Quick Answer

Choose the simplest SAR filing model your platform can run consistently and defend under review. The best setup is the one that produces complete, sufficient, and timely SARs for covered entities, preserves clear case evidence and non-filing decisions, and tracks acknowledgements and submission status in BSA E-Filing. In practice, case management depth, narrative quality, evidence retrievability, and explicit ownership matter more than adding more detection features.

Financial crime compliance for platforms without overbuilding#

- Start with a narrow promise

For platforms moving contractor, seller, or creator funds, when SAR filing applies, the goal is an operating approach your team can run consistently, not a system that tries to catch everything. You need alerts that get reviewed, cases backed by evidence, and filings you can defend. FFIEC describes suspicious activity reporting as the cornerstone of BSA reporting and emphasizes that SAR content quality is critical to the effectiveness of that system.

Start with a short list of suspicious activity scenarios, a decision log, and a reviewer checkpoint that confirms chronology, customer profile, and transaction context before escalation. In practice, teams can overbuild detection rules and underbuild case facts. That creates large alert queues with weak narratives.

- Keep the scope tight

This article focuses on AML/CFT, FinCEN SAR filing, and suspicious activity monitoring controls a platform team can actually operate. FATF frames AML/CFT as preventing abuse of the financial system and organizes its standards into 40 Recommendations, so implementation should fit your institution type and operating context.

In U.S. operations with a filing obligation, FinCEN's BSA E-Filing System is the filing channel and supports both SAR and CTR forms. If your structure includes a U.S. filing obligation, confirm early which entity files, who owns acceptance tracking in BSA E-Filing, and where rejected or corrected submissions are documented.

- Be explicit about the limits

This is operational guidance, not legal advice, and requirements vary by jurisdiction, product, and applicable BSA rule set. U.S. rules point firms to the suspicious transaction reporting requirements for their own financial institution category, so you should not assume one rule set applies across all entities or markets.

For banks, SAR timing is 30 calendar days from initial detection, with a 60 calendar day maximum when no suspect is identified initially. Use those numbers as a reference point, not a universal deadline for every platform entity in your structure.

- Use handoffs instead of centralizing everything

You reduce surprises when Compliance, Payments Ops, Legal, and Finance use clear handoffs instead of informal escalation. Compliance needs case evidence and a filing path. Finance needs defined control steps when suspicious activity decisions affect reserves, returns, write-offs, or reporting.

For filing mechanics and decision standards, see our SAR filing explainer. For Finance coordination, pair this with the ICFR controls article. Also document non-filing decisions, not just filed cases. The 2025 interagency FAQs clarify SAR/AML requirements, including non-filing documentation, and state they do not change existing BSA/AML requirements.

How to choose a SAR filing setup that fits your platform#

Choose the setup that improves SAR quality and evidence discipline first, not the one with the most detection features. The right fit is the one your team can run consistently: for covered entities, it should produce complete, sufficient, and timely SARs, track filing status in BSA E-Filing, and show a clear decision trail.

This section is for Compliance, Legal, Risk, Finance, and Payments Ops teams running AML/CFT controls in a platform that moves funds. It is not a consumer banking primer, and it does not assume every platform entity has a U.S. SAR obligation. Start by confirming entity classification and jurisdiction.

- BSA E-Filing readiness

A workable setup has to support electronic submission, acknowledgements, and submission status tracking in BSA E-Filing. For covered institutions, filing has been electronic-only since April 1, 2013, so PDF-driven or inbox-driven workflows are a poor fit.

The key differentiator is ownership. Assign a designated user with primary responsibility and keep a visible record of filing outcomes and follow-up actions.

- Case management depth

If quality is slipping, better case management usually matters more than more alert logic. Examiners focus on whether your process can identify, evaluate, and report suspicious activity effectively, so your system should preserve chronology, reviewer actions, escalation notes, and the basis for filing or not filing.

Use deadline-aware fields. For banks, the reference timing is 30 calendar days from initial detection, with up to 60 calendar days if no suspect is initially identified. Under other rule sets, keep a timestamped initial-detection field, not just an alert-created date. Structured non-filing documentation should also be part of the process.

- Narrative and evidence quality

Narrative quality is a core control because the narrative is the only free-text summary of suspicious activity. Your setup should reliably pull in readily available account-opening and due-diligence information, transaction context, investigator notes, and customer profile details.

What separates a workable process from a weak one is evidence retrievability. Supporting documentation must be producible to FinCEN or law enforcement on request, and required records are retained for five years. Before submission, confirm that each material narrative statement can be traced to case, profile, or transaction records.

- Platform reality fit

Pick for your operating reality, not a generic tool category. Cross-border volume, KYC and KYB maturity, and reviewer capacity often determine what is sustainable. If due-diligence coverage is weak, adding more rules can increase case volume without improving support quality.

If review capacity is already falling behind, prioritize case management and audit trail controls before you expand detection scenarios. For MSB-like profiles, keep the AML program risk-commensurate to location, size, and service volume, with baseline controls for customer identification, filing, and record retention.

Related: How to Pay Contractors in South Africa: RTGS EFT and SARB Compliance for Platforms.

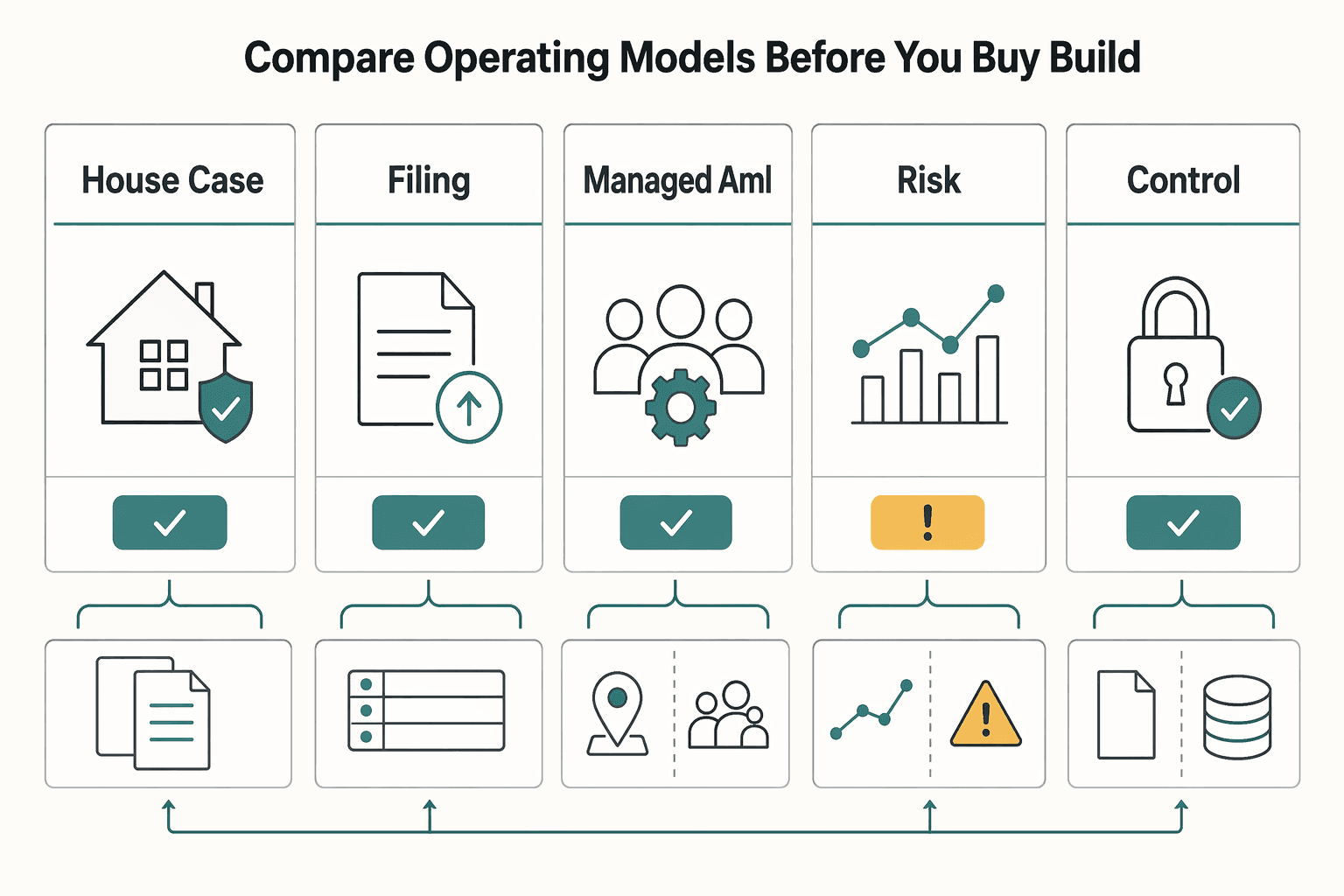

Compare the operating models before you buy or build#

Choose the simplest model you can defend: consistent SAR narrative quality, clear escalation ownership, and reliable acceptance tracking in the BSA E-Filing System.

Before you shortlist options, pressure-test the adjacent controls that usually break first, then use these verification checkpoints by model:

Section 314(b)readiness for voluntary sharing means you can manage the one-year notice lifecycle and verify the other financial institution before sharing.CTRreadiness means the model can support actual CTR filing artifacts for currency transactions over$10,000when that obligation applies to your entity.

| Model | Best for | Core stack shape | FinCEN SAR and CTR support | Section 314(b) information sharing readiness | Narrative quality control | Attachment hygiene | Escalation ownership | Acceptance tracking in the BSA E-Filing System | Pros | Cons | Typical failure mode |

|---|---|---|---|---|---|---|---|---|---|---|---|

| In-house case management + direct submission | Mature Compliance team with stable volumes | Internal alerts, internal case management, direct BSA E-Filing submission | Strong if you maintain form mapping, batch or individual filing, and acknowledgements | Usually manual, but workable with tracked notice renewal and counterparty verification | High control if QA is built into reviewer steps | Strong if evidence is retrievable and retained for five years | Clear internal owner in Compliance or Legal | Strong only if acknowledgements are written back into the case record | Full control, tighter fit to your risk taxonomy, strong audit trail | Training debt, maintenance burden, filing-spec change risk | Investigations are strong, but filing QA and acknowledgement capture are weak |

| In-house detection + managed filing support | Teams with solid triage but inconsistent filing execution | Internal alerts and cases, partner handles packaging, QA, and submission | Often good for filing operations; verify both SAR and CTR handling | Commonly outside partner scope, so usually manual internally | Partner can improve consistency, but handoff can flatten case facts | Depends on disciplined evidence transfer and version control | Split between your investigators and partner filing team | Useful only if partner status is written back into your case management | Faster quality lift without replacing detection | Handoff friction, duplicated records, continuity gaps | Filed case exists with partner, but internal record cannot show why it was filed |

| Managed AML platform with integrated SAR and CTR tooling | Lean or fast-growing teams needing one system | Vendor alerts, vendor case management, integrated filing connector | Convenient if true form support exists, not just export templates | Varies by vendor; verify notice tracking and counterparty verification fields | Standardized templates help, but can be rigid | Centralized storage helps retention and retrieval | Easier routing, but still needs named internal approvers | Often strongest when acknowledgement status stays on the same case | Unified case file, less manual stitching, easier reporting | Lower customization, vendor dependency, evidence-model mismatch risk | Vendor case file is clean, but linkage to KYC or KYB source evidence is weak |

| Hybrid by risk tier or market | Multi-entity or mixed-risk platforms | Internal path for high-risk cases, managed or vendor path for lower-risk segments | Workable only if both paths support filing and status records | Needs central governance or breaks quickly | Strong where hard cases stay internal, uneven elsewhere | Duplicate evidence stores are a common risk | Blurs unless one escalation matrix governs all paths | Often fragmented across tools | Better cost-to-control balance, focus on highest-risk work | Governance complexity, duplicate process, cross-track confusion | Case changes risk tier and loses chronology between tools |

| Minimum viable controls | Early-stage platforms with low volumes | KYC or KYB gates, narrow alerting, simple case queue, direct or light managed filing | Acceptable if it can produce forms, log status, and retain records | Usually manual only, if used at all | Manual checklist can work at low volume | Manual evidence pack is acceptable if retrievable and retained | One named owner and one backup | Simple status log works if it records receipt and follow-up | Low cost, clear responsibilities, fast to stand up | Key-person risk, thin capacity, low resilience | Non-filing decisions end up in chat or email instead of case management |

- In-house direct submission

Make sign-off explicit: investigator drafts, Compliance approves, Legal joins when needed. Keep chronology, reviewer actions, submitted-form snapshot, and acknowledgement record in case management. Document non-filing with a structured reason code and brief memo. Define an emergency path for cases that require immediate law-enforcement notification in addition to timely SAR filing.

- In-house detection + managed filing support

Use one shared case ID across internal and partner systems. Internal teams sign off on facts and suspicion, and the partner owns filing QA and submission mechanics. Keep non-filing decisions in your system so the internal audit trail stays complete.

- Managed AML platform with integrated filing

Keep internal approval even if the vendor workflow is complete. Require each material narrative statement to map to retrievable evidence. If evidence sits outside the platform, verify that links and access will still hold over retention periods.

- Hybrid by risk tier or market

Standardize sign-off rules before you split flows. Keep one searchable register for audit trail visibility across tools. Use the same non-filing taxonomy on both paths for defensible consistency.

- Minimum viable controls

Assign one accountable Compliance owner and one backup for escalation, filing-status review, and retention. Require a mandatory non-filing note and a visible FinCEN status log.

If you have to trade features for control discipline, choose control discipline. Detection coverage is never complete, so practical failures often come from weak narrative quality, incomplete supporting records, and inconsistent escalation or acceptance tracking.

Option 1 in-house case management with direct FinCEN submission#

This model makes sense when you want full SAR ownership and can sustain strong internal investigation, review, and filing QA. It is often a fit for teams with disciplined case management, stable alert volumes, and a clear internal owner for FinCEN submission.

The advantage is control. Investigators and reviewers keep the narrative close to the underlying customer and transaction evidence, and your internal risk taxonomy stays intact. If you design for it, alert history, investigator notes, reviewer decisions, the submitted-form snapshot, and the filing acknowledgement can stay in one case record.

Why this model fits some teams#

In-house direct filing is strongest when reviewers are calibrated on suspicious activity analysis, not just form completion. Narrative quality is a core control point, and the narrative is the critical free-text section, so narrative QA needs to be explicit and consistent.

A defensible operating pattern is simple: investigators build the case, Compliance approves, Legal joins when needed, and filing status is written back to the same case. Lower-volume teams can use discrete single-form BSA E-Filing transmission. Higher-volume teams can use batch filing, but that adds XML packaging, change control, and maintenance overhead.

Where the burden shows up#

The burden is operating discipline, not direct filing fees. BSA E-Filing has no direct fee, but indirect costs can show up in reviewer training, QA effort, and engineering support for submission workflows.

Two failure patterns to watch for:

- Narrative quality drifts across reviewers because QA does not consistently check who, what, when, where, and why against retrievable case evidence.

- Teams treat threshold amounts as the whole analysis. Activity at or near the $10,000 CTR threshold alone is not enough to require a SAR.

Checks that make this model defensible#

- Match the filing method to volume: discrete for lower volume, batch only if you can support testing and change control. New or revised batch submission procedures must be tested in the BSA E-Filing User Test system before production use.

- Keep a complete case record with SAR decision documentation and filing artifacts (such as the submitted-form snapshot and acknowledgement), and retain SAR data and supporting documentation for five years.

- Apply a consistent no-file documentation policy. The 2025 interagency FAQ guidance says there is no explicit BSA requirement to document no-file decisions, while FFIEC examination material emphasizes documenting SAR decision-making, including no-file outcomes.

Choose this option when you want ownership more than convenience and can maintain reviewer calibration, evidence discipline, and filing QA in one internal process.

Related reading: Gig Worker Financial Wellness: How Platforms Can Offer Savings and Insurance as Benefits.

Option 2 in-house detection with managed SAR filing support#

Use this model when your detection and triage are solid, but your filing execution is not. You keep internal ownership of suspicious activity decisions, and a managed partner supports packaging, QA, and submission through the BSA E-Filing System.

The advantage is focus. Your team stays close to alert review, customer context, and risk judgment. The partner handles repetitive filing work that often creates backlog: form completion, narrative QA, submission operations, and acknowledgment tracking.

Best fit#

This model fits teams that trust their detection logic more than their filing discipline. One common pattern is reliable suspicious activity identification paired with recurring narrative rework, weak form QA, or poor internal visibility into filing acknowledgments.

It is most useful when the gap is operational, not analytical. If investigators can explain why activity is suspicious but struggle to produce a concise, supportable filing package, managed support can strengthen the last mile without replacing internal review.

What you gain#

The main gain is stronger execution where examiners tend to focus: content quality, rationale, and evidence continuity. Narrative QA should confirm who, what, when, where, and why, with support in the case record for material statements.

You also get clearer status handling. BSA E-Filing issues acknowledgments for filings, and batch submissions include Process ID and Status metadata. If a partner runs submission operations, require those records in your internal audit trail, not just in the partner portal.

The real risks#

Managed filing support does not transfer accountability. Your institution remains responsible for BSA and AML outcomes. You need oversight of how the provider operates, how quality is reviewed, and how deadline risk is escalated before the 30 calendar day filing window is missed, or the 60 calendar day outer limit when no suspect is identified at initial detection.

One failure mode is broken continuity between your case record and the partner filing record:

- Evidence is transferred by email or spreadsheet without a durable link to the source case.

- Partner narrative edits are not approved or logged by Compliance.

- BSA E-Filing acknowledgments remain only in partner systems.

A second risk is optimizing for form submission instead of investigative support. SAR workflows also require collecting and maintaining supporting documentation, plus retaining SAR copies and supporting documents for five years.

What to insist on before you sign#

Set ownership in writing. Your team should own suspicious activity determinations, Legal escalation when needed, and final filing approval. The partner should own packaging, QA against filing requirements, and submission operations, with explicit controls, review procedures, and performance monitoring.

Use a strict handoff gate: no transfer unless the evidence pack and decision record are complete. That includes chronology, customer or business context, transaction details, investigator notes, filing or no-file rationale, and logged reviewer approval. If activity is near a CTR threshold, do not treat that fact alone as sufficient SAR logic. Pick this option when you need near-term operational support in filing execution without giving up internal judgment on what is suspicious.

This pairs well with our guide on Why RegTech Creates a Compliance Moat for Gig Platforms.

Option 3 managed AML platform with integrated SAR and CTR tooling#

This option can be a strong fit when your team is lean and the main gap is infrastructure, not risk judgment. If you need case management and filing operations in one place, a managed platform can help stabilize AML and CFT operations without stitching together separate tools.

Best fit#

This can work well when speed and consistency matter more than deep customization. A common case is a fast-growing payout platform with rising alert volume. It may need Suspicious Activity Report and Currency Transaction Report workflows in one system instead of across tickets, spreadsheets, and inboxes.

The practical upside is consolidation. Some vendors market one platform for KYC, monitoring, case management, and SAR filing, and the BSA E-Filing System supports both individual and batch filing. That can reduce handoffs and make filing status easier to track.

What to verify before you buy#

Do not accept "FinCEN integration" as a vague claim. Ask the vendor to show, in product, how it handles FinCEN Suspicious Activity Report (FinCEN Report 111) and FinCEN Currency Transaction Report (FinCEN Report 112). Also confirm whether FinCEN status messages are written back into your audit trail. Use these diligence checks:

- Confirm whether submission is direct, batch-based, or XML export only. FinCEN provides SAR and CTR XML user guides, and the distinction changes your operational workload.

- Check status handling. BSA E-Filing guidance says machine-readable submission messages are generally returned within 5 hours, so acknowledgments should be tied to the case record.

- Review closed and filed cases. Examiner focus is not only filing volume. SAR content quality is also critical, and your record should show why a case was filed or closed.

The tradeoffs#

You give up flexibility. A common risk is a mismatch between the vendor's evidence model and your internal KYC or KYB records, which can force manual rework and weaken narratives.

Roadmap dependency is another cost. If you need specialized review steps, market-specific escalation, or custom data lineage, you may be waiting on vendor changes while SAR timelines continue. The reference timing is 30 calendar days from initial detection, with an additional 30 calendar days allowed to identify a suspect and a 60-calendar-day maximum delay. For CTRs, make sure the system supports transactions in currency of more than $10,000 and the 15-day filing timeline where applicable.

Option 4 hybrid model by risk tier and market#

A hybrid can work when both lanes produce one unified record with clear case ownership, filing decisions, and acceptance or rejection tracking. It can balance cost and control for multi-market operations, but governance can break down when lanes keep different evidence standards.

Best fit#

This option can be practical when risk and data quality are uneven across products, entities, or markets. In that setup, you can keep higher-judgment cases in stricter internal case management and use managed filing support for lower-risk segments, with explicit escalation triggers between lanes.

That split is an operating decision, not a FinCEN mandate. If routing logic is vague, cases can churn between lanes and governance effort can rise.

Minimum controls to standardize before launch#

| Control point | Standardize across both lanes | Why it matters |

|---|---|---|

| Case record | One case ID, shared decision reasons, shared evidence checklist | Keeps decisions explainable across lanes |

| Acceptance tracking | Store structured acknowledgements in the case record | FinCEN filing materials include concrete status artifacts such as StatusCode values for tracking acceptance state |

| Data validation | Validate required elements before submission | FinCEN XML guidance shows missing required elements can cause rejection, including specific failures like Error Code A26 (state/country mismatch) |

Failure modes to watch first#

Hybrid designs can break at the handoff. For example, one lane may document decisions in detail while the other stores only filing artifacts, or acceptance status may never make it back into the main record. Cross-market field mapping can also fail when formats differ by region or entity type.

Rule-change drift is a quieter risk. FinCEN Notice FIN-2024-NTC7 (November 20, 2024) is a useful governance example: individuals whose reporting signature-authority due date had already been extended were further extended to April 15, 2027, while the due date for other individuals with an FBAR filing obligation remained April 15, 2026. Different report type, same operating lesson: if one lane updates and the other does not, control consistency breaks.

Option 5 minimum viable controls for early-stage platforms#

For an early-stage team, the right move is a thin but auditable baseline, not broad detection coverage. That baseline should stay simple: gated onboarding, one case queue, a documented SAR decision log, and filing-status traceability.

1. KYC and KYB gating#

Start upstream with written AML procedures for customer identification, reporting, and record retention, not just background vendor checks. If you onboard legal-entity customers, include beneficial ownership procedures where applicable, so SAR decisions have clearer ownership context.

Before a case reaches investigation, you should be able to pull customer profile, business details, and verification results in one place. If alerts are opened on half-built profiles, investigators may have to infer ownership, business purpose, or transaction context.

2. One queue with owned case states#

Keep one case-management queue with clear ownership and states. Every alert or referral should have an owner, timestamps, disposition, and notes or attachments, and escalations should show who took the case and why.

Feature depth matters less than traceability. If reviewers have to reconstruct facts across email, chat, and spreadsheets, the baseline is not credible.

3. A decision log tied to the FinCEN SAR record#

If you are in scope for U.S. SAR obligations, document why a SAR was filed or not filed. The SAR framework is completion of the report plus supporting documentation, and FinCEN SAR electronic filing requirements include retaining SAR data and supporting records for five years.

Keep decisions specific. For MSBs, SAR criteria include transactions involving at least $2,000, but activity near the $10,000 CTR threshold is not automatically SAR-reportable without suspicion indicators.

4. Submission status and urgent escalation#

For FinCEN SAR filing (FinCEN Report 111), use BSA E-Filing and write submission status back into the case record, including Track Status or Track Organization Status results. This gives you auditable filing-status traceability.

Treat status as evidence of submission, not evidence of narrative quality. Also make urgent escalation explicit: cases suggesting ongoing money laundering or other urgent violations should be routed for immediate attention in parallel with normal filing steps.

Escalation rules that prevent bad SAR decisions#

In U.S. bank contexts, an escalation rule that can reduce bad outcomes is simple: keep decision ownership separate from form preparation, and do not move a case to filing while core facts are still unstable.

1. Split decision ownership from form preparation#

Assign one owner per stage from alert creation through submission, and keep each handoff visible in the case record. Ops can collect facts. Compliance should coordinate day-to-day BSA/AML compliance, with a designated decision-maker owning the filing decision. Legal can review when disclosure risk or legal exposure is plausible. Engineering should support data integrity and controls rather than filing judgment.

Keep the separation explicit. Staff preparing SAR or CTR forms generally should not also decide whether to file. For each case, you should be able to show who opened it, who investigated it, who approved the filing or non-filing decision, and who submitted it.

2. Freeze weak cases for QA before narrative finalization#

If evidence is incomplete, contradictory, or missing chronology, pause the case for structured QA before the narrative is finalized. The QA check should confirm the core narrative elements: who, what, when, where, and why.

Run this rule alongside filing timelines, not instead of them. The baseline filing window is 30 calendar days from initial detection of facts that may justify filing. There is an additional 30 calendar days only when no suspect is identified, and never more than 60 calendar days total. A practical escalation rule is simple: if facts conflict, reconcile them first. If legal exposure is plausible, consider routing to Legal before narrative lock.

3. Treat Section 314(b) as a bounded tool, not a general sharing channel#

Use Section 314(b) only for its stated purpose: voluntary information sharing among financial institutions to identify and, where appropriate, report possible money laundering or terrorist activity. Do not turn it into a general channel for broad case sharing.

Apply the procedural boundaries every time. Before sharing, confirm required 314(b) notice status and take reasonable steps to verify the counterparty's status. Notice effectiveness runs for one year. For cross-entity or cross-market investigations, involve specialist counsel when recipient qualification, permitted purpose, or SAR confidentiality risk is unclear. Near-threshold activity, including activity at or near the $10,000 CTR threshold, is not by itself enough to require a SAR filing.

Evidence pack and audit trail checklist before filing#

Do not move a Suspicious Activity Report to filing until the evidence pack is complete, internally consistent, and traceable in your case record.

Pre-filing control risks include narratives that overstate the file, approvals that are hard to trace, or submission records disconnected from investigator work. Use this pre-filing checklist to catch those issues before they become control problems.

- Build chronology before narrative

Start with a dated sequence of facts, then draft. Tie together the alert, investigation steps, key transactions, relevant customer or business profile context, and the point when activity was escalated as suspicious. Keep the narrative anchored to who, what, when, where, and why. Prioritize order over volume. A clear timeline is stronger than a large but unstructured evidence folder.

- Treat supporting documentation as part of the SAR record

Keep the records that support the filing decision and narrative under one case identifier so they are retrievable. For banks under the cited SAR rules, supporting documentation is collected and maintained as part of the SAR record, and must be available to appropriate law enforcement on request. In bank rule context, retain a copy of the SAR and supporting documentation for five years from the filing date.

- Run narrative QA against filing instructions and case facts

Before submission, do a line-by-line consistency check between case notes and the SAR form using FinCEN SAR electronic filing requirements and FFIEC narrative guidance as your QA frame. Remove any statement that cannot be tied to a source record or investigator note. Incomplete, incorrect, or disorganized narratives are a known control risk. For filing mechanics background, see What is a Suspicious Activity Report (SAR) and When to File One.

- Apply a hard pre-submit gate and post-submit status logging

Block filing on missing required fields, weak or conflicting chronology, unsupported claims, or broken links between approval actions and submission records. If Legal review is required by your internal escalation rule, confirm that review is logged before filing. After submission, log acknowledgement and submission status in the same audit trail. Do not assume submission equals acceptance. Batch submissions can be rejected if they fail electronic filing requirements, and SDTM workflows return status files that should be retained with the case.

Do not let QA drift into deadline failure. In bank rule context, filing is generally due within 30 calendar days from initial detection, with up to an additional 30 calendar days when no suspect is identified, and never more than 60 calendar days total. If activity appears urgent or ongoing, escalate to law enforcement immediately in addition to timely SAR filing.

For a step-by-step walkthrough, see Digital Nomad Financial Review Checklist for Compliance, Cash Flow, and Resilience. For an implementation reference for policy gates, status tracking, and audit-ready event flows, review the Gruv docs.

Rollout sequence for the first implementation cycle#

Roll out in this order: map the real alert-to-SAR flow, assign ownership and escalation, configure case records and QA, and only then launch a narrow first scope.

- Map the current alert-to-reporting path end to end

Start with the process you actually run, not the one on a slide. Trace a case from alert creation through investigation, escalation, narrative drafting, submission, and post-submission status so handoffs, evidence location, and breakpoints are visible. Use this map to identify where the 30 calendar day filing clock starts from initial detection and where records fragment across teams.

- Assign named owners and explicit escalation routes

Set clear responsibility for identifying, researching, and reporting suspicious activity at each stage. Define where unusual activity is referred when a case needs escalation, and keep those communication lines explicit. Keep the timing guardrail explicit: if no suspect is identified, filing can extend, but never beyond 60 calendar days from initial detection.

- Configure case management and filing QA controls

Structure the case record so both outcomes are documented: file and do not file. Include the rationale for non-filing decisions in the same record rather than scattered notes. Run QA so filings are complete, sufficient, and timely, and retain submission-status evidence. For batch filing workflows, keep the confirmation record with Process ID and status information with the case file.

- Add safeguards, then go live with a narrower scenario set

Before launch, put safeguards in place to reduce avoidable control errors and keep case handling consistent. Start with suspicious activity scenarios where reviewers can apply standards consistently, then expand in phases as case outcomes remain reliable.

The practical next step for your team#

Start with the smallest control set you can defend under review: clear ownership, consistent evidence, verified submission status, and explicit escalation boundaries. If ownership is unclear or evidence quality is weak, fix that before expanding tooling.

- Lock one owner for each decision point

Map ownership from alert creation through SAR submission and status tracking in BSA E-Filing. Assign named accountability for triage, investigation, file-or-no-file decisions, Legal escalation, and deadline control. For teams subject to the cited bank rule, this is also a timing control: file within 30 calendar days from initial detection, with delay to identify a suspect capped at 60 calendar days total. Keep narrative drafting and deadline oversight as separate checks.

- Standardize the minimum evidence pack before expanding detection

Set one evidence standard for every case so decisions are reproducible. For example, preserve chronology, transaction context, investigator analysis, and the documented rationale for filing or not filing. Because content quality is central to process effectiveness, weak chronology or unsupported assertions should trigger structured QA before filing.

- Treat submission status as a control, not admin

Do not treat "submitted" in an internal queue as completion. Capture acknowledgement and submission-status evidence from BSA E-Filing and retain it with the case file. If a vendor or managed provider files on your behalf, require acknowledgement and status records to flow back into your system.

- Keep adjacent controls narrow and explicit

Keep CTR and Section 314(b) handling adjacent to, not merged into, your SAR workflow. Near-threshold CTR activity by itself is not sufficient to require a SAR, and 314(b) sharing is voluntary with notice, counterparty verification, and one-year renewal requirements. Escalate immediately when facts suggest urgent ongoing violations and assess whether immediate telephone notice to law enforcement is required in addition to timely SAR filing.

In the next 30 days, prioritize one ownership map, one evidence standard, one submission-status check, and one escalation rule your team actually follows.

Once you pick a target operating model, talk with Gruv to pressure-test market coverage and control design for your rollout.

Frequently Asked Questions

What is the minimum viable SAR workflow a payment platform needs to be credible?

The minimum credible workflow is to detect and open a case, investigate, document a file or no-file decision, file when required, and retain supporting documentation. Credibility comes from a clear record of who decided, when, and on what documented basis. For covered banks, the filing reference point is 30 calendar days from initial detection, with no more than 60 calendar days when no suspect is initially identified.

Which SAR tasks should be automated and which should always stay manual?

Automate repeatable mechanics such as intake, deadline tracking, data population, and batch submission where feasible. Keep suspicious-activity judgment, escalation decisions, and final filing determinations with trained reviewers.

What evidence should be attached or documented before filing a FinCEN SAR?

Before filing, document the factual basis for the filing or no-file decision in a case record you can produce later. Preserve chronology, customer or business context, transaction details, investigator notes, and supporting records tied to the same case. For covered banks, keep the SAR and supporting documentation for five years and provide supporting records on request.

How should teams track SAR submission status and acceptance in practice?

Track submission status as an operational control, not proof that the SAR is substantively sufficient. Use BSA E-Filing Track Status and retain acknowledgements or status records with the case file, especially for batch submissions. If your system shows "submitted" but status evidence is missing, treat that as a control gap.

When should a suspicious activity case be escalated to Legal instead of only Compliance?

Escalate to Legal when issues go beyond routine investigative judgment, including urgent situations where immediate law-enforcement notification may be required for covered banks. Escalate when legal interpretation is needed, such as institution-type rule boundaries or information-sharing constraints. Compliance should still own investigation quality and filing discipline.

How should platforms handle SAR-related controls when operating across multiple markets?

Apply U.S. controls only to the specific U.S. rule that matches your institution type, and handle other markets under their own legal regimes. Do not assume one entity type's rule, thresholds, or timelines automatically apply across all entities or markets.

Where do CTR and Section 314(b) fit without expanding scope too far?

Treat CTR and Section 314(b) as adjacent controls, not substitutes for SAR workflows. CTR covers currency transactions over $10,000 and is filed within 15 days when that obligation applies. Section 314(b) is voluntary AML/CFT information sharing with notice, counterparty verification, and one-year notice effectiveness requirements. Activity merely near the CTR threshold is not, by itself, enough to require a SAR.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- bsaaml.ffiec.gov/manual/AssessingComplianceWithBSARegulatoryR...trusted

- bsaaml.ffiec.gov/manual/Appendices/13trusted

- bsaefiling.fincen.govtrusted

- bsaefiling.fincen.gov/docs/FinCENSARElectronicFilingRequirements.pdftrusted

- ecfr.gov/current/title-31/subtitle-B/chapter-X/part-1...trusted

- ecfr.gov/current/title-31/subtitle-B/chapter-X/part-1...trusted

- federalreserve.gov/supervisionreg/srletters/SR2504a1.pdftrusted

- fincen.gov/system/files/2025-12/FBAR-FBAR-Filing-Requir...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.

How to Respond to a Subpoena for Business Records

Move fast, but do not produce records on instinct. If you need to **respond to a subpoena for business records**, your immediate job is to control deadlines, preserve records, and make any later production defensible.

A US Expat's Guide to Investing in UCITS ETFs to Avoid PFIC Issues

The real problem is a two-system conflict. U.S. tax treatment can punish the wrong fund choice, while local product-access constraints can block the funds you want to buy in the first place. For **us expat ucits etfs**, the practical question is not "Which product is best?" It is "What can I access, report, and keep doing every year without guessing?" Use this four-part filter before any trade: