Quick Answer

Start by treating continuous KYC monitoring as an operations control, not a one-time onboarding check. With continuous kyc monitoring platforms, require a live proof that one alert moves from trigger to reviewer ownership to recorded rationale and evidence export in the same case record. Use risk bands so weak adverse-media hits get analyst validation while high-confidence sanctions matches can trigger temporary restrictions. If a vendor cannot show that end-to-end flow, keep it in evaluation.

Continuous KYC monitoring is now a control decision, not a vendor checkbox#

Treat this as a control design decision first and a software purchase second. One-time onboarding checks can miss risk changes after approval. When you compare continuous KYC monitoring platforms, the real test is whether they help you decide when to re-verify, who reviews, and what evidence gets retained.

| Checkpoint | Supported practice | Warning sign |

|---|---|---|

| State over snapshot | Re-verification triggers when the risk profile changes and updates the same customer record | Another alert in another queue |

| Risk tiering | Low and medium-risk customers stay in automated checks with light-touch sampling; high-risk customers move to human review | Analysts are deciding severity from scratch on each case |

| One profile | One customer profile updates as new events happen | Analysts work across multiple tools and manually collect screenshots and PDFs |

| Evidence quality | Alert context, reviewer identity, decision rationale, and supporting documents stay together in one place | Rationale and evidence are not preserved together |

| Governance | Profile changes become review actions with preserved evidence | The same control gaps remain, just in a new interface |

In practice, you should be able to trace a single risk change from trigger to owner to documented action without rebuilding the case by hand from several systems.

That shift matters for compliance and risk owners because KYC sits inside AML/CFT obligations. If your process still treats KYC as a one-time pass-or-fail gate, you have a snapshot, not an ongoing control.

- State over snapshot

Continuous monitoring tracks identity state over time, not just whether a customer passed once. A practical test is whether the platform triggers re-verification when the risk profile changes and updates the same customer record instead of opening a brand-new case each time. That is the control distinction. A policy layer decides when the same user needs another check. If the only output is another alert in another queue, you have more data, not better control.

- Risk tiering over blanket review

Not every alert should get the same treatment. A risk-tiered model keeps low and medium-risk customers in highly automated checks with light-touch sampling, while high-risk customers move to human review. Without clear escalation ownership, handling can become inconsistent and hard to scale. Good design makes the first routing decision explicit so analysts are not deciding severity from scratch on each case.

- One profile over many tools

A strong operating checkpoint is one customer profile that updates as new events happen. The common failure mode is analysts working across multiple tools and manually collecting screenshots and PDFs. That does not scale, and it weakens audit explainability because the decision trail is fragmented. Even when you use more than one provider, the operating target should still be one internal record of truth.

- Evidence quality over alert volume

More alerts do not mean stronger control if decisions are hard to explain. Keep alert context, reviewer identity, decision rationale, and supporting documents together in one place. When those records are centralized, explaining decisions to auditors and regulators is much easier. Decisions are harder to defend when review rationale and evidence are not preserved together.

- Governance over feature lists

The legal backdrop is clear: KYC sits inside AML/CFT requirements, with European AML directives dating back to 1991, including 5AMLD (July 2018) and 6AMLD (December 2020). The real differentiator is governance discipline. If a vendor cannot show how profile changes become review actions with preserved evidence, treat that as a control risk.

Use this shortlist rule: do not buy for detection alone. Buy only if the product supports re-verification triggers, risk-tiered handling, and a defensible evidence trail. If those three are weak, the same control gaps remain, just in a new interface.

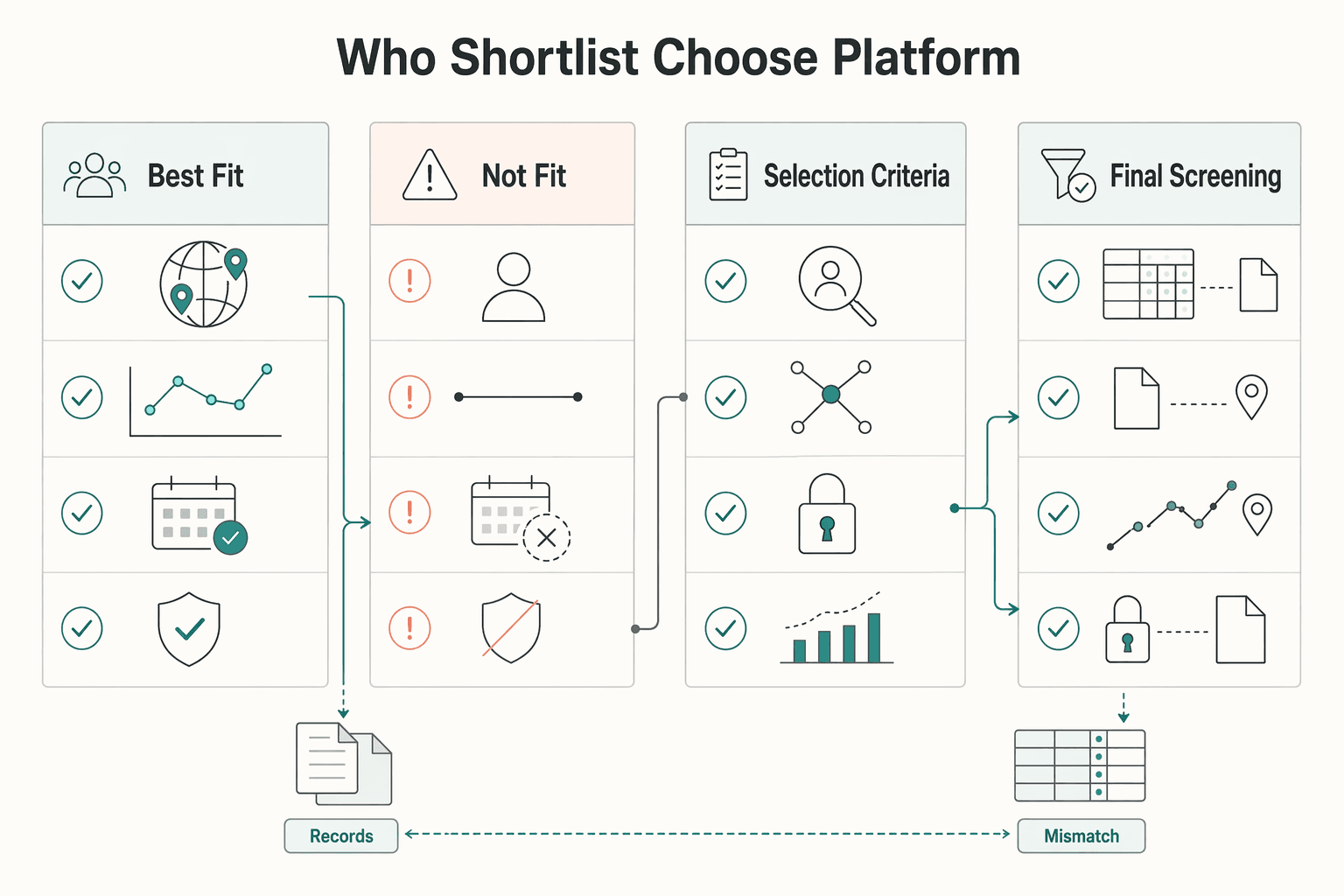

Who this shortlist is for and how to choose a platform#

This shortlist is for payout teams that need ongoing monitoring after onboarding, not one-time KYC only. If you run contractor, seller, or creator payouts across markets and screen for sanctions or watchlists, choose a vendor as an AML operations control, not just a procurement line item.

The right fit starts with your operating reality. Teams with real post-onboarding exposure, such as cross-border counterparties, risk profiles that change over time, and regular re-check decisions, get the most value here. Teams that only need onboarding checks usually do not.

- Best fit

The best fit is a team with real post-onboarding exposure: cross-border counterparties, risk profiles that change over time, and regular re-check decisions. Prioritize platforms that connect ongoing monitoring triggers, such as sanctions/watchlist hits and risk-scoring changes, to a clear evidence trail. Before demos, define your regulatory footprint, risk assessment, counterparty types, and operating model. That prep work helps you test whether the platform fits your process instead of adapting your process to the demo.

- Not a fit

If your needs stop at onboarding KYC and you do not run ongoing monitoring, this category is usually more than you need right now. A common failure mode is adding broad automation without enough oversight, then getting weak outcomes. In that case, optimize onboarding screening first and revisit ongoing monitoring later. A thinner control that your team can actually run is usually better than a broader one that sits half-owned.

- Selection criteria that matter

Start with trigger coverage, then validate operations. Check sanctions/watchlist screening, risk scoring, and ongoing monitoring tied to your risk rules. Then confirm how alerts become review cases, how reviewer rationale is recorded, and how the evidence file is retained for audit review. Also test integration readiness. Poor compatibility with your current systems, or no pre-integration testing, usually creates production friction. In the proof session, ask the vendor to show the same case in sequence: trigger received, review opened, rationale recorded, and evidence export produced.

- Final screening rule

De-prioritize vendors that cannot show live how an ongoing monitoring alert becomes a review action with retained evidence. Strong detection claims are not enough if data quality, rule changes, and oversight are weak. If you split providers by region to reduce single-vendor outage risk, account for the higher compliance cost and added operational complexity.

What continuous monitoring means in day-to-day operations#

In practice, continuous KYC monitoring means a risk change after onboarding triggers action now, not at the next scheduled refresh, for example every 12 or 36 months. pKYC updates the customer risk profile as new signals appear, so your team is not waiting on a calendar while exposure changes.

That operating difference matters because a periodic program shows a documented refresh cycle, while a continuous program shows how you respond to live risk change.

- Event-driven refresh, not calendar-driven review

KYC does not stop at onboarding. A customer that was clear at approval can appear on a sanctions list six months later, so qualifying changes should trigger immediate review instead of waiting for the next cycle. Periodic programs show a documented refresh cycle. Continuous programs show response to live risk change. The practical question for your team is simple: what happens in the first hour after the signal appears?

- Minimum trigger coverage should match real AML risk

Sanctions checks alone may miss relevant risk changes. Baseline trigger coverage should include adverse media, ownership or profile changes, and unusual transaction patterns tied to CDD. Teams can map different trigger types to different review paths so triage stays focused as new signals arrive.

- Detection only matters if response is fast and documented

You need to see how quickly an alert becomes a review action, whether risk status is updated, and whether reviewer rationale is recorded. In practice, sustained manual re-checking is time-intensive, so operating quality depends on clear review steps and evidence capture, not just alert generation. If your team cannot tell which alerts are pending first review versus waiting on added evidence, the process can slow down even when detection is working.

- Periodic and manual models have practical limits

Fixed-cycle reviews can leave long windows where risk changes go unnoticed. Manual ongoing review can also consume significant time. If your model relies on either approach, define where event-driven review takes priority so risk updates are handled when they happen, not only when the calendar turns.

Comparison table for continuous KYC monitoring platforms#

In this category, the core test is whether the platform supports your ongoing monitoring requirements and regulatory obligations in practice, not just how many features appear on a checklist.

One caution before the table. At least one vendor-roundup source in this research set says its comparisons are based on public online research, that it did not test each tool directly, and that it was last updated on April 1st 2026. So this comparison marks unknowns explicitly instead of guessing.

| Vendor | Best for | Strengths seen in current evidence | Known limitations | Alert-to-case handling | SAR support posture | API / webhook maturity | Evidence export readiness | Implementation unknowns | Operator risk if alerts spike |

|---|---|---|---|---|---|---|---|---|---|

| Moody's | Validation-only shortlist | No vendor-specific strength is verified in the available excerpts | Vendor-specific strengths, limitations, pricing, false-positive controls, and queue design are not established in the available excerpts | Unknown in available excerpts | Unknown in available excerpts | Unknown in available excerpts | Unknown in available excerpts | Benchmark method, integration timeline, analyst workload impact, and export detail need vendor proof | Unknown in available excerpts |

| Quantexa | Validation-only shortlist | No vendor-specific operational differentiator is verified in the available excerpts | No verified detail here on case management, exports, pricing, or implementation effort | Unknown in available excerpts | Unknown in available excerpts | Unknown in available excerpts | Unknown in available excerpts | Integration path, webhook behavior, benchmark methodology, and review queue design need validation | Unknown in available excerpts |

| DataWalk | Validation-only shortlist | No confirmed advantage is established in the available excerpts | Sparse excerpts mean vendor claims should not be treated as production proof | Unknown in available excerpts | Unknown in available excerpts | Unknown in available excerpts | Unknown in available excerpts | Pricing, timeline, evidence pack format, and case-SLA performance are not established | Unknown in available excerpts |

| iDenfy | Validation-only shortlist | No vendor-specific strength is verified in the available excerpts | Pricing, false-positive rates, benchmark methodology, integration timeline, and spike behavior are explicitly unknown in the available excerpts | Unknown in available excerpts | Unknown in available excerpts | Unknown in available excerpts | Unknown in available excerpts | API behavior, webhook reliability, export fields, and operational load during sanctions events need proof | Unknown in available excerpts |

How to read a table with this many unknowns#

Unknown means unverified, not weak. If a vendor cannot show live workflow evidence for ongoing monitoring during procurement, treat those capabilities as unproven.

The useful way to read this table is to separate market presence from operating proof. A practical shortlist should match your technical capacity, customer goals, and regulatory obligations. Without that discipline, selection decisions get volatile. In 2024, weak KYC procedures drew over £176 million in FCA fines, so unverified operating depth is a material risk. Treat each unknown column as a proof item to clear, not as a minor note to revisit after signing.

The decision columns that matter most#

Focus first on the columns where operators usually feel pain. In practice, that usually means:

- Alert-to-case handling: Ask for a live example of an alert moving into investigator review and a recorded outcome.

- SAR support posture: Check whether case records preserve enough detail for review decisions.

- API or webhook maturity: Ask how alerts and status changes are delivered into your systems.

- Evidence export readiness: Request a sample export with the original alert, user actions, review outcome, and related CDD or Enhanced Due Diligence context.

If any of these four areas remains unproven, treat that as an implementation risk and require proof before selection.

Verification checkpoints before you advance any vendor#

Use a documented proof session, not slides, as your gate. Require one end-to-end example from trigger to reviewer action to evidence export, and retain the output in your selection record.

For legal references, verify against official sources. If someone cites the Federal Register entry published on 09/04/2024, use the linked official govinfo PDF for document 2024-19260 rather than relying on site text alone.

Do not rank these vendors from thin excerpts. Rank them by what they can prove in ongoing monitoring, CDD support, sanctions-screening response, and audit-ready evidence. If the proof session produces only screenshots, ask for the underlying record flow before moving forward.

Moody's pKYC for enterprise-grade risk refresh#

Moody's can be a practical shortlist candidate when your main problem is stale KYC and CDD records across a counterparty base. The strongest supported position in the available material is pKYC as an automated, integrated, near-real-time refresh model. The missing piece is day-2 operating proof under live alert volume.

Best fit#

Best fit is a team moving from fixed review cycles to event-driven refresh. Moody's defines pKYC as maintaining current customer and counterparty records through automated checks in near real time, rather than only rerunning due diligence on set intervals. The cited intervals are 5 years for low risk, 3 years for medium, and 1 year for high.

The same evidence points to trigger events such as sanctions-list updates, election outcomes, and address changes. That is more useful than a generic continuous monitoring claim because it ties change events to follow-up due diligence decisions.

What stands out in the available evidence#

The clearest supported advantage is faster awareness of risk change. Moody's says this model helps institutions identify and respond more promptly when changes may require further due diligence, including escalation paths like enhanced due diligence or off-boarding.

A second useful signal is the trigger-based design. The report describes an ongoing KYC process based on specific triggers and real-time data inputs. The same materials also note that pKYC is not yet mainstream and that legacy KYC is often manual, time-consuming, and technically challenging. Treat this as a testable proposition, not proven operating performance. The concept is strong, but the procurement question is still whether the operational handoff works in your environment.

What you need to verify before advancing it#

The excerpts do not establish implementation effort, false-positive controls, pricing, or analyst queue design. Require a proof session focused on operating behavior:

- Show one sanctions-list change and one profile-change trigger moving to reviewer action, with timestamps, ownership, and final rationale.

- Show retained evidence for AML review, including the original alert, linked CDD material, and whether enhanced due diligence or off-boarding was considered.

- Show how duplicate or repeated alerts are handled.

Two potential failure modes should be tested. One is delayed detection under long periodic cycles, which Moody's says can expose institutions to bad actors, compliance failings, and reputational harm. Another is alert growth without matching decision throughput if trigger coverage expands faster than routing and noise controls. A workable demo should therefore show not only detection, but also how the queue stays usable when the same customer produces more than one signal over time.

Practical recommendation#

Use Moody's when the decision is mainly about faster KYC refresh and clearer linkage between risk changes and CDD follow-up actions. Do not select on narrative alone if you also need validated low-noise triage, clear queue ownership, and export-ready records for AML review. The pKYC report scope, 60 interviews, 58 firms, and 9 countries, is useful context. It is not a substitute for a live demonstration using your own counterparties, escalation rules, and review capacity.

For a step-by-step walkthrough, see KYC KYB CIP Explained for Cross-Border Freelancers and Small Teams.

Quantexa for broad shortlist evaluation and connected data context#

Quantexa can be a strong early shortlist candidate when your main question is investigation context, not proven perpetual-monitoring outcomes. Based on the available evidence, treat it as a serious evaluation option, not a confirmed winner for continuous monitoring performance.

Best fit#

Consider Quantexa in first-pass vendor triage for KYC and related KYB/AML investigation needs when your team is dealing with fragmented records, unclear ownership structures, and investigation work that requires too much manual stitching across systems.

A Celent case study dated March 15, 2022 describes ABN AMRO deploying Quantexa's Contextual Decision Intelligence platform to improve intelligence and efficiency in complex KYC investigations. The supported value is the investigation data foundation: entity resolution, relationship mapping, and decision context for analysts.

What stands out#

A clearly supported differentiator is entity resolution plus network analytics for corporate structures. In the cited use case, this includes resolving corporate entities, mapping hierarchies and connections, and identifying disclosed and undisclosed beneficial owners, including UBOs.

The same case study also describes investigator-facing outputs: interactive network visualizations with highlighted risks, and access to combined internal and external data for review and decision-making. That is stronger than a generic product claim because it shows how context is presented during case work. For teams that already know fragmented data is the bottleneck, this is the part worth testing first.

Where the evidence stops#

Do not treat the Celent market view as proof of superior perpetual KYC monitoring results. The broader Celent market view is useful for directional procurement context because it covers 17 profiled vendors, with 12 fully participating in the ABC Vendor View analysis. It is still not full operational validation for your environment.

These materials do not establish pricing, false-positive rates, benchmarked detection accuracy, API maturity, or SAR tooling depth. They also do not show whether investigation context translates cleanly into repeatable alert handling at scale.

What to verify before you advance it#

Use the ABN AMRO timeline as a checkpoint template, not a delivery promise: October 2019 PoC initiation, December 2019 technical PoC delivery, Q1 2020 PoC completion, December 2020 soft go-live, and June 2021 UI go-live.

In a proof session on your own data, require evidence of:

- Entity resolution behavior on messy KYB records, including what is auto-resolved versus left ambiguous for analyst confirmation.

- Retained investigation evidence, including network view, source records, analyst rationale, and final CDD decision output.

A key evaluation risk is assuming that richer graph context automatically improves outcomes. Celent notes incumbent AML systems often suffer high false positives under traditional rules. Validate independently whether Quantexa reduces that noise in production. If the demo is visually strong but weak on disposition workflow, keep it in evaluation rather than treating it as an answer to continuous monitoring on its own. For a related angle, see Best Merch Platforms for Creators Who Want Control and Compliance.

DataWalk for dynamic risk assessment use cases#

Treat DataWalk as an RFP-phase test candidate, not a final shortlist pick, when your priority is dynamic risk assessment in Perpetual KYC (pKYC). The provided excerpts are too limited to verify specific capabilities for continuous monitoring or changing risk posture. They also do not provide enough verified depth on Customer Due Diligence (CDD), Suspicious Activity Report (SAR) handling, or the integration model to support a stronger claim.

Best fit#

Keep it in scope when your core buying question is whether KYC refreshes actually change operational decisions. In AML workflows, that means a refreshed risk view should drive concrete case handling, not just update a score.

Why this angle is worth testing#

A January 2025 study provides context for the evaluation criteria, but it does not validate any specific vendor. It used a structured 5-point Likert survey with N = 168 valid responses. Of respondents, 42.3% were identified as transaction monitoring analysts. It reported the strongest correlations for perceived Compliance Risk Reduction with MDE (r = 0.72, p < .001) and AQWII (r = 0.69, p < .001).

The takeaway is practical. In this context, dynamic risk updates are most useful when they improve alert quality and analyst workload. The same study frames traditional rule-based AML/KYC monitoring as prone to high alert noise and inconsistent investigations, which is the failure mode to test for in pKYC demos. That is why an RFP should push past dashboards and ask how refreshed risk actually changes queue behavior and reviewer steps.

What to verify before shortlisting#

In the RFP, ask for one end-to-end example on your data or a close proxy, and verify:

- how a pKYC signal changes the active risk view

- what CDD evidence is attached, requested, or retained

- how weak or duplicate alerts are separated from higher-confidence cases

- what record is preserved if a case later moves into SAR consideration

If the demo stops at scoring or dashboards, de-prioritize it. For continuous review, the key checkpoint is whether pKYC outputs connect to documented analyst action, auditable rationale, and final disposition. If that path is missing, the platform may still be useful for analysis, but not yet for a control you need to defend.

iDenfy for automated transition from periodic to continuous checks#

iDenfy is a practical shortlist candidate when your goal is to replace fixed review cycles with trigger-based monitoring. In the provided material, pKYC is framed as continuous CDD: risk profiles update in real time, and new risk signals trigger immediate review.

Best fit#

This is most relevant for teams still relying on checks every 12 or 36 months. If a customer appears on a new sanctions list or shows transaction patterns that do not match the profile, a scheduled refresh window can be too slow. The cited periodic-model risk is clear: material changes can go undetected for years.

Why this is worth shortlisting#

What makes the iDenfy positioning useful is the trigger logic, not generic real-time language. The examples given are:

- a customer appearing on a new sanctions list

- unusual transaction patterns that do not match the customer profile

That aligns with a trigger-based pKYC model where checks start from rules or events rather than calendar intervals. Adjacent source context also highlights the first 30 to 90 days after onboarding as an early period where unusual activity can surface, rather than waiting for later refresh cycles. The material also states that FATF Recommendation 10 encourages ongoing monitoring, while local implementation still depends on jurisdiction. For teams moving off periodic review, this makes the operating model legible: detect, review, document, then decide whether the account can continue as normal.

What to validate before committing#

Treat this as a strong operating model, not proven delivery performance. The excerpts do not establish iDenfy metrics, detection rates, or implementation constraints. Before selection, verify:

- how a sanctions trigger creates an immediate review action, not only a score change

- what CDD evidence is attached and retained before and after the trigger

- how unusual behavior is defined against a customer profile, including newer accounts

- what audit trail is preserved from alert through analyst decision

For teams comparing platforms in this category, use this decision rule: shortlist iDenfy for the shift from periodic to event-driven checks. Commit only if trigger events map cleanly to documented CDD action and audit-ready records. If the model is sound but the evidence chain is thin, you may still recreate too much manually. Related: Continuous KYB for Platforms: How to Refresh Business Verification Without Re-Onboarding Everyone.

Build, buy, or hybrid decision rules for platform teams#

Pick your model based on the gap you need to close first: trigger coverage, control ownership, or audit traceability. This choice is less about feature count and more about who owns decision logic, downstream actions, and defensible records.

| Option | Brief description | Choose it when | Key differentiator | Main watch-out |

|---|---|---|---|---|

| Vendor-led pKYC | A vendor runs ongoing checks and much of the alerting flow using services such as sanctions screening, adverse media, identity verification, and document checks. | Your main gap is trigger coverage, especially for sanctions or adverse-media events. | A fast route to broader monitoring without building screening logic. | Detection alone is not enough if reviewer actions and final decisions are hard to prove later. |

| Internal orchestration over vendor feeds | You ingest external feeds, but your team owns a central policy layer for decisions. | You already have core KYC tools and need to unify fragmented rules. | Centralized control over rules, routing, overrides, and state, separated from execution tooling. | Engineering, maintenance, and scaling burden can grow quickly. |

| Hybrid KYC plus in-house risk routing | A vendor performs checks, while your team controls policy gates, escalation paths, and downstream actions. | You need tighter control over post-alert decisions without fully building in-house. | Balances control and efficiency. | Requires clear ownership and handoffs across teams. |

Buy first when trigger coverage is the gap#

If sanctions and adverse-media triggers are inconsistent or missing, a buy-first path can help stabilize signal intake before adding custom logic. Custom orchestration has limited value when core triggers are still immature. You need dependable inputs before internal routing can add much value.

Use hybrid when payment-side control is the priority#

When post-alert actions must stay aligned with internal policy gates, hybrid is often worth evaluating. Keep decision logic centralized and separate from execution tools so policy is not hard-coded into whichever vendor system came first. That separation can also make later vendor changes less disruptive.

If traceability is the gap, prioritize architecture#

If your issue is reconstructing decisions, prioritize an architecture where alerts, reviewer actions, overrides, and final outcomes are linked and exportable as one chain. Before committing, validate that one case record can show the full path from alert to final action. If you need several teams to explain one case, the architecture is probably still too fragmented.

One explicit no-go rule#

Do not scale broad automation until case ownership and escalation paths are clearly defined across teams. Without that, automation can speed up ambiguity instead of reducing risk. The result can be faster alert generation with slower real decisions.

Before final vendor selection, run one pilot where pKYC alerts map to reviewer ownership and export fields; use this implementation checklist in the Gruv docs.

Escalation decisions after a high-risk alert#

After a high-risk alert, map severity bands to default actions, and allow overrides when the reviewer records rationale and supporting evidence. This keeps decisions consistent without removing judgment.

| Band | Default action | Use when | Case record |

|---|---|---|---|

| Band 1 | Analyst review before customer-facing action | Weak or unverified signals, especially adverse media with uncertain entity matching | Confirm legal name, jurisdiction, and recent profile or KYB changes first |

| Band 2 | Enhanced CDD and additional evidence requests when justified | The signal is credible enough that standard monitoring is no longer sufficient | Expand the evidence set with targeted requests tied to the open risk question |

| Band 3 | Temporary restriction and investigation escalation | Higher-confidence signals where delay increases exposure, including strong sanctions-match scenarios | Log the restriction as part of the case record |

| Band 4 | Offboarding path and SAR consideration | Risk is confirmed, unresolved after enhanced review, or repeatedly returns with stronger evidence | Capture reviewer rationale, supporting evidence, and whether SAR review was considered |

This is where the earlier platform choice becomes real. Periodic-only reviews are not enough here. If reviews happen every 1 to 3 years, material risk can change between cycles, so escalation should be event-driven and tied to current signals.

- Band 1: analyst review before customer-facing action

Use this for weak or unverified signals, especially adverse media with uncertain entity matching. Confirm identity and profile basics first, for example legal name, jurisdiction, and recent profile or KYB changes. If you see duplicate or stale-profile alerts, consider routing them to tuning review rather than silently suppressing them. That helps separate a weak rule from a real case.

- Band 2: enhanced CDD (and additional evidence requests when justified)

Use this when the signal is credible enough that standard monitoring is no longer sufficient, but prohibition or exit is not yet established. Expand the evidence set with targeted requests, especially when ownership changes, business-status changes, sanctions exposure, or adverse media worsen the onboarding risk view. High-risk cases can require enhanced due diligence before approval. The point is not to request more documents by default, but to request the documents that answer the open risk question.

- Band 3: temporary restriction and investigation escalation

Use this for higher-confidence signals where delay increases exposure, including strong sanctions-match scenarios. One internal policy option is to apply temporary restrictions while investigation proceeds, with weaker unverified signals staying in analyst review first. Treat this as a policy choice, not a universal legal requirement. If you use this band, log the restriction as part of the case record.

- Band 4: offboarding path and SAR consideration

Use this when risk is confirmed, unresolved after enhanced review, or repeatedly returns with stronger evidence. Keep restrictions in place as policy requires, move toward offboarding where supported, and escalate for SAR review where appropriate. For defensibility, case records should capture the reviewer's rationale, supporting evidence, and whether SAR review was considered.

When alert volume rises and investigator capacity is constrained, escalation quality depends on control design as much as analyst effort. Repeated false positives are a calibration and scenario-logic issue to fix directly, especially in environments where false positives run around 90 to 95%. If every severe alert needs manual reinterpretation, the banding model is not doing enough work.

Monthly reporting and audit evidence package#

Your monthly evidence package should let an auditor follow the decision path without rebuilding it from raw records: what was reviewed, what decision was made, who approved it, and when.

| Package part | What to keep | Notable detail |

|---|---|---|

| Monthly control snapshot | One monthly summary showing what changed, what is still open, and what still needs judgment | Traceability to case IDs and reviewer IDs so samples can be tested quickly |

| Controlled case file set | Maximum-account-value support, threshold-check records, exchange-rate documentation when applicable, and approval records with timestamp and owner sign-off | Keep an index showing where each artifact lives and which decision it supported |

| Threshold and value support | Threshold and value support in the file for FBAR-relevant cases | Filing is required when a single account or aggregate maximum account values exceed $10,000 during the calendar year; round reported amounts up to the next whole U.S. dollar |

| Deadline exception tracking | Timing exceptions tracked explicitly | Certain individuals with signature authority and no financial interest may be extended to April 15, 2027; other individuals with an FBAR filing obligation remain due April 15, 2026 |

The simplest way to keep this useful is to build it around traceability, not volume. The package should show how an account review became a filing decision and how deadline exceptions were tracked.

- Monthly control snapshot

Keep one monthly summary that shows what changed, what is still open, and what still needs judgment for FBAR-related reviews. What matters most is traceability to case IDs and reviewer IDs so samples can be tested quickly. If the snapshot raises a question, the reviewer should be able to jump directly into the underlying case file.

- Controlled case file set

For each reviewed case, keep a clear evidence bundle: maximum-account-value support, threshold-check records, exchange-rate documentation when applicable, and approval records with timestamp and owner sign-off. You do not need every document in the monthly binder, but you do need an index showing where each artifact lives and which decision it supported. A short index is often what makes the whole package usable.

- Threshold and value support

For FBAR-relevant cases, keep threshold and value support in the file: filing is required when a single account or aggregate maximum account values exceed $10,000 during the calendar year, and not required when that threshold is not met. Keep the maximum-value method documented, including periodic statements when used, round reported amounts up to the next whole U.S. dollar (for example $15,265.25 -> $15,266), and record the source when a non-Treasury exchange rate is used.

- Deadline exception tracking

Track timing exceptions explicitly: certain individuals with signature authority and no financial interest may be extended to April 15, 2027, while other individuals with an FBAR filing obligation remain due April 15, 2026.

IRS IRM 4.26.9's "Records Commonly Found" and "Evidence" sections are a practical design check. Your package should make records easy to trace, test, and defend.

Choosing the platform is only half the decision#

Choose the operating model first, then the tool. If you pick software before you define trigger coverage, escalation ownership, and evidence standards, you may simply move the failure point.

That is the thread running through the whole shortlist: vendor capability matters, but control design determines whether you can operate it, defend it, and scale it.

- Define trigger coverage before vendor comparison

Start with the events that can change your KYC or AML judgment, then test vendor coverage against that list. Keep a written trigger register with the event, source, owner, and required action so evaluation maps to real decisions, not feature claims. This can also make later rule changes easier because the control logic already exists outside the sales narrative.

- Lock escalation ownership before launch

Perpetual KYC (pKYC) works best with explicit handoffs. Manual transitions are a known breakdown point, so write escalation paths for higher-risk cases and specify what additional evidence each path requires. Anchor those paths to a formal Customer Acceptance Policy (CAP), publish it internally, and review it regularly. If ownership is vague at launch, it usually stays vague when alert pressure rises.

- Set evidence standards early

Define what each case must retain so decisions are defensible and reproducible under pressure. During evaluation, run a detection-to-closure walkthrough and check whether your process can preserve alert context, decision rationale, and supporting records without manual reconstruction. The goal is not just retention, but repeatability.

- Prioritize unified context over fragmented tooling

Fragmented systems are a known operational and regulatory risk because alerts can stay isolated and cross-signal risk is harder to detect. Favor setups that give investigators a Single Customer View across identity, transaction, behavior, and related signals. The more your team relies on manual stitching, the harder it is to prove consistent treatment.

KYC operations are already costly and slow in cited benchmarks. One cited benchmark puts them at 95 days and $2,598 per corporate case. Enforcement exposure also remains material, with $1.23 billion in fines in the first half of 2025 in one cited source. If you operate in or into the EU, one cited source says pKYC is set to become a legal requirement by 2027. Use that as a planning marker: define your triggers, owners, and evidence standards first, then choose the platform.

If you want a control-design review for your exact markets and payout flow, request a practical walkthrough with Gruv's compliance and payments team.

Frequently Asked Questions

What is the difference between periodic KYC and continuous KYC monitoring?

Periodic KYC refreshes customer information on a fixed cycle, often every one, three, or five years. Continuous monitoring checks for new information between those cycles. The practical difference is that periodic-only programs can accumulate outdated customer data. Continuous models are designed to reduce that lag.

Which events should trigger immediate review?

There is no universal trigger list that fits every program or jurisdiction. Use a risk-based rule: if new information could change your customer due diligence judgment, review it now instead of waiting for the next cycle. Keep the trigger policy explicit so teams can apply it consistently, and document ownership for each trigger.

How often should risk scores update in a continuous model?

Do not rely only on annual or multi-year refresh points if you run continuous monitoring. Update risk assessments when meaningful new information appears, with a review rhythm your team can sustain. The cadence should match your risk profile, jurisdiction mix, and operational capacity.

What should happen right after a high-risk alert?

Start with a risk-based review: if the alert could change your customer due diligence judgment, assess it now instead of waiting for the next cycle. Then follow your documented policy for controls and due diligence. Keep a clear case record and system logs so the review is auditable.

Do all platforms support the same coverage and controls?

No. Coverage and controls vary by provider. Some market broad country coverage, API or webhook integrations, and audit-ready logs, but those claims are provider-specific. Validate actual trigger inputs, case workflow, and export detail against your own program needs before choosing a platform. Broad coverage claims do not automatically mean strong evidence handling.

What records should we keep for audits?

Keep records that let an auditor reconstruct the case without rebuilding it from raw systems. In practice, that means preserving due diligence and ongoing monitoring records, plus system logs where available. The key test is whether an independent reviewer can follow the sequence without manual reconstruction.

When should we involve specialist counsel?

Involve specialist counsel when your team cannot confidently resolve jurisdiction-specific requirements through normal compliance procedures. KYC obligations vary by country, so define an escalation path with your compliance officer and use it early for cross-border issues.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- bsaaml.ffiec.gov/docs/manual/BSA_AML_Man_2014_v2_CDDBO.pdftrusted

- bsaefiling.fincen.gov/docs/XMLUserGuide_FinCENFBAR.pdftrusted

- cppa.ca.gov/regulations/pdf/ccpa_updates_all_written_com...trusted

- federalregister.gov/documents/2024/09/04/2024-19260/financial-cr...trusted

- federalreserve.gov/files/cbdc-public-comments-3-20220215.pdftrusted

- fincen.gov/reporting-maximum-account-valuetrusted

- fincen.gov/report-foreign-bank-and-financial-accountstrusted

- irs.gov/irm/part4/irm_04-026-009trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Choosing a Defensible SAR Filing Model for Payment Platforms

For platforms moving contractor, seller, or creator funds, when SAR filing applies, the goal is an operating approach your team can run consistently, not a system that tries to catch everything. You need alerts that get reviewed, cases backed by evidence, and filings you can defend. FFIEC describes suspicious activity reporting as the cornerstone of BSA reporting and emphasizes that SAR content quality is critical to the effectiveness of that system.

Continuous KYB for Platforms Without Full Re-Onboarding

Continuous KYB should reduce surprises without turning onboarding into a recurring document chase. For platforms, this is a shift in operating model, not a bigger onboarding form. KYB starts as a legitimacy check, but it now needs to continue through the full merchant lifecycle so you can catch material changes early without dragging every business back through full re-onboarding.

When High-Risk Payout Accounts Need Source of Funds Checks Beyond KYC

A one-time KYC check may not be enough for higher-risk payout accounts. Risk can change after onboarding as transaction behavior shifts and customer risk profiles change.