Mental Model Before You Classify the Payment#

Start here: in these examples, honorarium is a label, not a full classification. Your reporting position should follow the facts you can document, not the label alone.

One example shows why. One advisory record described a $1,000 honorarium for a 2-day panel. A later request was $2,100 for a 5-day panel, with the increase tied to the longer panel length. That later request was also evaluated as similar to prior facts and circumstances. In plain terms, these payments can be tied to real participation work, but the amount and label still do not settle treatment by themselves.

The practical split is simple. If it looks like participation money with a light paper trail, capture that context clearly in your notes. If there is a more detailed agreement with defined scope, negotiated terms, invoicing, or deadlines, treat that as a signal to run a fuller review instead of stopping at the word "honorarium."

Your Tax Documentation is the control point. Keep the invitation or request, any agreement, agenda or scope details, payment message, invoice if any, and a short note on why the payment was made and whether it was one-off or recurring.

One more judgment call matters here: repetition changes risk. In the same advisory record, repeated similar requests were flagged as potentially problematic, with a direction to return for another hearing before accepting more. Use that as a working rule. If the same pattern keeps repeating, recheck classification before filing. For a related classification issue, see Tax Implications of Receiving Stock Options as a Freelancer.

Confirm Taxability and Reporting Duty First#

Use a conservative default: treat an honorarium as taxable income unless you have clear facts supporting a different treatment. That position is usually easier to defend than relying on the label alone.

Columbia policy is explicit that an honorarium is taxable income and reportable to the IRS. Use that as a framing signal, not a universal IRS classification rule. Start with the payment you received and the facts you can document.

Treat Form 1099-MISC as a reporting artifact#

Form 1099-MISC is an information return the payer may need to furnish. In the tax-exempt-organization context, the IRS says a payer generally furnishes it when it pays at least $600 during the year to a non-employee for services. The furnish date is January 31 of the following year.

Use the form for reconciliation, not as your only decision point. If you receive one, match the payer name, amount, and payment description to your records before you prepare Form 1040. If you do not receive one by January 31, follow up with the payer and document the response.

Build the file before you touch Form 1040#

Your defensible position comes from records, not memory. Build a compact file for each payment. Include the payer's legal name and contact details, the payment date and amount, the event or service purpose, the invitation, email thread, or request letter, whether there was any verbal or written negotiated agreement, and any invoice, receipt, or payment memo.

That agreement check matters. Columbia policy states that any verbal or written negotiated agreement creating a payment obligation for services is a contractual agreement, which can move the analysis away from a purely discretionary honorarium.

Watch the withholding signals#

A couple of early checks can save cleanup later. IRS guidance in this context says payers should request Form W-9 before work begins. If the payer does not obtain an SSN or EIN before payment, 24 percent backup withholding may apply.

If you are a nonresident alien paid for personal services performed in the United States, IRS guidance says payers generally must withhold at 30 percent unless an exemption or other rule applies. That rule applies regardless of payer residence, contract location, or payment location.

Before filing, confirm in writing who paid you, why they paid you, and whether the payment came from a negotiated service arrangement. That gives you a clean base for the return position.

Related: What are the Tax Implications of 'Bartering' Services with another Freelancer?.

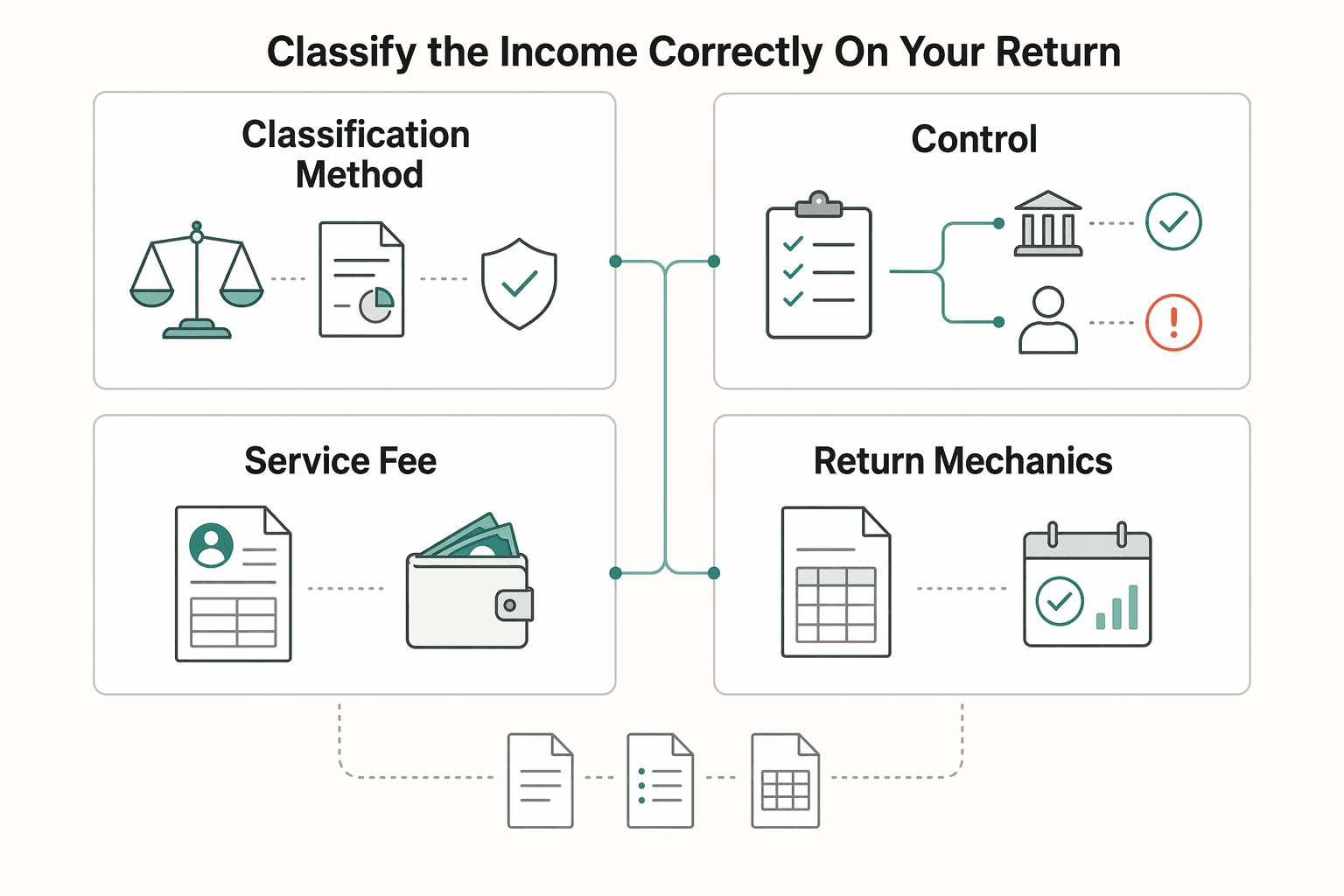

Classify the Income Correctly on Your Return#

Once you know the payment is taxable, the key filing decision is classification. The IRS frames this as an employee-versus-self-employed determination based on facts and circumstances under common-law rules. If the earnings are self-employment income from independent contractor services, use Schedule C (Form 1040) to report earnings and related expenses.

The IRS approach is based on the underlying facts, not labels alone. A core checkpoint is control: if the organization had the legal right to control what you did and how you did it, that points toward employee treatment, not independent contractor treatment.

| Signal | More consistent with employee treatment | More consistent with self-employment income | Red flag to investigate |

|---|---|---|---|

| Classification method | Position based mainly on labels | Position based on facts and circumstances under common-law rules | Return position relies on labels but facts point the other way |

| Control test | Payer had the legal right to control what was done and how | Payer did not have that legal right to control what/how | Control facts point to employee treatment, but income is filed as self-employment |

| Service-fee treatment | Facts do not support self-employment treatment | In IRS clergy guidance, direct fees for personal services are generally self-employment earnings | Treating personal-service fees as non-self-employment without clear supporting facts |

| Return mechanics and expenses | Not treated as self-employment income | Reported on Schedule C with related expenses handled there | Expense treatment does not match the chosen classification |

When Schedule C is the practical default#

Schedule C (Form 1040) is the path the IRS gives when income is self-employment income from independent contractor services. IRS guidance also notes, in a clergy example, that direct fees for personal services are generally self-employment earnings.

That does not create a universal rule for every payment. Use the facts and circumstances for each payment and document why self-employment treatment does or does not apply.

When treatment may remain outside Schedule C#

Treatment may remain outside Schedule C when the facts and circumstances do not support self-employment treatment, including cases where the legal-right-to-control test points to employee status. Use your records to test that position based on what happened in practice, not labels alone.

Do not skip the employee checkpoint. If the payer had the legal right to direct both what you did and how you did it, the issue is employee versus self-employed classification, not simply outside Schedule C versus Schedule C.

Verify the position before filing#

Before you submit Form 1040, run three checks:

- Confirm your classification is based on facts and circumstances under common-law rules.

- Confirm the control analysis supports the classification you chose.

- If you are treating the income as self-employment income, report it on

Schedule Cand make sure expense treatment matches that classification.

If you cannot explain the classification clearly from your documents, pause and review before filing.

Understand the Tax Consequences of Each Classification#

Classification can change total tax, not just where a payment appears on Form 1040. If income is treated as self-employment income, you may add a Schedule SE (Form 1040) obligation on top of regular income-tax reporting. Treat this as three separate checks:

| Tax layer | What it covers | What classification can change | What to check |

|---|---|---|---|

Federal Income Tax | Regular federal tax on taxable income | Reporting treatment | Confirm your return position matches your records |

Self-Employment Tax | Social Security and Medicare taxes for people who work for themselves | Whether Schedule SE applies and whether additional tax is due | Check net earnings from self-employment and the $400 threshold |

State Income Tax | State-level tax treatment | State treatment may differ from federal treatment | Review each State Tax Return separately |

Self-Employment Tax is its own layer. It does not replace other taxes. IRS guidance is explicit that it covers Social Security and Medicare taxes, not all taxes.

What usually changes when income is treated as self-employment#

The biggest shift is often the self-employment layer: 15.3% total (12.4% Social Security + 2.9% Medicare), generally applied to 92.35% of net self-employment earnings, with tax usually due at $400 or more in net earnings.

Use net earnings, not gross receipts. Net earnings are gross trade or business income minus ordinary and necessary trade or business expenses. This tax can still apply even if you already receive Social Security or Medicare benefits.

If self-employment treatment is correct, include Schedule SE. That schedule is used to calculate self-employment tax and is also used by the Social Security Administration for benefits.

Decision checkpoint before filing Form 1040#

If classification is close and the total tax difference is meaningful, run both scenarios before filing: one with self-employment treatment and one without. Use the same payment records and the same defensible expense set in both runs.

Document why you chose the final classification and the tax effect it creates. Federal treatment is the starting point, not the final answer for every state return.

For cross-border cases, add one more check: if you are a nonresident alien and personal services were performed in the United States, payers generally must withhold at 30 percent unless an exemption applies. Service location can change the compliance result even when the payment label does not.

Handle 1099-MISC and No-Form Cases Without Guessing#

Use one standard in every branch: report the amount you can support from your records, then reconcile to payer paperwork.

| Situation | What to do | Key details |

|---|---|---|

Payer issued Form 1099-MISC | Check payer details, your taxpayer details, and the reported amount; reconcile to payment proof, invoice or event records, bank deposit, and tax-year timing; map the amount to the return. | In the IRS award example, the amount is in Box 3 (Other Income) and is reported on Schedule 1 (Form 1040) line 8i attached to Form 1040. |

| No form shows up | File from your own Tax Documentation, including bank records, invoices, event correspondence, and year-end income records. | The IRS example says the payment is still reportable even if you do not receive Form 1099-MISC, and says you should receive one when the payment is $600 or more. |

| Payer data is wrong | Confirm amount, tax year, and payment channel from your records; identify the mismatch type; request correction from the payer and track it. | Some card or payment-network transactions are reported on Form 1099-K, not Form 1099-MISC or 1099-NEC; for paper corrections, the IRS instructions warn not to check VOID. |

When a payer issued Form 1099-MISC#

If a payer issued Form 1099-MISC, run this tie-out before filing:

- Check the form as issued: payer details, your taxpayer details, and reported amount. In the IRS award example, the amount is in

Box 3(Other Income). - Reconcile to your records: payment proof, invoice or event records, bank deposit, and tax-year timing.

- Map the amount to your return: in the IRS award example, report the payment on

Schedule 1 (Form 1040)line8iattached toForm 1040. - Check withholding assumptions: in the IRS example, there is no withholding unless the taxpayer did not provide a TIN.

If no form shows up#

A missing form does not remove the reporting duty. The IRS example says the payment is still reportable even if you do not receive Form 1099-MISC, and says you should receive one when the payment is $600 or more.

Use your own Tax Documentation to file: bank records, invoices, event correspondence, and year-end income records. A late or missing form does not change the reporting obligation in that IRS example.

What to do when payer data is wrong#

When payer data is wrong, use a fixed protocol:

- Correct your records first. Confirm amount, tax year, and payment channel from your documents.

- Identify the mismatch type: amount or timing error versus form-type issue. Some card or payment-network transactions are reported on

Form 1099-K, notForm 1099-MISCor1099-NEC. - Request correction from the payer and track it. For paper corrections, the IRS instructions warn not to check

VOID, or the correction will not be entered into IRS records. - If correction is still pending at filing time, keep an explanation-ready file with the original form, reconciliation sheet, payment proof, and correction correspondence.

The practical rule is simple: file from supportable records, not unverified form data.

Manage Multi-State Exposure Before Filing Season Gets Messy#

Start with California residency facts, then source each payment by where services were physically performed. If California and another state both have a plausible claim, escalate early instead of waiting for notices.

For California, the FTB framework is facts-and-circumstances based:

- Residents are taxed on all income regardless of source.

- Part-year residents are taxed on worldwide income while resident, and on California-source income while nonresident.

- Nonresidents are taxed on taxable income from California sources, including services performed there.

| Scenario | Where the service happened | Residence ties | Likely California filing trigger |

|---|---|---|---|

| Full-year California resident, event outside California | Outside California | Strong resident facts for the year | Income generally remains in the California resident tax base because residents are taxed on all income regardless of source |

| Not a California resident, but you traveled into California to perform services | In California | No California residency, ties elsewhere | A nonresident filing may be triggered because services performed there are California-source income |

| You moved into or out of California during the year | Mixed, or payment spans resident and nonresident periods | Part-year residency facts | Form 540NR may be in play for part-year reporting |

| You live outside California and split workdays between California and elsewhere | Some days in California, some elsewhere | Nonresident or part-year facts | California may expect reporting of the California-sourced share |

California case box#

If you live in Nevada, accept a payment for a Los Angeles conference, and perform part of the services there, California has a sourcing hook: services performed there. In a nonresident or part-year scenario, Form 540NR may be the relevant return.

When work is split across locations, use this allocation checkpoint:

CA Workdays / Total Workdays = % Ratio% Ratio x Total Income = CA Sourced Income

Also plan to support the position yourself. FTB says it will not issue written residency opinions for a specific period, so your records should carry that weight.

Sequence the analysis before preparing returns#

A clean sequence helps here. First, lock residency facts for the year. Then map each payment to where services were physically performed. Next, route each payment to the likely California filing lane, including whether Form 540NR is implicated. Finally, keep a reconciliation file with your calendar, travel proof, event records, payment support, and a short sourcing note.

When to escalate#

Escalate early when California and another state have plausible claims, especially with midyear moves or mixed-location service days. Early review is usually cleaner than retroactive cleanup after filing season.

Add Cross-Border Checks for Residency and Financial Accounts#

When your facts cross borders, treat this as two separate checks: report the income, then review foreign-account filing duties. Tax residency can turn a simple payment into a wider compliance issue.

Start with your U.S. status for the year. For Form 8938 analysis, specified-individual categories include a resident alien for any part of the tax year, and can include a nonresident alien who elects resident treatment for a joint return. That is why even a one-off payment may still require a foreign-asset review.

When residency changes the workload#

Income reporting comes first, but it is not the whole job. If you are required to file a U.S. income tax return and hold specified foreign financial assets above the applicable Form 8938 threshold, use Form 8938 to report them. A specified foreign financial asset includes any financial account maintained by a foreign financial institution.

Do not assume one threshold fits every filer. The IRS cites an aggregate value exceeding $50,000 for certain U.S. taxpayers, and also states that higher thresholds apply to joint filers and taxpayers residing abroad. If your year includes a move, time abroad, or a residency election, verify the threshold set that applies to your filing profile.

If you do not have to file an income tax return for the year, Form 8938 is not required for that year.

Keep income reporting separate from account reporting#

| Filing item | What it covers | Operator note |

|---|---|---|

| U.S. income tax return | Income reporting | Report the payment as income if you have a U.S. return filing obligation. |

Form 8938 | Specified foreign financial assets above the applicable threshold | Attach to your annual return and file by that return's due date, including extensions. |

FBAR (FinCEN Form 114) | Separate foreign account report | Filing Form 8938 does not remove a separate FBAR duty when FBAR is otherwise required. |

Use two checklist lines before filing: income reported and account reporting reviewed. Reporting income on your U.S. return does not by itself satisfy foreign-account reporting, and Form 8938 does not replace FBAR when FBAR applies. Before finalizing, list each non-U.S. financial account and reconcile that list against both checks.

Caveat

Country and program rules vary. U.S. income reporting and U.S. foreign-account reporting are separate regimes, so do not assume other countries apply the same logic. If the payer, account, or your residence is outside the U.S., confirm local treatment before applying U.S.-style rules.

If your filing footprint changed during the year, map your move dates and jurisdiction ties in the Tax Residency Tracker before you lock your federal and state filing plan.

Build an Evidence Pack You Can Defend in an Audit#

Build one audit folder now. Your goal is to show, quickly, how you chose a reporting treatment, such as Other Income or Schedule C (Form 1040), and keep documents that match that choice.

A practical working file set can include:

- payer email or message explaining why the payment was made

- event details, including date, role, agenda, and invitation page

- invoice, receipt, or payment confirmation trail

- a short classification note explaining why you used

Other IncomeorSchedule C

Keep that classification note tight and fact-based. IRS guidance says worker status is facts and circumstances, and expense treatment can differ based on whether income is treated as employee or self-employed. If you report on Schedule C, keep related expense support in the same folder.

At year end, store return-facing items together: Form 1099-MISC if issued, draft Form 1040 workpapers, and supporting documentation for each amount. In the IRS award example, the amount appears in Box 3 and is reported on Schedule 1 (Form 1040) line 8i, and reporting is required even if Form 1099-MISC is not received. Your file should show why your facts support the reporting line you used.

Use one pre-filing checkpoint: every number on the return ties to a source document, whether that is a form, invoice, bank record, or payer message. IRS exam materials reference Information Document Requests and bank document request lists, even though those guides are not binding law.

If a payer sends a paper 1099-MISC correction, keep the correction trail and the final corrected form. IRS instructions say a correction is not entered into IRS records if the VOID box is checked.

Follow a Filing Sequence That Reduces Rework#

Use a fixed sequence to reduce rework: set your federal classification first, complete the federal return, then run a separate state pass. This is a practical workflow, not an IRS-mandated order, but it can prevent cleanup later if classification changes.

| Step | Action | Article note |

|---|---|---|

| 1 | Collect payer records, payment trail, event details, and any Form 1099-MISC. | Start with the source documents before classifying the payment. |

| 2 | Classify the payment based on facts, such as Other Income versus Self-Employment Income. | This is the federal classification step. |

| 3 | Model the tax impact under that classification. | Use the chosen classification to see the tax effect before filing. |

| 4 | Complete Form 1040 and required federal schedules. | If the payment is Self-Employment Income, do not finalize Form 1040 until you complete a Schedule SE check. |

| 5 | After federal treatment is settled, validate State Income Tax exposure and any State Tax Return filings. | Federal treatment helps structure the review, but it does not by itself decide every state filing outcome. |

Put a hard stop on self-employment cases#

If you classify the payment as Self-Employment Income, do not finalize Form 1040 until you complete a Schedule SE (Form 1040) check. IRS guidance says Schedule SE is used to figure self-employment tax on net earnings, and the Social Security Administration uses that information for benefit calculations.

Start with net earnings, not gross receipts. Subtract ordinary and necessary business expenses from gross business income. If net earnings from self-employment are $400 or more, self-employment tax generally applies. The amount generally subject to that tax is 92.35% of net earnings, at a stated 15.3% rate (12.4% Social Security and 2.9% Medicare).

If self-employment tax is required, attach Schedule SE and Schedule 2 (Form 1040) with the Form 1040 series return. Keep the scope clear as well: this self-employment tax discussion covers Social Security and Medicare taxes, not every tax a self-employed person may owe.

Finish federal, then run a state pass#

Once federal classification is complete, run a separate state review with those facts fixed. Federal treatment helps structure the review, but it does not by itself decide every state filing outcome.

At minimum, confirm residency facts and whether any state filing duty still needs action. If residency is still unclear, resolve that before filing. For a deeper residency screen, see Do I Have to Pay State Taxes While Living Abroad as a Digital Nomad?.

Use a short pre-file hold list#

Before filing, stop if any of these are still open:

- unresolved payer mismatches, including unclear paper

1099-MISC/1099-NECcorrections - missing

Tax Documentationfor any reported amount - unanswered residency questions that could affect a

State Tax Return - self-employment classification without a documented

Schedule SEcheckpoint - stale form assumptions without checking current IRS instructions

Instruction freshness matters. IRS posted a correction to the 2025 Schedule SE instructions on 20-FEB-2026. Also, for paper 1099-MISC/1099-NEC corrections, IRS instructions warn that if the correction is marked with the VOID box, it will not be entered into IRS records.

Know Exactly When to Bring in a Tax Professional#

Bring in a tax professional before filing when foreign-asset reporting may apply and your filer status, reportable assets, or threshold profile is not clear. A pre-filing review can prevent missed filing requirements and cleanup later.

| Trigger | Why it matters | Article note |

|---|---|---|

| Mixed classification | Form 8938 analysis turns on whether you are a specified person and whether you have an interest in specified foreign financial assets required to be reported. | If you cannot explain both gates and tie that to your records, pause and get professional review before filing. |

| Mobility changed your profile | Thresholds vary by taxpayer profile, including higher thresholds for some joint filers and taxpayers residing abroad. | If your profile changed during the year, do not assume last year's threshold logic still applies. |

| Cross-border reporting may apply | Form 8938 and FBAR (FinCEN Form 114) are not interchangeable, and filing Form 8938 does not remove a separate FBAR requirement when that filing applies. | Form 8938 is attached to your annual return and filed by that return's due date, including extensions; if you are not required to file an income tax return for the year, you do not need to file Form 8938. |

Mixed classification is the first trigger#

For Form 8938, the first classification test is whether you are a specified person and whether you have an interest in specified foreign financial assets required to be reported. If you cannot explain how your facts fit both gates and tie that to your records, pause and get professional review before filing.

Mobility can raise filing risk quickly#

Thresholds vary by taxpayer profile, including higher thresholds for some joint filers and taxpayers residing abroad. If your profile changed during the year, do not assume last year's threshold logic still applies; get review before filing when the profile-to-threshold match is unclear.

Cross-border reporting is a separate lane#

Bring in a pro early when foreign accounts or assets may be reportable. Form 8938 and FBAR (FinCEN Form 114) are not interchangeable, and filing Form 8938 does not remove a separate FBAR requirement when that filing applies.

A cited trigger for certain U.S. taxpayers is aggregate value above $50,000; for specified domestic entities, the figures are $50,000 on the last day of the tax year or $75,000 at any time during the tax year.

Operationally, timing matters. Form 8938 is attached to your annual return and filed by that return's due date, including extensions. Also keep this exception in mind: if you are not required to file an income tax return for the year, you do not need to file Form 8938, even if foreign assets exceed threshold levels.

For a step-by-step walkthrough, see The Self-Employment Tax Trap: How Totalization Agreements Can Save US Expats Thousands.

Take the Low-Stress Compliance Path#

The low-stress path is consistent: work from facts, not the payment label, and keep enough documentation to defend the position you report on your federal return and each State Tax Return.

Start with day-one Tax Documentation: payment record, date, payer identity, where services happened, and residency-period facts. If California is involved, treat that as core analysis, not admin. The FTB frames residency as a facts-and-circumstances determination. For part-year residents, California tax scope changes by period: worldwide income while resident, and California-source income while nonresident. For nonresidents, California taxes California-source income, including services performed there.

Use the same sequence every year#

- Classify

Classify from underlying facts, not payer wording. If service location or residency period is mixed, flag it before drafting returns.

- Verify

Match each amount to support before filing. For California multi-state service work, use the published checkpoint: CA Workdays / Total Workdays = % Ratio, then % Ratio x Total Income = CA Sourced Income.

- File

File federal and state returns from the same documented fact pattern.

- Archive

Save calculations, source records, and a short written rationale together so your reporting logic is easy to defend later.

Treat cross-border and multi-state facts as early-review triggers#

If facts span states, or involve nonresident alien compensation for personal services performed in the United States, get review early as a cost-control step. The IRS states that payers generally must withhold at 30 percent on compensation paid to a nonresident alien for personal services performed in the United States unless an exception applies. This can apply regardless of payer location, contract location, or where payment occurs.

Use a strict trigger: if residency or sourcing facts involving California, cross-border service location, or more than one plausible state filing position appear in your file, escalate before filing. Final check: if you cannot explain your treatment in two or three plain sentences and point to supporting documents, pause and resolve the facts first.

For a low-stress final review, run your assumptions through Gruv's compliance tools, where enabled, before you file and archive your records.

Frequently Asked Questions

Is an honorarium payment taxable?

The provided sources do not establish whether an honorarium is taxable. They cover foreign account and asset reporting (Form 8938/FBAR), not honorarium income classification.

Do I still report honorarium income if I never received Form 1099-MISC?

These sources do not answer that question. They do not provide honorarium-specific rules for Form 1099-MISC situations.

When should an honorarium go on Other Income instead of Schedule C?

Confirm the correct placement of honorarium income — Other Income versus Schedule C — with a qualified tax adviser or the relevant authority.

Can an honorarium trigger Self-Employment Tax and Schedule SE?

Confirm whether an honorarium triggers self-employment tax and requires Schedule SE with a qualified tax adviser or the relevant authority.

Can one honorarium create filing obligations in more than one state?

These sources do not include state-tax sourcing or residency-allocation rules, so they cannot establish when one honorarium creates multi-state filing obligations. For a broader primer, see Do I Have to Pay State Taxes While Living Abroad as a Digital Nomad?.

If I live abroad, do FBAR, FATCA, or Form 8938 apply to this income?

Potentially, but not because of the payment by itself. For Form 8938, the IRS applies a threshold test, notes higher thresholds for joint filers and taxpayers residing abroad, and cites $50,000 as a trigger for certain U.S. taxpayers. Form 8938 is attached to your annual return and filed by that return’s due date, including extensions. Filing Form 8938 does not remove a separate FBAR (FinCEN Form 114) duty when FBAR otherwise applies. If you are not required to file an income tax return for the year, you do not need to file Form 8938 even if assets exceed a threshold.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

Digital Nomad Taxes in 2026 With a Defensible Filing Plan

With digital nomad taxes, the first move is not optimization. It is figuring out where you may be taxable, where filings may be required, and what proof supports that position.

Do I Have to Pay State Taxes While Living Abroad as a Digital Nomad?

Living abroad does not end `state income tax` exposure by itself. The first decision is practical: choose a filing position your facts can support, then build records that support the same story all year.

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.